Key Insights

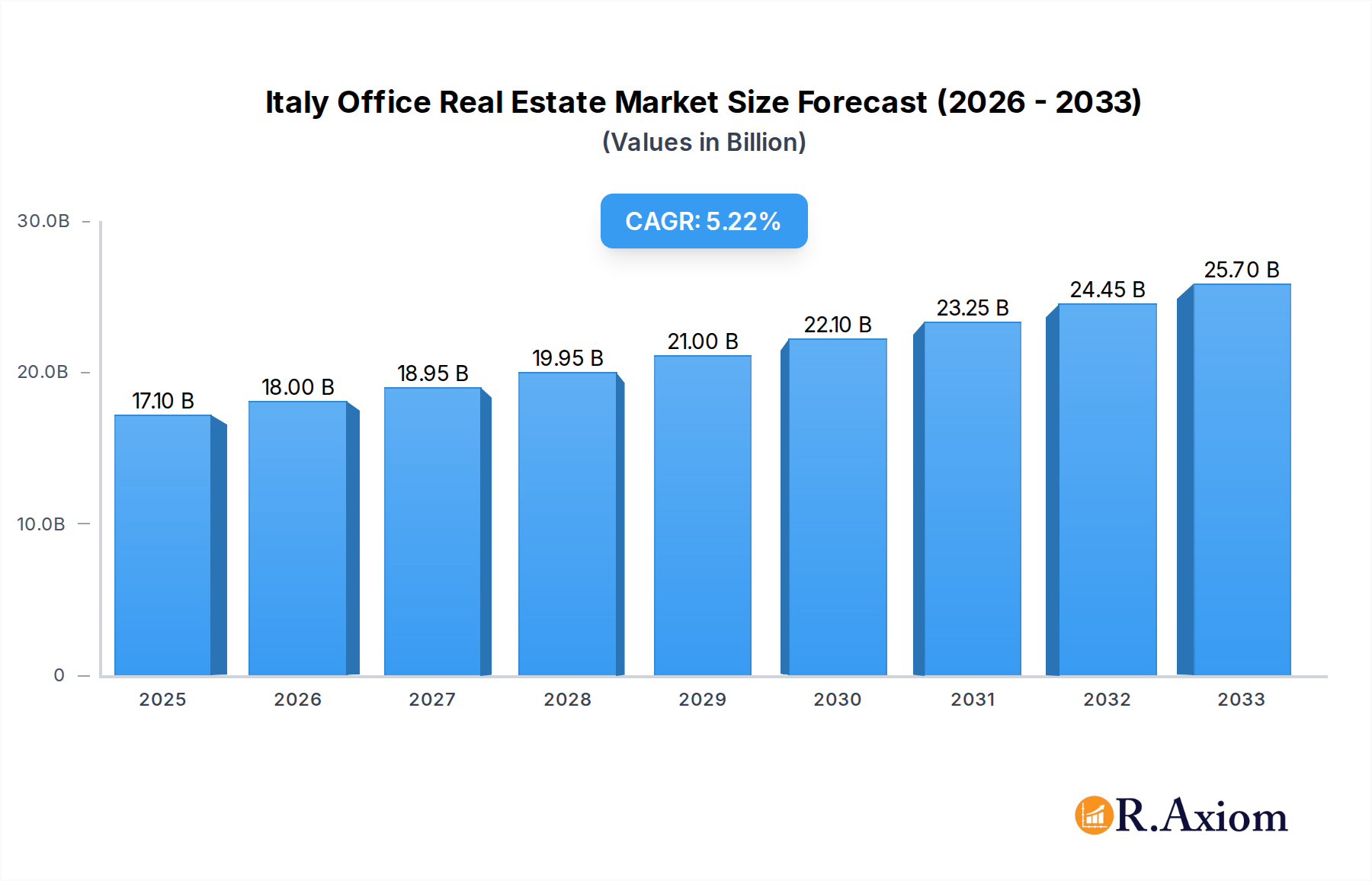

The Italy office real estate market is poised for significant expansion, projected to reach a market size of €17.1 billion in 2025, with a robust Compound Annual Growth Rate (CAGR) of 5.29% through 2033. This growth trajectory is fueled by a confluence of dynamic factors, primarily driven by increased demand for modern, flexible, and sustainable office spaces. Businesses are actively seeking environments that foster collaboration, innovation, and employee well-being, leading to a surge in demand for prime office locations in key cities such as Rome and Milan. The ongoing evolution of hybrid work models also plays a crucial role, as companies re-evaluate their spatial needs, opting for high-quality, centrally located offices that can serve as hubs for in-person interaction and strategic planning. Furthermore, significant infrastructure investments and urban regeneration projects across major Italian cities are enhancing the attractiveness and accessibility of office portfolios, creating a favorable environment for market expansion.

Italy Office Real Estate Market Market Size (In Billion)

The market's upward momentum is further supported by emerging trends such as the increasing adoption of smart building technologies, a focus on environmental, social, and governance (ESG) principles in property development, and the growing appeal of co-working and flexible office solutions. These trends are not only shaping the demand for office spaces but also influencing investment strategies and property management practices. While the market benefits from strong growth drivers, potential restraints such as fluctuating economic conditions and evolving regulatory frameworks require careful consideration. However, the underlying demand for quality office real estate, coupled with strategic investments and a commitment to sustainability, positions the Italy office real estate market for sustained and healthy growth throughout the forecast period. Major players like Impresa Pizzarotti, Webuild, and CBRE Italy are actively navigating these dynamics, contributing to the market's vibrant evolution.

Italy Office Real Estate Market Company Market Share

This in-depth report provides an exhaustive analysis of the Italy office real estate market, offering critical insights into its dynamics, trends, and future trajectory. Covering the period from 2019 to 2033, with a base and estimated year of 2025, this report is an essential resource for investors, developers, and industry stakeholders seeking to understand and capitalize on opportunities within one of Europe's key property markets. We delve into market concentration, innovation, dominant segments, product developments, key growth drivers, prevailing challenges, and emerging opportunities, all while providing a strategic outlook. The report features detailed segmentation by key cities including Rome, Milan, Naples, and Turin, alongside an analysis of 'Other Cities.' With a focus on high-impact keywords such as "Italian office space," "commercial property Italy," "Milan real estate," "Rome office market," and "real estate investment Italy," this report is meticulously crafted for maximum search visibility and engagement.

Italy Office Real Estate Market Market Concentration & Innovation

The Italian office real estate market exhibits a moderate level of concentration, with a few major international and domestic players holding significant market share. Innovation is increasingly driven by demand for flexible workspaces, sustainable building practices, and integrated technology solutions. Regulatory frameworks, while sometimes complex, are evolving to support modern development and investment. Product substitutes, such as co-working spaces and remote work policies, are influencing traditional office demand. End-user trends point towards a growing preference for amenity-rich, well-connected, and health-conscious office environments. Mergers and acquisitions (M&A) activity, valued in the billions, are a key indicator of market dynamism and consolidation. For instance, ongoing M&A activities reflect strategic consolidation and expansion by leading firms aiming to bolster their presence and service offerings across the Italian landscape. The market share distribution, while fluid, is influenced by successful project developments and strategic portfolio acquisitions.

Italy Office Real Estate Market Industry Trends & Insights

The Italian office real estate market is experiencing robust growth, driven by a confluence of economic recovery, foreign investment, and evolving workplace strategies. The Compound Annual Growth Rate (CAGR) is projected to be substantial, reflecting increasing demand for high-quality, modern office spaces in prime locations. Technological disruptions are playing a pivotal role, with the adoption of smart building technologies, AI-driven property management, and enhanced digital connectivity becoming standard expectations. Consumer preferences are shifting significantly, with tenants prioritizing flexible lease terms, sustainability credentials (ESG compliance), and a focus on employee well-being, including access to natural light, green spaces, and comprehensive amenities. Competitive dynamics are intensifying, with both established global real estate giants and agile local developers vying for prime assets and development opportunities. Market penetration of new office formats, such as flexible and hybrid work solutions, is expanding rapidly, reshaping leasing strategies and space utilization. The market's resilience is further underscored by its ability to adapt to global economic shifts, with a consistent influx of investment seeking attractive yields and long-term capital appreciation.

Dominant Markets & Segments in Italy Office Real Estate Market

Milan stands out as the unequivocally dominant market within the Italian office real estate sector. Its robust economy, status as a global financial and fashion hub, and strong international connectivity make it a magnet for corporate occupiers and investors alike.

- Economic Policies and Infrastructure: Milan benefits from favorable economic policies that encourage foreign investment and business expansion. Its world-class infrastructure, including major international airports, high-speed rail networks, and an extensive public transportation system, ensures seamless connectivity for businesses and their employees.

- Innovation and Talent Pool: The city is a hub for innovation and boasts a highly skilled talent pool, attracting multinational corporations and start-ups. This demand fuels the need for modern, high-quality office spaces that can accommodate diverse business needs.

- Foreign Direct Investment: Milan consistently attracts significant foreign direct investment into its commercial real estate sector, bolstering demand and driving up property values.

Rome, while historically significant, also presents a strong and stable office market, driven by its role as the capital city and a major administrative and tourism center. The presence of governmental institutions and international organizations ensures a steady demand for office space.

Naples and Turin are emerging as secondary markets with significant growth potential, fueled by targeted urban regeneration initiatives, growing tech sectors, and competitive rental rates compared to prime Milanese locations. These cities offer opportunities for businesses seeking to expand their reach at a more accessible cost base.

Other Cities across Italy present a mosaic of opportunities, with regional economic hubs and university towns showing increasing demand for office spaces, particularly for specialized industries and R&D facilities. The overall dominance of Milan is undeniable, but strategic investments in these secondary and tertiary markets are becoming increasingly prevalent, driven by diversification strategies and a search for value.

Italy Office Real Estate Market Product Developments

Product developments in the Italy office real estate market are increasingly focused on creating intelligent, sustainable, and human-centric workspaces. Innovations include the integration of IoT technology for smart building management, optimizing energy consumption and occupant comfort. Flexible office layouts, modular furniture, and adaptable spaces are becoming commonplace to accommodate hybrid work models. Biophilic design principles, incorporating natural elements and abundant natural light, are gaining traction to enhance employee well-being. Competitive advantages are being derived from offering a superior occupier experience, robust ESG credentials, and advanced technological integration, making properties more attractive to discerning tenants and investors in a competitive landscape.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the Italy office real estate market segmented by key cities: Rome, Milan, Naples, and Turin, alongside a broad category for 'Other Cities'.

- Milan: Expected to exhibit the highest market size and growth projections due to its status as a primary financial and commercial hub, attracting substantial foreign investment and a high concentration of multinational corporations. Competitive dynamics are intense, with a premium placed on Grade A office spaces.

- Rome: Demonstrates steady market size and growth, driven by its administrative importance and a consistent demand from government-related entities and international organizations. The market is characterized by a blend of historic and modern office stock.

- Naples: Projected to see significant growth in market size and penetration, fueled by urban regeneration projects and an expanding tech and service sector. Its competitive advantage lies in more accessible rental prices and growing opportunities for specialized office spaces.

- Turin: Exhibits moderate market size with promising growth potential, particularly in sectors like automotive and advanced manufacturing. Urban renewal efforts are enhancing its appeal for businesses seeking cost-effective yet strategic locations.

- Other Cities: Represents a diverse segment with varying market sizes and growth trajectories, influenced by local economic drivers, university presence, and specialized industry clusters. This segment offers niche opportunities for specialized office requirements.

Key Drivers of Italy Office Real Estate Market Growth

The growth of the Italy office real estate market is propelled by several key drivers. Economic recovery and sustained GDP growth across the Eurozone provide a stable foundation for increased business activity and office space demand. Significant foreign direct investment continues to flow into the Italian market, particularly into prime office assets in major cities, seeking attractive yields and capital appreciation. Technological advancements are reshaping the office landscape, with a growing demand for smart, connected, and sustainable buildings that enhance productivity and well-being. Evolving workplace strategies, including the adoption of hybrid work models, are creating demand for more flexible, amenity-rich, and collaborative office environments. Favorable regulatory frameworks and government incentives aimed at promoting urban regeneration and sustainable development further stimulate investment and construction activity, contributing to a dynamic and expanding market.

Challenges in the Italy Office Real Estate Market Sector

Despite robust growth, the Italy office real estate market faces several challenges. Navigating complex and sometimes bureaucratic regulatory frameworks can create delays and increase development costs. Supply chain disruptions and rising construction material costs can impact project timelines and profitability. Intense competition among developers and landlords for prime assets and desirable tenants can lead to pricing pressures. The ongoing transition to hybrid work models presents a challenge in fully understanding and meeting evolving tenant requirements for space optimization and flexibility. Furthermore, economic uncertainties, both domestic and global, can influence investment sentiment and leasing activity, posing a risk to market stability and growth projections.

Emerging Opportunities in Italy Office Real Estate Market

Emerging opportunities within the Italy office real estate market are abundant and diverse. The increasing focus on Environmental, Social, and Governance (ESG) principles presents a significant opportunity for developers and investors who can deliver certified sustainable buildings, meeting growing tenant and investor demand for green credentials. The rise of flexible and hybrid work models is creating demand for co-working spaces, serviced offices, and adaptable lease structures, opening new avenues for innovative business models. Urban regeneration projects in secondary and tertiary cities offer opportunities for value creation through the development of modern office spaces in revitalized areas. Technological integration, including smart building solutions and proptech innovations, presents avenues for enhancing building efficiency, tenant experience, and operational management, driving competitive advantage.

Leading Players in the Italy Office Real Estate Market Market

- Impresa Pizzarotti

- Engel & Volkers Commercial

- Webuild

- CBRE Italy

- Knight Frank

- Rizzani de Eccher

- Savills plc

- Astaldi

- JLL Italy

Key Developments in Italy Office Real Estate Market Industry

- November 2022: Macquarie Asset Management acquired a major Milan office building for approximately EUR 119 million (USD 126 Million). This acquisition highlights Milan's strong appeal as a gateway city for high-quality real estate with robust demand.

- February 2022: BC Partners European Real Estate I (BCPERE I) and Kervis Group finalized the acquisition of an office building in Milan's Piazza Trento, Porta Romana, from Europ Assistance Italy. This transaction underscored confidence in the stability of the Milanese office and residential markets.

Strategic Outlook for Italy Office Real Estate Market Market

The strategic outlook for the Italy office real estate market is overwhelmingly positive, driven by sustained economic recovery, increasing foreign investment, and a fundamental shift towards more flexible and sustainable workplace solutions. The market is poised for continued growth, particularly in prime locations like Milan, with a strong emphasis on ESG-compliant and technologically advanced properties. Opportunities abound for developers and investors who can adapt to evolving tenant demands for amenity-rich, adaptable, and health-conscious office environments. Strategic investments in urban regeneration and secondary cities are expected to gain momentum, offering diversification and attractive yield potential. The market's resilience and capacity for innovation position it as a compelling destination for real estate capital seeking long-term value and returns.

Italy Office Real Estate Market Segmentation

-

1. Key Cities

- 1.1. Rome

- 1.2. Milan

- 1.3. Naples

- 1.4. Turin

- 1.5. Other Cities

Italy Office Real Estate Market Segmentation By Geography

- 1. Italy

Italy Office Real Estate Market Regional Market Share

Geographic Coverage of Italy Office Real Estate Market

Italy Office Real Estate Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.29% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Key Cities

- 5.1.1. Rome

- 5.1.2. Milan

- 5.1.3. Naples

- 5.1.4. Turin

- 5.1.5. Other Cities

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Italy

- 5.1. Market Analysis, Insights and Forecast - by Key Cities

- 6. Italy Office Real Estate Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Key Cities

- 6.1.1. Rome

- 6.1.2. Milan

- 6.1.3. Naples

- 6.1.4. Turin

- 6.1.5. Other Cities

- 6.1. Market Analysis, Insights and Forecast - by Key Cities

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Impresa Pizzarotti

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Engel & Volkers Commercial

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Webuild

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 CBRE Italy

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Knight Frank

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Rizzani de Eccher

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Savills plc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Astaldi

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 JLL Italy

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Impresa Pizzarotti

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Italy Office Real Estate Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Italy Office Real Estate Market Share (%) by Company 2025

List of Tables

- Table 1: Italy Office Real Estate Market Revenue billion Forecast, by Key Cities 2020 & 2033

- Table 2: Italy Office Real Estate Market Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Italy Office Real Estate Market Revenue billion Forecast, by Key Cities 2020 & 2033

- Table 4: Italy Office Real Estate Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Italy Office Real Estate Market?

The projected CAGR is approximately 5.29%.

2. Which companies are prominent players in the Italy Office Real Estate Market?

Key companies in the market include Impresa Pizzarotti, Engel & Volkers Commercial, Webuild, CBRE Italy, Knight Frank, Rizzani de Eccher, Savills plc, Astaldi, JLL Italy.

3. What are the main segments of the Italy Office Real Estate Market?

The market segments include Key Cities.

4. Can you provide details about the market size?

The market size is estimated to be USD 17.1 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing geriatric population; Growing cases of chronic disease among senior citizens.

6. What are the notable trends driving market growth?

Occupier and Investment Focus in Milan.

7. Are there any restraints impacting market growth?

High cost of elderly care services; Lack of skilled staff.

8. Can you provide examples of recent developments in the market?

November 2022 - A major Milan office building was purchased by Macquarie Asset Management through an Italian real estate fund for roughly EUR 119 million (USD 126 Million). It has been an active participant in the Italian real estate market for a number of years, and it has now added this historic house to its portfolio of properties in the region. One of the most desirable gateway cities in Europe is Milan, with many opportunities to find higher-quality apartments with strong demand.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Italy Office Real Estate Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Italy Office Real Estate Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Italy Office Real Estate Market?

To stay informed about further developments, trends, and reports in the Italy Office Real Estate Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence