Key Insights

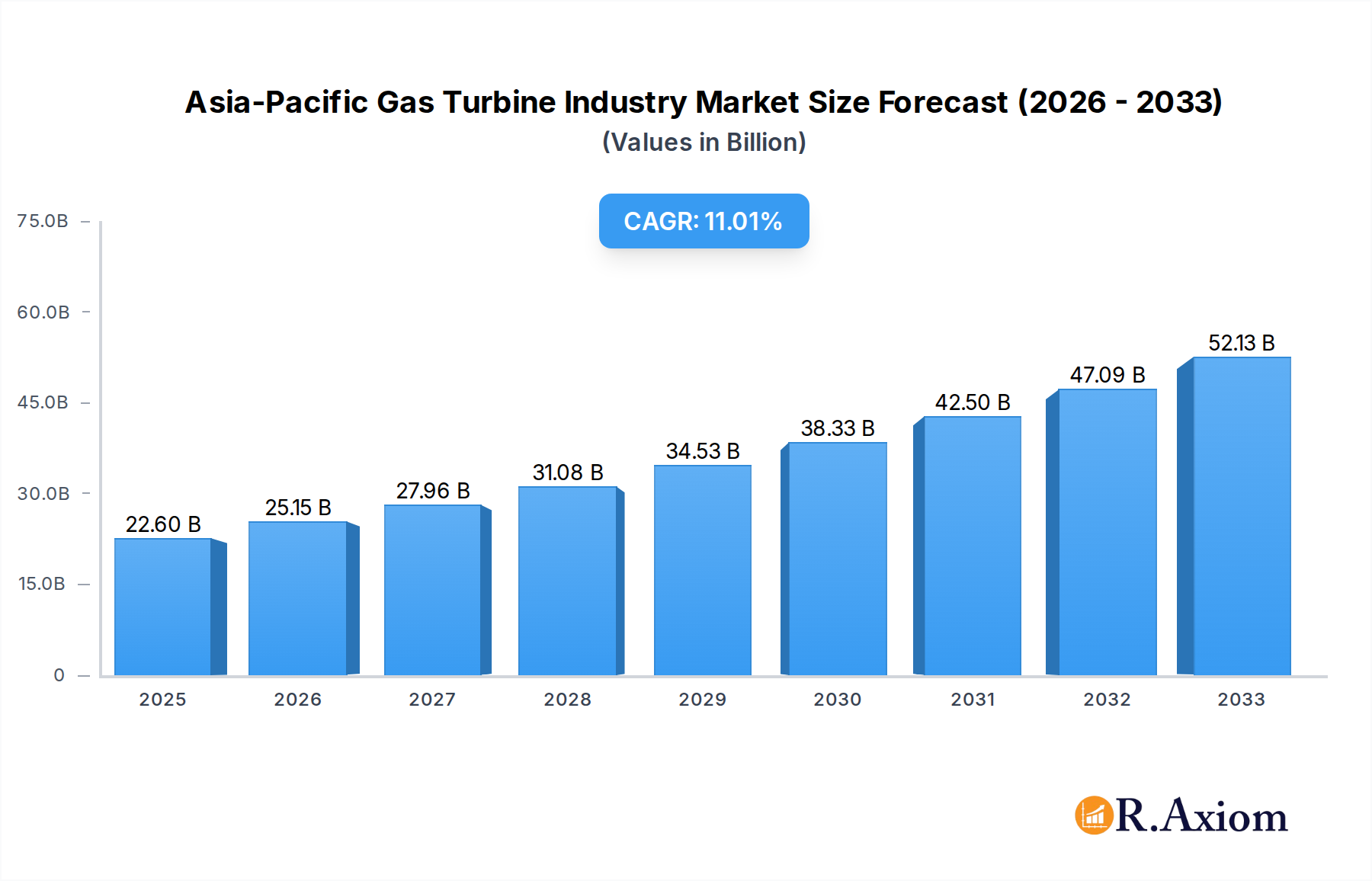

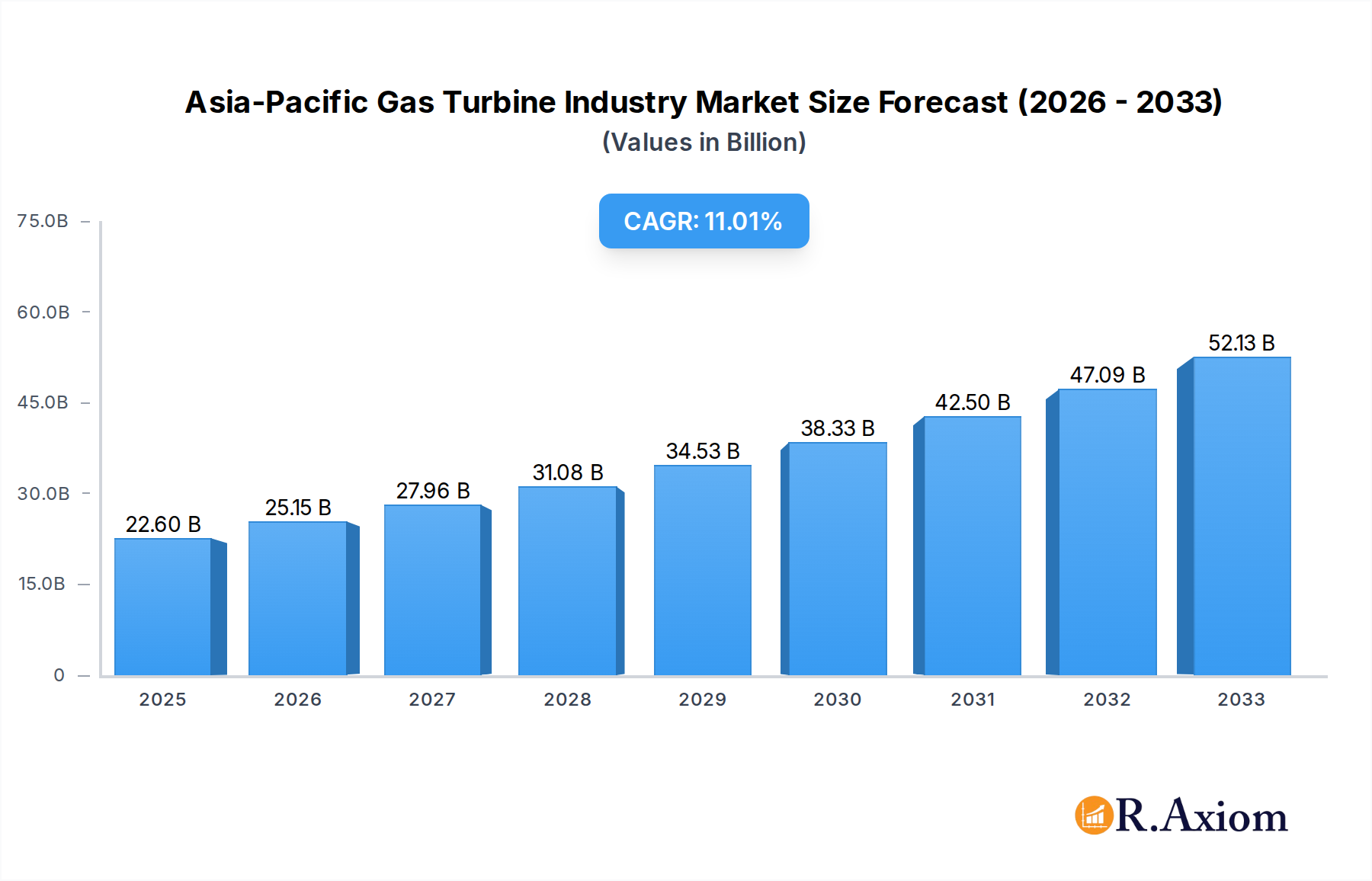

The Asia-Pacific Gas Turbine Industry is poised for significant expansion, with a projected market size of USD 22.6 billion in 2025, driven by a robust Compound Annual Growth Rate (CAGR) of 11.2% during the forecast period of 2025-2033. This impressive growth is primarily fueled by escalating energy demands across the region, particularly in rapidly developing economies like China and India. The increasing focus on cleaner energy alternatives and the need to upgrade aging power infrastructure are also key contributors. Furthermore, the oil and gas sector's continued exploration and production activities, coupled with the growing adoption of gas turbines in industrial applications beyond power generation, present substantial growth opportunities. The market segmentation reveals a strong presence in the 'Above 120 MW' capacity segment, indicating a demand for larger, more efficient turbines for utility-scale power plants. Combined Cycle turbines are dominant due to their superior efficiency, while Open Cycle turbines find application in peak demand scenarios and specific industrial processes.

Asia-Pacific Gas Turbine Industry Market Size (In Billion)

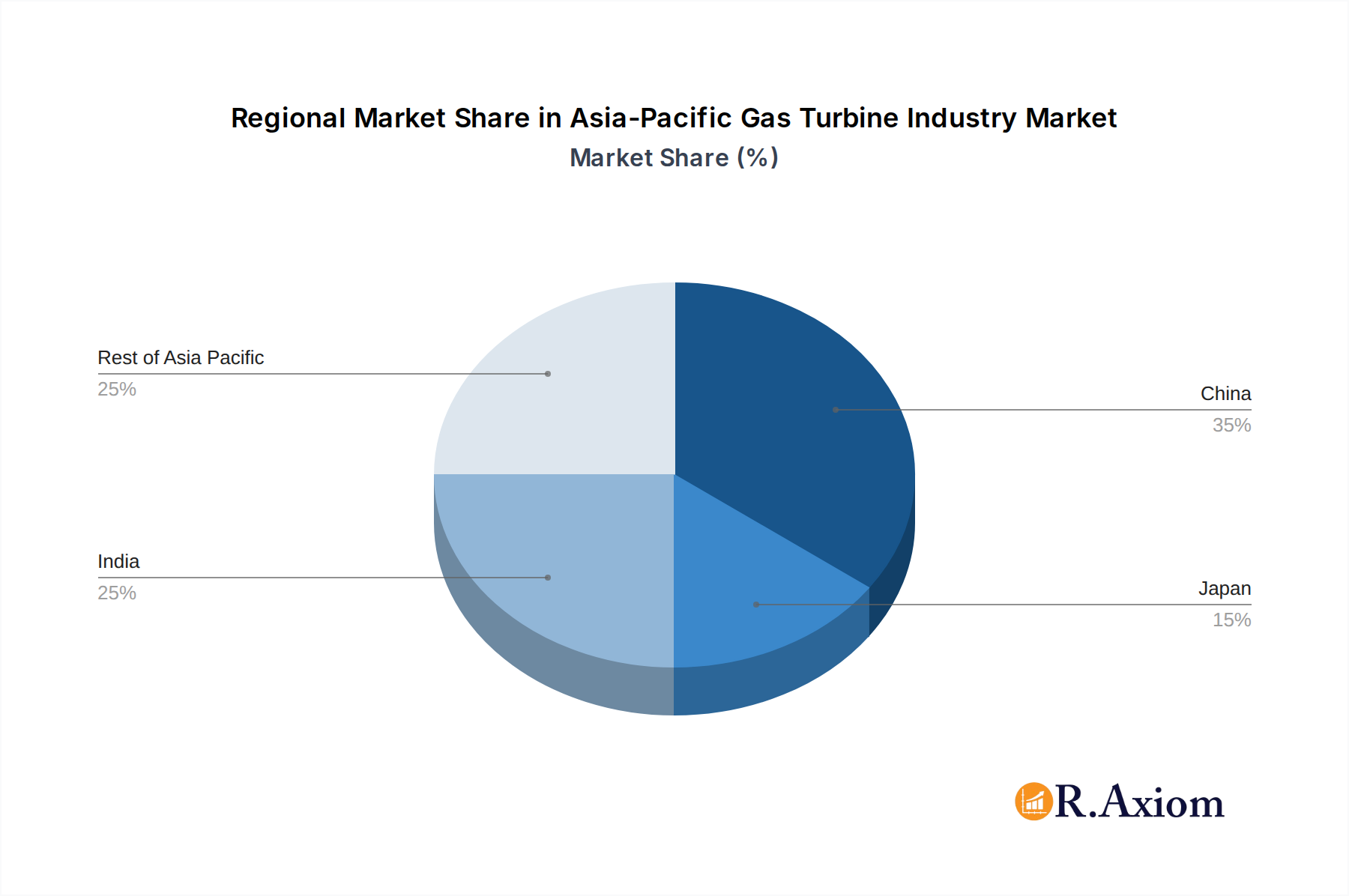

Geographically, China stands out as the largest market, owing to its extensive industrial base and ambitious renewable energy targets that often integrate gas turbines as baseload or backup power. India's rapidly growing economy and its emphasis on improving power generation capacity also make it a crucial market. Japan, while a mature market, continues to invest in advanced gas turbine technologies for its existing infrastructure and for potential integration with emerging energy solutions. The "Rest of Asia-Pacific" region, encompassing countries like South Korea, Indonesia, and Vietnam, is also expected to witness substantial growth due to increasing industrialization and urbanization. While the market benefits from strong demand drivers, potential restraints could include stringent environmental regulations, price volatility of natural gas, and the upfront capital investment required for gas turbine installations. However, the overarching trend towards decarbonization and enhanced energy security is expected to outweigh these challenges, ensuring a dynamic and expanding market landscape.

Asia-Pacific Gas Turbine Industry Company Market Share

Here is an SEO-optimized, detailed report description for the Asia-Pacific Gas Turbine Industry, incorporating high-traffic keywords and structured as requested.

Asia-Pacific Gas Turbine Industry Market Concentration & Innovation

The Asia-Pacific gas turbine market is characterized by a blend of established global players and burgeoning regional manufacturers, leading to a moderately concentrated industry landscape. Innovation is primarily driven by the escalating demand for efficient power generation, the growing adoption of renewable energy integration, and stringent environmental regulations necessitating lower emissions. Key innovation areas include advancements in hydrogen co-firing capabilities, enhanced thermal efficiency, and the development of smaller, modular gas turbine units for distributed power generation. The regulatory frameworks across China, India, Japan, and the Rest of Asia-Pacific are evolving, with a focus on decarbonization targets and energy security, influencing technology adoption and investment. Product substitutes, such as advanced solar photovoltaic (PV) and wind power solutions, are gaining traction, particularly for new capacity additions, though gas turbines remain crucial for grid stability and baseload power. End-user trends reveal a strong preference for combined-cycle gas turbines (CCGT) due to their superior efficiency in large-scale power generation and increasing interest in open-cycle turbines for peaking power and industrial applications. Mergers and acquisitions (M&A) activities, while not as frequent as in other sectors, are strategic moves by major players to consolidate market share, acquire innovative technologies, or expand geographical reach. Deal values in M&A are anticipated to increase as companies seek synergistic growth. Market share is currently dominated by a few key players, with ongoing efforts to gain a competitive edge through technological superiority and cost-effectiveness.

Asia-Pacific Gas Turbine Industry Industry Trends & Insights

The Asia-Pacific gas turbine industry is poised for substantial growth, fueled by robust economic expansion, rapid urbanization, and an increasing need for reliable and efficient power generation across the region. A significant CAGR is projected over the forecast period of 2025–2033, driven by the continuous expansion of power infrastructure to meet rising energy demands from industrial, commercial, and residential sectors. Technological disruptions are playing a pivotal role, with a growing emphasis on the integration of hydrogen and other renewable fuels into gas turbine operations to achieve lower carbon footprints. This trend is directly responding to evolving consumer preferences for cleaner energy solutions and governmental mandates aimed at reducing greenhouse gas emissions. The competitive dynamics within the market are intensifying, with leading companies investing heavily in research and development to enhance turbine efficiency, reduce operational costs, and develop solutions for a low-carbon future. Market penetration of advanced gas turbine technologies, particularly those capable of flexible operation and fuel diversification, is expected to surge. The ongoing digital transformation is also influencing the sector, with the adoption of AI-powered predictive maintenance and remote monitoring systems becoming a standard to optimize turbine performance and minimize downtime. Furthermore, the shift towards distributed power generation and microgrids is creating new market opportunities for smaller-capacity gas turbines, catering to the specific needs of industrial facilities and remote communities. The strategic importance of energy security and the desire to reduce reliance on imported fossil fuels are also significant drivers underpinning the sustained demand for domestic gas turbine manufacturing and deployment. The report will delve deep into these intricate trends, providing granular insights into market penetration rates, the impact of technological advancements on market share, and the evolving landscape of consumer and industrial demand.

Dominant Markets & Segments in Asia-Pacific Gas Turbine Industry

China stands out as the dominant market within the Asia-Pacific gas turbine industry, driven by its immense industrial base, rapid urbanization, and substantial government investments in energy infrastructure. The country's commitment to cleaner energy sources and its ambitious carbon neutrality goals are accelerating the adoption of advanced gas turbine technologies, particularly for replacing older, less efficient coal-fired power plants. India follows closely as a key growth engine, propelled by its expanding economy, increasing power demand, and ongoing efforts to enhance its power generation capacity. The Indian government's focus on energy security and the 'Make in India' initiative further bolster the domestic gas turbine market. Japan, a pioneer in advanced technology, continues to be a significant market, focusing on highly efficient, low-emission gas turbines, including those designed for hydrogen-fueled power generation.

- Capacity Segment Dominance: The 31-120 MW capacity segment is experiencing robust growth, catering to the needs of medium-sized power plants and industrial co-generation facilities. However, the Above 120 MW segment remains critical for large-scale baseload power generation, with significant demand from national grids. The Less than 30 MW segment is gaining traction due to the rise of distributed power generation and captive power solutions for industrial clients seeking energy independence.

- Type Segment Dominance: Combined Cycle turbines dominate the market due to their superior energy efficiency, making them the preferred choice for large-scale power generation. The demand for Open Cycle turbines is growing for peaking power applications and in industries requiring rapid power ramp-up capabilities.

- Application Segment Dominance: The Power sector is the primary driver, accounting for the largest share of gas turbine installations, supporting both grid power and captive power needs. The Oil and Gas sector also represents a substantial segment, with gas turbines used for power generation in upstream, midstream, and downstream operations, as well as for mechanical drive applications. Other Industries, including manufacturing and heavy industry, are increasingly adopting gas turbines for their operational power requirements.

- Geography Segment Dominance: China leads in market share due to its sheer scale of energy demand and production. India is projected to witness the fastest growth rate, driven by its massive power deficit and ambitious expansion plans. The Rest of Asia-Pacific, encompassing nations like South Korea, Australia, and Southeast Asian countries, contributes significantly through its diverse energy needs and adoption of advanced technologies.

Asia-Pacific Gas Turbine Industry Product Developments

Product development in the Asia-Pacific gas turbine industry is heavily focused on enhancing efficiency, reducing emissions, and enabling fuel flexibility. Key innovations include the advancement of turbines capable of significant hydrogen co-firing, crucial for meeting decarbonization targets. Manufacturers are also pushing the boundaries of thermal efficiency in both combined and open-cycle configurations. The development of modular and smaller-capacity units is enabling greater deployment flexibility for distributed power and industrial applications. These technological advancements provide a competitive advantage by addressing evolving regulatory landscapes and customer demands for sustainable and cost-effective energy solutions.

Report Scope & Segmentation Analysis

This report meticulously analyzes the Asia-Pacific Gas Turbine Industry, segmenting the market by capacity, type, application, and geography.

- Capacity: The market is segmented into Less than 30 MW, 31-120 MW, and Above 120 MW. Each segment's growth is influenced by evolving power needs, industrial requirements, and the scale of power projects.

- Type: Segmentation includes Combined Cycle and Open Cycle gas turbines, reflecting their distinct applications in baseload, peaking, and industrial power generation.

- Application: The analysis covers Power generation, Oil and Gas operations, and Other Industries, highlighting the diverse end-use sectors driving demand.

- Geography: The report provides detailed insights into China, Japan, India, and the Rest of Asia-Pacific, examining regional market dynamics, regulatory influences, and growth potential. Projections for market size and competitive landscapes within each segment are provided.

Key Drivers of Asia-Pacific Gas Turbine Industry Growth

The Asia-Pacific gas turbine industry's growth is primarily propelled by the escalating demand for electricity across rapidly developing economies. Urbanization and industrial expansion necessitate significant investments in new power generation capacity. Furthermore, the global push towards cleaner energy solutions is a major driver, encouraging the adoption of gas turbines as a transitional fuel source, especially those capable of hydrogen co-firing, to meet ambitious decarbonization goals. Favorable government policies, including subsidies for clean energy and incentives for domestic manufacturing, also play a crucial role in stimulating market growth.

Challenges in the Asia-Pacific Gas Turbine Industry Sector

Despite robust growth prospects, the Asia-Pacific gas turbine industry faces several challenges. Fluctuations in natural gas prices and availability can impact operational costs and project economics. Stringent environmental regulations, while driving innovation, also impose compliance costs and can lead to project delays. Intense competition from other power generation technologies, such as solar and wind, particularly for new capacity, poses a continuous threat. Furthermore, supply chain disruptions and geopolitical uncertainties can affect the timely delivery of components and raw materials, impacting project timelines and overall market stability.

Emerging Opportunities in Asia-Pacific Gas Turbine Industry

Emerging opportunities within the Asia-Pacific gas turbine sector are largely centered around the transition to a low-carbon economy. The increasing interest in hydrogen as a fuel source presents a significant opportunity for turbines equipped for hydrogen co-firing or 100% hydrogen operation. The growing trend of distributed power generation and microgrids offers scope for smaller, more flexible gas turbine units. Furthermore, the demand for repowering older, inefficient thermal power plants with modern gas turbine technology to improve efficiency and reduce emissions opens up substantial market potential.

Leading Players in the Asia-Pacific Gas Turbine Industry Market

- Opra Turbines BV

- Ansaldo Gas Turbine Technology Co Ltd

- Harbin Electric Co Ltd

- Bharat Heavy Electricals Limited

- Siemens AG

- General Electric Company

- Kawasaki Heavy Industries Ltd

- Capstone Turbine Corporation

- Mitsubishi Heavy Industries Ltd

Key Developments in Asia-Pacific Gas Turbine Industry Industry

- November 2022: Wärtsilä was awarded a contract to supply a gas-fueled 15.5 MW captive power plant under an engineering, procurement, and construction (EPC) contract along with a five-year Operation & Maintenance (O&M) agreement in Chennai, Tamilnadu, India. The order has been placed by Tamilnadu Petroproducts Limited (TPL), the world's leading manufacturer of linear alkyl benzene (LAB), a subsidiary of AM International, Singapore.

- October 2022: National Thermal Power Corporation (NTPC) and GE Gas Power signed a Memorandum of Understanding (MoU) to investigate the feasibility of combining hydrogen (H2) with natural gas in GE's 9E gas turbines installed at NTPC's Kawas combined-cycle gas power plant in Gujarat, India.

Strategic Outlook for Asia-Pacific Gas Turbine Industry Market

The strategic outlook for the Asia-Pacific gas turbine industry remains highly positive, driven by the region's sustained economic growth and the critical need for reliable energy solutions. The increasing focus on decarbonization presents a significant opportunity for the adoption of advanced gas turbine technologies that can integrate with renewable energy sources and utilize cleaner fuels like hydrogen. Investments in upgrading existing power infrastructure and the development of new, highly efficient power plants will continue to fuel demand. Companies that can offer innovative, cost-effective, and environmentally compliant solutions are well-positioned for sustained success in this dynamic market.

Asia-Pacific Gas Turbine Industry Segmentation

-

1. Capacity

- 1.1. Less than 30 MW

- 1.2. 31-120 MW

- 1.3. Above 120 MW

-

2. Type

- 2.1. Combined Cycle

- 2.2. Open Cycle

-

3. Application

- 3.1. Power

- 3.2. Oil and Gas

- 3.3. Other Industries

-

4. Geography

- 4.1. China

- 4.2. Japan

- 4.3. India

- 4.4. Rest of Asia-Pacific

Asia-Pacific Gas Turbine Industry Segmentation By Geography

- 1. China

- 2. Japan

- 3. India

- 4. Rest of Asia Pacific

Asia-Pacific Gas Turbine Industry Regional Market Share

Geographic Coverage of Asia-Pacific Gas Turbine Industry

Asia-Pacific Gas Turbine Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Capacity

- 5.1.1. Less than 30 MW

- 5.1.2. 31-120 MW

- 5.1.3. Above 120 MW

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Combined Cycle

- 5.2.2. Open Cycle

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Power

- 5.3.2. Oil and Gas

- 5.3.3. Other Industries

- 5.4. Market Analysis, Insights and Forecast - by Geography

- 5.4.1. China

- 5.4.2. Japan

- 5.4.3. India

- 5.4.4. Rest of Asia-Pacific

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. China

- 5.5.2. Japan

- 5.5.3. India

- 5.5.4. Rest of Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Capacity

- 6. Asia-Pacific Gas Turbine Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Capacity

- 6.1.1. Less than 30 MW

- 6.1.2. 31-120 MW

- 6.1.3. Above 120 MW

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Combined Cycle

- 6.2.2. Open Cycle

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Power

- 6.3.2. Oil and Gas

- 6.3.3. Other Industries

- 6.4. Market Analysis, Insights and Forecast - by Geography

- 6.4.1. China

- 6.4.2. Japan

- 6.4.3. India

- 6.4.4. Rest of Asia-Pacific

- 6.1. Market Analysis, Insights and Forecast - by Capacity

- 7. China Asia-Pacific Gas Turbine Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Capacity

- 7.1.1. Less than 30 MW

- 7.1.2. 31-120 MW

- 7.1.3. Above 120 MW

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Combined Cycle

- 7.2.2. Open Cycle

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Power

- 7.3.2. Oil and Gas

- 7.3.3. Other Industries

- 7.4. Market Analysis, Insights and Forecast - by Geography

- 7.4.1. China

- 7.4.2. Japan

- 7.4.3. India

- 7.4.4. Rest of Asia-Pacific

- 7.1. Market Analysis, Insights and Forecast - by Capacity

- 8. Japan Asia-Pacific Gas Turbine Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Capacity

- 8.1.1. Less than 30 MW

- 8.1.2. 31-120 MW

- 8.1.3. Above 120 MW

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Combined Cycle

- 8.2.2. Open Cycle

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Power

- 8.3.2. Oil and Gas

- 8.3.3. Other Industries

- 8.4. Market Analysis, Insights and Forecast - by Geography

- 8.4.1. China

- 8.4.2. Japan

- 8.4.3. India

- 8.4.4. Rest of Asia-Pacific

- 8.1. Market Analysis, Insights and Forecast - by Capacity

- 9. India Asia-Pacific Gas Turbine Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Capacity

- 9.1.1. Less than 30 MW

- 9.1.2. 31-120 MW

- 9.1.3. Above 120 MW

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Combined Cycle

- 9.2.2. Open Cycle

- 9.3. Market Analysis, Insights and Forecast - by Application

- 9.3.1. Power

- 9.3.2. Oil and Gas

- 9.3.3. Other Industries

- 9.4. Market Analysis, Insights and Forecast - by Geography

- 9.4.1. China

- 9.4.2. Japan

- 9.4.3. India

- 9.4.4. Rest of Asia-Pacific

- 9.1. Market Analysis, Insights and Forecast - by Capacity

- 10. Rest of Asia Pacific Asia-Pacific Gas Turbine Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Capacity

- 10.1.1. Less than 30 MW

- 10.1.2. 31-120 MW

- 10.1.3. Above 120 MW

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Combined Cycle

- 10.2.2. Open Cycle

- 10.3. Market Analysis, Insights and Forecast - by Application

- 10.3.1. Power

- 10.3.2. Oil and Gas

- 10.3.3. Other Industries

- 10.4. Market Analysis, Insights and Forecast - by Geography

- 10.4.1. China

- 10.4.2. Japan

- 10.4.3. India

- 10.4.4. Rest of Asia-Pacific

- 10.1. Market Analysis, Insights and Forecast - by Capacity

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Opra Turbines BV

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Ansaldo Gas Turbine Technology Co Ltd

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Harbin Electric Co Ltd

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Bharat Heavy Electricals Limited

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Siemens AG

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 General Electric Company

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Kawasaki Heavy Industries Ltd

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Capstone Turbine Corporation*List Not Exhaustive

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Mitsubishi Heavy Industries Ltd

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.1 Opra Turbines BV

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Asia-Pacific Gas Turbine Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Asia-Pacific Gas Turbine Industry Share (%) by Company 2025

List of Tables

- Table 1: Asia-Pacific Gas Turbine Industry Revenue billion Forecast, by Capacity 2020 & 2033

- Table 2: Asia-Pacific Gas Turbine Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Asia-Pacific Gas Turbine Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 4: Asia-Pacific Gas Turbine Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 5: Asia-Pacific Gas Turbine Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Asia-Pacific Gas Turbine Industry Revenue billion Forecast, by Capacity 2020 & 2033

- Table 7: Asia-Pacific Gas Turbine Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 8: Asia-Pacific Gas Turbine Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 9: Asia-Pacific Gas Turbine Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 10: Asia-Pacific Gas Turbine Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 11: Asia-Pacific Gas Turbine Industry Revenue billion Forecast, by Capacity 2020 & 2033

- Table 12: Asia-Pacific Gas Turbine Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 13: Asia-Pacific Gas Turbine Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 14: Asia-Pacific Gas Turbine Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 15: Asia-Pacific Gas Turbine Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Asia-Pacific Gas Turbine Industry Revenue billion Forecast, by Capacity 2020 & 2033

- Table 17: Asia-Pacific Gas Turbine Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Asia-Pacific Gas Turbine Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 19: Asia-Pacific Gas Turbine Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 20: Asia-Pacific Gas Turbine Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 21: Asia-Pacific Gas Turbine Industry Revenue billion Forecast, by Capacity 2020 & 2033

- Table 22: Asia-Pacific Gas Turbine Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 23: Asia-Pacific Gas Turbine Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 24: Asia-Pacific Gas Turbine Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 25: Asia-Pacific Gas Turbine Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia-Pacific Gas Turbine Industry?

The projected CAGR is approximately 11.2%.

2. Which companies are prominent players in the Asia-Pacific Gas Turbine Industry?

Key companies in the market include Opra Turbines BV, Ansaldo Gas Turbine Technology Co Ltd, Harbin Electric Co Ltd, Bharat Heavy Electricals Limited, Siemens AG, General Electric Company, Kawasaki Heavy Industries Ltd, Capstone Turbine Corporation*List Not Exhaustive, Mitsubishi Heavy Industries Ltd.

3. What are the main segments of the Asia-Pacific Gas Turbine Industry?

The market segments include Capacity, Type, Application, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 22.6 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Supportive Government Policies and Incentives4.; Environmental Concerns.

6. What are the notable trends driving market growth?

The Power Generation Segment is Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Fossil Fuel Subsidies.

8. Can you provide examples of recent developments in the market?

November 2022: Wärtsilä was awarded a contract to supply a gas-fueled 15.5 MW captive power plant under an engineering, procurement, and construction (EPC) contract along with a five-year Operation & Maintenance (O&M) agreement in Chennai, Tamilnadu, India. The order has been placed by Tamilnadu Petroproducts Limited (TPL), the world's leading manufacturer of linear alkyl benzene (LAB), a subsidiary of AM International, Singapore.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia-Pacific Gas Turbine Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia-Pacific Gas Turbine Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia-Pacific Gas Turbine Industry?

To stay informed about further developments, trends, and reports in the Asia-Pacific Gas Turbine Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence