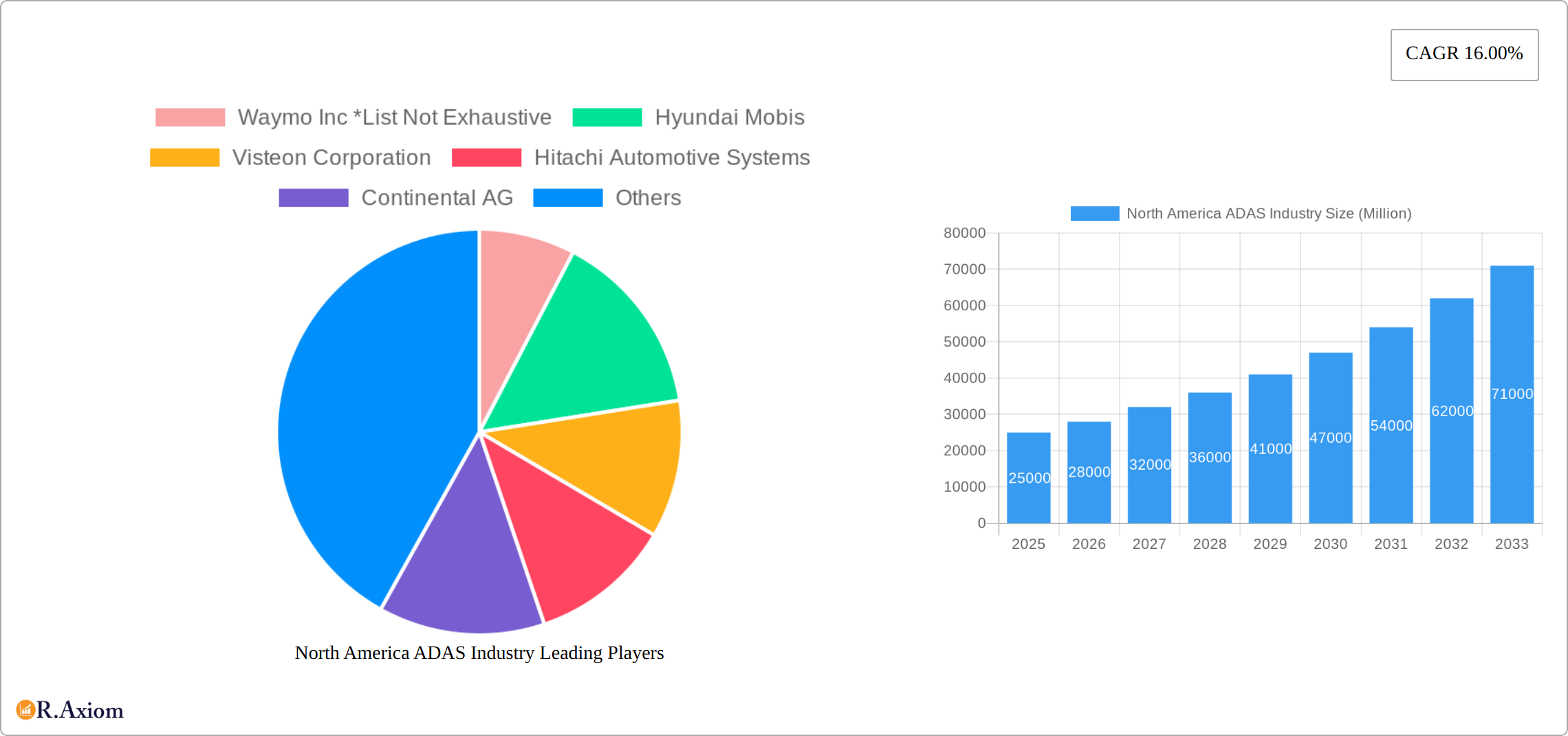

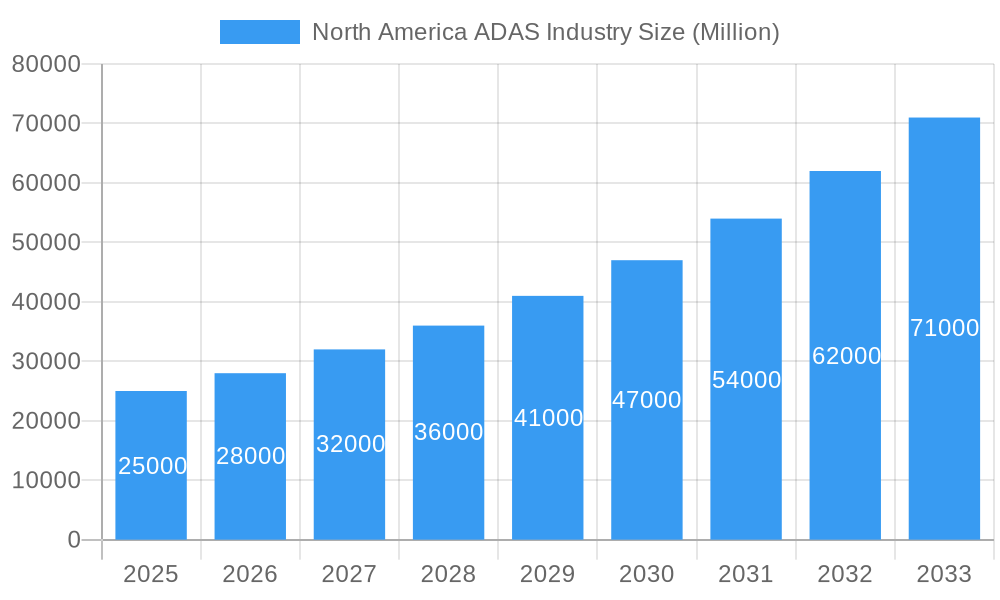

Key Insights

The North American Advanced Driver-Assistance Systems (ADAS) market is projected for substantial expansion, fueled by increasing vehicle production, stringent safety regulations, and growing consumer demand for enhanced vehicle safety. The market is anticipated to grow at a Compound Annual Growth Rate (CAGR) of 11.9%, with an estimated market size of 334 million in the base year 2024. Key growth drivers include the widespread adoption of ADAS technologies in passenger vehicles, such as Adaptive Cruise Control, Lane Keeping Assist, and Autonomous Emergency Braking. Innovations in sensor technologies, including radar, lidar, and advanced camera systems, are enabling more sophisticated and reliable ADAS functionalities. The integration of ADAS into commercial vehicles also presents a significant growth opportunity, driven by the imperative to enhance fleet safety and operational efficiency.

North America ADAS Industry Market Size (In Million)

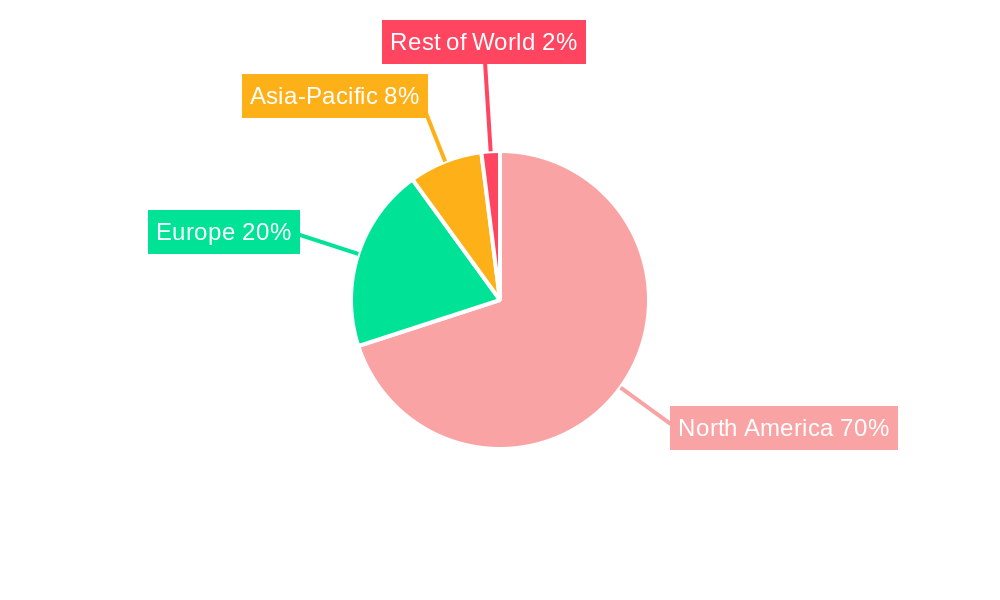

Regional market dynamics within North America show significant variations. The United States, benefiting from its extensive automotive industry and advanced technological infrastructure, holds the dominant market share. Canada and Mexico are also experiencing robust growth, driven by increasing automotive manufacturing and the harmonization of safety regulations with those in the US. Future market expansion will be shaped by the continuous development of autonomous driving technologies, the declining cost of ADAS components, and heightened consumer awareness of the safety benefits. However, challenges such as the high initial investment for ADAS implementation, data privacy and cybersecurity concerns associated with connected vehicles, and the requirement for supportive infrastructure for advanced autonomous systems persist.

North America ADAS Industry Company Market Share

This comprehensive report delivers an in-depth analysis of the North American ADAS market, covering the period from 2019 to 2033. It provides actionable insights for stakeholders, investors, and businesses aiming to understand market dynamics, growth prospects, and the competitive environment. The analysis incorporates extensive data, recent industry advancements, and a future-oriented perspective. Key segments examined include Adaptive Cruise Control, Autonomous Emergency Braking, and other ADAS features across passenger and commercial vehicles in the United States, Canada, and Mexico.

North America ADAS Industry Market Concentration & Innovation

The North American ADAS market is characterized by a moderately concentrated landscape, where a select group of major players command a significant share. While specific market share percentages are subject to annual fluctuations, industry stalwarts such as Robert Bosch GmbH, Continental AG, and Aptiv (formerly Delphi Technologies) consistently maintain substantial market positions. Innovation remains the paramount catalyst, propelled by relentless advancements in sensor technologies, including LiDAR, radar, and cameras, alongside breakthroughs in artificial intelligence and machine learning. The robust and evolving safety regulations enforced across North America underscore the imperative for continuous innovation and enhancement of ADAS functionalities. The market is dynamic, witnessing ongoing mergers and acquisitions (M&A) activity, with deal values often ranging from tens to hundreds of millions of USD. These strategic moves are aimed at expanding product portfolios and augmenting technological capabilities. A notable example is the recent collaboration between automotive giants like BMW and technology leaders such as Qualcomm and Arriver, signaling a significant stride towards more integrated ADAS solutions. While highly automated driving systems (Level 4 and 5 autonomy) represent potential product substitutes, they also present both formidable challenges and promising opportunities for the current ADAS market. Concurrently, end-user preferences are evolving towards higher tiers of driver assistance and advanced safety features, while simultaneously emphasizing the demand for cost-effective solutions.

- Key Market Share Holders (Estimated 2024): Robert Bosch GmbH (estimated 20-25%), Continental AG (estimated 15-20%), Aptiv (estimated 10-15%), ZF Friedrichshafen AG (estimated 8-12%), Magna International (estimated 5-8%), Others (remainder).

- M&A Activity (2019-2024): Total deal value estimated in the billions of USD, reflecting strategic consolidation and technology acquisition.

- Innovation Drivers: Pervasive advancements in sensor fusion, sophisticated AI algorithms, enhanced machine learning models, evolving vehicle-to-everything (V2X) communication, and increasingly stringent governmental safety mandates.

North America ADAS Industry Industry Trends & Insights

The North American ADAS market is experiencing robust growth, driven by increasing consumer demand for advanced safety features, supportive government regulations, and continuous technological advancements. The market is projected to grow at a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033), reaching an estimated market size of xx Million USD by 2033. This growth is significantly impacted by technological disruptions such as the widespread adoption of LiDAR technology and the increasing integration of artificial intelligence for improved decision-making within ADAS systems. Consumer preferences favor features that enhance safety and convenience, such as lane keeping assist, adaptive cruise control, and automatic emergency braking. The competitive landscape is intensely dynamic, with both established automotive suppliers and technology companies vying for market share. This leads to price competition, rapid product innovation, and continuous improvement in ADAS features. Market penetration for core ADAS features like lane departure warning systems has already reached significant levels, while other systems, such as driver drowsiness alerts, continue to see high adoption rates.

Dominant Markets & Segments in North America ADAS Industry

The United States represents the largest market for ADAS in North America, driven by high vehicle ownership, robust consumer spending on advanced vehicle technologies, and a well-developed automotive manufacturing sector. Within the ADAS segment breakdown:

- By Type: Autonomous Emergency Braking (AEB) and Adaptive Cruise Control (ACC) systems currently dominate the market due to their high demand and widespread adoption.

- By Technology Type: Camera-based systems currently hold a larger market share due to their cost-effectiveness and availability, however LiDAR and Radar are seeing significant growth due to their improved accuracy and capabilities in challenging conditions.

- By Vehicle Type: The passenger car segment leads the market, however, the commercial vehicle segment is showing strong growth potential due to rising demands for enhanced safety features within fleet operations.

Key Drivers for US Dominance:

- Strong consumer demand for advanced safety features.

- Favorable government regulations and safety standards.

- Large and established automotive manufacturing base.

- High level of technological innovation and development.

Canada and Mexico exhibit significant, albeit smaller, markets for ADAS. Their growth is influenced by increasing vehicle sales, government initiatives promoting road safety, and expanding automotive manufacturing activity.

North America ADAS Industry Product Developments

Recent product innovations focus on improving system accuracy, reliability, and integration with other vehicle systems. The integration of AI and machine learning is allowing for more sophisticated decision-making, leading to improved driver assistance and safety features. Several companies are focusing on the development of highly integrated ADAS platforms to reduce cost and complexity for automakers. The current trend is towards providing increasingly more advanced features as standard equipment, driving demand and market expansion. This move emphasizes not only safety but also enhances the overall driving experience and vehicle value proposition.

Report Scope & Segmentation Analysis

This report offers a comprehensive segmentation of the North American ADAS market, examining it across a variety of critical parameters:

By Type: Adaptive Cruise Control (ACC) Systems, Adaptive Front-lighting Systems (AFS), Night Vision Systems, Blind Spot Detection (BSD), Autonomous Emergency Braking (AEB) Systems, Lane Keeping Assist (LKA), Driver Drowsiness Alert (DDA), Lane Departure Warning (LDW), Pedestrian Detection Systems, Traffic Sign Recognition (TSR), and Other Advanced ADAS Features. Each category demonstrates distinct growth trajectories and market valuations, heavily influenced by evolving consumer preferences, the pace of technological innovation, and the enforcement of regulatory mandates.

By Technology Type: Radar, LiDAR, Camera Systems, Ultrasonic Sensors, and Sensor Fusion Technologies. The market share distribution among these technology types is anticipated to undergo continuous evolution as novel technologies emerge and existing ones achieve greater maturity and cost-effectiveness.

By Vehicle Type: Passenger Cars (including sedans, SUVs, hatchbacks, and luxury vehicles), Light Commercial Vehicles (LCVs), and Heavy Commercial Vehicles (HCVs). The commercial vehicle segment, in particular, exhibits robust growth prospects, driven by increasing fleet safety concerns, the imperative for operational efficiency, and supportive government regulations aimed at reducing accidents.

By Country: United States, Canada, and Mexico. Growth projections are diversified across these countries, reflecting variations in their economic landscapes, vehicle ownership penetration rates, regulatory frameworks, and the adoption pace of advanced automotive technologies.

Key Drivers of North America ADAS Industry Growth

The North American ADAS market is experiencing significant impetus from a confluence of potent drivers:

- Pioneering Technological Advancements: The relentless pace of innovation in sensor capabilities, the refinement of artificial intelligence algorithms for sophisticated perception and decision-making, and the continuous improvement of machine learning models are yielding ADAS systems that are increasingly accurate, reliable, and cost-efficient.

- Proactive Government Regulations and Safety Mandates: The implementation of increasingly stringent safety regulations across federal and state levels, which either mandate or strongly incentivize the integration of specific ADAS features in new vehicle production, is a fundamental growth driver.

- Surging Consumer Demand for Safety and Convenience: There is a discernible and growing consumer preference for advanced safety features that mitigate risks and enhance driving comfort, coupled with a desire for the convenience offered by intelligent driver assistance systems.

- Robust Economic Conditions and Vehicle Sales: Positive economic indicators, rising disposable incomes, and sustained demand for new vehicles, particularly in key segments, directly contribute to the adoption of vehicles equipped with ADAS technology.

- Electrification and Autonomous Driving Synergies: The parallel growth of electric vehicles (EVs) and the pursuit of higher levels of driving automation create natural synergies with ADAS development, as many underlying technologies and architectures are shared or complementary.

Challenges in the North America ADAS Industry Sector

Despite its promising trajectory, the North American ADAS industry faces several significant challenges:

- Substantial Development and Validation Costs: The intricate design, rigorous testing, and validation processes required for sophisticated ADAS systems represent substantial financial investments, which can pose a barrier to entry for smaller innovators and startups.

- Data Security and User Privacy Imperatives: The collection and processing of vast quantities of sensor and user data by ADAS systems raise critical concerns regarding data security, potential breaches, and the imperative to safeguard user privacy in compliance with evolving regulations.

- Global Supply Chain Vulnerabilities: The ADAS industry is heavily reliant on a complex global supply chain, particularly for semiconductor components, advanced sensors, and microprocessors. Occasional disruptions due to geopolitical factors, natural disasters, or manufacturing bottlenecks can impact production schedules and cost structures.

- Evolving Cybersecurity Threats: As ADAS systems become more connected and complex, their susceptibility to cyberattacks increases. Robust and continuously updated cybersecurity measures are essential to protect against unauthorized access, data manipulation, or system compromise, which could have severe safety implications.

- Standardization and Interoperability Hurdles: The lack of complete industry-wide standardization in ADAS functionalities and communication protocols can lead to interoperability issues between different vehicle brands and aftermarket solutions, potentially fragmenting the market and slowing adoption.

Emerging Opportunities in North America ADAS Industry

Emerging opportunities include:

- Expansion in Commercial Vehicles: The growing demand for safety and efficiency in commercial vehicles presents a significant market opportunity.

- Integration with Connected Car Technologies: Integrating ADAS with other connected car technologies can enhance safety and create new revenue streams.

- Development of Level 3+ Autonomous Driving Systems: Advances in ADAS will contribute to the development of more autonomous driving systems, creating significant long-term market expansion.

- Growth in Aftermarket ADAS: The aftermarket sector offers opportunities for retrofitting ADAS features in older vehicles.

Leading Players in the North America ADAS Industry Market

- Waymo Inc

- Hyundai Mobis

- Visteon Corporation

- Hitachi Automotive Systems

- Continental AG

- Velodyne Lidar

- Robert Bosch GmbH

- Delphi Technologies

- Magna International

- LG Electronics

- ZF Friedrichshafen AG

Key Developments in North America ADAS Industry Industry

- October 2022: Waymo expands its robotaxi services to Los Angeles, CA. This significantly increases the exposure and acceptance of autonomous driving technologies.

- October 2022: Mobileye files for an IPO, valuing the company at USD 16 Billion, highlighting investor confidence in the ADAS sector.

- June 2022: Stellantis selects Valeo's LiDAR solution for Level 3 autonomy, showcasing industry collaboration and the push toward higher levels of automation.

- March 2022: BMW, Qualcomm, and Arriver collaborate on ADAS development, demonstrating the increasing importance of partnerships in the sector.

Strategic Outlook for North America ADAS Industry Market

The North American ADAS market is on an accelerated path toward substantial expansion, driven by the synergistic forces of continuous technological innovation, supportive governmental policies aimed at enhancing road safety, and a burgeoning consumer appetite for advanced safety and convenience features in their vehicles. The increasing integration of ADAS functionalities with other connected vehicle technologies, such as advanced infotainment systems and over-the-air (OTA) updates, is poised to further amplify market growth and create new revenue streams. A significant trend will be the progressive shift towards higher levels of driving automation and the deployment of sophisticated AI-driven decision-making systems, unlocking novel avenues for pioneering innovation and strategic investment. The market landscape will continue to be dynamically shaped by strategic alliances, pivotal collaborations, and significant mergers and acquisitions involving established automotive manufacturers, Tier 1 suppliers, and cutting-edge technology companies, fostering a more competitive and innovative ecosystem.

North America ADAS Industry Segmentation

-

1. Type

- 1.1. Adaptive Cruise Control System

- 1.2. Adaptive Front-lighting

- 1.3. Night Vision System

- 1.4. Blind Spot Detection

- 1.5. Autonomous Emergency Braking System

- 1.6. Lane Keeping Assist

- 1.7. Driver Drowsiness Alert

- 1.8. Lane Departure Warning

- 1.9. Other Types

-

2. Technology Type

- 2.1. Radar

- 2.2. Li-Dar

- 2.3. Camera

-

3. Vehicle Type

- 3.1. Passenger Cars

- 3.2. Commercial Vehicles

North America ADAS Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America ADAS Industry Regional Market Share

Geographic Coverage of North America ADAS Industry

North America ADAS Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Adaptive Cruise Control System

- 5.1.2. Adaptive Front-lighting

- 5.1.3. Night Vision System

- 5.1.4. Blind Spot Detection

- 5.1.5. Autonomous Emergency Braking System

- 5.1.6. Lane Keeping Assist

- 5.1.7. Driver Drowsiness Alert

- 5.1.8. Lane Departure Warning

- 5.1.9. Other Types

- 5.2. Market Analysis, Insights and Forecast - by Technology Type

- 5.2.1. Radar

- 5.2.2. Li-Dar

- 5.2.3. Camera

- 5.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.3.1. Passenger Cars

- 5.3.2. Commercial Vehicles

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America ADAS Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Adaptive Cruise Control System

- 6.1.2. Adaptive Front-lighting

- 6.1.3. Night Vision System

- 6.1.4. Blind Spot Detection

- 6.1.5. Autonomous Emergency Braking System

- 6.1.6. Lane Keeping Assist

- 6.1.7. Driver Drowsiness Alert

- 6.1.8. Lane Departure Warning

- 6.1.9. Other Types

- 6.2. Market Analysis, Insights and Forecast - by Technology Type

- 6.2.1. Radar

- 6.2.2. Li-Dar

- 6.2.3. Camera

- 6.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.3.1. Passenger Cars

- 6.3.2. Commercial Vehicles

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Waymo Inc *List Not Exhaustive

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Hyundai Mobis

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Visteon Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Hitachi Automotive Systems

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Continental AG

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Velodyne Lidar

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Robert Bosch GmbH

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Delphi Technologies

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Magna International

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 LG Electronics

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 ZF Friedrichshafen AG

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 Waymo Inc *List Not Exhaustive

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America ADAS Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: North America ADAS Industry Share (%) by Company 2025

List of Tables

- Table 1: North America ADAS Industry Revenue million Forecast, by Type 2020 & 2033

- Table 2: North America ADAS Industry Revenue million Forecast, by Technology Type 2020 & 2033

- Table 3: North America ADAS Industry Revenue million Forecast, by Vehicle Type 2020 & 2033

- Table 4: North America ADAS Industry Revenue million Forecast, by Region 2020 & 2033

- Table 5: North America ADAS Industry Revenue million Forecast, by Type 2020 & 2033

- Table 6: North America ADAS Industry Revenue million Forecast, by Technology Type 2020 & 2033

- Table 7: North America ADAS Industry Revenue million Forecast, by Vehicle Type 2020 & 2033

- Table 8: North America ADAS Industry Revenue million Forecast, by Country 2020 & 2033

- Table 9: United States North America ADAS Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Canada North America ADAS Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 11: Mexico North America ADAS Industry Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America ADAS Industry?

The projected CAGR is approximately 11.9%.

2. Which companies are prominent players in the North America ADAS Industry?

Key companies in the market include Waymo Inc *List Not Exhaustive, Hyundai Mobis, Visteon Corporation, Hitachi Automotive Systems, Continental AG, Velodyne Lidar, Robert Bosch GmbH, Delphi Technologies, Magna International, LG Electronics, ZF Friedrichshafen AG.

3. What are the main segments of the North America ADAS Industry?

The market segments include Type, Technology Type, Vehicle Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 334 million as of 2022.

5. What are some drivers contributing to market growth?

Increase in Sales of Passenger Cars.

6. What are the notable trends driving market growth?

Growing Sales of Vehicles Fitted with LiDAR Driving the Market.

7. Are there any restraints impacting market growth?

Failure in Garage Equipment may Result in Downtime of the Repair Work.

8. Can you provide examples of recent developments in the market?

October, 2022: Waymo, the robotaxi services providing arm of Alphabet Inc., announced the expansion of its robotaxi taxi services to Los Angeles in California, United States.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America ADAS Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America ADAS Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America ADAS Industry?

To stay informed about further developments, trends, and reports in the North America ADAS Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence