Key Insights

The Canadian pharmaceutical market, a significant segment of the North American healthcare landscape, is projected to experience robust growth over the forecast period (2025-2033). With a 2025 market size estimated at $15 billion (derived proportionally from the global market size of $33.34 billion and considering Canada's share of the North American market), the industry benefits from a high per capita drug expenditure and a rapidly aging population requiring increased medication. This growth is driven by several factors: the increasing prevalence of chronic diseases like diabetes and cardiovascular conditions, the rising adoption of innovative therapies (e.g., biologics and targeted therapies), and a steady increase in government healthcare spending. Further driving market expansion are ongoing R&D efforts leading to the introduction of new drugs and the growing acceptance of generic drugs, presenting opportunities for both brand-name and generic pharmaceutical companies. However, challenges exist, including stringent regulatory approvals, increasing healthcare costs putting pressure on both government budgets and consumers, and the potential for price controls which could impact profitability.

Market segmentation reveals key trends within the Canadian pharmaceutical industry. The largest segments likely include Alimentary Tract and Metabolism drugs, followed by Cardiovascular System and Nervous System medications. Within drug types, prescription drugs dominate, while the over-the-counter (OTC) market, although smaller, is showing consistent growth due to rising self-medication practices. Major players like Novartis, Merck, Pfizer, and domestic Canadian players, actively participate in this competitive market through strategic partnerships, acquisitions, and the development of new and improved pharmaceutical products. Regional variations are likely to exist across provinces, with larger population centers exhibiting greater demand. The continued focus on innovation, patient access programs, and cost-effective solutions will be crucial for sustained growth and success in the Canadian pharmaceutical market.

Canadian Pharmaceutical Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Canadian pharmaceutical industry, covering market trends, competitive landscape, key players, and future growth prospects. The study period spans from 2019 to 2033, with 2025 serving as the base and estimated year. The forecast period is 2025-2033, and the historical period encompasses 2019-2024. The report uses Millions (M) for all values.

Canadian Pharmaceutical Industry Market Concentration & Innovation

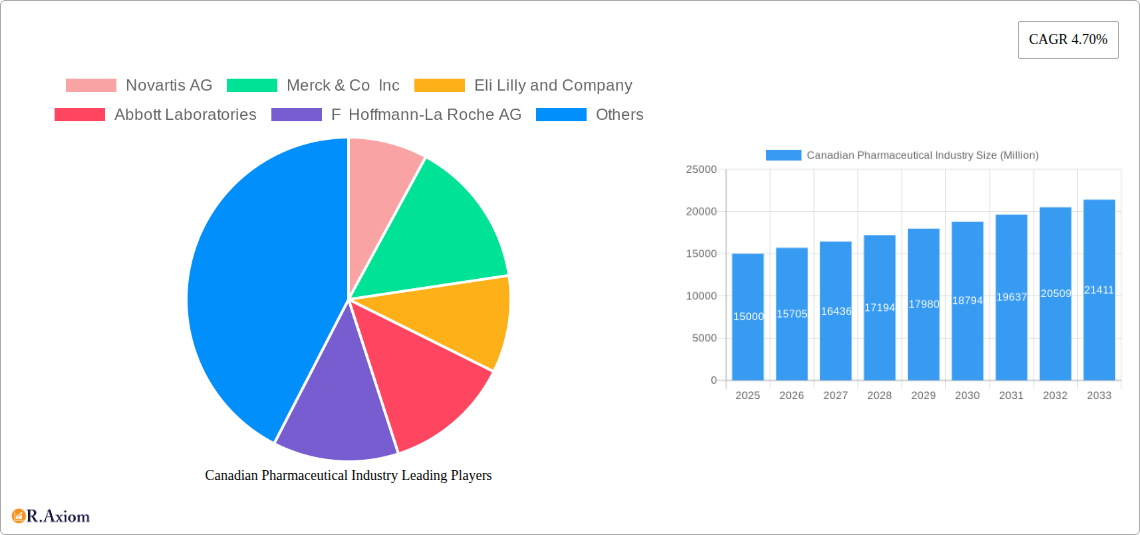

The Canadian pharmaceutical market exhibits a moderately concentrated structure, with a few multinational giants holding significant market share. Companies like Novartis AG, Merck & Co Inc, and Pfizer Inc. command substantial portions of the market, primarily driven by their extensive portfolios of innovative drugs and strong brand recognition. However, the presence of several large domestic players like Apotex Inc. adds a layer of competition. Innovation within the industry is largely driven by the need to address unmet medical needs, comply with stringent regulatory requirements (Health Canada), and compete for market share.

Market share data for 2024 suggests that the top 5 players hold approximately XX% of the market, with a further XX% distributed among the remaining companies. This concentration shows a potential for mergers and acquisitions (M&A) activity and vertical integration. Recent M&A activity has been characterized by a focus on acquiring smaller companies with promising drug pipelines or specialized therapeutic areas. The total value of M&A deals within the Canadian pharmaceutical industry in 2024 was approximately $XX Million.

- Key Drivers of Innovation:

- Stringent regulatory requirements from Health Canada.

- Focus on developing novel therapies for chronic diseases.

- Increasing R&D investment by major pharmaceutical companies.

- Emergence of biosimilars and generics.

- Key M&A Activities (2024):

- [List specific significant M&A deals with deal values if available, otherwise use "XX Million" as a placeholder for value]

Canadian Pharmaceutical Industry Industry Trends & Insights

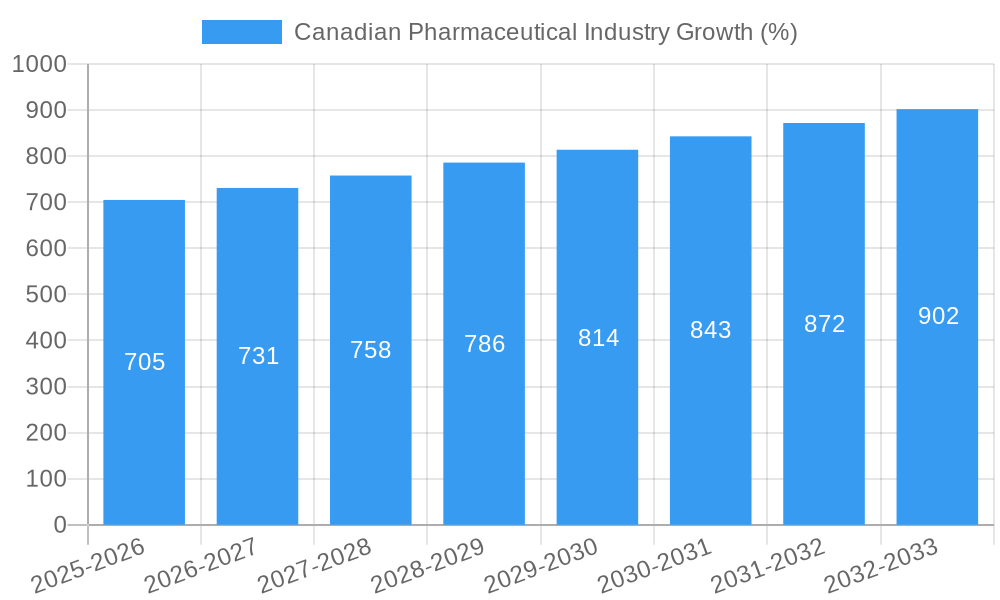

The Canadian pharmaceutical industry is experiencing robust growth, driven by several factors including an aging population, increasing prevalence of chronic diseases, and rising healthcare expenditure. The Compound Annual Growth Rate (CAGR) for the period 2019-2024 is estimated to be around XX%, with projections indicating a CAGR of XX% for the forecast period (2025-2033). Market penetration of innovative drugs is gradually increasing with approximately XX% of the market accounted for by new drugs in 2024. Technological disruptions are evident, particularly in areas such as personalized medicine, targeted therapies, and digital health. Consumer preferences are shifting towards convenient drug delivery formats and greater access to information. This, in turn, impacts competitive dynamics within the industry. Competition amongst generics and biosimilars is intensifying, putting pressure on pricing and profit margins for brand-name drugs. Moreover, growing emphasis on value-based healthcare is influencing drug development strategies and pricing negotiations. The increase in digital adoption and telehealth initiatives is also shaping industry trends, creating new opportunities while requiring strategic adaptation.

Dominant Markets & Segments in Canadian Pharmaceutical Industry

The Canadian pharmaceutical market is geographically concentrated, with the majority of sales occurring in urban centers with high population densities. By therapeutic area, several segments exhibit strong growth.

By ATC/Therapeutic Class:

- Antineoplastic and Immunomodulating Agents: This segment shows significant growth due to the rising incidence of cancer and the emergence of innovative targeted therapies.

- Cardiovascular System: This remains a dominant segment driven by the high prevalence of cardiovascular diseases in Canada's aging population.

- Nervous System: This segment is also experiencing strong growth due to the increasing incidence of neurological disorders, such as Alzheimer's disease.

By Drug Type:

- Prescription Drugs: This remains the largest segment, driven by the continued prevalence of chronic and acute diseases. The growth of this segment is further propelled by an expanding population and escalating healthcare spending.

- Generic Drugs: This segment is experiencing strong growth, driven by increasing affordability and the expiry of patents on many brand-name drugs.

Key Drivers:

- Economic Policies: Government healthcare funding and policies influence drug pricing and reimbursement.

- Infrastructure: Robust healthcare infrastructure supports the distribution and usage of pharmaceuticals.

- Demographics: Canada's aging population drives demand for medications for chronic conditions.

Canadian Pharmaceutical Industry Product Developments

Recent product developments in the Canadian pharmaceutical industry showcase a strong focus on novel therapies and improved drug delivery systems. The launch of biosimilars and generics contributes to increased affordability and accessibility, while innovations in targeted therapies enhance treatment efficacy and reduce side effects. Technological advancements such as personalized medicine and advanced diagnostics are transforming drug development and influencing market dynamics. A shift towards more patient-centric approaches is being observed, with a focus on enhancing patient adherence and overall healthcare outcomes.

Report Scope & Segmentation Analysis

This report segments the Canadian pharmaceutical market by ATC/Therapeutic Class (Alimentary Tract and Metabolism, Blood and Blood-forming Organs, Cardiovascular System, Dermatologicals, Genito Urinary System and Sex Hormones, Systemic Hormonal Preparations, Antiinfectives for Systemic Use, Antineoplastic and Immunomodulating Agents, Musculoskeletal System, Nervous System, Antiparasitic Products, Insecticides, and Repellents, Respiratory System, Sensory Organs, Various Other ATC/Therapeutic Classes) and Drug Type (Prescription, Generic, OTC Drugs). Each segment’s market size, growth projections, and competitive dynamics are analyzed in detail. For example, the Antineoplastic and Immunomodulating Agents segment is projected to grow at a CAGR of XX% during the forecast period, driven by increasing cancer incidence and technological advancements in treatment. The Generic Drugs segment is expected to witness significant growth owing to patent expiries and rising affordability.

Key Drivers of Canadian Pharmaceutical Industry Growth

Several key factors are driving the growth of the Canadian pharmaceutical industry, including:

- Aging population: Increasing prevalence of age-related diseases.

- Technological advancements: Development of innovative therapies and drug delivery systems.

- Rising healthcare expenditure: Increased government and private spending on healthcare.

- Favorable regulatory environment: Supportive policies for drug development and approval.

Challenges in the Canadian Pharmaceutical Industry Sector

The Canadian pharmaceutical industry faces several challenges, including:

- High drug prices: Influenced by factors including the cost of research and development, patent protection, and regulatory requirements.

- Stringent regulatory hurdles: Lengthy approval processes for new drugs, impacting market entry timelines and overall cost effectiveness.

- Supply chain vulnerabilities: Potential disruptions caused by global events or manufacturing issues.

- Intense competition: Pressure from generic and biosimilar manufacturers.

Emerging Opportunities in Canadian Pharmaceutical Industry

The Canadian pharmaceutical market presents several exciting opportunities, including:

- Personalized medicine: Tailoring treatments to individual patients based on genetic and other factors.

- Digital health: Utilizing technology to improve patient care and medication management.

- Biosimilars and generics: Increasing competition leading to more affordable drug options.

- Expansion into new therapeutic areas: Opportunities in developing medications for previously unmet needs.

Leading Players in the Canadian Pharmaceutical Industry Market

- Novartis AG

- Merck & Co Inc

- Eli Lilly and Company

- Abbott Laboratories

- F Hoffmann-La Roche AG

- Apotex Inc

- AbbVie Inc

- Bristol Myers Squibb Company

- Johnson & Johnson

- Pfizer Inc

Key Developments in Canadian Pharmaceutical Industry Industry

- October 2023: Panacea Biotec launched Paclitaxel protein-bound particles for injectable suspension (albumin-bound) for metastatic breast cancer, non-small cell lung cancer, and adenocarcinoma of the pancreas, through Apotex Inc. This expands treatment options for these cancers in Canada.

- March 2023: Natco Pharma introduced a generic version of Pomalidomide Capsules, the first generic alternative to Celgene Corporation’s Pomalyst, approved by Health Canada for multiple myeloma treatment. This increases affordability and access for patients.

Strategic Outlook for Canadian Pharmaceutical Industry Market

The Canadian pharmaceutical industry is poised for continued growth, driven by factors such as an aging population, advancements in medical technology, and increasing healthcare spending. The focus on innovation, personalized medicine, and digital health will play a pivotal role in shaping the industry's future. Opportunities exist for companies to capitalize on the increasing demand for affordable and effective medications and advanced treatment modalities, while addressing challenges associated with regulation, pricing, and competition. The strategic implementation of value-based healthcare models will necessitate a shift towards outcomes-based pricing and collaborative partnerships within the healthcare ecosystem.

Canadian Pharmaceutical Industry Segmentation

-

1. ATC/Therapeutic Class

- 1.1. Alimentary Tract and Metabolism

- 1.2. Blood and Blood-forming Organs

- 1.3. Cardiovascular System

- 1.4. Dermatologicals

- 1.5. Genito Urinary System and Sex Hormones

- 1.6. Systemic Hormonal Preparations

- 1.7. Antiinfectives for Systemic Use

- 1.8. Antineoplastic and Immunomodulating Agents

- 1.9. Musculoskeletal System

- 1.10. Nervous System

- 1.11. Antipara

- 1.12. Respiratory System

- 1.13. Sensory Organs

- 1.14. Various Other ATC/Therapeutic Classes

- 1.15. Others

-

2. Drug Type

-

2.1. By Prescription Type

- 2.1.1. Branded

- 2.1.2. Generic

- 2.2. OTC Drugs

-

2.1. By Prescription Type

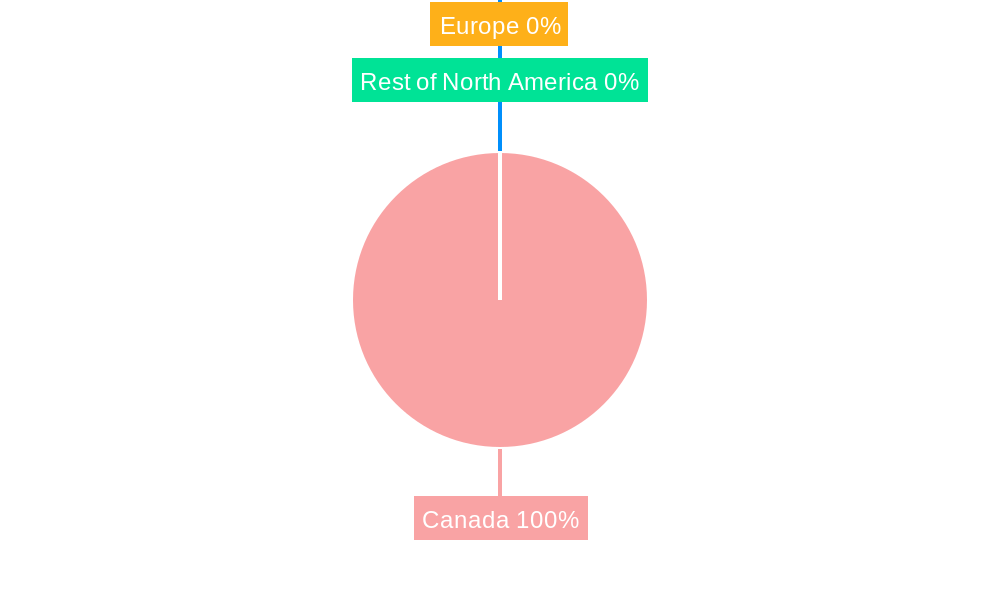

Canadian Pharmaceutical Industry Segmentation By Geography

- 1. Canada

Canadian Pharmaceutical Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.70% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rising Geriatric Population; Rising Incidence of Chronic Disease

- 3.3. Market Restrains

- 3.3.1. Highly Expensive Drugs

- 3.4. Market Trends

- 3.4.1. The Alimentary Tract and Metabolism Segment is Expected to Register Significant Growth Over the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Canadian Pharmaceutical Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by ATC/Therapeutic Class

- 5.1.1. Alimentary Tract and Metabolism

- 5.1.2. Blood and Blood-forming Organs

- 5.1.3. Cardiovascular System

- 5.1.4. Dermatologicals

- 5.1.5. Genito Urinary System and Sex Hormones

- 5.1.6. Systemic Hormonal Preparations

- 5.1.7. Antiinfectives for Systemic Use

- 5.1.8. Antineoplastic and Immunomodulating Agents

- 5.1.9. Musculoskeletal System

- 5.1.10. Nervous System

- 5.1.11. Antipara

- 5.1.12. Respiratory System

- 5.1.13. Sensory Organs

- 5.1.14. Various Other ATC/Therapeutic Classes

- 5.1.15. Others

- 5.2. Market Analysis, Insights and Forecast - by Drug Type

- 5.2.1. By Prescription Type

- 5.2.1.1. Branded

- 5.2.1.2. Generic

- 5.2.2. OTC Drugs

- 5.2.1. By Prescription Type

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Canada

- 5.1. Market Analysis, Insights and Forecast - by ATC/Therapeutic Class

- 6. North America Canadian Pharmaceutical Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 6.1.1 United States

- 6.1.2 Canada

- 6.1.3 Mexico

- 7. Europe Canadian Pharmaceutical Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 7.1.1 Germany

- 7.1.2 United Kingdom

- 7.1.3 France

- 7.1.4 Italy

- 7.1.5 Spain

- 7.1.6 Rest of Europe

- 8. Asia Pacific Canadian Pharmaceutical Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 8.1.1 China

- 8.1.2 Japan

- 8.1.3 India

- 8.1.4 Australia

- 8.1.5 South Korea

- 8.1.6 Rest of Asia Pacific

- 9. Middle East and Africa Canadian Pharmaceutical Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 9.1.1 GCC

- 9.1.2 South Africa

- 9.1.3 Rest of Middle East and Africa

- 10. South America Canadian Pharmaceutical Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 10.1.1 Brazil

- 10.1.2 Argentina

- 10.1.3 Rest of South America

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Novartis AG

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Merck & Co Inc

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Eli Lilly and Company

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Abbott Laboratories

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 F Hoffmann-La Roche AG

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Apotex Inc

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 AbbVie Inc

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Bristol Myers Squibb Company

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Johnson & Johnson

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Pfizer Inc

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Novartis AG

List of Figures

- Figure 1: Global Canadian Pharmaceutical Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America Canadian Pharmaceutical Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: North America Canadian Pharmaceutical Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe Canadian Pharmaceutical Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe Canadian Pharmaceutical Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Pacific Canadian Pharmaceutical Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Pacific Canadian Pharmaceutical Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: Middle East and Africa Canadian Pharmaceutical Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: Middle East and Africa Canadian Pharmaceutical Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: South America Canadian Pharmaceutical Industry Revenue (Million), by Country 2024 & 2032

- Figure 11: South America Canadian Pharmaceutical Industry Revenue Share (%), by Country 2024 & 2032

- Figure 12: Canada Canadian Pharmaceutical Industry Revenue (Million), by ATC/Therapeutic Class 2024 & 2032

- Figure 13: Canada Canadian Pharmaceutical Industry Revenue Share (%), by ATC/Therapeutic Class 2024 & 2032

- Figure 14: Canada Canadian Pharmaceutical Industry Revenue (Million), by Drug Type 2024 & 2032

- Figure 15: Canada Canadian Pharmaceutical Industry Revenue Share (%), by Drug Type 2024 & 2032

- Figure 16: Canada Canadian Pharmaceutical Industry Revenue (Million), by Country 2024 & 2032

- Figure 17: Canada Canadian Pharmaceutical Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Canadian Pharmaceutical Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Canadian Pharmaceutical Industry Revenue Million Forecast, by ATC/Therapeutic Class 2019 & 2032

- Table 3: Global Canadian Pharmaceutical Industry Revenue Million Forecast, by Drug Type 2019 & 2032

- Table 4: Global Canadian Pharmaceutical Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Global Canadian Pharmaceutical Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: United States Canadian Pharmaceutical Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Canada Canadian Pharmaceutical Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Mexico Canadian Pharmaceutical Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Global Canadian Pharmaceutical Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 10: Germany Canadian Pharmaceutical Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: United Kingdom Canadian Pharmaceutical Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: France Canadian Pharmaceutical Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Italy Canadian Pharmaceutical Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Spain Canadian Pharmaceutical Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Rest of Europe Canadian Pharmaceutical Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Global Canadian Pharmaceutical Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 17: China Canadian Pharmaceutical Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Japan Canadian Pharmaceutical Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: India Canadian Pharmaceutical Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Australia Canadian Pharmaceutical Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: South Korea Canadian Pharmaceutical Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Rest of Asia Pacific Canadian Pharmaceutical Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Global Canadian Pharmaceutical Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 24: GCC Canadian Pharmaceutical Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: South Africa Canadian Pharmaceutical Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Rest of Middle East and Africa Canadian Pharmaceutical Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Global Canadian Pharmaceutical Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 28: Brazil Canadian Pharmaceutical Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: Argentina Canadian Pharmaceutical Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Rest of South America Canadian Pharmaceutical Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 31: Global Canadian Pharmaceutical Industry Revenue Million Forecast, by ATC/Therapeutic Class 2019 & 2032

- Table 32: Global Canadian Pharmaceutical Industry Revenue Million Forecast, by Drug Type 2019 & 2032

- Table 33: Global Canadian Pharmaceutical Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canadian Pharmaceutical Industry?

The projected CAGR is approximately 4.70%.

2. Which companies are prominent players in the Canadian Pharmaceutical Industry?

Key companies in the market include Novartis AG, Merck & Co Inc, Eli Lilly and Company, Abbott Laboratories, F Hoffmann-La Roche AG, Apotex Inc , AbbVie Inc, Bristol Myers Squibb Company, Johnson & Johnson, Pfizer Inc.

3. What are the main segments of the Canadian Pharmaceutical Industry?

The market segments include ATC/Therapeutic Class, Drug Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 33.34 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Geriatric Population; Rising Incidence of Chronic Disease.

6. What are the notable trends driving market growth?

The Alimentary Tract and Metabolism Segment is Expected to Register Significant Growth Over the Forecast Period.

7. Are there any restraints impacting market growth?

Highly Expensive Drugs.

8. Can you provide examples of recent developments in the market?

October 2023: Panacea Biotec launched Paclitaxel protein-bound particles for injectable suspension (albumin-bound), which is indicated for the treatment of metastatic breast cancer, non-small cell lung cancer, and adenocarcinoma of the pancreas in the Canadian market through its strategic partner, Apotex Inc. of Canada.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canadian Pharmaceutical Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canadian Pharmaceutical Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canadian Pharmaceutical Industry?

To stay informed about further developments, trends, and reports in the Canadian Pharmaceutical Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence