Key Insights

The Asia-Pacific Armored Fighting Vehicles (AFV) Market is poised for robust expansion, projected to reach $5.37 billion by 2025, with a significant Compound Annual Growth Rate (CAGR) of 5.13% throughout the forecast period of 2025-2033. This growth is fueled by a confluence of escalating geopolitical tensions, ongoing military modernization programs across key nations, and a growing emphasis on homeland security. Countries in the region are actively investing in advanced AFVs to enhance their defense capabilities, counter emerging threats, and maintain regional stability. The demand for sophisticated Infantry Fighting Vehicles (IFVs) and Main Battle Tanks (MBTs) is particularly pronounced, driven by their crucial roles in modern warfare scenarios, including urban combat and expeditionary operations. Furthermore, the increasing adoption of networked warfare concepts and the integration of advanced technologies such as active protection systems, enhanced situational awareness, and improved mobility are shaping the evolution of AFVs in the region.

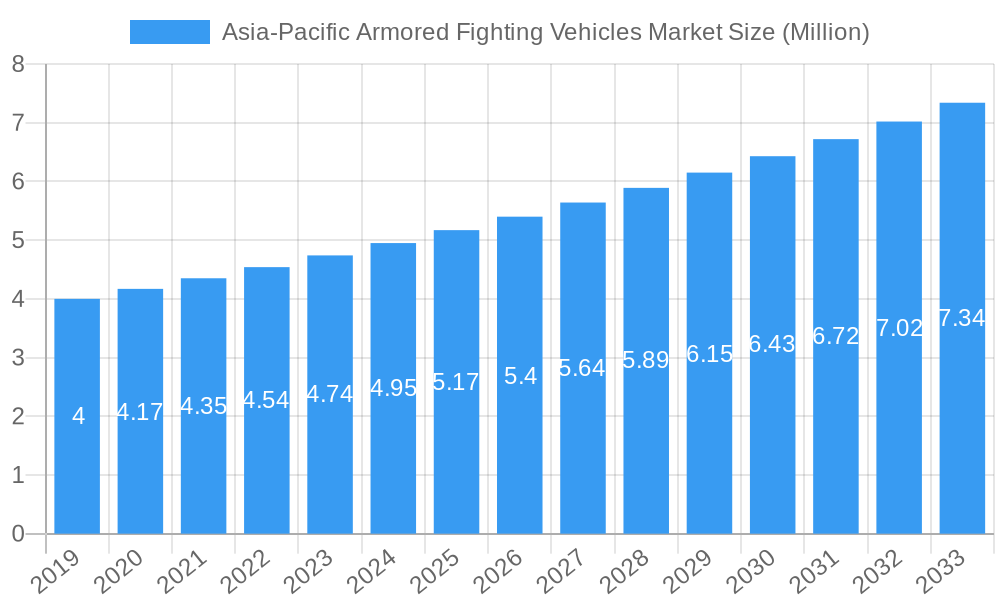

Asia-Pacific Armored Fighting Vehicles Market Market Size (In Million)

Key drivers propelling this market forward include the strategic imperative for national defense, coupled with substantial government spending allocated towards upgrading aging military fleets. The "Rest of Asia-Pacific" segment, encompassing nations with burgeoning defense industries and increasing security concerns, is expected to contribute significantly to overall market growth. Trends such as the development of lighter, more modular, and technologically advanced AFVs are evident, catering to diverse operational requirements. However, the market also faces certain restraints, including the high cost of advanced AFV acquisition and maintenance, as well as the availability of complex indigenous manufacturing capabilities in some established defense markets. Despite these challenges, the continuous pursuit of technological superiority and the evolving security landscape in the Asia-Pacific region underscore a positive outlook for the armored fighting vehicles market.

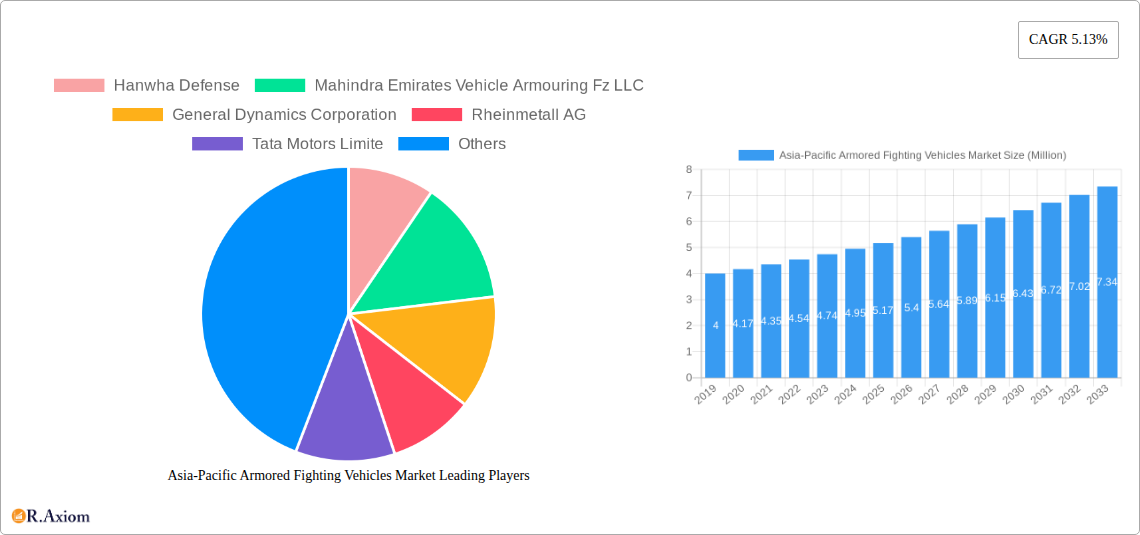

Asia-Pacific Armored Fighting Vehicles Market Company Market Share

Here is a detailed, SEO-optimized report description for the Asia-Pacific Armored Fighting Vehicles Market:

Asia-Pacific Armored Fighting Vehicles Market Market Concentration & Innovation

The Asia-Pacific Armored Fighting Vehicles (AFV) market exhibits a moderate to high degree of concentration, driven by a handful of dominant players and a growing number of regional manufacturers investing heavily in advanced technologies. Innovation is primarily fueled by the escalating geopolitical tensions, the need for enhanced battlefield survivability, and the integration of cutting-edge technologies like artificial intelligence (AI), advanced sensor suites, and improved defensive systems. Regulatory frameworks are becoming more stringent, with a focus on interoperability, cybersecurity, and adherence to international arms control treaties. Product substitutes are limited in the direct AFV market, but advancements in unmanned ground vehicles (UGVs) and drone technology present indirect competitive pressures. End-user trends indicate a strong preference for modular designs, enhanced C4ISR capabilities, and platform commonality to reduce logistical burdens. Mergers and acquisitions (M&A) activity is expected to rise as companies seek to expand their technological portfolios, market reach, and manufacturing capacities. For instance, strategic acquisitions of niche technology providers specializing in active protection systems or advanced materials are anticipated. Key M&A deal values are projected to reach several hundred million USD as consolidation efforts intensify to capture larger market shares.

- Market Concentration Drivers: Limited number of established global defense contractors, high capital investment requirements for R&D and manufacturing, and long procurement cycles.

- Innovation Focus Areas: Active protection systems (APS), modular armor solutions, AI-driven target recognition and situational awareness, advanced propulsion systems, and unmanned capabilities.

- Regulatory Influence: National defense modernization programs, export control regulations, and adherence to military standardization agreements.

- End-User Preferences: Increased demand for lightweight, versatile platforms, multi-role capabilities, and integrated network-centric warfare systems.

Asia-Pacific Armored Fighting Vehicles Market Industry Trends & Insights

The Asia-Pacific Armored Fighting Vehicles market is poised for significant growth, driven by a confluence of escalating regional security concerns, aggressive military modernization initiatives by several key nations, and the continuous pursuit of technological superiority. The market is expected to witness a compound annual growth rate (CAGR) of approximately 5.2% during the study period from 2019 to 2033, reaching an estimated market size of USD 25.8 Billion by 2033. This expansion is underpinned by substantial government investments in defense budgets across countries like China, India, and South Korea, aimed at bolstering their land forces' capabilities to counter evolving threats. Technological disruptions are playing a pivotal role, with the integration of AI for enhanced battlefield awareness, autonomous navigation, and improved fire control systems becoming a critical differentiator. Furthermore, the development of advanced composite materials and reactive armor is enhancing vehicle survivability against modern anti-tank guided missiles (ATGMs) and improvised explosive devices (IEDs). Consumer preferences, or rather end-user military requirements, are shifting towards more versatile and multi-mission platforms that can perform a range of tasks from troop transport to direct fire support and reconnaissance. The demand for wheeled vehicles, offering greater mobility and logistical efficiency, is also on the rise, complementing the continued need for tracked vehicles in demanding terrains. Competitive dynamics are characterized by intense rivalry among established global defense giants and increasingly capable regional manufacturers. Companies are investing heavily in research and development to offer next-generation AFVs that meet stringent military specifications while remaining cost-effective. The market penetration of advanced technologies is rapidly increasing, as nations prioritize equipping their forces with state-of-the-art armored platforms. For example, the ongoing development and deployment of new Infantry Fighting Vehicles (IFVs) with enhanced protection and firepower are reshaping land warfare doctrines across the region. The report will delve into the intricate interplay of these trends, providing granular insights into the future trajectory of the Asia-Pacific AFV market.

- Market Growth Drivers: Geopolitical tensions, defense budget increases, military modernization programs, and the need for force projection.

- Technological Advancements: AI integration, advanced armor solutions, active protection systems, hybrid-electric powertrains, and C4ISR upgrades.

- End-User Preferences: Versatility, modularity, survivability, network-centric capabilities, and logistical efficiency.

- Competitive Landscape: Intense competition, strategic partnerships, indigenous manufacturing capabilities, and focus on export markets.

- Market Penetration: Increasing adoption of advanced technologies and a shift towards lighter, more mobile platforms.

Dominant Markets & Segments in Asia-Pacific Armored Fighting Vehicles Market

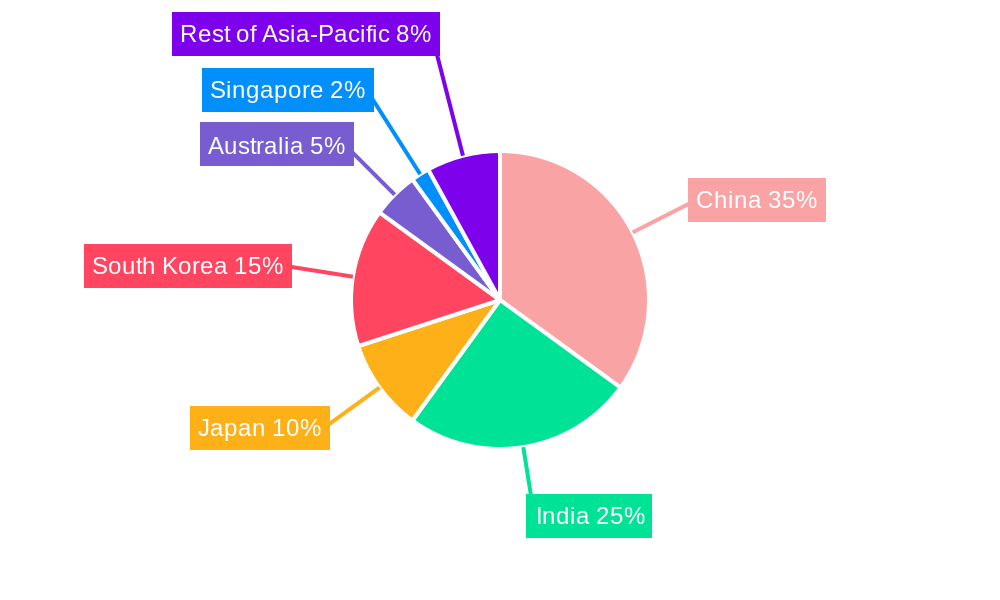

The Asia-Pacific Armored Fighting Vehicles (AFV) market is a dynamic landscape, with significant dominance exhibited by specific regions and segments. China stands as a pivotal market, driven by its immense defense budget, rapid technological advancement, and the sheer scale of its military. Its continued emphasis on modernizing its ground forces and its strategic objectives in the Indo-Pacific region fuel a robust demand for a wide array of AFVs. India follows closely, with its ambitious "Make in India" initiative and escalating border security concerns necessitating substantial investments in indigenous defense production and acquisition of advanced armored platforms. South Korea is another key player, not only as a significant consumer but also as a leading producer of sophisticated AFVs, exemplified by its advanced Main Battle Tank (MBT) programs.

The Main Battle Tank (MBT) segment is consistently dominant due to its critical role in offensive and defensive operations, requiring substantial firepower and protection. However, the Infantry Fighting Vehicle (IFV) segment is experiencing rapid growth, driven by the evolving nature of modern warfare that emphasizes mobile protected firepower to support infantry in complex environments. Armored Personnel Carriers (APCs) also hold a significant share, crucial for troop mobility and protection in lower-intensity conflicts and peacekeeping operations.

Dominant Geographies:

- China: Driven by a massive defense budget, ongoing military modernization, and regional security ambitions. China's large-scale production capabilities and focus on indigenous innovation make it a central market.

- Key Drivers: Force modernization, strategic positioning, technological self-reliance.

- India: Fueled by border tensions, large-scale procurement needs, and the government's push for domestic defense manufacturing. India's focus is on acquiring and developing versatile AFVs to meet diverse operational requirements.

- Key Drivers: Border security, "Make in India" initiative, multi-role platform demand.

- South Korea: Characterized by advanced technological development and export capabilities, particularly in MBTs and IFVs. Its strategic alliances and technological prowess are key to its market standing.

- Key Drivers: Technological innovation, export potential, advanced platform development.

- Australia: Focus on enhancing its naval and land capabilities with a strategic emphasis on interoperability with allies and adopting advanced, technologically sophisticated AFVs.

- Key Drivers: Interoperability, technological advancement, regional security posture.

- China: Driven by a massive defense budget, ongoing military modernization, and regional security ambitions. China's large-scale production capabilities and focus on indigenous innovation make it a central market.

Dominant Segments:

- Main Battle Tank (MBT): Essential for decisive land warfare, MBTs continue to be a cornerstone of military arsenals, demanding high levels of protection and firepower.

- Key Drivers: Deterrence, offensive operations, heavy firepower requirements.

- Infantry Fighting Vehicle (IFV): The growing demand for mobile protected firepower to support infantry in complex battlefields makes IFVs a rapidly expanding segment.

- Key Drivers: Mechanized infantry support, versatile firepower, enhanced survivability.

- Armored Personnel Carrier (APC): Crucial for troop transport and protection, APCs remain vital for logistical support and operations in various threat environments.

- Key Drivers: Troop mobility, protected transport, battlefield survivability.

- Main Battle Tank (MBT): Essential for decisive land warfare, MBTs continue to be a cornerstone of military arsenals, demanding high levels of protection and firepower.

The "Rest of Asia-Pacific" region, encompassing nations like Japan, Singapore, and Southeast Asian countries, also contributes significantly, albeit with varied adoption rates and focuses. Japan's recent procurement decisions highlight a growing emphasis on advanced wheeled armored vehicles, reflecting a strategic shift towards lighter, more mobile platforms. Singapore's focus on advanced technology and force projection further underscores the region's diverse and evolving needs in the armored fighting vehicles sector.

Asia-Pacific Armored Fighting Vehicles Market Product Developments

The Asia-Pacific Armored Fighting Vehicles (AFV) market is witnessing rapid product development driven by the demand for enhanced survivability, lethality, and versatility. Key innovations include the integration of advanced composite armor for improved protection against modern threats, active protection systems (APS) to intercept incoming projectiles, and sophisticated C4ISR (Command, Control, Communications, Computers, Intelligence, Surveillance, and Reconnaissance) suites for superior situational awareness. Companies are also focusing on modular designs that allow for rapid reconfiguration of weapon systems and armor packages, catering to diverse mission requirements. The trend towards lighter, more mobile platforms, including wheeled IFVs and APCs, is also prominent, offering logistical advantages and greater operational flexibility.

- Key Technological Trends: Active protection systems, modular armor, AI integration, advanced sensors, and hybrid propulsion.

- Market Fit: Products are increasingly tailored to meet specific regional threats and operational doctrines, emphasizing adaptability and interoperability.

- Competitive Advantage: Companies offering advanced integrated systems, modular designs, and superior cost-effectiveness are gaining a competitive edge.

Report Scope & Segmentation Analysis

This comprehensive report offers an in-depth analysis of the Asia-Pacific Armored Fighting Vehicles Market, covering the historical period from 2019 to 2024, the base year 2025, and a forecast period extending to 2033. The market is meticulously segmented by vehicle type and geography, providing granular insights into specific market dynamics and growth projections.

Type Segmentation:

- Armored Personnel Carrier (APC): This segment focuses on vehicles designed for troop transport and protection, with projected growth driven by ongoing modernization efforts in various Asia-Pacific nations. Market sizes are estimated to reach USD 4.5 Billion by 2033, with a CAGR of 4.8%.

- Infantry Fighting Vehicle (IFV): The IFV segment is anticipated to witness substantial growth due to increasing demand for direct fire support and troop mobility in complex combat scenarios. Projected market size by 2033 is USD 7.2 Billion, with a CAGR of 5.5%.

- Main Battle Tank (MBT): While a mature segment, MBTs will continue to be a critical component of land forces, with ongoing upgrades and limited new acquisitions driving market value. Expected market size by 2033 is USD 9.8 Billion, with a CAGR of 5.0%.

- Other Types: This includes specialized vehicles such as self-propelled artillery, armored recovery vehicles, and combat engineering vehicles, which collectively contribute to a growing niche market. Projected market size by 2033 is USD 4.3 Billion, with a CAGR of 4.9%.

Geography Segmentation:

- China: Dominant market with significant domestic production and procurement. Forecasted market size by 2033 is USD 8.1 Billion.

- India: Rapidly growing market driven by modernization and indigenous manufacturing initiatives. Forecasted market size by 2033 is USD 6.5 Billion.

- Japan: Focus on advanced wheeled vehicles and technological upgrades. Forecasted market size by 2033 is USD 2.1 Billion.

- South Korea: Leading player in both production and technological innovation. Forecasted market size by 2033 is USD 3.5 Billion.

- Australia: Emphasis on advanced platforms and interoperability. Forecasted market size by 2033 is USD 1.5 Billion.

- Singapore: Focused on high-tech solutions and advanced capabilities. Forecasted market size by 2033 is USD 1.1 Billion.

- Rest of Asia-Pacific: Encompasses emerging markets with diverse needs and growth potential. Forecasted market size by 2033 is USD 3.0 Billion.

Key Drivers of Asia-Pacific Armored Fighting Vehicles Market Growth

The Asia-Pacific Armored Fighting Vehicles (AFV) market is propelled by several critical growth drivers that underscore the region's evolving security landscape. Escalating geopolitical tensions and territorial disputes among several nations necessitate enhanced military capabilities, directly translating into increased demand for advanced AFVs. Aggressive military modernization programs undertaken by countries like China, India, and South Korea are a primary catalyst, as they seek to upgrade their aging fleets with state-of-the-art armored platforms incorporating cutting-edge technologies. Furthermore, the increasing threat from asymmetric warfare, including the proliferation of improvised explosive devices (IEDs) and advanced anti-tank guided missiles (ATGMs), compels militaries to invest in vehicles with superior protection and survivability.

- Geopolitical Instability: Rising regional tensions and border disputes are driving demand for enhanced defense capabilities.

- Military Modernization: Significant government investments in upgrading land forces with advanced armored platforms.

- Technological Advancements: Integration of AI, active protection systems, and advanced materials to counter evolving threats.

- Asymmetric Warfare Threats: The need for robust protection against IEDs and advanced anti-tank weapons.

- Economic Growth: Increased defense spending capacity in major Asia-Pacific economies.

Challenges in the Asia-Pacific Armored Fighting Vehicles Market Sector

Despite robust growth, the Asia-Pacific Armored Fighting Vehicles (AFV) market faces several significant challenges that could impact its trajectory. High procurement costs associated with advanced armored platforms represent a substantial barrier for many developing nations in the region, leading to protracted acquisition cycles and prioritization challenges. The complexity of integrating new technologies, such as artificial intelligence and advanced sensor systems, into existing military doctrines and operational frameworks requires extensive training and infrastructure development, posing a significant hurdle. Supply chain disruptions, exacerbated by geopolitical events and the reliance on a limited number of specialized component manufacturers, can lead to production delays and increased costs. Furthermore, stringent export control regulations imposed by major defense-exporting nations can limit the availability of critical technologies and components, impacting indigenous production capabilities and international collaborations.

- High Procurement Costs: The substantial financial investment required for advanced AFVs limits accessibility for some nations.

- Technological Integration Complexity: Challenges in integrating new technologies with existing military systems and personnel training.

- Supply Chain Vulnerabilities: Reliance on specialized components and potential disruptions from geopolitical events.

- Regulatory Hurdles: Stringent export controls and national defense procurement policies can impact market access.

- Skilled Workforce Shortage: A lack of trained personnel for operating and maintaining advanced armored systems.

Emerging Opportunities in Asia-Pacific Armored Fighting Vehicles Market

The Asia-Pacific Armored Fighting Vehicles (AFV) market presents numerous emerging opportunities for industry players. The growing demand for unmanned ground vehicles (UGVs) and remote weapon stations signifies a shift towards greater automation and reduced personnel risk in combat, creating a significant growth avenue. Advancements in artificial intelligence (AI) for enhanced battlefield awareness, target recognition, and autonomous operations offer substantial potential for differentiation and value creation. The increasing focus on modularity and platform commonality across different AFV types presents an opportunity for manufacturers to develop adaptable solutions that reduce lifecycle costs and logistical burdens for militaries. Furthermore, the burgeoning defense industries in Southeast Asian nations, coupled with ongoing modernization efforts in countries like Vietnam and Indonesia, represent untapped markets for established and emerging AFV providers.

- Unmanned Ground Vehicles (UGVs): Increasing demand for autonomous systems and remote-controlled platforms.

- Artificial Intelligence (AI) Integration: Opportunities in developing AI-powered solutions for enhanced situational awareness and operational efficiency.

- Modular and Common Platforms: Demand for adaptable vehicles that can be reconfigured for various missions, reducing costs and logistical complexity.

- Emerging Markets: Growth potential in Southeast Asian nations undergoing defense modernization.

- Upgrade and Modernization Programs: Opportunities to refurbish and enhance existing AFV fleets of various nations.

Leading Players in the Asia-Pacific Armored Fighting Vehicles Market Market

Hanwha Defense Mahindra Emirates Vehicle Armouring Fz LLC General Dynamics Corporation Rheinmetall AG Tata Motors Limited FNSS Savunma Sistemleri AŞ Kalyani Group Patria Group JSC Rosoboronexport (Rostec) BAE Systems plc Krauss-Maffei Wegmann GmbH & Co KG Defence Research and Development Organisation (DRDO) Mitsubishi Heavy Industries Ltd

Key Developments in Asia-Pacific Armored Fighting Vehicles Market Industry

- June 2023: South Korea announced the mass production of additional K2 Black Panther main battle tanks for an estimated USD 1.46 Billion, signaling a significant boost to its armored capabilities and export potential.

- December 2022: Japan selected Patria-built armored modular vehicles (AMV) to replace the Type-96 8X8 wheeled armored personnel carriers of the Japan Ground Self-Defense Force, indicating a strategic shift towards advanced wheeled armored platforms.

Strategic Outlook for Asia-Pacific Armored Fighting Vehicles Market Market

The strategic outlook for the Asia-Pacific Armored Fighting Vehicles (AFV) market remains exceptionally strong, fueled by a sustained demand for enhanced defense capabilities and technological advancements. The region's dynamic geopolitical environment, coupled with aggressive military modernization programs, will continue to drive significant investments in AFVs. Opportunities lie in focusing on modular, adaptable platforms that can be rapidly reconfigured for diverse mission requirements, catering to the evolving needs of modern warfare. The integration of artificial intelligence, advanced sensor systems, and active protection technologies will be crucial for maintaining a competitive edge. Furthermore, the growing emphasis on indigenous defense manufacturing within key Asia-Pacific nations presents opportunities for strategic partnerships and technology transfer, fostering local production capabilities and creating sustainable growth. The market is expected to witness a significant CAGR of 5.2% during the forecast period, driven by these underlying growth catalysts and the imperative for nations to ensure regional stability and security.

Asia-Pacific Armored Fighting Vehicles Market Segmentation

-

1. Type

- 1.1. Armored Personnel Carrier (APC)

- 1.2. Infantry Fighting Vehicle (IFV)

- 1.3. Main Battle Tank (MBT)

- 1.4. Other Types

-

2. Geography

- 2.1. China

- 2.2. India

- 2.3. Japan

- 2.4. South Korea

- 2.5. Australia

- 2.6. Singapore

- 2.7. Rest of Asia-Pacific

Asia-Pacific Armored Fighting Vehicles Market Segmentation By Geography

- 1. China

- 2. India

- 3. Japan

- 4. South Korea

- 5. Australia

- 6. Singapore

- 7. Rest of Asia Pacific

Asia-Pacific Armored Fighting Vehicles Market Regional Market Share

Geographic Coverage of Asia-Pacific Armored Fighting Vehicles Market

Asia-Pacific Armored Fighting Vehicles Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.13% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Armored Personnel Carrier (APC)

- 5.1.2. Infantry Fighting Vehicle (IFV)

- 5.1.3. Main Battle Tank (MBT)

- 5.1.4. Other Types

- 5.2. Market Analysis, Insights and Forecast - by Geography

- 5.2.1. China

- 5.2.2. India

- 5.2.3. Japan

- 5.2.4. South Korea

- 5.2.5. Australia

- 5.2.6. Singapore

- 5.2.7. Rest of Asia-Pacific

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. China

- 5.3.2. India

- 5.3.3. Japan

- 5.3.4. South Korea

- 5.3.5. Australia

- 5.3.6. Singapore

- 5.3.7. Rest of Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Asia-Pacific Armored Fighting Vehicles Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Armored Personnel Carrier (APC)

- 6.1.2. Infantry Fighting Vehicle (IFV)

- 6.1.3. Main Battle Tank (MBT)

- 6.1.4. Other Types

- 6.2. Market Analysis, Insights and Forecast - by Geography

- 6.2.1. China

- 6.2.2. India

- 6.2.3. Japan

- 6.2.4. South Korea

- 6.2.5. Australia

- 6.2.6. Singapore

- 6.2.7. Rest of Asia-Pacific

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. China Asia-Pacific Armored Fighting Vehicles Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Armored Personnel Carrier (APC)

- 7.1.2. Infantry Fighting Vehicle (IFV)

- 7.1.3. Main Battle Tank (MBT)

- 7.1.4. Other Types

- 7.2. Market Analysis, Insights and Forecast - by Geography

- 7.2.1. China

- 7.2.2. India

- 7.2.3. Japan

- 7.2.4. South Korea

- 7.2.5. Australia

- 7.2.6. Singapore

- 7.2.7. Rest of Asia-Pacific

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. India Asia-Pacific Armored Fighting Vehicles Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Armored Personnel Carrier (APC)

- 8.1.2. Infantry Fighting Vehicle (IFV)

- 8.1.3. Main Battle Tank (MBT)

- 8.1.4. Other Types

- 8.2. Market Analysis, Insights and Forecast - by Geography

- 8.2.1. China

- 8.2.2. India

- 8.2.3. Japan

- 8.2.4. South Korea

- 8.2.5. Australia

- 8.2.6. Singapore

- 8.2.7. Rest of Asia-Pacific

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Japan Asia-Pacific Armored Fighting Vehicles Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Armored Personnel Carrier (APC)

- 9.1.2. Infantry Fighting Vehicle (IFV)

- 9.1.3. Main Battle Tank (MBT)

- 9.1.4. Other Types

- 9.2. Market Analysis, Insights and Forecast - by Geography

- 9.2.1. China

- 9.2.2. India

- 9.2.3. Japan

- 9.2.4. South Korea

- 9.2.5. Australia

- 9.2.6. Singapore

- 9.2.7. Rest of Asia-Pacific

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. South Korea Asia-Pacific Armored Fighting Vehicles Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Armored Personnel Carrier (APC)

- 10.1.2. Infantry Fighting Vehicle (IFV)

- 10.1.3. Main Battle Tank (MBT)

- 10.1.4. Other Types

- 10.2. Market Analysis, Insights and Forecast - by Geography

- 10.2.1. China

- 10.2.2. India

- 10.2.3. Japan

- 10.2.4. South Korea

- 10.2.5. Australia

- 10.2.6. Singapore

- 10.2.7. Rest of Asia-Pacific

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Australia Asia-Pacific Armored Fighting Vehicles Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Armored Personnel Carrier (APC)

- 11.1.2. Infantry Fighting Vehicle (IFV)

- 11.1.3. Main Battle Tank (MBT)

- 11.1.4. Other Types

- 11.2. Market Analysis, Insights and Forecast - by Geography

- 11.2.1. China

- 11.2.2. India

- 11.2.3. Japan

- 11.2.4. South Korea

- 11.2.5. Australia

- 11.2.6. Singapore

- 11.2.7. Rest of Asia-Pacific

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Singapore Asia-Pacific Armored Fighting Vehicles Market Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Type

- 12.1.1. Armored Personnel Carrier (APC)

- 12.1.2. Infantry Fighting Vehicle (IFV)

- 12.1.3. Main Battle Tank (MBT)

- 12.1.4. Other Types

- 12.2. Market Analysis, Insights and Forecast - by Geography

- 12.2.1. China

- 12.2.2. India

- 12.2.3. Japan

- 12.2.4. South Korea

- 12.2.5. Australia

- 12.2.6. Singapore

- 12.2.7. Rest of Asia-Pacific

- 12.1. Market Analysis, Insights and Forecast - by Type

- 13. Rest of Asia Pacific Asia-Pacific Armored Fighting Vehicles Market Analysis, Insights and Forecast, 2020-2032

- 13.1. Market Analysis, Insights and Forecast - by Type

- 13.1.1. Armored Personnel Carrier (APC)

- 13.1.2. Infantry Fighting Vehicle (IFV)

- 13.1.3. Main Battle Tank (MBT)

- 13.1.4. Other Types

- 13.2. Market Analysis, Insights and Forecast - by Geography

- 13.2.1. China

- 13.2.2. India

- 13.2.3. Japan

- 13.2.4. South Korea

- 13.2.5. Australia

- 13.2.6. Singapore

- 13.2.7. Rest of Asia-Pacific

- 13.1. Market Analysis, Insights and Forecast - by Type

- 14. Competitive Analysis

- 14.1. Company Profiles

- 14.1.1 Hanwha Defense

- 14.1.1.1. Company Overview

- 14.1.1.2. Products

- 14.1.1.3. Company Financials

- 14.1.1.4. SWOT Analysis

- 14.1.2 Mahindra Emirates Vehicle Armouring Fz LLC

- 14.1.2.1. Company Overview

- 14.1.2.2. Products

- 14.1.2.3. Company Financials

- 14.1.2.4. SWOT Analysis

- 14.1.3 General Dynamics Corporation

- 14.1.3.1. Company Overview

- 14.1.3.2. Products

- 14.1.3.3. Company Financials

- 14.1.3.4. SWOT Analysis

- 14.1.4 Rheinmetall AG

- 14.1.4.1. Company Overview

- 14.1.4.2. Products

- 14.1.4.3. Company Financials

- 14.1.4.4. SWOT Analysis

- 14.1.5 Tata Motors Limite

- 14.1.5.1. Company Overview

- 14.1.5.2. Products

- 14.1.5.3. Company Financials

- 14.1.5.4. SWOT Analysis

- 14.1.6 FNSS Savunma Sistemleri AŞ

- 14.1.6.1. Company Overview

- 14.1.6.2. Products

- 14.1.6.3. Company Financials

- 14.1.6.4. SWOT Analysis

- 14.1.7 Kalyani Group

- 14.1.7.1. Company Overview

- 14.1.7.2. Products

- 14.1.7.3. Company Financials

- 14.1.7.4. SWOT Analysis

- 14.1.8 Patria Group

- 14.1.8.1. Company Overview

- 14.1.8.2. Products

- 14.1.8.3. Company Financials

- 14.1.8.4. SWOT Analysis

- 14.1.9 JSC Rosoboronexport (Rostec)

- 14.1.9.1. Company Overview

- 14.1.9.2. Products

- 14.1.9.3. Company Financials

- 14.1.9.4. SWOT Analysis

- 14.1.10 BAE Systems plc

- 14.1.10.1. Company Overview

- 14.1.10.2. Products

- 14.1.10.3. Company Financials

- 14.1.10.4. SWOT Analysis

- 14.1.11 Krauss-Maffei Wegmann GmbH & Co KG

- 14.1.11.1. Company Overview

- 14.1.11.2. Products

- 14.1.11.3. Company Financials

- 14.1.11.4. SWOT Analysis

- 14.1.12 Defence Research and Development Organisation (DRDO)

- 14.1.12.1. Company Overview

- 14.1.12.2. Products

- 14.1.12.3. Company Financials

- 14.1.12.4. SWOT Analysis

- 14.1.13 Mitsubishi Heavy Industries Ltd

- 14.1.13.1. Company Overview

- 14.1.13.2. Products

- 14.1.13.3. Company Financials

- 14.1.13.4. SWOT Analysis

- 14.1.1 Hanwha Defense

- 14.2. Market Entropy

- 14.2.1 Company's Key Areas Served

- 14.2.2 Recent Developments

- 14.3. Company Market Share Analysis 2025

- 14.3.1 Top 5 Companies Market Share Analysis

- 14.3.2 Top 3 Companies Market Share Analysis

- 14.4. List of Potential Customers

- 15. Research Methodology

List of Figures

- Figure 1: Asia-Pacific Armored Fighting Vehicles Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Asia-Pacific Armored Fighting Vehicles Market Share (%) by Company 2025

List of Tables

- Table 1: Asia-Pacific Armored Fighting Vehicles Market Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Asia-Pacific Armored Fighting Vehicles Market Revenue Million Forecast, by Geography 2020 & 2033

- Table 3: Asia-Pacific Armored Fighting Vehicles Market Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Asia-Pacific Armored Fighting Vehicles Market Revenue Million Forecast, by Type 2020 & 2033

- Table 5: Asia-Pacific Armored Fighting Vehicles Market Revenue Million Forecast, by Geography 2020 & 2033

- Table 6: Asia-Pacific Armored Fighting Vehicles Market Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Asia-Pacific Armored Fighting Vehicles Market Revenue Million Forecast, by Type 2020 & 2033

- Table 8: Asia-Pacific Armored Fighting Vehicles Market Revenue Million Forecast, by Geography 2020 & 2033

- Table 9: Asia-Pacific Armored Fighting Vehicles Market Revenue Million Forecast, by Country 2020 & 2033

- Table 10: Asia-Pacific Armored Fighting Vehicles Market Revenue Million Forecast, by Type 2020 & 2033

- Table 11: Asia-Pacific Armored Fighting Vehicles Market Revenue Million Forecast, by Geography 2020 & 2033

- Table 12: Asia-Pacific Armored Fighting Vehicles Market Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Asia-Pacific Armored Fighting Vehicles Market Revenue Million Forecast, by Type 2020 & 2033

- Table 14: Asia-Pacific Armored Fighting Vehicles Market Revenue Million Forecast, by Geography 2020 & 2033

- Table 15: Asia-Pacific Armored Fighting Vehicles Market Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Asia-Pacific Armored Fighting Vehicles Market Revenue Million Forecast, by Type 2020 & 2033

- Table 17: Asia-Pacific Armored Fighting Vehicles Market Revenue Million Forecast, by Geography 2020 & 2033

- Table 18: Asia-Pacific Armored Fighting Vehicles Market Revenue Million Forecast, by Country 2020 & 2033

- Table 19: Asia-Pacific Armored Fighting Vehicles Market Revenue Million Forecast, by Type 2020 & 2033

- Table 20: Asia-Pacific Armored Fighting Vehicles Market Revenue Million Forecast, by Geography 2020 & 2033

- Table 21: Asia-Pacific Armored Fighting Vehicles Market Revenue Million Forecast, by Country 2020 & 2033

- Table 22: Asia-Pacific Armored Fighting Vehicles Market Revenue Million Forecast, by Type 2020 & 2033

- Table 23: Asia-Pacific Armored Fighting Vehicles Market Revenue Million Forecast, by Geography 2020 & 2033

- Table 24: Asia-Pacific Armored Fighting Vehicles Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia-Pacific Armored Fighting Vehicles Market?

The projected CAGR is approximately 5.13%.

2. Which companies are prominent players in the Asia-Pacific Armored Fighting Vehicles Market?

Key companies in the market include Hanwha Defense, Mahindra Emirates Vehicle Armouring Fz LLC, General Dynamics Corporation, Rheinmetall AG, Tata Motors Limite, FNSS Savunma Sistemleri AŞ, Kalyani Group, Patria Group, JSC Rosoboronexport (Rostec), BAE Systems plc, Krauss-Maffei Wegmann GmbH & Co KG, Defence Research and Development Organisation (DRDO), Mitsubishi Heavy Industries Ltd.

3. What are the main segments of the Asia-Pacific Armored Fighting Vehicles Market?

The market segments include Type, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.37 Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Main Battle Tank Segment is Expected to Lead the Market during the Forecast Period.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

June 2023: South Korea announced the mass production of additional K2 Black Panther main battle tanks for an estimated USD 1.46 billion.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia-Pacific Armored Fighting Vehicles Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia-Pacific Armored Fighting Vehicles Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia-Pacific Armored Fighting Vehicles Market?

To stay informed about further developments, trends, and reports in the Asia-Pacific Armored Fighting Vehicles Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence