Key Insights

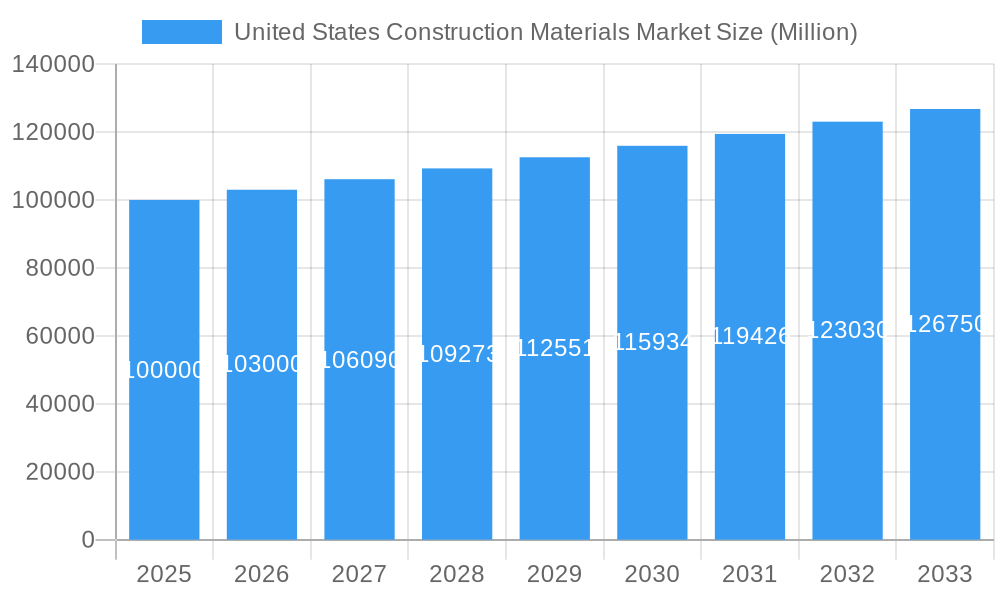

The United States Construction Materials Market is experiencing robust expansion, driven by significant infrastructure investments and a dynamic building sector. Valued at an estimated $139.42 billion in 2024, the market is projected to grow at a CAGR of 4% from 2025 to 2033. This growth is primarily fueled by the continued rollout of projects under the Bipartisan Infrastructure Law, stimulating demand for aggregates, cement, and steel across various public works. Residential construction, though facing interest rate fluctuations, remains a foundational driver, especially in high-growth regions. Furthermore, the booming development of commercial facilities, particularly data centers and large-scale logistics hubs, along with ongoing renovation and repair activities, consistently contributes to the demand for diverse material types, including specialized concretes and advanced building envelopes. The market is also benefiting from a renewed focus on domestic manufacturing and supply chain resilience, ensuring a steady procurement of essential construction inputs.

United States Construction Materials Market Market Size (In Billion)

Pivotal trends shaping the market include a pronounced shift towards sustainable and green building materials, such as low-carbon concrete, recycled aggregates, and energy-efficient insulation. Technological integration, encompassing Building Information Modeling (BIM), modular construction, and advanced material science, is enhancing efficiency and accelerating project timelines. However, the industry navigates persistent challenges, including volatile raw material prices, skilled labor shortages, and rising interest rates which can impact project financing. Leading players like Holcim, Vulcan Materials Company, Martin Marietta Materials, and CRH PLC are strategically investing in R&D for innovative material solutions, sustainable production methods, and optimizing their supply chains to maintain competitive advantages and meet evolving market demands for high-quality, durable, and environmentally responsible construction products.

United States Construction Materials Market Company Market Share

Report Description: Dive deep into the dynamic landscape of the United States Construction Materials Market with our comprehensive SEO-optimized report. This essential analysis provides critical insights into market concentration, innovation drivers, regulatory frameworks, and the competitive strategies of key players like Cemex Sab De CV, CRH PLC, Heidelberg Materials, Holcim, Martin Marietta Materials, and Vulcan Materials Company. From the bedrock of Aggregates (Sand, Gravel, Crushed Stone) to the sophisticated realm of low-carbon Cement & Concrete, Metals, and sustainable Wood and Glass solutions, our study meticulously dissects market segments by Material Type, Construction Type (New Construction, Renovation & Repair), Application (Structural, Envelope, Interior, Site & Landscaping), and End User (Residential, Commercial, Industrial Construction). With a Study Period spanning 2019–2033, a Base and Estimated Year of 2025, a Forecast Period from 2025–2033, and a Historical Period of 2019–2024, this report offers an unparalleled strategic roadmap for industry stakeholders, investors, and policymakers navigating the evolving US construction materials sector. Understand the forces shaping market growth, identify emerging opportunities, and gain a competitive edge in a market projected to reach over $450 billion by 2033.

United States Construction Materials Market Market Concentration & Innovation

The United States Construction Materials Market exhibits a moderate to high degree of concentration, with the top five players, including industry giants like Vulcan Materials Company, Martin Marietta Materials, Holcim, CRH PLC, and Cemex Sab De CV, collectively holding an estimated 40% of the market share, particularly within key segments such as aggregates and cement. This concentration is frequently bolstered by strategic mergers and acquisitions (M&A), a trend evident in recent activities that saw M&A deal values exceeding $15 billion in 2024. Innovation drivers are transforming the sector, pushing companies to invest heavily in sustainable construction materials, digital technologies, and advanced manufacturing processes. Regulatory frameworks, increasingly focused on environmental compliance and sustainability, are shaping product development and market entry barriers. For instance, stringent emissions standards for cement production necessitate investment in carbon capture technologies or the development of low-carbon alternatives.

Product substitutes, such as mass timber for steel or recycled concrete aggregates, are gaining traction, driven by environmental mandates and cost-efficiency considerations, posing a nuanced challenge to traditional materials. End-user trends reflect a growing demand for durable, energy-efficient, and aesthetically pleasing materials, particularly in high-growth areas like residential and commercial construction. This demand fosters innovation in composite materials and smart construction solutions. M&A activities, exemplified by Heidelberg Materials' acquisition of Carver Sand & Gravel and Cemex's joint venture in July 2024, are not merely about expanding geographic reach or capacity; they are strategic maneuvers to consolidate market power, secure raw material reserves, and integrate supply chains, ultimately enhancing operational efficiencies and competitive positioning. The drive for innovation is also spurred by the need to develop materials that can withstand extreme weather events and contribute to resilient infrastructure, aligning with national infrastructure modernization goals.

- Key Market Players' Influence: Top players command significant market share, especially in aggregates and cement.

- M&A Impact: Strategic consolidations drive market concentration and operational synergy.

- Innovation Focus: Sustainable materials, digital construction, and process optimization.

- Regulatory Influence: Environmental and safety regulations mandate cleaner production and material standards.

- Product Substitution: Growth of recycled and alternative materials challenging conventional options.

- End-User Demand: Preference for sustainable, energy-efficient, and durable building solutions.

United States Construction Materials Market Industry Trends & Insights

The United States Construction Materials Market is experiencing robust growth, primarily propelled by substantial investments in infrastructure development, a resilient housing market, and an increasing emphasis on sustainable building practices. The market is currently valued at over $300 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 5.2% from 2025 to 2033, reaching over $450 billion by the end of the forecast period. This growth trajectory is underpinned by significant government initiatives, such as the Infrastructure Investment and Jobs Act (IIJA), which allocates hundreds of billions of dollars towards roads, bridges, public transit, and utilities, creating consistent demand for Aggregates, Cement & Concrete, and Metals. Urbanization trends and population growth further fuel demand for Residential Construction and Commercial Construction, leading to increased consumption of core materials.

Technological disruptions are reshaping the industry, with advancements in areas such as 3D concrete printing, AI-driven material design, and advanced sensor technologies improving material quality, efficiency, and safety. The advent of low-carbon cement production techniques and the development of self-healing concrete are prime examples of innovation addressing both performance and environmental concerns. Consumer preferences are shifting dramatically towards green building materials and energy-efficient construction. There is a burgeoning demand for materials with reduced carbon footprints, enhanced durability, and improved thermal performance, driving the adoption of sustainable Wood, recycled Glass, and bio-based insulation products. This shift is not just limited to New Construction but also significantly impacts the Renovation & Repair segment, where homeowners and businesses increasingly seek eco-friendly upgrades.

Competitive dynamics within the market are intense, characterized by a mix of multinational corporations and strong regional players vying for market share. Companies are increasingly differentiating themselves through product innovation, strategic partnerships, and efficient supply chain management. The ability to offer integrated solutions, from raw material sourcing to specialized finished products, is becoming a key competitive advantage. Market penetration for advanced materials, while growing, still presents considerable opportunities as conventional materials dominate large segments. The rise of modular and prefabricated construction techniques also impacts material demand, favoring standardized and high-quality components. Furthermore, the volatility of raw material prices and energy costs continues to influence operational strategies, pushing companies to explore localized sourcing and renewable energy options to maintain profitability and reduce environmental impact. The demand for resilient materials capable of withstanding extreme weather events is another crucial trend, particularly in regions prone to natural disasters, influencing the specifications for Structural and Envelope applications.

Dominant Markets & Segments in United States Construction Materials Market

Within the multifaceted United States Construction Materials Market, Aggregates unequivocally stands out as the dominant material type, representing an estimated 45% of the total market volume and value in 2025. This segment, encompassing Sand, Gravel, Crushed Stone, and increasingly M-Sand and Granite, forms the foundational backbone of nearly all construction activities across the nation. Aggregates are indispensable for Structural applications, forming the bulk of concrete and asphalt, crucial for roads, bridges, buildings, and other critical infrastructure. The sheer volume required for large-scale New Construction projects, combined with ongoing Renovation & Repair of existing infrastructure, ensures its sustained dominance.

- Economic Policies: Government-backed infrastructure initiatives, such as the Infrastructure Investment and Jobs Act, directly drive massive demand for aggregates for public works projects.

- Urbanization & Housing: Continued urban development and the demand for new residential and commercial buildings necessitate vast quantities of sand, gravel, and crushed stone for foundations, concrete slabs, and landscaping.

- Construction Versatility: Aggregates are integral to multiple construction components – concrete, asphalt, road bases, railway ballast, and drainage systems – making them universally required across all Application and End User segments.

- Logistics & Availability: Despite regional variations, aggregates are widely available throughout the US, minimizing long-distance transportation costs and supporting widespread use.

By Construction Type, New Construction accounts for the largest share of material consumption. This segment is characterized by large-scale projects requiring substantial quantities of foundational materials like Cement & Concrete, Aggregates, and Metals for structural frameworks. The ongoing demand for new housing units, expansion of commercial real estate, and government-funded infrastructure projects consistently drive this segment. While Renovation & Repair is a significant and growing market, particularly for specialized materials, energy-efficient solutions, and aesthetic upgrades, the initial material outlay for new builds remains higher.

From an End User perspective, both Residential Construction and Commercial Construction are major drivers. Residential construction, fueled by population growth and housing demand, consumes vast amounts of wood, bricks, concrete, and aggregates for new homes and renovations. Commercial construction, encompassing offices, retail spaces, and industrial facilities, is a key consumer of steel, glass, and advanced concrete systems, with projects often having higher material specifications and structural complexity. Industrial construction, while important, represents a smaller but specialized segment, typically requiring high-strength concrete, specialized metals, and durable flooring materials.

United States Construction Materials Market Product Developments

Product developments in the United States Construction Materials Market are heavily influenced by the twin imperatives of sustainability and efficiency. Innovations include the widespread adoption of low-carbon cement and concrete mixes that significantly reduce CO2 emissions, aligning with global climate goals. The development of self-healing concrete, incorporating bacteria or microcapsules, promises extended structural longevity and reduced maintenance costs for Structural applications. Furthermore, advancements in recycled aggregates and bio-based materials like cross-laminated timber (CLT) offer sustainable alternatives to traditional resources, enhancing the environmental profile of New Construction projects. Smart glass technologies that adapt to sunlight and advanced insulation materials contribute to energy efficiency, particularly in Envelope applications for Commercial Construction. These technological trends are driving a market fit that prioritizes reduced environmental impact, improved material performance, and lifecycle cost savings.

Report Scope & Segmentation Analysis

The United States Construction Materials Market report provides a granular analysis across its key segments. By Material Type, the market is segmented into Aggregates (Sand, Gravel, Crushed Stone, M-Sand, Granite, Others), Cement & Concrete, Metals, Bricks and Blocks, Wood, Glass, and Others. Aggregates are projected to maintain the largest market share due to their fundamental role in infrastructure and building. The Construction Type segment distinguishes between New Construction and Renovation & Repair, with New Construction typically leading in material consumption, though Renovation & Repair is showing robust growth driven by aging infrastructure and energy efficiency upgrades. The Application segment covers Structural, Envelope, Interior, Site & Landscaping, and Others, detailing how materials are utilized across different building components. Finally, the End User segment dissects demand from Residential Construction, Commercial Construction, and Industrial Construction, each with unique material requirements and growth projections influenced by economic and demographic trends, providing a comprehensive view of market dynamics and competitive landscapes within each sub-segment.

Key Drivers of United States Construction Materials Market Growth

The United States Construction Materials Market is propelled by several robust growth drivers. Economically, the Infrastructure Investment and Jobs Act (IIJA) has earmarked over $200 billion for vital infrastructure projects, ensuring sustained demand for Aggregates, Cement & Concrete, and Metals for road, bridge, and utility construction. Simultaneously, a resilient housing market and growth in Commercial Construction driven by urbanization continue to fuel the need for a diverse range of building materials. Technologically, advancements in sustainable manufacturing processes, such as low-carbon concrete and recycled materials, are becoming key drivers, incentivized by environmental regulations and consumer preferences for green buildings. Regulatory factors, including stricter building codes for energy efficiency and resilience, are pushing the adoption of advanced insulation, smart glass, and durable Structural materials, fostering innovation across the industry.

Challenges in the United States Construction Materials Market Sector

The United States Construction Materials Market faces several significant challenges. Regulatory hurdles, particularly environmental compliance and complex permitting processes for quarrying and manufacturing, can lead to project delays and increased operational costs. Supply chain issues, exacerbated by global geopolitical tensions and logistics bottlenecks, frequently result in material shortages and price volatility for essential commodities like Metals and certain specialized Aggregates, impacting project timelines and budgets. Labor shortages in both manufacturing and skilled construction trades present a persistent barrier, driving up labor costs and slowing down construction activity. Furthermore, intense competitive pressures among major players and regional suppliers often lead to compressed profit margins, demanding continuous innovation and operational efficiencies to remain viable in the market.

Emerging Opportunities in United States Construction Materials Market

Significant emerging opportunities are transforming the United States Construction Materials Market. The escalating demand for Green Construction Materials, including low-carbon concrete, recycled aggregates, and sustainable wood products, presents a vast growth avenue, supported by government incentives and a growing environmentally conscious consumer base. Technological advancements in Modular and Prefabricated Construction offer opportunities for increased efficiency, reduced waste, and faster project completion, appealing to both Residential and Commercial Construction. The expansion of Smart Cities Initiatives creates demand for materials integrated with sensors and IoT capabilities, improving infrastructure monitoring and maintenance. Opportunities also abound in retrofitting existing buildings for energy efficiency and resilience, driving demand for innovative insulation, smart windows, and durable Envelope materials to withstand extreme weather events.

Leading Players in the United States Construction Materials Market Market

- Cemex Sab De CV

- Colorado Stone Quarries Inc

- Buckman

- CRH PLC

- Heidelberg Materials

- Holcim

- Knife River Corporation

- Martin Marietta Materials

- Summit Materials Inc

- Kemira Oyj

- United States Lime & Minerals Inc

- Vulcan Materials Company

- Others

Key Developments in United States Construction Materials Market Industry

- July 2024: CEMEX SAB de CV entered a joint venture with Couch Aggregates, a sand and gravel supplier, and Premier Holdings, a distributor of marine bulk products. This collaboration aims to bolster Cemex's aggregate reserves by focusing on the production, distribution, and sale of sand, gravel, and limestone in the Mid-South United States. As a result, Cemex is set to enhance its presence and offer improved, expedited services to this burgeoning region, significantly impacting its market share in the Aggregates segment.

- July 2024: Heidelberg Materials acquired Carver Sand & Gravel, the largest aggregates producer in Albany, New York. This acquisition boosted the company’s operations, including crushed stone, sand and gravel, asphalt, and logistics, with a combined material capacity of around 3 million metric tons annually. This strategic move directly strengthens Heidelberg Materials' position in the Northeast US, increasing its production capabilities and market reach within the critical Aggregates segment.

Strategic Outlook for United States Construction Materials Market Market

The strategic outlook for the United States Construction Materials Market remains exceptionally positive, driven by persistent growth catalysts. Continuous government investment in infrastructure, coupled with a robust residential and commercial construction pipeline, will ensure sustained demand across all material types, especially for Aggregates and Cement & Concrete. The increasing emphasis on sustainability and resilience will propel innovation in green building materials and smart construction technologies, creating new market opportunities and competitive advantages. Companies that strategically invest in sustainable production methods, enhance supply chain resilience, and embrace digitalization will be best positioned to capitalize on the market's future potential. Furthermore, a focus on regional expansion through targeted M&A and strategic partnerships will be crucial for securing raw material access and optimizing distribution networks, ensuring long-term growth and profitability in a dynamically evolving market.

United States Construction Materials Market Segmentation

-

1. Material Type

-

1.1. Aggregates

- 1.1.1. Sand

- 1.1.2. Gravel

- 1.1.3. Crushed Stone

- 1.1.4. M-Sand

- 1.1.5. Granite

- 1.1.6. Others

- 1.2. Cement & Concrete

- 1.3. Metals

- 1.4. Bricks and Blocks

- 1.5. Wood

- 1.6. Glass

- 1.7. Others

-

1.1. Aggregates

-

2. Construction Type

- 2.1. New Construction

- 2.2. Renovation & Repair

-

3. Application

- 3.1. Structural

- 3.2. Envelope

- 3.3. Interior

- 3.4. Site & Landscaping

- 3.5. Others

-

4. End User

- 4.1. Residential Construction

- 4.2. Commercial Construction

- 4.3. Industrial Construction

United States Construction Materials Market Segmentation By Geography

- 1. United States

United States Construction Materials Market Regional Market Share

Geographic Coverage of United States Construction Materials Market

United States Construction Materials Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 5.1.1. Aggregates

- 5.1.1.1. Sand

- 5.1.1.2. Gravel

- 5.1.1.3. Crushed Stone

- 5.1.1.4. M-Sand

- 5.1.1.5. Granite

- 5.1.1.6. Others

- 5.1.2. Cement & Concrete

- 5.1.3. Metals

- 5.1.4. Bricks and Blocks

- 5.1.5. Wood

- 5.1.6. Glass

- 5.1.7. Others

- 5.1.1. Aggregates

- 5.2. Market Analysis, Insights and Forecast - by Construction Type

- 5.2.1. New Construction

- 5.2.2. Renovation & Repair

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Structural

- 5.3.2. Envelope

- 5.3.3. Interior

- 5.3.4. Site & Landscaping

- 5.3.5. Others

- 5.4. Market Analysis, Insights and Forecast - by End User

- 5.4.1. Residential Construction

- 5.4.2. Commercial Construction

- 5.4.3. Industrial Construction

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. United States

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 6. United States Construction Materials Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 6.1.1. Aggregates

- 6.1.1.1. Sand

- 6.1.1.2. Gravel

- 6.1.1.3. Crushed Stone

- 6.1.1.4. M-Sand

- 6.1.1.5. Granite

- 6.1.1.6. Others

- 6.1.2. Cement & Concrete

- 6.1.3. Metals

- 6.1.4. Bricks and Blocks

- 6.1.5. Wood

- 6.1.6. Glass

- 6.1.7. Others

- 6.1.1. Aggregates

- 6.2. Market Analysis, Insights and Forecast - by Construction Type

- 6.2.1. New Construction

- 6.2.2. Renovation & Repair

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Structural

- 6.3.2. Envelope

- 6.3.3. Interior

- 6.3.4. Site & Landscaping

- 6.3.5. Others

- 6.4. Market Analysis, Insights and Forecast - by End User

- 6.4.1. Residential Construction

- 6.4.2. Commercial Construction

- 6.4.3. Industrial Construction

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Cemex Sab De CV

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Colorado Stone Quarries Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Buckman

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 CRH PLC

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Heidelberg Materials

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Holcim

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Knife River Corporation�

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Martin Marietta Materials

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Summit Materials Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Kemira Oyj

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 United States Lime & Minerals Inc

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Vulcan Materials Company

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Others

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.1 Cemex Sab De CV

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: United States Construction Materials Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: United States Construction Materials Market Share (%) by Company 2025

List of Tables

- Table 1: United States Construction Materials Market Revenue billion Forecast, by Material Type 2020 & 2033

- Table 2: United States Construction Materials Market Revenue billion Forecast, by Construction Type 2020 & 2033

- Table 3: United States Construction Materials Market Revenue billion Forecast, by Application 2020 & 2033

- Table 4: United States Construction Materials Market Revenue billion Forecast, by End User 2020 & 2033

- Table 5: United States Construction Materials Market Revenue billion Forecast, by Region 2020 & 2033

- Table 6: United States Construction Materials Market Revenue billion Forecast, by Material Type 2020 & 2033

- Table 7: United States Construction Materials Market Revenue billion Forecast, by Construction Type 2020 & 2033

- Table 8: United States Construction Materials Market Revenue billion Forecast, by Application 2020 & 2033

- Table 9: United States Construction Materials Market Revenue billion Forecast, by End User 2020 & 2033

- Table 10: United States Construction Materials Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United States Construction Materials Market?

The projected CAGR is approximately 4%.

2. Which companies are prominent players in the United States Construction Materials Market?

Key companies in the market include Cemex Sab De CV, Colorado Stone Quarries Inc, Buckman, CRH PLC, Heidelberg Materials, Holcim, Knife River Corporation�, Martin Marietta Materials, Summit Materials Inc, Kemira Oyj, United States Lime & Minerals Inc, Vulcan Materials Company, Others .

3. What are the main segments of the United States Construction Materials Market?

The market segments include Material Type, Construction Type, Application, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 145 billion as of 2022.

5. What are some drivers contributing to market growth?

Rising Investments in the Infrastructure and Industrial Sectors; Growing Mining Activities and Increasing Popularity of Dimension Stones.

6. What are the notable trends driving market growth?

Rising Investments in the Infrastructure and Industrial Sectors Driving the Market.

7. Are there any restraints impacting market growth?

Rising Investments in the Infrastructure and Industrial Sectors; Growing Mining Activities and Increasing Popularity of Dimension Stones.

8. Can you provide examples of recent developments in the market?

July 2024: CEMEX SAB de CV entered a joint venture with Couch Aggregates, a sand and gravel supplier, and Premier Holdings, a distributor of marine bulk products. This collaboration aims to bolster Cemex's aggregate reserves by focusing on the production, distribution, and sale of sand, gravel, and limestone in the Mid-South United States. As a result, Cemex is set to enhance its presence and offer improved, expedited services to this burgeoning region.July 2024: Heidelberg Materials acquired Carver Sand & Gravel, the largest aggregates producer in Albany, New York. This acquisition boosted the company’s operations, including crushed stone, sand and gravel, asphalt, and logistics, with a combined material capacity of around 3 million metric tons annually.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United States Construction Materials Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United States Construction Materials Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United States Construction Materials Market?

To stay informed about further developments, trends, and reports in the United States Construction Materials Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence