Key Insights

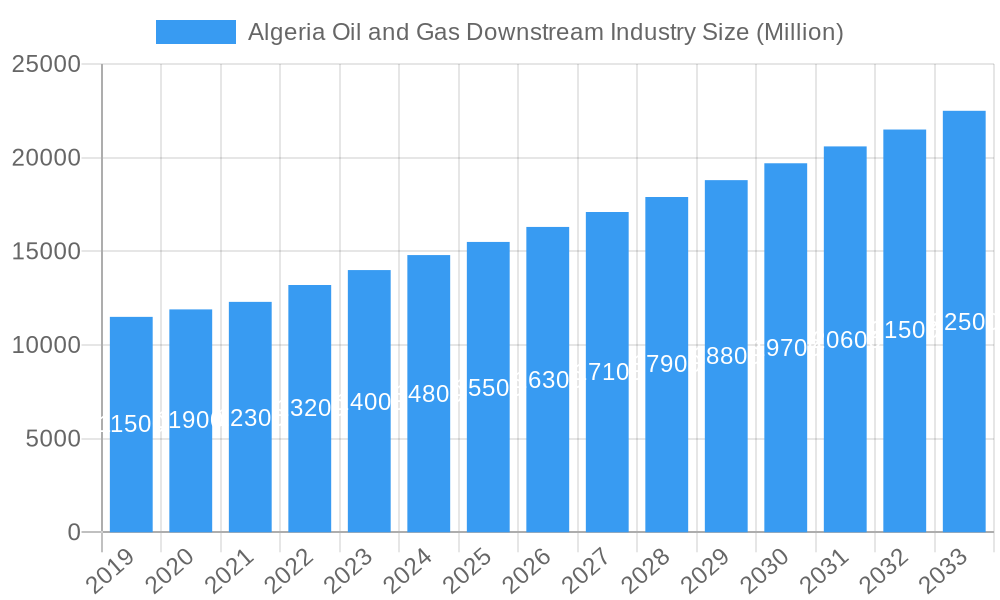

Algeria's Oil and Gas Downstream Industry is projected for significant expansion, fueled by escalating domestic energy consumption and strategic investments in refining and petrochemical infrastructure. The market, valued at $9.36 billion in the base year 2025, is anticipated to grow at a CAGR of 3.85%. This growth is propelled by Algeria's dedication to bolstering refining capacity, aiming to decrease reliance on imported refined products and enhance its export potential in value-added petrochemicals. Key initiatives focus on modernizing existing refineries and establishing new facilities to process greater volumes of crude oil and natural gas liquids into higher-margin products such as gasoline, diesel, jet fuel, lubricants, and petrochemical intermediates. Government policies designed to attract foreign direct investment and promote technological innovation are critical to this projected expansion.

Algeria Oil and Gas Downstream Industry Market Size (In Billion)

The downstream sector is central to Algeria's economic diversification strategy, extending beyond upstream exploration and production. Historical data from 2019-2024 shows a consistent upward trend. Future projections indicate the market will reach an estimated value by 2030 and further by the end of the forecast period in 2033. The increasing emphasis on developing a comprehensive petrochemical value chain, encompassing polymers, fertilizers, and specialty chemicals, will be a substantial driver of future market value. Additionally, the integration of renewable energy sources into oil and gas infrastructure will contribute to a more sustainable and resilient downstream sector, attracting further investment and ensuring long-term market health.

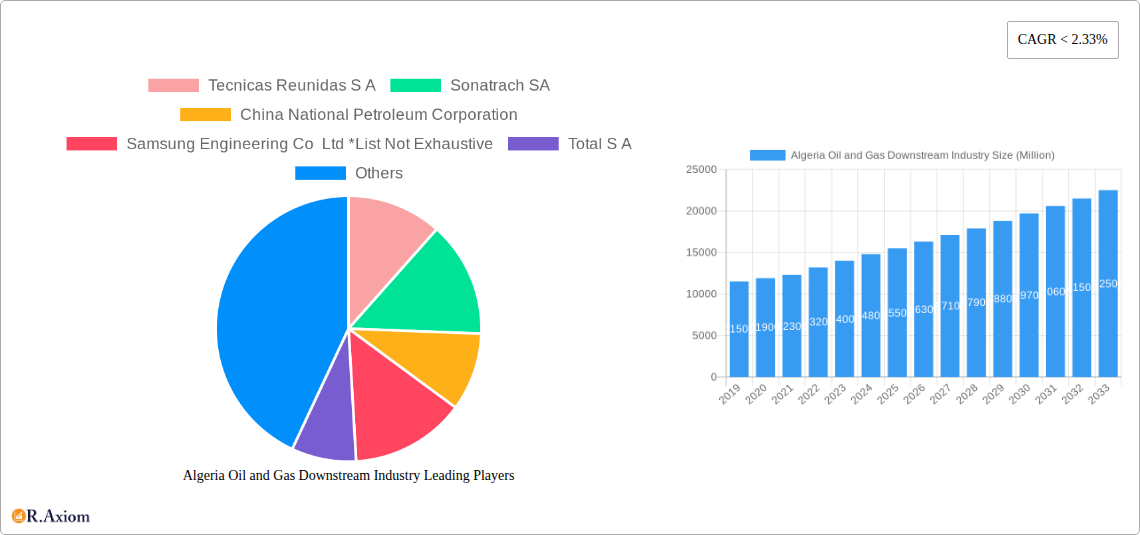

Algeria Oil and Gas Downstream Industry Company Market Share

Algeria Oil and Gas Downstream Industry Market Concentration & Innovation

This report provides a comprehensive analysis of the Algeria Oil and Gas Downstream Industry, focusing on market concentration, innovation drivers, and regulatory landscapes. The Algerian downstream sector, while dominated by state-owned Sonatrach SA, is witnessing increasing interest from international players like China National Petroleum Corporation and Samsung Engineering Co Ltd. This dynamic influences market concentration, with Sonatrach holding a significant market share of approximately 70% in refining operations. Innovation within the sector is driven by the need to enhance efficiency, reduce environmental impact, and meet growing domestic and international demand for refined products and petrochemicals. Key innovation areas include advanced refining technologies, the development of higher-value petrochemical derivatives, and the implementation of digital solutions for process optimization. Regulatory frameworks, primarily shaped by the Algerian government's energy policies, play a crucial role in attracting foreign investment and fostering sustainable growth. The presence of product substitutes, though limited in the immediate downstream oil and gas value chain, is considered in the context of alternative energy sources impacting long-term demand. End-user trends indicate a growing demand for cleaner fuels and specialized petrochemicals, prompting investments in upgrading existing infrastructure and developing new capacities. Merger and acquisition activities are relatively subdued but are anticipated to increase as the industry seeks consolidation and synergy. Estimated M&A deal values for significant downstream projects range from xx Million to xx Million.

Algeria Oil and Gas Downstream Industry Industry Trends & Insights

The Algeria Oil and Gas Downstream Industry is poised for significant expansion, driven by robust market growth drivers, anticipated technological disruptions, evolving consumer preferences, and intensifying competitive dynamics. The historical period from 2019 to 2024 saw steady growth, with an estimated Compound Annual Growth Rate (CAGR) of approximately 4.5%. This growth was primarily fueled by increasing domestic energy consumption, particularly for transportation fuels and a burgeoning petrochemical sector supplying raw materials for various industries. The base year of 2025 is projected to witness a market size of xx Billion, with a forecast period from 2025 to 2033 expected to maintain a healthy CAGR of 5.2%. This sustained growth will be propelled by substantial government investments in expanding refining capacities and developing integrated petrochemical complexes. Technological advancements are expected to play a pivotal role. The adoption of advanced catalytic processes, modular refining technologies, and digital transformation initiatives like AI-driven process control and predictive maintenance will enhance operational efficiency and product yields. These technological disruptions will also focus on sustainability, with increasing emphasis on reducing emissions and optimizing energy consumption throughout the downstream value chain. Consumer preferences are shifting towards higher-quality refined products, including low-sulfur fuels, and a wider range of petrochemical intermediates and finished products. This evolving demand necessitates a strategic shift towards higher-value-added products, moving beyond basic commodities. The competitive landscape is characterized by the dominance of Sonatrach SA, but the increasing participation of international players like China National Petroleum Corporation, Samsung Engineering Co Ltd, and Total S.A. is introducing a more dynamic and competitive environment. These players are bringing expertise, capital, and advanced technologies, driving innovation and pushing for greater operational excellence. Market penetration for advanced petrochemical products is expected to grow significantly as domestic manufacturing capabilities expand, reducing reliance on imports and fostering local industrial development. The overall trend indicates a move towards modernization, diversification, and value creation within Algeria's oil and gas downstream sector.

Dominant Markets & Segments in Algeria Oil and Gas Downstream Industry

The Algerian Oil and Gas Downstream Industry is characterized by the dominance of the Refineries: Overview segment, largely driven by the nation's strategic imperative to meet its substantial domestic fuel demand and contribute to export revenues. Within this segment, Existing Infrastructure forms the bedrock, with major refineries such as the Algiers Refinery and Arzew Refinery forming the backbone of the country's refining capacity. These facilities, while undergoing continuous upgrades, represent significant existing assets. However, the future dominance will be shaped by Projects in pipeline and Upcoming projects. Algeria has ambitious plans to expand its refining capacity to reduce reliance on imported refined products and to process a larger portion of its crude oil production domestically. These upcoming projects are critical for enhancing the country's refining sophistication, moving towards cleaner fuel production and maximizing the value extracted from each barrel of crude.

Parallel to refining, the Petrochemicals Plants: Overview segment is experiencing a surge in strategic importance and projected growth. While currently less dominant in terms of sheer capacity compared to refining, the Existing Infrastructure in petrochemicals, including facilities producing ethylene, propylene, and ammonia, is crucial for supporting downstream industries like plastics, fertilizers, and textiles. The real growth story for this segment lies in Projects in pipeline and Upcoming projects. Algeria aims to significantly diversify its petrochemical portfolio, moving into higher-value derivatives and specialty chemicals. These investments are driven by several key drivers:

- Economic Policies: The Algerian government's commitment to economic diversification away from crude oil exports is a primary catalyst. Developing a robust petrochemical industry is seen as a crucial avenue for job creation and industrial development.

- Infrastructure Development: Significant investments are being channeled into developing integrated industrial zones and enhancing logistics infrastructure to support the efficient operation of large-scale petrochemical complexes and their supply chains.

- Resource Abundance: Algeria's substantial natural gas reserves provide a cost-competitive feedstock for a wide range of petrochemical products, creating a strong competitive advantage.

- Growing Domestic and Regional Demand: The increasing demand for plastics, fertilizers, and other chemical-based products within Algeria and across the wider African continent presents a significant market opportunity.

The dominance of these segments will be further solidified by strategic investments in advanced technologies, the development of specialized product lines, and the integration of refining and petrochemical operations to create synergistic value chains. The forecast period is expected to witness substantial capacity additions and technological upgrades, positioning Algeria as a key player in the North African petrochemical market.

Algeria Oil and Gas Downstream Industry Product Developments

Product developments in Algeria's oil and gas downstream industry are increasingly focused on meeting evolving environmental standards and capturing higher market value. Significant advancements are being made in the production of cleaner fuels, such as ultra-low sulfur diesel (ULSD) and gasoline, to comply with stricter emission regulations and improve air quality. In the petrochemical sector, the emphasis is on developing a wider range of polymers, including specialized grades of polyethylene and polypropylene, to cater to the growing demand from the packaging, automotive, and construction industries. Furthermore, investments in ammonia and urea production are aimed at supporting the agricultural sector with enhanced fertilizer offerings. These product innovations offer competitive advantages by aligning with global sustainability trends and catering to specific end-user requirements.

Report Scope & Segmentation Analysis

This report meticulously analyzes the Algeria Oil and Gas Downstream Industry, segmenting the market into key operational areas. The primary focus is on Refineries: Overview, encompassing an analysis of the Existing Infrastructure, which provides insights into current operational capacities and technological sophistication of Algeria's refineries. It further details Projects in pipeline, outlining planned expansions and upgrades, and Upcoming projects, highlighting new refinery developments crucial for future market dynamics.

Concurrently, the report delves into Petrochemicals Plants: Overview. This includes an examination of Existing Infrastructure for petrochemical production, detailing current capacities and product ranges. It also provides detailed insights into Projects in pipeline and Upcoming projects within the petrochemical sector. These segments are analyzed for their respective market sizes, projected growth rates (CAGR), and the competitive dynamics shaping their future. The analysis aims to provide stakeholders with a granular understanding of opportunities and challenges within each critical downstream segment.

Key Drivers of Algeria Oil and Gas Downstream Industry Growth

The growth of Algeria's Oil and Gas Downstream Industry is propelled by a confluence of factors. Governmental Support and Investment: Algeria's national development plans prioritize the expansion and modernization of its downstream sector, attracting significant state-led investment and foreign direct investment through favorable policies. Increasing Domestic Demand: A growing population and expanding industrial base are driving higher consumption of refined fuels and petrochemical products. Resource Availability: Abundant crude oil and natural gas reserves provide a cost-effective feedstock for downstream operations, enhancing competitiveness. Technological Advancements: The adoption of modern refining and petrochemical technologies leads to improved efficiency, higher yields, and the production of higher-value products.

Challenges in the Algeria Oil and Gas Downstream Industry Sector

Despite its growth potential, the Algeria Oil and Gas Downstream Industry faces notable challenges. Aging Infrastructure: A significant portion of existing refining and petrochemical infrastructure requires substantial upgrades and modernization to meet international standards and improve efficiency. Regulatory Hurdles and Bureaucracy: Navigating complex regulatory frameworks and lengthy administrative processes can impede project execution and investment. Financing and Investment Gaps: Securing adequate long-term financing for large-scale downstream projects, especially in the current global economic climate, remains a persistent challenge. Skilled Workforce Shortage: A lack of adequately trained personnel in specialized downstream operations can impact operational efficiency and the adoption of new technologies.

Emerging Opportunities in Algeria Oil and Gas Downstream Industry

The Algerian Oil and Gas Downstream Industry is ripe with emerging opportunities. Petrochemical Diversification: Expanding into higher-value petrochemical derivatives, such as specialty polymers and advanced materials, presents significant growth potential and aligns with global market trends. Green Technologies and Sustainability: Investing in cleaner production methods, carbon capture technologies, and the development of biofuels or hydrogen production presents opportunities to align with global sustainability goals and create new revenue streams. Regional Market Expansion: Leveraging Algeria's strategic location, there are opportunities to export refined products and petrochemicals to underserved markets in Africa and Europe. Digital Transformation: Implementing advanced digital solutions, including AI, IoT, and Big Data analytics, can optimize operations, enhance predictive maintenance, and improve supply chain management.

Leading Players in the Algeria Oil and Gas Downstream Industry Market

- Sonatrach SA

- Tecnicas Reunidas S A

- China National Petroleum Corporation

- Samsung Engineering Co Ltd

- Total S A

Key Developments in Algeria Oil and Gas Downstream Industry Industry

- 2023: Sonatrach announces plans for a major expansion of its Arzew refinery to increase gasoline production capacity by 1 Million barrels per day.

- 2022: China National Petroleum Corporation signs a cooperation agreement with Sonatrach for potential investment in new petrochemical complexes.

- 2021: Samsung Engineering Co Ltd secures a contract for the engineering and construction of a new polypropylene plant in Skikda.

- 2020: Total S.A. expresses interest in participating in upcoming downstream infrastructure projects, focusing on refining upgrades and petrochemical ventures.

- 2019: The Algerian government approves several new projects aimed at increasing refining capacity by approximately 5 Million barrels per day by 2030.

Strategic Outlook for Algeria Oil and Gas Downstream Industry Market

The strategic outlook for Algeria's Oil and Gas Downstream Industry is exceptionally positive, characterized by a strong focus on modernization, diversification, and value creation. Continued investment in upgrading existing refineries and constructing new petrochemical facilities will be central to this strategy, aiming to meet escalating domestic demand and enhance export capabilities. The emphasis will shift towards producing higher-value products, including specialized petrochemicals and cleaner fuels, driven by both market demand and stringent environmental regulations. Collaborations with international players are anticipated to bring in advanced technologies and capital, fostering innovation and operational excellence. The industry is poised to become a significant driver of economic diversification, job creation, and industrial growth for Algeria.

Algeria Oil and Gas Downstream Industry Segmentation

-

1. Refineries

-

1.1. Overview

- 1.1.1. Existing Infrastructure

- 1.1.2. Projects in pipeline

- 1.1.3. Upcoming projects

-

1.1. Overview

-

2. Petrochemicals Plants

-

2.1. Overview

- 2.1.1. Existing Infrastructure

- 2.1.2. Projects in pipeline

- 2.1.3. Upcoming projects

-

2.1. Overview

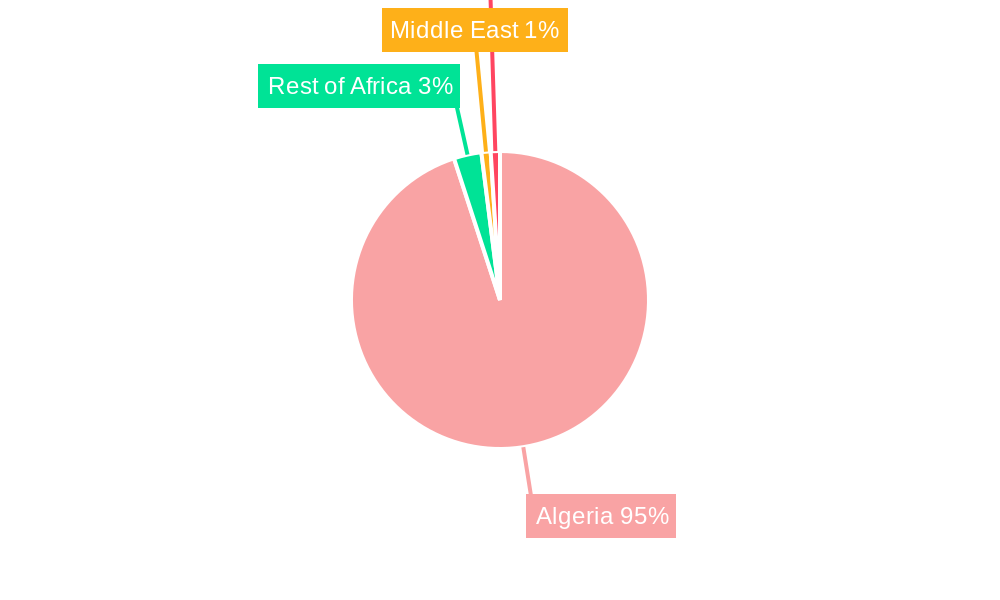

Algeria Oil and Gas Downstream Industry Segmentation By Geography

- 1. Algeria

Algeria Oil and Gas Downstream Industry Regional Market Share

Geographic Coverage of Algeria Oil and Gas Downstream Industry

Algeria Oil and Gas Downstream Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.85% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Refineries

- 5.1.1. Overview

- 5.1.1.1. Existing Infrastructure

- 5.1.1.2. Projects in pipeline

- 5.1.1.3. Upcoming projects

- 5.1.1. Overview

- 5.2. Market Analysis, Insights and Forecast - by Petrochemicals Plants

- 5.2.1. Overview

- 5.2.1.1. Existing Infrastructure

- 5.2.1.2. Projects in pipeline

- 5.2.1.3. Upcoming projects

- 5.2.1. Overview

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Algeria

- 5.1. Market Analysis, Insights and Forecast - by Refineries

- 6. Algeria Oil and Gas Downstream Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Refineries

- 6.1.1. Overview

- 6.1.1.1. Existing Infrastructure

- 6.1.1.2. Projects in pipeline

- 6.1.1.3. Upcoming projects

- 6.1.1. Overview

- 6.2. Market Analysis, Insights and Forecast - by Petrochemicals Plants

- 6.2.1. Overview

- 6.2.1.1. Existing Infrastructure

- 6.2.1.2. Projects in pipeline

- 6.2.1.3. Upcoming projects

- 6.2.1. Overview

- 6.1. Market Analysis, Insights and Forecast - by Refineries

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Tecnicas Reunidas S A

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Sonatrach SA

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 China National Petroleum Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Samsung Engineering Co Ltd *List Not Exhaustive

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Total S A

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.1 Tecnicas Reunidas S A

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Algeria Oil and Gas Downstream Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Algeria Oil and Gas Downstream Industry Share (%) by Company 2025

List of Tables

- Table 1: Algeria Oil and Gas Downstream Industry Revenue billion Forecast, by Refineries 2020 & 2033

- Table 2: Algeria Oil and Gas Downstream Industry Revenue billion Forecast, by Petrochemicals Plants 2020 & 2033

- Table 3: Algeria Oil and Gas Downstream Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Algeria Oil and Gas Downstream Industry Revenue billion Forecast, by Refineries 2020 & 2033

- Table 5: Algeria Oil and Gas Downstream Industry Revenue billion Forecast, by Petrochemicals Plants 2020 & 2033

- Table 6: Algeria Oil and Gas Downstream Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Algeria Oil and Gas Downstream Industry?

The projected CAGR is approximately 3.85%.

2. Which companies are prominent players in the Algeria Oil and Gas Downstream Industry?

Key companies in the market include Tecnicas Reunidas S A, Sonatrach SA, China National Petroleum Corporation, Samsung Engineering Co Ltd *List Not Exhaustive, Total S A.

3. What are the main segments of the Algeria Oil and Gas Downstream Industry?

The market segments include Refineries, Petrochemicals Plants.

4. Can you provide details about the market size?

The market size is estimated to be USD 9.36 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Demand for Clean Energy Sources4.; Supportive Government Policies.

6. What are the notable trends driving market growth?

Refining Capacity to Witness Growth.

7. Are there any restraints impacting market growth?

4.; Increasing Adoption of Other Alternative Clean Energy Sources.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Algeria Oil and Gas Downstream Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Algeria Oil and Gas Downstream Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Algeria Oil and Gas Downstream Industry?

To stay informed about further developments, trends, and reports in the Algeria Oil and Gas Downstream Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence