Key Insights

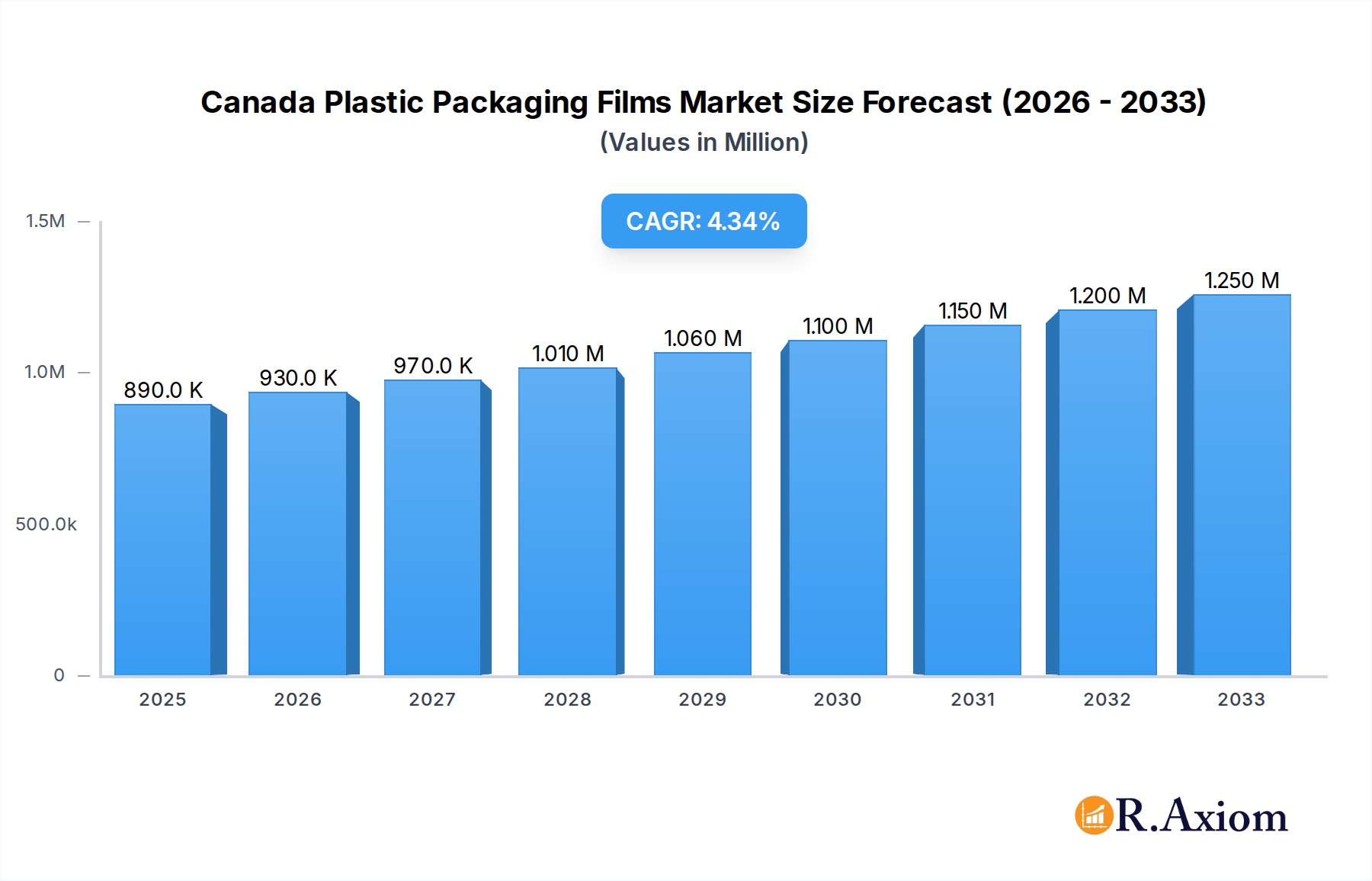

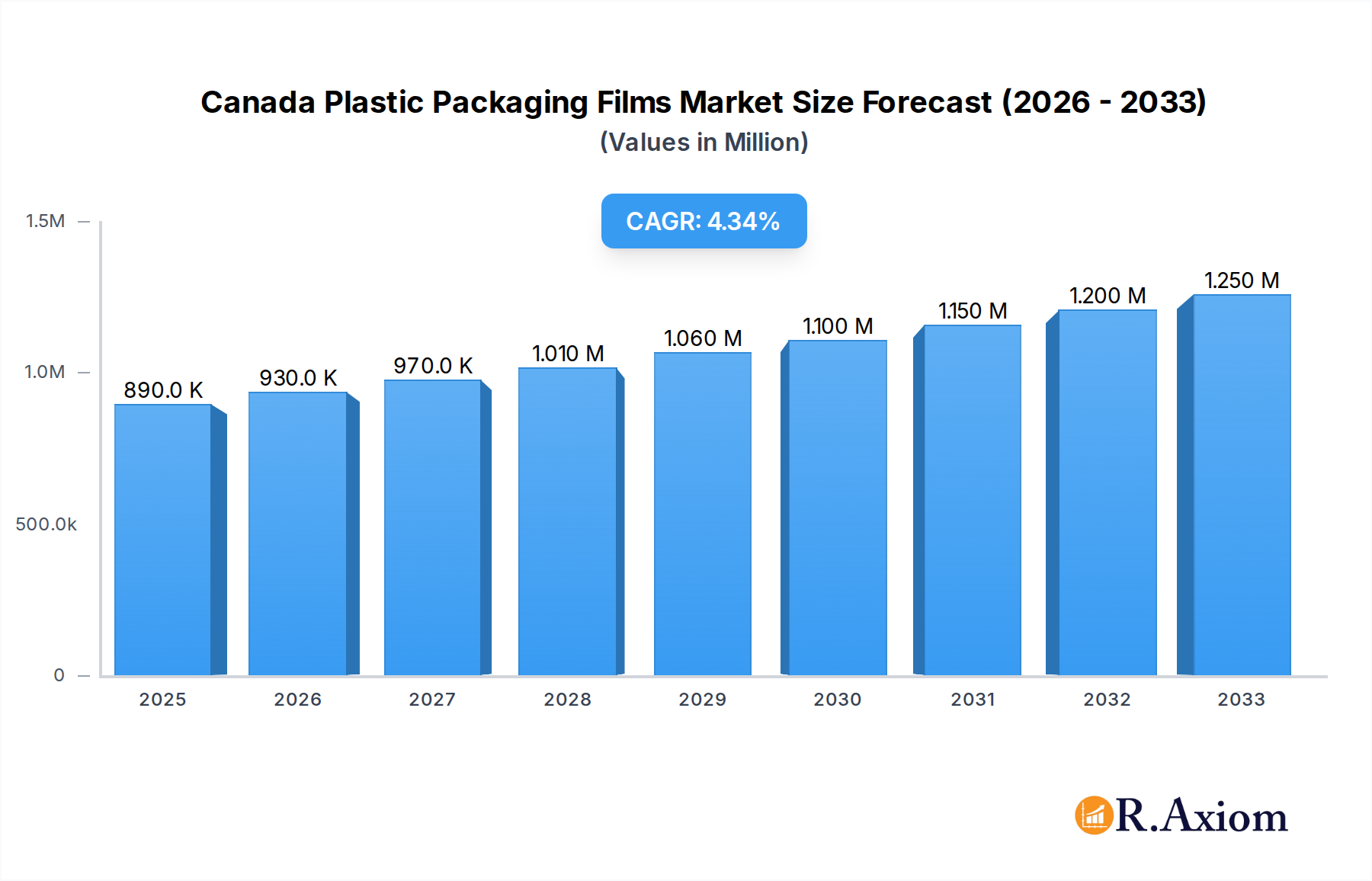

The Canadian plastic packaging films market is poised for robust growth, with an estimated market size of USD 0.89 million in 2025 and a projected Compound Annual Growth Rate (CAGR) of 4.71% through 2033. This expansion is primarily fueled by the escalating demand from the food and beverage sector, which accounts for a significant portion of plastic film consumption due to its excellent barrier properties, shelf-life extension capabilities, and cost-effectiveness for a wide range of products including candy & confectionery, frozen foods, fresh produce, dairy, dry foods, and meat, poultry, and seafood. The healthcare industry also presents a substantial growth avenue, driven by the increasing need for sterile and protective packaging for pharmaceuticals and medical devices. Furthermore, the personal care and home care segments are witnessing a steady rise in demand for flexible plastic films, supporting product innovation and consumer convenience.

Canada Plastic Packaging Films Market Market Size (In Million)

Emerging trends such as the growing consumer preference for sustainable packaging solutions, coupled with increasing regulatory pressure to reduce plastic waste, are shaping the market's evolution. This is driving innovation in bio-based and recyclable plastic films, alongside advancements in thinner yet more durable film technologies. The market's trajectory is also influenced by the industrial packaging sector's need for protective films for various goods during transit and storage. Despite these drivers, potential restraints include fluctuations in raw material prices, particularly for petroleum-based polymers like Polypropylene and Polyethylene, and the ongoing debate and policy shifts surrounding single-use plastics. However, the inherent versatility and cost-effectiveness of plastic films, especially when incorporating enhanced barrier properties through materials like EVOH and PETG, are expected to sustain market momentum.

Canada Plastic Packaging Films Market Company Market Share

Here's a comprehensive and SEO-optimized report description for the Canada Plastic Packaging Films Market:

Canada Plastic Packaging Films Market Market Concentration & Innovation

The Canada Plastic Packaging Films Market is characterized by a moderate level of market concentration, with key players like Amcor Group GmbH, Mondi Plc, and Berry Global Group Inc. holding significant market shares. Innovation within the sector is primarily driven by the escalating demand for sustainable and recyclable packaging solutions, coupled with advancements in film extrusion technologies. Regulatory frameworks, such as extended producer responsibility (EPR) schemes and single-use plastic bans, are actively shaping product development and pushing for greater adoption of bio-based and recycled content films. Product substitutes, including paper-based packaging and reusable containers, pose a growing challenge, necessitating continuous innovation in performance and cost-effectiveness from plastic film manufacturers. End-user trends are heavily influenced by consumer preferences for convenience, food safety, and reduced environmental impact, prompting the development of lightweight, high-barrier films. Mergers and acquisitions (M&A) are a notable strategy for market consolidation and expansion of capabilities, with recent M&A deal values reaching into the tens of millions of dollars as companies seek to bolster their market presence and technological portfolios.

Canada Plastic Packaging Films Market Industry Trends & Insights

The Canada Plastic Packaging Films Market is projected for robust growth, driven by a confluence of compelling industry trends and evolving consumer demands. The market is anticipated to witness a Compound Annual Growth Rate (CAGR) of approximately 4.5% between 2025 and 2033, reflecting a significant expansion in market penetration across various end-user industries. A primary growth driver is the ever-increasing demand from the food and beverage sector, which accounts for a substantial portion of plastic packaging films used for preserving freshness, ensuring safety, and enhancing shelf appeal for a wide array of products, from candy and confectionery to frozen foods, fresh produce, dairy, and meat, poultry, and seafood. The healthcare sector also contributes significantly, requiring specialized films for medical devices, pharmaceuticals, and sterile packaging. Furthermore, the personal care and home care industries rely heavily on plastic films for product containment and consumer-friendly packaging.

Technological disruptions are playing a pivotal role in shaping the market landscape. Innovations in material science are leading to the development of thinner yet stronger films, improved barrier properties to extend shelf life, and enhanced recyclability features. The advent of smart packaging technologies, incorporating features like sensors and indicators, is also gaining traction. Consumer preferences are increasingly shifting towards eco-friendly and sustainable packaging. This has spurred a surge in demand for bio-based and compostable plastic films, as well as films made from recycled content. Manufacturers are responding by investing in advanced recycling technologies and developing circular economy solutions. The competitive dynamics within the market are intense, characterized by strategic partnerships, product differentiation, and a focus on cost efficiency. Companies are vying to capture market share by offering innovative solutions that meet the evolving needs of businesses and consumers alike, while navigating the complexities of environmental regulations and supply chain optimization. The market penetration of advanced plastic packaging films is expected to deepen as the industry embraces sustainability and technological advancements.

Dominant Markets & Segments in Canada Plastic Packaging Films Market

The Canada Plastic Packaging Films Market is experiencing significant growth and diversification across its various segments. Within the Type segmentation, Polyethylene (PE) films, encompassing both LDPE and LLDPE, are demonstrably dominant. This is due to their versatility, cost-effectiveness, and excellent barrier properties, making them indispensable for a wide range of applications.

- Polyethylene (PE): Its dominance stems from its widespread use in flexible packaging for food, agriculture, and industrial applications. Key drivers include its low cost, high flexibility, and good moisture barrier properties.

- Polypropylene (PP): Following closely, PP films are favored for their clarity, heat sealability, and high tensile strength, finding extensive use in food packaging, labels, and textiles.

- PETG: Gaining traction for its excellent clarity, impact resistance, and chemical resistance, PETG is increasingly utilized in healthcare and consumer goods packaging where aesthetic appeal and durability are paramount.

- Bio-Based Films: This segment is experiencing rapid growth, driven by environmental consciousness and regulatory push for sustainable alternatives. Their dominance is expected to increase as production scales up and costs decrease.

- PVC, EVOH, Polystyrene, and Other Film Types: These segments cater to specific niche applications requiring unique properties like high gas barrier (EVOH), rigidity (Polystyrene), or specialized flexibility and clarity (PVC). While smaller in overall market share, they are crucial for specialized packaging needs.

In terms of End-User Industry segmentation, the Food Industry unequivocally dominates the Canadian plastic packaging films market. This dominance is fueled by the continuous and substantial demand for packaging solutions that ensure food safety, extend shelf life, maintain product freshness, and enhance consumer appeal across a broad spectrum of food categories.

- Food Industry:

- Candy & Confectionery: Requires high-clarity films with excellent printability and moisture barrier properties.

- Frozen Foods: Demands films with excellent low-temperature performance and moisture barrier to prevent freezer burn.

- Fresh Produce: Utilizes films that control respiration and moisture to maintain freshness and extend shelf life.

- Dairy Products: Needs films with superior barrier properties against oxygen and moisture to preserve quality and prevent spoilage.

- Dry Foods: Employs films that provide excellent moisture and oxygen barriers to maintain crispness and prevent degradation.

- Meat, Poultry, And Seafood: Requires high-barrier films to prevent oxidation, microbial growth, and maintain color and texture.

- Pet Food: Benefits from films that offer good barrier properties and durability for packaging dry and wet pet food products.

- Healthcare: A critical and growing segment, demanding high-performance films for sterile packaging, medical devices, and pharmaceutical applications, emphasizing barrier integrity and safety.

- Personal Care & Home Care: Relies on films for product containment, aesthetic appeal, and functionality in packaging items like soaps, detergents, and cosmetics.

- Industrial Packaging: Utilizes films for protective wrapping, palletizing, and securing goods during transit, emphasizing strength and durability.

Canada Plastic Packaging Films Market Product Developments

The Canada Plastic Packaging Films Market is witnessing continuous product innovation driven by the demand for enhanced functionality, sustainability, and cost-effectiveness. Key developments include the introduction of advanced multilayer films with improved barrier properties, such as oxygen and moisture resistance, crucial for extending the shelf life of food products. There is also a significant focus on the development of bio-based and biodegradable plastic films derived from renewable resources, directly addressing environmental concerns and regulatory pressures. Furthermore, manufacturers are innovating in the realm of recyclability, creating mono-material films that are easier to sort and reprocess within existing recycling infrastructures. These product advancements aim to provide competitive advantages by meeting stringent performance requirements and aligning with the growing consumer and industry preference for greener packaging solutions.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the Canada Plastic Packaging Films Market, meticulously segmenting it by Type and End-User Industry. The Type segmentation covers Polyprop, Polyethy (further broken down into LDPE and LLDPE), Polystyrene, Bio-Based, PVC, EVOH, PETG, and Other Film Types. The End-User Industry segmentation includes Food (with sub-segments such as Candy & Confectionery, Frozen Foods, Fresh Produce, Dairy Products, Dry Foods, Meat, Poultry, And Seafood, Pet Food, and Other Food), Healthcare, Personal Care & Home Care, Industrial Packaging, and Other End-User Industries. Each segment is analyzed for its market size, growth projections, and competitive dynamics, offering a detailed view of the market's intricate structure and future potential.

Key Drivers of Canada Plastic Packaging Films Market Growth

The growth of the Canada Plastic Packaging Films Market is propelled by several key factors. The ever-increasing demand from the food and beverage industry for packaging that ensures freshness, safety, and extended shelf life remains a primary driver. This is complemented by the growing awareness and preference for sustainable and eco-friendly packaging solutions, which is driving innovation in bio-based and recyclable films. Regulatory mandates and incentives aimed at promoting a circular economy and reducing plastic waste also play a significant role. Furthermore, advancements in material science and extrusion technology are enabling the development of higher-performance, lighter-weight films that offer superior barrier properties and cost efficiencies.

Challenges in the Canada Plastic Packaging Films Market Sector

Despite its growth, the Canada Plastic Packaging Films Market faces several challenges. Stringent regulatory frameworks and evolving environmental policies regarding plastic use and waste management can create compliance burdens and necessitate significant investment in new technologies and materials. Fluctuations in raw material prices, particularly for petrochemical-based resins, can impact production costs and profitability. The increasing competition from alternative packaging materials, such as paper and compostable options, poses a threat to market share. Moreover, complex supply chain dynamics and logistical complexities, especially for specialized films, can lead to delays and increased operational costs.

Emerging Opportunities in Canada Plastic Packaging Films Market

The Canada Plastic Packaging Films Market is ripe with emerging opportunities. The growing demand for sustainable packaging solutions, including films made from recycled content and bio-based materials, presents a significant growth avenue. The expansion of the e-commerce sector is creating opportunities for specialized films that offer enhanced protection and branding capabilities for shipped goods. Furthermore, the healthcare industry's continuous need for sterile and high-barrier packaging provides a stable and growing market. Innovations in smart packaging technologies, offering features like traceability and spoilage indication, also represent a nascent but promising area for market expansion.

Leading Players in the Canada Plastic Packaging Films Market Market

- Amcor Group GmbH

- Mondi Plc

- FLAIR Flexible Packaging Corporation

- C-P Flexible Packaging Inc

- ProAmpac LLC

- Emmerson Packaging Holdings Inc

- Sigma Plastics Group Inc

- Berry Global Group Inc

- Taghleef Industrie

Key Developments in Canada Plastic Packaging Films Market Industry

- January 2024: Revolution Sustainable Solutions, LLC (Revolution) acquired PolyAg Recycling, LTD (PolyAg), a Canadian mechanical recycler of agricultural films. This acquisition significantly enhances Revolution's recycling capacity and expands the company's circular solutions footprint.

- January 2024: The CPP, a cross-industry collaboration focused on promoting circular packaging solutions in Canada, expanded its network by adding key industry leaders, including Restaurants Canada, the Association of Plastic Recyclers (APR), and McDonald’s Canada. Restaurants Canada will collaborate with the CPP to minimize plastic waste and strengthen the foodservice sector's role in advancing a circular economy.

Strategic Outlook for Canada Plastic Packaging Films Market Market

The strategic outlook for the Canada Plastic Packaging Films Market is largely positive, driven by an intensified focus on sustainability and the adoption of circular economy principles. Investments in advanced recycling technologies and the development of high-performance, eco-friendly film solutions will be crucial for market leaders. The increasing collaboration between industry stakeholders, exemplified by initiatives like the CPP, will foster innovation and accelerate the transition towards more sustainable packaging practices. Furthermore, the expanding applications in critical sectors like healthcare and the growing demand from the food industry, coupled with advancements in material science, will continue to fuel market growth, presenting significant opportunities for companies that can adapt to evolving consumer preferences and regulatory landscapes.

Canada Plastic Packaging Films Market Segmentation

-

1. Type

- 1.1. Polyprop

- 1.2. Polyethy

- 1.3. Polyethy

- 1.4. Polystyrene

- 1.5. Bio-Based

- 1.6. PVC, EVOH, PETG, and Other Film Types

-

2. End-User Industry

-

2.1. Food

- 2.1.1. Candy & Confectionery

- 2.1.2. Frozen Foods

- 2.1.3. Fresh Produce

- 2.1.4. Dairy Products

- 2.1.5. Dry Foods

- 2.1.6. Meat, Poultry, And Seafood

- 2.1.7. Pet Food

- 2.1.8. Other Fo

- 2.2. Healthcare

- 2.3. Personal Care & Home Care

- 2.4. Industrial Packaging

- 2.5. Other En

-

2.1. Food

Canada Plastic Packaging Films Market Segmentation By Geography

- 1. Canada

Canada Plastic Packaging Films Market Regional Market Share

Geographic Coverage of Canada Plastic Packaging Films Market

Canada Plastic Packaging Films Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.71% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Polyprop

- 5.1.2. Polyethy

- 5.1.3. Polyethy

- 5.1.4. Polystyrene

- 5.1.5. Bio-Based

- 5.1.6. PVC, EVOH, PETG, and Other Film Types

- 5.2. Market Analysis, Insights and Forecast - by End-User Industry

- 5.2.1. Food

- 5.2.1.1. Candy & Confectionery

- 5.2.1.2. Frozen Foods

- 5.2.1.3. Fresh Produce

- 5.2.1.4. Dairy Products

- 5.2.1.5. Dry Foods

- 5.2.1.6. Meat, Poultry, And Seafood

- 5.2.1.7. Pet Food

- 5.2.1.8. Other Fo

- 5.2.2. Healthcare

- 5.2.3. Personal Care & Home Care

- 5.2.4. Industrial Packaging

- 5.2.5. Other En

- 5.2.1. Food

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Canada

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Canada Plastic Packaging Films Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Polyprop

- 6.1.2. Polyethy

- 6.1.3. Polyethy

- 6.1.4. Polystyrene

- 6.1.5. Bio-Based

- 6.1.6. PVC, EVOH, PETG, and Other Film Types

- 6.2. Market Analysis, Insights and Forecast - by End-User Industry

- 6.2.1. Food

- 6.2.1.1. Candy & Confectionery

- 6.2.1.2. Frozen Foods

- 6.2.1.3. Fresh Produce

- 6.2.1.4. Dairy Products

- 6.2.1.5. Dry Foods

- 6.2.1.6. Meat, Poultry, And Seafood

- 6.2.1.7. Pet Food

- 6.2.1.8. Other Fo

- 6.2.2. Healthcare

- 6.2.3. Personal Care & Home Care

- 6.2.4. Industrial Packaging

- 6.2.5. Other En

- 6.2.1. Food

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Amcor Group GmbH

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Mondi Plc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 FLAIR Flexible Packaging Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 C-P Flexible Packaging Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 ProAmpac LLC

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Emmerson Packaging Holdings Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Sigma Plastics Group Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Berry Global Group Inc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Taghleef Industrie

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Amcor Group GmbH

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Canada Plastic Packaging Films Market Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Canada Plastic Packaging Films Market Share (%) by Company 2025

List of Tables

- Table 1: Canada Plastic Packaging Films Market Revenue million Forecast, by Type 2020 & 2033

- Table 2: Canada Plastic Packaging Films Market Revenue million Forecast, by End-User Industry 2020 & 2033

- Table 3: Canada Plastic Packaging Films Market Revenue million Forecast, by Region 2020 & 2033

- Table 4: Canada Plastic Packaging Films Market Revenue million Forecast, by Type 2020 & 2033

- Table 5: Canada Plastic Packaging Films Market Revenue million Forecast, by End-User Industry 2020 & 2033

- Table 6: Canada Plastic Packaging Films Market Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canada Plastic Packaging Films Market?

The projected CAGR is approximately 4.71%.

2. Which companies are prominent players in the Canada Plastic Packaging Films Market?

Key companies in the market include Amcor Group GmbH, Mondi Plc, FLAIR Flexible Packaging Corporation, C-P Flexible Packaging Inc, ProAmpac LLC, Emmerson Packaging Holdings Inc, Sigma Plastics Group Inc, Berry Global Group Inc, Taghleef Industrie.

3. What are the main segments of the Canada Plastic Packaging Films Market?

The market segments include Type, End-User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 0.89 million as of 2022.

5. What are some drivers contributing to market growth?

E-commerce Growth Drives Plastic Packaging Films Demand in Canada; Rising Appetite for Convenience Foods Spurs Market Growth.

6. What are the notable trends driving market growth?

Polyethylene Segment is Expected to Witness Significant Growth.

7. Are there any restraints impacting market growth?

E-commerce Growth Drives Plastic Packaging Films Demand in Canada; Rising Appetite for Convenience Foods Spurs Market Growth.

8. Can you provide examples of recent developments in the market?

January 2024: Revolution Sustainable Solutions, LLC (Revolution), a United States provider of ESG material solutions, has acquired PolyAg Recycling, LTD (PolyAg), a prominent Canadian mechanical recycler of agricultural films. This acquisition significantly enhances Revolution's recycling capacity and expands the company's circular solutions footprint.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canada Plastic Packaging Films Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canada Plastic Packaging Films Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canada Plastic Packaging Films Market?

To stay informed about further developments, trends, and reports in the Canada Plastic Packaging Films Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence