Key Insights

China's burgeoning Hydrogen and Fuel Cells industry is projected for substantial growth, with an estimated market size of 12.94 billion by 2025, driven by a Compound Annual Growth Rate (CAGR) of 12.3%. This expansion is underpinned by China's commitment to decarbonization and its strategic focus on renewable energy systems. Supportive government policies, including substantial subsidies and regulations promoting hydrogen infrastructure and fuel cell adoption, are significant growth drivers. Fuel cell technology is increasingly being integrated into the transportation sector, particularly for heavy-duty vehicles, and into stationary power solutions for remote locations and backup power. Advancements in Polymer Electrolyte Membrane Fuel Cell (PEMFC) technology are improving efficiency and reducing costs, positioning fuel cells as a competitive alternative to conventional power sources.

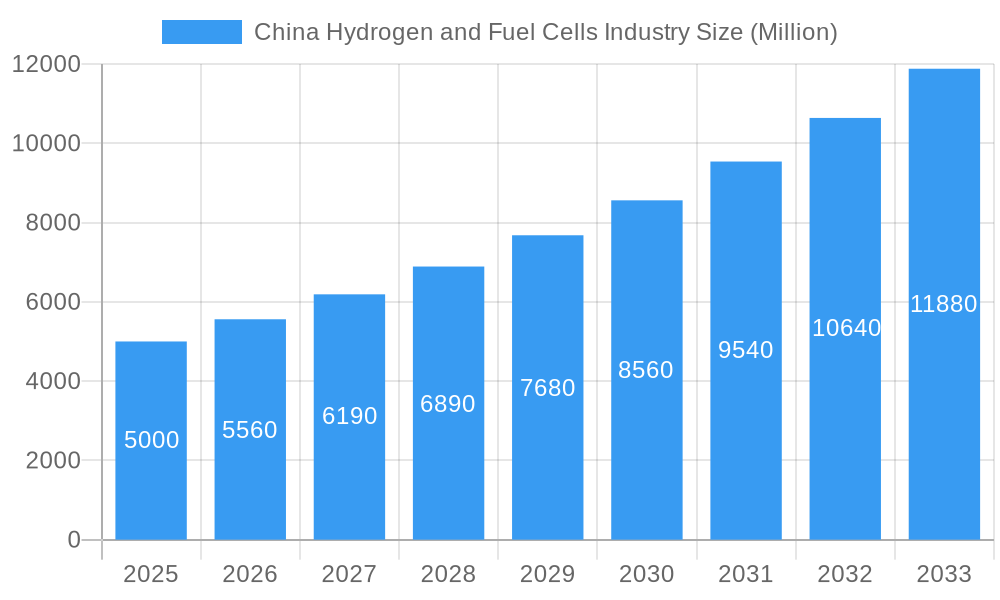

China Hydrogen and Fuel Cells Industry Market Size (In Billion)

Key industry trends include the development of large-scale hydrogen production (green and blue hydrogen) and the rapid expansion of hydrogen refueling infrastructure. Innovations in fuel cell stack manufacturing are reducing costs. However, the industry faces challenges such as high initial system costs, the need for a robust hydrogen supply chain, and ongoing safety considerations that necessitate rigorous standards and public education. Major global and domestic players are actively investing in R&D, forming strategic alliances, and scaling production to capture the significant market potential.

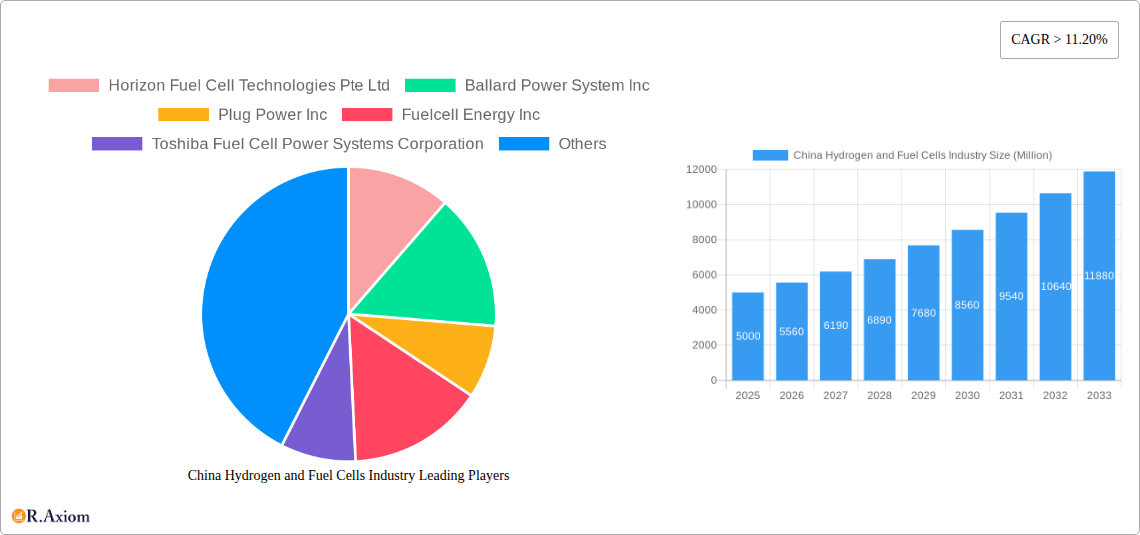

China Hydrogen and Fuel Cells Industry Company Market Share

Explore the comprehensive market outlook for the China Hydrogen and Fuel Cells Industry, including market size, growth projections, and key trends. This report provides an in-depth analysis of opportunities and challenges within this rapidly evolving sector.

China Hydrogen and Fuel Cells Industry Market Concentration & Innovation

The China Hydrogen and Fuel Cells Industry exhibits a dynamic landscape characterized by increasing market concentration and a strong drive for innovation. Government policies and significant investments are propelling the growth of this sector, with a focus on reducing carbon emissions and achieving energy independence. Key innovation drivers include advancements in fuel cell stack efficiency, hydrogen production technologies (especially green hydrogen), and integrated energy systems. Regulatory frameworks are rapidly evolving to support the widespread adoption of hydrogen fuel cells, providing subsidies, tax incentives, and clear roadmaps for infrastructure development. While product substitutes like battery electric vehicles exist, the unique advantages of hydrogen fuel cells, such as faster refueling times and longer range for heavy-duty applications, are solidifying their position. End-user trends indicate a strong preference for hydrogen in transportation (heavy-duty trucks, buses) and stationary power generation for industrial and backup purposes. Mergers and acquisitions (M&A) are becoming more frequent as larger companies seek to consolidate market share and acquire cutting-edge technologies. Recent M&A deal values have reached into the hundreds of millions, signaling robust investor confidence and strategic consolidation. The market share of leading players is steadily increasing, with significant investments in R&D and manufacturing capacity.

China Hydrogen and Fuel Cells Industry Industry Trends & Insights

The China Hydrogen and Fuel Cells Industry is experiencing an unprecedented surge in growth, driven by a confluence of powerful market drivers. The nation's ambitious decarbonization targets and its strategic vision for a hydrogen-powered future are the primary catalysts. Government policies, including the "New Energy Vehicle" (NEV) subsidy programs and the inclusion of hydrogen energy in national and provincial five-year plans, are providing substantial financial and regulatory support. This has fostered a CAGR of approximately 25% over the historical period and is projected to continue at a robust pace through the forecast period. Technological disruptions are at the forefront, with continuous improvements in the efficiency and durability of fuel cell stacks, particularly Polymer Electrolyte Membrane Fuel Cells (PEMFCs), and advancements in cost-effective green hydrogen production methods. Consumer preferences are shifting towards cleaner energy solutions, especially in urban centers and for commercial fleets, where the benefits of zero-emission transportation and reliable backup power are highly valued. The competitive dynamics are intensifying, with both domestic Chinese players and international companies vying for market leadership. Market penetration is rapidly increasing across various applications, with significant adoption in the transportation sector for buses and trucks, and growing interest in stationary power for data centers and industrial facilities. Investments in hydrogen refueling infrastructure are crucial for market expansion, and China is aggressively building out its network. Furthermore, the development of integrated hydrogen energy ecosystems, encompassing production, storage, transportation, and utilization, is a key trend shaping the industry's future. The increasing demand for high-performance, cost-competitive fuel cell systems and the exploration of new applications are further fueling market growth.

Dominant Markets & Segments in China Hydrogen and Fuel Cells Industry

The dominant markets and segments within the China Hydrogen and Fuel Cells Industry are being shaped by strategic government initiatives, technological advancements, and evolving end-user demands. Transportation is unequivocally the leading application segment, driven by national policies aimed at decarbonizing the logistics and public transport sectors.

- Transportation:

- Key Drivers:

- Government Mandates and Subsidies: National and provincial governments are actively promoting the adoption of fuel cell electric vehicles (FCEVs) through direct subsidies, tax incentives, and charging infrastructure support. Policies targeting commercial fleets, such as buses and heavy-duty trucks, are particularly influential.

- Infrastructure Development: Significant investment is being channeled into building hydrogen refueling stations across major transportation hubs and key industrial zones, alleviating range anxiety and enabling widespread adoption.

- Environmental Regulations: Stricter emission standards for vehicles are pushing fleet operators to seek cleaner alternatives, with fuel cell technology offering a compelling solution for long-haul and heavy-duty applications where battery-electric solutions face limitations.

- Corporate Sustainability Goals: Many logistics and transportation companies are setting ambitious sustainability targets, accelerating their transition to zero-emission vehicles.

- Key Drivers:

The Polymer Electrolyte Membrane Fuel Cell (PEMFC) technology segment is also demonstrating remarkable dominance.

- Fuel Cell Technology: Polymer Electrolyte Membrane Fuel Cell (PEMFC):

- Key Drivers:

- High Power Density and Efficiency: PEMFCs offer excellent power density, making them suitable for a wide range of vehicle applications. Their operational efficiency translates to lower fuel consumption and operational costs.

- Low Operating Temperature: Unlike Solid Oxide Fuel Cells (SOFCs), PEMFCs operate at relatively low temperatures, allowing for faster start-up times and making them ideal for mobile applications.

- Technological Maturity and Cost Reduction: Continuous research and development have led to significant improvements in PEMFC durability and cost-effectiveness, making them increasingly competitive. Major players are investing heavily in scaling up production, further driving down manufacturing costs.

- Established Supply Chain: The supply chain for PEMFC components, including catalysts and membranes, is becoming increasingly robust within China.

- Key Drivers:

While Stationary applications are a growing segment, particularly for backup power and distributed generation, and Solid Oxide Fuel Cell (SOFC) technology is showing promise for larger-scale, high-efficiency power generation, their current market penetration trails that of transportation and PEMFCs. The development of supporting infrastructure and further cost reductions will be critical for their broader adoption.

China Hydrogen and Fuel Cells Industry Product Developments

Product developments in the China Hydrogen and Fuel Cells Industry are characterized by a strong focus on enhancing performance, durability, and cost-effectiveness. Companies are innovating in fuel cell stack design, optimizing electrode materials, and developing advanced membrane technologies to improve efficiency and reduce reliance on precious metals. The integration of fuel cells into diverse applications, from heavy-duty trucks and buses to forklifts and stationary power systems for data centers and residential buildings, is a significant trend. Competitive advantages are being built through modular designs for scalability, improved thermal management systems, and the development of intelligent control systems for optimal energy management. The push towards higher power output and longer operational lifespans is also a key area of product innovation, ensuring greater reliability for demanding applications and facilitating wider market acceptance.

Report Scope & Segmentation Analysis

This report delves into the China Hydrogen and Fuel Cells Industry, encompassing a detailed segmentation across key areas to provide comprehensive market insights.

Application Segments: The market is analyzed based on its primary applications: Portable (e.g., backup power for electronics, portable generators), Stationary (e.g., distributed power generation, uninterruptible power supply for critical infrastructure), and Transportation (e.g., fuel cell electric vehicles for buses, trucks, and potentially passenger cars). Projections indicate significant growth in the Transportation segment due to strong policy support and infrastructure build-out, followed by Stationary applications, while Portable applications are expected to witness steady but more modest expansion.

Fuel Cell Technology Segments: The report further segments the market by core fuel cell technologies: Polymer Electrolyte Membrane Fuel Cell (PEMFC), Solid Oxide Fuel Cell (SOFC), and Other Fuel Cell Technologies (including Alkaline Fuel Cells, Phosphoric Acid Fuel Cells, etc.). PEMFCs are projected to dominate the market due to their versatility and suitability for the rapidly growing transportation sector. SOFCs are expected to see increasing adoption in stationary power generation due to their high efficiency. The "Other Fuel Cell Technologies" segment will be analyzed for niche applications and emerging innovations.

Key Drivers of China Hydrogen and Fuel Cells Industry Growth

The growth of the China Hydrogen and Fuel Cells Industry is propelled by several intertwined factors. Foremost are supportive government policies and ambitious national decarbonization goals, which provide substantial subsidies, tax incentives, and a clear regulatory roadmap for hydrogen energy development. Secondly, technological advancements in fuel cell efficiency, durability, and hydrogen production (particularly green hydrogen via electrolysis) are making these solutions more competitive and reliable. The growing demand for cleaner transportation alternatives, especially for heavy-duty vehicles with long ranges, is a significant driver. Furthermore, increasing investments in hydrogen infrastructure, including refueling stations and pipeline networks, are crucial for enabling wider adoption. Finally, corporate commitments to sustainability and ESG (Environmental, Social, and Governance) targets are compelling businesses across various sectors to explore and adopt hydrogen fuel cell solutions for their energy needs.

Challenges in the China Hydrogen and Fuel Cells Industry Sector

Despite its promising outlook, the China Hydrogen and Fuel Cells Industry faces several significant challenges. High upfront costs associated with fuel cell systems and hydrogen production remain a barrier to widespread adoption, although these costs are declining. Infrastructure limitations, particularly the availability and distribution network of hydrogen, present a significant hurdle, especially outside major urban centers. Safety concerns and public perception surrounding hydrogen handling and storage require continuous education and stringent safety protocols. Supply chain bottlenecks for critical components, though improving, can still impact production volumes and cost-effectiveness. Furthermore, competition from established battery electric vehicle (BEV) technology in certain segments poses a challenge, requiring clear differentiation and value proposition for hydrogen solutions. Regulatory fragmentation across different regions can also create complexities for market players.

Emerging Opportunities in China Hydrogen and Fuel Cells Industry

Emerging opportunities in the China Hydrogen and Fuel Cells Industry are abundant, driven by innovation and evolving market needs. The expansion of green hydrogen production capacity through renewable energy integration presents a massive opportunity for sustainable fuel sourcing. The development of advanced hydrogen storage solutions, including solid-state storage, offers pathways to safer and more efficient hydrogen transportation and utilization. Growth in industrial applications, such as hydrogen as a reducing agent in steelmaking and chemical production, represents a significant untapped market. The commercialization of hydrogen fuel cells in maritime and aviation sectors is an emerging frontier. Furthermore, the establishment of comprehensive hydrogen energy ecosystems and smart grids, integrating hydrogen production, storage, distribution, and consumption, will unlock new synergies and efficiencies. Opportunities also lie in developing standardized components and certifications to streamline the supply chain and foster international collaboration.

Leading Players in the China Hydrogen and Fuel Cells Industry Market

- Horizon Fuel Cell Technologies Pte Ltd

- Ballard Power System Inc

- Plug Power Inc

- Fuelcell Energy Inc

- Toshiba Fuel Cell Power Systems Corporation

Key Developments in China Hydrogen and Fuel Cells Industry Industry

- 2024: China announces ambitious targets for hydrogen fuel cell vehicle deployment, including increased subsidies for heavy-duty trucks and buses.

- 2023: Several major Chinese automakers initiate pilot programs for fuel cell electric trucks, showcasing advancements in range and refueling times.

- 2023: Significant investments are made in scaling up green hydrogen production facilities, with a focus on electrolyzer manufacturing capacity.

- 2023: New regulations are introduced to standardize hydrogen refueling station safety and operational procedures, aiming to accelerate infrastructure build-out.

- 2022: Several international fuel cell manufacturers announce joint ventures and partnerships with Chinese companies to localize production and R&D.

- 2021: China releases its mid-to-long-term plan for hydrogen energy development, outlining key goals for the next decade.

- 2020: Government incentives and pilot projects for hydrogen fuel cell buses and logistics vehicles gain significant traction in major cities.

- 2019: Initial policy frameworks and funding mechanisms are established to support the nascent hydrogen and fuel cell industry in China.

Strategic Outlook for China Hydrogen and Fuel Cells Industry Market

The strategic outlook for the China Hydrogen and Fuel Cells Industry is overwhelmingly positive, driven by the nation's unwavering commitment to achieving carbon neutrality and its aggressive pursuit of hydrogen energy as a cornerstone of its future energy system. Anticipated growth catalysts include continued strong government support through policy incentives and infrastructure investments, leading to the exponential expansion of the hydrogen refueling network. Technological advancements in fuel cell efficiency, durability, and cost reduction, coupled with breakthroughs in green hydrogen production and storage, will further enhance the competitiveness of hydrogen solutions. The increasing adoption of fuel cell technology in heavy-duty transportation, industrial decarbonization, and distributed power generation presents vast market opportunities. Strategic collaborations between domestic and international players, alongside robust R&D investments, will accelerate innovation and market penetration. The ongoing development of a comprehensive hydrogen value chain, from production to end-use, will solidify China's position as a global leader in the hydrogen economy.

China Hydrogen and Fuel Cells Industry Segmentation

-

1. Application

- 1.1. Portable

- 1.2. Stationary

- 1.3. Transportation

-

2. Fuel Cell Technology

- 2.1. Polymer Electrolyte Membrane Fuel Cell (PEMFC)

- 2.2. Solid Oxide Fuel Cell (SOFC)

- 2.3. Other Fuel Cell Technologies

China Hydrogen and Fuel Cells Industry Segmentation By Geography

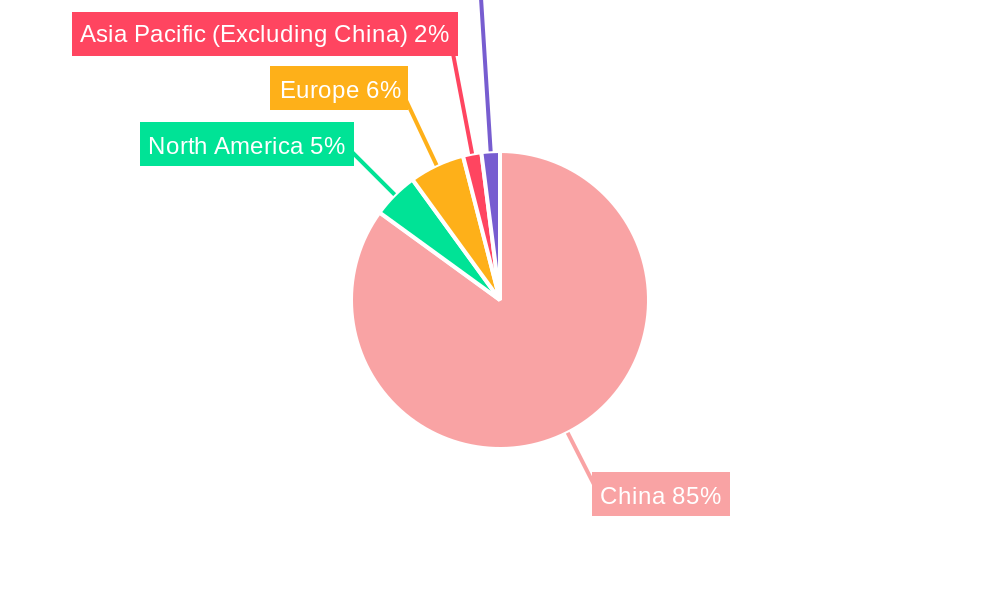

- 1. China

China Hydrogen and Fuel Cells Industry Regional Market Share

Geographic Coverage of China Hydrogen and Fuel Cells Industry

China Hydrogen and Fuel Cells Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Portable

- 5.1.2. Stationary

- 5.1.3. Transportation

- 5.2. Market Analysis, Insights and Forecast - by Fuel Cell Technology

- 5.2.1. Polymer Electrolyte Membrane Fuel Cell (PEMFC)

- 5.2.2. Solid Oxide Fuel Cell (SOFC)

- 5.2.3. Other Fuel Cell Technologies

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. China

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. China Hydrogen and Fuel Cells Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Portable

- 6.1.2. Stationary

- 6.1.3. Transportation

- 6.2. Market Analysis, Insights and Forecast - by Fuel Cell Technology

- 6.2.1. Polymer Electrolyte Membrane Fuel Cell (PEMFC)

- 6.2.2. Solid Oxide Fuel Cell (SOFC)

- 6.2.3. Other Fuel Cell Technologies

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Horizon Fuel Cell Technologies Pte Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Ballard Power System Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Plug Power Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Fuelcell Energy Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Toshiba Fuel Cell Power Systems Corporation

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.1 Horizon Fuel Cell Technologies Pte Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Hydrogen and Fuel Cells Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: China Hydrogen and Fuel Cells Industry Share (%) by Company 2025

List of Tables

- Table 1: China Hydrogen and Fuel Cells Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 2: China Hydrogen and Fuel Cells Industry Revenue billion Forecast, by Fuel Cell Technology 2020 & 2033

- Table 3: China Hydrogen and Fuel Cells Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: China Hydrogen and Fuel Cells Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 5: China Hydrogen and Fuel Cells Industry Revenue billion Forecast, by Fuel Cell Technology 2020 & 2033

- Table 6: China Hydrogen and Fuel Cells Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Hydrogen and Fuel Cells Industry?

The projected CAGR is approximately 12.3%.

2. Which companies are prominent players in the China Hydrogen and Fuel Cells Industry?

Key companies in the market include Horizon Fuel Cell Technologies Pte Ltd, Ballard Power System Inc, Plug Power Inc, Fuelcell Energy Inc, Toshiba Fuel Cell Power Systems Corporation.

3. What are the main segments of the China Hydrogen and Fuel Cells Industry?

The market segments include Application, Fuel Cell Technology.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.94 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Uninterrupted and Reliable Power Supply and Heavy Deployment of DG (diesel generator) Set4.; Improvement in Technology of Diesel Generator.

6. What are the notable trends driving market growth?

Transportation Sector to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; The Growing Trend of Renewable Power Generation.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Hydrogen and Fuel Cells Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Hydrogen and Fuel Cells Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Hydrogen and Fuel Cells Industry?

To stay informed about further developments, trends, and reports in the China Hydrogen and Fuel Cells Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence