Key Insights

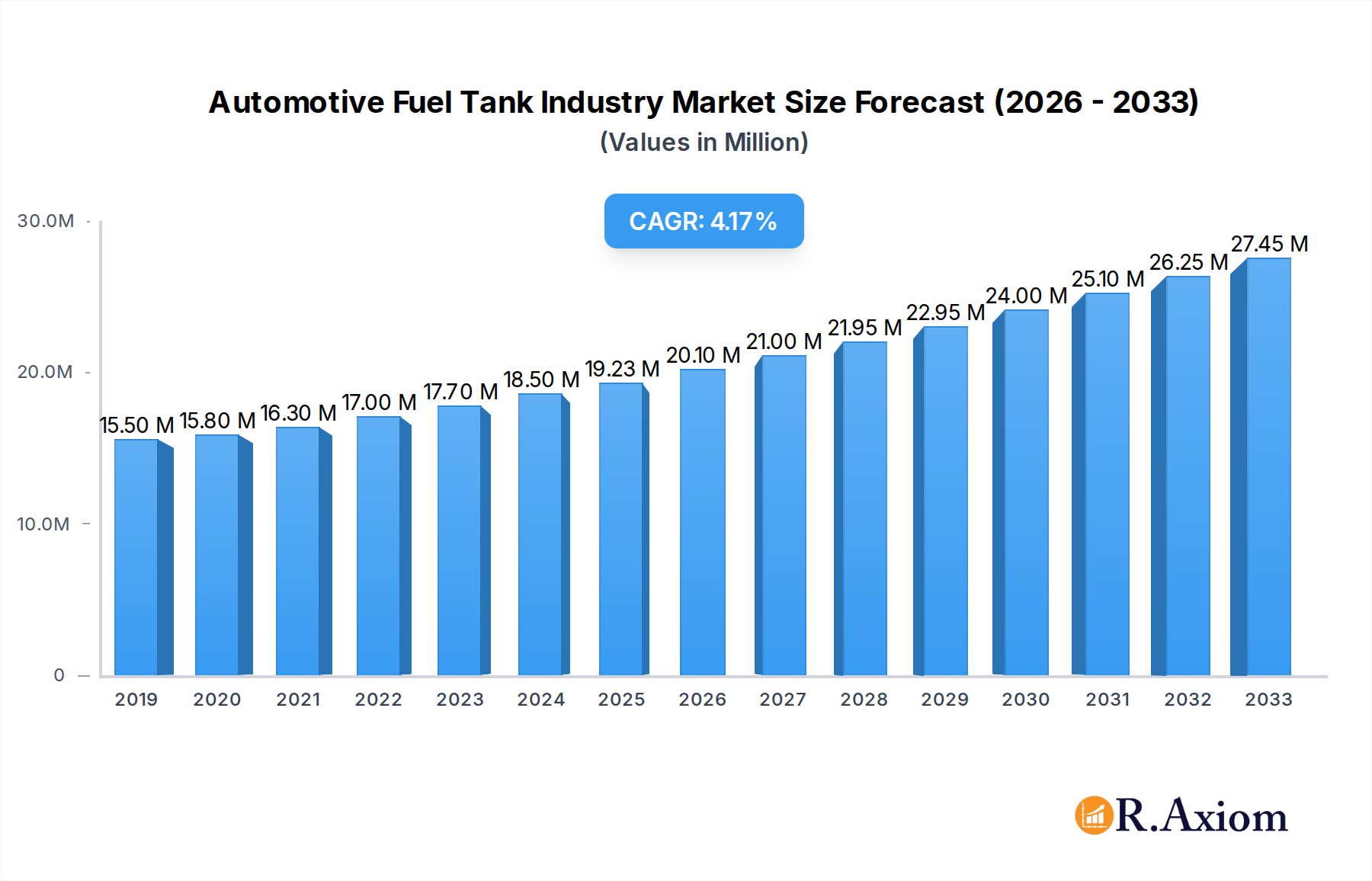

The global automotive fuel tank market is poised for steady expansion, projected to reach a USD 19.23 million valuation by 2025. This growth is underpinned by a compelling CAGR of 4.80%, indicating robust demand and innovation within the sector throughout the forecast period ending in 2033. Key drivers fueling this expansion include the increasing global vehicle production, particularly in emerging economies, and the ongoing integration of advanced fuel tank technologies that enhance safety, durability, and fuel efficiency. Furthermore, evolving regulatory landscapes concerning emissions and fuel containment standards are compelling manufacturers to adopt more sophisticated materials and designs, thereby stimulating market development. The market is segmented into various capacities, catering to diverse vehicle types. The "Above 70 liters" segment, for instance, likely sees significant traction in commercial vehicles and larger passenger cars, while "Less than 45 liters" and "45-70 liters" are crucial for compact and standard passenger vehicles. Material innovation, with plastic tanks offering cost-effectiveness and corrosion resistance, is a prominent trend, though aluminum and steel remain important for specific applications demanding higher structural integrity.

Automotive Fuel Tank Industry Market Size (In Million)

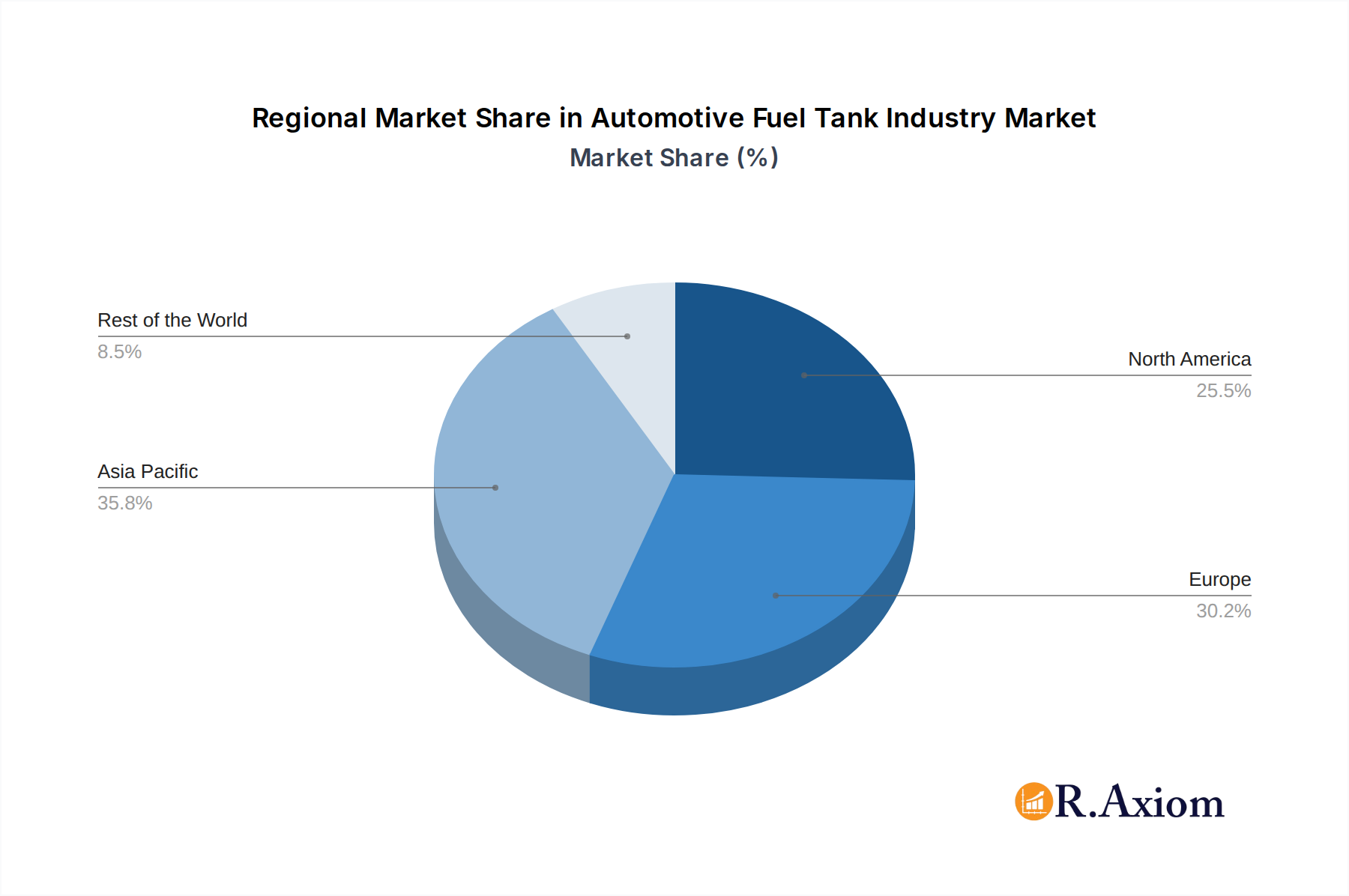

The competitive landscape is characterized by the presence of major global players like Compagnie Plastic Omnium SE, SKH Metals Ltd, and Magna International Inc., who are actively investing in research and development to offer advanced fuel tank solutions. These companies are focusing on lightweighting strategies, improved vapor control systems, and the development of tanks compatible with alternative fuels, which will further shape market dynamics. While the transition towards electric vehicles presents a long-term challenge, the continued dominance of internal combustion engine (ICE) vehicles, especially in certain segments and regions, ensures sustained demand for fuel tanks. Restraints such as fluctuating raw material prices and intense price competition among manufacturers are present, but the overarching demand for safer, more efficient, and compliant fuel systems is expected to drive consistent market growth. The Asia Pacific region, led by China and India, is anticipated to be a significant growth engine due to its massive automotive production and consumption.

Automotive Fuel Tank Industry Company Market Share

This in-depth report provides a comprehensive analysis of the global Automotive Fuel Tank Industry, encompassing market dynamics, trends, competitive landscape, and future projections from 2019 to 2033. The study focuses on a robust understanding of market concentration, innovation drivers, regulatory frameworks, product substitutes, end-user trends, and M&A activities. It also explores key industry trends, dominant markets and segments, product developments, growth drivers, challenges, emerging opportunities, leading players, and strategic outlook. With a base year of 2025 and a forecast period extending to 2033, this report offers actionable insights for stakeholders navigating the evolving automotive fuel tank market. The market is segmented by Capacity (Less than 45 liters, 45-70 liters, Above 70 liters), Material Type (Plastic, Aluminum, Steel), and Vehicle Type (Passenger Cars, Commercial Vehicles).

Automotive Fuel Tank Industry Market Concentration & Innovation

The Automotive Fuel Tank Industry exhibits a moderate level of market concentration, with a few key players holding significant market share. Companies like Compagnie Plastic Omnium SE, Magna International Inc., and TI Fluid Systems PLC are prominent, driving innovation through continuous research and development in lighter materials, enhanced safety features, and improved fuel efficiency. Regulatory frameworks, particularly emissions standards and fuel economy mandates, are significant innovation drivers, pushing manufacturers to develop advanced fuel tank solutions. Product substitutes, while limited for traditional internal combustion engines, are emerging in the form of advanced hydrogen tanks and battery casings for electric vehicles. End-user trends are shifting towards sustainability and safety, influencing the demand for robust and eco-friendly fuel tank materials. Mergers and acquisitions (M&A) activity is observed as companies seek to expand their product portfolios, geographical reach, and technological capabilities. For instance, M&A deal values in the broader automotive components sector often range in the hundreds of millions of dollars, reflecting strategic consolidations aimed at capturing greater market share and innovation synergies. The report details specific M&A activities and their impact on market dynamics, contributing to a concentrated yet evolving industry landscape.

Automotive Fuel Tank Industry Industry Trends & Insights

The Automotive Fuel Tank Industry is experiencing dynamic growth and transformation, driven by a confluence of technological advancements, shifting consumer preferences, and evolving regulatory landscapes. The global market is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 4.5% during the forecast period (2025-2033). This growth is underpinned by the increasing global vehicle production, particularly in emerging economies, and the continuous demand for efficient and safe fuel storage solutions. Technological disruptions are at the forefront, with a notable shift towards lightweight materials like advanced plastics and composite materials to improve fuel economy and reduce vehicle weight. Innovations in plastic fuel tanks, including multi-layer blow molding and advanced barrier technologies, are enhancing their performance and durability. Furthermore, the burgeoning interest in alternative fuel vehicles, such as hydrogen fuel cell vehicles (FCVs) and compressed natural gas (CNG) vehicles, is spurring the development of specialized fuel tank systems. Consumer preferences are increasingly leaning towards vehicles with superior fuel efficiency, enhanced safety features, and a reduced environmental footprint. This trend is directly impacting the demand for innovative fuel tank designs that minimize evaporative emissions and offer robust containment. The competitive dynamics within the industry are characterized by intense R&D efforts, strategic partnerships, and a focus on cost optimization. Market penetration of advanced fuel tank technologies is steadily increasing as automotive manufacturers strive to meet stringent global emission standards and consumer expectations. The industry is also witnessing a growing emphasis on circular economy principles, with a focus on recyclability and sustainability in material selection and manufacturing processes.

Dominant Markets & Segments in Automotive Fuel Tank Industry

The Automotive Fuel Tank Industry exhibits distinct regional and segment dominance, shaped by economic policies, infrastructure development, and vehicle production volumes.

- Dominant Vehicle Type: Passenger Cars currently represent the largest segment within the automotive fuel tank market, driven by their widespread global sales volumes and increasing adoption of advanced fuel tank technologies aimed at improving fuel efficiency. The demand for lightweight plastic fuel tanks is particularly high in this segment.

- Dominant Material Type: Plastic fuel tanks are the leading segment by material type, accounting for an estimated 70% of the market share. Their advantages in terms of weight reduction, design flexibility, corrosion resistance, and cost-effectiveness make them the preferred choice for a majority of passenger cars and light commercial vehicles. Aluminum fuel tanks are gaining traction in niche applications demanding higher structural integrity and specific performance characteristics, while steel tanks, though historically dominant, are increasingly being replaced by lighter alternatives in newer vehicle models.

- Dominant Capacity Segment: The 45-70 liters capacity segment typically holds the largest market share, catering to the fuel storage needs of a broad range of passenger cars and smaller commercial vehicles. This capacity range offers an optimal balance between driving range and vehicle packaging. However, larger capacities (Above 70 liters) are crucial for commercial vehicles and certain long-haul passenger vehicles, representing a significant and growing sub-segment.

- Dominant Region: Asia-Pacific, particularly China and India, is the dominant region in the automotive fuel tank market. This dominance is fueled by the region's massive vehicle production capacity, a burgeoning middle class driving vehicle sales, and favorable government initiatives promoting automotive manufacturing. North America and Europe remain significant markets, driven by stringent emission regulations and a strong focus on technological innovation and the adoption of advanced fuel tank systems.

Key drivers for this regional and segment dominance include:

- Economic Policies: Government incentives for automotive manufacturing and stringent emission regulations in key regions drive demand for compliant and efficient fuel tank solutions.

- Infrastructure Development: The availability of manufacturing facilities and robust supply chains in regions like Asia-Pacific supports large-scale production.

- Vehicle Production Volumes: High vehicle production numbers in key markets directly translate to substantial demand for fuel tanks.

- Technological Adoption: The increasing preference for lightweight and fuel-efficient vehicles accelerates the adoption of advanced materials like plastics.

Automotive Fuel Tank Industry Product Developments

Product development in the Automotive Fuel Tank Industry is intensely focused on enhancing safety, reducing weight, and improving environmental performance. Innovations include the development of advanced composite materials for lighter and stronger fuel tanks, particularly for high-pressure applications like hydrogen fuel cells. Multi-layer plastic fuel tanks with improved barrier properties are being engineered to minimize hydrocarbon emissions, meeting stringent environmental regulations. Furthermore, smart fuel tank technologies incorporating advanced sensors for fuel level monitoring, leak detection, and predictive maintenance are emerging. These developments aim to provide automotive manufacturers with solutions that offer competitive advantages in terms of fuel efficiency, safety compliance, and overall vehicle performance.

Report Scope & Segmentation Analysis

This report meticulously analyzes the Automotive Fuel Tank Industry across the following key segmentation dimensions:

- Capacity: The market is segmented into "Less than 45 liters," "45-70 liters," and "Above 70 liters." The "45-70 liters" segment is expected to maintain its leading position due to its widespread application in passenger cars, while "Above 70 liters" is poised for significant growth driven by commercial vehicle demand.

- Material Type: Segmentation includes "Plastic," "Aluminum," and "Steel." The "Plastic" segment is projected to dominate, driven by its lightweight properties and cost-effectiveness. "Aluminum" is expected to see steady growth due to its high strength-to-weight ratio and corrosion resistance, particularly in specialized applications.

- Vehicle Type: The market is divided into "Passenger Cars" and "Commercial Vehicles." "Passenger Cars" represent the largest segment by volume, while "Commercial Vehicles" offer substantial growth opportunities due to increasing demands for fuel efficiency and heavier payload capacities, requiring robust fuel tank solutions.

Key Drivers of Automotive Fuel Tank Industry Growth

The growth of the Automotive Fuel Tank Industry is propelled by several key factors. Stringent government regulations mandating improved fuel economy and reduced emissions are a primary driver, pushing for lighter and more efficient fuel tank designs. The increasing global demand for vehicles, particularly in emerging economies, directly translates to higher fuel tank production volumes. Technological advancements in material science, leading to the development of lightweight, durable, and cost-effective plastics and composites, are crucial. Furthermore, the growing adoption of alternative fuel vehicles, such as those powered by hydrogen or CNG, is creating new market opportunities for specialized fuel tank systems.

Challenges in the Automotive Fuel Tank Industry Sector

The Automotive Fuel Tank Industry faces several significant challenges. The increasing complexity of vehicle powertrains and the transition towards electric mobility present a long-term challenge to the traditional internal combustion engine fuel tank market. Volatile raw material prices, particularly for plastics and metals, can impact manufacturing costs and profitability. Stringent and evolving safety and environmental regulations necessitate continuous investment in R&D and retooling, adding to production expenses. Intense competition among manufacturers can lead to price pressures. Furthermore, supply chain disruptions, as witnessed globally in recent years, can affect the availability of key raw materials and components.

Emerging Opportunities in Automotive Fuel Tank Industry

Emerging opportunities within the Automotive Fuel Tank Industry are primarily linked to the electrification of vehicles and the development of alternative fuel infrastructure. The demand for lightweight, high-strength fuel tanks for hydrogen fuel cell vehicles (FCVs) presents a significant growth area. As the infrastructure for alternative fuels like CNG expands, the market for compatible fuel tanks will also grow. The development of advanced materials for enhanced safety and emission control in conventional fuel tanks continues to offer opportunities for innovation. Furthermore, the increasing focus on sustainability and recyclability in the automotive sector opens avenues for the development of eco-friendly fuel tank solutions.

Leading Players in the Automotive Fuel Tank Industry Market

- Compagnie Plastic Omnium SE

- SKH Metals Ltd

- Magna International Inc.

- Fuel Total Systems (FTS) Co Ltd

- Aptiv PLC

- YAPP Automotive Systems Co Ltd

- Yachiyo Industry Co Ltd

- Donghee America Inc.

- Sakamoto Industry Co Ltd

- SRD HOLDINGS Ltd

- TI Fluid Systems PLC

- Kautex Textron GmbH & Co KG

Key Developments in Automotive Fuel Tank Industry Industry

- December 2023: Toyota Motor Corporation partnered with UBE Corporation to develop a new type of polyamide 6 resin called UBE NYLON 1218IU. This innovative resin is used for the plastic liner material in the high-pressure hydrogen tank of the new Toyota Crown fuel-cell vehicle (FCV). The nylon 6 resin meets the stringent requirements to prevent any hydrogen leakage in the FCV's high-pressure hydrogen tank.

- November 2023: Robert Bosch GmbH launched H2 Mobility, a new technology that includes a fuel injection system, tank system, exhaust gas treatment system, sensors, and controllers. The technology is equipped with various components, such as an ignition coil, injectors, control unit, rail, DNOX, spark plug, Pr. sensor-EGT, and throttle valve. The company provides H2E technology for long-haul trucks and offers products for different segments, including SUVs, LCVs, coaches, and heavy-duty buses.

Strategic Outlook for Automotive Fuel Tank Industry Market

The strategic outlook for the Automotive Fuel Tank Industry is one of significant adaptation and innovation. The industry will continue to be shaped by the global shift towards sustainable mobility. While the demand for traditional fuel tanks for internal combustion engine vehicles will gradually decline in mature markets, it will remain substantial in emerging economies. The most significant growth catalysts will be the development and mass production of fuel tanks for alternative fuel vehicles, particularly hydrogen FCVs and potentially advanced biofuels. Companies that invest in lightweight materials, advanced manufacturing techniques, and robust safety features will be best positioned for success. Strategic partnerships and collaborations will be crucial for navigating technological complexities and expanding into new markets. The focus will increasingly shift towards integrated fuel system solutions that optimize performance, safety, and environmental compliance.

Automotive Fuel Tank Industry Segmentation

-

1. Capacity

- 1.1. Less than 45 liters

- 1.2. 45-70 liters

- 1.3. Above 70 liters

-

2. Material Type

- 2.1. Plastic

- 2.2. Aluminum

- 2.3. Steel

-

3. Vehicle Type

- 3.1. Passenger Cars

- 3.2. Commercial Vehicles

Automotive Fuel Tank Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Rest of North America

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

-

4. Rest of the World

- 4.1. South America

- 4.2. Middle East and Africa

Automotive Fuel Tank Industry Regional Market Share

Geographic Coverage of Automotive Fuel Tank Industry

Automotive Fuel Tank Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.80% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Capacity

- 5.1.1. Less than 45 liters

- 5.1.2. 45-70 liters

- 5.1.3. Above 70 liters

- 5.2. Market Analysis, Insights and Forecast - by Material Type

- 5.2.1. Plastic

- 5.2.2. Aluminum

- 5.2.3. Steel

- 5.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.3.1. Passenger Cars

- 5.3.2. Commercial Vehicles

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Capacity

- 6. Global Automotive Fuel Tank Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Capacity

- 6.1.1. Less than 45 liters

- 6.1.2. 45-70 liters

- 6.1.3. Above 70 liters

- 6.2. Market Analysis, Insights and Forecast - by Material Type

- 6.2.1. Plastic

- 6.2.2. Aluminum

- 6.2.3. Steel

- 6.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.3.1. Passenger Cars

- 6.3.2. Commercial Vehicles

- 6.1. Market Analysis, Insights and Forecast - by Capacity

- 7. North America Automotive Fuel Tank Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Capacity

- 7.1.1. Less than 45 liters

- 7.1.2. 45-70 liters

- 7.1.3. Above 70 liters

- 7.2. Market Analysis, Insights and Forecast - by Material Type

- 7.2.1. Plastic

- 7.2.2. Aluminum

- 7.2.3. Steel

- 7.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 7.3.1. Passenger Cars

- 7.3.2. Commercial Vehicles

- 7.1. Market Analysis, Insights and Forecast - by Capacity

- 8. Europe Automotive Fuel Tank Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Capacity

- 8.1.1. Less than 45 liters

- 8.1.2. 45-70 liters

- 8.1.3. Above 70 liters

- 8.2. Market Analysis, Insights and Forecast - by Material Type

- 8.2.1. Plastic

- 8.2.2. Aluminum

- 8.2.3. Steel

- 8.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 8.3.1. Passenger Cars

- 8.3.2. Commercial Vehicles

- 8.1. Market Analysis, Insights and Forecast - by Capacity

- 9. Asia Pacific Automotive Fuel Tank Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Capacity

- 9.1.1. Less than 45 liters

- 9.1.2. 45-70 liters

- 9.1.3. Above 70 liters

- 9.2. Market Analysis, Insights and Forecast - by Material Type

- 9.2.1. Plastic

- 9.2.2. Aluminum

- 9.2.3. Steel

- 9.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 9.3.1. Passenger Cars

- 9.3.2. Commercial Vehicles

- 9.1. Market Analysis, Insights and Forecast - by Capacity

- 10. Rest of the World Automotive Fuel Tank Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Capacity

- 10.1.1. Less than 45 liters

- 10.1.2. 45-70 liters

- 10.1.3. Above 70 liters

- 10.2. Market Analysis, Insights and Forecast - by Material Type

- 10.2.1. Plastic

- 10.2.2. Aluminum

- 10.2.3. Steel

- 10.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 10.3.1. Passenger Cars

- 10.3.2. Commercial Vehicles

- 10.1. Market Analysis, Insights and Forecast - by Capacity

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Compagnie Plastic Omnium SE

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 SKH Metals Lt

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Magna International Inc

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Fuel Total Systems (FTS) Co Ltd

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Aptiv PLC

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 YAPP Automotive Systems Co Ltd

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Yachiyo Industry Co Ltd

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Donghee America Inc

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Sakamoto Industry Co Ltd

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 SRD HOLDINGS Ltd

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 TI Fluid Systems PLC

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 Kautex Textron GmbH & Co KG

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.1 Compagnie Plastic Omnium SE

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Automotive Fuel Tank Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Automotive Fuel Tank Industry Revenue (Million), by Capacity 2025 & 2033

- Figure 3: North America Automotive Fuel Tank Industry Revenue Share (%), by Capacity 2025 & 2033

- Figure 4: North America Automotive Fuel Tank Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 5: North America Automotive Fuel Tank Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 6: North America Automotive Fuel Tank Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 7: North America Automotive Fuel Tank Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 8: North America Automotive Fuel Tank Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Automotive Fuel Tank Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Automotive Fuel Tank Industry Revenue (Million), by Capacity 2025 & 2033

- Figure 11: Europe Automotive Fuel Tank Industry Revenue Share (%), by Capacity 2025 & 2033

- Figure 12: Europe Automotive Fuel Tank Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 13: Europe Automotive Fuel Tank Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 14: Europe Automotive Fuel Tank Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 15: Europe Automotive Fuel Tank Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 16: Europe Automotive Fuel Tank Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Europe Automotive Fuel Tank Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Automotive Fuel Tank Industry Revenue (Million), by Capacity 2025 & 2033

- Figure 19: Asia Pacific Automotive Fuel Tank Industry Revenue Share (%), by Capacity 2025 & 2033

- Figure 20: Asia Pacific Automotive Fuel Tank Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 21: Asia Pacific Automotive Fuel Tank Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 22: Asia Pacific Automotive Fuel Tank Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 23: Asia Pacific Automotive Fuel Tank Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 24: Asia Pacific Automotive Fuel Tank Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Asia Pacific Automotive Fuel Tank Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Rest of the World Automotive Fuel Tank Industry Revenue (Million), by Capacity 2025 & 2033

- Figure 27: Rest of the World Automotive Fuel Tank Industry Revenue Share (%), by Capacity 2025 & 2033

- Figure 28: Rest of the World Automotive Fuel Tank Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 29: Rest of the World Automotive Fuel Tank Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 30: Rest of the World Automotive Fuel Tank Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 31: Rest of the World Automotive Fuel Tank Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 32: Rest of the World Automotive Fuel Tank Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: Rest of the World Automotive Fuel Tank Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Fuel Tank Industry Revenue Million Forecast, by Capacity 2020 & 2033

- Table 2: Global Automotive Fuel Tank Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 3: Global Automotive Fuel Tank Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 4: Global Automotive Fuel Tank Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Automotive Fuel Tank Industry Revenue Million Forecast, by Capacity 2020 & 2033

- Table 6: Global Automotive Fuel Tank Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 7: Global Automotive Fuel Tank Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 8: Global Automotive Fuel Tank Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: United States Automotive Fuel Tank Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Canada Automotive Fuel Tank Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Rest of North America Automotive Fuel Tank Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Global Automotive Fuel Tank Industry Revenue Million Forecast, by Capacity 2020 & 2033

- Table 13: Global Automotive Fuel Tank Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 14: Global Automotive Fuel Tank Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 15: Global Automotive Fuel Tank Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Germany Automotive Fuel Tank Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: United Kingdom Automotive Fuel Tank Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: France Automotive Fuel Tank Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Italy Automotive Fuel Tank Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Rest of Europe Automotive Fuel Tank Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Global Automotive Fuel Tank Industry Revenue Million Forecast, by Capacity 2020 & 2033

- Table 22: Global Automotive Fuel Tank Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 23: Global Automotive Fuel Tank Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 24: Global Automotive Fuel Tank Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 25: China Automotive Fuel Tank Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: India Automotive Fuel Tank Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Japan Automotive Fuel Tank Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: South Korea Automotive Fuel Tank Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: Rest of Asia Pacific Automotive Fuel Tank Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Global Automotive Fuel Tank Industry Revenue Million Forecast, by Capacity 2020 & 2033

- Table 31: Global Automotive Fuel Tank Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 32: Global Automotive Fuel Tank Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 33: Global Automotive Fuel Tank Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 34: South America Automotive Fuel Tank Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: Middle East and Africa Automotive Fuel Tank Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Fuel Tank Industry?

The projected CAGR is approximately 4.80%.

2. Which companies are prominent players in the Automotive Fuel Tank Industry?

Key companies in the market include Compagnie Plastic Omnium SE, SKH Metals Lt, Magna International Inc, Fuel Total Systems (FTS) Co Ltd, Aptiv PLC, YAPP Automotive Systems Co Ltd, Yachiyo Industry Co Ltd, Donghee America Inc, Sakamoto Industry Co Ltd, SRD HOLDINGS Ltd, TI Fluid Systems PLC, Kautex Textron GmbH & Co KG.

3. What are the main segments of the Automotive Fuel Tank Industry?

The market segments include Capacity, Material Type, Vehicle Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 19.23 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand for Fuel-efficient Vehicles.

6. What are the notable trends driving market growth?

45-70 Liters Hold Major Market Share.

7. Are there any restraints impacting market growth?

High initial costs may obstruct the growth.

8. Can you provide examples of recent developments in the market?

December 2023: Toyota Motor Corporation partnered with UBE Corporation to develop a new type of polyamide 6 resin called UBE NYLON 1218IU. This innovative resin is used for the plastic liner material in the high-pressure hydrogen tank of the new Toyota Crown fuel-cell vehicle (FCV). The nylon 6 resin meets the stringent requirements to prevent any hydrogen leakage in the FCV's high-pressure hydrogen tank.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Fuel Tank Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Fuel Tank Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Fuel Tank Industry?

To stay informed about further developments, trends, and reports in the Automotive Fuel Tank Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence