Key Insights

The German High Voltage Direct Current (HVDC) Transmission System market is projected for substantial growth, driven by a Compound Annual Growth Rate (CAGR) of 7.2%. The market, valued at 15.62 billion in the base year 2025, is expanding due to Germany's progressive energy transition (Energiewende) policies, the critical need for grid modernization to integrate renewable energy, and the increasing demand for efficient, long-distance power transmission. Significant investments in offshore wind farms, particularly in the North Sea, necessitate HVDC technology for connecting these remote generation sites to the national grid. Additionally, the phasing out of conventional power plants and the ongoing pursuit of grid stability and resilience in response to intermittent renewable energy sources further accelerate HVDC adoption.

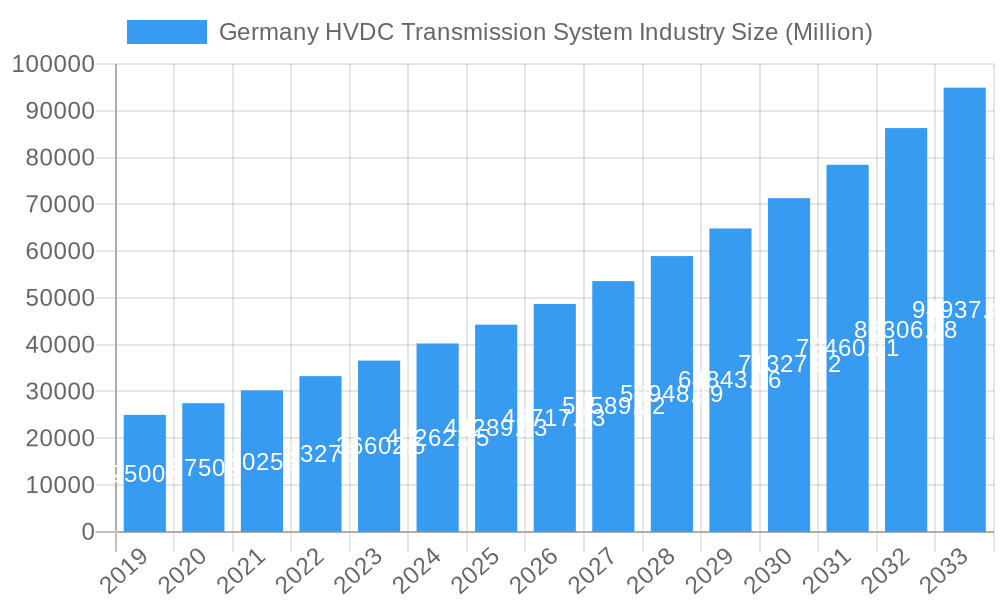

Germany HVDC Transmission System Industry Market Size (In Billion)

Market segmentation includes Submarine HVDC Systems, essential for offshore wind farm connectivity, alongside Overhead and Underground HVDC Systems for terrestrial grid reinforcement and interconnections. Key segments like Converter Stations and Transmission Cables are experiencing strong demand. Major global industry leaders, including Siemens AG, ABB Ltd, and Toshiba Corporation, are instrumental in driving technological advancements and project implementation in Germany. Future trends point towards modular converter stations for increased flexibility, improved cable technologies for higher capacity transmission, and the adoption of digital solutions for enhanced smart grid management. Potential challenges may encompass high initial capital expenditure for HVDC infrastructure, intricate permitting procedures, and the demand for specialized skilled labor.

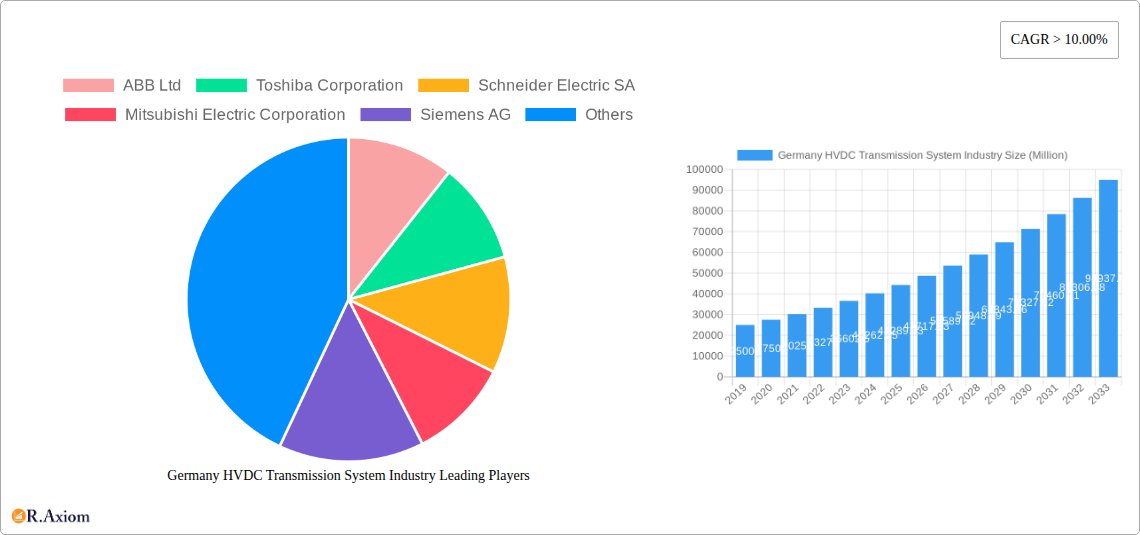

Germany HVDC Transmission System Industry Company Market Share

Germany HVDC Transmission System Industry Market Concentration & Innovation

The Germany HVDC Transmission System industry is characterized by a moderate to high market concentration, with a few dominant players, including ABB Ltd, Siemens AG, and Hitachi Ltd, holding significant market shares. Innovation in this sector is primarily driven by the increasing demand for grid modernization, the integration of renewable energy sources (RES), and the need for efficient long-distance power transmission. Regulatory frameworks, such as Germany's Energiewende (energy transition) policies, play a crucial role in shaping market dynamics by incentivizing investments in advanced transmission technologies. The report analyzes the impact of these regulations on market growth and technological adoption. Product substitutes, while limited in the direct sense of HVDC technology, include advancements in High-Voltage Alternating Current (HVAC) systems and distributed energy resources. End-user trends reveal a growing preference for highly reliable and secure power grids, particularly from utility companies and industrial consumers. Mergers and acquisitions (M&A) activities, while not as frequent as in some other industrial sectors, are strategic moves by key players to expand their technological capabilities and geographical reach. For instance, recent M&A deals in the broader European grid technology sector have amounted to several hundred million Euros, signaling consolidation and strategic realignments. The market share of the top three players is estimated to be around 65% in the base year of 2025, with ongoing efforts to maintain and expand this dominance through innovation and strategic partnerships.

Germany HVDC Transmission System Industry Industry Trends & Insights

The Germany HVDC Transmission System industry is poised for significant growth, driven by a confluence of technological advancements, evolving energy policies, and increasing demands for grid stability and efficiency. The Compound Annual Growth Rate (CAGR) for the forecast period (2025–2033) is projected to be robust, estimated at 8.5%, reflecting the substantial investments anticipated in the sector. This growth is underpinned by Germany's ambitious renewable energy targets, necessitating robust and flexible transmission infrastructure to manage the intermittency of solar and wind power. The market penetration of HVDC technology is steadily increasing, particularly for large-scale projects and interconnections requiring lower transmission losses over long distances.

Technological disruptions are at the forefront of industry evolution. Innovations in converter station technology, such as the development of Voltage Source Converters (VSCs) offering enhanced control and flexibility, are becoming increasingly prevalent. These advancements enable smoother integration of renewables and improved grid management. Furthermore, advancements in cable technologies, including extruded insulation and more efficient cooling systems for both submarine and underground applications, are contributing to higher capacity and reliability. The push towards digital substations and the integration of Artificial Intelligence (AI) for predictive maintenance and grid optimization are also key trends shaping the industry landscape.

Consumer preferences, primarily from utility operators and grid system integrators, are shifting towards solutions that offer greater operational efficiency, reduced environmental impact, and enhanced grid resilience. There is a growing demand for HVDC systems that can facilitate the efficient transfer of large amounts of power from offshore wind farms to onshore grids, as well as interconnections between different European grids to enhance energy security and market integration. Competitive dynamics within the industry are intense, with established global players like ABB Ltd, Siemens AG, and Toshiba Corporation vying for market share. These companies are investing heavily in research and development to stay ahead of the curve and are increasingly forming strategic alliances to tackle large-scale projects. The competitive landscape is also influenced by the emergence of specialized component manufacturers and the increasing focus on localized manufacturing and supply chains to ensure project delivery timelines. The overall market size for Germany's HVDC transmission system, estimated at XX Billion Euros in the base year of 2025, is expected to witness substantial expansion throughout the forecast period.

Dominant Markets & Segments in Germany HVDC Transmission System Industry

Within the Germany HVDC Transmission System industry, the HVDC Overhead Transmission System segment holds a dominant position, driven by its cost-effectiveness and widespread application in transmitting large quantities of power over significant distances, particularly connecting remote renewable energy generation sites to demand centers. The economic policies supporting the expansion of the national grid and the integration of onshore wind and solar farms are key drivers for this segment. For example, government subsidies and investment frameworks encouraging the development of new transmission corridors directly benefit overhead HVDC lines.

The Converter Stations segment is another critical and dominant component, as these stations are essential for converting direct current to alternating current and vice versa, enabling the integration of HVDC lines into existing AC grids. The technological advancements in converter technology, including the increasing adoption of Voltage Source Converters (VSCs), are fueling growth in this segment. The demand for higher power capacities and enhanced grid control capabilities further solidifies the dominance of converter stations. Major projects, such as the expansion of Germany's national grid to accommodate the energy transition, necessitate significant investments in state-of-the-art converter stations. The market size for converter stations is estimated to be XX Billion Euros in the base year of 2025.

While Submarine HVDC Transmission System projects are typically capital-intensive and project-specific, they play a crucial role in connecting offshore wind farms and facilitating cross-border interconnections. The German government's commitment to offshore wind energy development is a significant driver for this segment. Investments in projects like the NordLink interconnector, which connects Germany to Norway, highlight the strategic importance and growing dominance of submarine HVDC systems in facilitating the import and export of renewable energy.

The HVDC Underground Transmission System segment, while facing higher installation costs compared to overhead lines, is gaining traction in densely populated urban areas and environmentally sensitive regions where overhead lines are not feasible. Increasing awareness of visual impact and the demand for reliable underground infrastructure are contributing to its growth. The market size for cables, encompassing all HVDC transmission types, is estimated at XX Billion Euros in the base year of 2025, with a steady increase projected due to ongoing grid expansion and modernization efforts. The overall market growth is intricately linked to the successful implementation of Germany's energy transition strategy, which necessitates a robust and adaptable HVDC transmission network.

Germany HVDC Transmission System Industry Product Developments

Product development in the Germany HVDC Transmission System industry is centered on enhancing efficiency, reliability, and flexibility. Key innovations include the advancement of Voltage Source Converters (VSCs) with higher power ratings and reduced footprint, enabling more seamless integration of renewable energy sources and improved grid control. Development of advanced insulation materials and cable designs for both submarine and underground applications is leading to higher voltage capabilities and increased transmission capacity, minimizing energy losses. Furthermore, the integration of digital technologies, such as AI-powered monitoring systems and advanced control algorithms, is enhancing operational efficiency, predictive maintenance, and overall grid stability. These developments offer significant competitive advantages by reducing project costs, improving performance, and ensuring long-term operational reliability for grid operators.

Report Scope & Segmentation Analysis

The scope of this report encompasses a comprehensive analysis of the Germany HVDC Transmission System industry, segmented by transmission type and key components.

The Submarine HVDC Transmission System segment is analyzed, focusing on its role in offshore wind farm connections and international grid interconnections. Growth projections for this segment are tied to the expansion of offshore renewable energy capacity and strategic cross-border energy trading initiatives.

The HVDC Overhead Transmission System segment is examined in detail, considering its widespread application in connecting remote generation to demand centers and its cost-effectiveness for bulk power transfer. Its market size is projected to be substantial due to ongoing grid reinforcement projects.

The HVDC Underground Transmission System segment is assessed for its increasing relevance in urban areas and environmentally sensitive regions. Growth in this segment is driven by the need for discreet and reliable power infrastructure.

The Converter Stations segment is a critical focus, analyzing the technological advancements and market demand for VSCs and LCCs. Its market size is expected to grow in tandem with the overall HVDC network expansion.

The Transmission Medium (Cables) segment includes analysis of advancements in cable technology for all HVDC transmission types, focusing on higher voltage ratings, increased capacity, and improved longevity. Its market size is projected to increase with the growing demand for HVDC infrastructure.

Key Drivers of Germany HVDC Transmission System Industry Growth

The Germany HVDC Transmission System industry's growth is propelled by several key factors. Foremost among these is the Energiewende, Germany's ambitious energy transition policy, which necessitates the expansion and modernization of the power grid to integrate a higher share of renewable energy sources, particularly from offshore wind and solar farms. This transition requires efficient, low-loss transmission solutions over long distances, making HVDC technology indispensable. Secondly, the increasing demand for grid stability and reliability, especially in the face of growing demand and the inherent intermittency of renewables, drives investment in advanced transmission systems. Thirdly, technological advancements in HVDC converter technology and cable systems are improving efficiency, reducing costs, and enhancing operational capabilities, making HVDC a more attractive option. Finally, the need for interconnections with neighboring European countries to enhance energy security and facilitate cross-border power trading also fuels the demand for HVDC transmission systems.

Challenges in the Germany HVDC Transmission System Industry Sector

Despite the robust growth potential, the Germany HVDC Transmission System industry faces several challenges. Permitting and regulatory hurdles for new transmission lines, particularly overhead lines, can lead to significant project delays and increased costs due to complex environmental assessments and public opposition. High initial capital investment for HVDC projects, especially converter stations and long-distance cables, remains a significant barrier. Supply chain disruptions, as seen in recent global events, can impact the availability of critical components and lead to project timelines being extended. Furthermore, skilled workforce shortages in specialized areas like HVDC engineering and installation can impede the pace of development and deployment. Lastly, competition from alternative technologies and the increasing integration of distributed energy resources, while also driving HVDC demand, can present strategic challenges for traditional large-scale transmission projects.

Emerging Opportunities in Germany HVDC Transmission System Industry

Emerging opportunities within the Germany HVDC Transmission System industry are multifaceted. The continued expansion of offshore wind power presents a significant avenue for submarine HVDC transmission systems, connecting new wind farms to the onshore grid. The growing trend of sector coupling, integrating the electricity sector with heating, transport, and industry, will necessitate more flexible and efficient power transmission, favoring HVDC solutions. The development of energy islands and the creation of pan-European HVDC grids for enhanced energy security and market integration offer substantial long-term growth prospects. Furthermore, the increasing focus on grid modernization and digitalization presents opportunities for the deployment of smart HVDC systems with advanced control and monitoring capabilities, supporting grid resilience and stability. Innovations in underground HVDC technology for urban environments and the increasing demand for HVDC technology in industrial applications also represent promising new markets.

Leading Players in the Germany HVDC Transmission System Industry Market

- ABB Ltd

- Toshiba Corporation

- Schneider Electric SA

- Mitsubishi Electric Corporation

- Siemens AG

- Hitachi Ltd

- General Electric Company

Key Developments in Germany HVDC Transmission System Industry Industry

- 2023 February: Siemens AG announces the successful completion of a major HVDC converter station upgrade, enhancing grid stability for renewable energy integration.

- 2022 November: ABB Ltd secures a significant contract for a new offshore HVDC transmission system to connect a large-scale wind farm to the German grid.

- 2022 June: Hitachi Ltd unveils a new generation of VSC converter technology, promising higher efficiency and reduced environmental impact for HVDC transmission.

- 2021 September: TenneT, a major grid operator, announces plans for substantial investments in HVDC infrastructure to support Germany's energy transition goals.

- 2020 March: GE Company highlights advancements in HVDC cable technology, enabling higher voltage transmission with reduced losses.

Strategic Outlook for Germany HVDC Transmission System Industry Market

The strategic outlook for the Germany HVDC Transmission System industry is overwhelmingly positive, driven by the imperative to decarbonize the energy sector and enhance grid resilience. The sustained commitment to renewable energy integration, coupled with the increasing demand for secure and efficient power transmission, will continue to fuel investment in HVDC technology. Key growth catalysts include ongoing government support for grid expansion and modernization, technological advancements that reduce costs and improve performance, and the growing strategic importance of cross-border interconnections. Opportunities arising from sector coupling and the development of smart grid solutions will further bolster the market's trajectory. Industry stakeholders are advised to focus on innovation in VSC technology, advanced cable solutions, and digital integration to capitalize on the robust demand and secure a leading position in this evolving market.

Germany HVDC Transmission System Industry Segmentation

-

1. Transmission Type

- 1.1. Submarine HVDC Transmission System

- 1.2. HVDC Overhead Transmission System

- 1.3. HVDC Underground Transmission System

-

2. Component

- 2.1. Converter Stations

- 2.2. Transmission Medium (Cables)

Germany HVDC Transmission System Industry Segmentation By Geography

- 1. Germany

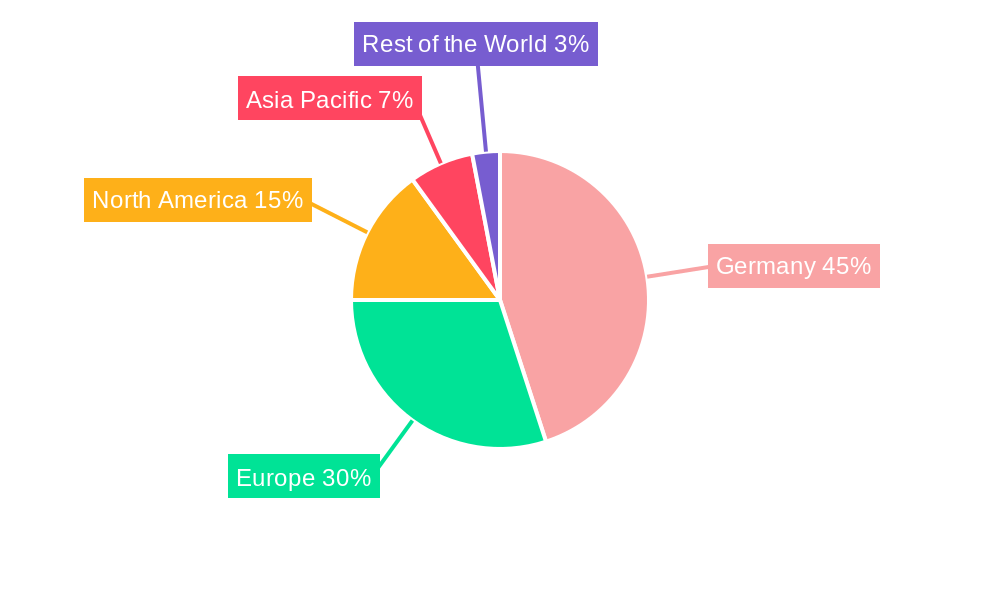

Germany HVDC Transmission System Industry Regional Market Share

Geographic Coverage of Germany HVDC Transmission System Industry

Germany HVDC Transmission System Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Transmission Type

- 5.1.1. Submarine HVDC Transmission System

- 5.1.2. HVDC Overhead Transmission System

- 5.1.3. HVDC Underground Transmission System

- 5.2. Market Analysis, Insights and Forecast - by Component

- 5.2.1. Converter Stations

- 5.2.2. Transmission Medium (Cables)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Germany

- 5.1. Market Analysis, Insights and Forecast - by Transmission Type

- 6. Germany HVDC Transmission System Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Transmission Type

- 6.1.1. Submarine HVDC Transmission System

- 6.1.2. HVDC Overhead Transmission System

- 6.1.3. HVDC Underground Transmission System

- 6.2. Market Analysis, Insights and Forecast - by Component

- 6.2.1. Converter Stations

- 6.2.2. Transmission Medium (Cables)

- 6.1. Market Analysis, Insights and Forecast - by Transmission Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 ABB Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Toshiba Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Schneider Electric SA

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Mitsubishi Electric Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Siemens AG

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Hitachi Lt

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 General Electric Company

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.1 ABB Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Germany HVDC Transmission System Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Germany HVDC Transmission System Industry Share (%) by Company 2025

List of Tables

- Table 1: Germany HVDC Transmission System Industry Revenue billion Forecast, by Transmission Type 2020 & 2033

- Table 2: Germany HVDC Transmission System Industry Volume kilovolts Forecast, by Transmission Type 2020 & 2033

- Table 3: Germany HVDC Transmission System Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 4: Germany HVDC Transmission System Industry Volume kilovolts Forecast, by Component 2020 & 2033

- Table 5: Germany HVDC Transmission System Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Germany HVDC Transmission System Industry Volume kilovolts Forecast, by Region 2020 & 2033

- Table 7: Germany HVDC Transmission System Industry Revenue billion Forecast, by Transmission Type 2020 & 2033

- Table 8: Germany HVDC Transmission System Industry Volume kilovolts Forecast, by Transmission Type 2020 & 2033

- Table 9: Germany HVDC Transmission System Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 10: Germany HVDC Transmission System Industry Volume kilovolts Forecast, by Component 2020 & 2033

- Table 11: Germany HVDC Transmission System Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Germany HVDC Transmission System Industry Volume kilovolts Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Germany HVDC Transmission System Industry?

The projected CAGR is approximately 7.2%.

2. Which companies are prominent players in the Germany HVDC Transmission System Industry?

Key companies in the market include ABB Ltd, Toshiba Corporation, Schneider Electric SA, Mitsubishi Electric Corporation, Siemens AG, Hitachi Lt, General Electric Company.

3. What are the main segments of the Germany HVDC Transmission System Industry?

The market segments include Transmission Type, Component.

4. Can you provide details about the market size?

The market size is estimated to be USD 15.62 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Domestic Oil and Gas Production4.; Investments in Oil and Gas Infrastructure Development.

6. What are the notable trends driving market growth?

Submarine HVDC Transmission System to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Growth of Renewable Energy.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in kilovolts.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Germany HVDC Transmission System Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Germany HVDC Transmission System Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Germany HVDC Transmission System Industry?

To stay informed about further developments, trends, and reports in the Germany HVDC Transmission System Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence