Key Insights

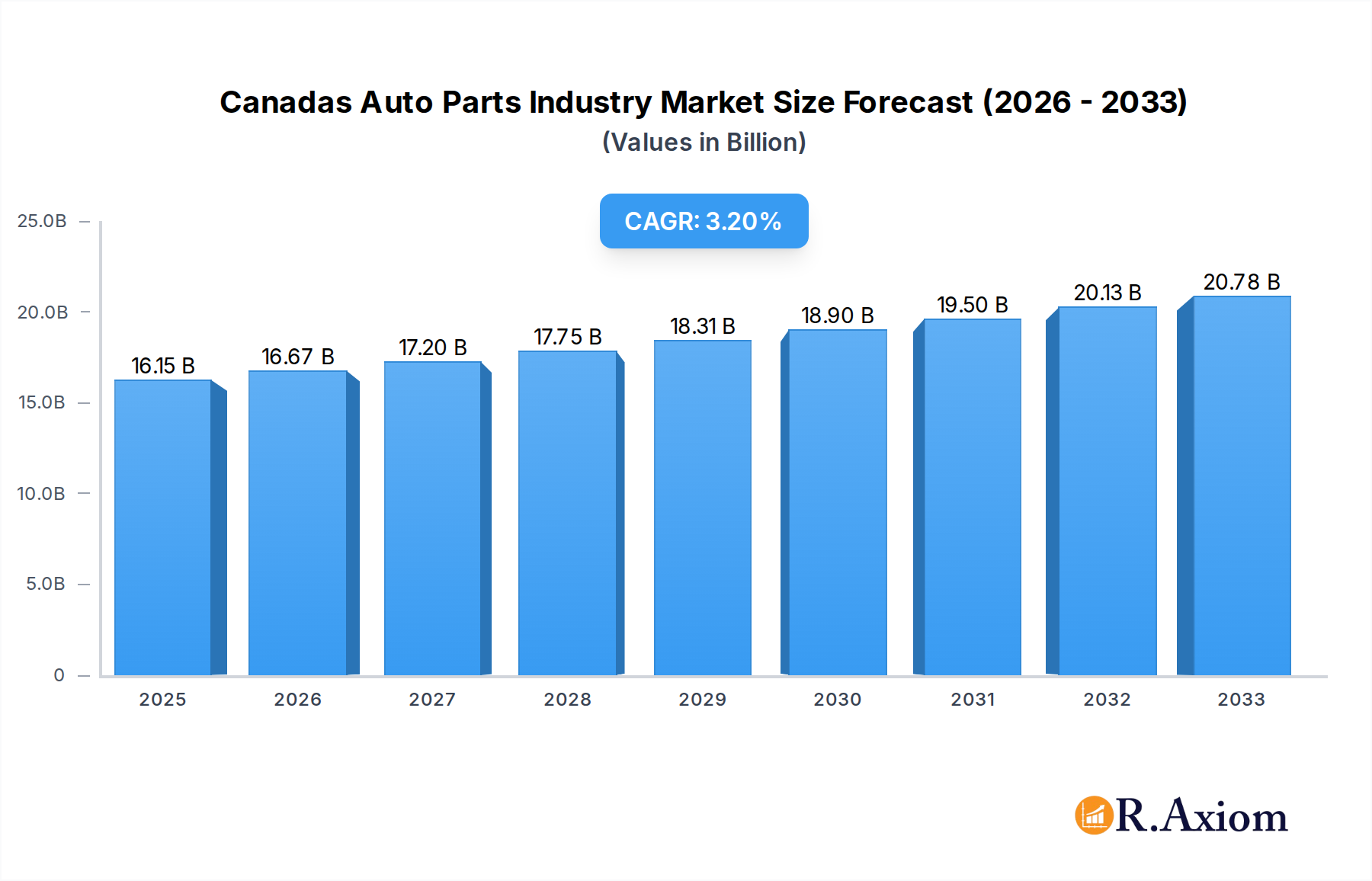

The Canadian automotive parts industry is poised for steady growth, with an estimated market size of $16,152.4 million in 2025. This expansion is fueled by increasing vehicle production and a growing demand for advanced, lightweight, and durable auto components. Key drivers include the rising adoption of electric vehicles (EVs), which necessitates specialized components like battery enclosures and thermal management systems, and the ongoing need for replacement parts as the Canadian vehicle parc ages. Furthermore, advancements in manufacturing technologies, such as sophisticated die casting techniques (Pressure, Vacuum, Squeeze, and Semi-Solid Die Casting), are enhancing efficiency and enabling the production of complex parts with improved performance characteristics. The industry's strategic focus on lightweight materials, including aluminum, zinc, and magnesium, is a critical trend, driven by regulatory pressures for improved fuel efficiency and reduced emissions. These trends collectively contribute to a robust market outlook for Canadian auto parts manufacturers.

Canadas Auto Parts Industry Market Size (In Billion)

The industry's CAGR of 3.2% between 2019 and 2033 indicates a sustainable expansion trajectory. While the market benefits from strong demand across various application types, including body assembly, engine parts, and transmission parts, potential restraints such as volatile raw material prices and intense global competition warrant careful strategic planning. Companies like SYX Die Casting, GIBBS DIE CASTING GROUP, and Endurance Technologies Ltd. are actively involved in shaping this market, investing in research and development and modernizing their production capabilities. The focus on innovation in die casting processes and the utilization of advanced raw materials will be crucial for Canadian players to maintain a competitive edge. Moreover, the evolving landscape of automotive manufacturing, particularly the shift towards smart manufacturing and the integration of Industry 4.0 principles, will further define the future growth and operational strategies within the Canadian auto parts sector.

Canadas Auto Parts Industry Company Market Share

Canadas Auto Parts Industry Market Concentration & Innovation

This comprehensive report delves into the Canadian auto parts industry, analyzing market concentration, innovation drivers, regulatory frameworks, product substitutes, end-user trends, and merger and acquisition (M&A) activities. The Canadian auto parts sector, while experiencing consolidation, remains a dynamic landscape with strategic investments driving innovation. Key players are focusing on advanced manufacturing techniques and sustainable materials to enhance competitiveness. Regulatory bodies are implementing policies to support domestic production and technological advancement, while the threat of product substitutes necessitates continuous product development and differentiation. End-user preferences are shifting towards lighter, more fuel-efficient components, influencing R&D priorities. M&A activities are anticipated to continue as companies seek to expand their capabilities and market reach, with estimated deal values reaching in the hundreds of millions.

- Market Share Dynamics: The top five companies are estimated to hold approximately 65% of the market share, indicating a moderately concentrated industry.

- Innovation Drivers: Focus on lightweight materials, electrification, and advanced manufacturing processes are paramount.

- Regulatory Framework: Government incentives for R&D and emissions reduction play a crucial role.

- Product Substitutes: The emergence of alternative materials and manufacturing methods poses a constant challenge.

- End-User Trends: Increasing demand for EV components and enhanced safety features.

- M&A Activities: Strategic acquisitions and partnerships are expected to reshape the competitive landscape, with potential deal values in the tens to hundreds of millions.

Canadas Auto Parts Industry Industry Trends & Insights

The Canadian auto parts industry is poised for significant growth, driven by a confluence of factors including robust demand for advanced automotive components, increasing adoption of electric vehicles (EVs), and supportive government policies. The projected Compound Annual Growth Rate (CAGR) for the industry is approximately 7.8% over the forecast period of 2025–2033, reflecting a strong upward trajectory. Technological disruptions, particularly in areas like electrification, autonomous driving, and lightweight materials, are reshaping product development and manufacturing processes. Consumer preferences are increasingly aligned with sustainability, fuel efficiency, and advanced safety features, compelling manufacturers to innovate rapidly. Competitive dynamics are intensifying, with both domestic and international players vying for market share. The industry's market penetration is expected to deepen as the automotive sector recovers and expands. Investments in advanced manufacturing, such as the adoption of Industry 4.0 technologies and intelligent automation, are critical for maintaining a competitive edge. The focus on reducing vehicle weight through the use of aluminum and magnesium alloys, for instance, is a prominent trend influencing the types of auto parts being produced. Furthermore, the growing demand for complex, integrated components, rather than individual parts, is driving innovation in assembly and supply chain management. The transition towards greener manufacturing practices, including the use of recycled materials and energy-efficient production, is also becoming a key differentiator. Strategic collaborations and partnerships are crucial for navigating the complex technological landscape and for sharing the substantial R&D costs associated with next-generation automotive technologies. The Canadian government's commitment to supporting the automotive sector through various grants and tax incentives further bolsters the industry's growth prospects, attracting significant investment and fostering innovation. The industry is also seeing a trend towards greater vertical integration by some of the larger players, aiming to control more of the value chain and improve efficiency. The adoption of big data analytics and AI is also on the rise, enabling better predictive maintenance, quality control, and supply chain optimization.

Dominant Markets & Segments in Canadas Auto Parts Industry

The Canadian auto parts industry exhibits dominance across several key segments, driven by a combination of technological advancement, raw material availability, and application demand. Pressure Die Casting stands out as the dominant Production Process Type, accounting for an estimated 75% of the market share due to its efficiency and suitability for high-volume production of intricate metal components. The Aluminum raw material segment also holds significant sway, representing approximately 60% of the market, owing to its lightweight properties and excellent recyclability, which are critical for modern vehicle manufacturing. Within Application Types, Engine Parts command the largest share, estimated at 40%, followed closely by Body Assembly components at 30%, reflecting the ongoing need for critical powertrain and structural elements.

Production Process Type Dominance:

- Pressure Die Casting: Driven by its cost-effectiveness, speed, and ability to produce complex geometries with high precision. This method is essential for components requiring tight tolerances and intricate designs, making it ideal for engine and transmission parts.

- Vacuum Die Casting: Growing in importance for specialized applications requiring enhanced material integrity and reduced porosity, particularly for high-performance engine components.

- Squeeze Die Casting: Emerging for its ability to produce near-net-shape parts with improved mechanical properties, suitable for structural applications and higher-strength engine components.

- Semi-Solid Die Casting: Represents a niche but growing segment, offering unique material properties and design flexibility for advanced applications.

Raw Material Dominance:

- Aluminum: Its lightweight nature is a primary driver, contributing to fuel efficiency and reduced emissions. Economic policies supporting aluminum sourcing and processing in Canada further bolster its position.

- Zinc: Continues to be a significant raw material, particularly for smaller, more intricate components and corrosion-resistant applications.

- Magnesium: Its ultralight properties are increasingly sought after for weight reduction in critical areas, though cost and processing challenges remain.

Application Type Dominance:

- Engine Parts: The fundamental need for pistons, engine blocks, manifolds, and other critical components ensures sustained demand. Technological advancements in engine design, including downsizing and turbocharging, further fuel this segment.

- Body Assembly: Includes a wide array of components from structural elements to exterior panels. The increasing use of aluminum and advanced alloys in body structures is a key growth driver.

- Transmission Parts: Essential for vehicle propulsion, this segment benefits from the complexity and precision required for gears, housings, and other transmission elements.

- Other Applications: Encompasses steering, braking, suspension, and interior components, all of which are experiencing innovation and growth.

Canadas Auto Parts Industry Product Developments

The Canadian auto parts industry is witnessing a wave of product developments centered around lightweighting, electrification, and enhanced performance. Manufacturers are heavily investing in the R&D of advanced aluminum and magnesium alloy components for both internal combustion engine and electric vehicle applications, aiming to reduce vehicle weight and improve fuel efficiency or electric range. The integration of smart technologies into components, such as sensors for predictive maintenance and advanced driver-assistance systems (ADAS), is also a key trend. These innovations offer competitive advantages by meeting stringent regulatory requirements and evolving consumer demands for safer, more sustainable, and technologically advanced vehicles.

Report Scope & Segmentation Analysis

This report provides an in-depth analysis of the Canadian auto parts industry, meticulously segmented to offer granular insights. The Production Process Type segmentation includes: Pressure Die Casting, Vacuum Die Casting, Squeeze Die Casting, and Semi-Solid Die Casting, each examined for its market size, growth projections (estimated CAGR of 7-9%), and competitive landscape. The Raw Material segmentation covers Aluminum, Zinc, Magnesium, and Other Raw Materials, with analysis of their market share (Aluminum estimated at 60%, Zinc at 25%, Magnesium at 10%, Other at 5%), supply chain dynamics, and price volatility. The Application Type segmentation focuses on Body Assembly, Engine Parts, Transmission Parts, and Other Applications, detailing their respective market shares (Engine Parts ~40%, Body Assembly ~30%, Transmission Parts ~20%, Other Applications ~10%), growth drivers, and key end-user demands.

Key Drivers of Canadas Auto Parts Industry Growth

The Canadian auto parts industry's growth is propelled by several key drivers. The increasing global demand for electric vehicles (EVs) is a significant catalyst, driving the need for specialized components like battery enclosures, electric motor housings, and lightweight structural parts. Supportive government policies, including investments in advanced manufacturing and R&D tax credits, foster innovation and attract foreign direct investment. Technological advancements in materials science, enabling the use of lighter and stronger alloys, are crucial for meeting fuel efficiency standards and improving vehicle performance. Furthermore, the ongoing modernization of automotive manufacturing, embracing Industry 4.0 principles and automation, enhances production efficiency and competitiveness.

Challenges in the Canadas Auto Parts Industry Sector

Despite robust growth prospects, the Canadian auto parts industry faces significant challenges. Intense global competition, particularly from low-cost manufacturing regions, puts pressure on profit margins. Supply chain disruptions, exacerbated by geopolitical events and raw material price volatility, can lead to production delays and increased costs. The rapid pace of technological change, especially in electrification and autonomous driving, requires substantial and continuous investment in R&D and workforce retraining, posing a financial and operational hurdle for many small and medium-sized enterprises. Stringent environmental regulations, while driving innovation, also necessitate costly compliance measures.

Emerging Opportunities in Canadas Auto Parts Industry

Emerging opportunities in the Canadian auto parts industry are primarily linked to the global transition towards sustainable mobility and advanced vehicle technologies. The burgeoning electric vehicle market presents a substantial opportunity for manufacturers specializing in battery components, thermal management systems, and lightweight structural parts made from aluminum and magnesium. The increasing adoption of autonomous driving features creates demand for sophisticated sensor integration, specialized electronic components, and advanced chassis systems. Furthermore, the focus on circular economy principles and sustainable manufacturing offers opportunities for companies involved in recycling, remanufacturing, and the use of bio-based or recycled materials.

Leading Players in the Canadas Auto Parts Industry Market

- SYX Die Casting

- GIBBS DIE CASTING GROUP

- CASTWEL AUTOPARTS PVT LTD

- Sunbeam Auto Pvt Ltd

- Sandar Technologies

- Amtek Group

- ECO Die Castings

- Endurance Technologies Ltd

- ALUMINIUM DIE CASTING (CHINA) LTD

- Dynacast Inc

Key Developments in Canadas Auto Parts Industry Industry

- May 2023: Linamar Corporation unveiled plans for a cutting-edge giga casting facility in Welland, Ontario. Spanning approximately 300,000 square feet, the plant will create employment for around 200 workers. The facility will house three 6,100-ton high-pressure die-cast machines, with the first installation scheduled for January 2024. This development signifies a significant investment in advanced manufacturing capabilities and large-scale die casting technology, poised to impact the production of structural components for next-generation vehicles.

- April 2023: Rheinmetall AG and Xiaomi formed a partnership to manufacture triangular beams supporting suspension strut mountings and assembly plates. Production, utilizing high-pressure die casting and special thermal processing, will commence in 2024. The Castings business unit, a 50:50 joint venture between Rheinmetall and HUAYU Automotive Systems (HASCO), a SAIC group subsidiary, will oversee the production process. This collaboration highlights the growing trend of strategic alliances between traditional auto parts manufacturers and technology giants, focusing on advanced materials and integrated solutions for vehicle structures.

Strategic Outlook for Canadas Auto Parts Industry Market

The strategic outlook for the Canadian auto parts industry is highly positive, driven by its adaptability to evolving automotive trends. Investments in advanced manufacturing, particularly in lightweight materials like aluminum and magnesium for EV components, will continue to be a key growth catalyst. The industry's ability to leverage government support for R&D and sustainable practices will solidify its position in the global market. Collaborations with technology firms and a focus on integrated, intelligent automotive solutions will be crucial for capturing future market share. The ongoing expansion of EV production in North America presents a significant opportunity for Canadian suppliers to become integral to the electric mobility supply chain.

Canadas Auto Parts Industry Segmentation

-

1. Production Process Type

- 1.1. Pressure Die Casting

- 1.2. Vacuum Die Casting

- 1.3. Squeeze Die Casting

- 1.4. Semi-Solid Die Casting

-

2. Raw Material

- 2.1. Aluminum

- 2.2. Zinc

- 2.3. Magnesium

- 2.4. Other Raw Materials

-

3. Application Type

- 3.1. Body Assembly

- 3.2. Engine Parts

- 3.3. Transmission Parts

- 3.4. Other Applications

Canadas Auto Parts Industry Segmentation By Geography

- 1. Canada

Canadas Auto Parts Industry Regional Market Share

Geographic Coverage of Canadas Auto Parts Industry

Canadas Auto Parts Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Production Process Type

- 5.1.1. Pressure Die Casting

- 5.1.2. Vacuum Die Casting

- 5.1.3. Squeeze Die Casting

- 5.1.4. Semi-Solid Die Casting

- 5.2. Market Analysis, Insights and Forecast - by Raw Material

- 5.2.1. Aluminum

- 5.2.2. Zinc

- 5.2.3. Magnesium

- 5.2.4. Other Raw Materials

- 5.3. Market Analysis, Insights and Forecast - by Application Type

- 5.3.1. Body Assembly

- 5.3.2. Engine Parts

- 5.3.3. Transmission Parts

- 5.3.4. Other Applications

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Canada

- 5.1. Market Analysis, Insights and Forecast - by Production Process Type

- 6. Canadas Auto Parts Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Production Process Type

- 6.1.1. Pressure Die Casting

- 6.1.2. Vacuum Die Casting

- 6.1.3. Squeeze Die Casting

- 6.1.4. Semi-Solid Die Casting

- 6.2. Market Analysis, Insights and Forecast - by Raw Material

- 6.2.1. Aluminum

- 6.2.2. Zinc

- 6.2.3. Magnesium

- 6.2.4. Other Raw Materials

- 6.3. Market Analysis, Insights and Forecast - by Application Type

- 6.3.1. Body Assembly

- 6.3.2. Engine Parts

- 6.3.3. Transmission Parts

- 6.3.4. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Production Process Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 SYX Die Casting

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 GIBBS DIE CASTING GROUP

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 CASTWEL AUTOPARTS PVT LTD

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Sunbeam Auto Pvt Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Sandar Technologies

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Amtek Group

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 ECO Die Castings

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Endurance Technologies Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 ALUMINIUM DIE CASTING (CHINA) LTD

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Dynacast Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 SYX Die Casting

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Canadas Auto Parts Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Canadas Auto Parts Industry Share (%) by Company 2025

List of Tables

- Table 1: Canadas Auto Parts Industry Revenue million Forecast, by Production Process Type 2020 & 2033

- Table 2: Canadas Auto Parts Industry Revenue million Forecast, by Raw Material 2020 & 2033

- Table 3: Canadas Auto Parts Industry Revenue million Forecast, by Application Type 2020 & 2033

- Table 4: Canadas Auto Parts Industry Revenue million Forecast, by Region 2020 & 2033

- Table 5: Canadas Auto Parts Industry Revenue million Forecast, by Production Process Type 2020 & 2033

- Table 6: Canadas Auto Parts Industry Revenue million Forecast, by Raw Material 2020 & 2033

- Table 7: Canadas Auto Parts Industry Revenue million Forecast, by Application Type 2020 & 2033

- Table 8: Canadas Auto Parts Industry Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canadas Auto Parts Industry?

The projected CAGR is approximately 3.2%.

2. Which companies are prominent players in the Canadas Auto Parts Industry?

Key companies in the market include SYX Die Casting, GIBBS DIE CASTING GROUP, CASTWEL AUTOPARTS PVT LTD, Sunbeam Auto Pvt Ltd, Sandar Technologies, Amtek Group, ECO Die Castings, Endurance Technologies Ltd, ALUMINIUM DIE CASTING (CHINA) LTD, Dynacast Inc.

3. What are the main segments of the Canadas Auto Parts Industry?

The market segments include Production Process Type, Raw Material, Application Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 16152.4 million as of 2022.

5. What are some drivers contributing to market growth?

Growth of the Automotive Industry to Drive Demand in the Die Casting Market; Growing Focus Toward Fuel Efficiency of IC Engine Vehicle to Drive Demand.

6. What are the notable trends driving market growth?

Automotive Segment will Drive The Market In Coming Year.

7. Are there any restraints impacting market growth?

High Processing Cost May Hamper Market Expansion.

8. Can you provide examples of recent developments in the market?

May 2023: Linamar Corporation unveiled plans for a cutting-edge giga casting facility in Welland, Ontario. Spanning approximately 300,000 square feet, the plant will create employment for around 200 workers. The facility will house three 6,100-ton high-pressure die-cast machines, with the first installation scheduled for January 2024.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canadas Auto Parts Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canadas Auto Parts Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canadas Auto Parts Industry?

To stay informed about further developments, trends, and reports in the Canadas Auto Parts Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence