Key Insights

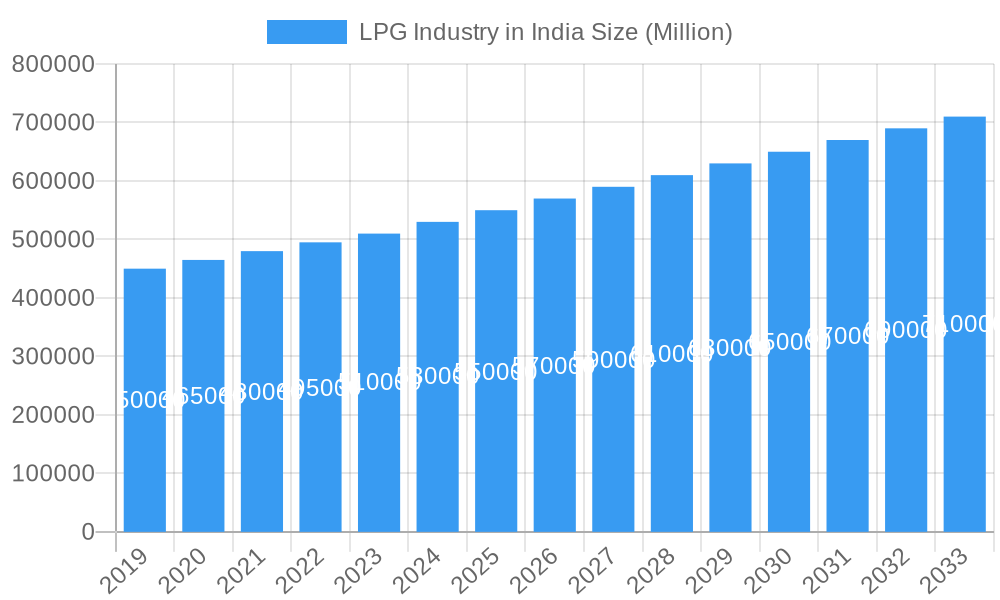

The Indian Liquefied Petroleum Gas (LPG) market is projected for significant growth, anticipating a market size of $136.548 billion by 2025, with a Compound Annual Growth Rate (CAGR) of 4.71% from 2025 to 2033. Key growth drivers include government initiatives like Pradhan Mantri Ujjwala Yojana (PMUY), which have substantially increased LPG adoption in the residential sector for clean cooking fuel. Growing industrialization and the increasing use of LPG as an environmentally friendly alternative to traditional fuels in commercial and industrial applications, including autogas, are also major contributors. Rising disposable incomes and greater consumer awareness of LPG's health and environmental benefits further support this positive trajectory.

LPG Industry in India Market Size (In Billion)

Market dynamics are shaped by the expanding autogas sector, driven by global efforts to reduce vehicular emissions. Technological advancements in LPG infrastructure and increased competition from established and new market players are also influencing the landscape. Potential market restraints include the volatility of global crude oil prices, which affect LPG procurement costs, and logistical challenges in last-mile delivery, particularly in remote areas. Despite these factors, robust residential demand and expanding applications in industrial and autogas sectors ensure a favorable outlook. The market is segmented by production source (Crude Oil, Natural Gas Liquids) and application (Residential & Commercial, Industrial, Autofuels, Others), with the residential segment leading. Key industry players, including Indian Oil Corporation Ltd., Bharat Petroleum Corporation Limited, and Hindustan Petroleum Corporation Limited, are instrumental in driving innovation and market expansion.

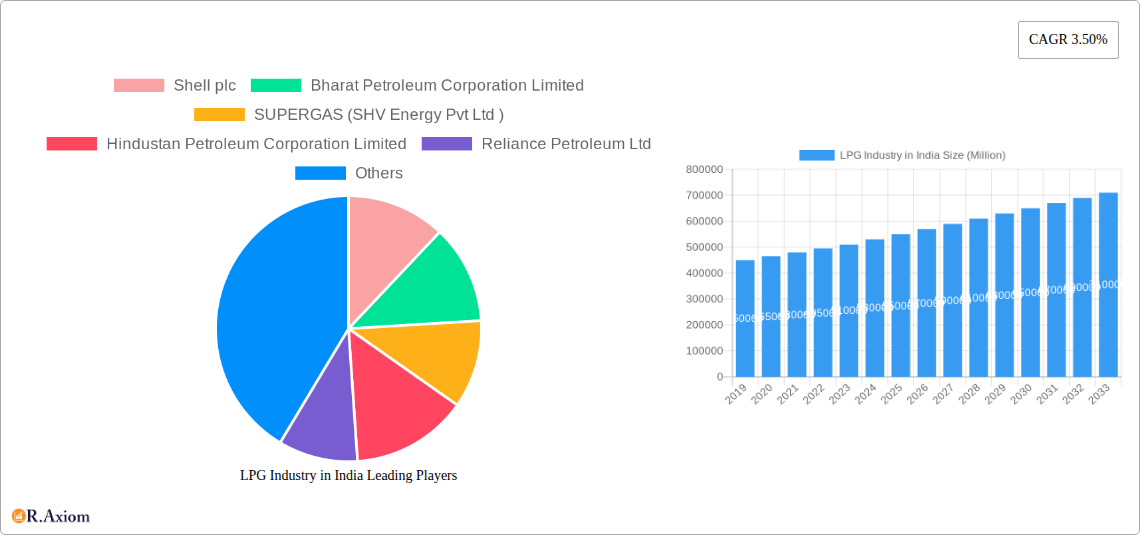

LPG Industry in India Company Market Share

India LPG Industry Market Analysis 2023-2033: Growth, Trends, and Opportunities

This comprehensive report offers an in-depth analysis of the Indian Liquefied Petroleum Gas (LPG) industry, covering the period from 2019 to 2033, with a base and estimated year of 2025. It provides crucial insights into market concentration, innovation, industry trends, dominant segments, product developments, and key growth drivers, challenges, and emerging opportunities. Essential for industry stakeholders, policymakers, investors, and market participants, this report leverages high-traffic keywords to enhance search visibility and deliver actionable intelligence.

LPG Industry in India Market Concentration & Innovation

The Indian LPG market exhibits a moderate to high concentration, with a few dominant public sector undertakings (PSUs) and private players controlling a significant market share. Indian Oil Corporation Ltd. commands a substantial share, followed closely by Bharat Petroleum Corporation Limited and Hindustan Petroleum Corporation Limited. Shell plc and TotalEnergies SE are also key international players with growing footprints. Innovation in the sector is primarily driven by technological advancements in storage and distribution, focus on enhanced safety features, and the development of cleaner, more efficient LPG-based appliances. Regulatory frameworks, primarily steered by the Ministry of Petroleum and Natural Gas, are crucial in shaping market dynamics, with initiatives like Pradhan Mantri Ujjwala Yojana (PMUY) significantly boosting adoption. Product substitutes, such as piped natural gas (PNG) and electricity, pose a competitive challenge, especially in urban centers. However, the widespread infrastructure and affordability of LPG ensure its continued dominance in many regions. End-user trends indicate a growing preference for cleaner cooking fuels, driving demand for LPG. Merger and acquisition (M&A) activities are relatively limited but are expected to increase as companies seek to consolidate their market position and expand their geographical reach. For instance, SUPERGAS (SHV Energy Pvt Ltd) has been active in strategic expansions and partnerships.

LPG Industry in India Industry Trends & Insights

The Indian LPG industry is poised for robust growth, driven by a confluence of factors including government initiatives, rising disposable incomes, and increasing urbanization. The market is expected to witness a Compound Annual Growth Rate (CAGR) of approximately 8-10% during the forecast period. The Pradhan Mantri Ujjwala Yojana (PMUY) has been a transformative force, significantly increasing LPG penetration in rural and underserved households, pushing market penetration rates towards 95% and beyond. Technological disruptions are primarily focused on enhancing the supply chain efficiency through advanced tracking and logistics, improved cylinder safety, and the adoption of smart metering technologies. The increasing adoption of LPG as a cleaner alternative to traditional biomass fuels is a significant trend, contributing to improved public health and environmental sustainability. Consumer preferences are shifting towards convenience and safety, leading to greater demand for services that offer hassle-free refills and reliable supply. Competitive dynamics are intensifying, with PSUs leveraging their vast distribution networks and private players focusing on premium services and specialized offerings. The 'Make in India' initiative is also spurring domestic manufacturing of LPG cylinders and related equipment, further strengthening the industry's value chain. The ongoing expansion of natural gas infrastructure, while a substitute in some applications, also presents opportunities for integrated energy solutions, where LPG can play a complementary role.

Dominant Markets & Segments in LPG Industry in India

The Residential & Commercial segment is the undisputed leader in the Indian LPG market, driven by its widespread adoption as a primary cooking fuel across urban and rural households. The government's sustained push through schemes like PMUY has been instrumental in its dominance, making LPG accessible to millions. Economic policies aimed at promoting cleaner energy and improving living standards directly fuel the demand in this segment. Infrastructure development, particularly the expansion of the LPG cylinder distribution network and the establishment of bottling plants, further solidifies its leading position.

The Industrial segment, while smaller than residential, presents significant growth potential. Industries ranging from hospitality and food processing to small-scale manufacturing rely on LPG for their energy needs due to its portability and relative cleanliness compared to other fuels. Infrastructure supporting industrial gas supply, though still developing, is a key driver.

Autofuels is an emerging and rapidly growing segment. The increasing adoption of LPG-fueled vehicles, driven by lower running costs and stricter emission norms, is a key trend. Government incentives for converting vehicles to LPG and the establishment of dedicated refueling stations are crucial economic policies supporting this segment's growth. The availability of efficient and safe LPG conversion kits is also a vital aspect of infrastructure development.

Other Applications, which include LPG use in sectors like agriculture (e.g., crop drying) and as a feedstock in certain chemical processes, contribute a smaller but consistent share to the overall market. The growth in this segment is often linked to advancements in specialized industrial processes and the availability of customized LPG solutions.

LPG Industry in India Product Developments

Product developments in the Indian LPG sector are primarily focused on enhancing user experience, safety, and efficiency. Innovations include the introduction of lighter and more robust composite LPG cylinders, offering enhanced safety and portability. Smart LPG stoves with improved thermal efficiency and advanced safety cut-off mechanisms are gaining traction. Furthermore, the development of integrated systems for seamless LPG refilling and automated distribution tracking through IoT technology is enhancing operational efficiency and customer convenience. Companies are also exploring advancements in LPG blending with other gases to optimize performance for specific industrial applications, thereby enhancing their competitive advantage.

LPG Industry in India Report Scope & Segmentation Analysis

This report segments the Indian LPG market based on the Source of Production and Application. The Source of Production includes Crude Oil and Natural Gas Liquids (NGLs), with NGLs being a primary contributor to domestic LPG production. For Applications, the market is segmented into Residential & Commercial, Industrial, Autofuels, and Other Applications. The Residential & Commercial segment currently holds the largest market share and is projected to maintain its dominance, driven by ongoing government initiatives to achieve universal LPG access. The Industrial segment is expected to exhibit steady growth due to increasing industrialization. Autofuels represent a rapidly expanding segment with significant growth projections due to favorable economics and environmental regulations. Other Applications offer niche growth opportunities tied to specific industrial and agricultural needs.

Key Drivers of LPG Industry in India Growth

The growth of the LPG industry in India is primarily propelled by strong government support, most notably through the Pradhan Mantri Ujjwala Yojana (PMUY), which aims to provide clean cooking fuel to rural and poor households. This initiative has significantly expanded market penetration. Rising disposable incomes and a growing middle class are increasing the affordability and demand for LPG. Urbanization also plays a crucial role, as densely populated areas benefit from efficient distribution networks. Furthermore, the recognition of LPG as a cleaner and more efficient alternative to traditional biomass fuels is a significant driver for both environmental and public health reasons. Technological advancements in storage, distribution, and appliance efficiency are also contributing to market expansion.

Challenges in the LPG Industry in India Sector

Despite its robust growth, the Indian LPG sector faces several challenges. The extensive geographical spread of India and the last-mile delivery hurdles in remote rural areas present significant logistical complexities. Fluctuations in global crude oil prices, which influence LPG import costs, can impact pricing and affordability. Regulatory compliance and the need for continuous upgrades in safety standards require substantial investment. Competition from alternative energy sources like piped natural gas (PNG) and electricity, especially in urban areas, poses a threat. Moreover, ensuring the consistent availability of high-quality cylinders and maintaining robust supply chains to meet the ever-increasing demand remain ongoing challenges for industry players.

Emerging Opportunities in LPG Industry in India

The Indian LPG industry is ripe with emerging opportunities. The untapped potential in remote and northeastern regions offers a significant avenue for market expansion. The growing demand for LPG as an automotive fuel presents a substantial opportunity with the potential for widespread adoption of LPG-powered vehicles. Innovations in smart LPG cylinders, IoT-enabled distribution networks, and advanced safety features offer opportunities for product differentiation and enhanced service offerings. Furthermore, the increasing focus on sustainability and cleaner energy solutions creates a fertile ground for the development and promotion of advanced LPG-powered industrial applications and blended fuels. Exploring opportunities in the petrochemical sector where LPG can be used as a feedstock also presents a promising avenue.

Leading Players in the LPG Industry in India Market

- Indian Oil Corporation Ltd

- Bharat Petroleum Corporation Limited

- Hindustan Petroleum Corporation Limited

- Shell plc

- SUPERGAS (SHV Energy Pvt Ltd)

- TotalEnergies SE

- Reliance Petroleum Ltd

- Eastern Gases Lt

- Jyothi Gas Pvt Ltd

Key Developments in LPG Industry in India Industry

- February 2022: Indian Oil Corp (IOC) announced plans to construct three new plants in Northeast India to increase its LPG bottling capacity by nearly 53% or to 8 crore cylinders annually by 2030, to meet the growing demand in the region. The total investment in the plant expansion is likely to range between INR 325-350 crore.

- Ongoing: Continuous expansion of Pradhan Mantri Ujjwala Yojana (PMUY) to cover more beneficiaries and increase LPG penetration in rural and underserved areas.

- 2023-2024: Increasing focus on digital transformation in LPG distribution, with companies investing in apps for booking refills, tracking deliveries, and customer service.

- Ongoing: Growing interest and investment in composite LPG cylinders for enhanced safety and lighter weight.

Strategic Outlook for LPG Industry in India Market

The strategic outlook for the Indian LPG industry remains highly optimistic, driven by a strong demographic advantage, sustained government support, and a growing awareness of cleaner energy benefits. The continued expansion of the PMUY scheme will ensure sustained demand growth in the residential sector. The burgeoning automotive sector presents a significant opportunity for LPG to capture a larger share of the fuel market. Investments in advanced logistics, smart technologies, and improved safety features will be crucial for maintaining a competitive edge and meeting evolving consumer expectations. Furthermore, the industry is well-positioned to leverage opportunities in industrial applications and explore innovative solutions that align with India's broader energy transition goals, ensuring continued relevance and growth.

LPG Industry in India Segmentation

-

1. Source of Production

- 1.1. Crude Oil

- 1.2. Natural Gas Liquids

-

2. Application

- 2.1. Residential & Commercial

- 2.2. Industrial

- 2.3. Autofuels

- 2.4. Other Applications

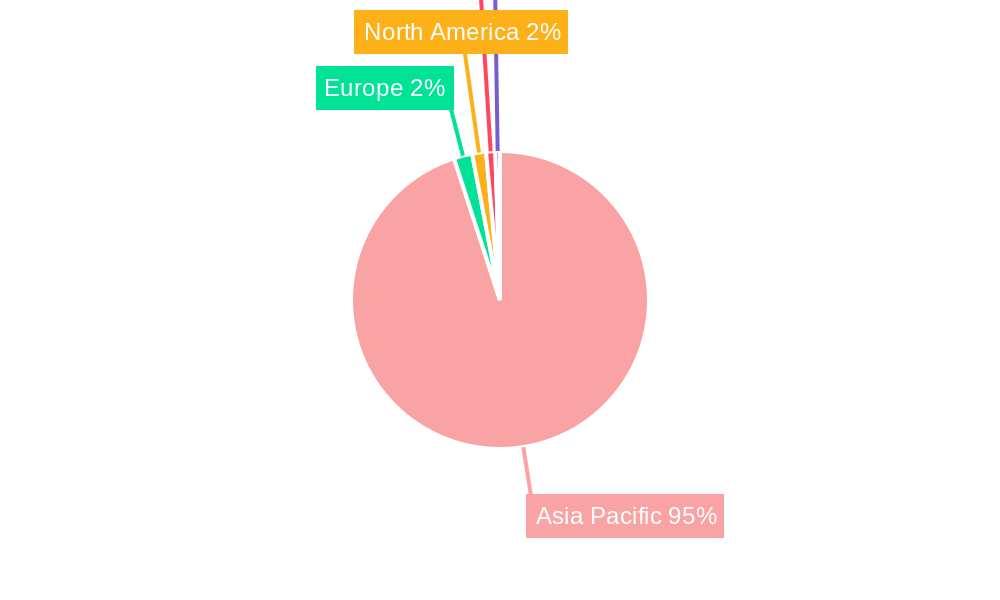

LPG Industry in India Segmentation By Geography

-

1. Asia Pacific

- 1.1. India

LPG Industry in India Regional Market Share

Geographic Coverage of LPG Industry in India

LPG Industry in India REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.71% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Source of Production

- 5.1.1. Crude Oil

- 5.1.2. Natural Gas Liquids

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Residential & Commercial

- 5.2.2. Industrial

- 5.2.3. Autofuels

- 5.2.4. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Source of Production

- 6. Global LPG Industry in India Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Source of Production

- 6.1.1. Crude Oil

- 6.1.2. Natural Gas Liquids

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Residential & Commercial

- 6.2.2. Industrial

- 6.2.3. Autofuels

- 6.2.4. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Source of Production

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Shell plc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Bharat Petroleum Corporation Limited

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 SUPERGAS (SHV Energy Pvt Ltd )

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Hindustan Petroleum Corporation Limited

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Reliance Petroleum Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 TotalEnergies SE

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Indian Oil Corporation Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Eastern Gases Lt

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Jyothi Gas Pvt Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Shell plc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Global LPG Industry in India Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Asia Pacific LPG Industry in India Revenue (billion), by Source of Production 2025 & 2033

- Figure 3: Asia Pacific LPG Industry in India Revenue Share (%), by Source of Production 2025 & 2033

- Figure 4: Asia Pacific LPG Industry in India Revenue (billion), by Application 2025 & 2033

- Figure 5: Asia Pacific LPG Industry in India Revenue Share (%), by Application 2025 & 2033

- Figure 6: Asia Pacific LPG Industry in India Revenue (billion), by Country 2025 & 2033

- Figure 7: Asia Pacific LPG Industry in India Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global LPG Industry in India Revenue billion Forecast, by Source of Production 2020 & 2033

- Table 2: Global LPG Industry in India Revenue billion Forecast, by Application 2020 & 2033

- Table 3: Global LPG Industry in India Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global LPG Industry in India Revenue billion Forecast, by Source of Production 2020 & 2033

- Table 5: Global LPG Industry in India Revenue billion Forecast, by Application 2020 & 2033

- Table 6: Global LPG Industry in India Revenue billion Forecast, by Country 2020 & 2033

- Table 7: India LPG Industry in India Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the LPG Industry in India?

The projected CAGR is approximately 4.71%.

2. Which companies are prominent players in the LPG Industry in India?

Key companies in the market include Shell plc, Bharat Petroleum Corporation Limited, SUPERGAS (SHV Energy Pvt Ltd ), Hindustan Petroleum Corporation Limited, Reliance Petroleum Ltd, TotalEnergies SE, Indian Oil Corporation Ltd, Eastern Gases Lt, Jyothi Gas Pvt Ltd.

3. What are the main segments of the LPG Industry in India?

The market segments include Source of Production, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 136.548 billion as of 2022.

5. What are some drivers contributing to market growth?

Declining Cost of Wind Energy. Increasing Investments in Wind Energy Power Generation Projects.

6. What are the notable trends driving market growth?

LPG Extracted From Natural Gas is Expected to Have Considerable Growth Rate.

7. Are there any restraints impacting market growth?

Increasing Adoption of Alternate Clean Power Sources.

8. Can you provide examples of recent developments in the market?

In February 2022, Indian Oil Corp (IOC) announced the plans to construct three new plants in Northeast India to increase its LPG bottling capacity by nearly 53% or to 8 crore cylinders annually by 2030, to meet the growing demand in the region. Furthermore, the total investment in the plant expansion is likely to range between INR 325-350 crore.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "LPG Industry in India," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the LPG Industry in India report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the LPG Industry in India?

To stay informed about further developments, trends, and reports in the LPG Industry in India, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence