Key Insights

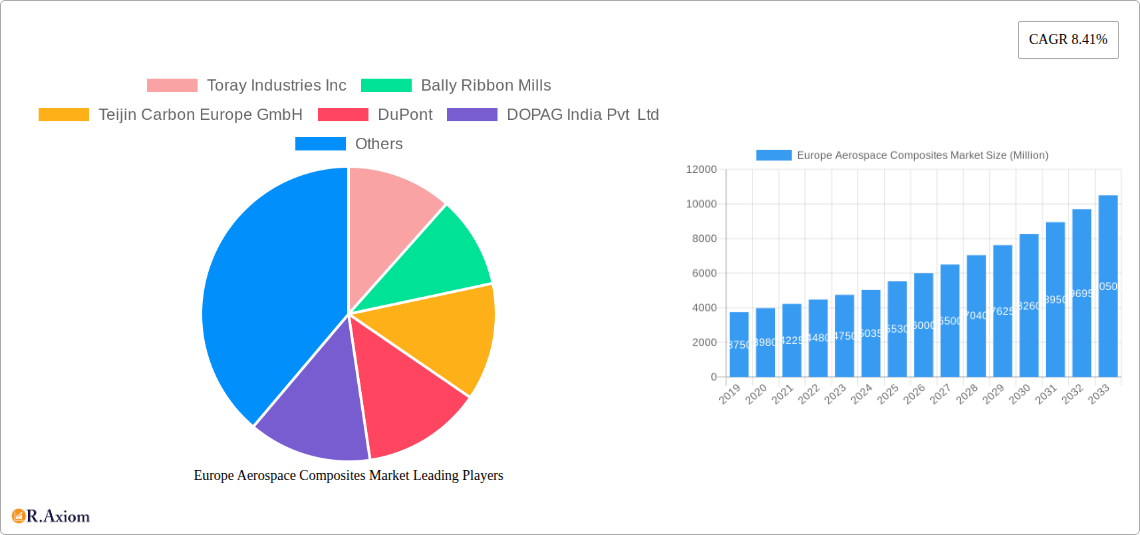

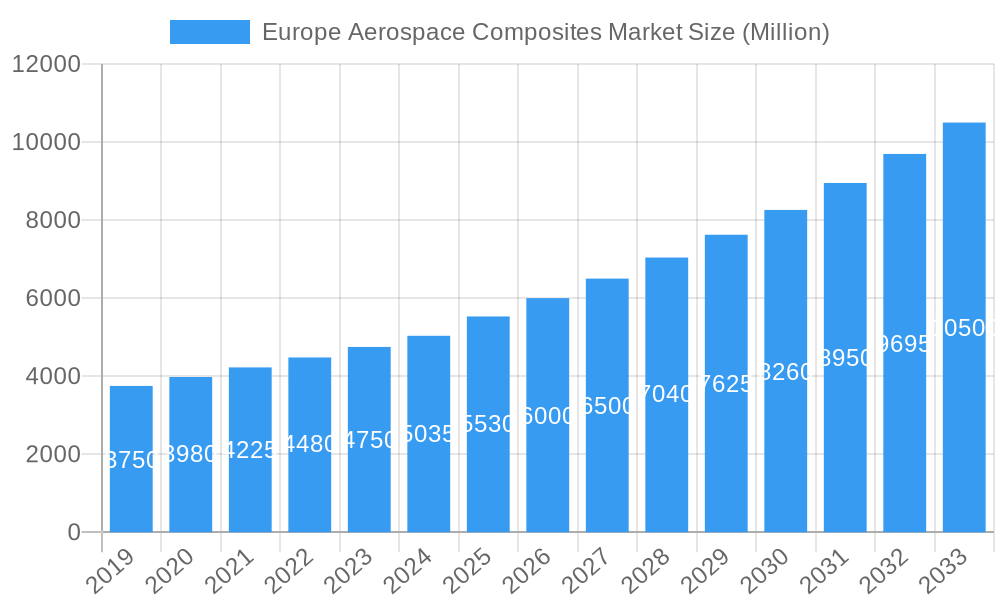

The Europe Aerospace Composites Market is poised for significant expansion, projected to reach a substantial value of $5.53 billion by 2025, with an anticipated Compound Annual Growth Rate (CAGR) of 8.41% through 2033. This robust growth is primarily fueled by the increasing demand for lightweight yet strong materials in both commercial and military aviation sectors, driven by stringent fuel efficiency regulations and the continuous pursuit of enhanced aircraft performance. Advanced composite materials, such as carbon fiber and glass fiber, are integral to modern aircraft design, enabling reductions in structural weight, which translates to lower fuel consumption and reduced environmental impact. The burgeoning space exploration initiatives across Europe also contribute significantly to this upward trajectory, with composites being crucial for spacecraft construction due to their high strength-to-weight ratios and resistance to extreme conditions. Emerging trends like the adoption of thermoplastic composites for faster manufacturing cycles and improved recyclability, alongside innovations in resin systems and manufacturing techniques, are further propelling market adoption.

Europe Aerospace Composites Market Market Size (In Billion)

However, the market faces certain restraints, including the high initial cost of raw materials and the complex manufacturing processes associated with aerospace composites, which can lead to higher aircraft development and maintenance expenses. Stringent certification requirements and the need for specialized workforce training also present challenges. Despite these hurdles, the unwavering commitment to innovation, coupled with increasing investments in research and development by key players like Toray Industries Inc., Hexcel Corporation, and Solvay SA, is expected to mitigate these limitations. Regional growth in Europe is particularly strong, with the United Kingdom, Germany, and France leading the adoption of advanced composites across their significant aerospace industries, driven by a strong aerospace manufacturing base and ongoing modernization programs for both civil and defense aircraft. The integration of composites into newer aircraft models and the retrofitting of existing fleets are key strategies for market players to capitalize on the sustained demand.

Europe Aerospace Composites Market Company Market Share

This in-depth report provides a detailed analysis of the Europe Aerospace Composites Market, offering critical insights for stakeholders navigating this dynamic sector. Covering the historical period of 2019–2024 and projecting through to 2033, with a base year of 2025, this study examines market dynamics, growth drivers, challenges, and emerging opportunities. We delve into key segments including Fiber Type (Glass Fiber, Carbon Fiber, Ceramic Fiber, Other Fiber Types) and Application (Commercial Aviation, Military Aviation, General Aviation, Space), and analyze the strategies of leading players shaping the future of aerospace composites.

Europe Aerospace Composites Market Market Concentration & Innovation

The Europe Aerospace Composites Market exhibits a moderate to high level of concentration, driven by the significant capital investment required for research, development, and manufacturing. Key innovation drivers include the persistent demand for lighter, stronger, and more fuel-efficient aircraft, alongside advancements in material science and manufacturing processes. Regulatory frameworks, such as EASA (European Union Aviation Safety Agency) certifications, play a crucial role, ensuring stringent safety and performance standards, thereby influencing product development and market entry. While direct product substitutes are limited due to the specialized nature of aerospace composites, incremental material improvements and alternative manufacturing techniques represent indirect competitive pressures. End-user trends are heavily influenced by the commercial aviation sector's focus on cost reduction and emissions targets, and the military sector's drive for enhanced performance and survivability. Mergers & Acquisitions (M&A) activities are strategically employed by major players to consolidate market share, acquire new technologies, and expand their geographical reach. For instance, recent M&A activities, with reported deal values often in the hundreds of millions of Euros, aim to integrate specialized composite expertise and accelerate product development cycles. Market share distribution indicates a strong presence of established composite manufacturers with robust R&D capabilities.

Europe Aerospace Composites Market Industry Trends & Insights

The Europe Aerospace Composites Market is poised for significant expansion, fueled by a confluence of technological advancements, evolving aircraft designs, and increasing global demand for air travel. The compound annual growth rate (CAGR) is projected to be robust, driven by the inherent advantages of composite materials – superior strength-to-weight ratios, corrosion resistance, and design flexibility. These properties are paramount in the aerospace industry, where fuel efficiency, payload capacity, and structural integrity are critical. Technological disruptions, including the adoption of automated manufacturing processes, additive manufacturing (3D printing) of composite parts, and the development of novel resin systems and fiber reinforcements, are reshaping production capabilities and enabling more complex designs. Consumer preferences, particularly within the commercial aviation sector, are increasingly prioritizing sustainability and reduced environmental impact, which directly benefits the adoption of lightweight composite materials that contribute to lower fuel consumption and emissions. Competitive dynamics are characterized by intense innovation and strategic partnerships between material suppliers, component manufacturers, and aircraft OEMs. Market penetration of advanced composites is steadily increasing across various aircraft platforms, from next-generation commercial airliners to advanced military jets and emerging space exploration vehicles. The continuous quest for optimized performance metrics, such as reduced fatigue life, enhanced thermal management, and improved acoustic damping, further propels the market forward.

Dominant Markets & Segments in Europe Aerospace Composites Market

Dominant Region: Western Europe, particularly Germany, France, the UK, and Italy, continues to be the dominant market for aerospace composites in Europe. This dominance is attributed to the presence of major aircraft manufacturers, a well-established aerospace supply chain, significant R&D investments, and supportive government policies fostering innovation and production.

Dominant Country: Germany stands out as a leading country due to its strong engineering base, advanced manufacturing capabilities, and the presence of key players in both material production and component manufacturing.

Dominant Fiber Type:

- Carbon Fiber: This segment holds the largest market share and is expected to exhibit the highest growth.

- Key Drivers: Its exceptional strength-to-weight ratio is crucial for weight reduction, leading to improved fuel efficiency in aircraft. Advancements in carbon fiber production technologies are making it more cost-competitive. Increasing use in primary and secondary aircraft structures, engine components, and satellite systems.

- Detailed Dominance Analysis: The aerospace industry’s relentless pursuit of performance enhancement and fuel economy directly translates into a high demand for carbon fiber. Its application extends from fuselage and wing structures to empennages and control surfaces, where its structural integrity and fatigue resistance are indispensable. The growing development of wide-body aircraft and the increasing complexity of military aircraft designs further solidify carbon fiber's dominant position.

Dominant Application:

- Commercial Aviation: This is the largest and fastest-growing application segment.

- Key Drivers: The need for lighter aircraft to reduce fuel consumption and emissions is a primary driver. The continuous modernization of global airline fleets and the introduction of new fuel-efficient aircraft models significantly boost demand. Increasing passenger traffic and the demand for long-haul flights necessitate more efficient aircraft, making composites indispensable.

- Detailed Dominance Analysis: The commercial aviation sector accounts for the lion's share of aerospace composite consumption due to the sheer volume of aircraft produced and the stringent weight-saving requirements. The development of single-aisle and wide-body aircraft by major OEMs, such as Airbus and Boeing, heavily relies on composite materials for structural components. This segment is expected to continue its dominance as airlines prioritize operational cost efficiency and environmental compliance.

Europe Aerospace Composites Market Product Developments

The Europe Aerospace Composites Market is characterized by continuous innovation in materials and manufacturing processes. Recent product developments focus on enhancing material properties such as improved fracture toughness, higher temperature resistance, and enhanced fire retardancy. Novel resin systems and curing techniques are being developed to accelerate production cycles and reduce manufacturing costs. The application of advanced composites is expanding beyond traditional structural components to include interior elements, engine parts, and even complex sub-assemblies. These innovations provide manufacturers with a competitive advantage by enabling lighter, stronger, and more durable aircraft structures, ultimately leading to improved performance, reduced maintenance, and enhanced safety. The market is witnessing a trend towards the development of integrated composite solutions, where materials and manufacturing processes are optimized in tandem to meet specific performance requirements.

Report Scope & Segmentation Analysis

This report segments the Europe Aerospace Composites Market by Fiber Type, including Glass Fiber, Carbon Fiber, Ceramic Fiber, and Other Fiber Types. It also segments the market by Application, encompassing Commercial Aviation, Military Aviation, General Aviation, and Space.

- Glass Fiber: While traditionally used in less critical applications, advancements are enhancing its use in certain aerospace components. Its market share is smaller compared to carbon fiber but remains relevant for specific structural and interior applications.

- Carbon Fiber: Dominant in the market due to its superior mechanical properties, enabling significant weight reduction and enhanced performance. Projections indicate continued strong growth driven by next-generation aircraft.

- Ceramic Fiber: Primarily used in high-temperature applications within engines and exhaust systems, offering excellent thermal insulation and resistance. Its market share is niche but critical for specific specialized uses.

- Other Fiber Types: This category may include aramid fibers and other specialized reinforcements that offer unique properties for specific aerospace applications. Their market penetration is evolving with technological advancements.

- Commercial Aviation: The largest application segment, driven by the demand for fuel-efficient passenger and cargo aircraft. This segment is expected to maintain its leading position with consistent growth.

- Military Aviation: Significant demand driven by the need for high-performance, durable, and stealthy aircraft. Advanced composite usage is critical for modern fighter jets and surveillance platforms.

- General Aviation: This segment includes smaller aircraft and business jets, where weight reduction and cost-effectiveness are key considerations. Growth is steady, influenced by economic conditions and private travel trends.

- Space: A rapidly growing segment driven by the expansion of satellite constellations, space exploration missions, and the burgeoning commercial space industry. Composites are essential for lightweight and high-strength spacecraft structures.

Key Drivers of Europe Aerospace Composites Market Growth

The Europe Aerospace Composites Market is propelled by several key drivers. Firstly, the unwavering demand for lightweight materials to enhance fuel efficiency and reduce carbon emissions in commercial aviation is a primary catalyst. Secondly, advancements in material science and manufacturing technologies, such as automated fiber placement and resin infusion, are making composites more accessible and cost-effective. Thirdly, the increasing demand for next-generation military aircraft with superior performance characteristics, including stealth capabilities and enhanced maneuverability, necessitates the extensive use of advanced composites. Fourthly, the burgeoning space sector, with its ambitious missions and expanding satellite constellations, relies heavily on the high strength-to-weight ratio and durability of composite materials. Finally, supportive government initiatives and aerospace industry investments in research and development further fuel innovation and market expansion.

Challenges in the Europe Aerospace Composites Market Sector

Despite robust growth prospects, the Europe Aerospace Composites Market faces several challenges. High initial investment costs for advanced manufacturing facilities and specialized equipment can be a significant barrier, particularly for smaller players. Stringent regulatory approval processes for new composite materials and components add to development timelines and costs. The availability and price volatility of raw materials, especially precursor fibers like carbon fiber, can impact production costs and supply chain stability. Skilled labor shortages in composite manufacturing and repair also pose a challenge. Furthermore, the inherent complexity of composite structures can lead to higher maintenance and repair costs compared to traditional metallic structures, requiring specialized training and infrastructure. Competitive pressures from alternative materials and emerging manufacturing techniques also demand continuous innovation and cost optimization.

Emerging Opportunities in Europe Aerospace Composites Market

The Europe Aerospace Composites Market presents numerous emerging opportunities. The increasing focus on sustainable aviation and the development of advanced air mobility (AAM) solutions are creating new avenues for composite material applications. The expansion of the global satellite market and the increasing complexity of spacecraft designs will drive demand for high-performance composites. Furthermore, advancements in recycling technologies for composite materials offer opportunities for a more circular economy within the aerospace sector. The development of smart composites with integrated sensing capabilities for structural health monitoring presents another significant growth area. The growing demand for regional jets and the modernization of existing aircraft fleets also provide substantial opportunities for composite suppliers. Innovations in additive manufacturing of composite parts are enabling the production of highly complex geometries, opening doors for new design possibilities and reduced part counts.

Leading Players in the Europe Aerospace Composites Market Market

- Toray Industries Inc

- Bally Ribbon Mills

- Teijin Carbon Europe GmbH

- DuPont

- DOPAG India Pvt Ltd

- Solvay SA

- Belotti SpA

- Mitsubishi Chemical Carbon Fiber and Composites Inc

- Hexcel Corporation

- Airborne

- SGL Carbon SE

- Materion Corporation

Key Developments in Europe Aerospace Composites Market Industry

- March 2023: SGL Carbon revealed the new SIGRAFIL T50-4.9/235 carbon fiber, thereby expanding its material portfolio with new carbon fiber for high-strength pressure vessels.

- March 2022: Solvay and Wichita State University's National Institute for Aviation Research (NIAR) announced a partnership on research and materials development at NIAR's facilities in Wichita, Kansas. The partnership is aimed at developing future solutions to bolster the aviation industry and create opportunities for companies of all sizes to revolutionize the future of flight.

Strategic Outlook for Europe Aerospace Composites Market Market

The strategic outlook for the Europe Aerospace Composites Market remains exceptionally positive, driven by the sector's commitment to innovation and sustainability. Key growth catalysts include the continuous development of lighter and stronger composite materials that directly translate into enhanced aircraft performance and reduced environmental impact. Investments in advanced manufacturing technologies, such as automation and additive manufacturing, will further optimize production processes and reduce costs, making composites more competitive. The growing demand from the commercial aviation sector for fleet modernization, coupled with the expansion of the space industry and the emergence of advanced air mobility, presents significant market potential. Strategic collaborations between material suppliers, component manufacturers, and aircraft OEMs will be crucial for developing integrated solutions and addressing complex design challenges. The ongoing push for sustainable aviation solutions will undoubtedly favor the adoption of composite materials, solidifying their indispensable role in the future of flight.

Europe Aerospace Composites Market Segmentation

-

1. Fiber Type

- 1.1. Glass Fiber

- 1.2. Carbon Fiber

- 1.3. Ceramic Fiber

- 1.4. Other Fiber Types

-

2. Application

- 2.1. Commercial Aviation

- 2.2. Military Aviation

- 2.3. General Aviation

- 2.4. Space

Europe Aerospace Composites Market Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Aerospace Composites Market Regional Market Share

Geographic Coverage of Europe Aerospace Composites Market

Europe Aerospace Composites Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.41% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Fiber Type

- 5.1.1. Glass Fiber

- 5.1.2. Carbon Fiber

- 5.1.3. Ceramic Fiber

- 5.1.4. Other Fiber Types

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Commercial Aviation

- 5.2.2. Military Aviation

- 5.2.3. General Aviation

- 5.2.4. Space

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Fiber Type

- 6. Europe Aerospace Composites Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Fiber Type

- 6.1.1. Glass Fiber

- 6.1.2. Carbon Fiber

- 6.1.3. Ceramic Fiber

- 6.1.4. Other Fiber Types

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Commercial Aviation

- 6.2.2. Military Aviation

- 6.2.3. General Aviation

- 6.2.4. Space

- 6.1. Market Analysis, Insights and Forecast - by Fiber Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Toray Industries Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Bally Ribbon Mills

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Teijin Carbon Europe GmbH

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 DuPont

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 DOPAG India Pvt Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Solvay SA

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Belotti SpA

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Mitsubishi Chemical Carbon Fiber and Composites Inc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Hexcel Corporation

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Airborne

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 SGL Carbon SE

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Materion Corporation

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Toray Industries Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Aerospace Composites Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe Aerospace Composites Market Share (%) by Company 2025

List of Tables

- Table 1: Europe Aerospace Composites Market Revenue Million Forecast, by Fiber Type 2020 & 2033

- Table 2: Europe Aerospace Composites Market Revenue Million Forecast, by Application 2020 & 2033

- Table 3: Europe Aerospace Composites Market Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Europe Aerospace Composites Market Revenue Million Forecast, by Fiber Type 2020 & 2033

- Table 5: Europe Aerospace Composites Market Revenue Million Forecast, by Application 2020 & 2033

- Table 6: Europe Aerospace Composites Market Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United Kingdom Europe Aerospace Composites Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Germany Europe Aerospace Composites Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: France Europe Aerospace Composites Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Italy Europe Aerospace Composites Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Spain Europe Aerospace Composites Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Netherlands Europe Aerospace Composites Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Belgium Europe Aerospace Composites Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Sweden Europe Aerospace Composites Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Norway Europe Aerospace Composites Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Poland Europe Aerospace Composites Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Denmark Europe Aerospace Composites Market Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Aerospace Composites Market?

The projected CAGR is approximately 8.41%.

2. Which companies are prominent players in the Europe Aerospace Composites Market?

Key companies in the market include Toray Industries Inc, Bally Ribbon Mills, Teijin Carbon Europe GmbH, DuPont, DOPAG India Pvt Ltd, Solvay SA, Belotti SpA, Mitsubishi Chemical Carbon Fiber and Composites Inc, Hexcel Corporation, Airborne, SGL Carbon SE, Materion Corporation.

3. What are the main segments of the Europe Aerospace Composites Market?

The market segments include Fiber Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.53 Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Commercial Aviation Segment to Continue its Dominance During the Forecast Period.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

March 2023: SGL Carbon revealed the new SIGRAFIL T50-4.9/235 carbon fiber, thereby expanding its material portfolio with new carbon fiber for high-strength pressure vessels.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Aerospace Composites Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Aerospace Composites Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Aerospace Composites Market?

To stay informed about further developments, trends, and reports in the Europe Aerospace Composites Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence