Key Insights

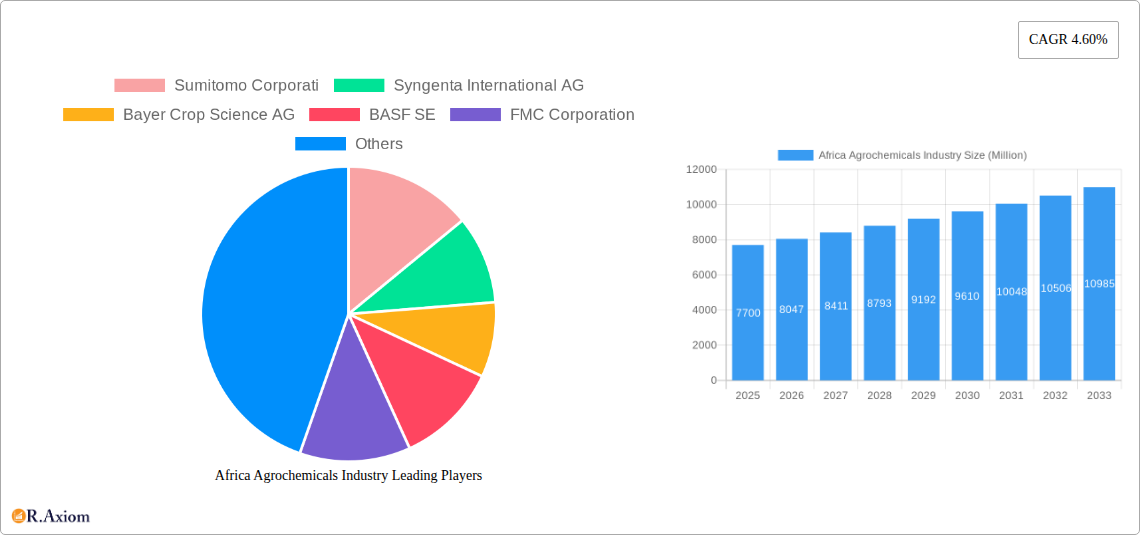

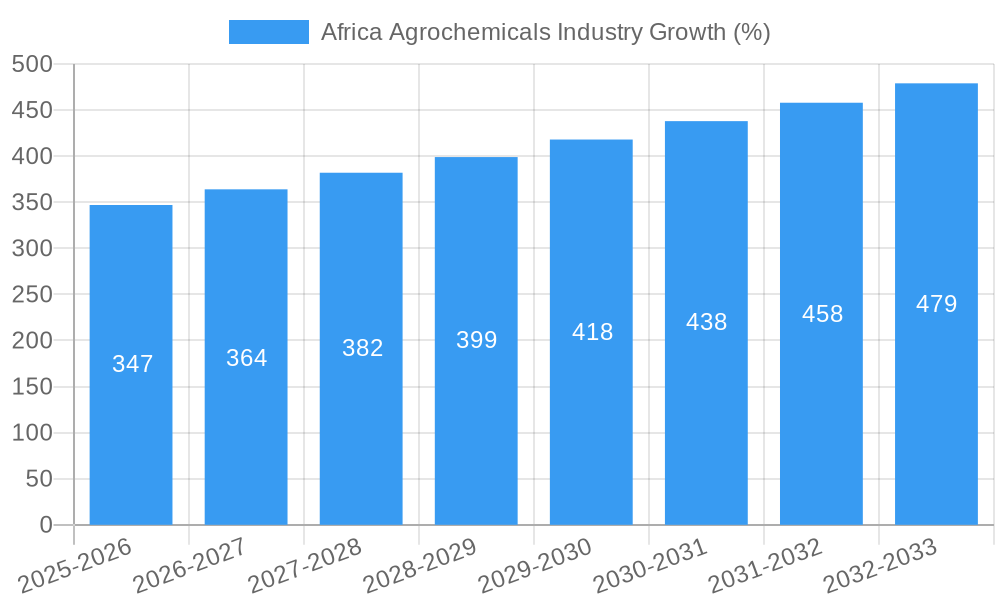

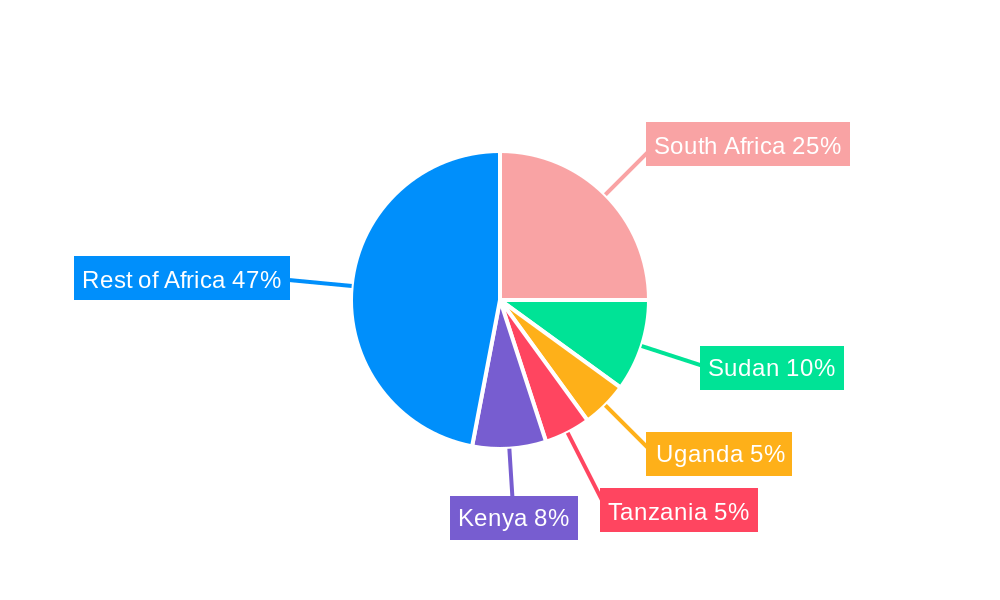

The African agrochemicals market, valued at $7.70 billion in 2025, is projected to experience robust growth, driven by factors such as increasing agricultural production to meet food security demands for a rapidly growing population, rising adoption of modern farming techniques, and government initiatives promoting agricultural development across the continent. The market's Compound Annual Growth Rate (CAGR) of 4.60% from 2025 to 2033 indicates a steady expansion, with significant potential for further acceleration. Key segments driving this growth include fertilizers, pesticides, and plant growth regulators, particularly within the grains and cereals, pulses and oilseeds, and fruits and vegetables application areas. The market is characterized by a mix of multinational corporations like Sumitomo, Syngenta, Bayer, BASF, FMC, Corteva, UPL, Yara, Nufar, and Adama, competing alongside local players. However, challenges such as limited access to credit and technology in certain regions, coupled with inconsistent infrastructure and climate variability, act as restraints to market expansion. Regional variations are substantial, with South Africa, Sudan, Uganda, Tanzania, and Kenya representing key markets within the diverse African landscape. Further growth is expected to be influenced by improvements in agricultural infrastructure, farmer education programs on best practices, and the increased availability of affordable and high-quality agrochemicals.

The forecast period (2025-2033) presents considerable opportunities for growth across the value chain, including manufacturing, distribution, and retail. Increased investment in research and development focused on developing climate-resilient crop varieties and sustainable agrochemical solutions will also stimulate market growth. Moreover, the adoption of precision agriculture techniques and digital technologies for improved farm management is likely to influence market dynamics positively. Competition is expected to intensify as companies strive to cater to the evolving needs of African farmers, focusing on product efficacy, affordability, and sustainable agricultural practices. Addressing issues of access, affordability, and environmental sustainability will be crucial for ensuring inclusive and responsible growth within the African agrochemicals market.

Africa Agrochemicals Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Africa agrochemicals industry, covering market size, growth drivers, challenges, opportunities, and key players. The report uses data from the historical period (2019-2024), the base year (2025), and projects market trends through the forecast period (2025-2033). The study period covers 2019-2033, offering a complete understanding of this dynamic market. This report is invaluable for industry stakeholders, investors, and anyone seeking to understand the complexities and potential of the African agrochemicals sector.

Africa Agrochemicals Industry Market Concentration & Innovation

The African agrochemicals market exhibits a moderately concentrated landscape, dominated by multinational corporations alongside several regional players. Market share is heavily influenced by product portfolio diversity, distribution networks, and regulatory compliance. While precise market share figures for individual companies vary across segments, key players like Sumitomo Corporation, Syngenta International AG, Bayer Crop Science AG, BASF SE, FMC Corporation, Corteva Agrisciences, UPL, Yara International, Nufar, and Adama Agricultural Solutions collectively account for a significant portion (estimated xx%) of the total market.

Innovation in the sector is driven by:

- Rising demand for higher-yielding crops: Leading to increased R&D in pest and disease control solutions.

- Growing adoption of precision agriculture: Demand for targeted agrochemical applications and data-driven solutions.

- Stringent regulations and environmental concerns: Driving the development of biopesticides and sustainable agricultural practices.

- Climate change adaptation: Necessitating the development of crop protection solutions resilient to changing weather patterns.

Mergers and acquisitions (M&A) are frequently observed, reflecting companies' strategies to expand market access, acquire new technologies, and diversify product portfolios. While precise deal values vary, recent years have witnessed significant M&A activity, with transaction values exceeding xx Million in several cases (Examples include Bayer's partnerships with M2i and Kimitec). This consolidation is expected to continue.

Africa Agrochemicals Industry Industry Trends & Insights

The African agrochemicals market is experiencing robust growth, driven primarily by a rapidly expanding agricultural sector, increasing food demand, and rising government investments in agricultural infrastructure and technology. The Compound Annual Growth Rate (CAGR) during the forecast period (2025-2033) is projected to be xx%, surpassing the global average. Market penetration of advanced agrochemicals remains relatively low, presenting significant opportunities for growth.

Key trends shaping the market include:

- Shift towards sustainable and bio-based agrochemicals: Growing awareness of environmental concerns is boosting the demand for biopesticides and other eco-friendly solutions. This trend, however, faces challenges related to efficacy and cost-effectiveness compared to conventional products.

- Technological advancements: Precision agriculture technologies such as drones and sensors are improving efficiency and reducing environmental impact. Digital solutions, including data analytics and farm management software, are increasingly adopted to improve decision making.

- Changing consumer preferences: Consumers are increasingly demanding higher quality, safer, and sustainably produced food. This drives demand for agrochemicals that ensure food safety and minimize environmental risks.

- Competitive landscape: The market is characterized by both multinational corporations and local players. Competition is intensifying, with companies focusing on product differentiation, innovation, and strategic partnerships to gain market share.

- Government policies and regulations: Government initiatives promoting agricultural development, investment in infrastructure, and regulations regarding agrochemical usage are significantly influencing the market trajectory. Subsidy programs can profoundly impact both market access and adoption rates of specific product types.

Dominant Markets & Segments in Africa Agrochemicals Industry

While the entire African continent presents opportunities, the Eastern and Southern African regions are currently dominant, driven by relatively developed agricultural sectors and substantial investments. Within countries, regions with established agricultural infrastructure and high crop production volumes witness higher agrochemical consumption.

Dominant Segments:

- Product Type: The Fertilizer Market and the Pesticides Market are currently the most significant segments, each accounting for approximately xx% and xx% of the total market, respectively. Growth in both sectors is driven by the increasing need for improved crop yields and efficient pest management. The Adjuvants Market and Plant Growth Regulators Market are witnessing notable growth due to increasing awareness of their benefits in optimizing crop production.

- Application: Grains and Cereals, Pulses and Oilseeds, and Fruits and Vegetables account for the largest shares of the application market, reflecting the significant importance of these crops in the region.

Key Drivers of Segment Dominance:

- Economic policies: Government support for agriculture, including subsidies and investment in infrastructure, plays a crucial role.

- Infrastructure: Availability of irrigation systems, storage facilities, and transportation networks strongly impacts market reach.

- Climate: Favorable climatic conditions for specific crops influence regional growth.

Africa Agrochemicals Industry Product Developments

Recent years have witnessed notable advancements, particularly in biopesticides and digital agriculture solutions. Companies are focusing on developing products that address specific crop needs, pest and disease pressures, and environmental concerns. The integration of digital technologies into agrochemical applications improves efficacy and reduces environmental impact. These new products and applications are tailored to suit specific agricultural practices and climatic conditions in different regions. Competitive advantage is determined by efficacy, cost-effectiveness, ease of use, and environmental compatibility.

Report Scope & Segmentation Analysis

This report comprehensively segments the Africa agrochemicals market across:

Product Type:

- Fertilizer Market: Growth is primarily driven by increasing demand for enhanced crop yields, driven by population growth and rising food demand. Market size is projected at xx Million in 2025.

- Pesticides Market: This segment is fuelled by increasing pest and disease pressure on crops and demand for efficient crop protection solutions. The market is anticipated to reach xx Million by 2025.

- Adjuvants Market: Growing awareness of their benefits in enhancing the efficacy of other agrochemicals drives this segment’s growth. The 2025 market size is estimated at xx Million.

- Plant Growth Regulators Market: The demand for optimized crop production and improved quality is propelling the growth of this segment, with a predicted market size of xx Million in 2025.

Application:

- Grains and Cereals: This remains a significant segment due to its substantial contribution to food security.

- Pulses and Oilseeds: The growing demand for these nutrient-rich crops is driving the growth of this segment.

- Fruits and Vegetables: The increasing focus on enhancing the quality and yields of these crops is impacting market dynamics.

- Commercial Crops: The growing demand for commercial crops such as cotton, coffee, and tea is contributing to the growth of this segment.

- Other Applications: This segment includes specialized applications in horticulture and other niche agricultural areas.

Each segment’s growth projection and competitive dynamics are thoroughly analyzed within the full report.

Key Drivers of Africa Agrochemicals Industry Growth

Several factors contribute to the industry’s robust growth. These include:

- Rising agricultural productivity: Increased demand for food and feed requires enhanced agricultural yields.

- Growing adoption of modern farming techniques: Precision agriculture and improved crop management practices drive the need for advanced agrochemicals.

- Favorable government policies: Government support for agricultural development stimulates investment and growth.

- Expanding agricultural land: The development of new arable land further fuels the demand for agrochemicals.

- Increasing investment in research and development: Innovation in agrochemical technology is leading to the development of more efficient and sustainable products.

Challenges in the Africa Agrochemicals Industry Sector

The industry faces several challenges, including:

- Inadequate infrastructure: Limited access to storage, transportation, and distribution networks hinders market penetration.

- Regulatory hurdles: Complex regulatory landscapes and varying pesticide registration requirements pose obstacles.

- Counterfeit products: The prevalence of counterfeit agrochemicals undermines market integrity and product quality.

- Climate change impact: Changing weather patterns affect crop yields and increase pest and disease pressure.

- Limited access to credit and financing: Smallholder farmers often lack access to credit, limiting their ability to purchase agrochemicals.

Emerging Opportunities in Africa Agrochemicals Industry

The African agrochemicals market presents several opportunities:

- Untapped market potential: A significant portion of the African market remains untapped, presenting substantial growth opportunities.

- Demand for sustainable solutions: Growing awareness of environmental concerns creates demand for eco-friendly agrochemicals.

- Technological advancements: The adoption of precision agriculture and digital technologies presents opportunities for innovation.

- Expanding middle class: The growing middle class increases demand for higher quality food, driving agrochemical consumption.

- Government initiatives: Government policies and programs supporting agricultural development present opportunities for investment.

Leading Players in the Africa Agrochemicals Industry Market

- Sumitomo Corporation

- Syngenta International AG

- Bayer Crop Science AG

- BASF SE

- FMC Corporation

- Corteva Agrisciences

- UPL

- Yara International

- Nufar

- Adama Agricultural Solutions

Key Developments in Africa Agrochemicals Industry Industry

- March 2022: Corteva Agrisciences launched Aubaine 518 SC herbicide in South Africa.

- February 2022: Bayer launched Flipper and Serenade crop protection products.

- February 2022: Bayer and Kimitec partnered for crop protection product development.

- January 2023: Bayer partnered with M2i Group for pheromone-based crop protection.

These developments highlight a shift towards sustainable and technologically advanced crop protection solutions.

Strategic Outlook for Africa Agrochemicals Industry Market

The African agrochemicals market is poised for significant growth, driven by increasing food demand, rising investments in agriculture, and technological advancements. The continued focus on sustainable solutions, coupled with supportive government policies and improving infrastructure, will fuel market expansion. Companies adopting innovative strategies, focusing on tailored product offerings, and embracing digital technologies will be best positioned to capitalize on this growth potential. The long-term outlook is exceptionally positive, reflecting the immense potential of the African agricultural sector.

Africa Agrochemicals Industry Segmentation

- 1. Production Analysis

- 2. Consumption Analysis

- 3. Import Market Analysis (Value & Volume)

- 4. Export Market Analysis (Value & Volume)

- 5. Price Trend Analysis

Africa Agrochemicals Industry Segmentation By Geography

-

1. Africa

- 1.1. Nigeria

- 1.2. South Africa

- 1.3. Egypt

- 1.4. Kenya

- 1.5. Ethiopia

- 1.6. Morocco

- 1.7. Ghana

- 1.8. Algeria

- 1.9. Tanzania

- 1.10. Ivory Coast

Africa Agrochemicals Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.60% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Adoption of Organic and Eco-friendly Farming Practices; Declining Area of Arable Land and Rising Food Security Concerns

- 3.3. Market Restrains

- 3.3.1. High Demand for Conventional and Synthetic Products; Lack of Awareness and Other Factors Limiting the Adoption of Agricultural Inoculants

- 3.4. Market Trends

- 3.4.1. Growing Food Demand Due to High Population Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Africa Agrochemicals Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 5.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 5.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 5.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 5.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. Africa

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 6. South Africa Africa Agrochemicals Industry Analysis, Insights and Forecast, 2019-2031

- 7. Sudan Africa Agrochemicals Industry Analysis, Insights and Forecast, 2019-2031

- 8. Uganda Africa Agrochemicals Industry Analysis, Insights and Forecast, 2019-2031

- 9. Tanzania Africa Agrochemicals Industry Analysis, Insights and Forecast, 2019-2031

- 10. Kenya Africa Agrochemicals Industry Analysis, Insights and Forecast, 2019-2031

- 11. Rest of Africa Africa Agrochemicals Industry Analysis, Insights and Forecast, 2019-2031

- 12. Competitive Analysis

- 12.1. Market Share Analysis 2024

- 12.2. Company Profiles

- 12.2.1 Sumitomo Corporati

- 12.2.1.1. Overview

- 12.2.1.2. Products

- 12.2.1.3. SWOT Analysis

- 12.2.1.4. Recent Developments

- 12.2.1.5. Financials (Based on Availability)

- 12.2.2 Syngenta International AG

- 12.2.2.1. Overview

- 12.2.2.2. Products

- 12.2.2.3. SWOT Analysis

- 12.2.2.4. Recent Developments

- 12.2.2.5. Financials (Based on Availability)

- 12.2.3 Bayer Crop Science AG

- 12.2.3.1. Overview

- 12.2.3.2. Products

- 12.2.3.3. SWOT Analysis

- 12.2.3.4. Recent Developments

- 12.2.3.5. Financials (Based on Availability)

- 12.2.4 BASF SE

- 12.2.4.1. Overview

- 12.2.4.2. Products

- 12.2.4.3. SWOT Analysis

- 12.2.4.4. Recent Developments

- 12.2.4.5. Financials (Based on Availability)

- 12.2.5 FMC Corporation

- 12.2.5.1. Overview

- 12.2.5.2. Products

- 12.2.5.3. SWOT Analysis

- 12.2.5.4. Recent Developments

- 12.2.5.5. Financials (Based on Availability)

- 12.2.6 Corteva Agrisciences

- 12.2.6.1. Overview

- 12.2.6.2. Products

- 12.2.6.3. SWOT Analysis

- 12.2.6.4. Recent Developments

- 12.2.6.5. Financials (Based on Availability)

- 12.2.7 UPL

- 12.2.7.1. Overview

- 12.2.7.2. Products

- 12.2.7.3. SWOT Analysis

- 12.2.7.4. Recent Developments

- 12.2.7.5. Financials (Based on Availability)

- 12.2.8 Yara International

- 12.2.8.1. Overview

- 12.2.8.2. Products

- 12.2.8.3. SWOT Analysis

- 12.2.8.4. Recent Developments

- 12.2.8.5. Financials (Based on Availability)

- 12.2.9 Nufar

- 12.2.9.1. Overview

- 12.2.9.2. Products

- 12.2.9.3. SWOT Analysis

- 12.2.9.4. Recent Developments

- 12.2.9.5. Financials (Based on Availability)

- 12.2.10 Adama Agricultural Solutions

- 12.2.10.1. Overview

- 12.2.10.2. Products

- 12.2.10.3. SWOT Analysis

- 12.2.10.4. Recent Developments

- 12.2.10.5. Financials (Based on Availability)

- 12.2.1 Sumitomo Corporati

List of Figures

- Figure 1: Africa Agrochemicals Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Africa Agrochemicals Industry Share (%) by Company 2024

List of Tables

- Table 1: Africa Agrochemicals Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Africa Agrochemicals Industry Revenue Million Forecast, by Production Analysis 2019 & 2032

- Table 3: Africa Agrochemicals Industry Revenue Million Forecast, by Consumption Analysis 2019 & 2032

- Table 4: Africa Agrochemicals Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2019 & 2032

- Table 5: Africa Agrochemicals Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2019 & 2032

- Table 6: Africa Agrochemicals Industry Revenue Million Forecast, by Price Trend Analysis 2019 & 2032

- Table 7: Africa Agrochemicals Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 8: Africa Agrochemicals Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 9: South Africa Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Sudan Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Uganda Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Tanzania Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Kenya Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Rest of Africa Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Africa Agrochemicals Industry Revenue Million Forecast, by Production Analysis 2019 & 2032

- Table 16: Africa Agrochemicals Industry Revenue Million Forecast, by Consumption Analysis 2019 & 2032

- Table 17: Africa Agrochemicals Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2019 & 2032

- Table 18: Africa Agrochemicals Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2019 & 2032

- Table 19: Africa Agrochemicals Industry Revenue Million Forecast, by Price Trend Analysis 2019 & 2032

- Table 20: Africa Agrochemicals Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 21: Nigeria Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: South Africa Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Egypt Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Kenya Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Ethiopia Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Morocco Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Ghana Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Algeria Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: Tanzania Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Ivory Coast Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Africa Agrochemicals Industry?

The projected CAGR is approximately 4.60%.

2. Which companies are prominent players in the Africa Agrochemicals Industry?

Key companies in the market include Sumitomo Corporati, Syngenta International AG, Bayer Crop Science AG, BASF SE, FMC Corporation, Corteva Agrisciences, UPL, Yara International, Nufar, Adama Agricultural Solutions.

3. What are the main segments of the Africa Agrochemicals Industry?

The market segments include Production Analysis, Consumption Analysis, Import Market Analysis (Value & Volume), Export Market Analysis (Value & Volume), Price Trend Analysis.

4. Can you provide details about the market size?

The market size is estimated to be USD 7.70 Million as of 2022.

5. What are some drivers contributing to market growth?

Adoption of Organic and Eco-friendly Farming Practices; Declining Area of Arable Land and Rising Food Security Concerns.

6. What are the notable trends driving market growth?

Growing Food Demand Due to High Population Growth.

7. Are there any restraints impacting market growth?

High Demand for Conventional and Synthetic Products; Lack of Awareness and Other Factors Limiting the Adoption of Agricultural Inoculants.

8. Can you provide examples of recent developments in the market?

January 2023: Bayer announced its Partnership with French company M2i Group which will provide Pheromone-based biological Crop Protection products. Bayer will integrate M2i's innovative press application technology into the product to form a digitally enabled solution.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Africa Agrochemicals Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Africa Agrochemicals Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Africa Agrochemicals Industry?

To stay informed about further developments, trends, and reports in the Africa Agrochemicals Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence