Key Insights

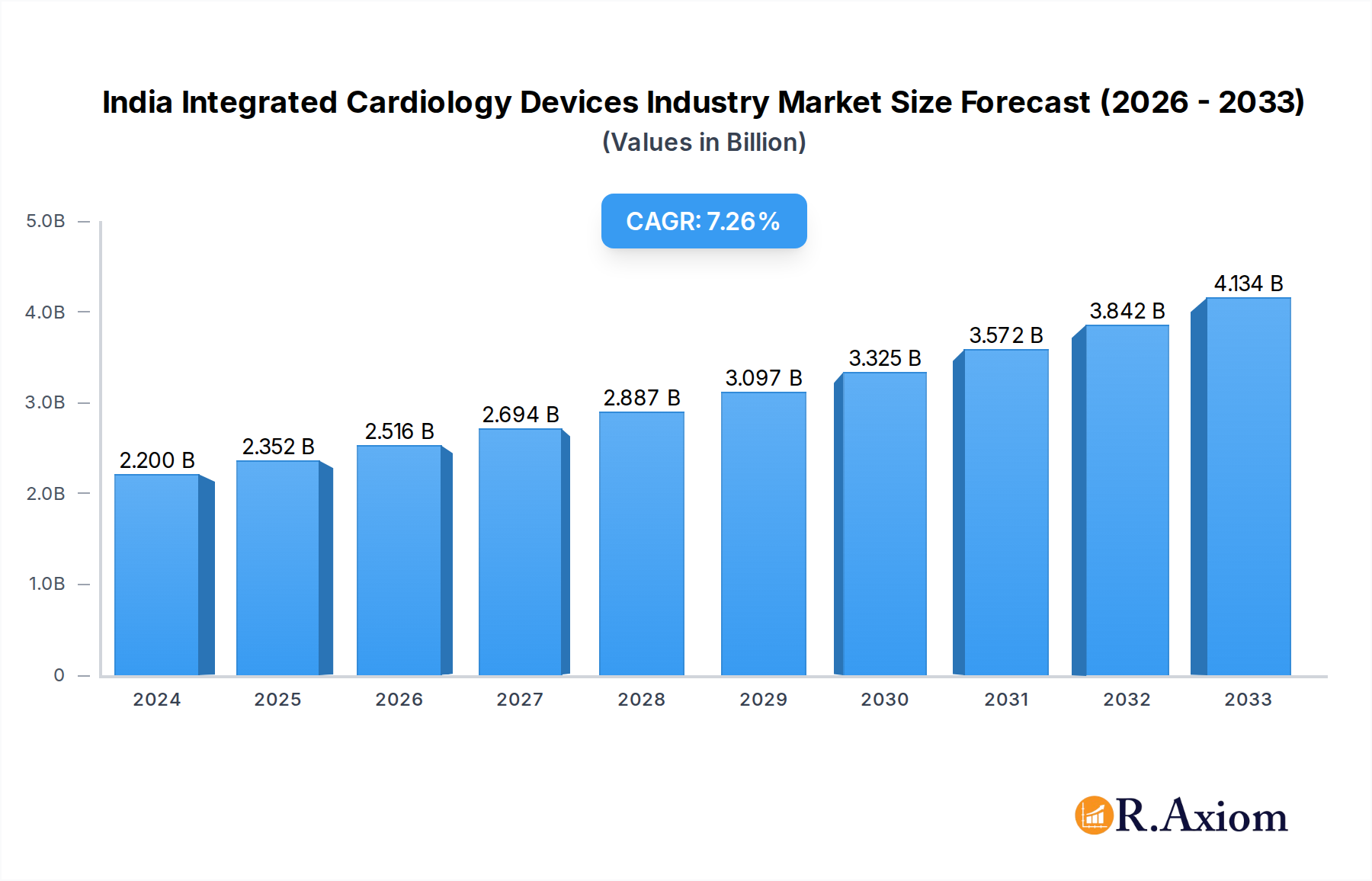

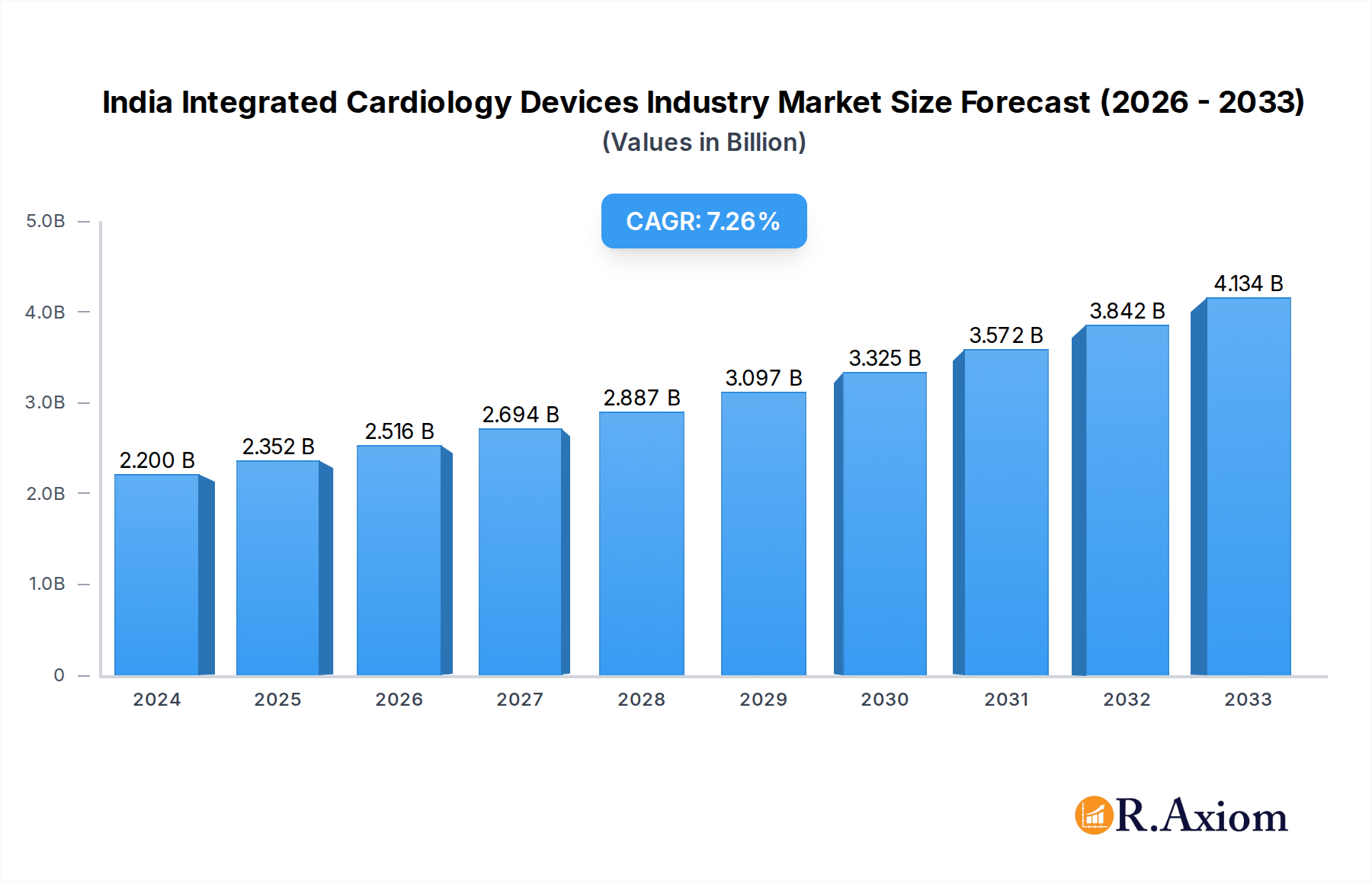

The Indian Integrated Cardiology Devices market is poised for significant expansion, projected to reach an estimated USD 2.2 billion in 2024. This robust growth is driven by a confluence of factors, including the escalating prevalence of cardiovascular diseases (CVDs) across the nation, an aging population, and increasing disposable incomes that enhance access to advanced healthcare solutions. The market is further propelled by governmental initiatives focused on improving healthcare infrastructure and promoting public health awareness regarding cardiac conditions. Key therapeutic areas, such as cardiac rhythm management devices, angioplasty stents, and advanced diagnostic tools like ECG and remote monitoring systems, are witnessing heightened demand. This surge is attributed to technological advancements leading to more effective, less invasive, and patient-friendly treatment options.

India Integrated Cardiology Devices Industry Market Size (In Billion)

The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% from 2025 to 2033, indicating sustained momentum. This growth trajectory is supported by a burgeoning healthcare sector, increasing investments in research and development by leading global and domestic players, and a growing preference for minimally invasive surgical procedures. The diagnostic and monitoring segment, encompassing ECG and remote cardiac monitoring, is expected to witness substantial uptake due to the increasing focus on early detection and continuous patient management. Similarly, the therapeutic and surgical devices segment, including cardiac assist devices, grafts, and heart valves, is benefiting from improved healthcare affordability and the availability of sophisticated medical technologies. Despite the promising outlook, challenges such as high costs of advanced devices and the need for specialized training for healthcare professionals may present some restraints.

India Integrated Cardiology Devices Industry Company Market Share

India Integrated Cardiology Devices Industry Market Concentration & Innovation

The Indian integrated cardiology devices market exhibits a moderate to high concentration, driven by a few key global and domestic players that command significant market share. Innovation is a crucial differentiator, with companies investing heavily in research and development to introduce advanced solutions for cardiac care.

- Market Share Dynamics: Leading companies like Medtronic PLC, Abbott Laboratories, and Siemens Healthineers hold substantial portions of the market. For instance, Medtronic's market share in cardiac rhythm management is estimated to be over 30 billion INR. Abbott Laboratories' diagnostics segment contributes another 25 billion INR to the overall market. GE Healthcare and Boston Scientific Corporation also maintain significant footprints.

- Innovation Drivers: Key innovation drivers include the increasing prevalence of cardiovascular diseases (CVDs) in India, rising disposable incomes, and a growing demand for minimally invasive procedures. Technological advancements in areas like remote monitoring and artificial intelligence are further propelling innovation.

- Regulatory Frameworks: The regulatory landscape, overseen by bodies like the Central Drugs Standard Control Organisation (CDSCO), is becoming more stringent, requiring rigorous product testing and approval processes, which can influence market entry for new players.

- Product Substitutes: While direct product substitutes are limited for advanced cardiac devices, less invasive or non-device-based treatments for certain cardiac conditions can pose indirect competition.

- End-User Trends: An increasing preference for patient-centric solutions, wearable diagnostic devices, and home-based monitoring systems is shaping product development and adoption.

- Mergers & Acquisitions (M&A): Strategic M&A activities are a key aspect of market consolidation and expansion. While specific deal values for India are not publicly disclosed, global M&A in cardiology devices often runs into billions of dollars. For example, historical global acquisitions by players like Boston Scientific or Abbott in similar segments often exceed 1 billion INR, indicating a trend towards strategic consolidation.

India Integrated Cardiology Devices Industry Industry Trends & Insights

The India Integrated Cardiology Devices Industry is poised for significant expansion, driven by a confluence of favorable demographic trends, escalating healthcare expenditure, and rapid technological advancements. The market is projected to witness a robust Compound Annual Growth Rate (CAGR) of approximately 12.5% from 2025 to 2033, reaching an estimated market size of over 150 billion INR by 2033. This impressive growth trajectory is underpinned by several dynamic forces shaping the landscape of cardiac care in the nation.

One of the primary growth drivers is the alarming rise in cardiovascular diseases (CVDs) across India. Factors such as changing lifestyles, increasing stress levels, sedentary habits, and a growing aging population have contributed to a surge in conditions like coronary artery disease, heart failure, and arrhythmias. This escalating disease burden directly translates into a higher demand for diagnostic, monitoring, and therapeutic cardiology devices. As the prevalence of CVDs continues to climb, the need for advanced medical interventions and sophisticated monitoring solutions becomes paramount, fueling market growth.

Technological disruptions are revolutionizing the cardiology devices sector. The integration of Artificial Intelligence (AI) and Machine Learning (ML) in diagnostic imaging and data analysis is enabling earlier and more accurate detection of cardiac abnormalities. Furthermore, the advent of wearable devices and remote patient monitoring systems is transforming how cardiac health is managed, allowing for continuous tracking of vital signs and timely interventions, thereby improving patient outcomes and reducing hospitalizations. Miniaturization and enhanced biocompatibility of devices, particularly in areas like pacemakers and artificial valves, are also key technological advancements enhancing patient comfort and device efficacy.

Consumer preferences are increasingly shifting towards accessible, affordable, and effective healthcare solutions. There is a growing awareness among the Indian populace about cardiac health and the importance of early diagnosis and treatment. This heightened awareness, coupled with rising disposable incomes and better insurance penetration, is driving the demand for sophisticated cardiology devices. Patients and healthcare providers alike are seeking minimally invasive procedures and long-term monitoring solutions that improve quality of life and reduce the overall cost of care. The demand for personalized medicine and patient-specific treatments is also gaining traction.

The competitive dynamics within the Indian integrated cardiology devices market are characterized by the presence of both established multinational corporations and emerging domestic players. Global giants like Medtronic PLC, Abbott Laboratories, Siemens Healthineers, GE Healthcare, and Boston Scientific Corporation hold a strong presence, leveraging their extensive product portfolios and technological expertise. However, domestic manufacturers are increasingly innovating and capturing market share, particularly in segments like basic diagnostic devices and certain therapeutic implants, often by offering more cost-effective solutions. Strategic collaborations, partnerships, and continuous product innovation are key strategies employed by players to maintain and enhance their market position. The competitive landscape is further shaped by evolving government policies aimed at boosting domestic manufacturing and healthcare infrastructure development.

Dominant Markets & Segments in India Integrated Cardiology Devices Industry

The India Integrated Cardiology Devices Industry is a multifaceted sector with distinct segments contributing to its overall growth. Understanding the dominance of specific markets and segments is crucial for strategic planning and investment.

Diagnostic and Monitoring Devices

This segment forms the bedrock of proactive cardiac care, enabling early detection, diagnosis, and continuous management of cardiovascular conditions.

- Electrocardiogram (ECG) Devices:

- Dominance Drivers: The widespread prevalence of cardiac ailments, coupled with increasing awareness about early diagnosis, makes ECG devices a cornerstone. The affordability and portability of modern ECG machines, including Holter monitors and event recorders, have significantly contributed to their adoption in both hospital settings and remote healthcare facilities. Government initiatives aimed at strengthening primary healthcare infrastructure also play a crucial role in driving the penetration of ECG devices.

- Market Penetration: ECG devices have achieved a high market penetration, especially in urban and semi-urban areas. The increasing use of wearable ECG monitors and smartphone-integrated ECG devices is further expanding their reach into households, enabling continuous patient monitoring and early anomaly detection.

- Remote Cardiac Monitoring:

- Dominance Drivers: The growing demand for chronic disease management, coupled with the need for continuous patient oversight without frequent hospital visits, has propelled remote cardiac monitoring. This includes implantable cardiac monitors, wearable patches, and mobile cardiac telemetry systems. The shift towards telehealth and home-based care models, accelerated by recent global health events, has further amplified the importance of this segment. The rising incidence of heart failure and atrial fibrillation necessitates constant monitoring for timely intervention.

- Market Penetration: While still a growing segment, remote cardiac monitoring is witnessing rapid adoption, particularly in managing post-operative patients and individuals with chronic cardiac conditions. The increasing availability of user-friendly devices and supportive reimbursement policies are key factors driving its penetration.

- Other Diagnostic and Monitoring Devices:

- Dominance Drivers: This sub-segment encompasses a range of devices such as cardiac ultrasound machines (echocardiography), cardiac MRI, cardiac CT scanners, and stress testing equipment. The increasing complexity of cardiac diagnoses and the need for detailed imaging and functional assessments drive the demand for these advanced diagnostic tools. Investments in upgrading hospital infrastructure and the growing number of specialized cardiology centers contribute to their dominance.

- Market Penetration: These advanced diagnostic tools have a strong presence in tertiary care hospitals and specialized cardiac centers. The evolving technological capabilities, offering higher resolution and faster scanning times, continue to drive their adoption and market penetration in advanced healthcare settings.

Therapeutic and Surgical Devices

This segment focuses on interventions, treatments, and surgical procedures aimed at managing and correcting cardiac conditions, representing a significant and high-value market.

- Cardiac Assist Devices:

- Dominance Drivers: The rising burden of heart failure and the growing need for mechanical circulatory support have fueled the demand for cardiac assist devices, including Ventricular Assist Devices (VADs) and artificial hearts. These devices offer a lifeline to patients awaiting heart transplants or those with end-stage heart failure. Advancements in device design, aiming for smaller footprints, longer battery life, and improved biocompatibility, are key drivers.

- Market Penetration: While still a niche segment due to high cost and complexity, the market penetration of cardiac assist devices is steadily increasing with improved clinical outcomes and growing expertise among cardiac surgeons.

- Cardiac Rhythm Management (CRM) Devices:

- Dominance Drivers: This segment, encompassing pacemakers, implantable cardioverter-defibrillators (ICDs), and cardiac resynchronization therapy (CRT) devices, is a major contributor to the market. The escalating prevalence of arrhythmias and heart failure, coupled with an aging population, drives the demand for these life-saving devices. Technological advancements in miniaturization, longer battery life, MRI compatibility, and remote monitoring capabilities for CRM devices further boost their adoption.

- Market Penetration: CRM devices have achieved significant market penetration, with a robust network of implanting centers and trained cardiologists across India. The increasing affordability of basic models also contributes to broader accessibility.

- Catheters:

- Dominance Drivers: Catheters, including diagnostic and interventional (e.g., angioplasty, ablation) catheters, are indispensable in minimally invasive cardiac procedures. The global shift towards percutaneous interventions (PCI) over open-heart surgery significantly boosts the demand for various types of catheters. Technological innovations focusing on steerability, trackability, and deliverability of complex devices are key growth catalysts.

- Market Penetration: Catheters exhibit very high market penetration, being integral to a wide array of cardiac procedures performed daily in cath labs across India.

- Grafts:

- Dominance Drivers: Vascular grafts are essential for bypass surgeries, particularly coronary artery bypass grafting (CABG). While the trend is shifting towards less invasive procedures, CABG remains a critical treatment for severe coronary artery disease. The demand is driven by the continued need for revascularization in complex multi-vessel disease.

- Market Penetration: Grafts have a consistent market penetration tied to the volume of bypass surgeries performed.

- Heart Valves:

- Dominance Drivers: The increasing incidence of valvular heart disease, particularly among the aging population, drives the demand for both surgical and transcatheter heart valves. The development of advanced transcatheter aortic valve implantation (TAVI) and transcatheter mitral valve repair/replacement (TMR/TMR) technologies is revolutionizing treatment options and expanding the market.

- Market Penetration: Traditional surgical heart valves have high penetration. Transcatheter heart valves are a rapidly growing segment with increasing penetration as technology matures and becomes more accessible.

- Stents:

- Dominance Drivers: Drug-eluting stents (DES) are the mainstay for treating coronary artery blockages through angioplasty. The high and growing prevalence of coronary artery disease in India ensures consistent demand. Innovations in stent technology, such as bioresorbable scaffolds and advanced drug-eluting coatings, continue to drive segment growth and market penetration.

- Market Penetration: Stents enjoy extremely high market penetration, being one of the most frequently implanted cardiac devices.

- Other Therapeutics and Surgical Devices:

- Dominance Drivers: This broad category includes surgical instruments, artificial blood pumps, occluders, septal defect closure devices, and annuloplasty rings. The expanding scope of cardiac interventions and the development of novel devices to address specific anatomical or physiological challenges drive the demand.

- Market Penetration: Penetration varies significantly based on the specific device, with some being standard across multiple procedures and others being used in highly specialized interventions.

India Integrated Cardiology Devices Industry Product Developments

Product development in the Indian integrated cardiology devices industry is characterized by a strong focus on enhancing patient outcomes and procedural efficiency. Innovations are geared towards miniaturization, improved biocompatibility, longer device longevity, and increased connectivity for remote monitoring. Companies are introducing advanced drug-eluting stents with novel drug coatings for better restenosis rates, and sophisticated cardiac rhythm management devices offering enhanced diagnostic capabilities and remote data transmission. Furthermore, the development of transcatheter valve technologies is revolutionizing structural heart interventions, offering less invasive alternatives for patients with valvular heart disease. The integration of AI and machine learning in diagnostic imaging and therapeutic planning further promises more personalized and precise cardiac care solutions.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the India Integrated Cardiology Devices Industry, segmented by Device Type. The two primary categories are:

Diagnostic and Monitoring Devices: This segment encompasses devices used for identifying and tracking cardiovascular conditions. It includes:

- Electrocardiogram (ECG) Devices: covering handheld ECGs, Holter monitors, and event recorders.

- Remote Cardiac Monitoring: including wearable patches, implantable monitors, and telemetry systems.

- Other Diagnostic and Monitoring Devices: such as echocardiography machines, cardiac CT scanners, and stress testing equipment.

Therapeutic and Surgical Devices: This segment comprises devices employed in treating and surgically managing cardiac ailments. It includes:

- Cardiac Assist Devices: such as Ventricular Assist Devices (VADs).

- Cardiac Rhythm Management Devices: including pacemakers, ICDs, and CRT devices.

- Catheter: both diagnostic and interventional catheters for various procedures.

- Grafts: used in bypass surgeries.

- Heart Valves: both surgical and transcatheter valves.

- Stents: primarily for coronary artery interventions.

- Other Therapeutics and Surgical Devices: covering a range of instruments and implants.

The analysis will detail market sizes, growth projections, and competitive dynamics within each of these sub-segments for the study period.

Key Drivers of India Integrated Cardiology Devices Industry Growth

The growth of the India Integrated Cardiology Devices Industry is propelled by several interconnected factors.

- Rising Prevalence of Cardiovascular Diseases: India faces an epidemic of heart disease, driven by lifestyle changes, obesity, and an aging population, creating a persistent and growing demand for cardiac devices.

- Increasing Healthcare Expenditure and Infrastructure Development: Both public and private investments in healthcare infrastructure, including the establishment of specialized cardiac centers and cath labs, directly fuel device adoption.

- Technological Advancements and Innovation: Continuous innovation in areas like minimally invasive techniques, miniaturization, remote monitoring, and AI-powered diagnostics leads to the development of more effective and patient-friendly devices.

- Growing Awareness and Demand for Advanced Healthcare: Increased patient awareness about cardiac health and a desire for better treatment outcomes drive the demand for sophisticated cardiology devices.

- Government Initiatives and Favorable Policies: Programs like "Make in India" and initiatives to improve access to quality healthcare indirectly support the domestic cardiology devices market.

Challenges in the India Integrated Cardiology Devices Industry Sector

Despite robust growth prospects, the India Integrated Cardiology Devices Industry faces several challenges.

- High Cost of Advanced Devices: Many sophisticated cardiology devices remain expensive, limiting accessibility for a significant portion of the population, especially in rural areas.

- Stringent Regulatory Approvals: Navigating the complex regulatory approval processes for medical devices can be time-consuming and costly, posing a barrier to entry for new players.

- Infrastructure Gaps: While improving, disparities in healthcare infrastructure, particularly in remote regions, hinder the widespread adoption and servicing of advanced cardiology devices.

- Skilled Workforce Shortage: A lack of adequately trained medical professionals for implanting and managing complex cardiac devices can be a bottleneck.

- Price Sensitivity and Competition: Intense competition, particularly from domestic manufacturers offering lower-cost alternatives for certain devices, puts pressure on profit margins for premium products.

Emerging Opportunities in India Integrated Cardiology Devices Industry

The Indian Integrated Cardiology Devices Industry is ripe with emerging opportunities.

- Expansion of Telemedicine and Remote Monitoring: The growing acceptance of telehealth presents a significant opportunity for remote cardiac monitoring devices, enabling continuous patient care and early intervention.

- Focus on Preventive Cardiology: Increased emphasis on preventive healthcare creates a demand for early diagnostic tools and wearable devices for continuous health tracking.

- Advancements in AI and Machine Learning: The integration of AI in device diagnostics and treatment planning offers potential for highly personalized and efficient cardiac care.

- Growth in Tier 2 and Tier 3 Cities: Expanding healthcare infrastructure and rising disposable incomes in smaller cities offer untapped market potential for a wider range of cardiology devices.

- Domestic Manufacturing and Innovation: Government support for domestic manufacturing and increasing R&D capabilities among Indian companies present opportunities for localized innovation and cost-effective solutions.

Leading Players in the India Integrated Cardiology Devices Industry Market

- Siemens Healthineers

- Terumo Corporation

- GE Healthcare

- Abbott Laboratories

- Cardinal Health Inc

- Medtronic PLC

- B Braun Melsungen AG

- W L Gore and Associates

- Canon Medical Systems

- Boston Scientific Corporation

Key Developments in India Integrated Cardiology Devices Industry Industry

- November 2021: India Medtronic Private Limited launched the Arctic Front Cardiac Cryoablation Catheter System, a cryoballoon catheter approved by CDSCO to treat atrial fibrillation (AF) in India.

- February 2021: Siemens Healthineers introduced Corindus CorPath GRX Robotic System for coronary and peripheral vascular interventions in India.

Strategic Outlook for India Integrated Cardiology Devices Industry Market

The strategic outlook for the India Integrated Cardiology Devices Industry remains exceptionally positive, driven by a growing and aging population, increasing prevalence of cardiovascular diseases, and a rapidly expanding healthcare sector. The market will witness continued growth fueled by technological advancements, particularly in minimally invasive techniques, remote patient monitoring, and AI-driven diagnostics. Key growth catalysts will include strategic partnerships between global and domestic players, increased government focus on healthcare accessibility, and a rising demand for advanced, patient-centric cardiac care solutions. Companies that can offer innovative, cost-effective, and integrated solutions, while navigating the evolving regulatory landscape, are well-positioned for sustained success and market leadership in the coming years. The emphasis on preventive cardiology and early detection will also unlock new market segments and opportunities for growth.

India Integrated Cardiology Devices Industry Segmentation

-

1. Device Type

-

1.1. Diagnostic and Monitoring Devices

- 1.1.1. Electrocardiogram (ECG)

- 1.1.2. Remote Cardiac Monitoring

- 1.1.3. Other Diagnostic and Monitoring Devices

-

1.2. Therapeutic and Surgical Devices

- 1.2.1. Cardiac Assist Devices

- 1.2.2. Cardiac Rhythm Management Devices

- 1.2.3. Catheter

- 1.2.4. Grafts

- 1.2.5. Heart Valves

- 1.2.6. Stents

- 1.2.7. Other Therapeutics and Surgical Devices

-

1.1. Diagnostic and Monitoring Devices

India Integrated Cardiology Devices Industry Segmentation By Geography

- 1. India

India Integrated Cardiology Devices Industry Regional Market Share

Geographic Coverage of India Integrated Cardiology Devices Industry

India Integrated Cardiology Devices Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 5.1.1. Diagnostic and Monitoring Devices

- 5.1.1.1. Electrocardiogram (ECG)

- 5.1.1.2. Remote Cardiac Monitoring

- 5.1.1.3. Other Diagnostic and Monitoring Devices

- 5.1.2. Therapeutic and Surgical Devices

- 5.1.2.1. Cardiac Assist Devices

- 5.1.2.2. Cardiac Rhythm Management Devices

- 5.1.2.3. Catheter

- 5.1.2.4. Grafts

- 5.1.2.5. Heart Valves

- 5.1.2.6. Stents

- 5.1.2.7. Other Therapeutics and Surgical Devices

- 5.1.1. Diagnostic and Monitoring Devices

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. India

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 6. India Integrated Cardiology Devices Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Device Type

- 6.1.1. Diagnostic and Monitoring Devices

- 6.1.1.1. Electrocardiogram (ECG)

- 6.1.1.2. Remote Cardiac Monitoring

- 6.1.1.3. Other Diagnostic and Monitoring Devices

- 6.1.2. Therapeutic and Surgical Devices

- 6.1.2.1. Cardiac Assist Devices

- 6.1.2.2. Cardiac Rhythm Management Devices

- 6.1.2.3. Catheter

- 6.1.2.4. Grafts

- 6.1.2.5. Heart Valves

- 6.1.2.6. Stents

- 6.1.2.7. Other Therapeutics and Surgical Devices

- 6.1.1. Diagnostic and Monitoring Devices

- 6.1. Market Analysis, Insights and Forecast - by Device Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Siemens Healthineers

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Terumo Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 GE Healthcare

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Abbott Laboratories

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Cardinal Health Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Medtronic PLC

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 B Braun Melsungen AG

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 W L Gore and Associates

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Canon Medical Systems

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Boston Scientific Corporation

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Siemens Healthineers

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: India Integrated Cardiology Devices Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: India Integrated Cardiology Devices Industry Share (%) by Company 2025

List of Tables

- Table 1: India Integrated Cardiology Devices Industry Revenue billion Forecast, by Device Type 2020 & 2033

- Table 2: India Integrated Cardiology Devices Industry Volume K Tons Forecast, by Device Type 2020 & 2033

- Table 3: India Integrated Cardiology Devices Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: India Integrated Cardiology Devices Industry Volume K Tons Forecast, by Region 2020 & 2033

- Table 5: India Integrated Cardiology Devices Industry Revenue billion Forecast, by Device Type 2020 & 2033

- Table 6: India Integrated Cardiology Devices Industry Volume K Tons Forecast, by Device Type 2020 & 2033

- Table 7: India Integrated Cardiology Devices Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 8: India Integrated Cardiology Devices Industry Volume K Tons Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Integrated Cardiology Devices Industry?

The projected CAGR is approximately 6.8%.

2. Which companies are prominent players in the India Integrated Cardiology Devices Industry?

Key companies in the market include Siemens Healthineers, Terumo Corporation, GE Healthcare, Abbott Laboratories, Cardinal Health Inc, Medtronic PLC, B Braun Melsungen AG, W L Gore and Associates, Canon Medical Systems, Boston Scientific Corporation.

3. What are the main segments of the India Integrated Cardiology Devices Industry?

The market segments include Device Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.2 billion as of 2022.

5. What are some drivers contributing to market growth?

Rapid Technological Advances; Increased Preference of Minimally Invasive Procedures.

6. What are the notable trends driving market growth?

Remote Cardiac Monitoring Devices are Expected to Witness Rapid Growth.

7. Are there any restraints impacting market growth?

Stringent Regulatory Policies; High Cost of Instruments and Procedures.

8. Can you provide examples of recent developments in the market?

In November 2021, India Medtronic Private Limited launched the Arctic Front Cardiac Cryoablation Catheter System, a cryoballoon catheter approved by CDSCO to treat atrial fibrillation (AF) in India.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Integrated Cardiology Devices Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Integrated Cardiology Devices Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Integrated Cardiology Devices Industry?

To stay informed about further developments, trends, and reports in the India Integrated Cardiology Devices Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence