Key Insights

The High Voltage Direct Current (HVDC) Converter Station market is projected to reach $15.62 billion by 2025, exhibiting a Compound Annual Growth Rate (CAGR) of 7.2%. This expansion is driven by the escalating global need for efficient, long-distance power transmission solutions, particularly for integrating remote renewable energy sources like wind and solar. Key growth catalysts include grid modernization initiatives, enhanced grid stability requirements, and the facilitation of intercontinental power trading. Voltage Source Converter (VSC) technology is gaining prominence due to its flexibility, precise control, and reactive power compensation capabilities, making it ideal for modern grids and renewable energy integration.

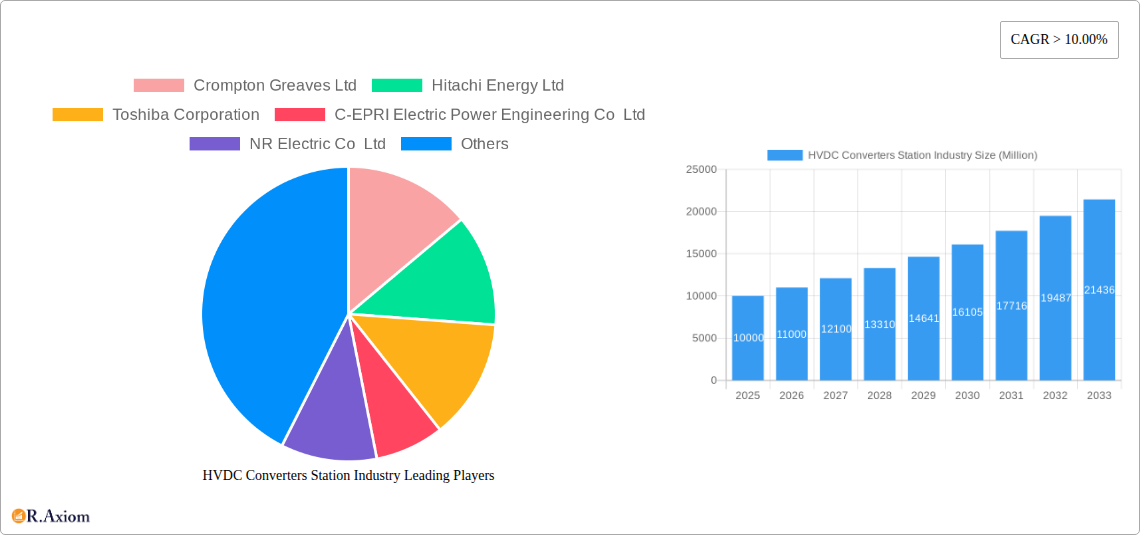

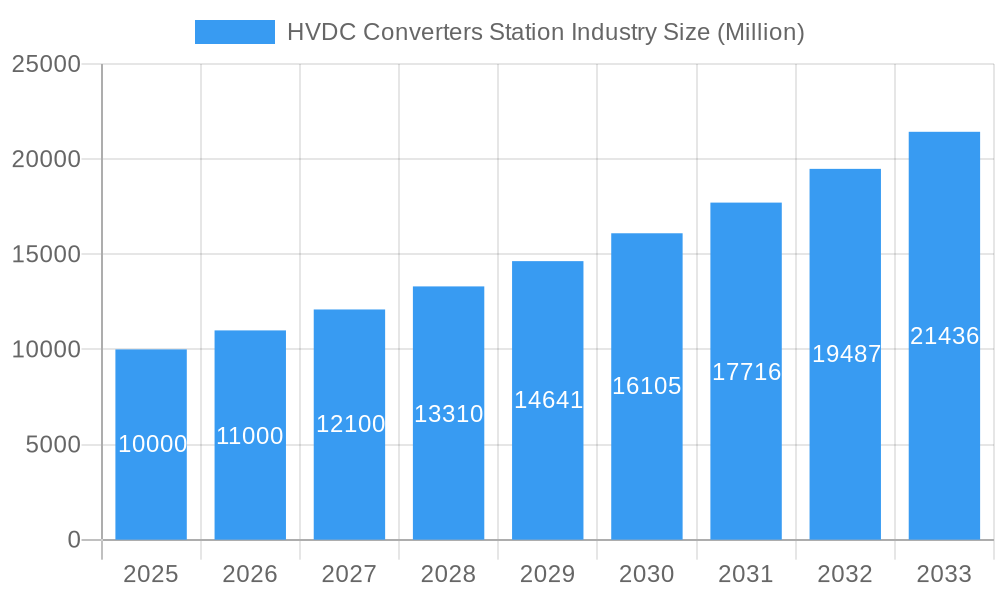

HVDC Converters Station Industry Market Size (In Billion)

Despite challenges such as substantial initial investment costs and the requirement for specialized expertise, continuous advancements in power electronics, digital control systems, and manufacturing efficiencies are expected to overcome these restraints. The market encompasses critical components including converters, DC equipment, and converter transformers. Leading players such as Hitachi Energy Ltd, Siemens Energy AG, and GE Grid Solutions LLC are actively pursuing research and development, strategic alliances, and manufacturing expansion. The Asia Pacific region is anticipated to lead market growth, fueled by rapid industrialization and significant renewable energy investments.

HVDC Converters Station Industry Company Market Share

This detailed report offers an SEO-optimized analysis of the HVDC Converter Station industry, covering market size, growth trends, and future forecasts.

HVDC Converters Station Industry Market Concentration & Innovation

The HVDC Converters Station Industry is characterized by a moderate to high market concentration, with a few dominant players holding substantial market share. Leading companies such as Hitachi Energy Ltd., Siemens Energy AG, and GE Grid Solutions LLC are at the forefront, driving innovation and technological advancements. The industry's growth is significantly fueled by increasing investments in renewable energy integration, grid modernization, and cross-border power transmission projects. Regulatory frameworks, particularly those promoting decarbonization and energy security, play a crucial role in shaping market dynamics. Product substitutes, while existing in conventional AC transmission, are becoming less viable for long-distance and bulk power transfer due to the inherent advantages of HVDC technology, such as lower line losses and reduced environmental impact. End-user trends indicate a growing demand for reliable and efficient power transmission solutions, driven by the expansion of smart grids and the electrification of various sectors. Mergers and acquisitions (M&A) activities are expected to continue, as companies seek to expand their geographical reach, diversify their product portfolios, and gain a competitive edge. For instance, M&A deal values are projected to reach XX Million over the forecast period, reflecting the strategic importance of consolidation in this capital-intensive sector. Innovation drivers include the development of advanced converter technologies, enhanced control systems, and solutions for grid stability and flexibility.

- Market Share Dominance: Leading companies are expected to maintain significant market shares, with Hitachi Energy Ltd. potentially holding between 15-20% and Siemens Energy AG between 12-17%.

- M&A Activity: Ongoing consolidation is anticipated, with XX Million in M&A deal values expected between 2025 and 2033.

- Innovation Focus: Key innovations revolve around higher voltage ratings, improved converter efficiency, and advanced digital solutions for grid management.

HVDC Converters Station Industry Industry Trends & Insights

The HVDC Converters Station Industry is poised for robust growth, driven by a confluence of technological advancements, escalating global energy demands, and a pronounced shift towards sustainable power systems. The market is experiencing a significant upswing, propelled by the imperative to integrate massive amounts of renewable energy sources, such as offshore wind farms and solar parks, into existing power grids. These intermittent sources necessitate efficient and reliable long-distance transmission, a domain where HVDC technology excels due to its lower transmission losses compared to HVAC. The projected Compound Annual Growth Rate (CAGR) for the HVDC Converters Station Industry is estimated to be XX% over the forecast period of 2025–2033, indicating a substantial expansion in market penetration and revenue. Technological disruptions, particularly in the realm of Voltage Source Converters (VSC), are further accelerating this growth. VSC technology offers superior controllability, enabling faster response times and enhanced grid stability, making it increasingly preferred for modern grid applications. Consumer preferences are evolving towards cleaner energy sources and more reliable power supply, aligning perfectly with the benefits offered by HVDC solutions. Competitive dynamics are intensifying, with established players like Toshiba Corporation and Mitsubishi Electric Corporation investing heavily in research and development to maintain their market leadership. New entrants, particularly from emerging economies, are also beginning to make their mark, spurred by government initiatives to bolster domestic manufacturing capabilities. The increasing electrification of transportation and industrial processes also contributes to the heightened demand for advanced power transmission infrastructure. Furthermore, the need for interconnecting power grids across regions and countries for enhanced energy security and economic efficiency is a significant growth driver. The global energy transition, with its ambitious decarbonization targets, underpins the long-term sustainability and growth trajectory of the HVDC Converters Station Industry. The development of sophisticated control systems, superconducting materials, and modular converter designs are key areas of innovation that will shape the future landscape of this vital industry. The adoption of digital twins and artificial intelligence for predictive maintenance and operational optimization is also gaining traction, promising to further enhance the efficiency and reliability of HVDC converter stations.

Dominant Markets & Segments in HVDC Converters Station Industry

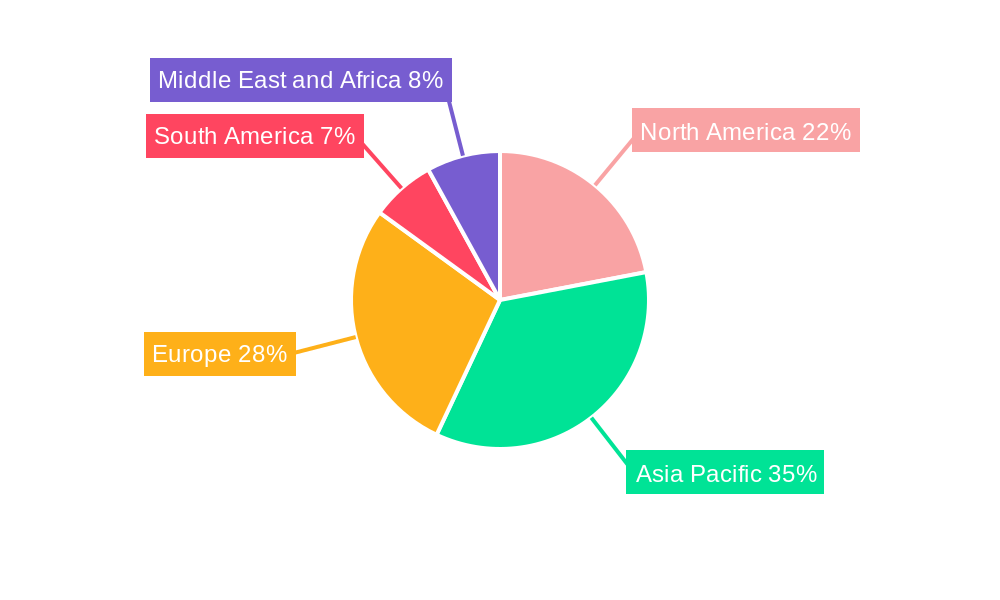

The HVDC Converters Station Industry exhibits distinct regional dominance and segment preferences, driven by economic policies, infrastructure development, and energy needs. Asia Pacific is emerging as the dominant region, propelled by rapid industrialization, escalating energy consumption, and substantial government investments in grid expansion and modernization. Countries like China, with its vast renewable energy deployment and extensive high-speed rail network, represent a key market. The Voltage Source Converter (VSC) technology segment is witnessing remarkable growth, outpacing its Line Commutated Converter (LCC) counterpart. This surge is attributable to VSC's superior flexibility, faster response times, and ability to provide reactive power support, making it ideal for integrating variable renewable energy sources and for meshed AC networks. Key drivers for VSC dominance include its role in enabling grid stability with high renewable penetration and its application in offshore wind connections.

- Leading Region: Asia Pacific, with an estimated market share of XX% by 2033, driven by China and India's massive infrastructure projects.

- Dominant Technology: Voltage Source Converter (VSC), projected to capture XX% of the market by 2033, owing to its flexibility and renewable integration capabilities.

- Key Segment Drivers:

- Economic Policies: Government incentives for renewable energy and grid upgrades.

- Infrastructure Development: Large-scale projects for long-distance power transmission and grid interconnections.

- Technological Advancements: Enhanced performance and cost-effectiveness of VSC technology.

- Renewable Energy Integration: The growing need to connect remote renewable energy sources to the grid.

The Converter Transformer segment is another critical component driving market growth, as these transformers are essential for voltage conversion in HVDC systems. Advancements in insulation materials and cooling techniques are enhancing the efficiency and reliability of these transformers, making them integral to new project deployments. The DC Equipment segment, encompassing high-voltage DC circuit breakers and smoothing reactors, is also experiencing sustained demand as HVDC networks become more complex and widespread. The Converter itself, as the core component of an HVDC station, continues to be a focal point of innovation, with manufacturers striving for higher power capacities and reduced losses. The Other Co segment, which includes ancillary services, control systems, and project engineering, also represents a growing area as the complexity of HVDC projects increases.

HVDC Converters Station Industry Product Developments

Product developments in the HVDC Converters Station Industry are largely centered on enhancing efficiency, reliability, and modularity. Innovations in semiconductor technology, such as the widespread adoption of Silicon Carbide (SiC) and Gallium Nitride (GaN), are leading to converters with higher switching frequencies, reduced energy losses, and a smaller physical footprint. Manufacturers are also focusing on developing ultra-high voltage (UHV) converter stations capable of transmitting power over significantly longer distances with minimal losses. The integration of advanced digital control systems and artificial intelligence for predictive maintenance and grid optimization is a key trend, offering enhanced operational flexibility and reduced downtime. These advancements are critical for integrating large-scale renewable energy projects and for strengthening intercontinental power grids.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the global HVDC Converters Station Industry, segmented by technology, component, and region. The Technology segmentation includes Voltage Source Converter (VSC) and Line Commutated Converter (LCC). VSC technology is projected to exhibit a CAGR of XX% during the forecast period, driven by its suitability for renewable energy integration. LCC technology, while mature, continues to be relevant for bulk power transmission. The Component segmentation covers Converter, DC Equipment, Converter Transformer, and Other Co. The Converter Transformer segment is expected to grow at a CAGR of XX%, owing to the increasing number of HVDC projects. DC Equipment, including circuit breakers and smoothing reactors, will see steady growth as HVDC networks expand. The Converter segment remains the core of the market, with continuous technological advancements. The Other Co segment, encompassing engineering, procurement, and construction (EPC) services, is also poised for substantial growth.

- Voltage Source Converter (VSC): Expected market size of XX Million by 2033, with a CAGR of XX%.

- Line Commutated Converter (LCC): Market size of XX Million by 2033, with a CAGR of XX%.

- Converter Transformer: Projected market size of XX Million by 2033, with a CAGR of XX%.

- DC Equipment: Expected market size of XX Million by 2033, with a CAGR of XX%.

- Converter: Market size of XX Million by 2033, with a CAGR of XX%.

Key Drivers of HVDC Converters Station Industry Growth

The growth of the HVDC Converters Station Industry is primarily propelled by the global shift towards renewable energy sources. The need to efficiently transmit large volumes of power from remote renewable generation sites, such as offshore wind farms, to demand centers is a major catalyst. Furthermore, government initiatives and supportive policies aimed at grid modernization and decarbonization are significantly boosting investment in HVDC infrastructure. Technological advancements, particularly in VSC technology, are enhancing the flexibility and controllability of HVDC systems, making them more attractive for grid applications. Increasing demand for energy security and the development of cross-border interconnections for improved grid reliability and economic efficiency also play a crucial role.

- Renewable Energy Integration: Essential for transmitting power from offshore wind and solar farms.

- Grid Modernization: Upgrading aging grid infrastructure with advanced transmission technologies.

- Government Support & Policies: Favorable regulations and incentives for clean energy and infrastructure development.

- Technological Advancements: Innovations in VSC technology and high-voltage equipment.

Challenges in the HVDC Converters Station Industry Sector

Despite its robust growth prospects, the HVDC Converters Station Industry faces several challenges. The high initial capital investment required for HVDC converter stations and associated infrastructure can be a significant barrier, particularly for developing economies. Complex regulatory approvals and lengthy permitting processes in various regions can also lead to project delays. Supply chain disruptions, particularly for specialized components, and geopolitical uncertainties can impact project timelines and costs. Moreover, the shortage of skilled labor required for the design, installation, and maintenance of these complex systems poses another hurdle. Competition from advanced High-Voltage Alternating Current (HVAC) technologies for certain applications, though diminishing for long-distance transmission, still exists.

- High Capital Expenditure: Significant upfront investment for HVDC infrastructure.

- Regulatory Hurdles: Complex and time-consuming approval processes.

- Supply Chain Vulnerabilities: Potential disruptions in the availability of specialized components.

- Skilled Labor Shortage: Difficulty in finding qualified personnel for specialized tasks.

Emerging Opportunities in HVDC Converters Station Industry

Emerging opportunities within the HVDC Converters Station Industry are vast and diverse. The increasing trend of offshore wind farms, requiring efficient long-distance power transmission, presents a significant growth avenue. The development of superconducting HVDC cables and converters promises even higher efficiencies and reduced transmission losses. The growing focus on smart grids and grid resilience is creating opportunities for advanced control systems and energy storage integration with HVDC stations. Furthermore, the expansion of cross-border electricity trade and the establishment of continental power grids offer substantial opportunities for large-scale HVDC interconnections. The electrification of transportation, particularly long-haul electric trucking, may also drive demand for supporting HVDC infrastructure in the future.

- Offshore Wind Integration: Massive demand for HVDC to connect offshore wind farms.

- Smart Grid Development: Opportunities for advanced control and integration with energy storage.

- Cross-Border Interconnections: Facilitating international electricity trade and grid stability.

- Superconducting Technology: Potential for highly efficient and compact transmission solutions.

Leading Players in the HVDC Converters Station Industry Market

- Crompton Greaves Ltd

- Hitachi Energy Ltd

- Toshiba Corporation

- C-EPRI Electric Power Engineering Co Ltd

- NR Electric Co Ltd

- Mitsubishi Electric Corporation

- Bharat Heavy Electricals Limited

- GE Grid Solutions LLC

- Siemens Energy AG

Key Developments in HVDC Converters Station Industry Industry

- 2023/11: Hitachi Energy Ltd. commissioned a major HVDC link in Europe, enhancing grid stability and enabling renewable energy integration.

- 2023/10: Siemens Energy AG announced a breakthrough in VSC converter technology, achieving higher power ratings and improved efficiency.

- 2023/09: GE Grid Solutions LLC secured a significant contract for a new HVDC converter station in North America, supporting grid modernization efforts.

- 2023/07: Toshiba Corporation expanded its HVDC converter manufacturing capabilities to meet rising global demand.

- 2023/06: C-EPRI Electric Power Engineering Co Ltd completed the installation of a key HVDC converter station in Asia, facilitating cross-border power transmission.

- 2023/05: Mitsubishi Electric Corporation launched a new generation of compact and efficient converter transformers for HVDC applications.

- 2023/04: Bharat Heavy Electricals Limited (BHEL) secured a prominent order for an HVDC converter station project in India.

- 2022/12: NR Electric Co Ltd announced the successful testing of their advanced HVDC circuit breaker technology.

- 2022/11: Crompton Greaves Ltd highlighted its role in supplying critical components for several ongoing HVDC projects.

Strategic Outlook for HVDC Converters Station Industry Market

The strategic outlook for the HVDC Converters Station Industry remains exceptionally positive, driven by the accelerating global energy transition and the increasing demand for efficient and reliable power transmission. Key growth catalysts include sustained investments in renewable energy infrastructure, the ongoing development of smart grids, and the growing importance of international grid interconnections for energy security and economic cooperation. Technological advancements, particularly in VSC technology and the integration of digital solutions, will continue to enhance the competitiveness and attractiveness of HVDC systems. Companies focusing on innovation, operational efficiency, and strategic partnerships are well-positioned to capitalize on the expanding market opportunities. The industry is expected to witness continued M&A activity as players seek to consolidate their market positions and expand their technological capabilities, further shaping the competitive landscape for years to come.

HVDC Converters Station Industry Segmentation

-

1. Technology

- 1.1. Voltage Source Converter (VSC)

- 1.2. Line Commutated Converter (LCC)

-

2. Component

- 2.1. Converter

- 2.2. DC Equipment

- 2.3. Converter Transformer

- 2.4. Other Co

HVDC Converters Station Industry Segmentation By Geography

- 1. North America

- 2. Asia Pacific

- 3. Europe

- 4. South America

- 5. Middle East and Africa

HVDC Converters Station Industry Regional Market Share

Geographic Coverage of HVDC Converters Station Industry

HVDC Converters Station Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 5.1.1. Voltage Source Converter (VSC)

- 5.1.2. Line Commutated Converter (LCC)

- 5.2. Market Analysis, Insights and Forecast - by Component

- 5.2.1. Converter

- 5.2.2. DC Equipment

- 5.2.3. Converter Transformer

- 5.2.4. Other Co

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Asia Pacific

- 5.3.3. Europe

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 6. Global HVDC Converters Station Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 6.1.1. Voltage Source Converter (VSC)

- 6.1.2. Line Commutated Converter (LCC)

- 6.2. Market Analysis, Insights and Forecast - by Component

- 6.2.1. Converter

- 6.2.2. DC Equipment

- 6.2.3. Converter Transformer

- 6.2.4. Other Co

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 7. North America HVDC Converters Station Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Technology

- 7.1.1. Voltage Source Converter (VSC)

- 7.1.2. Line Commutated Converter (LCC)

- 7.2. Market Analysis, Insights and Forecast - by Component

- 7.2.1. Converter

- 7.2.2. DC Equipment

- 7.2.3. Converter Transformer

- 7.2.4. Other Co

- 7.1. Market Analysis, Insights and Forecast - by Technology

- 8. Asia Pacific HVDC Converters Station Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Technology

- 8.1.1. Voltage Source Converter (VSC)

- 8.1.2. Line Commutated Converter (LCC)

- 8.2. Market Analysis, Insights and Forecast - by Component

- 8.2.1. Converter

- 8.2.2. DC Equipment

- 8.2.3. Converter Transformer

- 8.2.4. Other Co

- 8.1. Market Analysis, Insights and Forecast - by Technology

- 9. Europe HVDC Converters Station Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Technology

- 9.1.1. Voltage Source Converter (VSC)

- 9.1.2. Line Commutated Converter (LCC)

- 9.2. Market Analysis, Insights and Forecast - by Component

- 9.2.1. Converter

- 9.2.2. DC Equipment

- 9.2.3. Converter Transformer

- 9.2.4. Other Co

- 9.1. Market Analysis, Insights and Forecast - by Technology

- 10. South America HVDC Converters Station Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Technology

- 10.1.1. Voltage Source Converter (VSC)

- 10.1.2. Line Commutated Converter (LCC)

- 10.2. Market Analysis, Insights and Forecast - by Component

- 10.2.1. Converter

- 10.2.2. DC Equipment

- 10.2.3. Converter Transformer

- 10.2.4. Other Co

- 10.1. Market Analysis, Insights and Forecast - by Technology

- 11. Middle East and Africa HVDC Converters Station Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Technology

- 11.1.1. Voltage Source Converter (VSC)

- 11.1.2. Line Commutated Converter (LCC)

- 11.2. Market Analysis, Insights and Forecast - by Component

- 11.2.1. Converter

- 11.2.2. DC Equipment

- 11.2.3. Converter Transformer

- 11.2.4. Other Co

- 11.1. Market Analysis, Insights and Forecast - by Technology

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Crompton Greaves Ltd

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Hitachi Energy Ltd

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Toshiba Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 C-EPRI Electric Power Engineering Co Ltd

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 NR Electric Co Ltd

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Mitsubishi Electric Corporation

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Bharat Heavy Electricals Limited

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 GE Grid Solutions LLC

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Siemens Energy AG

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.1 Crompton Greaves Ltd

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global HVDC Converters Station Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America HVDC Converters Station Industry Revenue (billion), by Technology 2025 & 2033

- Figure 3: North America HVDC Converters Station Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 4: North America HVDC Converters Station Industry Revenue (billion), by Component 2025 & 2033

- Figure 5: North America HVDC Converters Station Industry Revenue Share (%), by Component 2025 & 2033

- Figure 6: North America HVDC Converters Station Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America HVDC Converters Station Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Asia Pacific HVDC Converters Station Industry Revenue (billion), by Technology 2025 & 2033

- Figure 9: Asia Pacific HVDC Converters Station Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 10: Asia Pacific HVDC Converters Station Industry Revenue (billion), by Component 2025 & 2033

- Figure 11: Asia Pacific HVDC Converters Station Industry Revenue Share (%), by Component 2025 & 2033

- Figure 12: Asia Pacific HVDC Converters Station Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Asia Pacific HVDC Converters Station Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe HVDC Converters Station Industry Revenue (billion), by Technology 2025 & 2033

- Figure 15: Europe HVDC Converters Station Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 16: Europe HVDC Converters Station Industry Revenue (billion), by Component 2025 & 2033

- Figure 17: Europe HVDC Converters Station Industry Revenue Share (%), by Component 2025 & 2033

- Figure 18: Europe HVDC Converters Station Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe HVDC Converters Station Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: South America HVDC Converters Station Industry Revenue (billion), by Technology 2025 & 2033

- Figure 21: South America HVDC Converters Station Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 22: South America HVDC Converters Station Industry Revenue (billion), by Component 2025 & 2033

- Figure 23: South America HVDC Converters Station Industry Revenue Share (%), by Component 2025 & 2033

- Figure 24: South America HVDC Converters Station Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: South America HVDC Converters Station Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa HVDC Converters Station Industry Revenue (billion), by Technology 2025 & 2033

- Figure 27: Middle East and Africa HVDC Converters Station Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 28: Middle East and Africa HVDC Converters Station Industry Revenue (billion), by Component 2025 & 2033

- Figure 29: Middle East and Africa HVDC Converters Station Industry Revenue Share (%), by Component 2025 & 2033

- Figure 30: Middle East and Africa HVDC Converters Station Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Middle East and Africa HVDC Converters Station Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global HVDC Converters Station Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 2: Global HVDC Converters Station Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 3: Global HVDC Converters Station Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global HVDC Converters Station Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 5: Global HVDC Converters Station Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 6: Global HVDC Converters Station Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global HVDC Converters Station Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 8: Global HVDC Converters Station Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 9: Global HVDC Converters Station Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Global HVDC Converters Station Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 11: Global HVDC Converters Station Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 12: Global HVDC Converters Station Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global HVDC Converters Station Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 14: Global HVDC Converters Station Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 15: Global HVDC Converters Station Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global HVDC Converters Station Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 17: Global HVDC Converters Station Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 18: Global HVDC Converters Station Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the HVDC Converters Station Industry?

The projected CAGR is approximately 7.2%.

2. Which companies are prominent players in the HVDC Converters Station Industry?

Key companies in the market include Crompton Greaves Ltd, Hitachi Energy Ltd, Toshiba Corporation, C-EPRI Electric Power Engineering Co Ltd, NR Electric Co Ltd, Mitsubishi Electric Corporation, Bharat Heavy Electricals Limited, GE Grid Solutions LLC, Siemens Energy AG.

3. What are the main segments of the HVDC Converters Station Industry?

The market segments include Technology, Component.

4. Can you provide details about the market size?

The market size is estimated to be USD 15.62 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Demand For Power Quality In Industrial And Manufacturing Sectors4.; Increase In Smart Grid Infrastructure.

6. What are the notable trends driving market growth?

HVDC Converter Segment to Witness Significant Demand.

7. Are there any restraints impacting market growth?

4.; High Costs Of Power Quality Equipment.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "HVDC Converters Station Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the HVDC Converters Station Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the HVDC Converters Station Industry?

To stay informed about further developments, trends, and reports in the HVDC Converters Station Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence