Key Insights

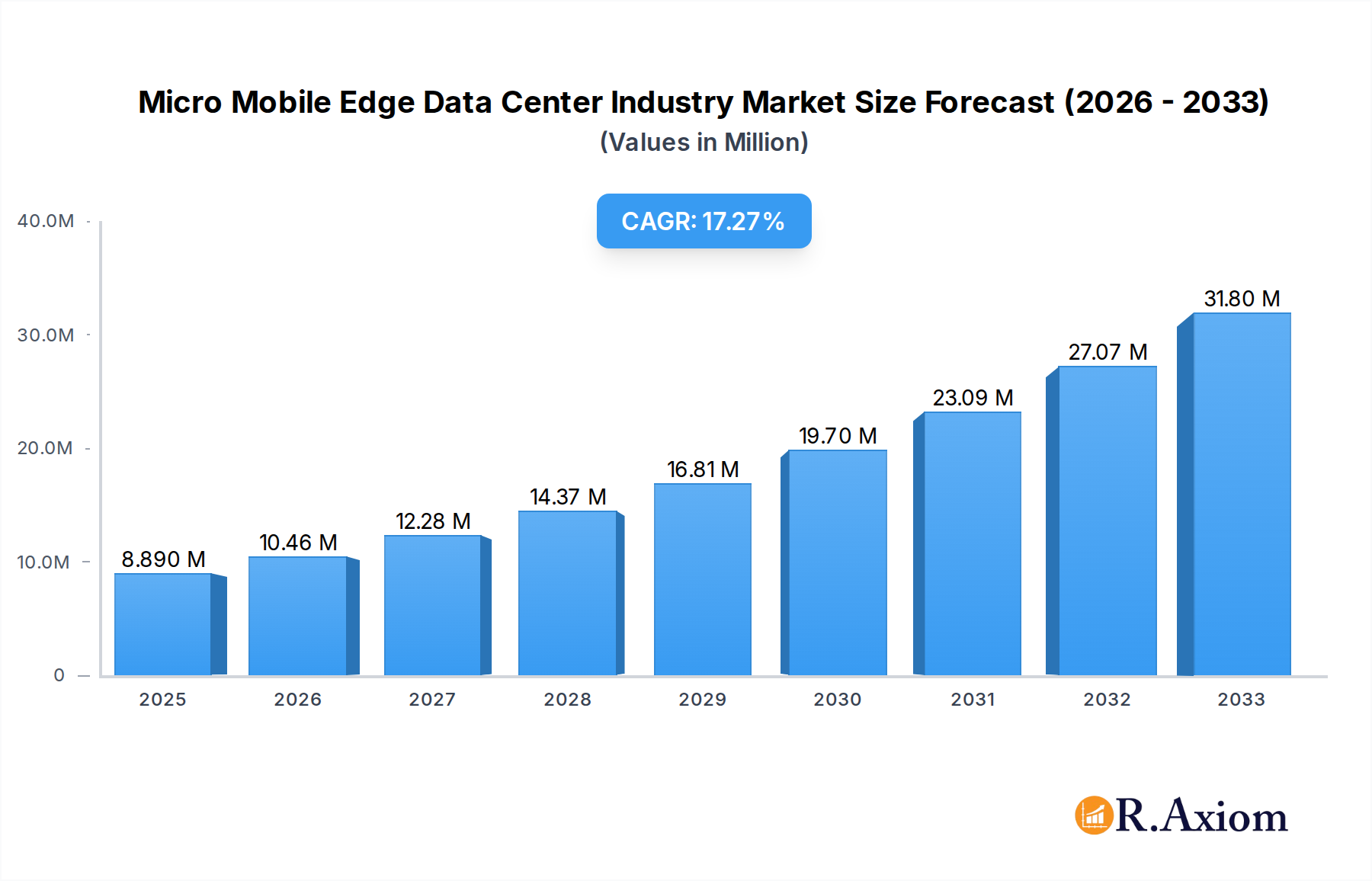

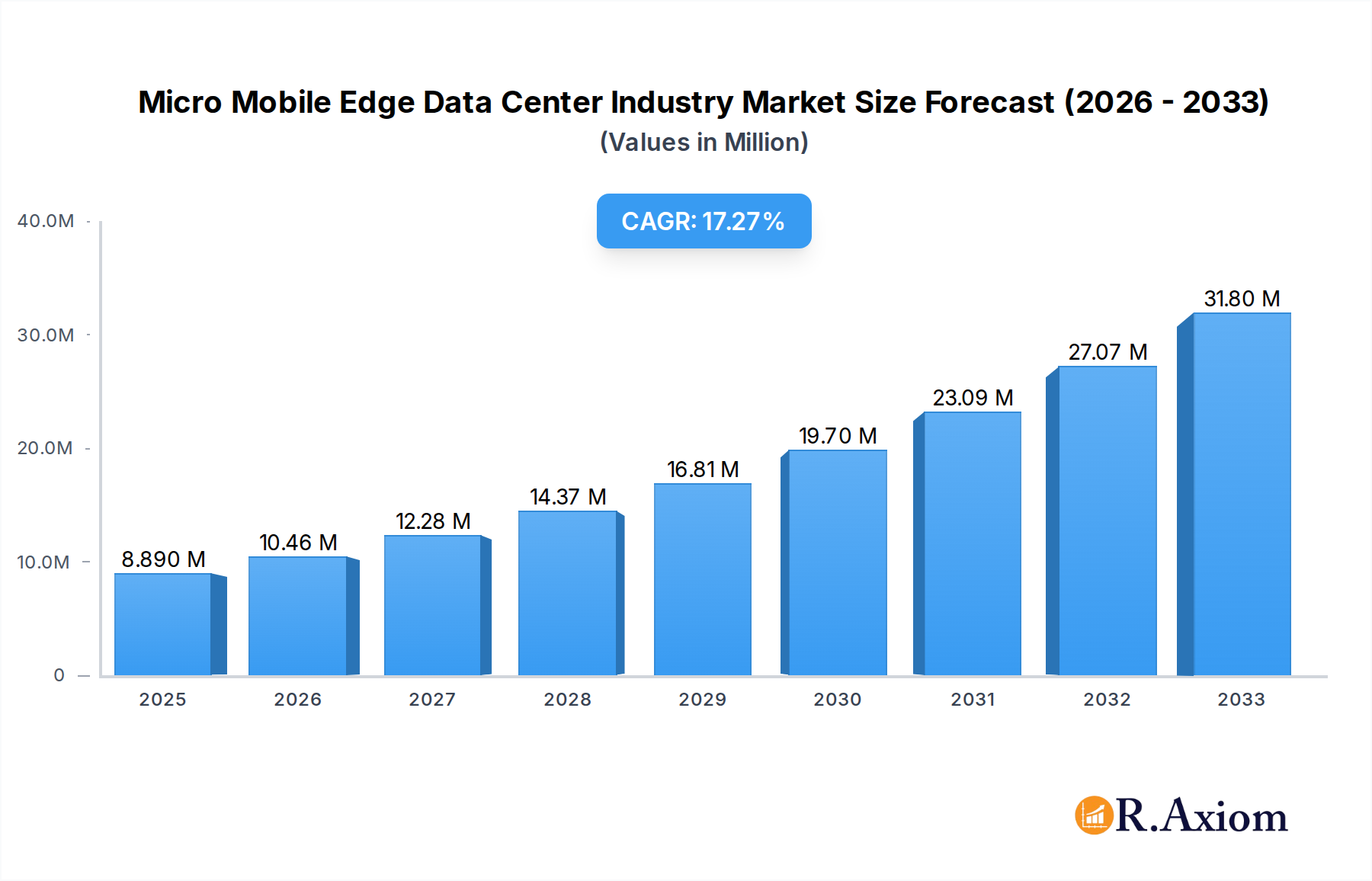

The Micro Mobile Edge Data Center Industry is poised for remarkable expansion, with the current market size estimated at $8.89 million. Projections indicate a robust compound annual growth rate (CAGR) of 17.62% over the forecast period of 2025-2033. This significant growth is driven by the escalating demand for localized data processing and low-latency applications across various sectors. Key drivers include the proliferation of IoT devices, the increasing adoption of 5G networks, and the need for real-time analytics in industries such as retail, manufacturing, and healthcare. The convenience and cost-effectiveness of deploying micro mobile edge data centers, particularly for small and medium-sized enterprises (SMEs), further fuel this market's trajectory. The flexibility to scale operations and address specific geographic or application requirements makes these solutions highly attractive.

Micro Mobile Edge Data Center Industry Market Size (In Million)

The market segmentation highlights a diverse range of applications, from smaller deployments catering to specific edge computing needs (Up to 25 RU) to larger enterprise solutions (Above 40 RU). The adoption is widespread across enterprise types, with both SMEs and Large Enterprises recognizing the strategic advantages. End-user verticals like Retail and E-commerce are leveraging these solutions for enhanced customer experiences and inventory management, while BFSI and IT and Telecommunication sectors are utilizing them for secure and efficient data handling. Healthcare benefits from real-time patient data processing, and the Government and Defense sectors rely on them for critical operational support. While the market is characterized by strong growth, potential restraints could include the complexities of managing distributed infrastructure and evolving cybersecurity threats, necessitating robust management and security protocols. Leading companies such as Panduit Corp, Dell EMC Inc, IBM Corporation, and Huawei Technologies Co Ltd are actively innovating and expanding their offerings to capture this burgeoning market.

Micro Mobile Edge Data Center Industry Company Market Share

Micro Mobile Edge Data Center Industry: Market Analysis & Forecast 2019–2033

This comprehensive report delves into the dynamic Micro Mobile Edge Data Center Industry, providing an in-depth analysis of market trends, growth drivers, challenges, and opportunities. Covering the study period of 2019–2033, with a base year of 2025 and a forecast period of 2025–2033, this report offers actionable insights for industry stakeholders, including manufacturers, solution providers, and end-users. Our analysis spans critical segments such as Up to 25 RU, 25-40 RU, and Above 40 RU for type, Small and Medium Enterprise (SME) and Large Enterprise for enterprise type, and diverse end-user verticals including Retail and E-commerce, Education, BFSI, IT and Telecommunication, Healthcare, Government and Defense, and Energy and Utilities.

Micro Mobile Edge Data Center Industry Market Concentration & Innovation

The Micro Mobile Edge Data Center Industry exhibits a moderately concentrated market landscape, characterized by the presence of both established global players and emerging specialized vendors. Innovation is a key differentiator, driven by the increasing demand for localized data processing, reduced latency, and enhanced security for edge computing applications. Key innovation drivers include advancements in power efficiency, cooling technologies, miniaturization of IT hardware, and the development of robust, all-weather enclosures. Regulatory frameworks, while still evolving, are increasingly focusing on data sovereignty and localized data handling, indirectly benefiting the adoption of edge data centers. Product substitutes, such as cloud-based solutions and larger centralized data centers, are present but struggle to match the agility and proximity benefits offered by micro mobile edge data centers. End-user trends are strongly skewed towards industries requiring real-time data analysis and decentralized operations. Merger and acquisition (M&A) activities are anticipated to rise as larger IT infrastructure companies seek to expand their edge computing portfolios and gain market share. For instance, M&A deal values in this nascent sector could reach several hundred million dollars as companies consolidate capabilities and accelerate product development. Market share for leading players is estimated to be around 5-10% each, with a significant portion held by smaller, specialized providers.

- Innovation Drivers:

- Demand for low-latency processing

- Increased adoption of IoT and AI at the edge

- Developments in modular and prefabricated designs

- Enhanced power and cooling efficiency solutions

- Robust and secure enclosure technologies

- Regulatory Impact:

- Data sovereignty laws

- Local data processing mandates

- Cybersecurity standards for distributed infrastructure

- Market Concentration Metrics:

- Estimated market share of top 5 players: 30-40%

- M&A activity: Expecting deal values to range from USD 50 million to USD 500 million in strategic acquisitions.

Micro Mobile Edge Data Center Industry Industry Trends & Insights

The Micro Mobile Edge Data Center Industry is experiencing robust growth, fueled by an unprecedented surge in data generation and the imperative for real-time processing closer to the source. The compound annual growth rate (CAGR) for this sector is projected to be in the range of 15-20% over the forecast period. This rapid expansion is underpinned by a confluence of factors, including the proliferation of the Internet of Things (IoT) devices, the accelerating adoption of artificial intelligence (AI) and machine learning (ML) at the edge, and the increasing need for low-latency applications across various industries. Technological disruptions, such as the evolution of 5G networks, are critical enablers, providing the high-speed, low-latency connectivity required for effective edge data center deployment. Consumer preferences are shifting towards experiences that demand immediate data processing, such as augmented reality (AR), autonomous vehicles, and smart city initiatives. The competitive dynamics are intensifying, with a mix of established IT infrastructure giants and agile startups vying for market dominance. Market penetration is still in its early stages, offering significant headroom for growth as organizations recognize the strategic advantages of decentralized data infrastructure. The ongoing digital transformation across enterprises is a primary market growth driver, pushing businesses to rethink their data architectures and embrace edge computing solutions for enhanced agility, resilience, and cost-efficiency. The development of standardized, scalable, and easily deployable micro mobile edge data centers is crucial for widespread adoption. The estimated market penetration currently stands at approximately 10-15%, with substantial growth expected as awareness and infrastructure mature.

- Market Growth Drivers:

- Explosive growth in IoT device deployments

- Demand for real-time AI/ML analytics

- Advancements in 5G network capabilities

- Need for enhanced cybersecurity and data privacy at the edge

- Cost-optimization through localized processing

- Technological Disruptions:

- Software-defined networking (SDN) and network function virtualization (NFV)

- Containerization technologies (e.g., Docker, Kubernetes)

- Improved energy-efficient computing hardware

- Advanced cooling solutions for dense environments

- Market Penetration:

- Estimated current market penetration: 10-15%

- Projected market penetration by 2033: 40-50%

- CAGR:

- Projected CAGR (2025-2033): 15-20%

Dominant Markets & Segments in Micro Mobile Edge Data Center Industry

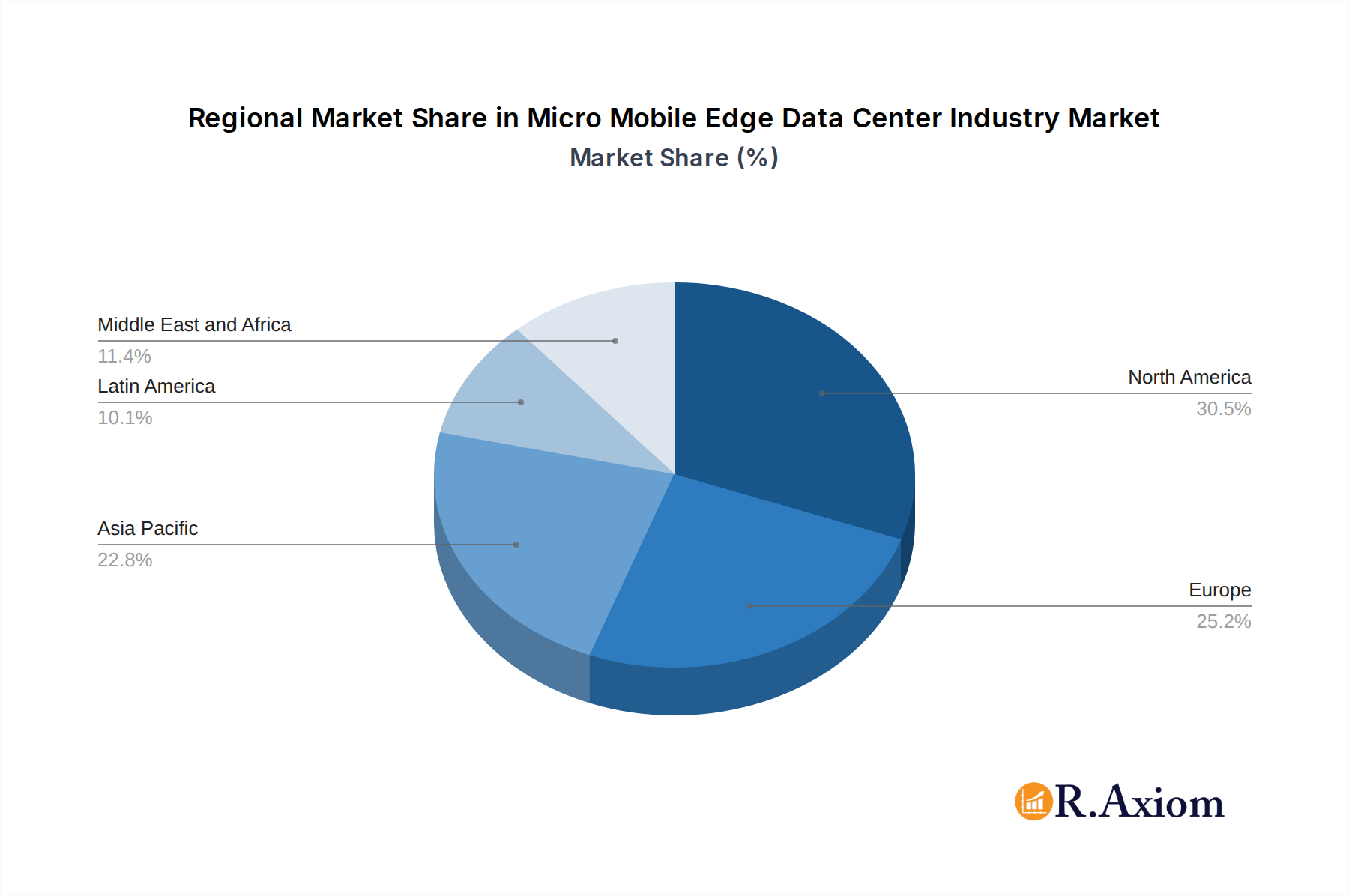

The Micro Mobile Edge Data Center Industry is witnessing significant traction across several key regions and segments. North America and Europe currently lead in market adoption, driven by strong technological infrastructure, advanced digital economies, and early adoption of edge computing principles. Within these regions, countries like the United States, Germany, and the United Kingdom are at the forefront. The IT and Telecommunication sector is the dominant end-user vertical, owing to the inherent need for distributed computing power to support 5G rollouts, cloud services, and network infrastructure. The Healthcare sector is rapidly emerging as a strong contender, driven by the need for real-time patient data processing, remote monitoring, and AI-powered diagnostics within hospitals and clinics.

Dominant Type Segments:

- 25-40 RU: This segment is particularly dominant, offering a balanced capacity for a wide range of edge computing applications without being overly bulky. It strikes a critical balance between density and deployability.

- Above 40 RU: Growing demand from large enterprises and specific industry verticals requiring higher compute and storage capabilities at the edge is pushing the growth of this segment.

- Up to 25 RU: This segment is vital for highly localized deployments and niche applications where space and power are extremely constrained, such as retail stores or remote industrial sites.

Dominant Enterprise Types:

- Large Enterprise: These organizations have the scale and complexity to leverage micro mobile edge data centers for distributed operations, improved resilience, and advanced analytics across multiple locations.

- Small and Medium Enterprise (SME): As the cost of edge infrastructure decreases and ease of deployment increases, SMEs are increasingly adopting these solutions to compete with larger players by accessing advanced IT capabilities.

Dominant End-User Verticals:

- IT and Telecommunication: Critical for network densification, 5G core deployment, and edge data services.

- Healthcare: Enabling real-time patient monitoring, hospital IoT, AI diagnostics, and secure medical data processing at the point of care.

- Retail and E-commerce: Supporting in-store analytics, localized inventory management, personalized customer experiences, and smart checkout systems.

- Government and Defense: Facilitating secure, resilient, and deployable IT infrastructure for remote operations, intelligence gathering, and critical command and control systems.

- BFSI: Enhancing fraud detection, real-time transaction processing, and personalized customer services at branch locations.

- Energy and Utilities: Enabling smart grid management, remote asset monitoring, and predictive maintenance for distributed energy infrastructure.

- Education: Supporting campus-wide IoT deployments, smart classroom technologies, and localized research computing.

Key Drivers for Dominance:

- Economic Policies: Government initiatives promoting digital transformation and investment in advanced infrastructure.

- Infrastructure Development: Proactive investments in network connectivity (5G) and power grids.

- Industry-Specific Regulations: Mandates for data localization and stringent security requirements in sectors like healthcare and finance.

- Technological Readiness: High adoption rates of IoT, AI, and cloud technologies.

Micro Mobile Edge Data Center Industry Product Developments

Product developments in the Micro Mobile Edge Data Center Industry are intensely focused on miniaturization, increased modularity, and enhanced environmental resilience. Innovations include integrated cooling systems that can operate efficiently in extreme temperatures, robust power backup solutions, and simplified deployment mechanisms. The competitive advantage lies in offering highly customizable, plug-and-play solutions that can be deployed rapidly in diverse and challenging locations. Technological trends are pushing towards AI-enabled self-monitoring and predictive maintenance capabilities within these micro data centers, reducing the need for on-site technical expertise. Applications are expanding beyond traditional IT rooms to include remote industrial sites, retail environments, and mobile command centers, highlighting the versatility and growing market fit of these solutions.

Report Scope & Segmentation Analysis

This report encompasses a comprehensive analysis of the Micro Mobile Edge Data Center Industry, segmented across crucial parameters to provide granular insights.

- Type Segmentation:

- Up to 25 RU: Encompasses compact, highly portable units designed for very specific, localized edge computing needs.

- 25-40 RU: Represents the most versatile segment, offering a balance of capacity and deployability for a wide array of edge applications.

- Above 40 RU: Caters to enterprise-level edge deployments requiring significant compute and storage density.

- Enterprise Type Segmentation:

- Small and Medium Enterprise (SME): Focuses on providing scalable and cost-effective edge solutions enabling SMEs to leverage advanced IT capabilities.

- Large Enterprise: Analyzes the deployment of micro mobile edge data centers within large organizations for distributed operations, enhanced resilience, and specialized edge computing workloads.

- End-User Vertical Segmentation:

- Retail and E-commerce: Examining the use of edge data centers for in-store analytics, inventory management, and personalized customer experiences.

- Education: Assessing the integration of edge computing for smart campuses, research, and localized IT support.

- BFSI: Detailing applications in fraud detection, real-time transaction processing, and branch office IT.

- IT and Telecommunication: Covering the critical role in 5G infrastructure, network edge, and data service delivery.

- Healthcare: Analyzing deployments for patient monitoring, hospital IoT, and point-of-care data processing.

- Government and Defense: Exploring secure, deployable solutions for remote operations and critical infrastructure.

- Energy and Utilities: Investigating applications in smart grids, asset monitoring, and operational efficiency.

Key Drivers of Micro Mobile Edge Data Center Industry Growth

The Micro Mobile Edge Data Center Industry is propelled by several interconnected drivers. The exponential growth of the Internet of Things (IoT) necessitates localized data processing to handle the vast influx of data generated by connected devices. The increasing adoption of Artificial Intelligence (AI) and Machine Learning (ML) at the edge, for real-time analytics and decision-making, is a significant catalyst. The widespread rollout of 5G networks is a crucial enabler, providing the low-latency, high-bandwidth connectivity required for efficient edge deployments. Furthermore, stringent data privacy regulations and the demand for data sovereignty are driving organizations to process data closer to its source. Economic factors, such as the potential for cost savings through localized processing and reduced bandwidth consumption, also contribute to growth.

Challenges in the Micro Mobile Edge Data Center Industry Sector

Despite the promising growth trajectory, the Micro Mobile Edge Data Center Industry faces several significant challenges. Regulatory hurdles, particularly concerning data governance, security standards, and varying compliance requirements across different jurisdictions, can slow down adoption. Supply chain disruptions, exacerbated by global events, can impact the availability and cost of essential components, leading to extended lead times for deployments. The complexity of managing a distributed network of edge data centers, including remote monitoring, maintenance, and security, requires specialized skills and robust management platforms. Competitive pressures from established cloud providers offering integrated edge solutions also pose a challenge. The initial capital investment for deploying multiple edge data centers, while offering long-term ROI, can be a barrier for some organizations.

Emerging Opportunities in Micro Mobile Edge Data Center Industry

The Micro Mobile Edge Data Center Industry is rife with emerging opportunities. The continued expansion of smart city initiatives worldwide presents a substantial market for deploying edge infrastructure to support connected urban services, from traffic management to public safety. The increasing adoption of industrial IoT (IIoT) in manufacturing, logistics, and agriculture creates demand for ruggedized and deployable edge data centers in remote or harsh environments. The growth of augmented reality (AR) and virtual reality (VR) applications, requiring ultra-low latency, will drive further innovation and adoption of edge solutions. The development of more energy-efficient and sustainable micro data center designs will open doors in environmentally conscious markets. Furthermore, the rise of specialized edge AI hardware and software solutions will create new revenue streams and partnerships within the ecosystem.

Leading Players in the Micro Mobile Edge Data Center Industry Market

- Panduit Corp

- Dell EMC Inc

- IBM Corporation

- Canovate Group

- Hitachi Ltd

- Vertiv Co

- Schneider Electric SE

- Hewlett Packard Enterprise Development LP

- Eaton Corporation PLC

- Dataracks

- Rittal GmbH & Co Kg

- Huawei Technologies Co Ltd

- Zellabox Pty Ltd

- Instant Data Centers LLC

Key Developments in Micro Mobile Edge Data Center Industry Industry

- November 2023: Schneider Electric, a leader in digital transformation of energy management and automation, announced a USD 3 billion multi-year agreement with Compass Datacenters at its Capital Markets Day. This agreement strengthens their partnership by integrating supply chains for the manufacture and delivery of prefabricated modular data center solutions.

- June 2023: Secure I.T. Environments delivered a 42U Micro Data Centre to the intensive care unit (ICU) of Barnet Hospital in London, United Kingdom. This containerized facility, capable of handling up to a 12kW load, provides essential network and communications services for the ICU's operations.

Strategic Outlook for Micro Mobile Edge Data Center Industry Market

The strategic outlook for the Micro Mobile Edge Data Center Industry is overwhelmingly positive, driven by the persistent need for distributed intelligence and localized data processing. Key growth catalysts include the ongoing digital transformation across all sectors, the maturation of 5G networks, and the relentless advancement of IoT and AI technologies. The market is poised for significant expansion as enterprises increasingly recognize the operational efficiencies, enhanced security, and improved customer experiences that edge computing offers. Future market potential is immense, fueled by the development of more intelligent, autonomous, and sustainable micro mobile edge data center solutions. Opportunities will arise from the integration of advanced cooling technologies, software-defined management, and seamless connectivity to broader cloud infrastructures, solidifying the role of edge data centers as a critical component of the modern IT landscape.

Micro Mobile Edge Data Center Industry Segmentation

-

1. Type

- 1.1. Up to 25 RU

- 1.2. 25-40 RU

- 1.3. Above 40 RU

-

2. Enterprise Type

- 2.1. Small and Medium Enterprise (SME)

- 2.2. Large Enterprise

-

3. End-user Vertical

- 3.1. Retail and E-commerce

- 3.2. Education

- 3.3. BFSI

- 3.4. IT and Telecommunication

- 3.5. Healthcare

- 3.6. Government and Defense

- 3.7. Energy and Utilities

Micro Mobile Edge Data Center Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Micro Mobile Edge Data Center Industry Regional Market Share

Geographic Coverage of Micro Mobile Edge Data Center Industry

Micro Mobile Edge Data Center Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 17.62% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Up to 25 RU

- 5.1.2. 25-40 RU

- 5.1.3. Above 40 RU

- 5.2. Market Analysis, Insights and Forecast - by Enterprise Type

- 5.2.1. Small and Medium Enterprise (SME)

- 5.2.2. Large Enterprise

- 5.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 5.3.1. Retail and E-commerce

- 5.3.2. Education

- 5.3.3. BFSI

- 5.3.4. IT and Telecommunication

- 5.3.5. Healthcare

- 5.3.6. Government and Defense

- 5.3.7. Energy and Utilities

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Latin America

- 5.4.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Micro Mobile Edge Data Center Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Up to 25 RU

- 6.1.2. 25-40 RU

- 6.1.3. Above 40 RU

- 6.2. Market Analysis, Insights and Forecast - by Enterprise Type

- 6.2.1. Small and Medium Enterprise (SME)

- 6.2.2. Large Enterprise

- 6.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 6.3.1. Retail and E-commerce

- 6.3.2. Education

- 6.3.3. BFSI

- 6.3.4. IT and Telecommunication

- 6.3.5. Healthcare

- 6.3.6. Government and Defense

- 6.3.7. Energy and Utilities

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Micro Mobile Edge Data Center Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Up to 25 RU

- 7.1.2. 25-40 RU

- 7.1.3. Above 40 RU

- 7.2. Market Analysis, Insights and Forecast - by Enterprise Type

- 7.2.1. Small and Medium Enterprise (SME)

- 7.2.2. Large Enterprise

- 7.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 7.3.1. Retail and E-commerce

- 7.3.2. Education

- 7.3.3. BFSI

- 7.3.4. IT and Telecommunication

- 7.3.5. Healthcare

- 7.3.6. Government and Defense

- 7.3.7. Energy and Utilities

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Micro Mobile Edge Data Center Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Up to 25 RU

- 8.1.2. 25-40 RU

- 8.1.3. Above 40 RU

- 8.2. Market Analysis, Insights and Forecast - by Enterprise Type

- 8.2.1. Small and Medium Enterprise (SME)

- 8.2.2. Large Enterprise

- 8.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 8.3.1. Retail and E-commerce

- 8.3.2. Education

- 8.3.3. BFSI

- 8.3.4. IT and Telecommunication

- 8.3.5. Healthcare

- 8.3.6. Government and Defense

- 8.3.7. Energy and Utilities

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific Micro Mobile Edge Data Center Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Up to 25 RU

- 9.1.2. 25-40 RU

- 9.1.3. Above 40 RU

- 9.2. Market Analysis, Insights and Forecast - by Enterprise Type

- 9.2.1. Small and Medium Enterprise (SME)

- 9.2.2. Large Enterprise

- 9.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 9.3.1. Retail and E-commerce

- 9.3.2. Education

- 9.3.3. BFSI

- 9.3.4. IT and Telecommunication

- 9.3.5. Healthcare

- 9.3.6. Government and Defense

- 9.3.7. Energy and Utilities

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Latin America Micro Mobile Edge Data Center Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Up to 25 RU

- 10.1.2. 25-40 RU

- 10.1.3. Above 40 RU

- 10.2. Market Analysis, Insights and Forecast - by Enterprise Type

- 10.2.1. Small and Medium Enterprise (SME)

- 10.2.2. Large Enterprise

- 10.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 10.3.1. Retail and E-commerce

- 10.3.2. Education

- 10.3.3. BFSI

- 10.3.4. IT and Telecommunication

- 10.3.5. Healthcare

- 10.3.6. Government and Defense

- 10.3.7. Energy and Utilities

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Middle East and Africa Micro Mobile Edge Data Center Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Up to 25 RU

- 11.1.2. 25-40 RU

- 11.1.3. Above 40 RU

- 11.2. Market Analysis, Insights and Forecast - by Enterprise Type

- 11.2.1. Small and Medium Enterprise (SME)

- 11.2.2. Large Enterprise

- 11.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 11.3.1. Retail and E-commerce

- 11.3.2. Education

- 11.3.3. BFSI

- 11.3.4. IT and Telecommunication

- 11.3.5. Healthcare

- 11.3.6. Government and Defense

- 11.3.7. Energy and Utilities

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Panduit Corp

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Dell EMC Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 IBM Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Canovate Group*List Not Exhaustive

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Hitachi Ltd

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Vertiv Co

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Schneider Electric SE

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Hewlett Packard Enterprise Development LP

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Eaton Corporation PLC

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Dataracks

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Rittal GmbH & Co Kg

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Huawei Technologies Co Ltd

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Zellabox Pty Ltd

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Instant Data Centers LLC

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 Panduit Corp

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Micro Mobile Edge Data Center Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Micro Mobile Edge Data Center Industry Revenue (Million), by Type 2025 & 2033

- Figure 3: North America Micro Mobile Edge Data Center Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Micro Mobile Edge Data Center Industry Revenue (Million), by Enterprise Type 2025 & 2033

- Figure 5: North America Micro Mobile Edge Data Center Industry Revenue Share (%), by Enterprise Type 2025 & 2033

- Figure 6: North America Micro Mobile Edge Data Center Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 7: North America Micro Mobile Edge Data Center Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 8: North America Micro Mobile Edge Data Center Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Micro Mobile Edge Data Center Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Micro Mobile Edge Data Center Industry Revenue (Million), by Type 2025 & 2033

- Figure 11: Europe Micro Mobile Edge Data Center Industry Revenue Share (%), by Type 2025 & 2033

- Figure 12: Europe Micro Mobile Edge Data Center Industry Revenue (Million), by Enterprise Type 2025 & 2033

- Figure 13: Europe Micro Mobile Edge Data Center Industry Revenue Share (%), by Enterprise Type 2025 & 2033

- Figure 14: Europe Micro Mobile Edge Data Center Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 15: Europe Micro Mobile Edge Data Center Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 16: Europe Micro Mobile Edge Data Center Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Europe Micro Mobile Edge Data Center Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Micro Mobile Edge Data Center Industry Revenue (Million), by Type 2025 & 2033

- Figure 19: Asia Pacific Micro Mobile Edge Data Center Industry Revenue Share (%), by Type 2025 & 2033

- Figure 20: Asia Pacific Micro Mobile Edge Data Center Industry Revenue (Million), by Enterprise Type 2025 & 2033

- Figure 21: Asia Pacific Micro Mobile Edge Data Center Industry Revenue Share (%), by Enterprise Type 2025 & 2033

- Figure 22: Asia Pacific Micro Mobile Edge Data Center Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 23: Asia Pacific Micro Mobile Edge Data Center Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 24: Asia Pacific Micro Mobile Edge Data Center Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Asia Pacific Micro Mobile Edge Data Center Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Latin America Micro Mobile Edge Data Center Industry Revenue (Million), by Type 2025 & 2033

- Figure 27: Latin America Micro Mobile Edge Data Center Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: Latin America Micro Mobile Edge Data Center Industry Revenue (Million), by Enterprise Type 2025 & 2033

- Figure 29: Latin America Micro Mobile Edge Data Center Industry Revenue Share (%), by Enterprise Type 2025 & 2033

- Figure 30: Latin America Micro Mobile Edge Data Center Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 31: Latin America Micro Mobile Edge Data Center Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 32: Latin America Micro Mobile Edge Data Center Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: Latin America Micro Mobile Edge Data Center Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East and Africa Micro Mobile Edge Data Center Industry Revenue (Million), by Type 2025 & 2033

- Figure 35: Middle East and Africa Micro Mobile Edge Data Center Industry Revenue Share (%), by Type 2025 & 2033

- Figure 36: Middle East and Africa Micro Mobile Edge Data Center Industry Revenue (Million), by Enterprise Type 2025 & 2033

- Figure 37: Middle East and Africa Micro Mobile Edge Data Center Industry Revenue Share (%), by Enterprise Type 2025 & 2033

- Figure 38: Middle East and Africa Micro Mobile Edge Data Center Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 39: Middle East and Africa Micro Mobile Edge Data Center Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 40: Middle East and Africa Micro Mobile Edge Data Center Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Middle East and Africa Micro Mobile Edge Data Center Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Micro Mobile Edge Data Center Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Global Micro Mobile Edge Data Center Industry Revenue Million Forecast, by Enterprise Type 2020 & 2033

- Table 3: Global Micro Mobile Edge Data Center Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 4: Global Micro Mobile Edge Data Center Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Micro Mobile Edge Data Center Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 6: Global Micro Mobile Edge Data Center Industry Revenue Million Forecast, by Enterprise Type 2020 & 2033

- Table 7: Global Micro Mobile Edge Data Center Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 8: Global Micro Mobile Edge Data Center Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: Global Micro Mobile Edge Data Center Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 10: Global Micro Mobile Edge Data Center Industry Revenue Million Forecast, by Enterprise Type 2020 & 2033

- Table 11: Global Micro Mobile Edge Data Center Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 12: Global Micro Mobile Edge Data Center Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global Micro Mobile Edge Data Center Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 14: Global Micro Mobile Edge Data Center Industry Revenue Million Forecast, by Enterprise Type 2020 & 2033

- Table 15: Global Micro Mobile Edge Data Center Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 16: Global Micro Mobile Edge Data Center Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 17: Global Micro Mobile Edge Data Center Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 18: Global Micro Mobile Edge Data Center Industry Revenue Million Forecast, by Enterprise Type 2020 & 2033

- Table 19: Global Micro Mobile Edge Data Center Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 20: Global Micro Mobile Edge Data Center Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: Global Micro Mobile Edge Data Center Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 22: Global Micro Mobile Edge Data Center Industry Revenue Million Forecast, by Enterprise Type 2020 & 2033

- Table 23: Global Micro Mobile Edge Data Center Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 24: Global Micro Mobile Edge Data Center Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Micro Mobile Edge Data Center Industry?

The projected CAGR is approximately 17.62%.

2. Which companies are prominent players in the Micro Mobile Edge Data Center Industry?

Key companies in the market include Panduit Corp, Dell EMC Inc, IBM Corporation, Canovate Group*List Not Exhaustive, Hitachi Ltd, Vertiv Co, Schneider Electric SE, Hewlett Packard Enterprise Development LP, Eaton Corporation PLC, Dataracks, Rittal GmbH & Co Kg, Huawei Technologies Co Ltd, Zellabox Pty Ltd, Instant Data Centers LLC.

3. What are the main segments of the Micro Mobile Edge Data Center Industry?

The market segments include Type, Enterprise Type, End-user Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.89 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Penetration of IOT Devices Enterprises; Increasing Speed and Volume of Digital Data Generation.

6. What are the notable trends driving market growth?

Healthcare End User Vertical is Expected to Hold a Significant Market Share.

7. Are there any restraints impacting market growth?

Cryptojacking Threats.

8. Can you provide examples of recent developments in the market?

November 2023 - At its Capital Markets Day meeting with investors, Schneider Electric, one of the leaders in the digital transformation of energy management and automation, announced a USD 3 billion multi-year agreement with Compass Datacenters. The agreement extends the companies' existing relationship, integrating their respective supply chains to manufacture and deliver prefabricated modular data center solutions.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Micro Mobile Edge Data Center Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Micro Mobile Edge Data Center Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Micro Mobile Edge Data Center Industry?

To stay informed about further developments, trends, and reports in the Micro Mobile Edge Data Center Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence