Key Insights

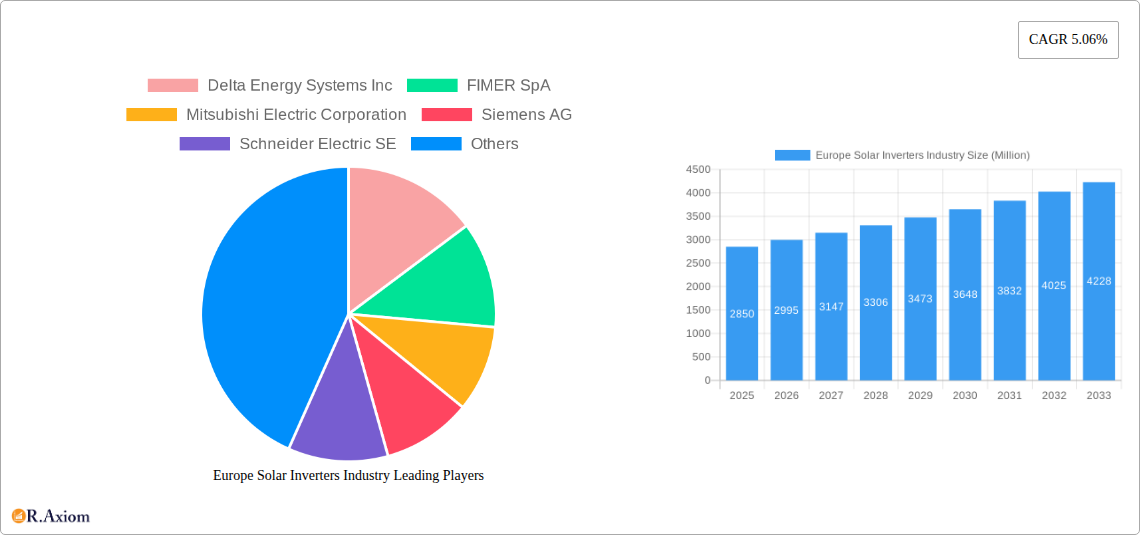

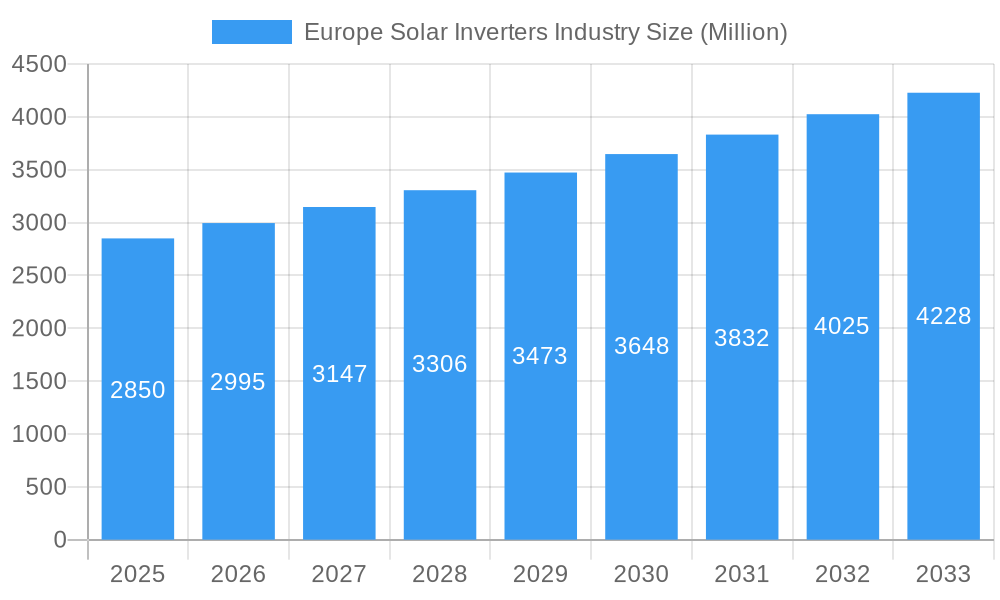

The European solar inverter market is poised for significant expansion, with a projected market size of USD 2.85 billion in 2025. Driven by a robust CAGR of 5.06%, the market is expected to reach approximately USD 3.80 billion by 2033. This growth is primarily fueled by escalating government initiatives and supportive policies promoting renewable energy adoption across the continent, coupled with a growing awareness of climate change and the urgent need for sustainable energy solutions. Furthermore, declining costs of solar panels and advancements in inverter technology, leading to improved efficiency and reliability, are also key contributors. The increasing demand for energy independence and the desire to reduce reliance on fossil fuels are further bolstering the market's upward trajectory. Europe's commitment to ambitious renewable energy targets, such as those outlined in the EU Green Deal, provides a strong regulatory push for solar installations, thereby directly stimulating the demand for solar inverters.

Europe Solar Inverters Industry Market Size (In Billion)

The market segmentation reveals a dynamic landscape with substantial opportunities across various inverter types and applications. String inverters currently dominate the market due to their cost-effectiveness and suitability for a wide range of solar projects, from residential to large-scale utility operations. However, microinverters are gaining traction, particularly in residential and commercial applications, offering benefits like enhanced energy harvesting and module-level monitoring. Central inverters continue to be a crucial component for large utility-scale projects. The application segments are equally diverse, with residential installations experiencing consistent growth driven by prosumer trends and self-consumption goals. The commercial and industrial (C&I) sector is also a significant growth engine, as businesses increasingly invest in solar to lower operational costs and improve their environmental footprint. Utility-scale projects, while requiring substantial initial investment, remain a cornerstone of Europe's renewable energy strategy, further solidifying the demand for solar inverters across all segments. Key players like Huawei Technologies Co. Ltd, SMA Solar Technology AG, and Schneider Electric SE are actively shaping the market through innovation and strategic expansion.

Europe Solar Inverters Industry Company Market Share

This comprehensive report delves into the dynamic Europe Solar Inverters Industry, providing an in-depth analysis of market dynamics, key players, technological advancements, and future projections. Covering the study period from 2019 to 2033, with a base year of 2025, this report offers invaluable insights for stakeholders seeking to understand and capitalize on the evolving solar energy landscape in Europe.

Europe Solar Inverters Industry Market Concentration & Innovation

The Europe Solar Inverters Industry exhibits a moderate to high degree of market concentration, with several dominant players vying for market share. Innovation is a critical differentiator, driven by the constant pursuit of higher efficiency, enhanced grid integration, and advanced digital features. Regulatory frameworks, such as renewable energy targets and grid connection standards, play a pivotal role in shaping market entry and product development. The threat of product substitutes, while currently limited for core inverter functionalities, is an ongoing consideration as emerging energy storage and management solutions evolve. End-user preferences are increasingly leaning towards smart inverters with remote monitoring capabilities and seamless integration with home energy management systems. Merger and acquisition (M&A) activities, though not extensively documented with precise values, are strategically important for market consolidation and technology acquisition, aiming to enhance competitive positioning.

- Innovation Drivers: Increased energy efficiency, advanced grid management features, smart grid compatibility, cybersecurity enhancements, and hybrid inverter solutions.

- Regulatory Frameworks: EU directives on renewable energy, national feed-in tariffs, grid connection codes, and energy efficiency standards.

- End-User Trends: Demand for integrated energy solutions, smart home connectivity, enhanced system reliability, and cost-effectiveness.

- M&A Activities: Strategic acquisitions to expand product portfolios, gain market access, and acquire advanced technologies.

Europe Solar Inverters Industry Industry Trends & Insights

The Europe Solar Inverters Industry is experiencing robust growth, fueled by escalating demand for renewable energy sources and supportive government policies. The compound annual growth rate (CAGR) is projected to remain strong throughout the forecast period (2025–2033), driven by the urgent need to decarbonize the European energy sector and achieve ambitious climate targets. Technological disruptions are at the forefront, with advancements in inverter efficiency, the integration of artificial intelligence (AI) for performance optimization, and the development of advanced grid-forming capabilities. Consumer preferences are shifting towards higher power density, improved reliability, and user-friendly interfaces with sophisticated monitoring and control systems. Competitive dynamics are characterized by intense rivalry among established global manufacturers and emerging regional players, each striving to capture market share through product differentiation and strategic partnerships. Market penetration of solar inverters is expected to deepen across all segments, driven by declining solar panel costs and increasing awareness of the benefits of solar energy. The industry is witnessing a trend towards digitalization, with a focus on smart inverters that offer enhanced functionality, such as predictive maintenance and demand-response capabilities. The growing adoption of battery energy storage systems (BESS) is also influencing inverter development, leading to the rise of hybrid inverters that seamlessly manage both solar generation and energy storage.

Dominant Markets & Segments in Europe Solar Inverters Industry

The Europe Solar Inverters Industry is characterized by a dynamic landscape of dominant markets and segments. The Utility-scale application segment is a significant driver of growth, owing to large-scale solar power plant development across the continent. Key economic policies, such as renewable energy auctions and power purchase agreements (PPAs), coupled with substantial infrastructure investments in grid modernization, are instrumental in this dominance.

- Utility-scale Dominance Drivers:

- Ambitious renewable energy targets set by the European Union and individual member states.

- Declining levelized cost of electricity (LCOE) for solar power, making it competitive with traditional energy sources.

- Large-scale solar farm projects supported by favorable financing mechanisms and long-term contracts.

- Government incentives and subsidies for utility-scale solar installations.

- Technological advancements in high-capacity inverters suited for large solar parks.

In terms of inverter types, String Inverters continue to hold a dominant position due to their cost-effectiveness and versatility for a wide range of solar installations, from residential to commercial and industrial applications. Their ease of installation and modularity make them a preferred choice for many projects.

- String Inverter Dominance Drivers:

- Cost-competitiveness compared to central inverters for medium to large installations.

- Flexibility in system design and scalability for diverse project sizes.

- Proven reliability and widespread availability of models from leading manufacturers.

- Simpler installation and maintenance requirements.

The Commercial and Industrial (C&I) application segment is also experiencing substantial growth, driven by businesses seeking to reduce energy costs, enhance sustainability, and gain energy independence. Government initiatives promoting corporate solar adoption and the increasing focus on environmental, social, and governance (ESG) criteria are major catalysts.

- Commercial and Industrial Segment Growth Drivers:

- Rising electricity prices and demand for energy cost reduction.

- Corporate sustainability goals and the demand for green energy procurement.

- Government incentives and tax benefits for on-site solar generation.

- Technological advancements in C&I-specific inverters, offering advanced monitoring and management features.

Europe Solar Inverters Industry Product Developments

Product development in the Europe Solar Inverters Industry is focused on enhancing efficiency, reliability, and smart capabilities. Innovations include advanced Maximum Power Point Tracking (MPPT) algorithms for optimized energy harvest, improved cooling mechanisms for extended lifespan, and integrated communication protocols for seamless grid interaction and remote monitoring. The trend towards hybrid inverters, capable of managing both solar power and battery storage, is gaining momentum, offering comprehensive energy management solutions. Competitive advantages are being built through superior energy conversion efficiency, robust build quality for diverse environmental conditions, and the integration of advanced digital features, such as predictive maintenance and cybersecurity measures, catering to the evolving demands of the solar energy market.

Report Scope & Segmentation Analysis

This report segments the Europe Solar Inverters Industry by Inverter Type, including Central Inverters, String Inverters, and Micro Inverters. Each segment is analyzed for its market size, growth projections, and competitive dynamics. Central Inverters are typically used in large-scale solar power plants, offering high power output but requiring specialized installation. String Inverters are a versatile choice for residential, commercial, and industrial applications, offering a balance of cost and performance. Micro Inverters are gaining traction in residential and small commercial systems, providing module-level optimization and enhanced safety features.

The market is further segmented by Application, encompassing Residential, Commercial and Industrial, and Utility-scale. The Residential segment is driven by homeowner adoption of solar for energy savings and sustainability. The Commercial and Industrial segment focuses on businesses seeking cost reduction and energy independence. The Utility-scale segment comprises large solar farms, catering to the growing demand for grid-scale renewable energy.

Key Drivers of Europe Solar Inverters Industry Growth

The Europe Solar Inverters Industry is propelled by several key drivers. Foremost among these are the ambitious renewable energy targets set by the European Union and individual member states, which necessitate a significant expansion of solar power capacity. Technological advancements leading to increased inverter efficiency and lower manufacturing costs are making solar energy more economically viable. Supportive government policies, including subsidies, tax incentives, and favorable feed-in tariffs, further stimulate market growth. Growing environmental awareness and the increasing demand for clean energy solutions from both consumers and corporations are also significant contributing factors.

Challenges in the Europe Solar Inverters Industry Sector

Despite the positive growth trajectory, the Europe Solar Inverters Industry faces several challenges. Intense competition among manufacturers can lead to price pressures and reduced profit margins. Supply chain disruptions, particularly for critical components, can impact production and delivery timelines. Evolving regulatory landscapes and complex grid connection standards across different European countries can create administrative hurdles. Furthermore, the intermittency of solar power requires robust grid integration solutions, necessitating ongoing investment in advanced inverter technology and grid infrastructure.

Emerging Opportunities in Europe Solar Inverters Industry

Emerging opportunities in the Europe Solar Inverters Industry are diverse and promising. The increasing integration of battery energy storage systems (BESS) presents a significant opportunity for hybrid inverter manufacturers. The growing demand for smart grid solutions and energy management systems creates a market for inverters with advanced digital capabilities. Expansion into emerging European markets with nascent solar industries, coupled with the development of solutions for decentralized energy generation and microgrids, offers further growth potential.

Leading Players in the Europe Solar Inverters Industry Market

- Delta Energy Systems Inc

- FIMER SpA

- Mitsubishi Electric Corporation

- Siemens AG

- Schneider Electric SE

- Omron Corporation

- KACO New Energy GmbH

- Huawei Technologies Co Ltd

- General Electric Company

- SMA Solar Technology AG

Key Developments in Europe Solar Inverters Industry Industry

- June 2022: SMA Solar Technology AG announced plans to build a solar inverter manufacturing facility in Niestetal, Germany. The new gigawatt factory is a part of the company’s target to double the production capacity from 21GW (present) to 40GW by 2024. The construction was expected to begin by the end of 2022.

- April 2022: SMA Solar Technology AG launched four new models of solar inverters for commercial and residential PV systems with power outputs of up to 135kW. The new Sunny Tripower-X models with ratings of 12kW, 15kW, 20kW, and 25kW feature an exclusive system manager, three independent MPP trackers, and six-string inputs. The inverters provide grid-compliant power control of entire systems and over-dimensioning PV systems by up to 150%.

Strategic Outlook for Europe Solar Inverters Industry Market

The strategic outlook for the Europe Solar Inverters Industry is highly positive, driven by the ongoing energy transition and a strong commitment to sustainable energy solutions. Key growth catalysts include continued innovation in inverter technology, focusing on higher efficiency, enhanced grid services, and seamless integration with energy storage. Strategic partnerships and collaborations will be crucial for market expansion and technological advancement. The increasing adoption of smart grid technologies and the development of decentralized energy systems will further boost demand for sophisticated inverter solutions. Manufacturers that can offer reliable, cost-effective, and feature-rich inverters, while adapting to evolving regulatory landscapes and consumer needs, are well-positioned for sustained success in this dynamic market.

Europe Solar Inverters Industry Segmentation

-

1. Inverter Type

- 1.1. Central Inverters

- 1.2. String Inverters

- 1.3. Micro Inverters

-

2. Application

- 2.1. Residential

- 2.2. Commercial and Industrial

- 2.3. Utility-scale

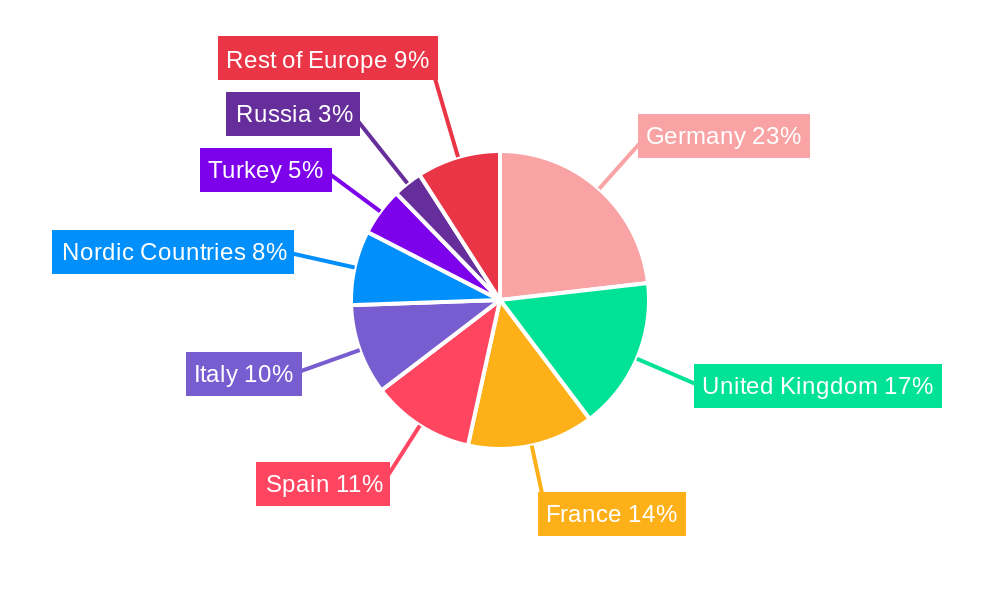

Europe Solar Inverters Industry Segmentation By Geography

- 1. Germany

- 2. United Kingdom

- 3. France

- 4. Spain

- 5. Italy

- 6. Nordic Countries

- 7. Turkey

- 8. Russia

- 9. Rest of Europe

Europe Solar Inverters Industry Regional Market Share

Geographic Coverage of Europe Solar Inverters Industry

Europe Solar Inverters Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.06% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Inverter Type

- 5.1.1. Central Inverters

- 5.1.2. String Inverters

- 5.1.3. Micro Inverters

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Residential

- 5.2.2. Commercial and Industrial

- 5.2.3. Utility-scale

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Germany

- 5.3.2. United Kingdom

- 5.3.3. France

- 5.3.4. Spain

- 5.3.5. Italy

- 5.3.6. Nordic Countries

- 5.3.7. Turkey

- 5.3.8. Russia

- 5.3.9. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Inverter Type

- 6. Europe Solar Inverters Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Inverter Type

- 6.1.1. Central Inverters

- 6.1.2. String Inverters

- 6.1.3. Micro Inverters

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Residential

- 6.2.2. Commercial and Industrial

- 6.2.3. Utility-scale

- 6.1. Market Analysis, Insights and Forecast - by Inverter Type

- 7. Germany Europe Solar Inverters Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Inverter Type

- 7.1.1. Central Inverters

- 7.1.2. String Inverters

- 7.1.3. Micro Inverters

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Residential

- 7.2.2. Commercial and Industrial

- 7.2.3. Utility-scale

- 7.1. Market Analysis, Insights and Forecast - by Inverter Type

- 8. United Kingdom Europe Solar Inverters Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Inverter Type

- 8.1.1. Central Inverters

- 8.1.2. String Inverters

- 8.1.3. Micro Inverters

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Residential

- 8.2.2. Commercial and Industrial

- 8.2.3. Utility-scale

- 8.1. Market Analysis, Insights and Forecast - by Inverter Type

- 9. France Europe Solar Inverters Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Inverter Type

- 9.1.1. Central Inverters

- 9.1.2. String Inverters

- 9.1.3. Micro Inverters

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Residential

- 9.2.2. Commercial and Industrial

- 9.2.3. Utility-scale

- 9.1. Market Analysis, Insights and Forecast - by Inverter Type

- 10. Spain Europe Solar Inverters Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Inverter Type

- 10.1.1. Central Inverters

- 10.1.2. String Inverters

- 10.1.3. Micro Inverters

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Residential

- 10.2.2. Commercial and Industrial

- 10.2.3. Utility-scale

- 10.1. Market Analysis, Insights and Forecast - by Inverter Type

- 11. Italy Europe Solar Inverters Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Inverter Type

- 11.1.1. Central Inverters

- 11.1.2. String Inverters

- 11.1.3. Micro Inverters

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Residential

- 11.2.2. Commercial and Industrial

- 11.2.3. Utility-scale

- 11.1. Market Analysis, Insights and Forecast - by Inverter Type

- 12. Nordic Countries Europe Solar Inverters Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Inverter Type

- 12.1.1. Central Inverters

- 12.1.2. String Inverters

- 12.1.3. Micro Inverters

- 12.2. Market Analysis, Insights and Forecast - by Application

- 12.2.1. Residential

- 12.2.2. Commercial and Industrial

- 12.2.3. Utility-scale

- 12.1. Market Analysis, Insights and Forecast - by Inverter Type

- 13. Turkey Europe Solar Inverters Industry Analysis, Insights and Forecast, 2020-2032

- 13.1. Market Analysis, Insights and Forecast - by Inverter Type

- 13.1.1. Central Inverters

- 13.1.2. String Inverters

- 13.1.3. Micro Inverters

- 13.2. Market Analysis, Insights and Forecast - by Application

- 13.2.1. Residential

- 13.2.2. Commercial and Industrial

- 13.2.3. Utility-scale

- 13.1. Market Analysis, Insights and Forecast - by Inverter Type

- 14. Russia Europe Solar Inverters Industry Analysis, Insights and Forecast, 2020-2032

- 14.1. Market Analysis, Insights and Forecast - by Inverter Type

- 14.1.1. Central Inverters

- 14.1.2. String Inverters

- 14.1.3. Micro Inverters

- 14.2. Market Analysis, Insights and Forecast - by Application

- 14.2.1. Residential

- 14.2.2. Commercial and Industrial

- 14.2.3. Utility-scale

- 14.1. Market Analysis, Insights and Forecast - by Inverter Type

- 15. Rest of Europe Europe Solar Inverters Industry Analysis, Insights and Forecast, 2020-2032

- 15.1. Market Analysis, Insights and Forecast - by Inverter Type

- 15.1.1. Central Inverters

- 15.1.2. String Inverters

- 15.1.3. Micro Inverters

- 15.2. Market Analysis, Insights and Forecast - by Application

- 15.2.1. Residential

- 15.2.2. Commercial and Industrial

- 15.2.3. Utility-scale

- 15.1. Market Analysis, Insights and Forecast - by Inverter Type

- 16. Competitive Analysis

- 16.1. Company Profiles

- 16.1.1 Delta Energy Systems Inc

- 16.1.1.1. Company Overview

- 16.1.1.2. Products

- 16.1.1.3. Company Financials

- 16.1.1.4. SWOT Analysis

- 16.1.2 FIMER SpA

- 16.1.2.1. Company Overview

- 16.1.2.2. Products

- 16.1.2.3. Company Financials

- 16.1.2.4. SWOT Analysis

- 16.1.3 Mitsubishi Electric Corporation

- 16.1.3.1. Company Overview

- 16.1.3.2. Products

- 16.1.3.3. Company Financials

- 16.1.3.4. SWOT Analysis

- 16.1.4 Siemens AG

- 16.1.4.1. Company Overview

- 16.1.4.2. Products

- 16.1.4.3. Company Financials

- 16.1.4.4. SWOT Analysis

- 16.1.5 Schneider Electric SE

- 16.1.5.1. Company Overview

- 16.1.5.2. Products

- 16.1.5.3. Company Financials

- 16.1.5.4. SWOT Analysis

- 16.1.6 Omron Corporation

- 16.1.6.1. Company Overview

- 16.1.6.2. Products

- 16.1.6.3. Company Financials

- 16.1.6.4. SWOT Analysis

- 16.1.7 KACO New Energy GmbH*List Not Exhaustive 6 4 Market Ranking/Share Analysi

- 16.1.7.1. Company Overview

- 16.1.7.2. Products

- 16.1.7.3. Company Financials

- 16.1.7.4. SWOT Analysis

- 16.1.8 Huawei Technologies Co Ltd

- 16.1.8.1. Company Overview

- 16.1.8.2. Products

- 16.1.8.3. Company Financials

- 16.1.8.4. SWOT Analysis

- 16.1.9 General Electric Company

- 16.1.9.1. Company Overview

- 16.1.9.2. Products

- 16.1.9.3. Company Financials

- 16.1.9.4. SWOT Analysis

- 16.1.10 SMA Solar Technology AG

- 16.1.10.1. Company Overview

- 16.1.10.2. Products

- 16.1.10.3. Company Financials

- 16.1.10.4. SWOT Analysis

- 16.1.1 Delta Energy Systems Inc

- 16.2. Market Entropy

- 16.2.1 Company's Key Areas Served

- 16.2.2 Recent Developments

- 16.3. Company Market Share Analysis 2025

- 16.3.1 Top 5 Companies Market Share Analysis

- 16.3.2 Top 3 Companies Market Share Analysis

- 16.4. List of Potential Customers

- 17. Research Methodology

List of Figures

- Figure 1: Europe Solar Inverters Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe Solar Inverters Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Solar Inverters Industry Revenue Million Forecast, by Inverter Type 2020 & 2033

- Table 2: Europe Solar Inverters Industry Volume K Unit Forecast, by Inverter Type 2020 & 2033

- Table 3: Europe Solar Inverters Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 4: Europe Solar Inverters Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 5: Europe Solar Inverters Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Europe Solar Inverters Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: Europe Solar Inverters Industry Revenue Million Forecast, by Inverter Type 2020 & 2033

- Table 8: Europe Solar Inverters Industry Volume K Unit Forecast, by Inverter Type 2020 & 2033

- Table 9: Europe Solar Inverters Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 10: Europe Solar Inverters Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 11: Europe Solar Inverters Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Europe Solar Inverters Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 13: Europe Solar Inverters Industry Revenue Million Forecast, by Inverter Type 2020 & 2033

- Table 14: Europe Solar Inverters Industry Volume K Unit Forecast, by Inverter Type 2020 & 2033

- Table 15: Europe Solar Inverters Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 16: Europe Solar Inverters Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 17: Europe Solar Inverters Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 18: Europe Solar Inverters Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 19: Europe Solar Inverters Industry Revenue Million Forecast, by Inverter Type 2020 & 2033

- Table 20: Europe Solar Inverters Industry Volume K Unit Forecast, by Inverter Type 2020 & 2033

- Table 21: Europe Solar Inverters Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 22: Europe Solar Inverters Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 23: Europe Solar Inverters Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: Europe Solar Inverters Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 25: Europe Solar Inverters Industry Revenue Million Forecast, by Inverter Type 2020 & 2033

- Table 26: Europe Solar Inverters Industry Volume K Unit Forecast, by Inverter Type 2020 & 2033

- Table 27: Europe Solar Inverters Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 28: Europe Solar Inverters Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 29: Europe Solar Inverters Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 30: Europe Solar Inverters Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 31: Europe Solar Inverters Industry Revenue Million Forecast, by Inverter Type 2020 & 2033

- Table 32: Europe Solar Inverters Industry Volume K Unit Forecast, by Inverter Type 2020 & 2033

- Table 33: Europe Solar Inverters Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 34: Europe Solar Inverters Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 35: Europe Solar Inverters Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 36: Europe Solar Inverters Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 37: Europe Solar Inverters Industry Revenue Million Forecast, by Inverter Type 2020 & 2033

- Table 38: Europe Solar Inverters Industry Volume K Unit Forecast, by Inverter Type 2020 & 2033

- Table 39: Europe Solar Inverters Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 40: Europe Solar Inverters Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 41: Europe Solar Inverters Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 42: Europe Solar Inverters Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 43: Europe Solar Inverters Industry Revenue Million Forecast, by Inverter Type 2020 & 2033

- Table 44: Europe Solar Inverters Industry Volume K Unit Forecast, by Inverter Type 2020 & 2033

- Table 45: Europe Solar Inverters Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 46: Europe Solar Inverters Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 47: Europe Solar Inverters Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 48: Europe Solar Inverters Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 49: Europe Solar Inverters Industry Revenue Million Forecast, by Inverter Type 2020 & 2033

- Table 50: Europe Solar Inverters Industry Volume K Unit Forecast, by Inverter Type 2020 & 2033

- Table 51: Europe Solar Inverters Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 52: Europe Solar Inverters Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 53: Europe Solar Inverters Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 54: Europe Solar Inverters Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 55: Europe Solar Inverters Industry Revenue Million Forecast, by Inverter Type 2020 & 2033

- Table 56: Europe Solar Inverters Industry Volume K Unit Forecast, by Inverter Type 2020 & 2033

- Table 57: Europe Solar Inverters Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 58: Europe Solar Inverters Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 59: Europe Solar Inverters Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 60: Europe Solar Inverters Industry Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Solar Inverters Industry?

The projected CAGR is approximately 5.06%.

2. Which companies are prominent players in the Europe Solar Inverters Industry?

Key companies in the market include Delta Energy Systems Inc, FIMER SpA, Mitsubishi Electric Corporation, Siemens AG, Schneider Electric SE, Omron Corporation, KACO New Energy GmbH*List Not Exhaustive 6 4 Market Ranking/Share Analysi, Huawei Technologies Co Ltd, General Electric Company, SMA Solar Technology AG.

3. What are the main segments of the Europe Solar Inverters Industry?

The market segments include Inverter Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.85 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Supportive Government Initiatives4.; Investment in Electrification Using Solar Energy.

6. What are the notable trends driving market growth?

Central Inverters Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Lack of General Awareness. Infrastructure Development Costs. and Recent Subsidy Cuts on Solar Panels.

8. Can you provide examples of recent developments in the market?

June 2022: SMA Solar Technology AG announced plans to build a solar inverter manufacturing facility in Niestetal, Germany. The new gigawatt factory is a part of the company’s target to double the production capacity from 21GW (present) to 40GW by 2024. The construction was expected to begin by the end of 2022.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Solar Inverters Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Solar Inverters Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Solar Inverters Industry?

To stay informed about further developments, trends, and reports in the Europe Solar Inverters Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence