Key Insights

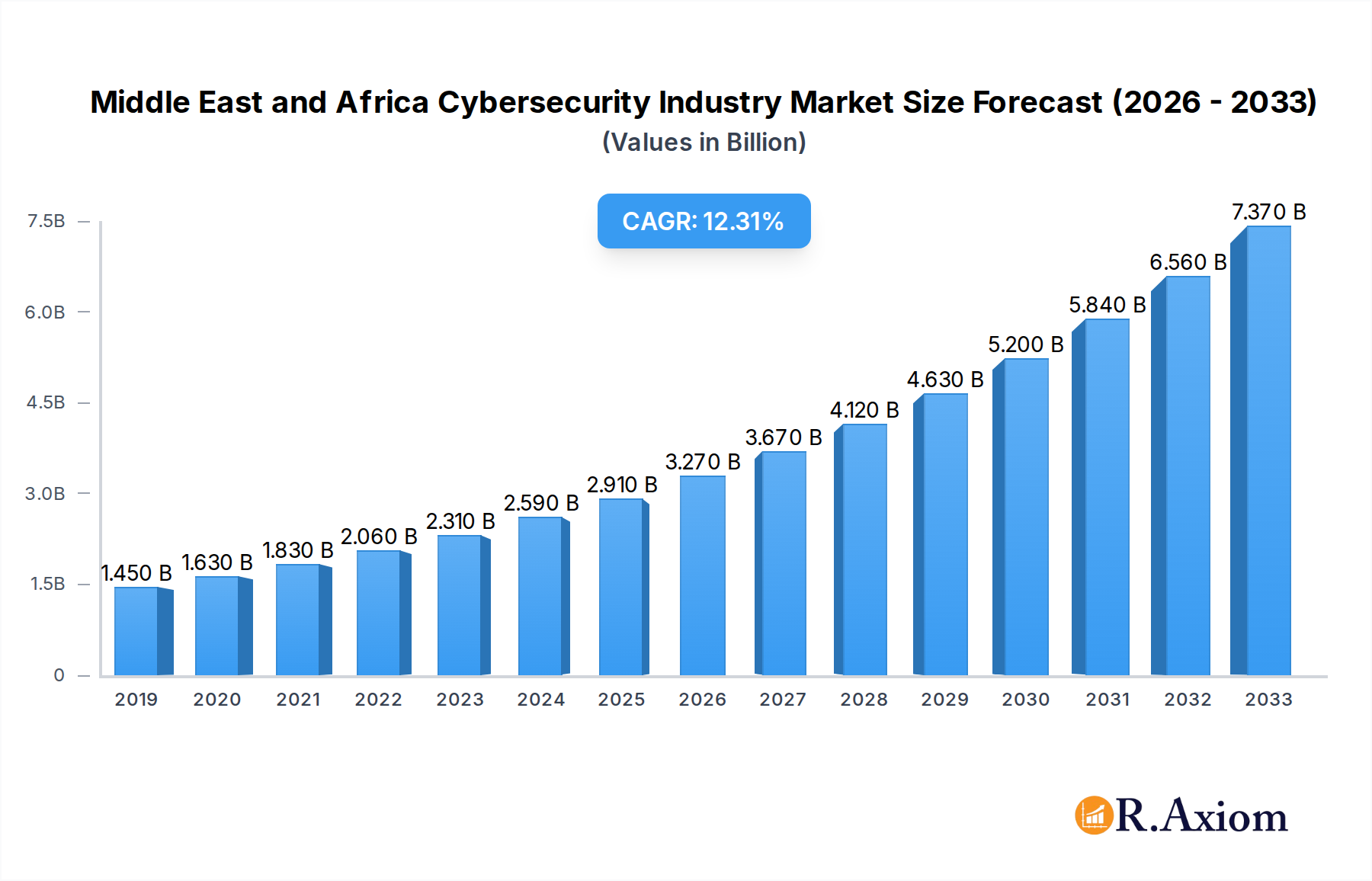

The Middle East and Africa (MEA) cybersecurity market is poised for substantial growth, projected to reach USD 2.91 Billion by 2025, exhibiting a robust Compound Annual Growth Rate (CAGR) of 12.42% over the forecast period. This expansion is primarily driven by escalating cyber threats and the increasing adoption of sophisticated security solutions across various sectors. The region's growing digital transformation initiatives, coupled with stringent data protection regulations, are compelling organizations to invest heavily in advanced cybersecurity measures. Key segments such as Threat Intelligence and Response Management, Identity and Access Management, and Data Loss Prevention Management are experiencing significant demand. Furthermore, the shift towards cloud-based security solutions is accelerating, offering scalability and cost-effectiveness for businesses in the MEA region. The increasing reliance on managed services and professional services for cybersecurity implementation and maintenance also underscores the growing complexity of the threat landscape and the need for specialized expertise.

Middle East and Africa Cybersecurity Industry Market Size (In Billion)

Several factors contribute to the market's upward trajectory. The burgeoning IT and Telecommunication sector, alongside critical industries like BFSI, Healthcare, and Government, are primary adopters of cybersecurity solutions, seeking to protect sensitive data and ensure operational continuity. Emerging economies within the MEA, particularly in the Middle East like Saudi Arabia and the United Arab Emirates, are at the forefront of this cybersecurity investment. However, challenges such as a shortage of skilled cybersecurity professionals and the high cost of advanced security technologies can act as restraints. Despite these, the persistent and evolving nature of cyber threats, including ransomware, phishing, and advanced persistent threats (APTs), necessitates continuous investment and innovation in the cybersecurity domain, ensuring sustained market growth. Companies like Palo Alto Networks, Cisco Systems, and IBM Corporation are key players actively shaping this dynamic market.

Middle East and Africa Cybersecurity Industry Company Market Share

Here is a comprehensive, SEO-optimized report description for the Middle East and Africa Cybersecurity Industry.

Middle East and Africa Cybersecurity Industry Market Concentration & Innovation

The Middle East and Africa (MEA) cybersecurity market is experiencing dynamic shifts characterized by increasing market concentration in key solutions and services, driven by a rising tide of sophisticated cyber threats and the urgent need for robust digital defenses. Innovation is paramount, with significant investments in advanced technologies such as AI-powered threat detection, cloud security, and identity and access management (IAM). Regulatory frameworks are evolving rapidly across the region, with countries like the UAE and Saudi Arabia implementing stricter data protection and cybersecurity mandates, further stimulating market growth. Product substitutes, while present in basic security solutions, are rapidly being outpaced by integrated, intelligent platforms. End-user adoption is expanding beyond traditional BFSI and government sectors to embrace manufacturing, healthcare, and retail, recognizing the pervasive risk of cyberattacks. Mergers and acquisitions (M&A) are becoming a crucial strategy for market leaders to expand their portfolios and geographical reach. For instance, significant M&A deal values are projected to cross $250 Million in the forecast period, with key players like Palo Alto Networks Inc and Cisco Systems Inc actively consolidating their market positions through strategic acquisitions. Companies such as IBM Corporation and Broadcom Inc (Symantec Corporation) are also prominent in this consolidation landscape, aiming to capture larger market shares and enhance their competitive edge by offering comprehensive cybersecurity solutions. The overall market share distribution indicates a competitive yet consolidating environment, with a few dominant players holding substantial portions of the market, particularly in areas like threat intelligence and managed services.

Middle East and Africa Cybersecurity Industry Industry Trends & Insights

The Middle East and Africa (MEA) cybersecurity industry is on an accelerated growth trajectory, fueled by an escalating cyber threat landscape and a growing awareness of digital vulnerabilities across diverse sectors. The projected Compound Annual Growth Rate (CAGR) for the MEA cybersecurity market is an impressive 18.5% for the forecast period of 2025–2033, indicating robust expansion. This growth is significantly propelled by the increasing digitalization of economies across the region, leading to a larger attack surface for cybercriminals. Technological disruptions, including the widespread adoption of cloud computing, the proliferation of IoT devices, and the growing use of artificial intelligence and machine learning in cybersecurity solutions, are reshaping the market. Consumer preferences are shifting towards proactive, integrated security solutions that offer end-to-end protection rather than fragmented point solutions. Businesses are prioritizing managed security services and cloud-based cybersecurity platforms due to their scalability, cost-effectiveness, and ability to address the shortage of skilled cybersecurity professionals in the region. The competitive dynamics are intensifying, with both global cybersecurity giants and agile regional players vying for market dominance. Key market penetration is expected to reach 65% by 2033, underscoring the critical importance of cybersecurity for businesses of all sizes. The rise in ransomware attacks, data breaches, and sophisticated phishing campaigns continues to be a primary driver, compelling organizations to allocate substantial budgets towards cybersecurity investments. Furthermore, government initiatives aimed at fostering digital economies and protecting critical infrastructure are creating a favorable environment for cybersecurity adoption. The demand for advanced threat intelligence and response management solutions is particularly high, as organizations seek to not only prevent attacks but also to effectively detect and respond to them in real-time. The BFSI sector, in particular, remains a frontrunner in cybersecurity spending due to stringent regulatory requirements and the sensitive nature of the data they handle. The IT and Telecommunication sector also plays a crucial role as a foundational element for digital infrastructure, requiring robust security to maintain trust and operational continuity. The increasing adoption of remote work models also necessitates enhanced endpoint security and secure network access solutions. The MEA region, with its rapidly developing economies and growing digital footprint, presents a fertile ground for cybersecurity innovation and market expansion, projected to reach an estimated market size of $22 Billion by 2033.

Dominant Markets & Segments in Middle East and Africa Cybersecurity Industry

The Middle East and Africa (MEA) cybersecurity market exhibits distinct patterns of dominance across various segments, influenced by economic policies, infrastructure development, and localized threat landscapes.

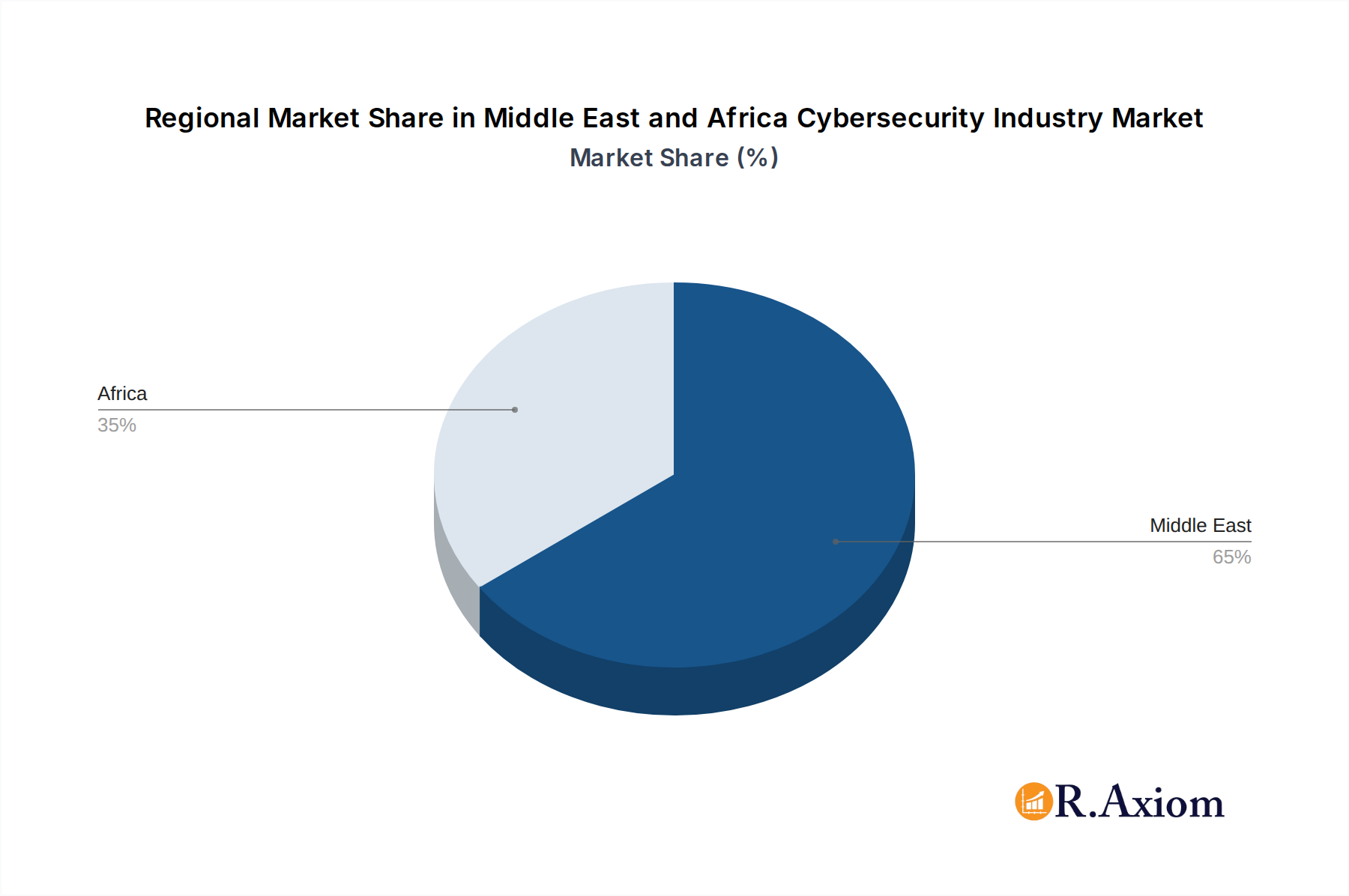

Leading Regions and Countries: The United Arab Emirates (UAE) and Saudi Arabia are emerging as dominant markets within the MEA region. Their proactive government initiatives, substantial investments in digital transformation, and strict regulatory frameworks for data protection and cybersecurity have fostered high adoption rates of advanced security solutions. These nations are at the forefront of implementing sophisticated cybersecurity strategies to protect critical national infrastructure and burgeoning digital economies.

Dominant Solutions:

- Security and Vulnerability Management: This segment holds significant sway due to the pervasive need for organizations to identify and remediate weaknesses in their digital assets. The increasing sophistication of cyberattacks makes continuous vulnerability assessment and management a top priority.

- Threat Intelligence and Response Management: With the escalating volume and complexity of cyber threats, the demand for real-time threat intelligence and efficient response mechanisms is paramount. This segment is crucial for proactive defense and rapid incident handling, valued at approximately $4.5 Billion in 2025.

- Identity and Access Management (IAM): As remote work and cloud adoption grow, securing user identities and controlling access to sensitive data becomes critical. IAM solutions are essential for preventing unauthorized access and are projected to grow by 20% annually.

Dominant Services:

- Managed Services: The scarcity of skilled cybersecurity professionals across the MEA region drives the strong demand for managed security services (MSS). Businesses are increasingly outsourcing their cybersecurity operations to expert providers to ensure continuous monitoring, threat detection, and incident response. This segment is estimated to reach $5 Billion in market value by 2028.

- Professional Services: Complementing managed services, professional services encompassing consulting, implementation, and security audits are also in high demand, helping organizations align their security strategies with business objectives and regulatory compliance.

Dominant Deployments:

- Cloud: The rapid migration of data and applications to cloud environments is accelerating the adoption of cloud-based cybersecurity solutions. These offer scalability, flexibility, and cost-effectiveness, making them the preferred choice for many organizations. Cloud deployment is expected to account for over 60% of new cybersecurity investments by 2030.

- On-Premise: While cloud adoption is on the rise, on-premise deployments remain significant for organizations with highly sensitive data or strict regulatory requirements that necessitate complete control over their infrastructure.

Dominant End Users:

- BFSI (Banking, Financial Services, and Insurance): This sector consistently leads in cybersecurity spending due to the highly regulated nature of their operations and the immense value of the financial data they manage. The BFSI segment is projected to contribute $3.8 Billion to the cybersecurity market in 2025.

- Government: National security concerns and the protection of critical infrastructure make government entities major investors in cybersecurity. Initiatives to build smart cities and enhance digital governance further amplify this demand.

- IT and Telecommunication: As the backbone of digital connectivity, this sector requires robust security to safeguard networks, data centers, and customer information. Their investments are crucial for enabling the broader digital ecosystem.

- Aerospace and Defense: This sector demands highly advanced and secure solutions due to the sensitive nature of their operations and the potential for nation-state sponsored attacks, representing a significant market share of $1.2 Billion in 2025.

Middle East and Africa Cybersecurity Industry Product Developments

Product development in the MEA cybersecurity industry is increasingly focused on leveraging artificial intelligence and machine learning for predictive threat analysis and automated response. Innovations are geared towards unified platforms that integrate threat intelligence, endpoint security, and cloud access security broker (CASB) functionalities. Companies are developing solutions with enhanced data loss prevention (DLP) capabilities, tailored for the specific regulatory environments of the MEA region. Furthermore, there is a growing emphasis on user-friendly interfaces and simplified deployment models, particularly for small and medium-sized enterprises (SMEs), to address the skills gap. Competitive advantages are being built through comprehensive threat detection, rapid incident remediation, and robust compliance management features.

Report Scope & Segmentation Analysis

This report meticulously analyzes the Middle East and Africa Cybersecurity Industry across its key segments. The Solution segmentation includes: Threat Intelligence and Response Management, Identity and Access Management, Data Loss Prevention Management, Security and Vulnerability Management, Unified Threat Management, and Enterprise Risk and Compliance. The Service segmentation covers Managed Services and Professional Services. Deployment options analyzed are Cloud and On-premise. Finally, the End User segmentation spans Aerospace and Defense, BFSI, Healthcare, Manufacturing, Retail, Government, IT and Telecommunication, and Other End users. Projections indicate robust growth across all segments, with particular acceleration anticipated in cloud-based solutions and managed services, driven by the increasing demand for scalable and efficient cybersecurity strategies. Competitive dynamics are intense, with both global and regional players vying for market share.

Key Drivers of Middle East and Africa Cybersecurity Industry Growth

Several factors are propelling the growth of the MEA cybersecurity industry. Firstly, the escalating frequency and sophistication of cyberattacks, including ransomware, phishing, and data breaches, are compelling organizations across all sectors to enhance their defenses. Secondly, rapid digitalization and digital transformation initiatives across governments and private enterprises are expanding the attack surface, necessitating robust security measures. Thirdly, evolving regulatory frameworks and data privacy laws in countries like the UAE and Saudi Arabia are mandating compliance, thereby driving investments in cybersecurity solutions. Lastly, increasing awareness of the economic and reputational damage associated with cyber incidents is fostering a proactive approach to security.

Challenges in the Middle East and Africa Cybersecurity Industry Sector

Despite the robust growth, the MEA cybersecurity sector faces several challenges. A significant hurdle is the shortage of skilled cybersecurity professionals, which limits the ability of organizations to effectively manage and operate advanced security solutions. Regulatory fragmentation across different MEA countries can create complexities for businesses operating regionally, requiring diverse compliance strategies. Furthermore, the high cost of implementing and maintaining advanced cybersecurity solutions can be a barrier for small and medium-sized enterprises (SMEs). Supply chain vulnerabilities in the technology sector can also impact the availability and timely deployment of critical security hardware and software. The competitive pressure from numerous vendors offering overlapping solutions can also lead to market confusion.

Emerging Opportunities in Middle East and Africa Cybersecurity Industry

The MEA cybersecurity industry is ripe with emerging opportunities. The increasing adoption of IoT devices in smart cities and industrial settings presents a significant need for specialized IoT security solutions. The growing focus on cloud security, particularly for hybrid and multi-cloud environments, offers substantial potential for service providers and platform vendors. The demand for cybersecurity training and awareness programs is also on the rise, creating opportunities for specialized educational and consulting services. Furthermore, emerging economies within Africa are rapidly adopting digital technologies, creating nascent but rapidly growing markets for cybersecurity solutions. The increasing threat of nation-state attacks also fuels the demand for advanced threat intelligence and nation-state level cybersecurity services.

Leading Players in the Middle East and Africa Cybersecurity Industry Market

- Paramount Computer Systems LLC

- FireEye Inc

- IBM Corporation

- Trend Micro Inc

- Kaspersky Lab

- Check Point Software Technologies Ltd

- Cisco Systems Inc

- Broadcom Inc (Symantec Corporation)

- DTS Solutions In

- Palo Alto Networks Inc

- Dell Technologies

Key Developments in Middle East and Africa Cybersecurity Industry Industry

- February 2023: Mastercard partnered with Nigeria-based digital payment startup NowNow to help SMEs avoid the risk of cyberattacks. The alliance aims to provide free resources to SMEs for education and strengthening their cybersecurity ecosystem. NowNow conducts regular web application penetration tests to protect SMEs' applications from cyber threats.

- January 2023: Tata Communications International Pte Ltd, a subsidiary of Tata Communications Ltd, expanded its collaboration with Intertec Systems, a UAE-based system integrator, to offer managed services in the region. Tata Communications contributes its Cyber Security Operations Centre (SOC) and managed security services to bolster regional firms' cyber defenses.

Strategic Outlook for Middle East and Africa Cybersecurity Industry Market

The strategic outlook for the Middle East and Africa cybersecurity industry is exceptionally promising, driven by the imperative for robust digital protection in an increasingly interconnected world. Key growth catalysts include the ongoing digital transformation agendas of regional governments, the accelerating adoption of cloud and hybrid cloud infrastructures, and the continuous evolution of sophisticated cyber threats. Organizations are expected to increasingly prioritize integrated cybersecurity platforms that offer comprehensive threat intelligence, proactive vulnerability management, and agile response capabilities. The burgeoning demand for managed security services will continue to shape the market, addressing the persistent skills gap. Furthermore, strategic partnerships and M&A activities will likely intensify as major players seek to consolidate their market positions and expand their service offerings, creating a more mature and resilient cybersecurity ecosystem across the MEA region.

Middle East and Africa Cybersecurity Industry Segmentation

-

1. Solution

- 1.1. Threat Intelligence and Response Management

- 1.2. Identity and Access Management

- 1.3. Data Loss Prevention Management

- 1.4. Security and Vulnerability Management

- 1.5. Unified Threat Management

- 1.6. Enterprise Risk and Compliance

-

2. Service

- 2.1. Managed Services

- 2.2. Professional Services

-

3. Deployment

- 3.1. Cloud

- 3.2. On-premise

-

4. End User

- 4.1. Aerospace and Defense

- 4.2. BFSI

- 4.3. Healthcare

- 4.4. Manufacturing

- 4.5. Retail

- 4.6. Government

- 4.7. IT and Telecommunication

- 4.8. Other End users

Middle East and Africa Cybersecurity Industry Segmentation By Geography

-

1. Middle East

- 1.1. Saudi Arabia

- 1.2. United Arab Emirates

- 1.3. Israel

- 1.4. Qatar

- 1.5. Kuwait

- 1.6. Oman

- 1.7. Bahrain

- 1.8. Jordan

- 1.9. Lebanon

Middle East and Africa Cybersecurity Industry Regional Market Share

Geographic Coverage of Middle East and Africa Cybersecurity Industry

Middle East and Africa Cybersecurity Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.42% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Solution

- 5.1.1. Threat Intelligence and Response Management

- 5.1.2. Identity and Access Management

- 5.1.3. Data Loss Prevention Management

- 5.1.4. Security and Vulnerability Management

- 5.1.5. Unified Threat Management

- 5.1.6. Enterprise Risk and Compliance

- 5.2. Market Analysis, Insights and Forecast - by Service

- 5.2.1. Managed Services

- 5.2.2. Professional Services

- 5.3. Market Analysis, Insights and Forecast - by Deployment

- 5.3.1. Cloud

- 5.3.2. On-premise

- 5.4. Market Analysis, Insights and Forecast - by End User

- 5.4.1. Aerospace and Defense

- 5.4.2. BFSI

- 5.4.3. Healthcare

- 5.4.4. Manufacturing

- 5.4.5. Retail

- 5.4.6. Government

- 5.4.7. IT and Telecommunication

- 5.4.8. Other End users

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Solution

- 6. Middle East and Africa Cybersecurity Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Solution

- 6.1.1. Threat Intelligence and Response Management

- 6.1.2. Identity and Access Management

- 6.1.3. Data Loss Prevention Management

- 6.1.4. Security and Vulnerability Management

- 6.1.5. Unified Threat Management

- 6.1.6. Enterprise Risk and Compliance

- 6.2. Market Analysis, Insights and Forecast - by Service

- 6.2.1. Managed Services

- 6.2.2. Professional Services

- 6.3. Market Analysis, Insights and Forecast - by Deployment

- 6.3.1. Cloud

- 6.3.2. On-premise

- 6.4. Market Analysis, Insights and Forecast - by End User

- 6.4.1. Aerospace and Defense

- 6.4.2. BFSI

- 6.4.3. Healthcare

- 6.4.4. Manufacturing

- 6.4.5. Retail

- 6.4.6. Government

- 6.4.7. IT and Telecommunication

- 6.4.8. Other End users

- 6.1. Market Analysis, Insights and Forecast - by Solution

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Paramount Computer Systems LLC

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 FireEye Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 IBM Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Trend Micro Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Kaspersky Lab

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Check Point Software Technologies Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Cisco Systems Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Broadcom Inc (Symantec Corporation)

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 DTS Solutions In

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Palo Alto Networks Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Dell Technologies

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 Paramount Computer Systems LLC

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Middle East and Africa Cybersecurity Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Middle East and Africa Cybersecurity Industry Share (%) by Company 2025

List of Tables

- Table 1: Middle East and Africa Cybersecurity Industry Revenue Million Forecast, by Solution 2020 & 2033

- Table 2: Middle East and Africa Cybersecurity Industry Revenue Million Forecast, by Service 2020 & 2033

- Table 3: Middle East and Africa Cybersecurity Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 4: Middle East and Africa Cybersecurity Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 5: Middle East and Africa Cybersecurity Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Middle East and Africa Cybersecurity Industry Revenue Million Forecast, by Solution 2020 & 2033

- Table 7: Middle East and Africa Cybersecurity Industry Revenue Million Forecast, by Service 2020 & 2033

- Table 8: Middle East and Africa Cybersecurity Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 9: Middle East and Africa Cybersecurity Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 10: Middle East and Africa Cybersecurity Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 11: Saudi Arabia Middle East and Africa Cybersecurity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: United Arab Emirates Middle East and Africa Cybersecurity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Israel Middle East and Africa Cybersecurity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Qatar Middle East and Africa Cybersecurity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Kuwait Middle East and Africa Cybersecurity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Oman Middle East and Africa Cybersecurity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Bahrain Middle East and Africa Cybersecurity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Jordan Middle East and Africa Cybersecurity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Lebanon Middle East and Africa Cybersecurity Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Middle East and Africa Cybersecurity Industry?

The projected CAGR is approximately 12.42%.

2. Which companies are prominent players in the Middle East and Africa Cybersecurity Industry?

Key companies in the market include Paramount Computer Systems LLC, FireEye Inc, IBM Corporation, Trend Micro Inc, Kaspersky Lab, Check Point Software Technologies Ltd, Cisco Systems Inc, Broadcom Inc (Symantec Corporation), DTS Solutions In, Palo Alto Networks Inc, Dell Technologies.

3. What are the main segments of the Middle East and Africa Cybersecurity Industry?

The market segments include Solution, Service, Deployment , End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.91 Million as of 2022.

5. What are some drivers contributing to market growth?

Rapidly Increasing Cyber Security Incidents; Consistent Threats From the Underground Market.

6. What are the notable trends driving market growth?

Cloud Segment is expected to grow at a higher pace..

7. Are there any restraints impacting market growth?

Lack of Cyber Security Professionals; High Reliance on Traditional Authentication Methods and Low Preparedness.

8. Can you provide examples of recent developments in the market?

February 2023: Mastercard has partnered with Nigeria-based digital payment startup NowNow to help SMEs avoid the risk of cyberattacks. The alliance intends to accomplish this by giving free resources to SMEs to assist in educating and strengthening their cybersecurity ecosystem. Through regular web application penetration tests, NowNow strives to protect SMEs. Such checks guarantee that SMEs' apps are not vulnerable to cyber threats.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Middle East and Africa Cybersecurity Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Middle East and Africa Cybersecurity Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Middle East and Africa Cybersecurity Industry?

To stay informed about further developments, trends, and reports in the Middle East and Africa Cybersecurity Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence