Key Insights

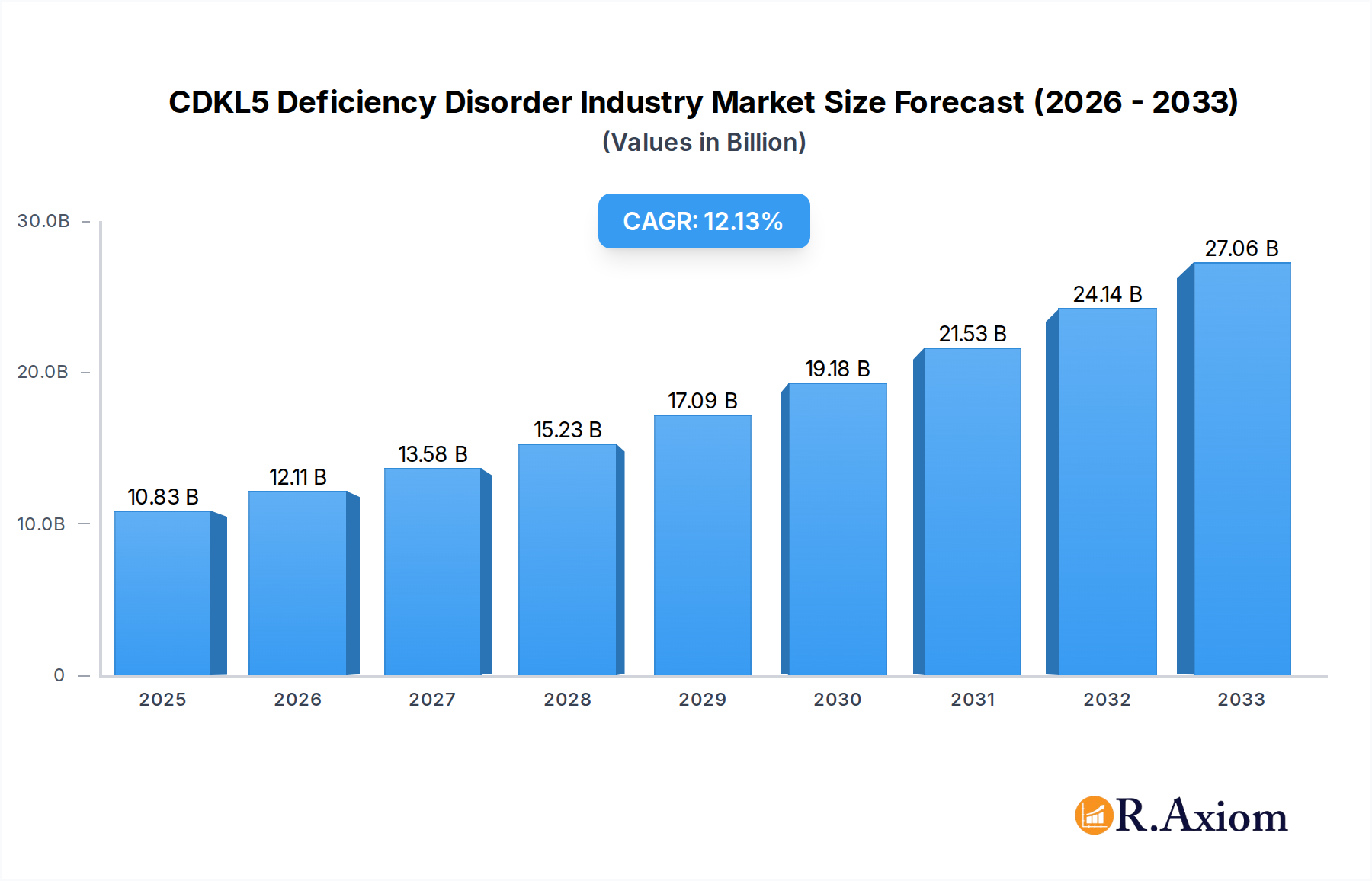

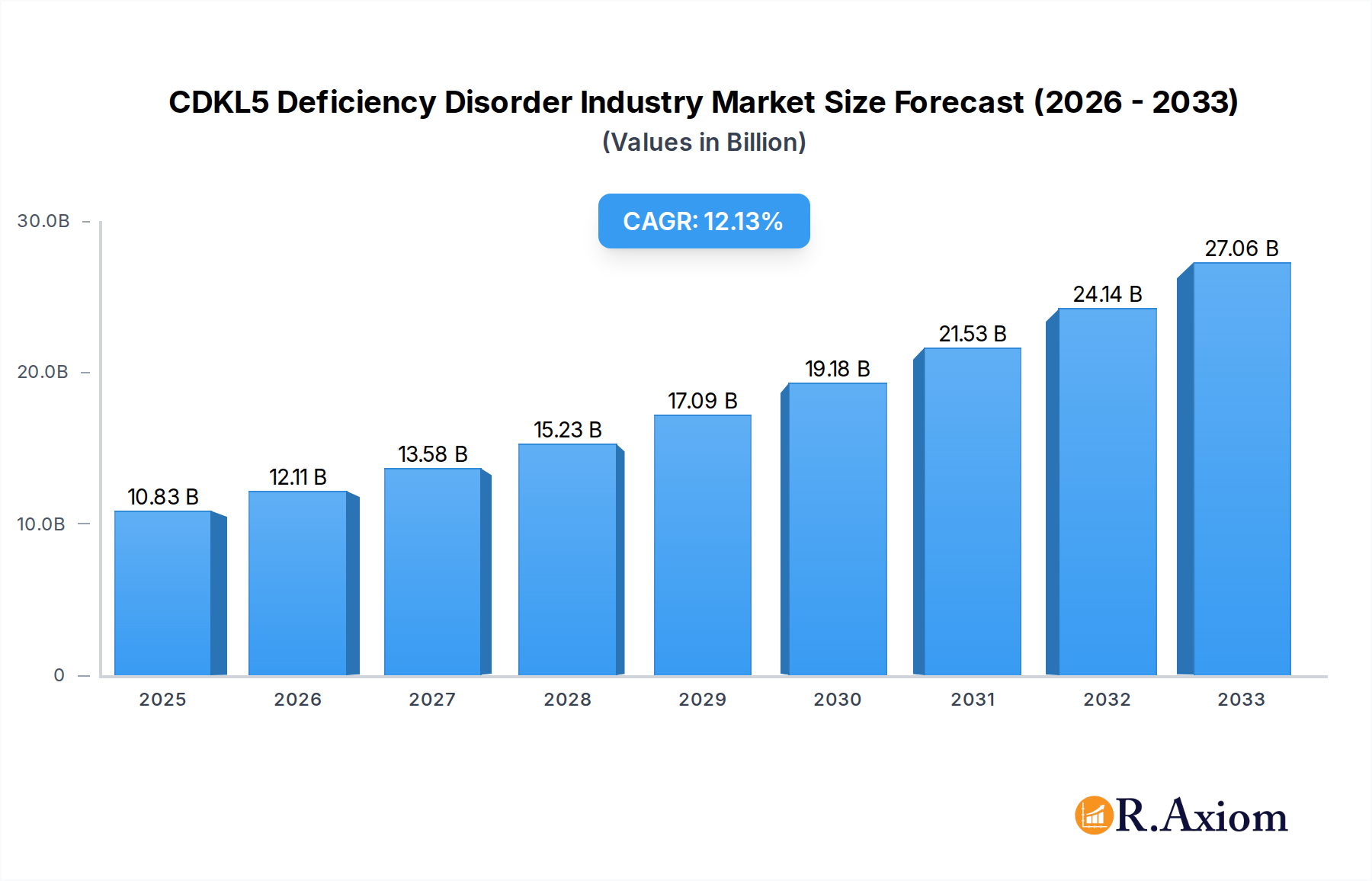

The CDKL5 Deficiency Disorder (CDD) market is poised for substantial growth, projected to reach $10.83 billion by 2025 with a compelling Compound Annual Growth Rate (CAGR) of 11.55% through 2033. This significant expansion is fueled by increasing awareness of rare genetic disorders, advancements in diagnostic capabilities, and a robust pipeline of innovative therapies. The market's trajectory is primarily driven by the growing understanding of CDD's genetic basis and the urgent unmet medical need for effective treatments that can address the severe developmental and neurological challenges faced by affected individuals. The rising investment in rare disease research and development, coupled with supportive regulatory pathways for orphan drugs, further bolsters this optimistic outlook.

CDKL5 Deficiency Disorder Industry Market Size (In Billion)

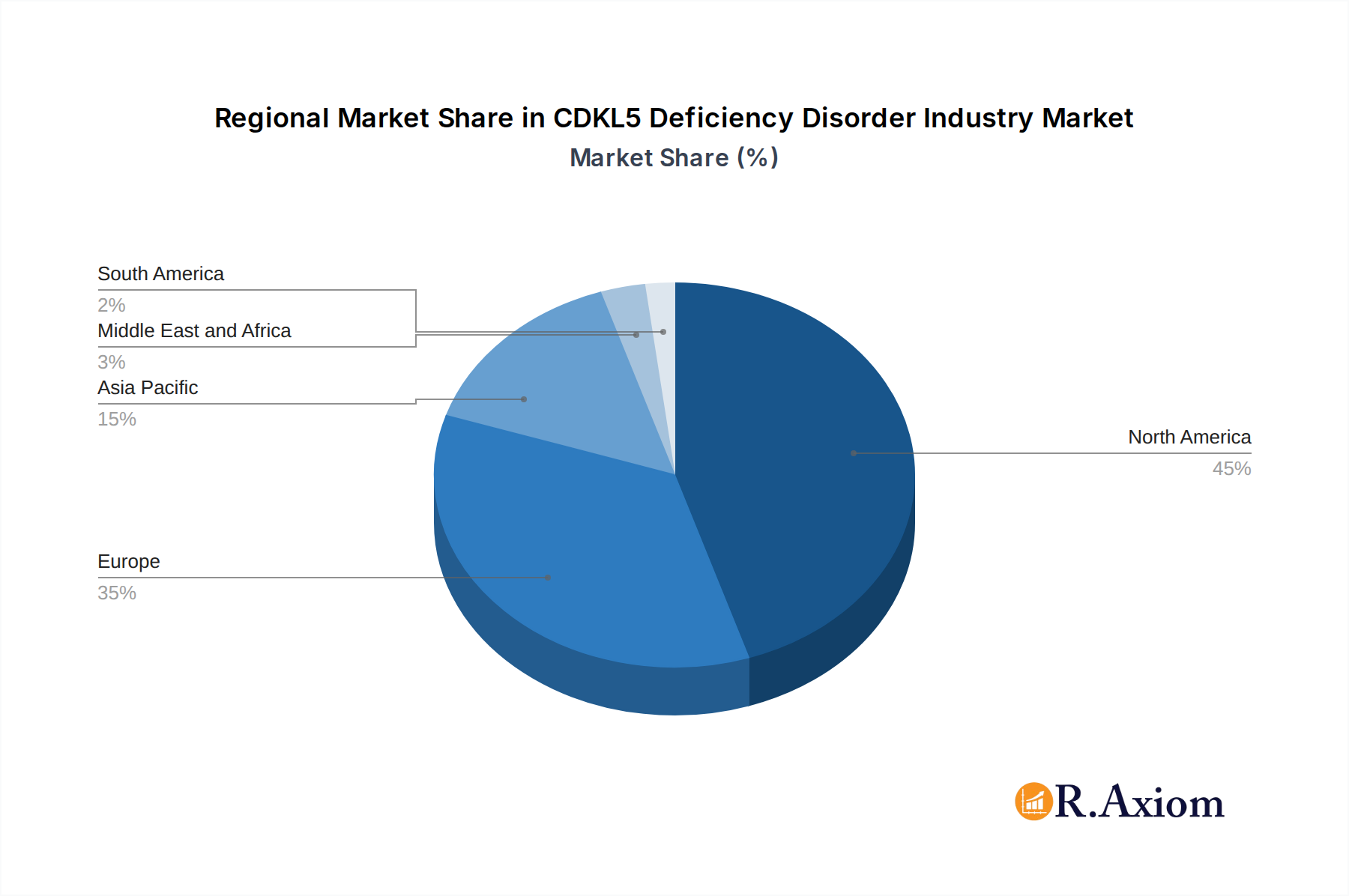

The CDD market is segmented into various therapeutic lines, with the Second Line of Therapy anticipated to witness accelerated growth as more targeted treatments become available. Distribution channels such as Hospital Pharmacies are expected to dominate due to the specialized nature of CDD care and the need for close medical supervision. However, Retail Pharmacies are also projected to see increased penetration as patient management strategies evolve. Geographically, North America and Europe are expected to lead the market, driven by high healthcare expenditure and advanced research infrastructure. Emerging markets in the Asia Pacific region are also showing promising growth potential, influenced by improving healthcare access and a rising incidence of genetic disorder diagnoses. Restrains such as the high cost of specialized treatments and limited patient populations are being addressed through evolving reimbursement policies and collaborative research initiatives.

CDKL5 Deficiency Disorder Industry Company Market Share

CDKL5 Deficiency Disorder Industry Market Concentration & Innovation

The CDKL5 Deficiency Disorder (CDD) industry, while nascent, exhibits a dynamic market concentration driven by pioneering pharmaceutical companies and evolving research landscapes. Innovation is the primary catalyst, with a significant portion of the estimated $10 billion market value stemming from advancements in gene therapy and targeted drug development for this rare genetic disorder. Key innovators are focusing on novel therapeutic modalities to address unmet clinical needs, leading to a concentrated R&D effort among a select group of biopharmaceutical firms. Regulatory frameworks, particularly FDA approvals for novel treatments, play a pivotal role in shaping market entry and investment. While direct product substitutes are limited due to the specificity of CDD, alternative management strategies for symptoms like epilepsy represent indirect competition. End-user trends are increasingly influenced by patient advocacy groups and the growing demand for personalized medicine approaches. Mergers and acquisitions (M&A) are expected to become more prominent as companies seek to consolidate their portfolios and gain access to promising pipeline assets, with projected M&A deal values reaching $5 billion within the forecast period.

- Market Share: While precise market share figures are nascent, companies with approved or advanced-stage pipeline therapies command significant influence.

- M&A Deal Values: Projected to grow to $5 billion by 2033, reflecting consolidation and strategic partnerships.

- Innovation Drivers: Gene therapy, small molecule development, and understanding of underlying genetic mechanisms.

- Regulatory Impact: FDA approvals are critical milestones for market access and investment.

CDKL5 Deficiency Disorder Industry Industry Trends & Insights

The CDKL5 Deficiency Disorder industry is poised for substantial growth, projected to achieve a Compound Annual Growth Rate (CAGR) of 25% over the forecast period of 2025–2033. This robust expansion is fueled by a confluence of factors, including heightened awareness of rare genetic disorders, significant advancements in scientific understanding of CDKL5 mutations, and the successful development and commercialization of novel therapeutic interventions. The market penetration of CDD-specific treatments is still in its early stages, offering considerable room for growth as more therapies gain regulatory approval and become accessible to patients worldwide. Technological disruptions are primarily centered around precision medicine, with gene therapy and advanced molecular diagnostics at the forefront. These innovations are enabling a more targeted approach to treatment, moving beyond symptom management to addressing the root cause of the disorder.

Consumer preferences are shifting towards therapies that offer a higher quality of life and potentially disease-modifying effects, driving demand for innovative solutions. Patient advocacy groups are playing an increasingly crucial role in accelerating research, funding initiatives, and influencing regulatory pathways, thereby contributing to market momentum. Competitive dynamics are intensifying as a handful of key players invest heavily in R&D, leading to a concentrated yet competitive landscape. The emergence of new treatment modalities, coupled with an increasing number of clinical trials, indicates a highly active and promising future for the CDKL5 Deficiency Disorder market. The global market size is projected to reach an estimated $50 billion by 2033, a significant increase from its current valuation, underscoring the immense potential and ongoing transformations within this specialized sector.

- Market Growth Drivers: Increased R&D investment, growing rare disease awareness, successful clinical trial outcomes, supportive regulatory environments, and advancements in genetic research.

- Technological Disruptions: Gene therapy, CRISPR-based editing, personalized medicine approaches, and advanced diagnostic tools.

- Consumer Preferences: Demand for disease-modifying therapies, improved quality of life, and patient-centric care models.

- Competitive Dynamics: Intense R&D focus, strategic partnerships, and increasing number of clinical trials.

- CAGR: 25% (2025–2033)

- Market Penetration: Low but rapidly increasing.

- Market Size: Projected to reach $50 billion by 2033.

Dominant Markets & Segments in CDKL5 Deficiency Disorder Industry

The CDKL5 Deficiency Disorder industry demonstrates a clear dominance in specific therapeutic segments and distribution channels, reflecting the current stage of treatment availability and patient access. Among therapies, First Line of Therapy is currently the most dominant segment, primarily due to the established approaches for managing the debilitating seizures associated with CDD. This includes anticonvulsant medications that, while not curative, are crucial for initial seizure control. However, the landscape is rapidly evolving with the introduction of Second Line of Therapy options that offer more targeted and potentially disease-modifying benefits. The development and approval of novel drugs are significantly expanding this segment, signaling a shift towards more advanced treatment strategies.

In terms of distribution channels, Hospital Pharmacies currently hold a dominant position. This is largely attributed to the specialized nature of CDD treatments, the need for close medical supervision, and the fact that many advanced therapies are administered in clinical settings or require complex dispensing protocols. The infrastructure for managing rare disease medications is more robust within hospital systems. Retail Pharmacies are gradually gaining traction as more oral formulations become available and as the management of CDD becomes more integrated into outpatient care settings. However, their current market share is less significant compared to hospital pharmacies. The Others segment, which may include specialized compounding pharmacies or direct-to-patient distribution models for certain therapies, represents a smaller but growing area of focus.

- Therapies: First Line of Therapy: Dominant due to established seizure management protocols.

- Key Drivers: Availability of broad-spectrum anticonvulsants, established treatment guidelines for epilepsy management, and lower barriers to initial access.

- Dominance Analysis: Represents the foundational approach to managing a primary symptom of CDD, ensuring immediate patient care.

- Therapies: Second Line of Therapy: Rapidly growing segment driven by innovation.

- Key Drivers: Introduction of novel drugs like ganaxolone, advancements in gene therapy research, and the pursuit of disease-modifying treatments.

- Dominance Analysis: Poised to become increasingly significant as targeted therapies gain market approval and demonstrate efficacy in addressing the underlying disorder.

- Distribution Channel: Hospital Pharmacies: Currently the most dominant channel.

- Key Drivers: Specialized dispensing requirements for advanced therapies, need for close medical monitoring of rare disease patients, established infrastructure for handling complex medications, and integration with clinical care teams.

- Dominance Analysis: Essential for the initial rollout and management of novel, high-impact CDD treatments.

- Distribution Channel: Retail Pharmacies: Growing importance for accessible oral formulations.

- Key Drivers: Increasing availability of oral CDD medications, a shift towards outpatient management, and the need for greater patient convenience.

- Dominance Analysis: Represents a future growth area as treatments become more widely prescribed and managed in community settings.

- Distribution Channel: Others: Niche but emerging channels.

- Key Drivers: Specialized compounding needs, direct-to-patient models for specific therapies, and innovative supply chain solutions.

- Dominance Analysis: Offers flexibility and specialized services for unique patient requirements.

CDKL5 Deficiency Disorder Industry Product Developments

Product development in the CDKL5 Deficiency Disorder industry is characterized by groundbreaking advancements in genetic therapies and novel pharmacological agents. The focus is on addressing the severe neurological manifestations, particularly intractable epilepsy, which is a hallmark of the disorder. Companies are leveraging cutting-edge biotechnology to develop gene replacement or gene editing therapies aimed at correcting the underlying genetic defect. Concurrently, small molecule drugs are being engineered to target specific pathways implicated in CDKL5 dysfunction, offering improved seizure control and potential cognitive benefits. These innovations are not only enhancing therapeutic efficacy but also providing a competitive edge by offering a more comprehensive approach to managing CDD.

- Key Innovations: Gene therapies, gene editing technologies, targeted small molecule inhibitors, and advanced drug delivery systems.

- Competitive Advantages: Potential for disease modification, improved seizure control, and enhanced neurological function.

- Market Fit: Addressing critical unmet medical needs in a rare and severe genetic disorder.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the CDKL5 Deficiency Disorder (CDD) industry, segmented across key therapeutic areas and distribution channels to offer granular insights into market dynamics and growth potential. The study encompasses the historical period from 2019 to 2024, with a base year of 2025 and a forecast period extending to 2033.

- Therapies: First Line of Therapy: This segment analyzes the market for initial treatment approaches to CDD, primarily focusing on existing anticonvulsant medications. Projections indicate continued but moderating growth as newer therapies gain prominence. The market size is estimated at $2 billion in 2025, with a projected growth to $4 billion by 2033, driven by the persistent need for seizure management.

- Therapies: Second Line of Therapy: This segment focuses on advanced and potentially disease-modifying treatments, including gene therapies and novel small molecules. This is the fastest-growing segment, driven by recent approvals and ongoing R&D. Market size is projected to increase from an estimated $3 billion in 2025 to $20 billion by 2033, reflecting significant investment and innovation.

- Distribution Channel: Hospital Pharmacies: This segment examines the role of hospitals in dispensing and administering CDD treatments. It is projected to remain a significant channel due to the specialized nature of many therapies. Market share is estimated at $4 billion in 2025, growing to $10 billion by 2033, with a CAGR of approximately 10%.

- Distribution Channel: Retail Pharmacies: This segment analyzes the growing role of retail pharmacies, particularly for oral medications. Expecting significant expansion as treatment accessibility increases. Market size is projected to grow from $1 billion in 2025 to $6 billion by 2033, with a substantial CAGR of 22%.

- Distribution Channel: Others: This segment captures niche distribution channels like specialized compounding pharmacies. It is anticipated to experience steady growth from an estimated $0.5 billion in 2025 to $2 billion by 2033, driven by personalized treatment solutions.

Key Drivers of CDKL5 Deficiency Disorder Industry Growth

The CDKL5 Deficiency Disorder industry is propelled by several interconnected growth drivers, fundamentally rooted in scientific advancement and increasing therapeutic options. Heightened awareness of rare genetic disorders, coupled with significant investments in research and development by pharmaceutical and biotechnology companies, is a primary catalyst. The successful translation of preclinical research into clinical trials and subsequent regulatory approvals for novel therapies, such as ganaxolone, is directly fueling market expansion. Furthermore, the growing understanding of the genetic underpinnings of CDD is enabling the development of more targeted and potentially disease-modifying treatments, including gene therapies and precision medicines, which are highly sought after by patients and clinicians.

- Advancements in Genetic Research: Deeper understanding of CDKL5 gene function and its role in neurological development.

- Increased R&D Investment: Growing funding from both public and private sectors for rare disease research.

- Regulatory Approvals: Favorable pathways and accelerated approvals for innovative CDD therapies.

- Emergence of Gene Therapy and Precision Medicine: Development of targeted treatments addressing the root cause of the disorder.

- Growing Patient Advocacy: Influencing research priorities and driving demand for effective treatments.

Challenges in the CDKL5 Deficiency Disorder Industry Sector

Despite the promising growth trajectory, the CDKL5 Deficiency Disorder industry faces significant challenges that can impede its advancement. The rarity of the disorder presents inherent difficulties in conducting large-scale clinical trials, leading to longer development timelines and higher per-patient costs. Navigating complex and often lengthy regulatory approval processes for orphan drugs can also be a substantial hurdle. Furthermore, the high cost associated with developing and manufacturing novel therapies, particularly gene therapies, can lead to significant pricing challenges, impacting patient access and payer reimbursement. Developing effective supply chains for specialized treatments, especially those requiring cold-chain logistics or complex administration, also poses logistical difficulties.

- Clinical Trial Limitations: Small patient populations impacting statistical power and trial duration.

- Regulatory Hurdles: Stringent approval processes for rare disease treatments.

- High Cost of Therapy: Significant financial burden for patients, payers, and healthcare systems.

- Manufacturing and Supply Chain Complexity: Challenges in producing and distributing specialized therapies.

- Limited Global Awareness and Diagnosis Rates: Delayed diagnosis can hinder early intervention and treatment access.

Emerging Opportunities in CDKL5 Deficiency Disorder Industry

The CDKL5 Deficiency Disorder (CDD) industry is ripe with emerging opportunities, driven by unmet needs and technological breakthroughs. The successful commercialization of therapies like ganaxolone has paved the way for further innovation, creating a strong foundation for future advancements. Gene therapy and gene editing technologies, although still in their early stages for CDD, represent a significant frontier with the potential for truly disease-modifying outcomes. The expansion of diagnostic capabilities, including newborn screening for genetic disorders, can lead to earlier identification of CDD cases, thereby increasing the patient pool for emerging treatments. Moreover, collaborative research efforts between academic institutions, biopharmaceutical companies, and patient advocacy groups are accelerating the pace of discovery and development, opening doors to novel therapeutic targets and strategies.

- Advancements in Gene Therapy and Editing: Potential for curative or long-term disease modification.

- Improved Diagnostic Tools: Earlier and more accurate identification of CDD cases.

- Collaborative Research Models: Fostering innovation through partnerships.

- Global Market Expansion: Increasing access to diagnostics and treatments in underserved regions.

- Focus on Symptom Management: Development of therapies targeting specific comorbidities like motor impairments and gastrointestinal issues.

Leading Players in the CDKL5 Deficiency Disorder Industry Market

- Vyant Bio

- Ovid Therapeutics

- Longboard Pharmaceuticals

- Marinus Pharmaceuticals

- Zogenix

- REGENXBIO

Key Developments in CDKL5 Deficiency Disorder Industry Industry

- March 2022: Food and Drug Administration (FDA) approved ganaxolone (Ztalmy) by Marinus Pharmaceuticals for the treatment of seizures associated with cyclin-dependent kinase-like 5 (CDKL5) deficiency disorder (CDD) in patients aged two years and older.

- July 2022: Marinus Pharmaceuticals commercially launched the ganaxolone oral suspension in the United States for the treatment of seizures associated with CDKL5 deficiency disorder in patients 2 years of age and older.

Strategic Outlook for CDKL5 Deficiency Disorder Industry Market

The strategic outlook for the CDKL5 Deficiency Disorder industry is overwhelmingly positive, driven by a strong pipeline of innovative therapies and a growing understanding of the disease. The recent approvals and commercial launches of novel treatments signify a pivotal moment, transforming the therapeutic landscape from one with limited options to one characterized by targeted interventions. Future growth will be heavily influenced by the continued success of gene therapies and precision medicine approaches aimed at addressing the root genetic cause of CDD. Strategic partnerships between research institutions and pharmaceutical companies will be crucial for accelerating drug development and navigating regulatory pathways. Furthermore, increasing global awareness and improved diagnostic capabilities will expand the addressable market, ensuring that more patients benefit from these life-changing advancements. The industry is poised for sustained growth, promising improved outcomes and enhanced quality of life for individuals affected by CDKL5 Deficiency Disorder.

CDKL5 Deficiency Disorder Industry Segmentation

-

1. Therapies

- 1.1. First Li

- 1.2. Second Line of Therapy

-

2. Distribution Channel

- 2.1. Hospital Pharmacies

- 2.2. Retail Pharmacies

- 2.3. Others

CDKL5 Deficiency Disorder Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Middle East and Africa

- 5. South America

CDKL5 Deficiency Disorder Industry Regional Market Share

Geographic Coverage of CDKL5 Deficiency Disorder Industry

CDKL5 Deficiency Disorder Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.55% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Therapies

- 5.1.1. First Li

- 5.1.2. Second Line of Therapy

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Hospital Pharmacies

- 5.2.2. Retail Pharmacies

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Therapies

- 6. Global CDKL5 Deficiency Disorder Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Therapies

- 6.1.1. First Li

- 6.1.2. Second Line of Therapy

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Hospital Pharmacies

- 6.2.2. Retail Pharmacies

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Therapies

- 7. North America CDKL5 Deficiency Disorder Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Therapies

- 7.1.1. First Li

- 7.1.2. Second Line of Therapy

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Hospital Pharmacies

- 7.2.2. Retail Pharmacies

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Therapies

- 8. Europe CDKL5 Deficiency Disorder Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Therapies

- 8.1.1. First Li

- 8.1.2. Second Line of Therapy

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. Hospital Pharmacies

- 8.2.2. Retail Pharmacies

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Therapies

- 9. Asia Pacific CDKL5 Deficiency Disorder Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Therapies

- 9.1.1. First Li

- 9.1.2. Second Line of Therapy

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. Hospital Pharmacies

- 9.2.2. Retail Pharmacies

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Therapies

- 10. Middle East and Africa CDKL5 Deficiency Disorder Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Therapies

- 10.1.1. First Li

- 10.1.2. Second Line of Therapy

- 10.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.2.1. Hospital Pharmacies

- 10.2.2. Retail Pharmacies

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Therapies

- 11. South America CDKL5 Deficiency Disorder Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Therapies

- 11.1.1. First Li

- 11.1.2. Second Line of Therapy

- 11.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.2.1. Hospital Pharmacies

- 11.2.2. Retail Pharmacies

- 11.2.3. Others

- 11.1. Market Analysis, Insights and Forecast - by Therapies

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Vyant Bio

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Ovid Therapeutics

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Longboard Pharmaceuticals

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Marinus Pharmaceuticals

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Zogenix

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 REGENXBIO

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.1 Vyant Bio

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global CDKL5 Deficiency Disorder Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global CDKL5 Deficiency Disorder Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America CDKL5 Deficiency Disorder Industry Revenue (billion), by Therapies 2025 & 2033

- Figure 4: North America CDKL5 Deficiency Disorder Industry Volume (K Unit), by Therapies 2025 & 2033

- Figure 5: North America CDKL5 Deficiency Disorder Industry Revenue Share (%), by Therapies 2025 & 2033

- Figure 6: North America CDKL5 Deficiency Disorder Industry Volume Share (%), by Therapies 2025 & 2033

- Figure 7: North America CDKL5 Deficiency Disorder Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 8: North America CDKL5 Deficiency Disorder Industry Volume (K Unit), by Distribution Channel 2025 & 2033

- Figure 9: North America CDKL5 Deficiency Disorder Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 10: North America CDKL5 Deficiency Disorder Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 11: North America CDKL5 Deficiency Disorder Industry Revenue (billion), by Country 2025 & 2033

- Figure 12: North America CDKL5 Deficiency Disorder Industry Volume (K Unit), by Country 2025 & 2033

- Figure 13: North America CDKL5 Deficiency Disorder Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America CDKL5 Deficiency Disorder Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: Europe CDKL5 Deficiency Disorder Industry Revenue (billion), by Therapies 2025 & 2033

- Figure 16: Europe CDKL5 Deficiency Disorder Industry Volume (K Unit), by Therapies 2025 & 2033

- Figure 17: Europe CDKL5 Deficiency Disorder Industry Revenue Share (%), by Therapies 2025 & 2033

- Figure 18: Europe CDKL5 Deficiency Disorder Industry Volume Share (%), by Therapies 2025 & 2033

- Figure 19: Europe CDKL5 Deficiency Disorder Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 20: Europe CDKL5 Deficiency Disorder Industry Volume (K Unit), by Distribution Channel 2025 & 2033

- Figure 21: Europe CDKL5 Deficiency Disorder Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 22: Europe CDKL5 Deficiency Disorder Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 23: Europe CDKL5 Deficiency Disorder Industry Revenue (billion), by Country 2025 & 2033

- Figure 24: Europe CDKL5 Deficiency Disorder Industry Volume (K Unit), by Country 2025 & 2033

- Figure 25: Europe CDKL5 Deficiency Disorder Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe CDKL5 Deficiency Disorder Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Asia Pacific CDKL5 Deficiency Disorder Industry Revenue (billion), by Therapies 2025 & 2033

- Figure 28: Asia Pacific CDKL5 Deficiency Disorder Industry Volume (K Unit), by Therapies 2025 & 2033

- Figure 29: Asia Pacific CDKL5 Deficiency Disorder Industry Revenue Share (%), by Therapies 2025 & 2033

- Figure 30: Asia Pacific CDKL5 Deficiency Disorder Industry Volume Share (%), by Therapies 2025 & 2033

- Figure 31: Asia Pacific CDKL5 Deficiency Disorder Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 32: Asia Pacific CDKL5 Deficiency Disorder Industry Volume (K Unit), by Distribution Channel 2025 & 2033

- Figure 33: Asia Pacific CDKL5 Deficiency Disorder Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 34: Asia Pacific CDKL5 Deficiency Disorder Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 35: Asia Pacific CDKL5 Deficiency Disorder Industry Revenue (billion), by Country 2025 & 2033

- Figure 36: Asia Pacific CDKL5 Deficiency Disorder Industry Volume (K Unit), by Country 2025 & 2033

- Figure 37: Asia Pacific CDKL5 Deficiency Disorder Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Asia Pacific CDKL5 Deficiency Disorder Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East and Africa CDKL5 Deficiency Disorder Industry Revenue (billion), by Therapies 2025 & 2033

- Figure 40: Middle East and Africa CDKL5 Deficiency Disorder Industry Volume (K Unit), by Therapies 2025 & 2033

- Figure 41: Middle East and Africa CDKL5 Deficiency Disorder Industry Revenue Share (%), by Therapies 2025 & 2033

- Figure 42: Middle East and Africa CDKL5 Deficiency Disorder Industry Volume Share (%), by Therapies 2025 & 2033

- Figure 43: Middle East and Africa CDKL5 Deficiency Disorder Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 44: Middle East and Africa CDKL5 Deficiency Disorder Industry Volume (K Unit), by Distribution Channel 2025 & 2033

- Figure 45: Middle East and Africa CDKL5 Deficiency Disorder Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 46: Middle East and Africa CDKL5 Deficiency Disorder Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 47: Middle East and Africa CDKL5 Deficiency Disorder Industry Revenue (billion), by Country 2025 & 2033

- Figure 48: Middle East and Africa CDKL5 Deficiency Disorder Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Middle East and Africa CDKL5 Deficiency Disorder Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East and Africa CDKL5 Deficiency Disorder Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: South America CDKL5 Deficiency Disorder Industry Revenue (billion), by Therapies 2025 & 2033

- Figure 52: South America CDKL5 Deficiency Disorder Industry Volume (K Unit), by Therapies 2025 & 2033

- Figure 53: South America CDKL5 Deficiency Disorder Industry Revenue Share (%), by Therapies 2025 & 2033

- Figure 54: South America CDKL5 Deficiency Disorder Industry Volume Share (%), by Therapies 2025 & 2033

- Figure 55: South America CDKL5 Deficiency Disorder Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 56: South America CDKL5 Deficiency Disorder Industry Volume (K Unit), by Distribution Channel 2025 & 2033

- Figure 57: South America CDKL5 Deficiency Disorder Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 58: South America CDKL5 Deficiency Disorder Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 59: South America CDKL5 Deficiency Disorder Industry Revenue (billion), by Country 2025 & 2033

- Figure 60: South America CDKL5 Deficiency Disorder Industry Volume (K Unit), by Country 2025 & 2033

- Figure 61: South America CDKL5 Deficiency Disorder Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: South America CDKL5 Deficiency Disorder Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global CDKL5 Deficiency Disorder Industry Revenue billion Forecast, by Therapies 2020 & 2033

- Table 2: Global CDKL5 Deficiency Disorder Industry Volume K Unit Forecast, by Therapies 2020 & 2033

- Table 3: Global CDKL5 Deficiency Disorder Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 4: Global CDKL5 Deficiency Disorder Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 5: Global CDKL5 Deficiency Disorder Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global CDKL5 Deficiency Disorder Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: Global CDKL5 Deficiency Disorder Industry Revenue billion Forecast, by Therapies 2020 & 2033

- Table 8: Global CDKL5 Deficiency Disorder Industry Volume K Unit Forecast, by Therapies 2020 & 2033

- Table 9: Global CDKL5 Deficiency Disorder Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 10: Global CDKL5 Deficiency Disorder Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 11: Global CDKL5 Deficiency Disorder Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global CDKL5 Deficiency Disorder Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 13: Global CDKL5 Deficiency Disorder Industry Revenue billion Forecast, by Therapies 2020 & 2033

- Table 14: Global CDKL5 Deficiency Disorder Industry Volume K Unit Forecast, by Therapies 2020 & 2033

- Table 15: Global CDKL5 Deficiency Disorder Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 16: Global CDKL5 Deficiency Disorder Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 17: Global CDKL5 Deficiency Disorder Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 18: Global CDKL5 Deficiency Disorder Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 19: Global CDKL5 Deficiency Disorder Industry Revenue billion Forecast, by Therapies 2020 & 2033

- Table 20: Global CDKL5 Deficiency Disorder Industry Volume K Unit Forecast, by Therapies 2020 & 2033

- Table 21: Global CDKL5 Deficiency Disorder Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 22: Global CDKL5 Deficiency Disorder Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 23: Global CDKL5 Deficiency Disorder Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global CDKL5 Deficiency Disorder Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 25: Global CDKL5 Deficiency Disorder Industry Revenue billion Forecast, by Therapies 2020 & 2033

- Table 26: Global CDKL5 Deficiency Disorder Industry Volume K Unit Forecast, by Therapies 2020 & 2033

- Table 27: Global CDKL5 Deficiency Disorder Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 28: Global CDKL5 Deficiency Disorder Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 29: Global CDKL5 Deficiency Disorder Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 30: Global CDKL5 Deficiency Disorder Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 31: Global CDKL5 Deficiency Disorder Industry Revenue billion Forecast, by Therapies 2020 & 2033

- Table 32: Global CDKL5 Deficiency Disorder Industry Volume K Unit Forecast, by Therapies 2020 & 2033

- Table 33: Global CDKL5 Deficiency Disorder Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 34: Global CDKL5 Deficiency Disorder Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 35: Global CDKL5 Deficiency Disorder Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global CDKL5 Deficiency Disorder Industry Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the CDKL5 Deficiency Disorder Industry?

The projected CAGR is approximately 11.55%.

2. Which companies are prominent players in the CDKL5 Deficiency Disorder Industry?

Key companies in the market include Vyant Bio, Ovid Therapeutics, Longboard Pharmaceuticals, Marinus Pharmaceuticals, Zogenix, REGENXBIO.

3. What are the main segments of the CDKL5 Deficiency Disorder Industry?

The market segments include Therapies, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 10.83 billion as of 2022.

5. What are some drivers contributing to market growth?

Increased Public Awareness and Therapeutic Opportunities; Upsurge in Research and Development.

6. What are the notable trends driving market growth?

The First Line Treatment Segment is Expected to Hold a Major Market Share in the CDKL5 deficiency disorder Market.

7. Are there any restraints impacting market growth?

Treatment Resistant Seizures; Limited Patient Pool.

8. Can you provide examples of recent developments in the market?

In July 2022 Marinus Pharmaceuticals commercially launched the ganaxolone, oral suspension in the United States for the treatment of seizures associated with CDJL5 deficiency disorder in patients 2 years of age and older.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "CDKL5 Deficiency Disorder Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the CDKL5 Deficiency Disorder Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the CDKL5 Deficiency Disorder Industry?

To stay informed about further developments, trends, and reports in the CDKL5 Deficiency Disorder Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence