Key Insights

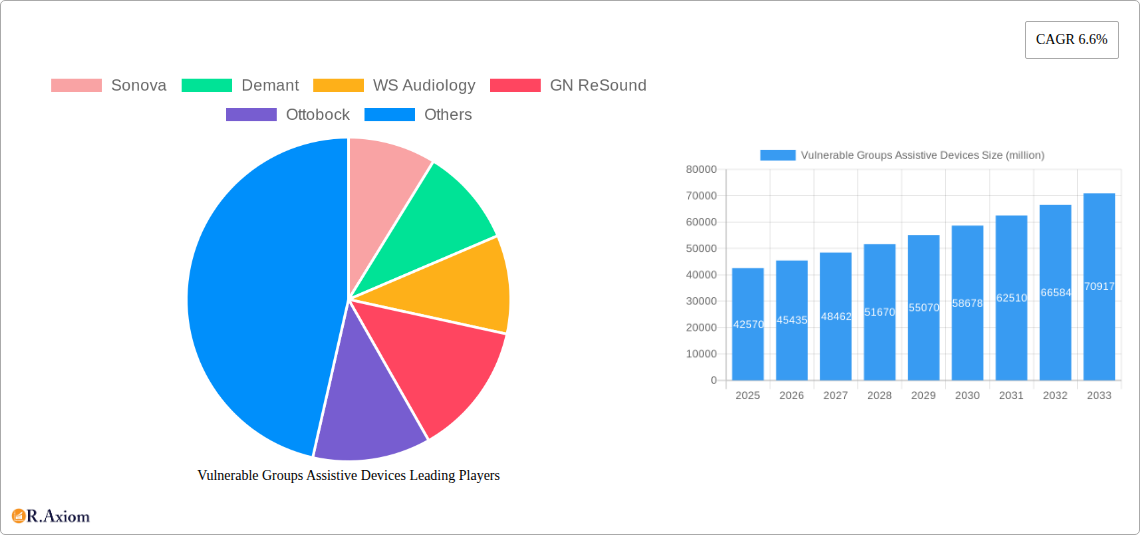

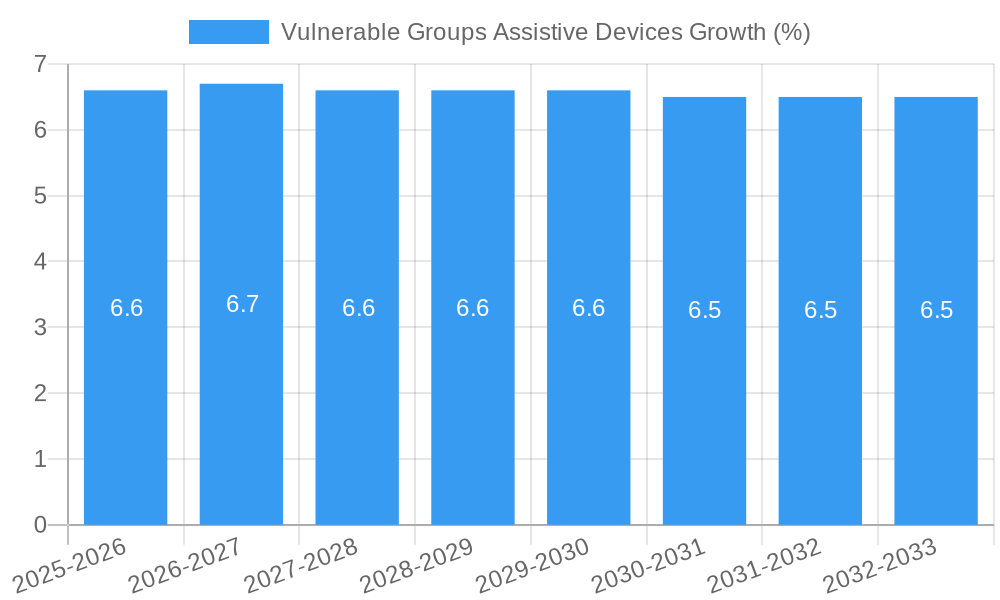

The Vulnerable Groups Assistive Devices market is poised for substantial growth, projected to reach an estimated value of $42,570 million, demonstrating a robust Compound Annual Growth Rate (CAGR) of 6.6% from 2025 to 2033. This expansion is propelled by a confluence of critical drivers, including the increasing prevalence of age-related chronic conditions and disabilities, a growing awareness and adoption of assistive technologies, and supportive government initiatives aimed at improving the quality of life for vulnerable populations. The rising global elderly population, coupled with advancements in medical technology and a greater emphasis on independent living, further fuels demand. The market is segmented into key applications such as Home Care Settings and Hospitals, with Hearing Aids, Mobility Aids Devices, and Vision & Reading Aids representing the dominant product types. Innovations in miniaturization, AI integration, and enhanced user-friendliness are continuously shaping the product landscape, making these devices more accessible and effective.

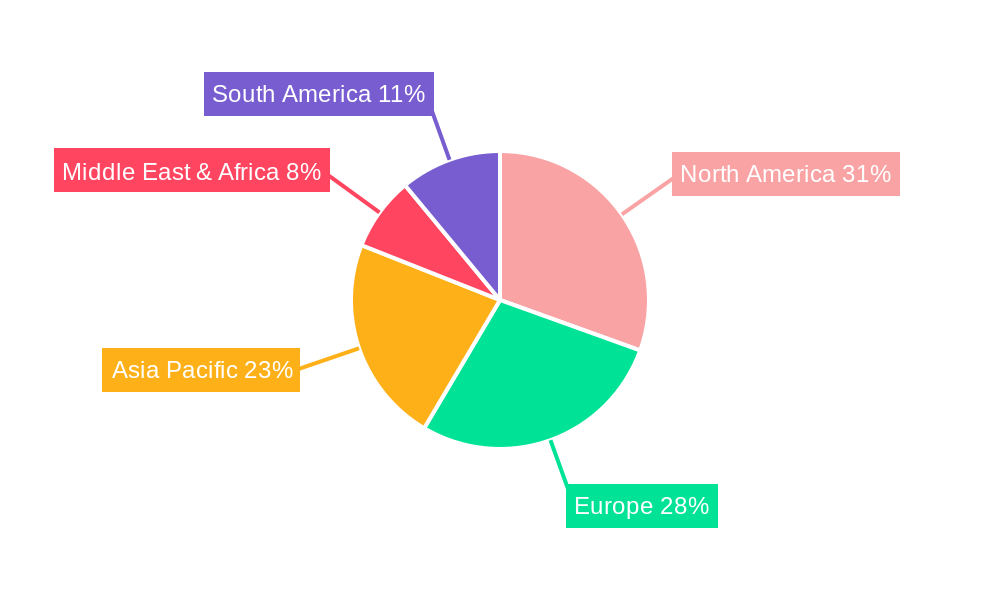

The market's trajectory is also influenced by significant trends like the shift towards personalized and smart assistive devices, increasing integration of IoT and wearable technology for remote monitoring and enhanced functionality, and a growing preference for home-based care solutions. However, certain restraints, such as the high cost of advanced assistive devices and limited reimbursement policies in some regions, could temper the pace of adoption. Despite these challenges, the market is expected to witness strong growth across major regions, with North America and Europe leading in terms of value, driven by established healthcare infrastructure and high disposable incomes. The Asia Pacific region, however, presents the fastest-growing market due to its large and aging population, increasing healthcare expenditure, and a rising demand for advanced medical devices. Key players like Sonova, Demant, and WS Audiology are actively investing in research and development to introduce innovative products and expand their market reach, further solidifying the market's positive outlook.

Sure, here is an SEO-optimized and detailed report description for Vulnerable Groups Assistive Devices:

Vulnerable Groups Assistive Devices Market Concentration & Innovation

This comprehensive report delves into the intricate landscape of the Vulnerable Groups Assistive Devices market, analyzing its concentration, key innovation drivers, and the overarching regulatory frameworks influencing its trajectory. With a study period spanning from 2019 to 2033, a base year of 2025, and a forecast period from 2025 to 2033, the report offers deep insights into market dynamics. Major companies such as Sonova, Demant, WS Audiology, GN ReSound, Ottobock, Invacare, Enovis, Starkey, Ossur, Rion, Cochlear, Sunrise Medical, Permobil Corp, MED-EL, Pride Mobility, Hoveround Corp, Merits Health Products, Drive Medical, GF Health, and Vispero are meticulously profiled. The analysis highlights significant market share contributions and M&A deal values, estimated to be in the billions, underscoring the consolidation and strategic investments within the sector.

- Market Concentration: The market is characterized by a moderate to high concentration, with a few key players holding substantial market share, particularly in specialized segments like hearing aids and advanced mobility devices.

- Innovation Drivers: Technological advancements in AI, miniaturization, and connectivity are paramount, alongside an increasing focus on user-centric design and personalized solutions for diverse needs.

- Regulatory Frameworks: Stringent regulatory approvals (e.g., FDA, CE marking) significantly influence product development and market entry, ensuring safety and efficacy.

- Product Substitutes: While direct substitutes are limited, alternative therapeutic interventions and technological workarounds represent potential competitive pressures.

- End-User Trends: An aging global population, rising prevalence of chronic conditions, and a growing awareness of assistive technologies are major demand drivers.

- M&A Activities: The market has witnessed significant M&A activities, with estimated deal values in the hundreds of millions, indicating strategic consolidation and expansion by leading firms.

Vulnerable Groups Assistive Devices Industry Trends & Insights

The Vulnerable Groups Assistive Devices market is poised for substantial growth, driven by a confluence of demographic shifts, technological breakthroughs, and evolving consumer preferences. This report provides an in-depth exploration of the industry's current state and future outlook, with a projected Compound Annual Growth Rate (CAGR) of approximately 7.5% over the forecast period (2025–2033). The base year of 2025 sees a market value estimated in the tens of billions, with significant expansion anticipated. Technological disruptions, particularly in artificial intelligence, smart connectivity, and advanced materials, are reshaping product capabilities and user experiences. AI-powered features in hearing aids, for instance, are enhancing speech clarity and environmental sound adaptation. Similarly, advancements in lightweight materials and electric propulsion are revolutionizing mobility aids, offering greater independence and mobility to users.

Consumer preferences are increasingly shifting towards personalized and discreet solutions. Users are seeking assistive devices that integrate seamlessly into their daily lives, offering both functionality and aesthetic appeal. This trend is particularly evident in the hearing aids segment, where smaller, more aesthetically pleasing designs and advanced connectivity options are in high demand. The market penetration of advanced assistive devices is steadily increasing as awareness grows and affordability improves, albeit with regional disparities. The competitive landscape is intensifying, with established players like Sonova, Demant, and WS Audiology continuously innovating, while new entrants leverage emerging technologies. This dynamic environment fosters rapid product development and a focus on delivering superior value to end-users. The increasing prevalence of age-related conditions such as hearing loss, visual impairment, and mobility challenges due to arthritis and other chronic diseases directly fuels the demand for these specialized devices. Furthermore, supportive government initiatives and reimbursement policies in developed nations are crucial in driving market adoption and accessibility. The report meticulously analyzes these trends, providing actionable insights for stakeholders to navigate this evolving market effectively.

Dominant Markets & Segments in Vulnerable Groups Assistive Devices

The Vulnerable Groups Assistive Devices market is characterized by distinct regional dominance and segment leadership, driven by a combination of economic, demographic, and infrastructural factors. North America and Europe currently represent the dominant markets, attributed to higher disposable incomes, robust healthcare infrastructure, and proactive government support for assistive technologies. The United States, in particular, stands out due to its large aging population and advanced healthcare reimbursement systems. Within these regions, Home Care Settings are emerging as a pivotal application, experiencing rapid growth due to the increasing preference for in-home care and the development of user-friendly, connected assistive devices. This trend is projected to outpace the growth in Hospital settings and other applications.

- Dominant Region: North America and Europe lead due to strong economic policies, advanced healthcare infrastructure, and high awareness of assistive technologies.

- Dominant Country: The United States exhibits significant market dominance owing to its demographic profile and supportive reimbursement frameworks.

- Dominant Application: Home Care Settings are expected to witness the fastest growth, driven by convenience, technological integration, and an aging population’s preference for in-home solutions. This segment's growth is estimated to be over 8.0% CAGR.

- Dominant Type: Mobility Aids Devices currently hold the largest market share, reflecting the significant unmet needs related to age-related mobility impairments. However, Hearing Aids are experiencing rapid innovation and adoption, positioning them for significant future growth, with an estimated market share projected to reach over 30% by 2033.

Key drivers underpinning this dominance include favorable economic policies that incentivize healthcare spending, extensive public and private insurance coverage, and a well-established distribution network for assistive devices. Infrastructure development, particularly in digital connectivity, is also crucial for the uptake of smart assistive technologies. The growing awareness of the benefits of assistive devices in enhancing quality of life and promoting independence among vulnerable populations further solidifies the dominance of these leading markets and segments.

Vulnerable Groups Assistive Devices Product Developments

The Vulnerable Groups Assistive Devices market is experiencing a wave of innovation, with a strong focus on enhancing user experience and functional efficacy. Recent product developments emphasize miniaturization, improved connectivity, and the integration of artificial intelligence. For instance, next-generation hearing aids now offer seamless Bluetooth connectivity, personalized soundscapes managed via smartphone apps, and AI-driven noise reduction for superior audibility in complex environments. In the mobility sector, lightweight, foldable electric wheelchairs and advanced exoskeletons are empowering users with unprecedented freedom of movement. Vision and reading aids are incorporating optical character recognition (OCR) technology for real-time text-to-speech conversion, significantly improving accessibility for visually impaired individuals. These advancements are creating significant competitive advantages for companies investing in R&D, leading to improved market penetration and user satisfaction.

Report Scope & Segmentation Analysis

This report provides a comprehensive segmentation of the Vulnerable Groups Assistive Devices market, offering detailed analysis across key categories. The market is segmented by Application into Home Care Settings, Hospitals, and Others, with Home Care Settings projected to exhibit the highest growth rate, estimated at over 8.0% CAGR. By Type, the segmentation includes Hearing Aids, Mobility Aids Devices, Vision & Reading Aids, and Others. Hearing Aids are a rapidly evolving segment, expected to gain significant market share, driven by technological advancements and increasing awareness. Mobility Aids Devices currently hold the largest share, addressing critical needs for individuals with physical limitations.

- Application Segmentation:

- Home Care Settings: This segment is forecast to grow robustly due to the increasing trend of aging in place and the development of smart, user-friendly assistive devices for home use. Market size is projected to reach over $30 billion by 2033.

- Hospitals: While still significant, this segment's growth rate is moderate, driven by rehabilitation and long-term care needs.

- Others: This includes specialized settings like educational institutions and community centers, with steady but slower growth.

- Type Segmentation:

- Hearing Aids: Experiencing rapid innovation and adoption, with a projected CAGR of approximately 7.0% and a market value estimated to exceed $20 billion by 2033.

- Mobility Aids Devices: Currently the largest segment, projected to maintain strong growth driven by an aging population and advancements in electric and lightweight technologies.

- Vision & Reading Aids: A growing segment with increasing demand for digital solutions like OCR-enabled devices.

- Others: Encompasses a range of assistive products like communication devices and personal emergency response systems.

Key Drivers of Vulnerable Groups Assistive Devices Growth

The growth of the Vulnerable Groups Assistive Devices market is propelled by a potent combination of demographic, technological, and economic factors. The persistently aging global population is a primary driver, as age-related conditions like hearing loss, visual impairment, and mobility issues necessitate the use of assistive technologies. Technological advancements, including AI integration, miniaturization, and enhanced connectivity (e.g., IoT for smart devices), are creating more effective, user-friendly, and personalized solutions. Furthermore, increasing healthcare expenditure, both public and private, coupled with government initiatives and reimbursement policies aimed at improving the quality of life for vulnerable populations, are significantly boosting market demand. Growing awareness among end-users and caregivers about the benefits of these devices further fuels adoption.

Challenges in the Vulnerable Groups Assistive Devices Sector

Despite the robust growth prospects, the Vulnerable Groups Assistive Devices sector faces several significant challenges. High product costs can be a major barrier to adoption, particularly in developing economies, limiting accessibility for lower-income populations. Regulatory hurdles, though essential for product safety, can be time-consuming and expensive, potentially slowing down market entry for new innovations. Supply chain disruptions, as experienced globally in recent years, can impact the availability and cost of critical components. Furthermore, ensuring adequate training and support for end-users and healthcare professionals is crucial for effective device utilization, and this often requires substantial investment. Competitive pressures from both established players and emerging technologies also necessitate continuous innovation and cost-efficiency.

Emerging Opportunities in Vulnerable Groups Assistive Devices

The Vulnerable Groups Assistive Devices market presents numerous emerging opportunities for innovation and growth. The increasing demand for personalized and customizable solutions, driven by a deeper understanding of individual needs, opens avenues for bespoke device development. The integration of telehealth and remote monitoring technologies offers significant potential for improved patient care and device management, particularly for individuals in remote areas. The untapped potential of emerging markets, with their growing aging populations and increasing healthcare investments, represents a vast opportunity for market expansion. Furthermore, the development of more affordable and user-friendly versions of advanced assistive technologies can unlock new consumer segments and drive widespread adoption. The growing focus on preventative healthcare and early intervention also creates opportunities for assistive devices that can aid in early detection and management of conditions.

Leading Players in the Vulnerable Groups Assistive Devices Market

- Sonova

- Demant

- WS Audiology

- GN ReSound

- Ottobock

- Invacare

- Enovis

- Starkey

- Ossur

- Rion

- Cochlear

- Sunrise Medical

- Permobil Corp

- MED-EL

- Pride Mobility

- Hoveround Corp

- Merits Health Products

- Drive Medical

- GF Health

- Vispero

Key Developments in Vulnerable Groups Assistive Devices Industry

- 2023/Q4: Launch of advanced AI-powered hearing aids by Sonova, offering enhanced speech clarity and personalized sound experiences.

- 2023/Q3: Demant expands its research and development in neuro-technology for advanced hearing implant solutions.

- 2023/Q2: WS Audiology announces strategic partnership with a technology firm to integrate IoT capabilities into its hearing care solutions.

- 2023/Q1: Ottobock introduces a new generation of lightweight, electric wheelchairs with extended battery life, enhancing user mobility.

- 2022/Q4: Invacare acquires a company specializing in adaptive seating solutions to broaden its mobility product portfolio.

- 2022/Q3: Starkey introduces a new line of hearing aids with advanced connectivity features for seamless integration with smart devices.

- 2022/Q2: Cochlear receives regulatory approval for a new cochlear implant system offering improved sound processing capabilities.

- 2022/Q1: Permobil Corp launches an innovative power assist device for manual wheelchairs, enhancing user independence.

- 2021/Q4: Pride Mobility expands its range of electric scooters with enhanced safety features and longer travel distances.

- 2021/Q3: MED-EL introduces a novel system for auditory brainstem implantation, addressing specific types of hearing loss.

Strategic Outlook for Vulnerable Groups Assistive Devices Market

The strategic outlook for the Vulnerable Groups Assistive Devices market is exceptionally positive, driven by sustained demographic trends and rapid technological innovation. Future growth will be fueled by the increasing adoption of smart, connected devices that offer personalized functionalities and seamless integration into users' lives. Companies that prioritize user-centric design, invest in AI and IoT capabilities, and focus on expanding their reach into emerging markets are best positioned for success. Strategic collaborations and acquisitions will continue to play a vital role in consolidating market positions and expanding product portfolios. Furthermore, a commitment to affordability and accessibility, coupled with effective distribution and after-sales support, will be crucial for capturing a larger share of this expanding global market. The ongoing focus on enhancing the quality of life and independence for vulnerable populations will remain the core catalyst for market expansion.

Vulnerable Groups Assistive Devices Segmentation

-

1. Application

- 1.1. Home Care Settings

- 1.2. Hospitals

- 1.3. Others

-

2. Type

- 2.1. Hearing Aids

- 2.2. Mobility Aids Devices

- 2.3. Vision & Reading Aids

- 2.4. Others

Vulnerable Groups Assistive Devices Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Vulnerable Groups Assistive Devices REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.6% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Vulnerable Groups Assistive Devices Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Home Care Settings

- 5.1.2. Hospitals

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Hearing Aids

- 5.2.2. Mobility Aids Devices

- 5.2.3. Vision & Reading Aids

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Vulnerable Groups Assistive Devices Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Home Care Settings

- 6.1.2. Hospitals

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Hearing Aids

- 6.2.2. Mobility Aids Devices

- 6.2.3. Vision & Reading Aids

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Vulnerable Groups Assistive Devices Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Home Care Settings

- 7.1.2. Hospitals

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Hearing Aids

- 7.2.2. Mobility Aids Devices

- 7.2.3. Vision & Reading Aids

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Vulnerable Groups Assistive Devices Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Home Care Settings

- 8.1.2. Hospitals

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Hearing Aids

- 8.2.2. Mobility Aids Devices

- 8.2.3. Vision & Reading Aids

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Vulnerable Groups Assistive Devices Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Home Care Settings

- 9.1.2. Hospitals

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Hearing Aids

- 9.2.2. Mobility Aids Devices

- 9.2.3. Vision & Reading Aids

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Vulnerable Groups Assistive Devices Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Home Care Settings

- 10.1.2. Hospitals

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Hearing Aids

- 10.2.2. Mobility Aids Devices

- 10.2.3. Vision & Reading Aids

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Sonova

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Demant

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 WS Audiology

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 GN ReSound

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Ottobock

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Invacare

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Enovis

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Starkey

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Ossur

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Rion

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Cochlear

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Sunrise Medical

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Permobil Corp

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 MED-EL

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Pride Mobility

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Hoveround Corp

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Merits Health Products

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Drive Medical

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 GF Health

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Vispero

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.1 Sonova

List of Figures

- Figure 1: Global Vulnerable Groups Assistive Devices Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Vulnerable Groups Assistive Devices Revenue (million), by Application 2024 & 2032

- Figure 3: North America Vulnerable Groups Assistive Devices Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Vulnerable Groups Assistive Devices Revenue (million), by Type 2024 & 2032

- Figure 5: North America Vulnerable Groups Assistive Devices Revenue Share (%), by Type 2024 & 2032

- Figure 6: North America Vulnerable Groups Assistive Devices Revenue (million), by Country 2024 & 2032

- Figure 7: North America Vulnerable Groups Assistive Devices Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Vulnerable Groups Assistive Devices Revenue (million), by Application 2024 & 2032

- Figure 9: South America Vulnerable Groups Assistive Devices Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Vulnerable Groups Assistive Devices Revenue (million), by Type 2024 & 2032

- Figure 11: South America Vulnerable Groups Assistive Devices Revenue Share (%), by Type 2024 & 2032

- Figure 12: South America Vulnerable Groups Assistive Devices Revenue (million), by Country 2024 & 2032

- Figure 13: South America Vulnerable Groups Assistive Devices Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Vulnerable Groups Assistive Devices Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Vulnerable Groups Assistive Devices Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Vulnerable Groups Assistive Devices Revenue (million), by Type 2024 & 2032

- Figure 17: Europe Vulnerable Groups Assistive Devices Revenue Share (%), by Type 2024 & 2032

- Figure 18: Europe Vulnerable Groups Assistive Devices Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Vulnerable Groups Assistive Devices Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Vulnerable Groups Assistive Devices Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Vulnerable Groups Assistive Devices Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Vulnerable Groups Assistive Devices Revenue (million), by Type 2024 & 2032

- Figure 23: Middle East & Africa Vulnerable Groups Assistive Devices Revenue Share (%), by Type 2024 & 2032

- Figure 24: Middle East & Africa Vulnerable Groups Assistive Devices Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Vulnerable Groups Assistive Devices Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Vulnerable Groups Assistive Devices Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Vulnerable Groups Assistive Devices Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Vulnerable Groups Assistive Devices Revenue (million), by Type 2024 & 2032

- Figure 29: Asia Pacific Vulnerable Groups Assistive Devices Revenue Share (%), by Type 2024 & 2032

- Figure 30: Asia Pacific Vulnerable Groups Assistive Devices Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Vulnerable Groups Assistive Devices Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Vulnerable Groups Assistive Devices Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Vulnerable Groups Assistive Devices Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Vulnerable Groups Assistive Devices Revenue million Forecast, by Type 2019 & 2032

- Table 4: Global Vulnerable Groups Assistive Devices Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Vulnerable Groups Assistive Devices Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Vulnerable Groups Assistive Devices Revenue million Forecast, by Type 2019 & 2032

- Table 7: Global Vulnerable Groups Assistive Devices Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Vulnerable Groups Assistive Devices Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Vulnerable Groups Assistive Devices Revenue million Forecast, by Type 2019 & 2032

- Table 13: Global Vulnerable Groups Assistive Devices Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Vulnerable Groups Assistive Devices Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Vulnerable Groups Assistive Devices Revenue million Forecast, by Type 2019 & 2032

- Table 19: Global Vulnerable Groups Assistive Devices Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Vulnerable Groups Assistive Devices Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Vulnerable Groups Assistive Devices Revenue million Forecast, by Type 2019 & 2032

- Table 31: Global Vulnerable Groups Assistive Devices Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Vulnerable Groups Assistive Devices Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Vulnerable Groups Assistive Devices Revenue million Forecast, by Type 2019 & 2032

- Table 40: Global Vulnerable Groups Assistive Devices Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Vulnerable Groups Assistive Devices Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Vulnerable Groups Assistive Devices?

The projected CAGR is approximately 6.6%.

2. Which companies are prominent players in the Vulnerable Groups Assistive Devices?

Key companies in the market include Sonova, Demant, WS Audiology, GN ReSound, Ottobock, Invacare, Enovis, Starkey, Ossur, Rion, Cochlear, Sunrise Medical, Permobil Corp, MED-EL, Pride Mobility, Hoveround Corp, Merits Health Products, Drive Medical, GF Health, Vispero.

3. What are the main segments of the Vulnerable Groups Assistive Devices?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 42570 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Vulnerable Groups Assistive Devices," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Vulnerable Groups Assistive Devices report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Vulnerable Groups Assistive Devices?

To stay informed about further developments, trends, and reports in the Vulnerable Groups Assistive Devices, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence