Key Insights

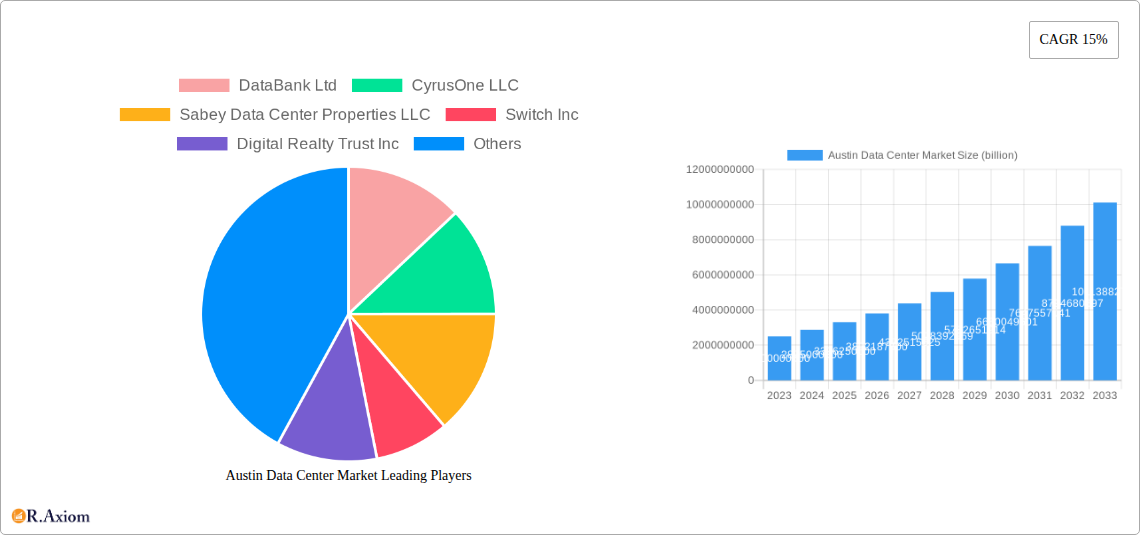

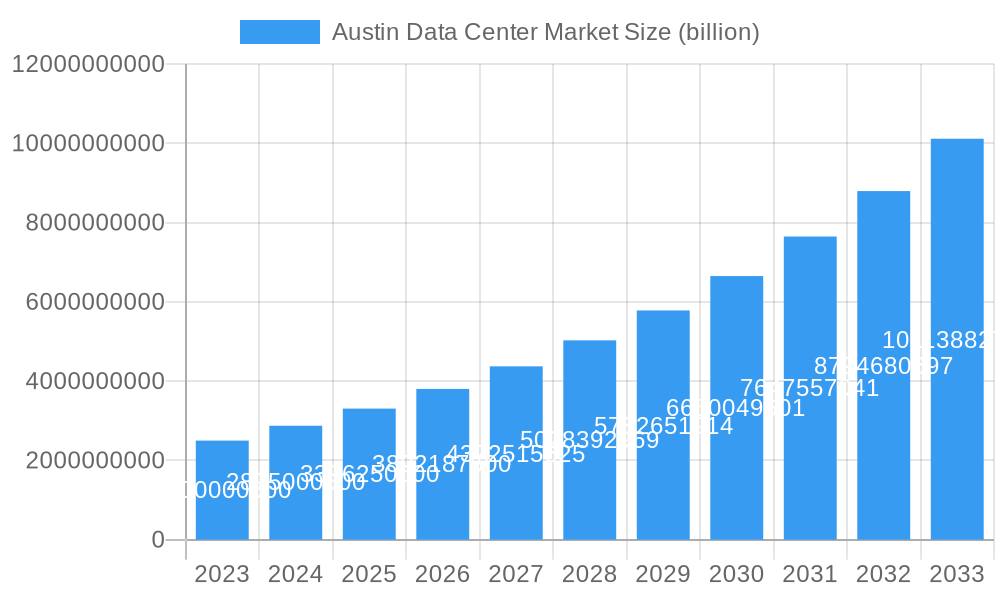

The Austin data center market is experiencing robust expansion, driven by significant technological advancements and a burgeoning digital economy. With a projected market size of $2.5 billion in 2023, the sector is poised for substantial growth, exhibiting a compelling Compound Annual Growth Rate (CAGR) of 15%. This remarkable expansion is fueled by an increasing demand for cloud computing services, the proliferation of 5G technology, and the continuous influx of technology companies and startups to the Austin metropolitan area. Key drivers include the escalating need for hyperscale and enterprise data center capacities to support big data analytics, artificial intelligence (AI), and the Internet of Things (IoT) ecosystems. The adoption of colocation services, particularly wholesale and hyperscale, is a significant trend, as businesses increasingly outsource their IT infrastructure to specialized providers to benefit from cost efficiencies, scalability, and enhanced security. Furthermore, the rising consumption of digital media and entertainment, coupled with the growing presence of BFSI and government entities in the region, is further amplifying the demand for advanced data processing and storage solutions.

Austin Data Center Market Market Size (In Billion)

While the market demonstrates immense potential, certain restraints could influence the pace of growth. The increasing cost of real estate and energy in the Austin area presents a significant hurdle for new developments and expansions. Securing adequate power supply and managing the associated energy costs are critical considerations for data center operators. Additionally, stringent environmental regulations and the growing focus on sustainability may necessitate significant investments in energy-efficient technologies and renewable energy sources. The market is segmented by data center size, encompassing small, medium, large, massive, and mega facilities, each catering to distinct client needs. Tier classifications (Tier 1-4) highlight varying levels of redundancy and uptime, influencing investment decisions. The absorption of capacity through utilized colocation, spanning retail, wholesale, and hyperscale, is a critical metric, alongside the growing non-utilized segment representing future potential. Key end-users like Cloud & IT, Telecom, Media & Entertainment, Government, BFSI, Manufacturing, and E-Commerce are actively shaping the demand landscape. Prominent companies such as DataBank Ltd, CyrusOne LLC, Sabey Data Center Properties LLC, Switch Inc, and Digital Realty Trust Inc are strategically positioning themselves to capitalize on Austin's dynamic data center market.

Austin Data Center Market Company Market Share

Austin Data Center Market Report: Comprehensive Analysis & Future Outlook (2019-2033)

This in-depth report offers a detailed examination of the Austin Data Center Market, providing critical insights for industry stakeholders, investors, and technology providers. Covering the period from 2019 to 2033, with a base and estimated year of 2025 and a forecast period extending to 2033, this analysis delves into market dynamics, growth drivers, segmentation, and competitive landscapes. The report leverages high-traffic keywords such as "Austin data center," "colocation," "hyperscale," "cloud computing," "digital infrastructure," and "Texas data center market" to ensure optimal search visibility. We present a comprehensive overview of the market, including detailed segmentation by DC Size (Small, Medium, Large, Massive, Mega), Tier Type (Tier 1 & 2, Tier 3, Tier 4), and Absorption (Utilized – Colocation Type: Retail, Wholesale, Hyperscale; End User: Cloud & IT, Telecom, Media & Entertainment, Government, BFSI, Manufacturing, E-Commerce, Other End User; Non-Utilized).

Austin Data Center Market Market Concentration & Innovation

The Austin data center market exhibits a dynamic concentration landscape, driven by significant innovation and strategic investments. Key players like DataBank Ltd, CyrusOne LLC, Sabey Data Center Properties LLC, Switch Inc, and Digital Realty Trust Inc are actively shaping the market through expansion and technological advancements. Innovation in cooling technologies, power efficiency, and AI-driven management systems are crucial differentiators. Regulatory frameworks, while supportive of growth, necessitate adherence to environmental and construction standards. Product substitutes, such as on-premises server rooms, are steadily being replaced by the scalability and cost-effectiveness of colocation and cloud solutions. End-user trends clearly point towards increasing demand for hyperscale facilities driven by cloud adoption and the burgeoning digital economy. Mergers and acquisitions (M&A) activities are expected to intensify as larger entities seek to consolidate their presence and acquire specialized capabilities, with M&A deal values projected to reach billions. Market share is influenced by capacity, connectivity, and service offerings, with hyperscale providers currently holding a significant portion of the utilized space.

Austin Data Center Market Industry Trends & Insights

The Austin data center market is poised for substantial growth, fueled by a confluence of powerful industry trends and emerging insights. The accelerated adoption of cloud computing services across all sectors is a primary growth driver, with businesses increasingly migrating their IT infrastructure to off-premise solutions for enhanced flexibility, scalability, and cost efficiency. The proliferation of 5G technology and the subsequent explosion in data generation from IoT devices are creating an insatiable demand for localized processing and storage, thereby boosting the need for robust data center infrastructure. Furthermore, the booming technology and startup ecosystem in Austin, often dubbed the "Silicon Hills," continues to attract significant investment and foster innovation, leading to a sustained demand for high-performance computing and colocation services.

Technological disruptions, including advancements in artificial intelligence, machine learning, and edge computing, are not only increasing the complexity and density of workloads but also necessitating more sophisticated and energy-efficient data center designs. Consumer preferences are shifting towards solutions that offer higher levels of security, reliability, and sustainability. Equinix's pledge to increase operating temperatures within its data centers, as announced in December 2022, exemplifies this trend towards environmental consciousness and operational efficiency, aiming to reduce carbon footprints for both the provider and its thousands of customers. This move aligns with a broader industry push towards greener IT practices.

The competitive dynamics within the Austin data center market are intensifying, with both established global players and regional providers vying for market share. The market penetration of advanced data center solutions is steadily increasing, as more businesses recognize the strategic advantages of leveraging specialized infrastructure. The Compound Annual Growth Rate (CAGR) for the Austin data center market is projected to be in the high single digits to low double digits over the forecast period, indicating a robust and sustained expansion trajectory. This growth is underpinned by a strong economic environment in Texas and Austin's status as a hub for innovation and digital transformation, attracting continuous investment in new facilities and expansions.

Dominant Markets & Segments in Austin Data Center Market

The Austin data center market’s dominance is characterized by a clear hierarchy across various segments, driven by distinct economic policies, infrastructure development, and evolving end-user demands.

DC Size:

- Massive and Mega facilities are emerging as dominant forces, catering to the insatiable demands of hyperscale cloud providers and large enterprises. The need for vast computing power and storage for big data analytics, AI/ML workloads, and global cloud services dictates the preference for these large-scale deployments.

- Large facilities continue to hold significant market share, serving a broad spectrum of wholesale colocation clients and mid-to-large enterprises requiring dedicated space and power.

- Medium and Small facilities cater to the retail colocation needs of small to medium-sized businesses (SMBs), startups, and specialized applications requiring flexible and scalable deployments.

Tier Type:

- Tier 3 and Tier 4 facilities are increasingly dominating the market, particularly for mission-critical applications. The inherent redundancy, fault tolerance, and uptime guarantees offered by these higher-tier facilities are paramount for industries such as BFSI, Government, and Cloud & IT, where service continuity is non-negotiable.

- While Tier 1 & 2 facilities may exist for less critical operations, the trend is a strong preference for the enhanced reliability and availability of Tier 3 and Tier 4 certifications.

Absorption:

- Utilized Absorption:

- Hyperscale Colocation is the most significant driver of absorption, with major cloud providers (e.g., AWS, Google Cloud, Microsoft Azure) expanding their presence to support their vast customer bases and internal operations. This segment consumes the largest percentage of available capacity.

- Wholesale Colocation is a substantial segment, providing dedicated space, power, and cooling to larger enterprises, content delivery networks (CDNs), and service providers.

- Retail Colocation serves a diverse range of clients, from SMBs to enterprises requiring flexible rack space and managed services.

- End User Dominance:

- Cloud & IT sector is the paramount end-user, representing the largest share of data center utilization due to the widespread adoption of cloud services and the continuous expansion of IT infrastructure.

- BFSI (Banking, Financial Services, and Insurance) and Government sectors are significant consumers, demanding high levels of security, compliance, and uptime for their critical operations.

- Telecom providers are essential for network connectivity and the expansion of 5G infrastructure, driving demand for edge data center solutions.

- Media & Entertainment and E-Commerce sectors show robust growth, fueled by streaming services, digital content creation, and online retail.

- Manufacturing and Other End User segments are also contributing to the demand as digital transformation initiatives proliferate across industries.

- Non-Utilized: While a healthy level of non-utilized capacity is essential for market flexibility and accommodating new demand, the trend is towards decreasing vacancy rates as demand outpaces new supply in key segments.

- Utilized Absorption:

Austin Data Center Market Product Developments

Product developments in the Austin data center market are characterized by a focus on enhanced performance, sustainability, and intelligent management. Innovations in high-density computing solutions, advanced cooling techniques like liquid cooling, and modular data center designs are gaining traction. Competitive advantages are being forged through the integration of AI for predictive maintenance and energy optimization, as well as the development of secure, scalable, and low-latency network architectures. The market is also seeing the introduction of specialized solutions for emerging technologies such as edge computing and the metaverse, ensuring market fit by addressing the specific needs of these rapidly evolving sectors.

Report Scope & Segmentation Analysis

The Austin Data Center Market is segmented comprehensively across multiple dimensions to provide granular insights. This includes segmentation by DC Size (Small, Medium, Large, Massive, Mega), reflecting varying capacity requirements. Tier Type (Tier 1 & 2, Tier 3, Tier 4) segments differentiate facilities based on their redundancy and availability levels, crucial for different application criticality. The Absorption segment is further divided into Utilized and Non-Utilized capacity. Utilized absorption is broken down by Colocation Type (Retail, Wholesale, Hyperscale) and End User (Cloud & IT, Telecom, Media & Entertainment, Government, BFSI, Manufacturing, E-Commerce, Other End User). Growth projections indicate strong upward trends across most segments, with hyperscale and higher-tier facilities experiencing the most rapid expansion. Market sizes are substantial and growing, with competitive dynamics shaped by the strategic investments of leading players and the increasing demand from burgeoning industries within the Austin region.

Key Drivers of Austin Data Center Market Growth

The Austin data center market's growth is propelled by several key factors. Technologically, the pervasive adoption of cloud computing, the expansion of 5G networks, and the rise of AI/ML applications are creating unprecedented demand for data processing and storage. Economically, Austin's robust tech sector, a thriving startup ecosystem, and its status as a growing metropolitan area attract significant investment and enterprise expansion. Regulatory frameworks in Texas are generally supportive of business growth, with initiatives aimed at attracting technology companies and infrastructure development. The increasing volume of data generated by the Internet of Things (IoT) devices further fuels the need for localized and scalable data center solutions, solidifying Austin's position as a critical digital infrastructure hub.

Challenges in the Austin Data Center Market Sector

Despite its strong growth trajectory, the Austin data center market faces several challenges. Regulatory hurdles, particularly concerning environmental impact and land use, can sometimes lead to project delays and increased costs. Supply chain issues for critical components and construction materials can affect expansion timelines and overall project feasibility, especially in a rapidly growing market. Intense competitive pressures among established players and new entrants can lead to price sensitivity and the need for continuous innovation to maintain market share. Furthermore, the escalating demand for power and the ongoing efforts to ensure sustainable energy sources present a significant operational and strategic challenge for data center operators in the region.

Emerging Opportunities in Austin Data Center Market

Emerging opportunities in the Austin data center market are abundant, driven by technological advancements and shifting market demands. The burgeoning edge computing market presents a significant opportunity for decentralized data center deployments closer to end-users, supporting latency-sensitive applications like autonomous vehicles and real-time analytics. The increasing demand for specialized colocation services for AI and high-performance computing (HPC) workloads offers a niche for providers with advanced infrastructure capabilities. Sustainability initiatives, including renewable energy integration and advanced cooling technologies, represent a growing market segment for environmentally conscious enterprises. Furthermore, the continued economic growth and influx of businesses into the Austin area create ongoing opportunities for capacity expansion and the provision of new, innovative digital infrastructure solutions.

Leading Players in the Austin Data Center Market Market

- DataBank Ltd

- CyrusOne LLC

- Sabey Data Center Properties LLC

- Switch Inc

- Digital Realty Trust Inc

Key Developments in Austin Data Center Market Industry

- January 2023: NTT intends to build a new data center in Texas. NTT filed for a new data center dubbed 'TX3 Data Centre' with the Texas Department of Licensing and Regulation (TDLR). According to the business, the 230,000 square foot (21,350 square metres) facility includes a data center and a two-story office. The corporation intends to invest USD110 million in the project, which is scheduled to start building in March 2023 and finish in April 2024. This expansion signifies ongoing investment and capacity growth in the Texas region.

- December 2022: Equinix, Inc., the world's digital infrastructure firm, announced the first pledge by a colocation data centre operator to reduce overall power consumption by increasing operating temperature ranges within its data centres. Equinix will begin defining a multi-year global roadmap for thermal operations within its data centres immediately, aiming for much more efficient cooling and lower carbon footprints while maintaining the premium operating environment for which Equinix is recognized. This programme is expected to help thousands of Equinix customers to reduce the Scope 3 carbon emissions connected with their data centre operations over time, as supply chain sustainability becomes an increasingly essential aspect of today's enterprises' total environmental activities. This development highlights a critical industry trend towards sustainability and operational efficiency.

Strategic Outlook for Austin Data Center Market Market

The strategic outlook for the Austin data center market is exceptionally promising, characterized by sustained growth fueled by robust demand from diverse sectors. Future market potential lies in the continued expansion of hyperscale cloud services, the increasing adoption of edge computing solutions, and the growing need for specialized data center capacity to support AI and HPC workloads. Strategic investments in sustainable infrastructure, including renewable energy procurement and energy-efficient cooling technologies, will be crucial for long-term success and competitive advantage. The market is expected to witness further consolidation and strategic partnerships as key players aim to expand their footprints and service offerings, catering to the evolving digital transformation needs of businesses in Austin and beyond.

Austin Data Center Market Segmentation

-

1. DC Size

- 1.1. Small

- 1.2. Medium

- 1.3. Large

- 1.4. Massive

- 1.5. Mega

-

2. Tier Type

- 2.1. Tier 1 & 2

- 2.2. Tier 3

- 2.3. Tier 4

-

3. Absorption

-

3.1. Utilized

-

3.1.1. Colocation Type

- 3.1.1.1. Retail

- 3.1.1.2. Wholesale

- 3.1.1.3. Hyperscale

-

3.1.2. End User

- 3.1.2.1. Cloud & IT

- 3.1.2.2. Telecom

- 3.1.2.3. Media & Entertainment

- 3.1.2.4. Government

- 3.1.2.5. BFSI

- 3.1.2.6. Manufacturing

- 3.1.2.7. E-Commerce

- 3.1.2.8. Other End User

-

3.1.1. Colocation Type

- 3.2. Non-Utilized

-

3.1. Utilized

Austin Data Center Market Segmentation By Geography

- 1. Austin

Austin Data Center Market Regional Market Share

Geographic Coverage of Austin Data Center Market

Austin Data Center Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by DC Size

- 5.1.1. Small

- 5.1.2. Medium

- 5.1.3. Large

- 5.1.4. Massive

- 5.1.5. Mega

- 5.2. Market Analysis, Insights and Forecast - by Tier Type

- 5.2.1. Tier 1 & 2

- 5.2.2. Tier 3

- 5.2.3. Tier 4

- 5.3. Market Analysis, Insights and Forecast - by Absorption

- 5.3.1. Utilized

- 5.3.1.1. Colocation Type

- 5.3.1.1.1. Retail

- 5.3.1.1.2. Wholesale

- 5.3.1.1.3. Hyperscale

- 5.3.1.2. End User

- 5.3.1.2.1. Cloud & IT

- 5.3.1.2.2. Telecom

- 5.3.1.2.3. Media & Entertainment

- 5.3.1.2.4. Government

- 5.3.1.2.5. BFSI

- 5.3.1.2.6. Manufacturing

- 5.3.1.2.7. E-Commerce

- 5.3.1.2.8. Other End User

- 5.3.1.1. Colocation Type

- 5.3.2. Non-Utilized

- 5.3.1. Utilized

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Austin

- 5.1. Market Analysis, Insights and Forecast - by DC Size

- 6. Austin Data Center Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by DC Size

- 6.1.1. Small

- 6.1.2. Medium

- 6.1.3. Large

- 6.1.4. Massive

- 6.1.5. Mega

- 6.2. Market Analysis, Insights and Forecast - by Tier Type

- 6.2.1. Tier 1 & 2

- 6.2.2. Tier 3

- 6.2.3. Tier 4

- 6.3. Market Analysis, Insights and Forecast - by Absorption

- 6.3.1. Utilized

- 6.3.1.1. Colocation Type

- 6.3.1.1.1. Retail

- 6.3.1.1.2. Wholesale

- 6.3.1.1.3. Hyperscale

- 6.3.1.2. End User

- 6.3.1.2.1. Cloud & IT

- 6.3.1.2.2. Telecom

- 6.3.1.2.3. Media & Entertainment

- 6.3.1.2.4. Government

- 6.3.1.2.5. BFSI

- 6.3.1.2.6. Manufacturing

- 6.3.1.2.7. E-Commerce

- 6.3.1.2.8. Other End User

- 6.3.1.1. Colocation Type

- 6.3.2. Non-Utilized

- 6.3.1. Utilized

- 6.1. Market Analysis, Insights and Forecast - by DC Size

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 DataBank Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 CyrusOne LLC

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Sabey Data Center Properties LLC

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Switch Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Digital Realty Trust Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.1 DataBank Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Austin Data Center Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Austin Data Center Market Share (%) by Company 2025

List of Tables

- Table 1: Austin Data Center Market Revenue billion Forecast, by DC Size 2020 & 2033

- Table 2: Austin Data Center Market Revenue billion Forecast, by Tier Type 2020 & 2033

- Table 3: Austin Data Center Market Revenue billion Forecast, by Absorption 2020 & 2033

- Table 4: Austin Data Center Market Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Austin Data Center Market Revenue billion Forecast, by DC Size 2020 & 2033

- Table 6: Austin Data Center Market Revenue billion Forecast, by Tier Type 2020 & 2033

- Table 7: Austin Data Center Market Revenue billion Forecast, by Absorption 2020 & 2033

- Table 8: Austin Data Center Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Austin Data Center Market?

The projected CAGR is approximately 15%.

2. Which companies are prominent players in the Austin Data Center Market?

Key companies in the market include DataBank Ltd, CyrusOne LLC, Sabey Data Center Properties LLC, Switch Inc, Digital Realty Trust Inc.

3. What are the main segments of the Austin Data Center Market?

The market segments include DC Size, Tier Type, Absorption.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.5 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Adoption of Cloud Services is expected to flourish the market; Increasing Growth in Wholesale Datacenter Multi-tenant Spaces to propel demand (albeit from a lower base); Increased Emphasis on Compliance with Data Regulations and Cost-Effective Nature of Multi-tenant Facilities to Drive Adoption among SME's.

6. What are the notable trends driving market growth?

Tier 4 is Expected to Hold Significant Share of the Market.

7. Are there any restraints impacting market growth?

Dependence on Regulatory Landscape & Stringent Security Requirements.

8. Can you provide examples of recent developments in the market?

January 2023 : NTT intends to build a new data center in Texas. NTT filed for a new data center dubbed 'TX3 Data Centre' with the Texas Department of Licensing and Regulation (TDLR) . According to the business, the 230,000 square foot (21,350 square metres) facility includes a data center and a two-story office. The corporation intends to invest USD110 million in the project, which is scheduled to start building in March 2023 and finish in April 2024.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Austin Data Center Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Austin Data Center Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Austin Data Center Market?

To stay informed about further developments, trends, and reports in the Austin Data Center Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence