Key Insights

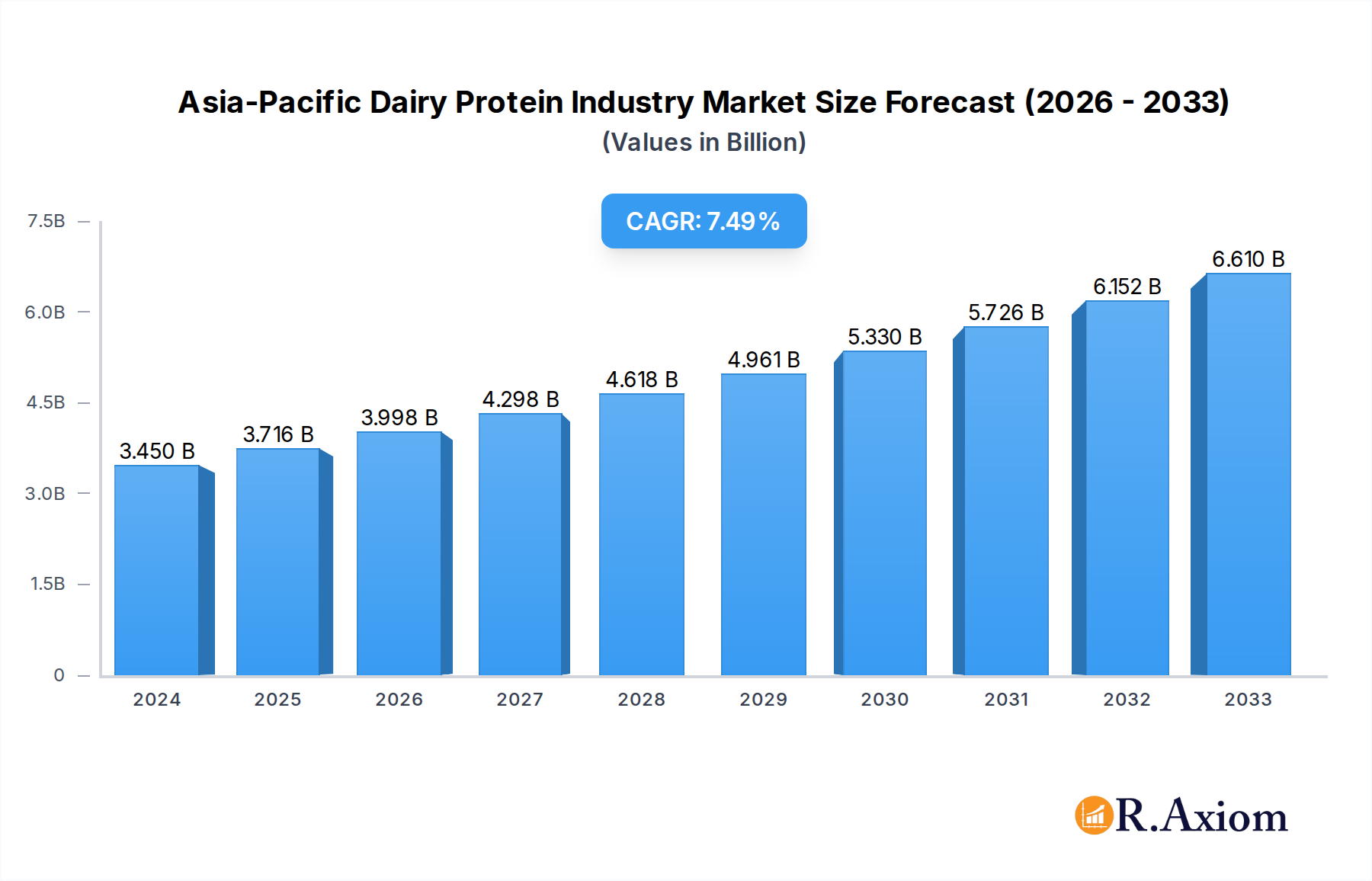

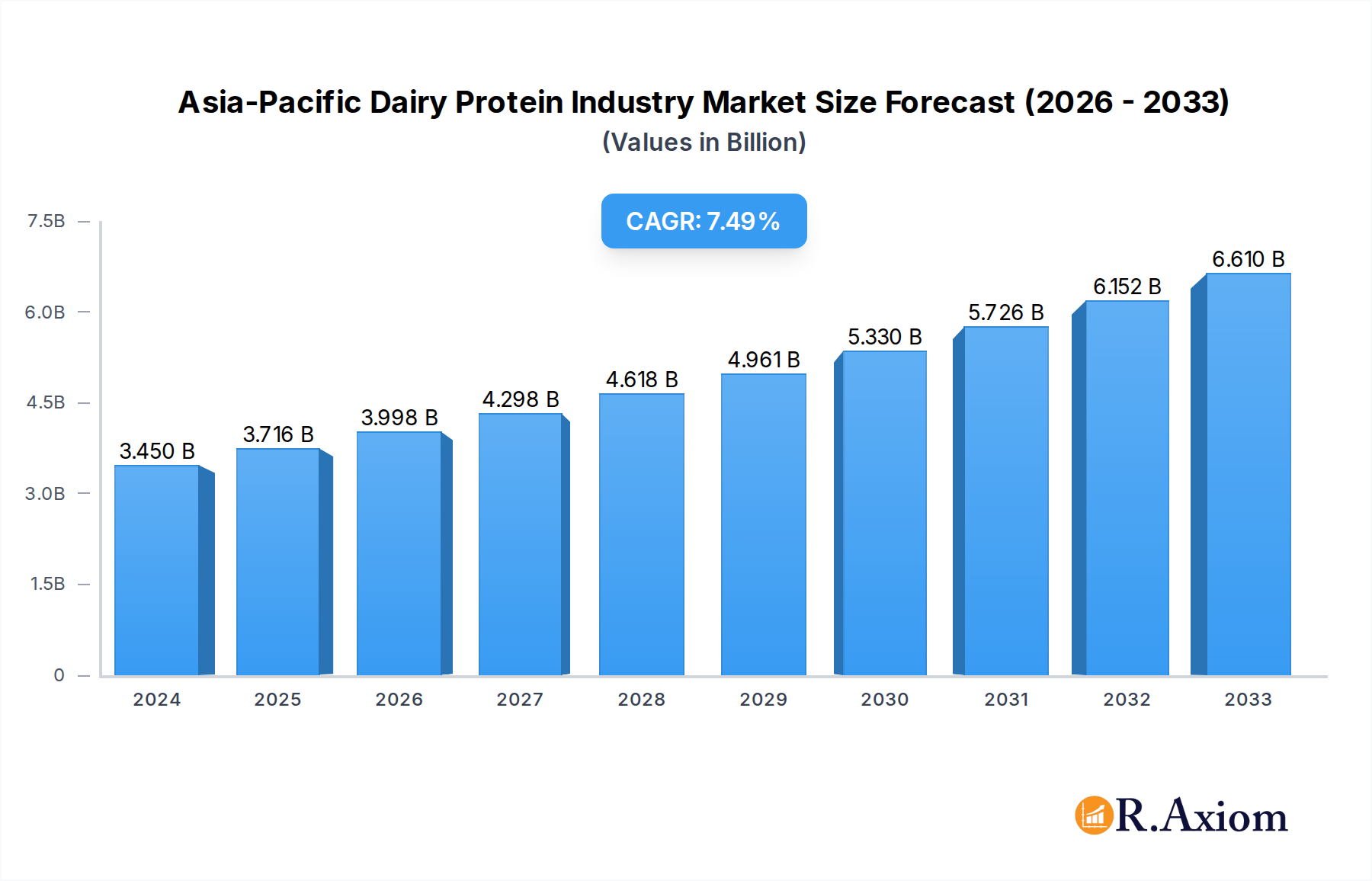

The Asia-Pacific dairy protein market is poised for significant expansion, driven by a confluence of evolving consumer preferences, rising health consciousness, and increasing demand from various end-use industries. With a projected market size of USD 3.45 billion in 2024, this dynamic sector is expected to experience a robust CAGR of 7.6%, culminating in substantial growth over the forecast period. Key growth drivers include the escalating demand for high-protein diets, particularly among health-conscious consumers and athletes seeking performance enhancement. The burgeoning infant nutrition segment, propelled by increasing birth rates and parental emphasis on early childhood development and nutrition, represents a major growth avenue. Furthermore, the expanding application of dairy proteins in functional foods, beverages, and even personal care products, owing to their versatile nutritional and functional properties, is significantly contributing to market momentum.

Asia-Pacific Dairy Protein Industry Market Size (In Billion)

The market is characterized by a diverse range of dairy protein segments, with Milk Protein Concentrates (MPCs) and Whey Protein Concentrates (WPCs) leading the pack due to their widespread use in food and beverage applications. Whey Protein Isolates (WPIs) and Milk Protein Isolates (MPIs) are also gaining traction due to their higher protein content and lower lactose levels, catering to lactose-intolerant consumers and specialized dietary needs. The "Others" category, encompassing specialized proteins, is also showing promise. Geographically, while China, India, and Southeast Asian nations are anticipated to be major growth engines, established markets like Japan and South Korea will continue to contribute substantially. Restraints, such as fluctuating raw material prices and stringent regulatory landscapes in certain regions, are present, but the overarching positive trends in consumer demand and product innovation are expected to outweigh these challenges, ensuring a healthy growth trajectory for the Asia-Pacific dairy protein industry.

Asia-Pacific Dairy Protein Industry Company Market Share

The Asia-Pacific dairy protein market exhibits moderate to high concentration, driven by a handful of global and regional players alongside a growing number of specialized ingredient suppliers. Innovation is a critical differentiator, with companies investing heavily in advanced processing techniques to enhance protein purity, functionality, and bioavailability. This includes developments in membrane filtration, chromatography, and enzymatic modification to produce higher-value ingredients like Milk Protein Isolates (MPIs) and Whey Protein Isolates (WPIs). Regulatory frameworks vary across the region, with stringent standards for infant nutrition in countries like Japan and China, influencing product formulations and quality control. Product substitutes, such as plant-based proteins, are gaining traction but are yet to fully displace the perceived superior nutritional profile and functional properties of dairy proteins for many applications. End-user trends are overwhelmingly positive, with rising disposable incomes and a growing health-conscious population fueling demand for protein-enriched foods and beverages. Mergers and acquisitions (M&A) are a key strategic tool for market consolidation and technology acquisition, with an estimated total deal value of over $5 billion in the historical period (2019-2024). Key players like Fonterra Co-operative Group (NZMP) and Hoogwegt are actively involved in strategic partnerships and acquisitions to expand their regional footprint and product portfolios.

Asia-Pacific Dairy Protein Industry Industry Trends & Insights

The Asia-Pacific dairy protein industry is poised for significant growth, driven by a confluence of robust market expansion drivers and evolving consumer preferences. The projected Compound Annual Growth Rate (CAGR) for the forecast period (2025-2033) is estimated to be approximately 7.5%, indicating substantial upward momentum. This growth is underpinned by an increasing health and wellness consciousness among consumers, particularly in emerging economies, who are actively seeking protein-fortified products to support active lifestyles and age-related nutritional needs. Infant nutrition remains a dominant application segment, propelled by a large and growing infant population and a parental inclination towards premium, protein-rich formulas. The demand for sports and performance nutrition products is also experiencing a surge, fueled by the rising popularity of fitness activities and a greater understanding of the role of protein in muscle recovery and building. Technological disruptions are playing a pivotal role in shaping the industry, with advancements in extraction and purification technologies enabling the production of higher-value ingredients with improved functional properties and solubility. Companies are investing in research and development to create novel protein ingredients tailored to specific applications, such as slow-release proteins for sustained energy or highly digestible whey hydrolysates. Competitive dynamics are intensifying, with both established global players and agile local manufacturers vying for market share. Strategic collaborations, joint ventures, and M&A activities are becoming increasingly common as companies seek to expand their product offerings, geographical reach, and technological capabilities. The penetration of dairy protein ingredients into novel applications like personal care and cosmetics is also an emerging trend, driven by their recognized moisturizing and skin-conditioning properties. The overall market penetration of dairy protein ingredients is expected to continue its upward trajectory throughout the forecast period.

Dominant Markets & Segments in Asia-Pacific Dairy Protein Industry

The Asia-Pacific dairy protein industry is characterized by its dynamic regional and segment-specific dominance. China stands out as the leading market, driven by its massive population, increasing disposable incomes, and a rapidly expanding middle class with a growing awareness of health and nutrition. Economic policies that favor domestic production and consumption, coupled with substantial investments in dairy infrastructure, further bolster China's position. The Food application segment is undeniably dominant, accounting for an estimated 75% of the total market revenue. Within the food sector, Infant Nutrition holds the largest share, driven by consistently high birth rates and parental prioritization of high-quality, protein-rich infant formulas. The demand for dairy-based foods, including yogurts, cheeses, and nutritional beverages, also significantly contributes to this segment's dominance. The Bakery and Confectionery and Frozen Desserts sub-segments are experiencing robust growth, as manufacturers increasingly incorporate dairy proteins to enhance texture, nutritional value, and shelf life.

- Leading Region: China, followed by India and Southeast Asian nations.

- Key Drivers:

- Large and growing consumer base.

- Rising disposable incomes and urbanization.

- Government initiatives promoting dairy consumption and food security.

- Increasing adoption of Western dietary habits.

- Key Drivers:

- Dominant Application Segment: Food (estimated 75% market share).

- Sub-Segment Dominance: Infant Nutrition.

- Key Drivers:

- High birth rates.

- Premiumization of infant formulas.

- Stringent regulatory standards ensuring quality and safety.

- Growing parental emphasis on early childhood nutrition.

- Key Drivers:

- Other Significant Food Sub-Segments: Dairy Based Food, Bakery, Confectionary and Frozen Desserts, Sports and Performance Nutrition.

- Key Drivers:

- Demand for convenient and healthy food options.

- Growing fitness culture and awareness of protein benefits.

- Innovations in food processing and formulation.

- Key Drivers:

- Sub-Segment Dominance: Infant Nutrition.

- Dominant Ingredients Type: Whey Protein Concentrates (WPCs) are the largest segment, owing to their versatility, cost-effectiveness, and widespread use in various food applications. Milk Protein Concentrates (MPCs) are also a significant contributor, valued for their balanced protein profile.

- Key Drivers for Ingredient Dominance:

- Cost-effectiveness and availability.

- Functional properties (emulsification, gelation, water-holding capacity).

- Nutritional profile (amino acid composition).

- Established manufacturing processes.

- Key Drivers for Ingredient Dominance:

Asia-Pacific Dairy Protein Industry Product Developments

Recent product developments in the Asia-Pacific dairy protein industry are centered on enhancing functionality and expanding application reach. Innovations include the development of microencapsulated whey proteins for improved stability and controlled release in beverages and food products, and highly purified caseinates designed for specific textures in processed foods and nutritional supplements. Companies are also focusing on creating plant-based protein alternatives that mimic the sensory and nutritional profiles of dairy proteins, as well as exploring novel applications in personal care for their moisturizing and anti-aging properties. These developments aim to capitalize on emerging consumer preferences for natural, high-protein, and functional ingredients, providing competitive advantages through superior performance and targeted market appeal.

Report Scope & Segmentation Analysis

This report provides an in-depth analysis of the Asia-Pacific dairy protein industry, segmented by ingredient type and application.

- Ingredients Type: The market is segmented into Milk Protein Concentrates (MPCs), Whey Protein Concentrates (WPCs), Milk Protein Isolates (MPIs), Whey Protein Isolates (WPIs), Casein and Caseinates, and Others. WPCs and MPCs are expected to dominate in terms of market size and growth due to their extensive use in mainstream food applications, while MPIs and WPIs are projected for higher growth rates driven by demand in specialized nutrition and functional foods.

- Application: The key application segments include Food, Beverage, Personal care & Cosmetics, and Animal Feed. Within the Food segment, further segmentation includes Infant Nutrition, Dairy Based Food, Bakery, Confectionery and Frozen Desserts, and Sports and Performance Nutrition. Infant Nutrition is the largest application segment and is expected to maintain its lead, followed by the broader Dairy Based Food category. Sports and Performance Nutrition is anticipated to witness the highest CAGR, reflecting the growing health and fitness trends.

Key Drivers of Asia-Pacific Dairy Protein Industry Growth

The growth of the Asia-Pacific dairy protein industry is propelled by several key drivers. Firstly, increasing consumer awareness regarding the health benefits of protein consumption, including muscle building, satiety, and overall well-being, is a primary catalyst. Secondly, the burgeoning infant nutrition market, driven by high birth rates and a growing demand for premium formulas, significantly contributes to market expansion. Thirdly, the rise of the sports nutrition segment, fueled by the increasing popularity of fitness and athletic activities, is creating sustained demand for high-quality protein ingredients. Fourthly, advancements in processing technologies are enabling the production of specialized and highly functional dairy protein ingredients, catering to diverse application needs. Finally, favorable economic conditions and rising disposable incomes across the region are enabling consumers to opt for protein-enriched food and beverage products.

Challenges in the Asia-Pacific Dairy Protein Industry Sector

Despite its robust growth, the Asia-Pacific dairy protein industry faces several challenges. Fluctuations in raw milk prices due to seasonal variations and geopolitical factors can impact ingredient costs and profit margins. Stringent and evolving regulatory landscapes across different countries, particularly concerning food safety and labeling, necessitate continuous compliance efforts and can lead to increased operational costs. The increasing availability and adoption of plant-based protein alternatives pose a competitive threat, especially in niche markets and among environmentally conscious consumers. Furthermore, supply chain disruptions, exacerbated by logistical complexities and trade barriers in certain regions, can affect the availability and timely delivery of dairy protein ingredients.

Emerging Opportunities in Asia-Pacific Dairy Protein Industry

Emerging opportunities in the Asia-Pacific dairy protein industry lie in catering to evolving consumer demands and leveraging technological advancements. The growing interest in clean label and natural ingredients presents an opportunity for manufacturers to develop minimally processed dairy protein products. The expanding functional food and beverage market, which seeks ingredients with specific health benefits beyond basic nutrition, offers significant potential. Furthermore, the increasing adoption of dairy proteins in the personal care and cosmetics industry, for their moisturizing and skin-conditioning properties, represents a nascent but promising growth avenue. The development of specialized protein formulations for elderly nutrition and medical foods also holds substantial untapped potential.

Leading Players in the Asia-Pacific Dairy Protein Industry Market

- Fonterra Co-operative Group (NZMP)

- Charotar Casein Company

- Hoogwegt

- Interfood Holding

- Foodchem International Corporation

- The Tatua Cooperative Dairy Company Ltd

Key Developments in Asia-Pacific Dairy Protein Industry Industry

- 2023: Fonterra launches a new range of high-purity whey protein isolates targeting the sports nutrition market in Southeast Asia.

- 2022: Hoogwegt expands its distribution network in India to meet the growing demand for dairy ingredients.

- 2021: Foodchem International Corporation invests in advanced membrane filtration technology to enhance its production capacity for milk protein concentrates.

- 2020: The Tatua Cooperative Dairy Company Ltd introduces innovative caseinates for bakery applications, focusing on improved texture and shelf-life.

- 2019: Interfood Holding announces strategic partnerships with regional infant nutrition manufacturers to strengthen its market position.

Strategic Outlook for Asia-Pacific Dairy Protein Industry Market

The strategic outlook for the Asia-Pacific dairy protein industry is highly optimistic, driven by sustained demand from a growing, health-conscious population and continuous innovation in product development and application. Key growth catalysts include the ongoing premiumization of food and beverage products, the expansion of sports and performance nutrition, and the increasing adoption of dairy proteins in emerging sectors like personal care. Companies that focus on high-value ingredients, technological advancements, and a deep understanding of regional consumer preferences are best positioned to capitalize on the market's significant future potential and emerging opportunities. Strategic collaborations and investments in sustainable production practices will also be crucial for long-term success.

Asia-Pacific Dairy Protein Industry Segmentation

-

1. Ingredients Type

- 1.1. Milk Protein Concentrates (MPCs)

- 1.2. Whey Protein Concentrates (WPCs)

- 1.3. Milk Protein Isolates (MPIs)

- 1.4. Whey Protein Isolates (WPIs)

- 1.5. Casein and Caseinates

- 1.6. Others

-

2. Application

-

2.1. Food

- 2.1.1. Infant Nutrition

- 2.1.2. Dairy Based Food

- 2.1.3. Bakery, Confectionary and Frozen Desserts

- 2.1.4. Sports and Performance Nutrition

- 2.1.5. Others

- 2.2. Beverage

- 2.3. Personal care & Cosmetics

- 2.4. Animal Feed

-

2.1. Food

Asia-Pacific Dairy Protein Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. Japan

- 1.3. South Korea

- 1.4. India

- 1.5. Australia

- 1.6. New Zealand

- 1.7. Indonesia

- 1.8. Malaysia

- 1.9. Singapore

- 1.10. Thailand

- 1.11. Vietnam

- 1.12. Philippines

Asia-Pacific Dairy Protein Industry Regional Market Share

Geographic Coverage of Asia-Pacific Dairy Protein Industry

Asia-Pacific Dairy Protein Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Ingredients Type

- 5.1.1. Milk Protein Concentrates (MPCs)

- 5.1.2. Whey Protein Concentrates (WPCs)

- 5.1.3. Milk Protein Isolates (MPIs)

- 5.1.4. Whey Protein Isolates (WPIs)

- 5.1.5. Casein and Caseinates

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Food

- 5.2.1.1. Infant Nutrition

- 5.2.1.2. Dairy Based Food

- 5.2.1.3. Bakery, Confectionary and Frozen Desserts

- 5.2.1.4. Sports and Performance Nutrition

- 5.2.1.5. Others

- 5.2.2. Beverage

- 5.2.3. Personal care & Cosmetics

- 5.2.4. Animal Feed

- 5.2.1. Food

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Ingredients Type

- 6. Asia-Pacific Dairy Protein Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Ingredients Type

- 6.1.1. Milk Protein Concentrates (MPCs)

- 6.1.2. Whey Protein Concentrates (WPCs)

- 6.1.3. Milk Protein Isolates (MPIs)

- 6.1.4. Whey Protein Isolates (WPIs)

- 6.1.5. Casein and Caseinates

- 6.1.6. Others

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Food

- 6.2.1.1. Infant Nutrition

- 6.2.1.2. Dairy Based Food

- 6.2.1.3. Bakery, Confectionary and Frozen Desserts

- 6.2.1.4. Sports and Performance Nutrition

- 6.2.1.5. Others

- 6.2.2. Beverage

- 6.2.3. Personal care & Cosmetics

- 6.2.4. Animal Feed

- 6.2.1. Food

- 6.1. Market Analysis, Insights and Forecast - by Ingredients Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Fonterra Co-operative Group (NZMP)

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Charotar Casein Company*List Not Exhaustive

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Hoogwegt

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Interfood Holding

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Foodchem International Corporation

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 The Tatua Cooperative Dairy Company Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.1 Fonterra Co-operative Group (NZMP)

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Asia-Pacific Dairy Protein Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Asia-Pacific Dairy Protein Industry Share (%) by Company 2025

List of Tables

- Table 1: Asia-Pacific Dairy Protein Industry Revenue billion Forecast, by Ingredients Type 2020 & 2033

- Table 2: Asia-Pacific Dairy Protein Industry Volume K Units Forecast, by Ingredients Type 2020 & 2033

- Table 3: Asia-Pacific Dairy Protein Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 4: Asia-Pacific Dairy Protein Industry Volume K Units Forecast, by Application 2020 & 2033

- Table 5: Asia-Pacific Dairy Protein Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Asia-Pacific Dairy Protein Industry Volume K Units Forecast, by Region 2020 & 2033

- Table 7: Asia-Pacific Dairy Protein Industry Revenue billion Forecast, by Ingredients Type 2020 & 2033

- Table 8: Asia-Pacific Dairy Protein Industry Volume K Units Forecast, by Ingredients Type 2020 & 2033

- Table 9: Asia-Pacific Dairy Protein Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 10: Asia-Pacific Dairy Protein Industry Volume K Units Forecast, by Application 2020 & 2033

- Table 11: Asia-Pacific Dairy Protein Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Asia-Pacific Dairy Protein Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 13: China Asia-Pacific Dairy Protein Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: China Asia-Pacific Dairy Protein Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 15: Japan Asia-Pacific Dairy Protein Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Japan Asia-Pacific Dairy Protein Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 17: South Korea Asia-Pacific Dairy Protein Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: South Korea Asia-Pacific Dairy Protein Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 19: India Asia-Pacific Dairy Protein Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: India Asia-Pacific Dairy Protein Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 21: Australia Asia-Pacific Dairy Protein Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Australia Asia-Pacific Dairy Protein Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 23: New Zealand Asia-Pacific Dairy Protein Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: New Zealand Asia-Pacific Dairy Protein Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 25: Indonesia Asia-Pacific Dairy Protein Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Indonesia Asia-Pacific Dairy Protein Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 27: Malaysia Asia-Pacific Dairy Protein Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Malaysia Asia-Pacific Dairy Protein Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 29: Singapore Asia-Pacific Dairy Protein Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Singapore Asia-Pacific Dairy Protein Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 31: Thailand Asia-Pacific Dairy Protein Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Thailand Asia-Pacific Dairy Protein Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 33: Vietnam Asia-Pacific Dairy Protein Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Vietnam Asia-Pacific Dairy Protein Industry Volume (K Units) Forecast, by Application 2020 & 2033

- Table 35: Philippines Asia-Pacific Dairy Protein Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Philippines Asia-Pacific Dairy Protein Industry Volume (K Units) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia-Pacific Dairy Protein Industry?

The projected CAGR is approximately 7.6%.

2. Which companies are prominent players in the Asia-Pacific Dairy Protein Industry?

Key companies in the market include Fonterra Co-operative Group (NZMP), Charotar Casein Company*List Not Exhaustive, Hoogwegt, Interfood Holding, Foodchem International Corporation, The Tatua Cooperative Dairy Company Ltd.

3. What are the main segments of the Asia-Pacific Dairy Protein Industry?

The market segments include Ingredients Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.45 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Protein Rich Food and Supplements; Increasing Application of Collagen in Personal Care Products.

6. What are the notable trends driving market growth?

Rising Demand for Whey Protein Concentrate (WPC).

7. Are there any restraints impacting market growth?

Increasing Demand for Plant-Based Protein.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Units.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia-Pacific Dairy Protein Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia-Pacific Dairy Protein Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia-Pacific Dairy Protein Industry?

To stay informed about further developments, trends, and reports in the Asia-Pacific Dairy Protein Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence