Key Insights

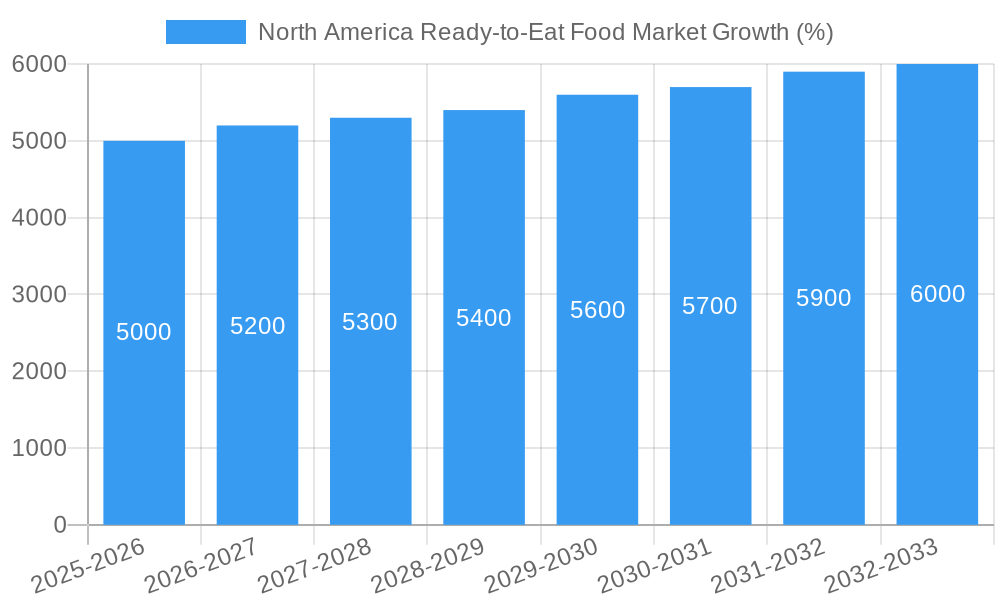

The North American ready-to-eat (RTE) food market, valued at approximately $XX million in 2025, is projected to experience steady growth, exhibiting a compound annual growth rate (CAGR) of 3.36% from 2025 to 2033. This growth is fueled by several key drivers. The increasing prevalence of busy lifestyles and dual-income households is significantly boosting demand for convenient meal options. Consumers are prioritizing time-saving solutions without compromising on taste or nutritional value, driving the popularity of RTE meals, snacks, and breakfast options. Furthermore, the rising disposable incomes in certain segments of the North American population contribute to increased spending on convenient and often premium RTE foods. Innovation within the RTE food sector, encompassing healthier options, diverse flavor profiles, and sustainable packaging, further enhances market appeal. The growth is particularly strong in segments such as instant breakfast cereals and ready meals, reflecting changing consumer preferences towards quick and nutritious food solutions. However, restraints such as concerns about high sodium and sugar content in some RTE products and fluctuating raw material prices could potentially dampen the market's growth trajectory. The market is segmented by product type (instant breakfast/cereals, instant soups and snacks, ready meals, baked goods, meat products, other) and distribution channel (hypermarkets/supermarkets, convenience stores, online retail stores, other). The dominance of hypermarkets and supermarkets as distribution channels is expected to continue, although online retail is gaining traction, reflecting the broader shift towards e-commerce.

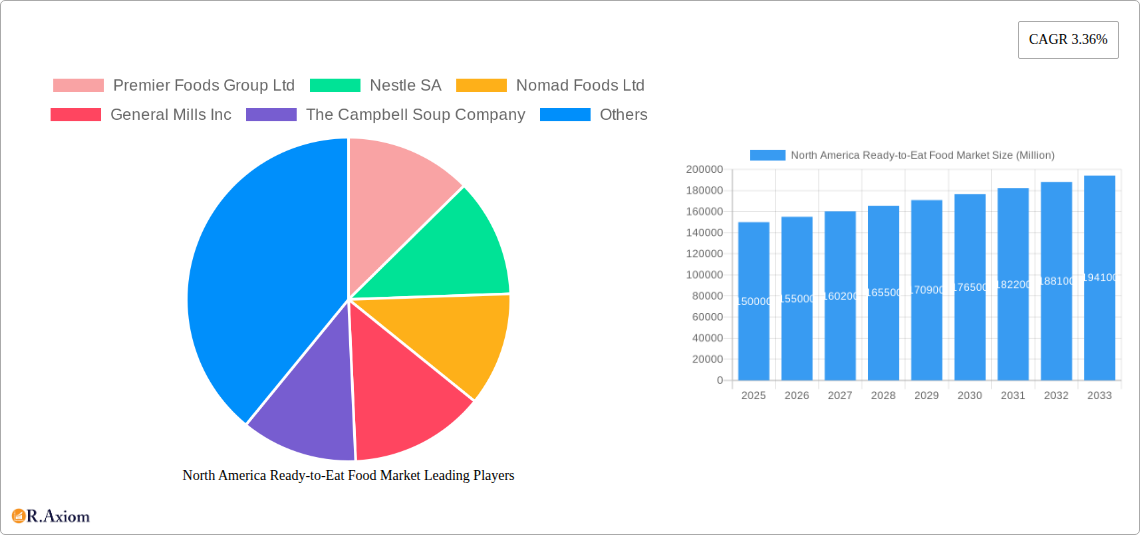

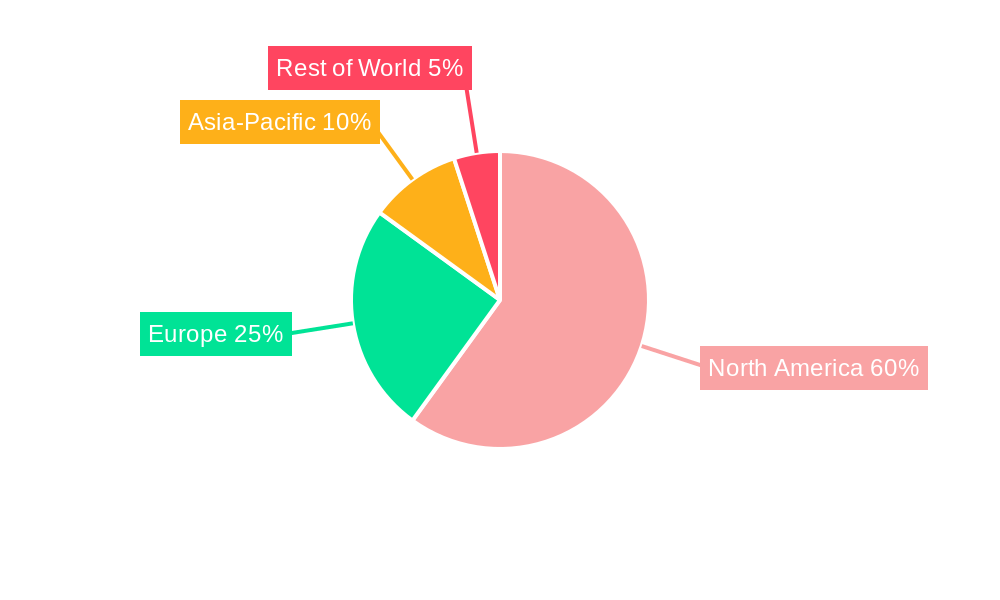

The competitive landscape is highly fragmented, with key players including Premier Foods Group Ltd, Nestlé SA, Nomad Foods Ltd, General Mills Inc, The Campbell Soup Company, and others actively vying for market share through product diversification, brand building, and strategic partnerships. The North American market is expected to continue its lead in terms of market share due to factors such as high consumer spending power and well-established distribution networks. While specific regional data is limited for the forecast period, we can expect a relatively balanced growth across the United States, Canada, and Mexico within the North American region, influenced by regional economic factors and consumer preferences. Growth will likely be slightly stronger in urban areas due to higher population density and busier lifestyles. The forecast period suggests a continuous upward trend driven by ongoing demographic shifts and evolving consumer demands for convenient, healthy, and flavorful ready-to-eat food options.

North America Ready-to-Eat Food Market: A Comprehensive Report (2019-2033)

This comprehensive report provides an in-depth analysis of the North America ready-to-eat food market, covering the period from 2019 to 2033. It offers invaluable insights into market dynamics, growth drivers, challenges, and emerging opportunities for industry stakeholders, including manufacturers, distributors, and investors. The report leverages extensive primary and secondary research to deliver actionable intelligence and robust forecasts.

North America Ready-to-Eat Food Market Market Concentration & Innovation

The North America ready-to-eat food market exhibits a moderately consolidated structure, with several large multinational corporations holding significant market share. Key players such as Nestle SA, General Mills Inc., and The Kraft Heinz Company exert considerable influence, driving innovation and shaping market trends. However, smaller, specialized companies are also gaining traction through product differentiation and niche market targeting. The market share of the top 5 players is estimated at xx% in 2025.

Innovation within the industry is fueled by several factors, including:

- Health and Wellness Trends: Growing consumer demand for healthier options is pushing companies to develop products with reduced sodium, sugar, and fat content, as well as incorporating functional ingredients.

- Technological Advancements: Improvements in food processing and packaging technologies allow for longer shelf life, improved product quality, and enhanced convenience. This includes advancements in freezing, preservation, and packaging materials.

- Sustainable Practices: Increasing awareness of environmental concerns is driving the adoption of sustainable packaging and sourcing practices. This includes the rise in plant-based alternatives and reduced plastic usage.

Regulatory frameworks, such as food safety regulations and labeling requirements, play a significant role in shaping market practices. The presence of substitute products, including home-cooked meals and restaurant dining, keeps competitive pressure high. Mergers and acquisitions (M&A) activity is a key characteristic, with deal values averaging xx Million in the period 2019-2024. Notable M&A activities involved acquisitions of smaller brands by major players to expand product portfolios and market reach. End-user preferences, particularly among millennials and Gen Z, favor convenience, health, and ethically sourced products.

North America Ready-to-Eat Food Market Industry Trends & Insights

The North America ready-to-eat food market is experiencing robust growth, driven by several key factors. The market is projected to register a CAGR of xx% during the forecast period (2025-2033), reaching a market value of xx Million by 2033.

This growth is fueled by:

- Busy Lifestyles: The increasing number of dual-income households and busy lifestyles are significantly driving demand for convenient food options.

- E-commerce Growth: Online retail channels are experiencing substantial growth, providing consumers with readily accessible options and greater choice. Market penetration of online retail within this segment is estimated at xx% in 2025.

- Changing Consumer Preferences: Consumers are increasingly seeking healthier, more diverse, and convenient options, impacting product formulation and innovation. There is a marked shift toward organic, plant-based, and ethically sourced products.

- Technological Disruption: Advancements in food technology, packaging, and online ordering are transforming the landscape. Precision fermentation and alternative protein sources are gaining traction.

- Competitive Landscape: Intense competition among major players is driving innovation and pricing strategies.

These factors, combined with evolving consumer demographics and preferences, are shaping the trajectory of the ready-to-eat food market.

Dominant Markets & Segments in North America Ready-to-Eat Food Market

The United States represents the largest market within North America for ready-to-eat foods. Within the product type segments, ready meals are currently the dominant category, driven by increasing demand for convenience and variety.

By Product Type:

- Ready Meals: High demand driven by convenience, portion control, and diverse meal options.

- Instant Soups & Snacks: Significant growth fueled by on-the-go consumption and affordability.

- Baked Goods: Steady demand driven by breakfast and snacking occasions.

- Meat Products: Growth influenced by demand for convenience and diverse protein sources.

- Instant Breakfast/Cereals: Stable demand but facing some competition from newer, healthier alternatives.

- Other Product Types: This segment represents a varied range of products and demonstrates considerable growth potential.

By Distribution Channel:

- Hypermarkets/Supermarkets: This remains the primary distribution channel, offering broad product selection and established consumer habits.

- Convenience Stores: These channels cater to on-the-go consumption, driving significant sales in ready-to-eat snacks and meals.

- Online Retail Stores: Rapid growth is projected, boosted by ease of access and expanding home delivery services.

- Other Distribution Channels: This includes food service businesses and specialized retailers.

Key drivers for regional dominance include robust economic growth, well-developed retail infrastructure, and changing consumer lifestyles.

North America Ready-to-Eat Food Market Product Developments

Recent product innovations focus on healthier options, enhanced convenience, and improved sustainability. This includes the rise of plant-based alternatives, single-serve packaging, and more sustainable packaging materials. Companies are leveraging technology such as sous vide and other advanced cooking techniques to deliver high-quality, flavorful, and convenient products. The market is also witnessing the emergence of personalized nutrition solutions and meal kits tailored to individual dietary needs. These advancements are aligning product offerings with consumer demands for health, convenience, and sustainability.

Report Scope & Segmentation Analysis

This report segments the North American ready-to-eat food market by product type (Instant Breakfast/Cereals, Instant Soups and Snacks, Ready Meals, Baked Goods, Meat Products, Other Product Types) and distribution channel (Hypermarkets/Supermarkets, Convenience Stores, Online Retail Stores, Other Distribution Channels). Each segment’s market size, growth projections, and competitive dynamics are comprehensively analyzed. The market is expected to witness significant growth across all segments, driven by factors such as increasing consumer demand and technological advancements. The ready meals segment is projected to maintain its market leadership, while the online retail channel is expected to experience the fastest growth. Competitive dynamics are shaped by factors such as product innovation, brand reputation, and pricing strategies.

Key Drivers of North America Ready-to-Eat Food Market Growth

Several factors contribute to the market’s growth. Increasing disposable incomes and busy lifestyles fuel the demand for convenient food options. Technological advancements in food processing and packaging enhance product quality and shelf life. Favorable government policies supporting the food industry contribute to a positive business environment. The growing popularity of online grocery shopping further boosts market expansion.

Challenges in the North America Ready-to-Eat Food Market Sector

The industry faces challenges such as stringent food safety regulations, fluctuating raw material costs, and intense competition. Supply chain disruptions, particularly impacting imported ingredients, can lead to production delays and cost increases. Maintaining consistent product quality while balancing cost-effectiveness presents a significant hurdle. Furthermore, changing consumer preferences and the rise of health-conscious diets create pressure to adapt product offerings.

Emerging Opportunities in North America Ready-to-Eat Food Market

The market presents several opportunities, including the growing demand for healthy and sustainable options, the rise of personalized nutrition, and the expansion of e-commerce. Companies can capitalize on these trends by developing innovative products catering to specific dietary needs, embracing sustainable practices, and strengthening their online presence. The increasing popularity of plant-based and alternative protein sources opens up new avenues for product development.

Leading Players in the North America Ready-to-Eat Food Market Market

- Premier Foods Group Ltd

- Nestle SA

- Nomad Foods Ltd

- General Mills Inc

- The Campbell Soup Company

- Dr August Oetker Nahrugsmittel KG

- Fleury Michon

- Conagra Brands Inc

- The Kraft Heinz Company

- McCain Foods Limited

Key Developments in North America Ready-to-Eat Food Market Industry

- 2023-Q3: Nestle SA launched a new line of plant-based ready meals.

- 2022-Q4: General Mills Inc. acquired a smaller organic food company, expanding its portfolio of healthier options.

- 2021-Q2: Conagra Brands Inc. invested in advanced packaging technology to enhance product shelf life. (Further developments to be added upon data availability).

Strategic Outlook for North America Ready-to-Eat Food Market Market

The North America ready-to-eat food market holds substantial growth potential driven by evolving consumer preferences, technological advancements, and the expansion of e-commerce. Companies that successfully adapt to evolving consumer preferences, invest in innovation, and adopt sustainable practices are well-positioned for long-term success. Focusing on health and wellness, convenience, and sustainable practices will be crucial for capturing market share and achieving sustainable growth.

North America Ready-to-Eat Food Market Segmentation

-

1. Product Type

- 1.1. Instant Breakfast/ Cereals

- 1.2. Instant Soups and Snacks

- 1.3. Ready Meals

- 1.4. Baked Goods

- 1.5. Meat Products

- 1.6. Other Product Types

-

2. Distribution Channel

- 2.1. Hypermarkets/ Supermarkets

- 2.2. Convinience Stores

- 2.3. Online Retail Stores

- 2.4. Other Distribution Channels

-

3. Geography

- 3.1. United States

- 3.2. Canada

- 3.3. Mexico

- 3.4. Rest of North America

North America Ready-to-Eat Food Market Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Mexico

- 4. Rest of North America

North America Ready-to-Eat Food Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 3.36% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. The numerous benefits offered by collagen in the food and beverage industry

- 3.3. Market Restrains

- 3.3.1. Increasing vegan population in the region

- 3.4. Market Trends

- 3.4.1. Convenience of Use Driving the Ready-to-Eat Food Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Ready-to-Eat Food Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Instant Breakfast/ Cereals

- 5.1.2. Instant Soups and Snacks

- 5.1.3. Ready Meals

- 5.1.4. Baked Goods

- 5.1.5. Meat Products

- 5.1.6. Other Product Types

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Hypermarkets/ Supermarkets

- 5.2.2. Convinience Stores

- 5.2.3. Online Retail Stores

- 5.2.4. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. United States

- 5.3.2. Canada

- 5.3.3. Mexico

- 5.3.4. Rest of North America

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Mexico

- 5.4.4. Rest of North America

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. United States North America Ready-to-Eat Food Market Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Instant Breakfast/ Cereals

- 6.1.2. Instant Soups and Snacks

- 6.1.3. Ready Meals

- 6.1.4. Baked Goods

- 6.1.5. Meat Products

- 6.1.6. Other Product Types

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Hypermarkets/ Supermarkets

- 6.2.2. Convinience Stores

- 6.2.3. Online Retail Stores

- 6.2.4. Other Distribution Channels

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. United States

- 6.3.2. Canada

- 6.3.3. Mexico

- 6.3.4. Rest of North America

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Canada North America Ready-to-Eat Food Market Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Instant Breakfast/ Cereals

- 7.1.2. Instant Soups and Snacks

- 7.1.3. Ready Meals

- 7.1.4. Baked Goods

- 7.1.5. Meat Products

- 7.1.6. Other Product Types

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Hypermarkets/ Supermarkets

- 7.2.2. Convinience Stores

- 7.2.3. Online Retail Stores

- 7.2.4. Other Distribution Channels

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. United States

- 7.3.2. Canada

- 7.3.3. Mexico

- 7.3.4. Rest of North America

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Mexico North America Ready-to-Eat Food Market Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Instant Breakfast/ Cereals

- 8.1.2. Instant Soups and Snacks

- 8.1.3. Ready Meals

- 8.1.4. Baked Goods

- 8.1.5. Meat Products

- 8.1.6. Other Product Types

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. Hypermarkets/ Supermarkets

- 8.2.2. Convinience Stores

- 8.2.3. Online Retail Stores

- 8.2.4. Other Distribution Channels

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. United States

- 8.3.2. Canada

- 8.3.3. Mexico

- 8.3.4. Rest of North America

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Rest of North America North America Ready-to-Eat Food Market Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Instant Breakfast/ Cereals

- 9.1.2. Instant Soups and Snacks

- 9.1.3. Ready Meals

- 9.1.4. Baked Goods

- 9.1.5. Meat Products

- 9.1.6. Other Product Types

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. Hypermarkets/ Supermarkets

- 9.2.2. Convinience Stores

- 9.2.3. Online Retail Stores

- 9.2.4. Other Distribution Channels

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. United States

- 9.3.2. Canada

- 9.3.3. Mexico

- 9.3.4. Rest of North America

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. United States North America Ready-to-Eat Food Market Analysis, Insights and Forecast, 2019-2031

- 11. Canada North America Ready-to-Eat Food Market Analysis, Insights and Forecast, 2019-2031

- 12. Mexico North America Ready-to-Eat Food Market Analysis, Insights and Forecast, 2019-2031

- 13. Rest of North America North America Ready-to-Eat Food Market Analysis, Insights and Forecast, 2019-2031

- 14. Competitive Analysis

- 14.1. Market Share Analysis 2024

- 14.2. Company Profiles

- 14.2.1 Premier Foods Group Ltd

- 14.2.1.1. Overview

- 14.2.1.2. Products

- 14.2.1.3. SWOT Analysis

- 14.2.1.4. Recent Developments

- 14.2.1.5. Financials (Based on Availability)

- 14.2.2 Nestle SA

- 14.2.2.1. Overview

- 14.2.2.2. Products

- 14.2.2.3. SWOT Analysis

- 14.2.2.4. Recent Developments

- 14.2.2.5. Financials (Based on Availability)

- 14.2.3 Nomad Foods Ltd

- 14.2.3.1. Overview

- 14.2.3.2. Products

- 14.2.3.3. SWOT Analysis

- 14.2.3.4. Recent Developments

- 14.2.3.5. Financials (Based on Availability)

- 14.2.4 General Mills Inc

- 14.2.4.1. Overview

- 14.2.4.2. Products

- 14.2.4.3. SWOT Analysis

- 14.2.4.4. Recent Developments

- 14.2.4.5. Financials (Based on Availability)

- 14.2.5 The Campbell Soup Company

- 14.2.5.1. Overview

- 14.2.5.2. Products

- 14.2.5.3. SWOT Analysis

- 14.2.5.4. Recent Developments

- 14.2.5.5. Financials (Based on Availability)

- 14.2.6 Dr August Oetker Nahrugsmittel KG

- 14.2.6.1. Overview

- 14.2.6.2. Products

- 14.2.6.3. SWOT Analysis

- 14.2.6.4. Recent Developments

- 14.2.6.5. Financials (Based on Availability)

- 14.2.7 Fleury Michon

- 14.2.7.1. Overview

- 14.2.7.2. Products

- 14.2.7.3. SWOT Analysis

- 14.2.7.4. Recent Developments

- 14.2.7.5. Financials (Based on Availability)

- 14.2.8 Conagra Brands Inc

- 14.2.8.1. Overview

- 14.2.8.2. Products

- 14.2.8.3. SWOT Analysis

- 14.2.8.4. Recent Developments

- 14.2.8.5. Financials (Based on Availability)

- 14.2.9 The Kraft Heinz Company*List Not Exhaustive

- 14.2.9.1. Overview

- 14.2.9.2. Products

- 14.2.9.3. SWOT Analysis

- 14.2.9.4. Recent Developments

- 14.2.9.5. Financials (Based on Availability)

- 14.2.10 McCain Foods Limited

- 14.2.10.1. Overview

- 14.2.10.2. Products

- 14.2.10.3. SWOT Analysis

- 14.2.10.4. Recent Developments

- 14.2.10.5. Financials (Based on Availability)

- 14.2.1 Premier Foods Group Ltd

List of Figures

- Figure 1: North America Ready-to-Eat Food Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Ready-to-Eat Food Market Share (%) by Company 2024

List of Tables

- Table 1: North America Ready-to-Eat Food Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Ready-to-Eat Food Market Revenue Million Forecast, by Product Type 2019 & 2032

- Table 3: North America Ready-to-Eat Food Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 4: North America Ready-to-Eat Food Market Revenue Million Forecast, by Geography 2019 & 2032

- Table 5: North America Ready-to-Eat Food Market Revenue Million Forecast, by Region 2019 & 2032

- Table 6: North America Ready-to-Eat Food Market Revenue Million Forecast, by Country 2019 & 2032

- Table 7: United States North America Ready-to-Eat Food Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Canada North America Ready-to-Eat Food Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Mexico North America Ready-to-Eat Food Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Rest of North America North America Ready-to-Eat Food Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: North America Ready-to-Eat Food Market Revenue Million Forecast, by Product Type 2019 & 2032

- Table 12: North America Ready-to-Eat Food Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 13: North America Ready-to-Eat Food Market Revenue Million Forecast, by Geography 2019 & 2032

- Table 14: North America Ready-to-Eat Food Market Revenue Million Forecast, by Country 2019 & 2032

- Table 15: North America Ready-to-Eat Food Market Revenue Million Forecast, by Product Type 2019 & 2032

- Table 16: North America Ready-to-Eat Food Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 17: North America Ready-to-Eat Food Market Revenue Million Forecast, by Geography 2019 & 2032

- Table 18: North America Ready-to-Eat Food Market Revenue Million Forecast, by Country 2019 & 2032

- Table 19: North America Ready-to-Eat Food Market Revenue Million Forecast, by Product Type 2019 & 2032

- Table 20: North America Ready-to-Eat Food Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 21: North America Ready-to-Eat Food Market Revenue Million Forecast, by Geography 2019 & 2032

- Table 22: North America Ready-to-Eat Food Market Revenue Million Forecast, by Country 2019 & 2032

- Table 23: North America Ready-to-Eat Food Market Revenue Million Forecast, by Product Type 2019 & 2032

- Table 24: North America Ready-to-Eat Food Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 25: North America Ready-to-Eat Food Market Revenue Million Forecast, by Geography 2019 & 2032

- Table 26: North America Ready-to-Eat Food Market Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Ready-to-Eat Food Market?

The projected CAGR is approximately 3.36%.

2. Which companies are prominent players in the North America Ready-to-Eat Food Market?

Key companies in the market include Premier Foods Group Ltd, Nestle SA, Nomad Foods Ltd, General Mills Inc, The Campbell Soup Company, Dr August Oetker Nahrugsmittel KG, Fleury Michon, Conagra Brands Inc, The Kraft Heinz Company*List Not Exhaustive, McCain Foods Limited.

3. What are the main segments of the North America Ready-to-Eat Food Market?

The market segments include Product Type, Distribution Channel, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

The numerous benefits offered by collagen in the food and beverage industry.

6. What are the notable trends driving market growth?

Convenience of Use Driving the Ready-to-Eat Food Market.

7. Are there any restraints impacting market growth?

Increasing vegan population in the region.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Ready-to-Eat Food Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Ready-to-Eat Food Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Ready-to-Eat Food Market?

To stay informed about further developments, trends, and reports in the North America Ready-to-Eat Food Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence