Key Insights

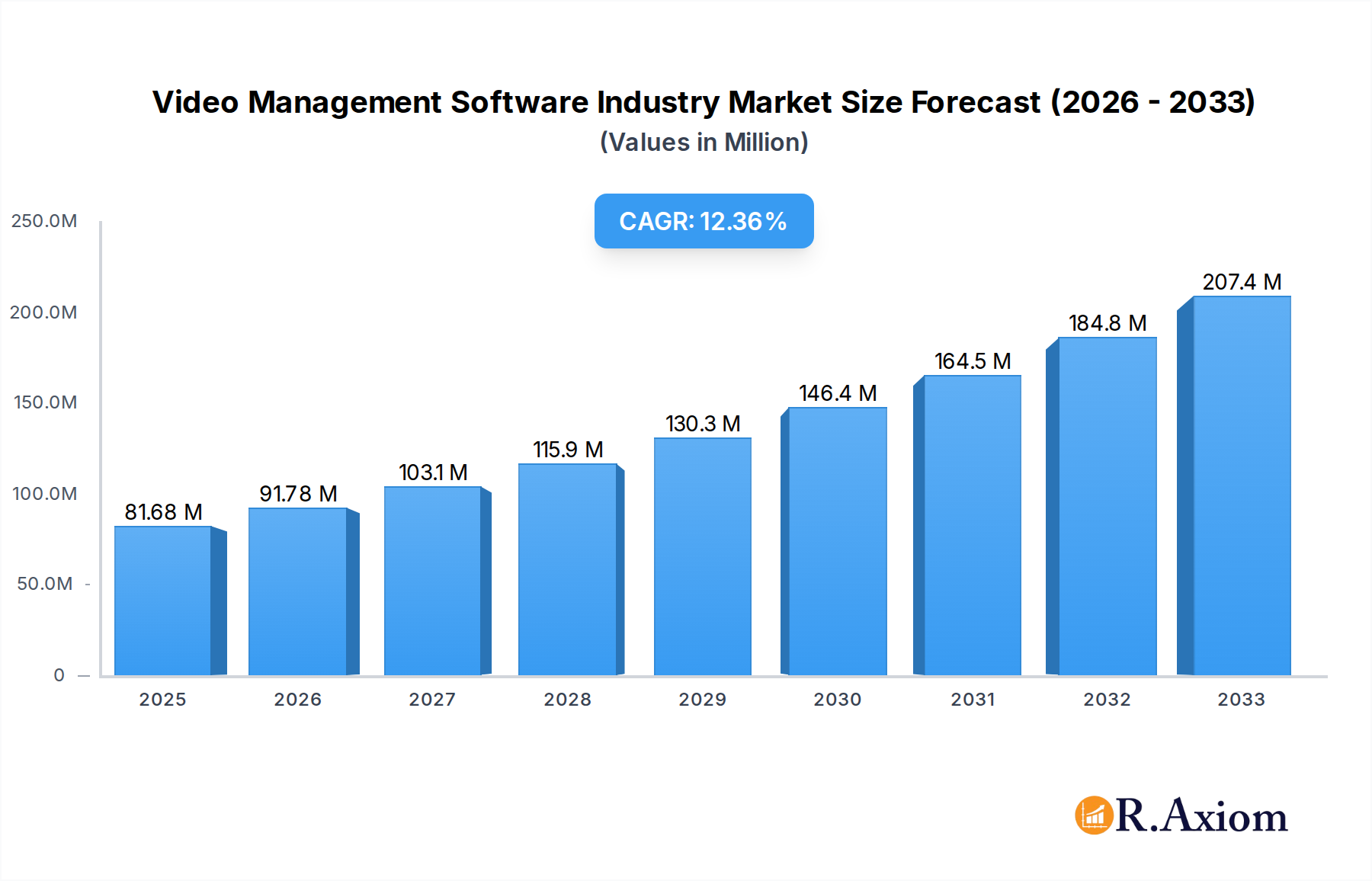

The global Video Management Software (VMS) market is poised for substantial expansion, with a current market size of 81.68 Million projected to grow at a robust Compound Annual Growth Rate (CAGR) of 12.22%. This upward trajectory is primarily driven by the escalating need for advanced security solutions across diverse sectors. The increasing adoption of IP cameras, coupled with the rising sophistication of video analytics, is a significant catalyst. Furthermore, the growing demand for centralized surveillance systems in commercial establishments, critical infrastructure, and institutional settings to enhance operational efficiency and security compliance fuels market growth. The integration of cloud-based solutions, such as Video Surveillance as a Service (VSaaS), is also playing a pivotal role, offering scalability, flexibility, and cost-effectiveness to businesses of all sizes. The trend towards smart cities and the proliferation of IoT devices further amplify the need for sophisticated VMS to manage and analyze the vast amounts of video data generated.

Video Management Software Industry Market Size (In Million)

Despite the promising growth, the market faces certain restraints. The initial high cost of advanced VMS solutions and the complexities associated with integration and implementation can be a deterrent for smaller organizations. Concerns regarding data privacy and cybersecurity also present challenges that VMS providers must address through robust security features and compliance measures. Geographically, North America and Europe are expected to continue leading the market, driven by strong regulatory frameworks and advanced technological adoption. However, the Asia Pacific region is anticipated to witness the fastest growth, fueled by rapid urbanization, infrastructure development, and increasing security investments in countries like China and India. The competitive landscape is characterized by the presence of major global players like Hangzhou Hikvision Digital Technology Company Limited, Zhejiang Dahua Technology Company Limited, and Bosch Security Systems Incorporated, alongside innovative emerging companies, all striving to capture market share through product innovation and strategic partnerships.

Video Management Software Industry Company Market Share

Video Management Software Industry Market Concentration & Innovation

The Video Management Software (VMS) market exhibits a moderate to high level of concentration, with a few dominant players holding significant market share. Key companies like Hangzhou Hikvision Digital Technology Company Limited, Zhejiang Dahua Technology Company Limited, and Bosch Security Systems Incorporated are leading the charge, bolstered by extensive product portfolios and global distribution networks. Innovation is primarily driven by advancements in Artificial Intelligence (AI) for sophisticated video analytics, including object detection, facial recognition, and behavioral analysis. The increasing adoption of IP cameras and cloud-based solutions (VSaaS) further fuels this innovation. Regulatory frameworks, particularly concerning data privacy and cybersecurity, are becoming increasingly stringent, influencing product development and compliance strategies. Product substitutes, such as basic CCTV systems and third-party analytics platforms, exist but often lack the integrated capabilities of comprehensive VMS. End-user trends point towards a growing demand for centralized management, remote access, and scalable solutions across all verticals. Merger and acquisition (M&A) activities are prevalent, with larger players acquiring smaller, specialized technology firms to expand their offerings and market reach. For instance, the acquisition of Qognify Inc. by Battery Ventures highlights strategic consolidation. The estimated total M&A deal value within the VMS sector is expected to reach hundreds of millions to billions of dollars over the forecast period. The continuous evolution of camera technology, from analog to advanced IP and hybrid systems, alongside robust storage solutions, underpins the growth and innovation within the VMS industry.

Video Management Software Industry Industry Trends & Insights

The Video Management Software (VMS) industry is experiencing robust growth, driven by a confluence of technological advancements, escalating security concerns, and evolving end-user demands. The Compound Annual Growth Rate (CAGR) for the VMS market is projected to be approximately 15% to 20% during the forecast period of 2025–2033. This significant expansion is fueled by the increasing global adoption of surveillance systems across commercial, industrial, and residential sectors, aiming to enhance security, operational efficiency, and loss prevention.

Technological disruptions are a primary catalyst. The integration of Artificial Intelligence (AI) and Machine Learning (ML) into VMS platforms is revolutionizing how video data is analyzed and utilized. Features such as advanced video analytics, including facial recognition, license plate recognition (LPR), crowd analysis, and anomaly detection, are becoming standard, enabling proactive threat identification and smarter decision-making. The shift from traditional on-premise VMS to cloud-based Video Surveillance as a Service (VSaaS) is another major trend. VSaaS offers scalability, flexibility, and reduced upfront infrastructure costs, making advanced surveillance solutions accessible to a wider range of businesses. The increasing prevalence of high-definition IP cameras, coupled with advancements in video compression technologies like H.265, contributes to better image quality and reduced bandwidth requirements, further supporting the growth of IP-based VMS solutions.

Consumer preferences are leaning towards more integrated and user-friendly systems. End-users are demanding VMS solutions that offer seamless integration with other security systems, such as access control, intrusion detection, and alarm management. The need for remote accessibility and mobile monitoring capabilities is paramount, allowing users to access live and recorded footage from anywhere, at any time, through web browsers or mobile applications. The growing emphasis on data security and privacy is also influencing VMS development, with a focus on robust encryption, secure access protocols, and compliance with data protection regulations.

Competitive dynamics within the VMS industry are characterized by intense innovation and strategic partnerships. Leading players are continuously investing in R&D to enhance their AI capabilities, cloud offerings, and user experience. Collaborations between VMS providers, camera manufacturers, and other security technology companies are becoming increasingly common to offer comprehensive, end-to-end solutions. The market penetration of advanced VMS features is steadily increasing as organizations recognize the tangible benefits of intelligent video surveillance in terms of improved security and operational intelligence. The overall market size is projected to reach tens of billions of dollars by the end of the forecast period, underscoring the significant economic impact and growth potential of the VMS industry.

Dominant Markets & Segments in Video Management Software Industry

The Video Management Software (VMS) industry is characterized by significant regional dominance and a diverse segmentation across hardware, software, and services, catering to a broad spectrum of end-user verticals.

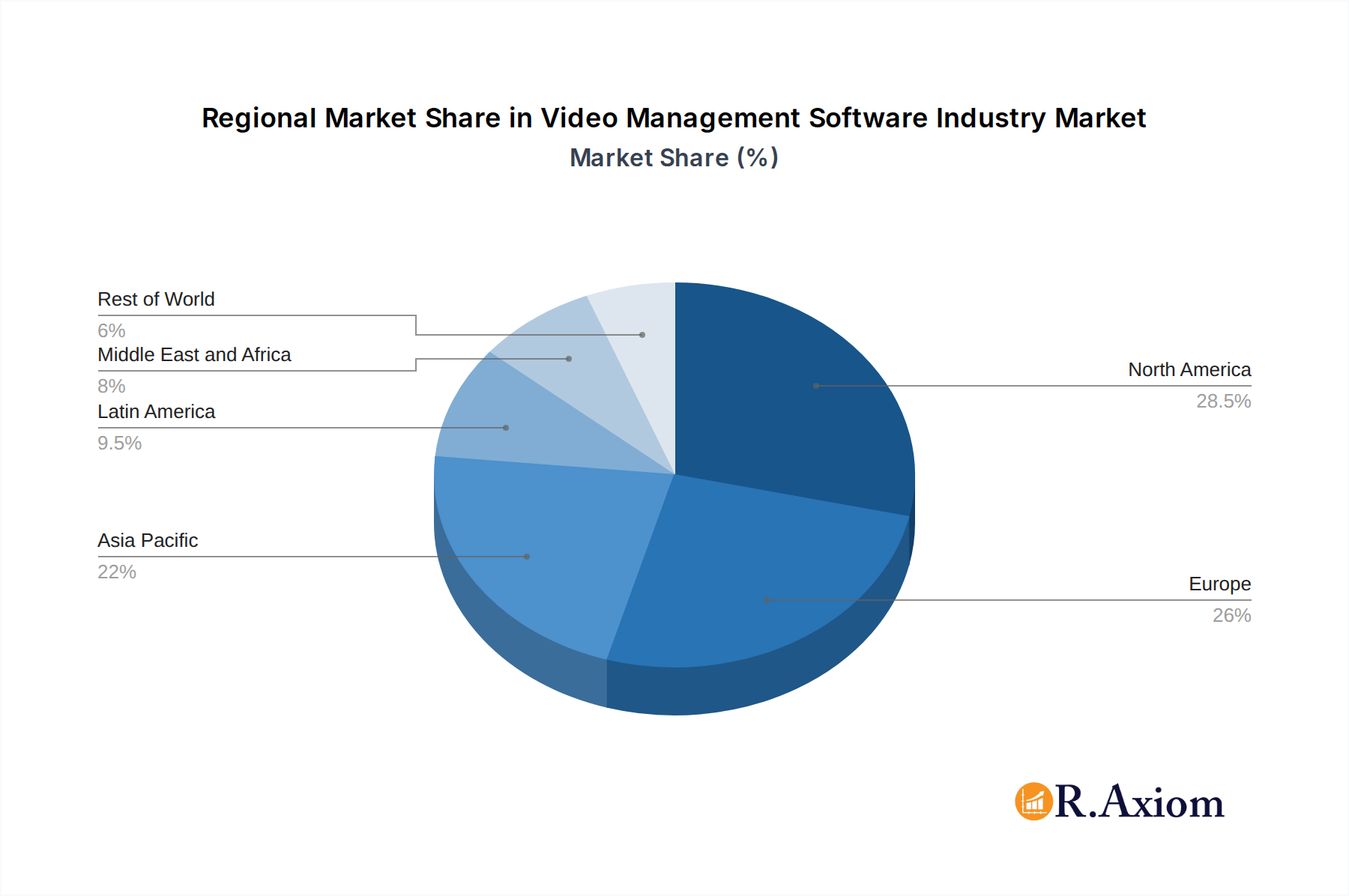

Regional Dominance: North America and Asia Pacific currently stand as the dominant regions in the global VMS market. North America's leadership is attributed to its early adoption of advanced security technologies, robust regulatory frameworks supporting surveillance, and a high concentration of commercial and industrial enterprises. The United States, in particular, represents a substantial market due to significant investments in infrastructure security, public safety, and smart city initiatives.

The Asia Pacific region is witnessing the fastest growth, propelled by rapid urbanization, increasing disposable incomes, and a rising awareness of security needs. Countries like China, India, and South Korea are major contributors, driven by government investments in smart city projects, manufacturing growth, and a burgeoning retail sector. The strong manufacturing base of VMS hardware and software solutions in these regions also plays a crucial role.

Segmentation Analysis:

Type:

- Hardware:

- Cameras:

- IP Cameras: These are the most dominant segment within cameras, accounting for over 70% of camera sales. Their superior resolution, flexibility, and network capabilities make them the preferred choice for modern surveillance systems. The market for IP cameras is valued in the billions of dollars.

- Analog Cameras: While declining, analog cameras still hold a significant share, particularly in regions with existing infrastructure or for cost-sensitive applications. Their market value is in the hundreds of millions of dollars.

- Hybrid Cameras: These offer a bridge between analog and IP, providing flexibility for upgrades. Their market is also in the hundreds of millions of dollars.

- Storage: Solutions ranging from Network Attached Storage (NAS) and Storage Area Networks (SAN) to cloud storage are critical. The storage segment for VMS is valued in the billions of dollars, with a growing preference for high-capacity, scalable solutions.

- Cameras:

- Software:

- Video Analytics: This is a high-growth segment, driven by AI integration. The market for video analytics is projected to reach billions of dollars, offering advanced insights from video feeds.

- Video Management Software (VMS): The core of the market, VMS platforms are essential for managing and analyzing video streams. The VMS software market itself is valued in the billions of dollars, with steady growth fueled by feature enhancements and cloud adoption.

- Services:

- VSaaS (Video Surveillance as a Service): This cloud-based service model is rapidly gaining traction, offering subscription-based access to VMS functionalities. The VSaaS market is valued in the hundreds of millions to billions of dollars, with significant growth potential.

- Hardware:

End-user Vertical:

- Commercial: This is the largest and most diverse vertical, encompassing retail, hospitality, and corporate offices. Demand is driven by loss prevention, customer analytics, and employee safety. The commercial sector accounts for a substantial portion of the market, estimated to be in the billions of dollars.

- Infrastructure: This includes transportation hubs, utilities, and critical infrastructure. Security and monitoring are paramount, driving significant investments. The infrastructure segment is valued in the billions of dollars.

- Institutional: This comprises educational institutions, healthcare facilities, and government buildings. Focus areas include campus safety, patient monitoring, and secure access. The institutional sector's market value is in the billions of dollars.

- Industrial: Manufacturing plants, warehouses, and oil & gas facilities rely on VMS for operational efficiency, safety compliance, and asset protection. This segment is valued in the billions of dollars.

- Defense: Government and military applications require advanced surveillance for border security, intelligence gathering, and base protection. The defense sector represents a significant, albeit often specialized, market valued in the hundreds of millions to billions of dollars.

- Residential: Home security and smart home integration are driving growth in the residential VMS market, particularly with the rise of DIY security systems and VSaaS. This segment, while smaller than commercial, is growing rapidly and is valued in the hundreds of millions of dollars.

Key drivers for dominance in these segments include technological advancements, favorable economic policies, infrastructure development, and the increasing awareness of security and operational benefits offered by advanced VMS solutions. The interplay between these segments and verticals shapes the overall landscape and future trajectory of the Video Management Software industry.

Video Management Software Industry Product Developments

The VMS industry is witnessing continuous product innovation focused on enhancing intelligence, integration, and user experience. Key trends include the incorporation of advanced AI-powered video analytics for real-time threat detection, such as anomaly detection and predictive analytics. Manufacturers are emphasizing seamless integration with a broader ecosystem of security devices and IT infrastructure, enabling a unified security management approach. The development of scalable, cloud-native VMS platforms, including VSaaS, is accelerating, offering greater flexibility and accessibility. Furthermore, there's a growing focus on cybersecurity features to protect video data from unauthorized access and tampering, ensuring data integrity and compliance. Competitive advantages are being derived from user-friendly interfaces, mobile accessibility, and specialized solutions tailored to specific industry verticals, making VMS an indispensable tool for modern security and operational management.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the global Video Management Software (VMS) industry, covering the period from 2019 to 2033, with a base year of 2025 and a forecast period of 2025–2033. The segmentation analysis delves into the market across key dimensions to offer granular insights.

Type Segmentation: The market is segmented by Type, encompassing Hardware, Software, and Services. Hardware includes Cameras (Analog, IP Cameras, Hybrid) and Storage solutions. Software covers Video Analytics and the core Video Management Software itself. Services primarily include VSaaS (Video Surveillance as a Service). Each of these segments is analyzed for market size, growth projections, and competitive dynamics, with IP Cameras and Video Analytics software expected to exhibit the highest growth rates.

End-user Vertical Segmentation: The report further segments the market by End-user Verticals such as Commercial, Infrastructure, Institutional, Industrial, Defense, and Residential. This segmentation highlights the diverse applications and demand drivers across different industries. The Commercial and Infrastructure verticals are anticipated to lead in terms of market share, while the Residential sector is expected to show the fastest growth due to increasing home security awareness. Growth projections and competitive landscapes for each vertical are detailed.

Key Drivers of Video Management Software Industry Growth

The growth of the Video Management Software (VMS) industry is propelled by several key factors. Technological advancements, particularly in Artificial Intelligence (AI) and machine learning, are driving the development of intelligent video analytics, enabling proactive threat detection and operational insights. The escalating global concerns for public safety and security, coupled with rising crime rates and the need for asset protection, are significant demand generators. The widespread adoption of IP cameras and IoT devices creates a growing volume of data that necessitates sophisticated management and analysis. Furthermore, the increasing trend towards remote monitoring and cloud-based solutions (VSaaS), offering scalability and cost-effectiveness, is significantly boosting market penetration. Government initiatives supporting smart city development and infrastructure upgrades also contribute to substantial market expansion.

Challenges in the Video Management Software Industry Sector

Despite its robust growth, the Video Management Software (VMS) industry faces several challenges. Data privacy and cybersecurity concerns are paramount, as the vast amounts of video data collected are sensitive and vulnerable to breaches. Stringent regulations like GDPR and CCPA require VMS providers to implement robust data protection measures, adding complexity and cost. The interoperability between different hardware manufacturers and software platforms can be a hurdle, leading to vendor lock-in and integration challenges. The high initial investment cost for advanced VMS solutions and associated hardware can be a barrier for small and medium-sized enterprises. Finally, the increasing complexity of AI algorithms and their deployment, along with the need for skilled personnel to manage and interpret the data, presents a technical and operational challenge.

Emerging Opportunities in Video Management Software Industry

The Video Management Software (VMS) industry is ripe with emerging opportunities. The rapid advancement and adoption of AI and machine learning present a significant avenue for developing more sophisticated video analytics, such as predictive policing and behavioral analysis. The growth of VSaaS (Video Surveillance as a Service) continues to expand, offering recurring revenue streams and making advanced VMS accessible to a wider market. The increasing integration of VMS with other smart city technologies and IoT platforms opens up new applications in traffic management, public safety, and environmental monitoring. Furthermore, the demand for edge computing capabilities in VMS allows for real-time data processing closer to the source, reducing latency and bandwidth requirements. The focus on video data security and privacy compliance is creating opportunities for specialized solutions and certifications.

Leading Players in the Video Management Software Industry Market

- Samsung Group

- Infinova Corporation

- Hangzhou Hikvision Digital Technology Company Limited

- Bosch Security Systems Incorporated

- Honeywell Security Group

- Schneider Electric SE

- FLIR Systems Inc

- Sony Corporation

- Zhejiang Dahua Technology Company Limited

- Qognify Inc (Battery Ventures)

- Axis Communications AB

- Panasonic Corporation

Key Developments in Video Management Software Industry Industry

- May 2022 - Tenda introduced the CP3 security camera in India. This security camera features pan and tilt functions and full-duplex 2-way audio communication. This security camera is aimed for use in small and home offices. The camera is an AI-powered security camera system that identifies and tracks motion. It has a full-HD 1080p image sensor that rotates 360 degrees to cover the majority of home and small office spaces.

- June 2022 - Canon India opened an experience center in New Delhi to showcase the company's full range of Network Video Surveillance (NVS) technologies. Canon's target is to become an end-to-end surveillance solutions provider and systems integrator, providing consultation and services on CCTV surveillance, access control, public address, and video analytics while addressing the entire networking and surveillance life cycle with this launch. Canon is also bringing together top surveillance industry leaders Axis, Milestone, and BCD under one umbrella to expand their NVS product range further to develop advanced video solutions in the Indian market.

- December 2021 - Axis Communications has launched an open-source video authentication project used in the company's cameras to ensure the integrity of surveillance video. Axis has released a document outlining partners' framework when deploying integrated video authentication solutions.

- September 2021 - LENSEC's Perspective Video Management Software was integrated with Bosch's Intrusion Control Panels (B and G Series). The new collaboration between the companies will allow security operators to manage intrusion, fire, and access control systems while viewing video surveillance cameras through a single pane of glass.

Strategic Outlook for Video Management Software Industry Market

The strategic outlook for the Video Management Software (VMS) industry is overwhelmingly positive, characterized by continued innovation and market expansion. Future growth will be significantly driven by the deeper integration of Artificial Intelligence (AI), enabling predictive analytics and automated threat response. The shift towards cloud-native VMS and VSaaS models will accelerate, offering greater flexibility, scalability, and cost-efficiency for end-users. Strategic partnerships and M&A activities are expected to continue as companies seek to consolidate their market position and acquire specialized technologies. The increasing emphasis on cybersecurity and data privacy will foster the development of robust, compliant VMS solutions. Furthermore, the expansion of VMS into emerging markets and its integration with broader IoT and smart city ecosystems will unlock new revenue streams and application areas, solidifying its position as an indispensable technology for security, operations, and intelligence.

Video Management Software Industry Segmentation

-

1. Type

-

1.1. Hardware

-

1.1.1. Camera

- 1.1.1.1. Analog

- 1.1.1.2. IP Cameras

- 1.1.1.3. Hybrid

- 1.1.2. Storage

-

1.1.1. Camera

-

1.2. Software

- 1.2.1. Video Analytics

- 1.2.2. Video Management Software

- 1.3. Services (VSaaS)

-

1.1. Hardware

-

2. End-user Vertical

- 2.1. Commercial

- 2.2. Infrastructure

- 2.3. Institutional

- 2.4. Industrial

- 2.5. Defense

- 2.6. Residential

Video Management Software Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Rest of Asia Pacific

-

4. Latin America

- 4.1. Brazil

- 4.2. Mexico

- 4.3. Rest of Latin America

-

5. Middle East and Africa

- 5.1. United Arab Emirates

- 5.2. Saudi Arabia

- 5.3. Rest of Middle East and Africa

Video Management Software Industry Regional Market Share

Geographic Coverage of Video Management Software Industry

Video Management Software Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.22% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Hardware

- 5.1.1.1. Camera

- 5.1.1.1.1. Analog

- 5.1.1.1.2. IP Cameras

- 5.1.1.1.3. Hybrid

- 5.1.1.2. Storage

- 5.1.1.1. Camera

- 5.1.2. Software

- 5.1.2.1. Video Analytics

- 5.1.2.2. Video Management Software

- 5.1.3. Services (VSaaS)

- 5.1.1. Hardware

- 5.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 5.2.1. Commercial

- 5.2.2. Infrastructure

- 5.2.3. Institutional

- 5.2.4. Industrial

- 5.2.5. Defense

- 5.2.6. Residential

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Video Management Software Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Hardware

- 6.1.1.1. Camera

- 6.1.1.1.1. Analog

- 6.1.1.1.2. IP Cameras

- 6.1.1.1.3. Hybrid

- 6.1.1.2. Storage

- 6.1.1.1. Camera

- 6.1.2. Software

- 6.1.2.1. Video Analytics

- 6.1.2.2. Video Management Software

- 6.1.3. Services (VSaaS)

- 6.1.1. Hardware

- 6.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 6.2.1. Commercial

- 6.2.2. Infrastructure

- 6.2.3. Institutional

- 6.2.4. Industrial

- 6.2.5. Defense

- 6.2.6. Residential

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Video Management Software Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Hardware

- 7.1.1.1. Camera

- 7.1.1.1.1. Analog

- 7.1.1.1.2. IP Cameras

- 7.1.1.1.3. Hybrid

- 7.1.1.2. Storage

- 7.1.1.1. Camera

- 7.1.2. Software

- 7.1.2.1. Video Analytics

- 7.1.2.2. Video Management Software

- 7.1.3. Services (VSaaS)

- 7.1.1. Hardware

- 7.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 7.2.1. Commercial

- 7.2.2. Infrastructure

- 7.2.3. Institutional

- 7.2.4. Industrial

- 7.2.5. Defense

- 7.2.6. Residential

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Video Management Software Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Hardware

- 8.1.1.1. Camera

- 8.1.1.1.1. Analog

- 8.1.1.1.2. IP Cameras

- 8.1.1.1.3. Hybrid

- 8.1.1.2. Storage

- 8.1.1.1. Camera

- 8.1.2. Software

- 8.1.2.1. Video Analytics

- 8.1.2.2. Video Management Software

- 8.1.3. Services (VSaaS)

- 8.1.1. Hardware

- 8.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 8.2.1. Commercial

- 8.2.2. Infrastructure

- 8.2.3. Institutional

- 8.2.4. Industrial

- 8.2.5. Defense

- 8.2.6. Residential

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific Video Management Software Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Hardware

- 9.1.1.1. Camera

- 9.1.1.1.1. Analog

- 9.1.1.1.2. IP Cameras

- 9.1.1.1.3. Hybrid

- 9.1.1.2. Storage

- 9.1.1.1. Camera

- 9.1.2. Software

- 9.1.2.1. Video Analytics

- 9.1.2.2. Video Management Software

- 9.1.3. Services (VSaaS)

- 9.1.1. Hardware

- 9.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 9.2.1. Commercial

- 9.2.2. Infrastructure

- 9.2.3. Institutional

- 9.2.4. Industrial

- 9.2.5. Defense

- 9.2.6. Residential

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Latin America Video Management Software Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Hardware

- 10.1.1.1. Camera

- 10.1.1.1.1. Analog

- 10.1.1.1.2. IP Cameras

- 10.1.1.1.3. Hybrid

- 10.1.1.2. Storage

- 10.1.1.1. Camera

- 10.1.2. Software

- 10.1.2.1. Video Analytics

- 10.1.2.2. Video Management Software

- 10.1.3. Services (VSaaS)

- 10.1.1. Hardware

- 10.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 10.2.1. Commercial

- 10.2.2. Infrastructure

- 10.2.3. Institutional

- 10.2.4. Industrial

- 10.2.5. Defense

- 10.2.6. Residential

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Middle East and Africa Video Management Software Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Hardware

- 11.1.1.1. Camera

- 11.1.1.1.1. Analog

- 11.1.1.1.2. IP Cameras

- 11.1.1.1.3. Hybrid

- 11.1.1.2. Storage

- 11.1.1.1. Camera

- 11.1.2. Software

- 11.1.2.1. Video Analytics

- 11.1.2.2. Video Management Software

- 11.1.3. Services (VSaaS)

- 11.1.1. Hardware

- 11.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 11.2.1. Commercial

- 11.2.2. Infrastructure

- 11.2.3. Institutional

- 11.2.4. Industrial

- 11.2.5. Defense

- 11.2.6. Residential

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Samsung Group

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Infinova Corporation

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Hangzhou Hikvision Digital Technology Company Limited

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Bosch Security Systems Incorporated

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Honeywell Security Group

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Schneider Electric SE

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 FLIR systems Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Sony Corporation

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Zhejiang Dahua Technology Company Limited

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Qognify Inc (Battery Ventures)

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Axis Communications AB

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Panasonic Corporation

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Samsung Group

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Video Management Software Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Video Management Software Industry Revenue (Million), by Type 2025 & 2033

- Figure 3: North America Video Management Software Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Video Management Software Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 5: North America Video Management Software Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 6: North America Video Management Software Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Video Management Software Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Video Management Software Industry Revenue (Million), by Type 2025 & 2033

- Figure 9: Europe Video Management Software Industry Revenue Share (%), by Type 2025 & 2033

- Figure 10: Europe Video Management Software Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 11: Europe Video Management Software Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 12: Europe Video Management Software Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Video Management Software Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Video Management Software Industry Revenue (Million), by Type 2025 & 2033

- Figure 15: Asia Pacific Video Management Software Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Asia Pacific Video Management Software Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 17: Asia Pacific Video Management Software Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 18: Asia Pacific Video Management Software Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Pacific Video Management Software Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America Video Management Software Industry Revenue (Million), by Type 2025 & 2033

- Figure 21: Latin America Video Management Software Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: Latin America Video Management Software Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 23: Latin America Video Management Software Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 24: Latin America Video Management Software Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Latin America Video Management Software Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Video Management Software Industry Revenue (Million), by Type 2025 & 2033

- Figure 27: Middle East and Africa Video Management Software Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: Middle East and Africa Video Management Software Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 29: Middle East and Africa Video Management Software Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 30: Middle East and Africa Video Management Software Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Middle East and Africa Video Management Software Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Video Management Software Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Global Video Management Software Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 3: Global Video Management Software Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Video Management Software Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: Global Video Management Software Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 6: Global Video Management Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States Video Management Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada Video Management Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Global Video Management Software Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 10: Global Video Management Software Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 11: Global Video Management Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Germany Video Management Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: United Kingdom Video Management Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: France Video Management Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Rest of Europe Video Management Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Global Video Management Software Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 17: Global Video Management Software Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 18: Global Video Management Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 19: China Video Management Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Japan Video Management Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: India Video Management Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Rest of Asia Pacific Video Management Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Global Video Management Software Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 24: Global Video Management Software Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 25: Global Video Management Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 26: Brazil Video Management Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Mexico Video Management Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Rest of Latin America Video Management Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: Global Video Management Software Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 30: Global Video Management Software Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 31: Global Video Management Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 32: United Arab Emirates Video Management Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: Saudi Arabia Video Management Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Rest of Middle East and Africa Video Management Software Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Video Management Software Industry?

The projected CAGR is approximately 12.22%.

2. Which companies are prominent players in the Video Management Software Industry?

Key companies in the market include Samsung Group, Infinova Corporation, Hangzhou Hikvision Digital Technology Company Limited, Bosch Security Systems Incorporated, Honeywell Security Group, Schneider Electric SE, FLIR systems Inc, Sony Corporation, Zhejiang Dahua Technology Company Limited, Qognify Inc (Battery Ventures), Axis Communications AB, Panasonic Corporation.

3. What are the main segments of the Video Management Software Industry?

The market segments include Type, End-user Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 81.68 Million as of 2022.

5. What are some drivers contributing to market growth?

5.; Augmented Demand of IP Cameras5.; Emergence Of Video Surveillance-as-a-Service (VSAAS)5.; Increasing Demand For Video Analytics.

6. What are the notable trends driving market growth?

Infrastructure Segment is Expected to Register Significant Growth.

7. Are there any restraints impacting market growth?

5.; Need for High-capacity Storage for High-resolution Images5.; Privacy and Security Issues.

8. Can you provide examples of recent developments in the market?

May 2022 - Tenda introduced the CP3 security camera in India. This security camera features pan and tilt functions and full-duplex 2-way audio communication. This security camera is aimed for use in small and home offices. The camera is an AI-powered security camera system that identifies and tracks motion. It has a full-HD 1080p image sensor that rotates 360 degrees to cover the majority of home and small office spaces.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Video Management Software Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Video Management Software Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Video Management Software Industry?

To stay informed about further developments, trends, and reports in the Video Management Software Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence