Key Insights

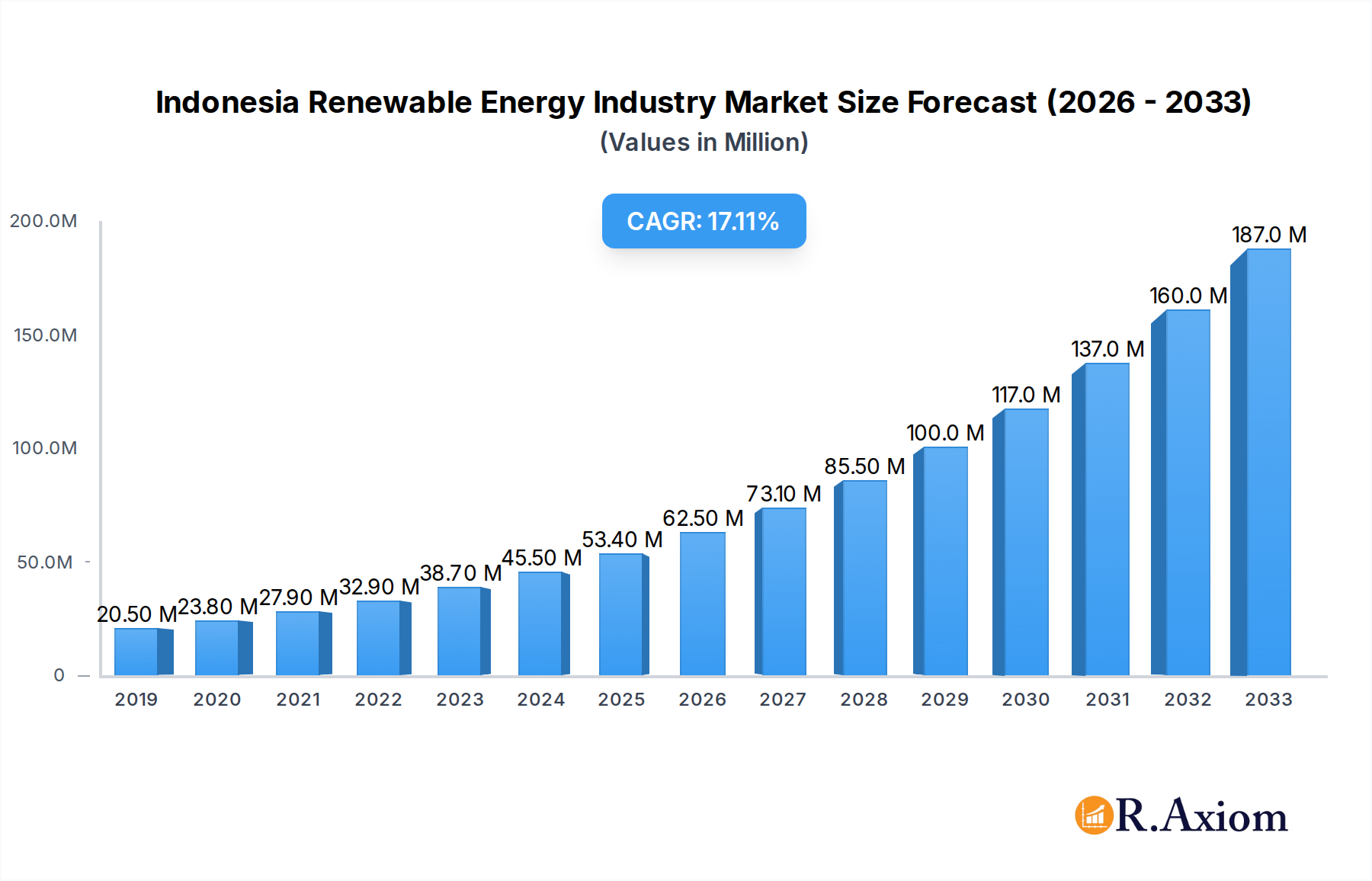

The Indonesia Renewable Energy Industry is poised for substantial growth, driven by ambitious government targets and a burgeoning demand for sustainable power. Valued at an estimated 63.21 billion USD in 2025, the market is projected to expand significantly with a robust CAGR of 15.2% from 2025 to 2033. This impressive trajectory is primarily fueled by Indonesia's strategic commitment to achieving Net Zero Emissions, coupled with the imperative to enhance energy security and reduce reliance on conventional fossil fuels. Rapid urbanization and industrial expansion across the archipelago are also escalating electricity demand, creating a fertile ground for renewable energy adoption. Key players like PLN Renewables, Pertamina Geothermal Energy, and Medco Power Indonesia, alongside international firms such as Canadian Solar Inc. and Trina Solar Ltd, are actively investing in the sector, particularly in solar, geothermal, and hydropower projects, capitalizing on the country's abundant natural resources.

Indonesia Renewable Energy Industry Market Size (In Billion)

Emerging trends underscore the market's dynamic evolution, with accelerated deployment of rooftop solar installations and a strong focus on harnessing Indonesia's vast geothermal potential, given its position on the Ring of Fire. The increasing emphasis on off-grid solutions, particularly in remote islands, alongside advancements in smart grid technology and energy storage, is transforming the energy landscape. However, the industry faces hurdles such as substantial initial capital requirements, complexities in land acquisition and permitting processes, and the need for robust grid infrastructure upgrades to integrate intermittent renewable sources effectively. Despite these challenges, the market offers immense opportunities across diverse segments, including solar (active and passive), wind (offshore and onshore), hydroelectric, and biomass, with applications spanning electricity generation, heating, cooling, and transportation. The residential, commercial, industrial, and utility sectors are all crucial end-users, propelling the demand for both on-grid and off-grid renewable solutions, making Indonesia a pivotal market for green energy innovation and investment.

Indonesia Renewable Energy Industry Company Market Share

This comprehensive report offers an in-depth analysis of the burgeoning Indonesia Renewable Energy Industry, a critical sector poised for significant expansion amidst global decarbonization efforts and increasing domestic energy demand. Spanning the historical period of 2019–2024, with 2025 as the base and estimated year, and forecasting market trends through 2033, this study delivers unparalleled insights into market drivers, challenges, emerging opportunities, and competitive landscapes. We explore critical segments like Solar Energy (Active Energy, Passive Energy), Wind Energy (Offshore, Onshore), Hydroelectric Energy, Ocean Energy, Geothermal Energy, and Biomass Energy (Biowaste, Biofuel, Wood, Others), alongside connectivity (On-grid, Off-grid), applications (Heating and Cooling, Electricity Generation, Transportation), and diverse end-user segments (Residential, Commercial, Industrial, Utility). Unlock strategic decision-making with data-driven projections and expert analysis for stakeholders navigating Indonesia's dynamic clean energy transition.

Indonesia Renewable Energy Industry Market Concentration & Innovation

The Indonesia Renewable Energy Industry exhibits a moderate level of market concentration, with several established players alongside a growing number of new entrants, fostering a dynamic yet competitive environment. While state-owned entities like PLN Renewables and Pertamina Geothermal Energy command significant portions of the market, particularly in utility-scale projects, private and international firms like Medco Power Indonesia, Star Energy Geothermal, and newer players such as Xurya Daya Indonesia are rapidly expanding their footprints, especially in solar and distributed generation. The top three players collectively held an estimated xx billion in market share in 2024, primarily driven by large-scale infrastructure projects and concessions. Innovation drivers are multifaceted, propelled by favorable regulatory frameworks, technological advancements, and increasing private investment in sustainable energy solutions.

Regulatory frameworks, including the National Energy Policy (KEN) and various incentive schemes, are crucial in shaping market dynamics and encouraging innovation. These policies aim to reduce reliance on fossil fuels and achieve ambitious renewable energy targets, stimulating R&D in areas like high-efficiency solar panels, advanced geothermal drilling technologies, and sophisticated battery storage solutions. Product substitutes, predominantly coal and natural gas, still represent a significant challenge, requiring continuous innovation in cost reduction and efficiency to enhance the competitiveness of renewables. End-user trends show a growing preference for decentralized energy solutions and increased awareness of environmental benefits, driving demand for rooftop solar (Active Energy) in residential and commercial sectors.

Mergers and acquisitions (M&A) activities are strategically shaping the industry landscape. In 2023, M&A deal values in the sector surpassed xx billion, reflecting consolidation efforts and strategic partnerships aimed at expanding portfolios, gaining technological edge, or securing market access. For instance, Canadian Solar Inc. and Trina Solar Ltd often engage in strategic collaborations or supply chain partnerships to strengthen their presence. The partnership between SEG Solar and PT ATW Investasi Selaras for a 5GW solar cell manufacturing facility, involving a USD 500 million investment, exemplifies a significant strategic move towards localizing technology and supply chains, enhancing the nation’s renewable energy independence and fostering domestic innovation. This focus on local manufacturing not only mitigates supply chain risks but also creates a robust ecosystem for further technological advancements within Indonesia.

Indonesia Renewable Energy Industry Industry Trends & Insights

The Indonesia Renewable Energy Industry is on an accelerated growth trajectory, driven by robust market growth drivers including escalating energy demand, ambitious climate change mitigation targets, and increasing foreign and domestic investments. The nation’s rapidly expanding economy and population necessitate a substantial increase in electricity generation, with renewable sources offering a sustainable path forward. Government initiatives, such as the target to achieve 23% renewable energy in the national energy mix by 2025 and net-zero emissions by 2060, are providing strong policy impetus and regulatory certainty, attracting significant capital inflows into the sector. Global commitments to decarbonization and the availability of green financing mechanisms further bolster investment, positioning Indonesia as a key player in the global energy transition. The industry is projected to grow at a Compound Annual Growth Rate (CAGR) of xx% from 2025 to 2033, fueled by these converging factors.

Technological disruptions are fundamentally reshaping the competitive landscape. Advancements in solar photovoltaic (PV) technology, including higher efficiency rates and reduced manufacturing costs, are making solar energy increasingly competitive. Similarly, improvements in wind turbine design, energy storage solutions like lithium-ion batteries, and smart grid integration technologies are enhancing the reliability and scalability of renewable power. Geothermal energy, a natural advantage for Indonesia given its volcanic belt, is seeing innovations in drilling techniques and resource exploration, unlocking previously inaccessible reserves. These technological leaps are not only driving down the Levelized Cost of Energy (LCOE) but also enabling more efficient resource utilization and grid integration. The market penetration of renewable energy reached an estimated xx% of the total energy mix in 2024, showcasing a tangible shift towards cleaner power sources.

Consumer preferences are also playing a pivotal role in shaping industry trends. A growing awareness of environmental issues, coupled with the desire for energy independence and resilience, is driving demand for distributed generation solutions like rooftop solar among residential and commercial end-users. Businesses are increasingly seeking renewable energy options to meet their sustainability goals and reduce operational costs, influencing the rise of Corporate Power Purchase Agreements (PPAs). This shift is particularly evident in the Industrial segment, where companies are looking to secure stable, green energy supplies. Competitive dynamics are characterized by intense rivalry among established players and agile new entrants. Cost leadership, technological differentiation, and robust project development capabilities are key success factors. Companies like TotalEnergies ENEOS, ACWA Power, and Masdar are bringing international expertise and capital, intensifying competition but also accelerating innovation and development within the Indonesian market. The availability of diverse financing options, including green bonds and project finance, is also impacting competitive strategies, allowing companies to undertake larger and more complex projects, further diversifying Indonesia's renewable energy portfolio.

Dominant Markets & Segments in Indonesia Renewable Energy Industry

Within the Indonesia Renewable Energy Industry, Solar Energy stands out as the dominant segment, commanding significant attention and investment, and is projected to expand robustly throughout the forecast period. This dominance is primarily driven by its versatility, rapid deployment capabilities, and decreasing cost profile, making it highly attractive across various applications and end-user segments. Solar Energy (Active Energy, Passive Energy) held an estimated market value of over xx billion in 2024 and is projected to expand at a CAGR of xx% from 2025 to 2033. While Indonesia possesses immense geothermal potential, the scalability and quicker deployment of solar projects, coupled with strong government support and technological advancements, position it as the frontrunner.

Key drivers contributing to Solar Energy’s dominance include:

- Favorable Economic Policies: Government initiatives like net metering, feed-in tariffs, and tax incentives for renewable energy projects, particularly solar, significantly reduce initial investment burdens and improve project viability.

- Abundant Solar Irradiation: Indonesia benefits from high levels of solar irradiation across its archipelago, making solar power generation highly efficient and geographically widespread.

- Technological Advancements and Cost Reduction: Continuous improvements in solar panel efficiency, battery storage solutions, and inverter technologies, coupled with global reductions in manufacturing costs, have made solar power increasingly competitive with conventional energy sources.

- Infrastructure Development: The expansion of national grid infrastructure facilitates the integration of utility-scale solar farms, while the growing demand for off-grid solutions in remote areas further propels smaller-scale solar installations.

- Rapid Deployment and Scalability: Solar projects, from residential rooftop installations to large utility-scale farms, can be deployed relatively quickly compared to other renewable energy sources, addressing urgent energy demand.

- Environmental Imperatives: Growing public and corporate awareness of climate change, along with Indonesia's commitment to reducing carbon emissions, fosters a strong demand for clean energy alternatives like solar.

Solar Energy's dominance is further reinforced by its broad applicability across end-user segments. In the Residential and Commercial sectors, rooftop solar (Active Energy) installations are booming due to direct cost savings and energy independence. The Industrial sector increasingly adopts solar for significant operational cost reductions and to meet sustainability targets. Furthermore, the Utility segment is investing heavily in large-scale solar farms, often hybridized with battery storage, to stabilize the grid and meet peak demand. The recent announcement by SEG Solar and PT ATW Investasi Selaras to invest USD 500 million in developing a 5GW solar cell and 3GW solar module manufacturing facility in Central Java underscores the immense potential and strategic importance of solar power in Indonesia. This investment not only enhances domestic manufacturing capacity but also solidifies Indonesia's position in the global solar supply chain, ensuring long-term growth and technological self-sufficiency in this dominant segment. While Geothermal Energy remains strategically vital due to its baseload capacity and significant untapped potential, and Hydroelectric Energy provides substantial contributions from existing infrastructure, Solar Energy's immediate scalability, economic viability, and widespread adoption capabilities firmly establish its leading position in Indonesia's renewable energy landscape.

Indonesia Renewable Energy Industry Product Developments

Product developments in the Indonesia Renewable Energy Industry are focused on enhancing efficiency, reducing costs, and improving grid integration. Innovations in solar energy include high-efficiency monocrystalline and bifacial PV modules, alongside advanced inverter technologies that optimize energy harvesting. Battery energy storage systems (BESS) are gaining traction, allowing for better grid stability and the integration of intermittent renewables. For geothermal, advancements in drilling techniques and binary cycle power plants are enabling the exploitation of lower-temperature resources, expanding viable sites. Biomass energy sees innovations in sustainable feedstock sourcing and efficient conversion technologies for biowaste and biofuel production. These technological trends are crucial for increasing the market fit of renewables, ensuring they provide reliable and competitive power across diverse applications from large utility grids to remote off-grid communities.

Report Scope & Segmentation Analysis

This report meticulously segments the Indonesia Renewable Energy Industry to provide granular insights. The Type segment encompasses Solar Energy (Active Energy, Passive Energy), Wind Energy (Offshore, Onshore), Hydroelectric Energy, Ocean Energy, Geothermal Energy, and Biomass Energy (Biowaste, Biofuel, Wood, Others). Solar Energy is projected to be valued at over xx billion in 2025, driven by declining costs and widespread adoption. The Connectivity segment differentiates between On-grid and Off-grid solutions, with Off-grid systems seeing significant growth in remote areas, valued at xx billion in 2025 due to electrification initiatives. The Application segment covers Heating and Cooling, Electricity Generation, and Transportation, with Electricity Generation dominating, poised to reach xx billion by 2025 as the primary use case. Lastly, the End User segment analyzes uptake across Residential, Commercial, Industrial, and Utility sectors, where the Utility segment holds the largest market share, estimated at xx billion, reflecting large-scale project investments and government mandates.

Key Drivers of Indonesia Renewable Energy Industry Growth

Indonesia’s renewable energy sector growth is significantly propelled by several key factors. Technologically, the declining cost of renewable energy components, particularly solar PV and wind turbines, coupled with advancements in energy storage solutions, makes clean energy increasingly competitive. Economically, the country's surging electricity demand, driven by population growth and industrial expansion, necessitates diversified energy sources beyond fossil fuels. Robust investment incentives, including tax holidays, import duty exemptions, and supportive financing mechanisms for green projects, are attracting substantial domestic and foreign capital. Regulatory factors play a crucial role, with the Indonesian government's ambitious renewable energy targets (23% by 2025) and commitment to net-zero emissions by 2060 providing a strong policy framework. For instance, PLN's green initiatives and collaborations like the pilot biomass project in South Sumatra underscore the commitment to meeting these goals and reducing greenhouse gas emissions.

Challenges in the Indonesia Renewable Energy Industry Sector

Despite immense potential, the Indonesia Renewable Energy Industry faces significant challenges. Regulatory hurdles, characterized by complex permitting processes, inconsistent policy implementation, and occasional delays in project approvals, can deter potential investors, potentially delaying projects worth billions. Supply chain issues, particularly reliance on imported components for solar and wind projects, can lead to increased costs and project timelines, impacting overall economic viability by an estimated xx%. Competitive pressures from heavily subsidized fossil fuels, coupled with established infrastructure for conventional power, create an uneven playing field for renewables. Land acquisition difficulties, particularly for large-scale utility projects, and inadequate transmission infrastructure in remote resource-rich areas further constrain development, potentially limiting capacity additions by several gigawatts annually and increasing investment risk by xx%.

Emerging Opportunities in Indonesia Renewable Energy Industry

The Indonesia Renewable Energy Industry is rich with emerging opportunities driven by evolving market dynamics and technological advancements. New market segments, particularly off-grid and hybrid energy solutions for the nation's vast archipelago, present significant growth potential, addressing energy access for millions. The development of green industrial zones, powered entirely by renewables, offers a chance for sustainable economic growth and attracts environmentally conscious foreign investment. Emerging technologies, such as advanced energy storage systems (e.g., pumped-hydro storage, green hydrogen production), floating solar PV, and smart grid solutions, promise to enhance grid stability and reliability. Moreover, a growing consumer preference for sustainable practices is opening avenues for innovative applications like electric vehicle (EV) charging infrastructure powered by renewables and smart home energy management systems, expanding the market beyond traditional utility-scale projects.

Leading Players in the Indonesia Renewable Energy Industry Market

- PLN Renewables

- Pertamina Geothermal Energy

- Star Energy Geothermal

- Medco Power Indonesia

- Canadian Solar Inc.

- Trina Solar Ltd

- PT Sumber Energi Sukses Makmur

- PT Barito Renewables Energy Tbk

- SEG Solar

- PT ATW Solar Indonesia

- Fourth Partner Energy Pvt Ltd

- Xurya Daya Indonesia

- TotalEnergies ENEOS

- ACWA Power

- Masdar

- Northstar PLTS

- Bright PLN Batam

- Others

Key Developments in Indonesia Renewable Energy Industry Industry

- June 2023: SEG Solar (SEG) and PT Kawasan Industri Terpadu Batang (KITB) entered a binding agreement for the lease of approximately 41 hectares of land in Batang Regency, Central Java, Indonesia. Through their joint-venture, PT SEG ATW Solar Manufaktur Indonesia, SEG plans a USD 500 million investment to construct a 5GW solar cell manufacturing facility and a 3GW solar module manufacturing facility. This pivotal development, in partnership with PT ATW Investasi Selaras (ATW Group), signifies a massive leap in localizing the solar energy supply chain, drastically boosting Indonesia's domestic manufacturing capacity for solar components and reducing reliance on imports. This move is expected to attract further investments and create thousands of jobs, significantly impacting market dynamics by fostering greater price competitiveness and technological self-sufficiency.

- December 2022: PT Bukit Asam Tbk (PTBA), a leading coal mining services provider, collaborated with the Ministry for Maritime Affairs and Investment and the Forest and Environmental Management ministry to develop a pilot biomass project in South Sumatra. This strategic collaboration highlights Indonesia's commitment to diversifying its energy mix beyond coal and aligning with greenhouse gas emission reduction targets. The project, expected to contribute to mangrove rehabilitation, demonstrates a multi-sectoral approach to sustainable development. This initiative supports the government’s broader environmental goals and aims to foster a domestic biomass supply chain, generating new economic opportunities while promoting a circular economy approach to waste management and energy production.

Strategic Outlook for Indonesia Renewable Energy Industry Market

The strategic outlook for the Indonesia Renewable Energy Industry market is overwhelmingly positive, characterized by strong growth catalysts that promise sustained expansion throughout the forecast period. The government's unwavering commitment to energy transition, coupled with a robust pipeline of private and public investments, forms the bedrock of future growth. Continued technological advancements, particularly in solar PV, energy storage, and smart grid integration, will further enhance the economic viability and operational efficiency of renewable projects. Indonesia's rising energy demand, driven by industrialization and urbanization, ensures a consistently expanding market for clean energy solutions. This confluence of factors presents immense future market potential, not only for achieving energy security and sustainability goals but also for positioning Indonesia as a regional leader in the green economy. Opportunities abound in developing innovative financing models, fostering local manufacturing, and leveraging Indonesia's rich natural resources for a diversified and resilient energy future.

Indonesia Renewable Energy Industry Segmentation

-

1. Type

-

1.1. Solar Energy

- 1.1.1. Active Energy

- 1.1.2. Passive Energy

-

1.2. Wind Energy

- 1.2.1. Offshore

- 1.2.2. Onshore

- 1.3. Hydroelectric Energy

- 1.4. Ocean Energy

- 1.5. Geothermal Energy

-

1.6. Biomass Energy

- 1.6.1. Biowaste

- 1.6.2. Biofuel

- 1.6.3. Wood

- 1.6.4. Others

-

1.1. Solar Energy

-

2. Connectivity

- 2.1. On-grid

- 2.2. Off-grid

-

3. Application

- 3.1. Heating and Cooling

- 3.2. Electricity Generation

- 3.3. Transportation

- 3.4. Others

-

4. End User

- 4.1. Residential

- 4.2. Commercial

- 4.3. Industrial

- 4.4. Utility

Indonesia Renewable Energy Industry Segmentation By Geography

- 1. Indonesia

Indonesia Renewable Energy Industry Regional Market Share

Geographic Coverage of Indonesia Renewable Energy Industry

Indonesia Renewable Energy Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Solar Energy

- 5.1.1.1. Active Energy

- 5.1.1.2. Passive Energy

- 5.1.2. Wind Energy

- 5.1.2.1. Offshore

- 5.1.2.2. Onshore

- 5.1.3. Hydroelectric Energy

- 5.1.4. Ocean Energy

- 5.1.5. Geothermal Energy

- 5.1.6. Biomass Energy

- 5.1.6.1. Biowaste

- 5.1.6.2. Biofuel

- 5.1.6.3. Wood

- 5.1.6.4. Others

- 5.1.1. Solar Energy

- 5.2. Market Analysis, Insights and Forecast - by Connectivity

- 5.2.1. On-grid

- 5.2.2. Off-grid

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Heating and Cooling

- 5.3.2. Electricity Generation

- 5.3.3. Transportation

- 5.3.4. Others

- 5.4. Market Analysis, Insights and Forecast - by End User

- 5.4.1. Residential

- 5.4.2. Commercial

- 5.4.3. Industrial

- 5.4.4. Utility

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. Indonesia

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Indonesia Renewable Energy Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Solar Energy

- 6.1.1.1. Active Energy

- 6.1.1.2. Passive Energy

- 6.1.2. Wind Energy

- 6.1.2.1. Offshore

- 6.1.2.2. Onshore

- 6.1.3. Hydroelectric Energy

- 6.1.4. Ocean Energy

- 6.1.5. Geothermal Energy

- 6.1.6. Biomass Energy

- 6.1.6.1. Biowaste

- 6.1.6.2. Biofuel

- 6.1.6.3. Wood

- 6.1.6.4. Others

- 6.1.1. Solar Energy

- 6.2. Market Analysis, Insights and Forecast - by Connectivity

- 6.2.1. On-grid

- 6.2.2. Off-grid

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Heating and Cooling

- 6.3.2. Electricity Generation

- 6.3.3. Transportation

- 6.3.4. Others

- 6.4. Market Analysis, Insights and Forecast - by End User

- 6.4.1. Residential

- 6.4.2. Commercial

- 6.4.3. Industrial

- 6.4.4. Utility

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 PLN Renewables

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Pertamina Geothermal Energy

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Star Energy Geothermal

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Medco Power Indonesia

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Canadian Solar Inc.

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Trina Solar Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 PT Sumber Energi Sukses Makmur

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 PT Barito Renewables Energy Tbk

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 SEG Solar

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 PT ATW Solar Indonesia

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Fourth Partner Energy Pvt Ltd

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Xurya Daya Indonesia

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 TotalEnergies ENEOS

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 ACWA Power

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 Masdar

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.16 Northstar PLTS

- 7.1.16.1. Company Overview

- 7.1.16.2. Products

- 7.1.16.3. Company Financials

- 7.1.16.4. SWOT Analysis

- 7.1.17 Bright PLN Batam

- 7.1.17.1. Company Overview

- 7.1.17.2. Products

- 7.1.17.3. Company Financials

- 7.1.17.4. SWOT Analysis

- 7.1.18 Others

- 7.1.18.1. Company Overview

- 7.1.18.2. Products

- 7.1.18.3. Company Financials

- 7.1.18.4. SWOT Analysis

- 7.1.1 PLN Renewables

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Indonesia Renewable Energy Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Indonesia Renewable Energy Industry Share (%) by Company 2025

List of Tables

- Table 1: Indonesia Renewable Energy Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Indonesia Renewable Energy Industry Volume gigawatt Forecast, by Type 2020 & 2033

- Table 3: Indonesia Renewable Energy Industry Revenue billion Forecast, by Connectivity 2020 & 2033

- Table 4: Indonesia Renewable Energy Industry Volume gigawatt Forecast, by Connectivity 2020 & 2033

- Table 5: Indonesia Renewable Energy Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 6: Indonesia Renewable Energy Industry Volume gigawatt Forecast, by Application 2020 & 2033

- Table 7: Indonesia Renewable Energy Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 8: Indonesia Renewable Energy Industry Volume gigawatt Forecast, by End User 2020 & 2033

- Table 9: Indonesia Renewable Energy Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 10: Indonesia Renewable Energy Industry Volume gigawatt Forecast, by Region 2020 & 2033

- Table 11: Indonesia Renewable Energy Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Indonesia Renewable Energy Industry Volume gigawatt Forecast, by Type 2020 & 2033

- Table 13: Indonesia Renewable Energy Industry Revenue billion Forecast, by Connectivity 2020 & 2033

- Table 14: Indonesia Renewable Energy Industry Volume gigawatt Forecast, by Connectivity 2020 & 2033

- Table 15: Indonesia Renewable Energy Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 16: Indonesia Renewable Energy Industry Volume gigawatt Forecast, by Application 2020 & 2033

- Table 17: Indonesia Renewable Energy Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 18: Indonesia Renewable Energy Industry Volume gigawatt Forecast, by End User 2020 & 2033

- Table 19: Indonesia Renewable Energy Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 20: Indonesia Renewable Energy Industry Volume gigawatt Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Indonesia Renewable Energy Industry?

The projected CAGR is approximately 15.2%.

2. Which companies are prominent players in the Indonesia Renewable Energy Industry?

Key companies in the market include PLN Renewables, Pertamina Geothermal Energy, Star Energy Geothermal, Medco Power Indonesia, Canadian Solar Inc., Trina Solar Ltd, PT Sumber Energi Sukses Makmur, PT Barito Renewables Energy Tbk, SEG Solar, PT ATW Solar Indonesia, Fourth Partner Energy Pvt Ltd, Xurya Daya Indonesia, TotalEnergies ENEOS, ACWA Power, Masdar, Northstar PLTS, Bright PLN Batam, Others.

3. What are the main segments of the Indonesia Renewable Energy Industry?

The market segments include Type, Connectivity, Application, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 63.21 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Immense Potential in Renewable sector due to Natural Landscape of the country4.; Supportive Government Policies and Initiatives.

6. What are the notable trends driving market growth?

Solar Energy Is Expected to Witness Significant Growth.

7. Are there any restraints impacting market growth?

4.; Rising Adoption of Alternate Clean Power Sources.

8. Can you provide examples of recent developments in the market?

June 2023: SEG Solar (SEG) and PT Kawasan Industri Terpadu Batang (KITB) have announced they have entered into a binding agreement for the lease of approximately 41 hectares of land located in the Batang Regency, Central Java, Indonesia. Through PT SEG ATW Solar Manufaktur Indonesia, a joint-venture project company, SEG intends to invest USD 500 million in developing the land to construct a 5GW solar cell manufacturing facility and a 3GW solar module manufacturing facility. To assist with developing local facilities in Indonesia, SEG has partnered with PT ATW Investasi Selaras (ATW Group).

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in gigawatt.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Indonesia Renewable Energy Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Indonesia Renewable Energy Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Indonesia Renewable Energy Industry?

To stay informed about further developments, trends, and reports in the Indonesia Renewable Energy Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence