Key Insights

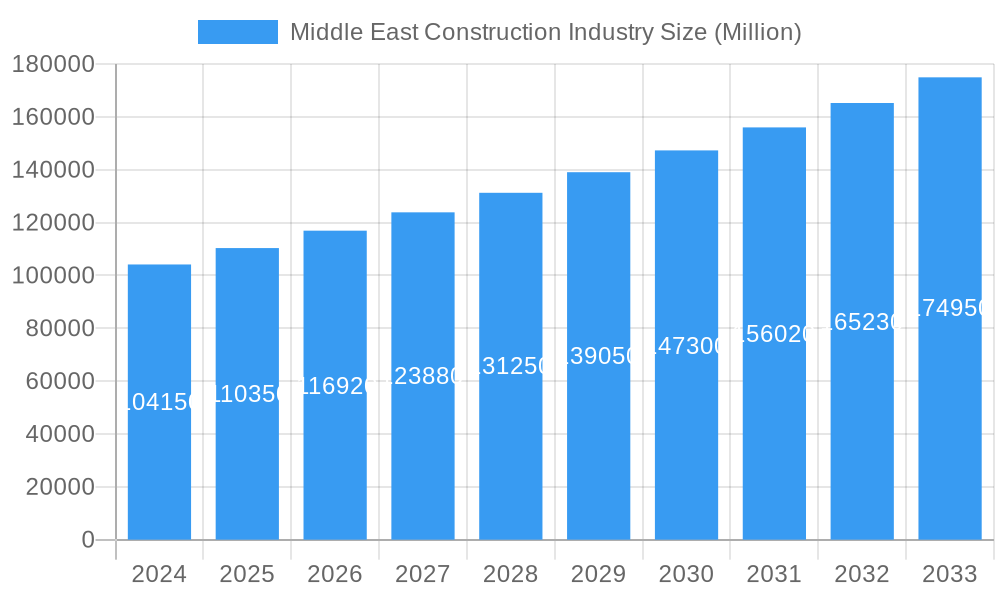

The Middle East construction industry is poised for substantial growth, with the market size estimated at 104.15 billion in 2024 and projected to expand at a robust CAGR of 5.89% through 2033. This upward trajectory is propelled by a confluence of strategic initiatives and burgeoning demand across various sectors. Key drivers include significant government investments in infrastructure development, particularly in the lead-up to major international events and long-term economic diversification plans like Saudi Vision 2030 and the UAE's own ambitious projects. The region's focus on smart city development, sustainable building practices, and a growing population further fuels the demand for construction materials and services. Innovations in construction technology, such as prefabrication and modular construction, are also contributing to efficiency and cost-effectiveness, bolstering market expansion. The increasing adoption of advanced materials like polymers and specialized metals in roofing and structural applications, driven by their durability and aesthetic appeal, is a notable trend.

Middle East Construction Industry Market Size (In Billion)

The market is segmented by materials such as bitumen, rubber, metal, and polymer, catering to diverse end-user needs in residential, commercial, and industrial sectors. While the overall outlook is positive, certain restraints may emerge, including fluctuating raw material prices and geopolitical uncertainties that can impact investment flows. However, the persistent commitment to developing world-class infrastructure, coupled with a strong emphasis on creating sustainable and resilient built environments, ensures a dynamic and evolving market landscape. Companies like Gautruss Pty Ltd, Corrugated Sheet Ltd, Clotan Steel, and Palram Industries Ltd are actively shaping this market through their innovative product offerings and strategic regional presence. The Middle East, with Saudi Arabia and the United Arab Emirates leading the charge, represents a critical hub for this expansion, with significant opportunities across its diverse economic activities.

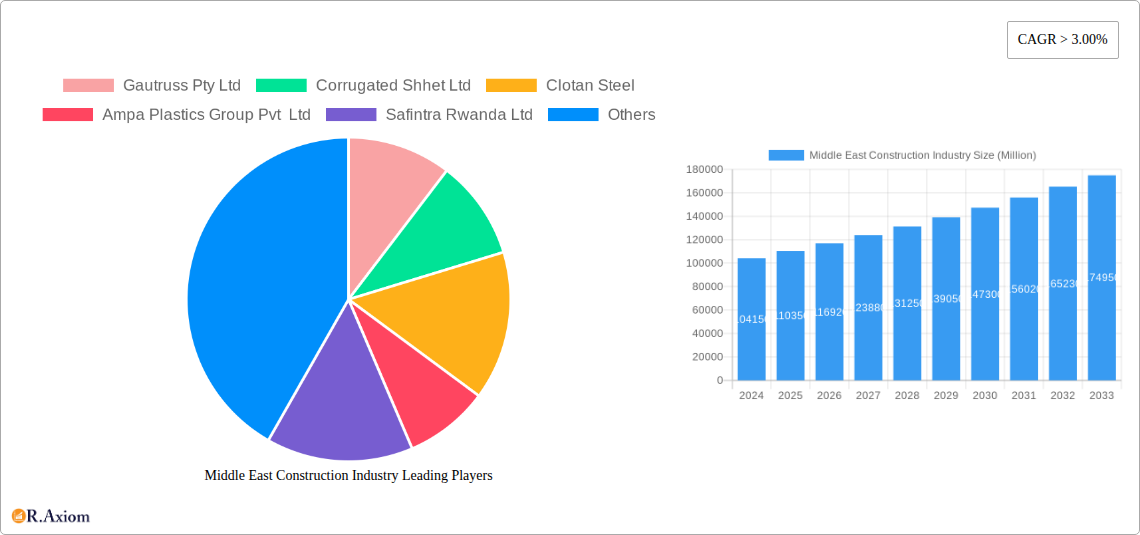

Middle East Construction Industry Company Market Share

This in-depth report provides a definitive analysis of the Middle East construction industry, a dynamic sector valued in billions of dollars, encompassing intricate market dynamics, emerging trends, and future growth trajectories. Spanning a study period from 2019 to 2033, with a base year of 2025 and an estimated year of 2025, this report delves into historical performance (2019-2024) and offers robust forecasts for the 2025-2033 period. With a focus on high-traffic keywords, this report is designed to enhance search visibility and engage all industry stakeholders, from material suppliers to end-users and leading construction firms.

Middle East Construction Industry Market Concentration & Innovation

The Middle East construction industry exhibits a moderate to high market concentration, driven by the significant capital investment required for large-scale projects and the influence of government-backed initiatives. Key innovation drivers include the adoption of sustainable building materials, advanced prefabrication techniques, and smart building technologies aimed at improving efficiency and reducing environmental impact. Regulatory frameworks, particularly concerning building codes, safety standards, and sustainability mandates, play a crucial role in shaping market entry and operational strategies. Product substitutes, such as alternative roofing materials and façade systems, are increasingly challenging traditional offerings, forcing manufacturers to focus on value-added solutions and performance enhancements. End-user trends are shifting towards demand for energy-efficient homes, flexible commercial spaces, and technologically integrated industrial facilities. Mergers and acquisition (M&A) activities are observed, with deal values estimated in the hundreds of billions of dollars, indicating a consolidation trend as larger players seek to expand their market share and capabilities. For instance, acquisitions of specialized engineering firms or material suppliers are strategic moves to bolster portfolios and address evolving project demands.

Middle East Construction Industry Industry Trends & Insights

The Middle East construction industry is experiencing robust growth, projected to witness a Compound Annual Growth Rate (CAGR) of approximately 8.5% over the forecast period. This expansion is primarily fueled by significant government investments in infrastructure development, including ambitious smart city projects, transportation networks, and renewable energy facilities. The region's focus on economic diversification away from oil and gas is a paramount growth driver, leading to substantial capital allocation in tourism, hospitality, and real estate sectors. Technological disruptions are rapidly transforming the construction landscape. The increasing adoption of Building Information Modeling (BIM) enhances project planning, collaboration, and lifecycle management, leading to improved cost control and reduced timelines. Drones are being utilized for site surveying, progress monitoring, and safety inspections, boosting operational efficiency. 3D printing technology, while still nascent, holds immense potential for rapid prototyping and on-site construction of complex structures, reducing waste and labor costs.

Consumer preferences are evolving, with a growing demand for sustainable, energy-efficient, and technologically advanced buildings. This includes a rise in demand for green building certifications and smart home features in the residential sector. In the commercial space, flexibility and adaptability are key, with businesses seeking spaces that can be easily reconfigured to meet changing operational needs. The industrial sector is witnessing a push towards highly automated and data-driven facilities. Competitive dynamics are intensifying, with both local and international players vying for market share. Companies are increasingly differentiating themselves through innovation, specialization, and the ability to deliver complex, large-scale projects. Market penetration for advanced construction technologies is steadily increasing, driven by their proven ability to deliver tangible benefits in terms of cost savings, time efficiency, and enhanced project quality. The integration of digital platforms for project management and supply chain optimization is becoming a standard practice.

Dominant Markets & Segments in Middle East Construction Industry

The Metal segment is a dominant force within the Middle East construction industry, particularly in steel and aluminum products, driven by their widespread application in structural components, roofing, facades, and interior finishing across all end-user segments. Economic policies promoting industrialization and infrastructure development, such as those seen in Saudi Arabia's Vision 2030 and the UAE's National Industrial Strategy, directly bolster demand for metal construction materials.

- Key Drivers for Metal Dominance:

- Infrastructure Projects: Large-scale projects like new airports, high-speed rail networks, and urban regeneration schemes heavily rely on steel and other metals for structural integrity and durability.

- Economic Diversification: Initiatives encouraging manufacturing and industrial growth necessitate significant use of metal in factory construction and expansion.

- Durability and Strength: Metal's inherent properties make it ideal for the region's climatic conditions and for constructing resilient structures.

- Aesthetics and Design Flexibility: Modern architectural designs often incorporate metal for its sleek appearance and versatility.

The Commercial end-user segment is another area of significant dominance. Driven by substantial investments in tourism, retail, and hospitality infrastructure, the demand for office buildings, shopping malls, hotels, and entertainment venues is consistently high. The UAE and Saudi Arabia are at the forefront of this growth, with mega-developments and the hosting of major global events acting as powerful catalysts.

- Key Drivers for Commercial Dominance:

- Tourism and Hospitality Boom: Ambitious tourism strategies are leading to the construction of numerous hotels, resorts, and entertainment complexes.

- Retail Expansion: The growing middle class and increasing disposable incomes fuel the demand for modern retail spaces and shopping centers.

- Corporate Headquarters: As regional economies grow, there is a continuous need for new and upgraded corporate office spaces.

- Urban Development: Redevelopment of city centers and the creation of new business districts contribute significantly to commercial construction activity.

Within the Material segment, Polymer-based products, including advanced plastics and composites, are demonstrating substantial growth, driven by their lightweight nature, durability, and versatility in applications ranging from insulation and piping to facades and interior finishes.

- Key Drivers for Polymer Growth:

- Innovation in Building Materials: Development of high-performance polymers for enhanced insulation and weather resistance.

- Cost-Effectiveness: Polymers often offer a more economical alternative to traditional materials without compromising performance.

- Ease of Installation: Their lightweight nature simplifies logistics and construction processes.

The Industrial end-user segment is also a key contributor, with ongoing investments in manufacturing facilities, logistics hubs, and energy infrastructure, particularly in sectors like petrochemicals, renewable energy, and advanced manufacturing.

- Key Drivers for Industrial Sector Growth:

- Petrochemical Expansion: Continued investment in refining and petrochemical plants.

- Renewable Energy Projects: Development of solar and wind power facilities requiring substantial construction.

- Logistics and Warehousing: Growth in e-commerce and trade necessitates expanded logistics and warehousing infrastructure.

Middle East Construction Industry Product Developments

Product developments in the Middle East construction industry are increasingly focused on sustainability, efficiency, and smart integration. Innovations include advanced composite materials offering superior strength-to-weight ratios, reducing structural load and material usage. High-performance insulation products made from recycled polymers are gaining traction, addressing the region's significant cooling demands and energy efficiency goals. Smart roofing solutions incorporating integrated solar panels and intelligent water management systems are emerging. Furthermore, advancements in prefabrication and modular construction techniques are enabling faster project delivery and improved quality control. The competitive advantage lies in offering products that meet stringent environmental regulations, reduce operational costs for end-users, and contribute to the aesthetic and functional appeal of modern infrastructure.

Report Scope & Segmentation Analysis

This report meticulously segments the Middle East construction industry across key material types and end-user applications. The material segmentation includes Bitumen, Rubber, Metal, and Polymer. The end-user segmentation covers Residential, Commercial, and Industrial sectors.

Bitumen: Market size estimated in hundreds of billions of dollars, with steady growth driven by infrastructure projects and the use in roofing and paving.

Rubber: Market size in hundreds of billions of dollars, with growth fueled by applications in waterproofing, vibration dampening, and industrial flooring.

Metal: Dominant segment, market size in billions of dollars, driven by structural applications and infrastructure development, with strong growth projections.

Polymer: High growth segment, market size in hundreds of billions of dollars, driven by innovation in insulation, piping, and façade systems.

Residential: Market size in billions of dollars, characterized by increasing demand for affordable housing and premium smart homes, with moderate growth.

Commercial: Significant market size in billions of dollars, experiencing robust growth due to tourism, retail, and hospitality development.

Industrial: Market size in billions of dollars, with strong growth driven by manufacturing, logistics, and energy sector investments.

Key Drivers of Middle East Construction Industry Growth

The Middle East construction industry is propelled by a confluence of powerful drivers. Economic diversification initiatives, particularly in Saudi Arabia and the UAE, are a primary catalyst, channeling billions into non-oil sectors. Ambitious government infrastructure spending, encompassing mega-projects like NEOM, Riyadh Metro, and Expo City Dubai, creates substantial demand for construction services and materials. The burgeoning tourism and hospitality sectors, coupled with a growing population, fuel residential and commercial construction. Technological advancements, including BIM and prefabrication, are enhancing project efficiency and cost-effectiveness. Furthermore, a growing emphasis on sustainability and green building standards is driving innovation in material selection and construction practices.

Challenges in the Middle East Construction Industry Sector

Despite its growth, the Middle East construction industry faces several challenges. Fluctuations in commodity prices, particularly oil, can impact government spending and project pipelines, although diversification efforts are mitigating this risk. Supply chain disruptions and the reliance on imported materials can lead to cost overruns and delays. Intense competition among a large number of players, including international firms, can put pressure on profit margins. Labor shortages and the need for skilled workers, especially in specialized areas, remain a concern. Regulatory complexities and evolving building codes require continuous adaptation from construction firms. The significant capital investment required for projects also poses a financial hurdle for smaller entities.

Emerging Opportunities in Middle East Construction Industry

Emerging opportunities in the Middle East construction industry are abundant and diverse. The ongoing development of smart cities presents a significant avenue for growth, demanding innovative construction solutions and integrated technologies. The renewable energy sector, with its focus on solar and wind power, requires substantial infrastructure development. The growing demand for sustainable and green buildings offers opportunities for companies specializing in eco-friendly materials and construction techniques. The rise of e-commerce is driving the need for advanced logistics and warehousing facilities. Furthermore, the increasing focus on retrofitting and upgrading existing infrastructure provides a consistent stream of renovation and refurbishment projects, valued in billions.

Leading Players in the Middle East Construction Industry Market

- Gautruss Pty Ltd

- Corrugated Shhet Ltd

- Clotan Steel

- Ampa Plastics Group Pvt Ltd

- Safintra Rwanda Ltd

- Algoa Steel & Roofing

- Kirby International (List Not Exhaustive)

- Al Shafar Steel Engineering

- Palram Industries Ltd

- Youngman

Key Developments in Middle East Construction Industry Industry

- 2023/Q1: Launch of major infrastructure projects in Saudi Arabia, including expansions to the Red Sea Project and AMAALA, injecting billions into the construction sector.

- 2023/Q2: Increased adoption of modular construction techniques by several key players in the UAE to expedite housing and commercial developments, valued in billions.

- 2023/Q3: Significant investment in smart building technologies and IoT integration across commercial and residential projects in Qatar, with an estimated market impact in billions.

- 2023/Q4: Announcement of new sustainability regulations for construction materials in Oman, driving demand for eco-friendly product innovations.

- 2024/Q1: Mergers and acquisitions activity intensifies, with several regional steel manufacturers consolidating to enhance production capacity and market reach, deal values in billions.

- 2024/Q2: Introduction of advanced prefabrication solutions for industrial facilities in Bahrain, promising faster project completion times and cost savings in billions.

- 2024/Q3: Growing trend towards the use of recycled construction materials in large-scale public works in Kuwait, reflecting a push for circular economy principles.

- 2024/Q4: Expansion of BIM adoption across all major project types in Jordan, leading to improved project management and reduced waste, with an estimated market benefit in billions.

Strategic Outlook for Middle East Construction Industry Market

The strategic outlook for the Middle East construction industry remains exceptionally strong, underpinned by a sustained commitment to economic diversification and mega-infrastructure development. Future growth will be driven by continued investment in smart cities, renewable energy, and advanced manufacturing facilities, creating demand valued in billions of dollars. The increasing focus on sustainability and energy efficiency presents significant opportunities for companies offering green building solutions and innovative materials. Technological adoption, particularly in areas like AI-driven project management and automated construction, will be crucial for maintaining a competitive edge. Strategic partnerships and M&A activities are expected to continue as companies seek to consolidate expertise and expand their service offerings, further shaping the market landscape.

Middle East Construction Industry Segmentation

-

1. Material

- 1.1. Bitumen

- 1.2. Rubber

- 1.3. Metal

- 1.4. Polymer

-

2. End User

- 2.1. Residential

- 2.2. Commercial

- 2.3. Industrial

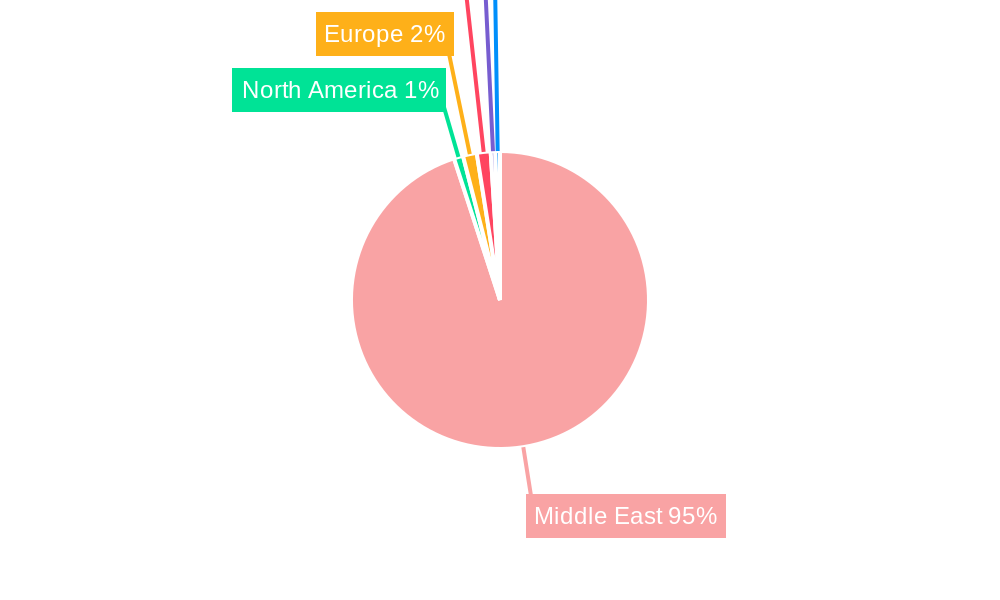

Middle East Construction Industry Segmentation By Geography

-

1. Middle East

- 1.1. Saudi Arabia

- 1.2. United Arab Emirates

- 1.3. Israel

- 1.4. Qatar

- 1.5. Kuwait

- 1.6. Oman

- 1.7. Bahrain

- 1.8. Jordan

- 1.9. Lebanon

Middle East Construction Industry Regional Market Share

Geographic Coverage of Middle East Construction Industry

Middle East Construction Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.89% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material

- 5.1.1. Bitumen

- 5.1.2. Rubber

- 5.1.3. Metal

- 5.1.4. Polymer

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Residential

- 5.2.2. Commercial

- 5.2.3. Industrial

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Material

- 6. Middle East Construction Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material

- 6.1.1. Bitumen

- 6.1.2. Rubber

- 6.1.3. Metal

- 6.1.4. Polymer

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Residential

- 6.2.2. Commercial

- 6.2.3. Industrial

- 6.1. Market Analysis, Insights and Forecast - by Material

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Gautruss Pty Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Corrugated Shhet Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Clotan Steel

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Ampa Plastics Group Pvt Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Safintra Rwanda Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Algoa Steel & Roofing

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Kirby International**List Not Exhaustive

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Al Shafar Steel Engineering

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Palram Industries Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Youngman

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Gautruss Pty Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Middle East Construction Industry Revenue Breakdown (undefined, %) by Product 2025 & 2033

- Figure 2: Middle East Construction Industry Share (%) by Company 2025

List of Tables

- Table 1: Middle East Construction Industry Revenue undefined Forecast, by Material 2020 & 2033

- Table 2: Middle East Construction Industry Revenue undefined Forecast, by End User 2020 & 2033

- Table 3: Middle East Construction Industry Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Middle East Construction Industry Revenue undefined Forecast, by Material 2020 & 2033

- Table 5: Middle East Construction Industry Revenue undefined Forecast, by End User 2020 & 2033

- Table 6: Middle East Construction Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: Saudi Arabia Middle East Construction Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: United Arab Emirates Middle East Construction Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Israel Middle East Construction Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Qatar Middle East Construction Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 11: Kuwait Middle East Construction Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 12: Oman Middle East Construction Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 13: Bahrain Middle East Construction Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Jordan Middle East Construction Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Lebanon Middle East Construction Industry Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Middle East Construction Industry?

The projected CAGR is approximately 5.89%.

2. Which companies are prominent players in the Middle East Construction Industry?

Key companies in the market include Gautruss Pty Ltd, Corrugated Shhet Ltd, Clotan Steel, Ampa Plastics Group Pvt Ltd, Safintra Rwanda Ltd, Algoa Steel & Roofing, Kirby International**List Not Exhaustive, Al Shafar Steel Engineering, Palram Industries Ltd, Youngman.

3. What are the main segments of the Middle East Construction Industry?

The market segments include Material, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

4.; Rapid Urabanization4.; Increasing government investments.

6. What are the notable trends driving market growth?

Construction Activities Playing a Significant Role in the Construction Sheets Market.

7. Are there any restraints impacting market growth?

4.; Increasing cost of raw materials affecting the construction industry4.; Slowdown in economic growth affecting the market.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Middle East Construction Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Middle East Construction Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Middle East Construction Industry?

To stay informed about further developments, trends, and reports in the Middle East Construction Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence