Key Insights

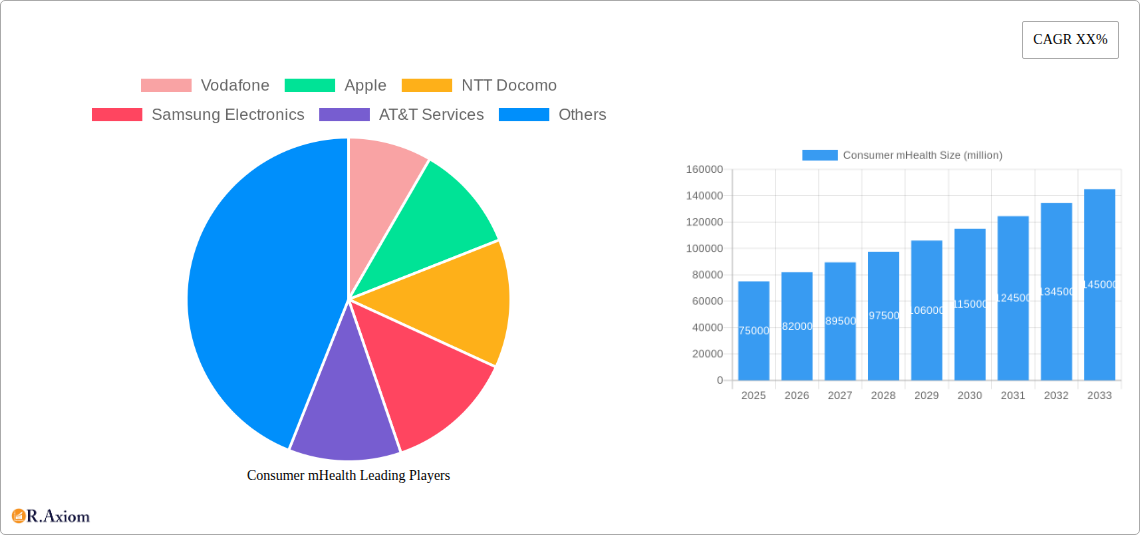

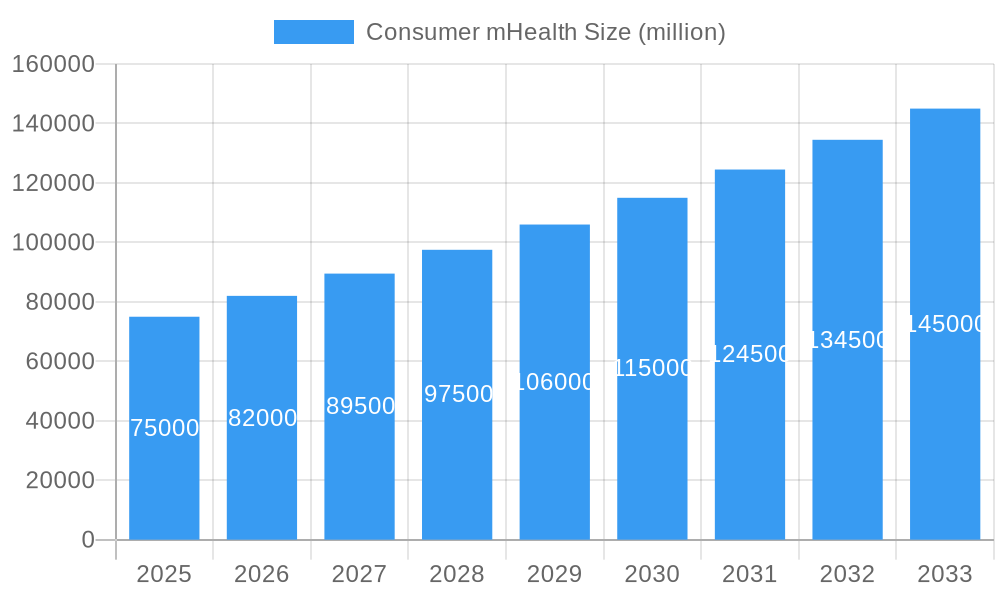

The global Consumer mHealth market is poised for robust expansion, with an estimated market size of approximately \$75 billion in 2025, projected to ascend to over \$150 billion by 2033. This impressive growth is underpinned by a Compound Annual Growth Rate (CAGR) of roughly 9.5%, fueled by an increasing consumer awareness of health and wellness, coupled with the pervasive adoption of smartphones and wearable technology. Key drivers include the escalating prevalence of chronic diseases, a growing demand for remote patient monitoring solutions, and the continuous innovation in mHealth applications and devices. The market is witnessing a significant shift towards personalized health management, empowering individuals to take a more proactive role in their well-being. The integration of artificial intelligence and machine learning is further enhancing the capabilities of mHealth solutions, offering advanced analytics and predictive insights.

Consumer mHealth Market Size (In Billion)

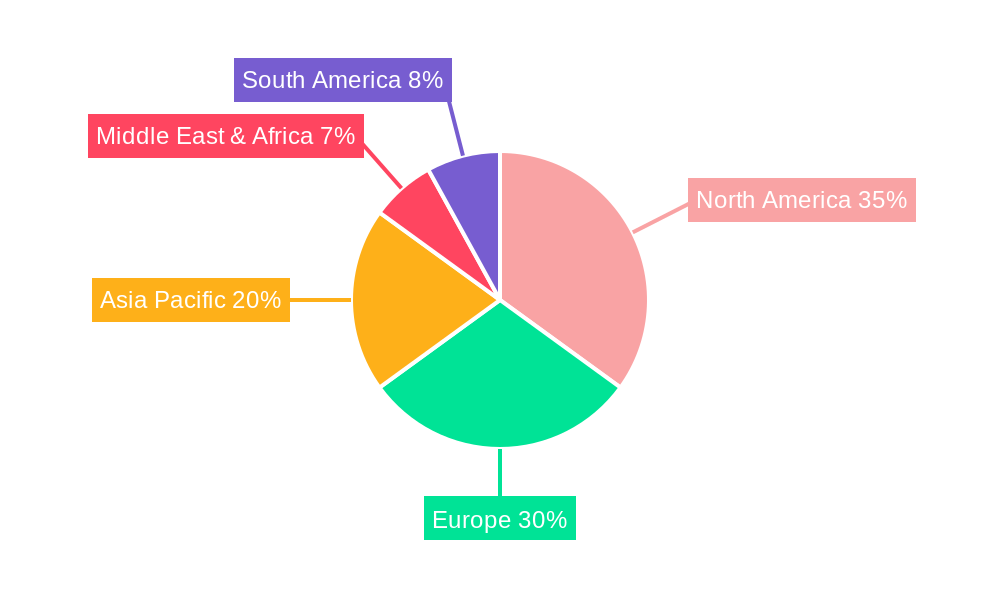

The market's segmentation reveals a dynamic landscape. In terms of applications, adults represent the largest segment due to higher health consciousness and the prevalence of lifestyle-related ailments, followed by teenagers and children, where preventative health and fitness tracking are gaining traction. By type, Blood Glucose Meters and Blood Pressure Monitors are dominant, reflecting the significant burden of diabetes and hypertension globally. However, the growth in Neurological Monitoring Devices and ECG Monitors signifies a broadening scope for mHealth in addressing a wider spectrum of health concerns. Leading technology giants like Apple, Samsung Electronics, and Vodafone are actively investing in this sector, driving innovation and expanding market reach. Geographically, North America and Europe currently lead the market, driven by advanced healthcare infrastructure and high disposable incomes. However, the Asia Pacific region is expected to witness the fastest growth, propelled by rising healthcare expenditure, a burgeoning tech-savvy population, and increasing government initiatives promoting digital health.

Consumer mHealth Company Market Share

This comprehensive report delves into the dynamic global Consumer mHealth market, providing an in-depth analysis of its growth trajectory, key trends, and future potential. With a study period spanning from 2019 to 2033, this report offers a meticulous examination of market concentration, innovation drivers, regulatory landscapes, product substitutes, evolving end-user preferences, and significant Mergers & Acquisitions (M&A) activities. It includes current market share estimates and projected M&A deal values, offering valuable insights for stakeholders. The report details market growth drivers, technological disruptions, shifting consumer preferences, and the competitive dynamics shaping the industry. It also highlights dominant regions, countries, and specific market segments, supported by economic policies and infrastructure development. Product innovations, applications, and competitive advantages are thoroughly explored, emphasizing technological trends and market fit. This report offers a detailed segmentation analysis across applications such as Adults, Teenagers, and Children, and device types including Blood Glucose Meters, Blood Pressure Monitors, Neurological Monitoring Devices, ECG Monitors, and Others, complete with growth projections, market sizes, and competitive dynamics. Key growth drivers, challenges, and emerging opportunities are meticulously outlined, providing a clear roadmap for navigating this rapidly evolving sector. Leading players and pivotal developments within the Consumer mHealth industry are also featured, offering a complete strategic outlook for the market's future potential.

Consumer mHealth Market Concentration & Innovation

The global Consumer mHealth market is characterized by a moderate level of concentration, with a few major players holding significant market share. However, the landscape is increasingly dynamic due to continuous innovation and the entry of new participants. Key innovation drivers include the miniaturization of sensors, advancements in wearable technology, the integration of Artificial Intelligence (AI) and Machine Learning (ML) for data analysis, and the increasing focus on personalized health and wellness solutions. Regulatory frameworks, while evolving, are crucial in shaping product development and market access. The United States and European Union nations lead in establishing guidelines for digital health, impacting market entry strategies for companies like Vodafone and Apple. Product substitutes are emerging, ranging from traditional medical devices to advanced consumer electronics with health-monitoring capabilities, such as those offered by Samsung Electronics and Apple. End-user trends point towards a growing demand for convenient, accessible, and data-driven health monitoring solutions, particularly among tech-savvy demographics. M&A activities are a significant aspect of market consolidation and expansion. Recent M&A deal values have reached substantial figures, with strategic acquisitions aimed at bolstering product portfolios and expanding geographical reach. For instance, acquisitions of smaller tech firms by established players like AT&T Services and Qualcomm are common. The market share of leading companies is continuously influenced by their ability to innovate and adapt to these evolving trends.

Consumer mHealth Industry Trends & Insights

The Consumer mHealth industry is experiencing robust growth, propelled by a confluence of factors that are reshaping healthcare delivery and personal well-being. The market is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 18.5% over the forecast period, driven by increasing health consciousness among global populations, the proliferation of smartphones and connected devices, and a growing need for remote patient monitoring and chronic disease management solutions. Market penetration is steadily increasing, particularly in developed economies, as individuals become more proactive in managing their health. Technological disruptions are at the forefront of this expansion. The integration of advanced sensors into wearables, such as smartwatches and fitness trackers, allows for continuous collection of physiological data, including heart rate, sleep patterns, and activity levels. Furthermore, the rise of AI and ML algorithms is enabling sophisticated data analysis, providing personalized health insights and early detection of potential health issues. The development of mobile applications for condition management, such as for diabetes (e.g., Blood Glucose Meters) and hypertension (e.g., Blood Pressure Monitors), is significantly enhancing patient engagement and adherence to treatment plans. The shift towards preventative healthcare models further fuels the demand for mHealth solutions, as they empower individuals to take control of their health and well-being. The increasing adoption of telehealth services, facilitated by mHealth platforms, has been further accelerated by global events, demonstrating its resilience and essentiality. The competitive dynamics are intense, with both established technology giants like Apple and Samsung Electronics, and specialized mHealth providers such as MQure Health and Healthdirect, vying for market share. Strategic partnerships between telecommunication companies like Vodafone and AT&T Services, and healthcare technology providers are becoming increasingly common, creating integrated ecosystems for seamless health management. The expansion of 5G networks is also a significant enabler, promising faster data transmission and lower latency, which is critical for real-time health monitoring and remote diagnostics. Emerging markets, with their burgeoning middle class and increasing smartphone adoption, represent significant untapped potential for mHealth solutions. The focus on personalized medicine, driven by genetic data and individual health profiles, is another key trend that mHealth platforms are well-positioned to support. The ongoing research and development in areas like advanced biosensors and non-invasive monitoring technologies will continue to drive innovation and broaden the scope of applications for Consumer mHealth devices and services.

Dominant Markets & Segments in Consumer mHealth

North America currently holds the dominant position in the Consumer mHealth market, driven by high disposable incomes, advanced technological infrastructure, and a strong emphasis on preventative healthcare. The United States, in particular, leads with significant market penetration and a robust ecosystem of technology companies, healthcare providers, and regulatory bodies that foster innovation. Key drivers of this dominance include government initiatives promoting digital health adoption, substantial investments in healthcare technology R&D, and a consumer base that is highly receptive to adopting new technologies for personal health management. Economic policies in the region have consistently favored healthcare innovation, leading to substantial private and public sector funding for mHealth solutions. The availability of advanced infrastructure, including widespread broadband internet access and high smartphone penetration, further supports the widespread adoption of these technologies.

Within the application segments, Adults represent the largest and most dominant segment. This is due to several factors: a higher prevalence of chronic diseases among the adult population, increased awareness regarding health and wellness, and greater disposable income for investing in health-monitoring devices and applications. Adults are actively seeking solutions for managing conditions like hypertension, diabetes, and cardiovascular diseases, making devices such as Blood Pressure Monitors and Blood Glucose Meters highly sought after.

In terms of device types, Blood Glucose Meters and Blood Pressure Monitors currently dominate the market. The growing global epidemic of diabetes and hypertension has created a substantial demand for these devices. Their widespread use in managing chronic conditions, coupled with advancements in connectivity and user-friendliness, makes them essential components of home healthcare. The increasing availability of smart, connected versions of these devices, which can sync data with smartphones and share it with healthcare providers, further solidifies their market leadership.

The Teenagers segment is experiencing rapid growth, driven by a focus on fitness tracking, mental well-being applications, and early detection of lifestyle-related health issues. As this demographic becomes more health-conscious and technologically adept, the demand for personalized health insights and preventive solutions is increasing.

The Children segment, while smaller, is also showing promising growth. This is primarily attributed to the increasing use of mHealth for pediatric chronic disease management, remote monitoring of specific conditions, and parental oversight of children's health and activity levels.

Neurological Monitoring Devices and ECG Monitors are emerging segments with significant growth potential. Advancements in AI-powered diagnostics and the increasing need for early detection of neurological disorders and cardiac abnormalities are driving the development and adoption of these sophisticated mHealth solutions. While currently niche, their impact on managing critical health conditions is substantial and expected to grow. The "Others" category, encompassing a wide range of devices from sleep trackers to remote diagnostics tools, is also a dynamic area, constantly evolving with new technological innovations.

Consumer mHealth Product Developments

Recent product developments in Consumer mHealth focus on enhanced accuracy, improved user experience, and seamless data integration. Innovations include miniaturized biosensors for continuous, non-invasive monitoring, AI-powered diagnostic algorithms for early disease detection, and the development of more sophisticated wearable devices that track a broader range of physiological parameters. Applications are expanding beyond basic fitness tracking to include comprehensive chronic disease management platforms, mental wellness support, and personalized health coaching. Competitive advantages are being gained through advanced data analytics capabilities, strong partnerships with healthcare providers, and user-friendly interfaces that promote consistent engagement. Companies are also prioritizing the development of devices that offer greater personalization and actionable insights, moving from simple data collection to providing meaningful health guidance.

Report Scope & Segmentation Analysis

This report meticulously analyzes the global Consumer mHealth market, encompassing a comprehensive segmentation across key applications and device types. The application segments include Adults, Teenagers, and Children. Growth projections for the Adults segment are robust, driven by chronic disease management needs, with projected market sizes in the tens of millions. For Teenagers, growth is fueled by fitness and wellness trends, with increasing market penetration. The Children segment, though smaller, shows steady growth, particularly in remote monitoring and management of specific pediatric conditions.

Device type segmentation includes Blood Glucose Meters, Blood Pressure Monitors, Neurological Monitoring Devices, ECG Monitors, and Others. Blood Glucose Meters and Blood Pressure Monitors represent mature yet growing markets, with significant market sizes in the hundreds of millions due to high prevalence of related chronic conditions. Neurological Monitoring Devices and ECG Monitors are emerging segments with high growth potential, driven by technological advancements and increasing adoption for early diagnosis and ongoing patient care. The competitive dynamics within each segment vary, with some being highly competitive and others presenting opportunities for specialized innovators.

Key Drivers of Consumer mHealth Growth

The growth of the Consumer mHealth market is propelled by several key drivers. Firstly, the increasing prevalence of chronic diseases such as diabetes, hypertension, and cardiovascular conditions globally necessitates continuous monitoring and management, which mHealth solutions effectively provide. Secondly, the rapid advancements in wearable technology and sensor innovation are leading to more accurate, sophisticated, and user-friendly devices. Thirdly, a growing global health consciousness and the desire for personalized health insights empower individuals to take a more proactive role in managing their well-being. Fourthly, the widespread adoption of smartphones and the continuous evolution of mobile internet infrastructure are creating a fertile ground for the proliferation of mHealth applications and services. Finally, supportive government initiatives and regulatory frameworks in various regions are encouraging the development and adoption of digital health solutions.

Challenges in the Consumer mHealth Sector

Despite its immense growth potential, the Consumer mHealth sector faces several significant challenges. Regulatory hurdles and the lack of standardized approval processes for certain mHealth devices can impede market entry and product innovation. Data privacy and security concerns remain paramount, as the collection of sensitive health information requires robust safeguards to maintain user trust. Interoperability issues between different mHealth platforms and existing healthcare systems can limit seamless data sharing and integration, impacting the comprehensive care continuum. Furthermore, the cost of advanced mHealth devices and the need for digital literacy among certain population segments can create barriers to access, particularly in developing regions. Fierce competition and the rapid pace of technological change also pressure companies to constantly innovate and adapt, which can be resource-intensive.

Emerging Opportunities in Consumer mHealth

The Consumer mHealth sector is ripe with emerging opportunities. The integration of AI and machine learning for predictive analytics and personalized health interventions offers a significant avenue for growth, enabling earlier disease detection and more effective treatment strategies. The expansion of telehealth services, supported by mHealth platforms, presents an opportunity to improve healthcare access and affordability, especially in remote or underserved areas. The growing demand for mental health and wellness tracking applications, coupled with stress management tools, opens up new market segments. Furthermore, the increasing focus on preventive healthcare and early intervention strategies positions mHealth as a crucial tool for population health management. The development of more advanced and non-invasive biosensors, along with the continued evolution of wearable technology, will unlock new applications and enhance the capabilities of existing devices.

Leading Players in the Consumer mHealth Market

- Vodafone

- Apple

- NTT Docomo

- Samsung Electronics

- AT&T Services

- Healthdirect

- MQure Health

- Allscripts Healthcare Solutions

- Qualcomm

Key Developments in Consumer mHealth Industry

- 2023 Q4: Launch of advanced AI-powered diagnostic features integrated into smartwatches by major tech companies, enhancing early detection capabilities for cardiac irregularities.

- 2024 Q1: Significant M&A activity involving the acquisition of specialized remote patient monitoring solution providers by larger healthcare technology firms, aiming to expand service offerings.

- 2024 Q2: Introduction of new non-invasive glucose monitoring sensors by leading medical device manufacturers, promising greater comfort and accuracy for diabetic patients.

- 2024 Q3: Expansion of 5G network coverage and its integration with mHealth devices, enabling real-time data transmission for critical care applications.

- 2024 Q4: Increased partnerships between telecommunication companies and healthcare providers to offer bundled mHealth solutions and services to consumers.

- 2025 Q1: Regulatory bodies in North America and Europe streamline approval processes for certain mHealth applications, accelerating market entry for innovative solutions.

Strategic Outlook for Consumer mHealth Market

The strategic outlook for the Consumer mHealth market remains exceptionally positive, fueled by a relentless drive towards personalized, accessible, and proactive healthcare. Future growth will be significantly catalyzed by the deeper integration of AI and machine learning, enabling sophisticated predictive analytics and hyper-personalized health interventions. The expansion of telehealth, bolstered by robust mHealth infrastructure, will democratize healthcare access, particularly for chronic disease management and routine health monitoring. As technology continues to advance, leading to more accurate and diverse biosensing capabilities, the scope of mHealth applications will broaden, encompassing mental wellness, preventative diagnostics, and enhanced elderly care. Strategic collaborations between technology giants, healthcare providers, and telecommunication companies will be crucial in building integrated ecosystems that deliver seamless and comprehensive health management solutions, positioning the Consumer mHealth market for sustained and significant expansion in the coming years.

Consumer mHealth Segmentation

-

1. Application

- 1.1. Adults

- 1.2. Teenagers

- 1.3. Children

-

2. Types

- 2.1. Blood Glucose Meters

- 2.2. Blood Pressure Monitors

- 2.3. Neurological Monitoring Devices

- 2.4. ECG Monitors

- 2.5. Others

Consumer mHealth Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Consumer mHealth Regional Market Share

Geographic Coverage of Consumer mHealth

Consumer mHealth REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Adults

- 5.1.2. Teenagers

- 5.1.3. Children

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Blood Glucose Meters

- 5.2.2. Blood Pressure Monitors

- 5.2.3. Neurological Monitoring Devices

- 5.2.4. ECG Monitors

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Consumer mHealth Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Adults

- 6.1.2. Teenagers

- 6.1.3. Children

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Blood Glucose Meters

- 6.2.2. Blood Pressure Monitors

- 6.2.3. Neurological Monitoring Devices

- 6.2.4. ECG Monitors

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Consumer mHealth Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Adults

- 7.1.2. Teenagers

- 7.1.3. Children

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Blood Glucose Meters

- 7.2.2. Blood Pressure Monitors

- 7.2.3. Neurological Monitoring Devices

- 7.2.4. ECG Monitors

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Consumer mHealth Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Adults

- 8.1.2. Teenagers

- 8.1.3. Children

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Blood Glucose Meters

- 8.2.2. Blood Pressure Monitors

- 8.2.3. Neurological Monitoring Devices

- 8.2.4. ECG Monitors

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Consumer mHealth Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Adults

- 9.1.2. Teenagers

- 9.1.3. Children

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Blood Glucose Meters

- 9.2.2. Blood Pressure Monitors

- 9.2.3. Neurological Monitoring Devices

- 9.2.4. ECG Monitors

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Consumer mHealth Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Adults

- 10.1.2. Teenagers

- 10.1.3. Children

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Blood Glucose Meters

- 10.2.2. Blood Pressure Monitors

- 10.2.3. Neurological Monitoring Devices

- 10.2.4. ECG Monitors

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Consumer mHealth Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Adults

- 11.1.2. Teenagers

- 11.1.3. Children

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Blood Glucose Meters

- 11.2.2. Blood Pressure Monitors

- 11.2.3. Neurological Monitoring Devices

- 11.2.4. ECG Monitors

- 11.2.5. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Vodafone

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Apple

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 NTT Docomo

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Samsung Electronics

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 AT&T Services

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Healthdirect

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 MQure Health

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Allscripts Healthcare Solutions

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Qualcomm

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.1 Vodafone

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Consumer mHealth Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Consumer mHealth Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Consumer mHealth Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Consumer mHealth Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Consumer mHealth Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Consumer mHealth Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Consumer mHealth Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Consumer mHealth Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Consumer mHealth Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Consumer mHealth Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Consumer mHealth Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Consumer mHealth Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Consumer mHealth Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Consumer mHealth Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Consumer mHealth Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Consumer mHealth Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Consumer mHealth Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Consumer mHealth Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Consumer mHealth Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Consumer mHealth Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Consumer mHealth Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Consumer mHealth Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Consumer mHealth Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Consumer mHealth Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Consumer mHealth Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Consumer mHealth Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Consumer mHealth Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Consumer mHealth Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Consumer mHealth Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Consumer mHealth Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Consumer mHealth Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Consumer mHealth Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Consumer mHealth Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Consumer mHealth Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Consumer mHealth Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Consumer mHealth Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Consumer mHealth Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Consumer mHealth Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Consumer mHealth Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Consumer mHealth Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Consumer mHealth Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Consumer mHealth Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Consumer mHealth Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Consumer mHealth Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Consumer mHealth Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Consumer mHealth Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Consumer mHealth Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Consumer mHealth Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Consumer mHealth Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Consumer mHealth Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Consumer mHealth?

The projected CAGR is approximately 14.1%.

2. Which companies are prominent players in the Consumer mHealth?

Key companies in the market include Vodafone, Apple, NTT Docomo, Samsung Electronics, AT&T Services, Healthdirect, MQure Health, Allscripts Healthcare Solutions, Qualcomm.

3. What are the main segments of the Consumer mHealth?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 62.7 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Consumer mHealth," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Consumer mHealth report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Consumer mHealth?

To stay informed about further developments, trends, and reports in the Consumer mHealth, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence