Key Insights

The multi-tenant data center industry is poised for robust expansion, driven by the escalating demand for flexible, scalable, and cost-effective IT infrastructure solutions. The market is currently valued at an estimated $38.7 billion in 2024, with a projected Compound Annual Growth Rate (CAGR) of 6% through 2033. This substantial growth is fueled by several key factors, including the pervasive adoption of cloud computing models (both public and private), the burgeoning volume of data generated by digital transformation initiatives across various sectors, and the increasing need for colocation services to house critical IT equipment. Enterprises across industries such as IT & Telecom, Healthcare, Defense, Manufacturing, and Retail are increasingly relying on multi-tenant data centers to manage their IT infrastructure efficiently, reducing capital expenditure and operational overhead. This shift is further amplified by the growing trend of edge computing, requiring decentralized data processing capabilities.

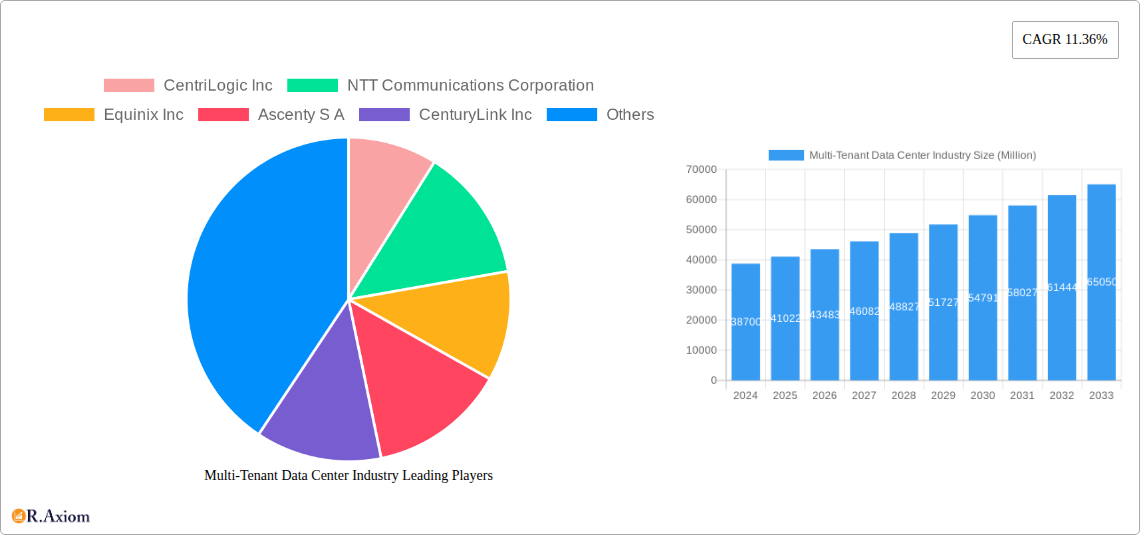

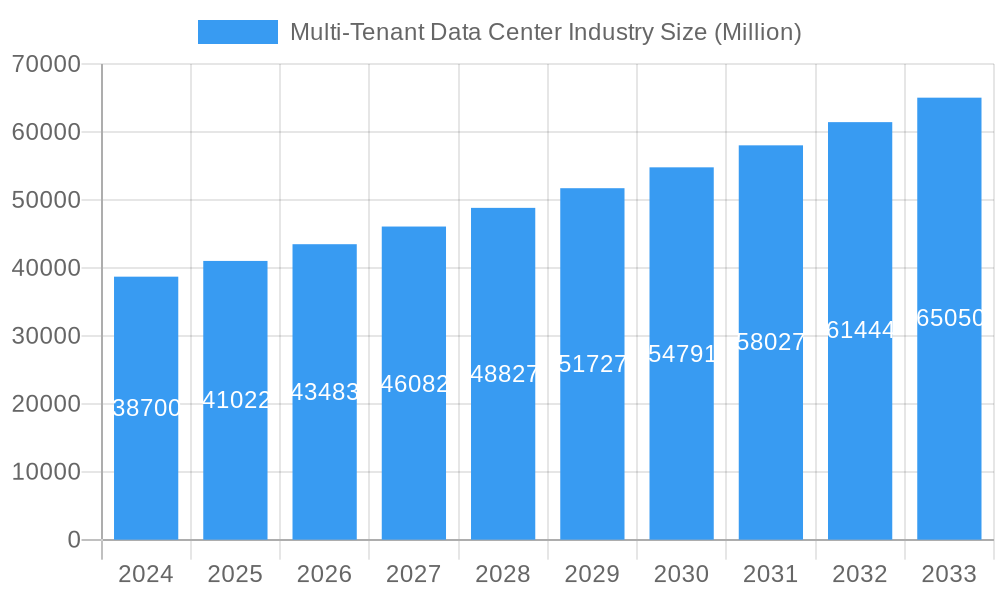

Multi-Tenant Data Center Industry Market Size (In Billion)

The multi-tenant data center market is characterized by distinct segments, including Retail Colocation and Wholesale Colocation, catering to a diverse range of customer needs, from smaller deployments to large-scale enterprise requirements. Leading companies such as Equinix Inc., NTT Communications Corporation, and IBM Corporation are at the forefront of this market, investing heavily in expanding their global footprints and enhancing their service offerings. While the market benefits from strong growth drivers, it also faces certain restraints, such as high capital investment for data center construction and the need to comply with stringent data privacy regulations in different regions. Geographically, North America and Europe currently dominate the market, but the Asia Pacific region is emerging as a significant growth area due to rapid digital adoption and increasing investments in cloud infrastructure. Ongoing technological advancements, including AI and IoT, are expected to further propel the demand for advanced colocation services, ensuring sustained market vitality.

Multi-Tenant Data Center Industry Company Market Share

Here's an SEO-optimized, detailed report description for the Multi-Tenant Data Center Industry, designed for immediate use without modification:

Multi-Tenant Data Center Industry Market Concentration & Innovation

This report delves into the intricate market concentration and innovation landscape of the multi-tenant data center industry, a sector projected to reach a valuation of over $200 billion by 2033. Analyzing the period from 2019 to 2033, with a base year of 2025, we dissect key drivers of innovation, including advancements in cloud computing, AI, and edge technologies. Regulatory frameworks governing data privacy and security, such as GDPR and CCPA, are examined for their impact on operational strategies and market entry. The report identifies and evaluates product substitutes, including on-premises data centers and hybrid cloud solutions, and assesses their evolving competitive standing. End-user trends, such as the escalating demand for hyperscale capacity and the growing adoption of colocation by enterprises across various sectors, are highlighted. Mergers and acquisitions (M&A) activities are a critical component of market consolidation, with a focus on significant deal values exceeding $1 billion in recent years. The competitive landscape is shaped by a dynamic interplay of established players and emerging providers, driving continuous investment in capacity expansion and technological upgrades. Understanding these factors is crucial for stakeholders navigating the evolving multi-tenant data center market.

- Market Share Dynamics: Analysis of leading companies' market share in retail and wholesale colocation segments.

- Innovation Drivers: Identification of technological advancements fueling market growth, such as liquid cooling and advanced power management.

- Regulatory Impact: Assessment of how evolving data sovereignty laws influence data center development and operations.

- M&A Landscape: Examination of significant acquisition activities and their impact on market concentration, with deal values often in the multi-billion dollar range.

Multi-Tenant Data Center Industry Industry Trends & Insights

The multi-tenant data center industry is experiencing a period of unprecedented growth, fueled by a confluence of robust market drivers, transformative technological disruptions, evolving consumer preferences, and intense competitive dynamics. The historical period of 2019-2024 witnessed a steady expansion, with the forecast period of 2025-2033 anticipating an accelerated growth trajectory. The Compound Annual Growth Rate (CAGR) is projected to be robust, estimated at over 15%, reflecting the insatiable demand for digital infrastructure. Market penetration for colocation services is rapidly increasing across all end-user industries, driven by the critical need for scalable, secure, and cost-effective data storage and processing capabilities. Key growth catalysts include the exponential rise in data generation from IoT devices, the widespread adoption of AI and machine learning, the continuous expansion of public and private cloud services, and the increasing complexity of cybersecurity threats that necessitate specialized infrastructure. Furthermore, the digital transformation initiatives undertaken by governments and enterprises globally are directly translating into higher demand for multi-tenant data center capacity. The industry is also witnessing a significant push towards sustainability, with a growing emphasis on renewable energy sources and energy-efficient designs, influencing investment decisions and operational strategies. The competitive landscape is characterized by strategic partnerships, capacity expansions, and a focus on delivering value-added services beyond basic colocation, such as connectivity, managed services, and specialized cloud interconnectivity. This dynamic environment presents both immense opportunities and strategic challenges for market participants aiming to capture a significant share of this burgeoning market.

Dominant Markets & Segments in Multi-Tenant Data Center Industry

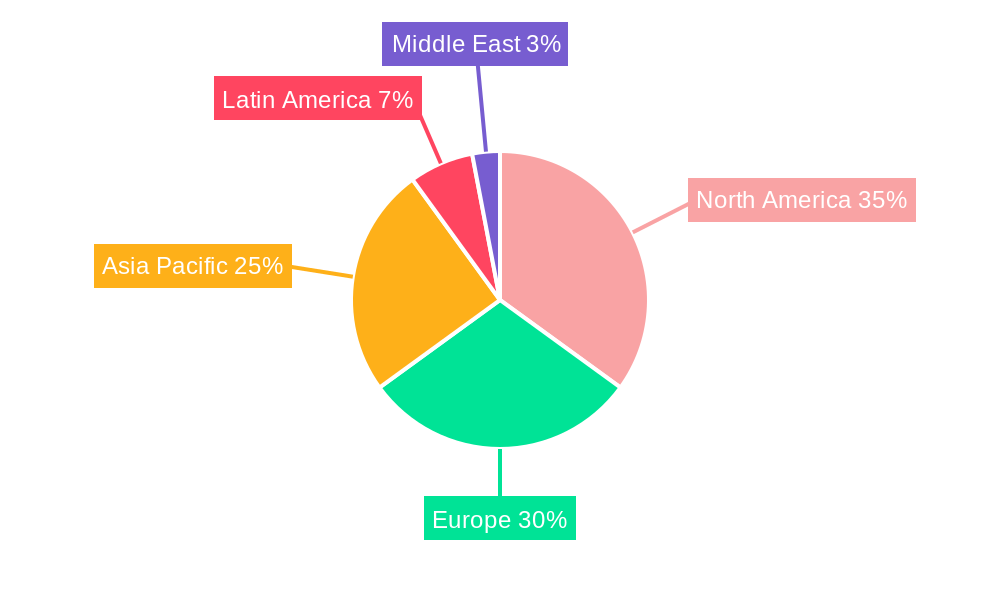

The multi-tenant data center industry is characterized by diverse regional dominance and segment specialization. North America, particularly the United States, currently stands as the dominant market, driven by its mature digital economy, extensive cloud infrastructure, and significant enterprise adoption of colocation services. Key drivers for this dominance include proactive economic policies supporting technology infrastructure development, substantial investments in fiber optic networks, and a high concentration of major technology companies and financial institutions.

Solution Type Dominance:

- Wholesale Colocation: This segment exhibits strong growth, especially in North America and Europe, catering to hyperscale cloud providers and large enterprises requiring substantial, dedicated infrastructure. The demand for hyperscale data centers, often exceeding 10 megawatts (MW) of capacity, is a significant growth driver.

- Retail Colocation: While wholesale dominates in terms of capacity, retail colocation is crucial for a wider range of businesses, including SMEs, offering flexible space, power, and cooling solutions. Its growth is propelled by the increasing need for localized edge computing and proximity to end-users.

Application Dominance:

- Public Cloud: The overwhelming demand for public cloud services is the primary growth engine for multi-tenant data centers. Hyperscalers like Google, AWS, and Microsoft Azure rely heavily on colocation facilities to expand their global reach and capacity. Google's investment of $730 million in a Japanese data center by 2023, collaborating with providers like Equinix, exemplifies this trend.

- Private Cloud: While public cloud leads, private cloud adoption remains strong, particularly in sectors with stringent data security and compliance requirements. This includes defense and regulated industries like healthcare.

End-user Industry Dominance:

- IT & Telecom: This sector remains the largest consumer of multi-tenant data center services, driven by the continuous demand for network infrastructure, cloud services, and digital content delivery. The expansion of 5G networks and the increasing reliance on cloud-native applications further bolster this demand.

- Healthcare: Driven by the digitization of patient records, telehealth expansion, and the need for secure data storage, the healthcare sector is a rapidly growing segment. Compliance with regulations like HIPAA is a key consideration, driving demand for secure and reliable colocation.

- Defense: Government and defense organizations increasingly leverage multi-tenant data centers for secure hosting of sensitive data and critical applications, benefiting from robust security measures and geographic redundancy.

- Manufacturing: The adoption of Industry 4.0 technologies, including IoT sensors, AI-driven analytics, and automation, is creating substantial data processing needs, leading manufacturing companies to increasingly utilize colocation facilities.

- Retail: E-commerce growth and the need for enhanced customer experiences are driving retailers to invest in robust IT infrastructure, often through colocation, to support online operations and data analytics.

- Other End-user Industries: Emerging sectors like finance, media, and education are also significant contributors to market growth, driven by their own digital transformation journeys.

Multi-Tenant Data Center Industry Product Developments

Product developments in the multi-tenant data center industry are increasingly focused on enhancing efficiency, security, and sustainability. Innovations include advanced cooling technologies, such as liquid cooling, to support high-density computing environments driven by AI and HPC. The integration of AI for predictive maintenance and operational optimization is becoming standard. Furthermore, the development of modular and pre-fabricated data center solutions enables faster deployment and scalability. Competitive advantages are derived from offering ultra-low latency connectivity, robust cybersecurity features, and compliance certifications for specific industries. The increasing demand for specialized environments, such as those required for quantum computing and edge deployments, is also spurring product innovation. These advancements are critical for meeting the evolving needs of businesses seeking reliable and high-performance digital infrastructure.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the multi-tenant data center industry, segmented across critical categories to offer granular insights. The study period spans from 2019 to 2033, with a base year of 2025 and a forecast period from 2025 to 2033. The segmentation encompasses:

- Solution Type:

- Retail Colocation: This segment is characterized by smaller footprints, offering flexible services to a broad range of businesses. Projected growth is steady, driven by SMEs and niche applications.

- Wholesale Colocation: This segment focuses on larger deployments for hyperscale providers and enterprises. It is expected to experience significant growth, fueled by the demand for massive data processing capabilities.

- Application:

- Public Cloud: This is the largest and fastest-growing segment, driven by the massive adoption of cloud services by businesses of all sizes. Projections indicate continued double-digit growth.

- Private Cloud: While smaller than public cloud, private cloud adoption remains robust, particularly in highly regulated sectors. Its growth is steady, driven by security and compliance needs.

- End-user Industry:

- IT & Telecom: This remains the dominant end-user industry, with sustained high growth driven by ongoing digital transformation and network expansion.

- Healthcare: A rapidly expanding segment, driven by data digitization and telehealth. High growth projections are anticipated due to increasing data needs and regulatory demands.

- Defense: Steady growth is expected, fueled by government investments in secure data infrastructure and critical applications.

- Manufacturing: Significant growth is projected as Industry 4.0 adoption accelerates, creating demand for data processing and analytics.

- Retail: Growth is propelled by e-commerce expansion and the need for data-driven customer insights.

- Other End-user Industries: This broad category includes finance, media, and education, all exhibiting healthy growth as they embrace digital transformation.

Key Drivers of Multi-Tenant Data Center Industry Growth

The multi-tenant data center industry's growth is underpinned by several powerful drivers. The exponential increase in data generation from IoT devices, big data analytics, and digital content consumption necessitates robust and scalable infrastructure. The pervasive adoption of cloud computing, both public and private, directly translates into demand for colocation services. Furthermore, the ongoing digital transformation initiatives across all industries, from healthcare to manufacturing, are accelerating the migration of IT workloads to third-party data centers. Advancements in technologies like Artificial Intelligence (AI), Machine Learning (ML), and High-Performance Computing (HPC) require significant processing power and specialized infrastructure that multi-tenant data centers are well-equipped to provide. Additionally, the increasing need for data sovereignty and compliance with stringent data privacy regulations, such as GDPR, is pushing organizations towards secure and geographically distributed colocation facilities. The shift towards edge computing also contributes, requiring localized data processing closer to end-users.

Challenges in the Multi-Tenant Data Center Industry Sector

Despite its robust growth, the multi-tenant data center industry faces several significant challenges. High capital expenditure for building and maintaining data centers, coupled with rising operational costs including energy consumption, presents a considerable financial hurdle. The escalating demand for power and the increasing focus on sustainability and carbon emissions place pressure on operators to adopt renewable energy sources and improve energy efficiency, which can involve substantial investment. Regulatory hurdles, including complex permitting processes, zoning laws, and evolving data privacy legislation across different jurisdictions, can impede development and expansion. Supply chain disruptions for critical components, such as servers, networking equipment, and power infrastructure, can lead to project delays and cost overruns. Intense competition among existing players and the emergence of new entrants also exert pressure on pricing and profit margins. Furthermore, finding and retaining skilled personnel for the operation and maintenance of advanced data center facilities remains a challenge.

Emerging Opportunities in Multi-Tenant Data Center Industry

The multi-tenant data center industry is ripe with emerging opportunities driven by technological innovation and evolving market demands. The rapid expansion of edge computing presents a significant opportunity for distributed data center deployments closer to end-users, catering to low-latency applications like autonomous vehicles and IoT analytics. The growing demand for specialized infrastructure to support Artificial Intelligence (AI) and High-Performance Computing (HPC) workloads, which require higher power densities and advanced cooling solutions, creates a niche market. The increasing focus on sustainability and the push towards net-zero emissions are driving opportunities for data centers powered by renewable energy sources and utilizing innovative energy-efficient designs. The continued growth of emerging markets, particularly in Asia-Pacific and Latin America, offers substantial expansion potential for data center providers. Furthermore, the convergence of 5G networks and cloud services creates demand for edge data centers that can process and distribute data at unprecedented speeds. The development of smart data centers, leveraging AI for autonomous operations and predictive maintenance, also presents a significant avenue for future growth and competitive differentiation.

Leading Players in the Multi-Tenant Data Center Industry Market

- CentriLogic Inc

- NTT Communications Corporation

- Equinix Inc

- Ascenty S A

- CenturyLink Inc

- IBM Corporation

- Internap Corporation

- Global Switch Ltd

- AT&T Inc

- Rackspace Inc

Key Developments in Multi-Tenant Data Center Industry Industry

- October 2022: Google announced its intention to establish its first data center in Japan by 2023, located in Inzai City, Chiba. This initiative is supported by a USD 730 million infrastructure fund until 2024 and involves collaboration with colocation facility providers like Equinix to power Google Cloud services. The company is also constructing its own data centers to support services like YouTube and Gmail.

- February 2022: Kao Data launched a 16 megawatt (MW) carrier-neutral data center in Slough, West London, following an investment of approximately GBP 130 million from Infratil Limited. This expansion enhances Kao Data's sustainable data center platform in a key global hub, emphasizing high security and energy efficiency.

Strategic Outlook for Multi-Tenant Data Center Industry Market

The strategic outlook for the multi-tenant data center industry is exceptionally strong, driven by a sustained increase in digital data creation and consumption, coupled with the accelerating adoption of cloud services, AI, and IoT. The industry is poised for significant expansion, with a growing emphasis on sustainability and energy efficiency becoming a key differentiator. Future growth will be significantly influenced by the development of edge computing infrastructure to support low-latency applications and the continued demand for hyperscale capacity from major cloud providers. Strategic investments in renewable energy sources, advanced cooling technologies, and robust cybersecurity measures will be crucial for market leadership. Expansion into emerging markets and the development of specialized data center solutions for industries like AI, HPC, and quantum computing represent key opportunities. Furthermore, the increasing need for data sovereignty and compliance will continue to shape the deployment strategies of colocation providers. The industry's trajectory indicates continued innovation and robust demand for digital infrastructure services.

Multi-Tenant Data Center Industry Segmentation

-

1. Solution Type

- 1.1. Retail Colocation

- 1.2. Wholesale Colocation

-

2. Application

- 2.1. Public Cloud

- 2.2. Private Cloud

-

3. End-user Industry

- 3.1. IT & Telecom

- 3.2. Healthcare

- 3.3. Defense

- 3.4. Manufacturing

- 3.5. Retail

- 3.6. Other End-user Industries

Multi-Tenant Data Center Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East

Multi-Tenant Data Center Industry Regional Market Share

Geographic Coverage of Multi-Tenant Data Center Industry

Multi-Tenant Data Center Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 19.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Solution Type

- 5.1.1. Retail Colocation

- 5.1.2. Wholesale Colocation

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Public Cloud

- 5.2.2. Private Cloud

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. IT & Telecom

- 5.3.2. Healthcare

- 5.3.3. Defense

- 5.3.4. Manufacturing

- 5.3.5. Retail

- 5.3.6. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Latin America

- 5.4.5. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Solution Type

- 6. Global Multi-Tenant Data Center Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Solution Type

- 6.1.1. Retail Colocation

- 6.1.2. Wholesale Colocation

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Public Cloud

- 6.2.2. Private Cloud

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. IT & Telecom

- 6.3.2. Healthcare

- 6.3.3. Defense

- 6.3.4. Manufacturing

- 6.3.5. Retail

- 6.3.6. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Solution Type

- 7. North America Multi-Tenant Data Center Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Solution Type

- 7.1.1. Retail Colocation

- 7.1.2. Wholesale Colocation

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Public Cloud

- 7.2.2. Private Cloud

- 7.3. Market Analysis, Insights and Forecast - by End-user Industry

- 7.3.1. IT & Telecom

- 7.3.2. Healthcare

- 7.3.3. Defense

- 7.3.4. Manufacturing

- 7.3.5. Retail

- 7.3.6. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Solution Type

- 8. Europe Multi-Tenant Data Center Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Solution Type

- 8.1.1. Retail Colocation

- 8.1.2. Wholesale Colocation

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Public Cloud

- 8.2.2. Private Cloud

- 8.3. Market Analysis, Insights and Forecast - by End-user Industry

- 8.3.1. IT & Telecom

- 8.3.2. Healthcare

- 8.3.3. Defense

- 8.3.4. Manufacturing

- 8.3.5. Retail

- 8.3.6. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Solution Type

- 9. Asia Pacific Multi-Tenant Data Center Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Solution Type

- 9.1.1. Retail Colocation

- 9.1.2. Wholesale Colocation

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Public Cloud

- 9.2.2. Private Cloud

- 9.3. Market Analysis, Insights and Forecast - by End-user Industry

- 9.3.1. IT & Telecom

- 9.3.2. Healthcare

- 9.3.3. Defense

- 9.3.4. Manufacturing

- 9.3.5. Retail

- 9.3.6. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Solution Type

- 10. Latin America Multi-Tenant Data Center Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Solution Type

- 10.1.1. Retail Colocation

- 10.1.2. Wholesale Colocation

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Public Cloud

- 10.2.2. Private Cloud

- 10.3. Market Analysis, Insights and Forecast - by End-user Industry

- 10.3.1. IT & Telecom

- 10.3.2. Healthcare

- 10.3.3. Defense

- 10.3.4. Manufacturing

- 10.3.5. Retail

- 10.3.6. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Solution Type

- 11. Middle East Multi-Tenant Data Center Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Solution Type

- 11.1.1. Retail Colocation

- 11.1.2. Wholesale Colocation

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Public Cloud

- 11.2.2. Private Cloud

- 11.3. Market Analysis, Insights and Forecast - by End-user Industry

- 11.3.1. IT & Telecom

- 11.3.2. Healthcare

- 11.3.3. Defense

- 11.3.4. Manufacturing

- 11.3.5. Retail

- 11.3.6. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Solution Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 CentriLogic Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 NTT Communications Corporation

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Equinix Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Ascenty S A

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 CenturyLink Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 IBM Corporation*List Not Exhaustive

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Internap Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Global Switch Ltd

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 AT&T Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Rackspace Inc

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 CentriLogic Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Multi-Tenant Data Center Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Multi-Tenant Data Center Industry Revenue (billion), by Solution Type 2025 & 2033

- Figure 3: North America Multi-Tenant Data Center Industry Revenue Share (%), by Solution Type 2025 & 2033

- Figure 4: North America Multi-Tenant Data Center Industry Revenue (billion), by Application 2025 & 2033

- Figure 5: North America Multi-Tenant Data Center Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Multi-Tenant Data Center Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 7: North America Multi-Tenant Data Center Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 8: North America Multi-Tenant Data Center Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: North America Multi-Tenant Data Center Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Multi-Tenant Data Center Industry Revenue (billion), by Solution Type 2025 & 2033

- Figure 11: Europe Multi-Tenant Data Center Industry Revenue Share (%), by Solution Type 2025 & 2033

- Figure 12: Europe Multi-Tenant Data Center Industry Revenue (billion), by Application 2025 & 2033

- Figure 13: Europe Multi-Tenant Data Center Industry Revenue Share (%), by Application 2025 & 2033

- Figure 14: Europe Multi-Tenant Data Center Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 15: Europe Multi-Tenant Data Center Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 16: Europe Multi-Tenant Data Center Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Europe Multi-Tenant Data Center Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Multi-Tenant Data Center Industry Revenue (billion), by Solution Type 2025 & 2033

- Figure 19: Asia Pacific Multi-Tenant Data Center Industry Revenue Share (%), by Solution Type 2025 & 2033

- Figure 20: Asia Pacific Multi-Tenant Data Center Industry Revenue (billion), by Application 2025 & 2033

- Figure 21: Asia Pacific Multi-Tenant Data Center Industry Revenue Share (%), by Application 2025 & 2033

- Figure 22: Asia Pacific Multi-Tenant Data Center Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 23: Asia Pacific Multi-Tenant Data Center Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: Asia Pacific Multi-Tenant Data Center Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Asia Pacific Multi-Tenant Data Center Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Latin America Multi-Tenant Data Center Industry Revenue (billion), by Solution Type 2025 & 2033

- Figure 27: Latin America Multi-Tenant Data Center Industry Revenue Share (%), by Solution Type 2025 & 2033

- Figure 28: Latin America Multi-Tenant Data Center Industry Revenue (billion), by Application 2025 & 2033

- Figure 29: Latin America Multi-Tenant Data Center Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Latin America Multi-Tenant Data Center Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 31: Latin America Multi-Tenant Data Center Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 32: Latin America Multi-Tenant Data Center Industry Revenue (billion), by Country 2025 & 2033

- Figure 33: Latin America Multi-Tenant Data Center Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East Multi-Tenant Data Center Industry Revenue (billion), by Solution Type 2025 & 2033

- Figure 35: Middle East Multi-Tenant Data Center Industry Revenue Share (%), by Solution Type 2025 & 2033

- Figure 36: Middle East Multi-Tenant Data Center Industry Revenue (billion), by Application 2025 & 2033

- Figure 37: Middle East Multi-Tenant Data Center Industry Revenue Share (%), by Application 2025 & 2033

- Figure 38: Middle East Multi-Tenant Data Center Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 39: Middle East Multi-Tenant Data Center Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 40: Middle East Multi-Tenant Data Center Industry Revenue (billion), by Country 2025 & 2033

- Figure 41: Middle East Multi-Tenant Data Center Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Multi-Tenant Data Center Industry Revenue billion Forecast, by Solution Type 2020 & 2033

- Table 2: Global Multi-Tenant Data Center Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 3: Global Multi-Tenant Data Center Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 4: Global Multi-Tenant Data Center Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Global Multi-Tenant Data Center Industry Revenue billion Forecast, by Solution Type 2020 & 2033

- Table 6: Global Multi-Tenant Data Center Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 7: Global Multi-Tenant Data Center Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 8: Global Multi-Tenant Data Center Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: Global Multi-Tenant Data Center Industry Revenue billion Forecast, by Solution Type 2020 & 2033

- Table 10: Global Multi-Tenant Data Center Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Multi-Tenant Data Center Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 12: Global Multi-Tenant Data Center Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global Multi-Tenant Data Center Industry Revenue billion Forecast, by Solution Type 2020 & 2033

- Table 14: Global Multi-Tenant Data Center Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 15: Global Multi-Tenant Data Center Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 16: Global Multi-Tenant Data Center Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 17: Global Multi-Tenant Data Center Industry Revenue billion Forecast, by Solution Type 2020 & 2033

- Table 18: Global Multi-Tenant Data Center Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 19: Global Multi-Tenant Data Center Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 20: Global Multi-Tenant Data Center Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 21: Global Multi-Tenant Data Center Industry Revenue billion Forecast, by Solution Type 2020 & 2033

- Table 22: Global Multi-Tenant Data Center Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 23: Global Multi-Tenant Data Center Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 24: Global Multi-Tenant Data Center Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Multi-Tenant Data Center Industry?

The projected CAGR is approximately 19.7%.

2. Which companies are prominent players in the Multi-Tenant Data Center Industry?

Key companies in the market include CentriLogic Inc, NTT Communications Corporation, Equinix Inc, Ascenty S A, CenturyLink Inc, IBM Corporation*List Not Exhaustive, Internap Corporation, Global Switch Ltd, AT&T Inc, Rackspace Inc.

3. What are the main segments of the Multi-Tenant Data Center Industry?

The market segments include Solution Type, Application, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 448.95 billion as of 2022.

5. What are some drivers contributing to market growth?

Increased Demand For Green Data Centers; Growing Internet Data Traffic.

6. What are the notable trends driving market growth?

Retail colocation is Expected to Hold Significant Growth Rate.

7. Are there any restraints impacting market growth?

Consolidation of Data Centers; Data Security Concerns.

8. Can you provide examples of recent developments in the market?

October 2022: Google intends to establish its first data center in Japan by 2023. The company declared that this data center would be based in Inzai City, Chiba, and would be funded by a USD 730 million infrastructure fund until 2024. Also, the company collaborates with colocation facility providers like Equinix to power these regions for Google Cloud customers. However, it is currently building its own data center to support its services, including YouTube, Gmail, and the rest.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Multi-Tenant Data Center Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Multi-Tenant Data Center Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Multi-Tenant Data Center Industry?

To stay informed about further developments, trends, and reports in the Multi-Tenant Data Center Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence