Key Insights

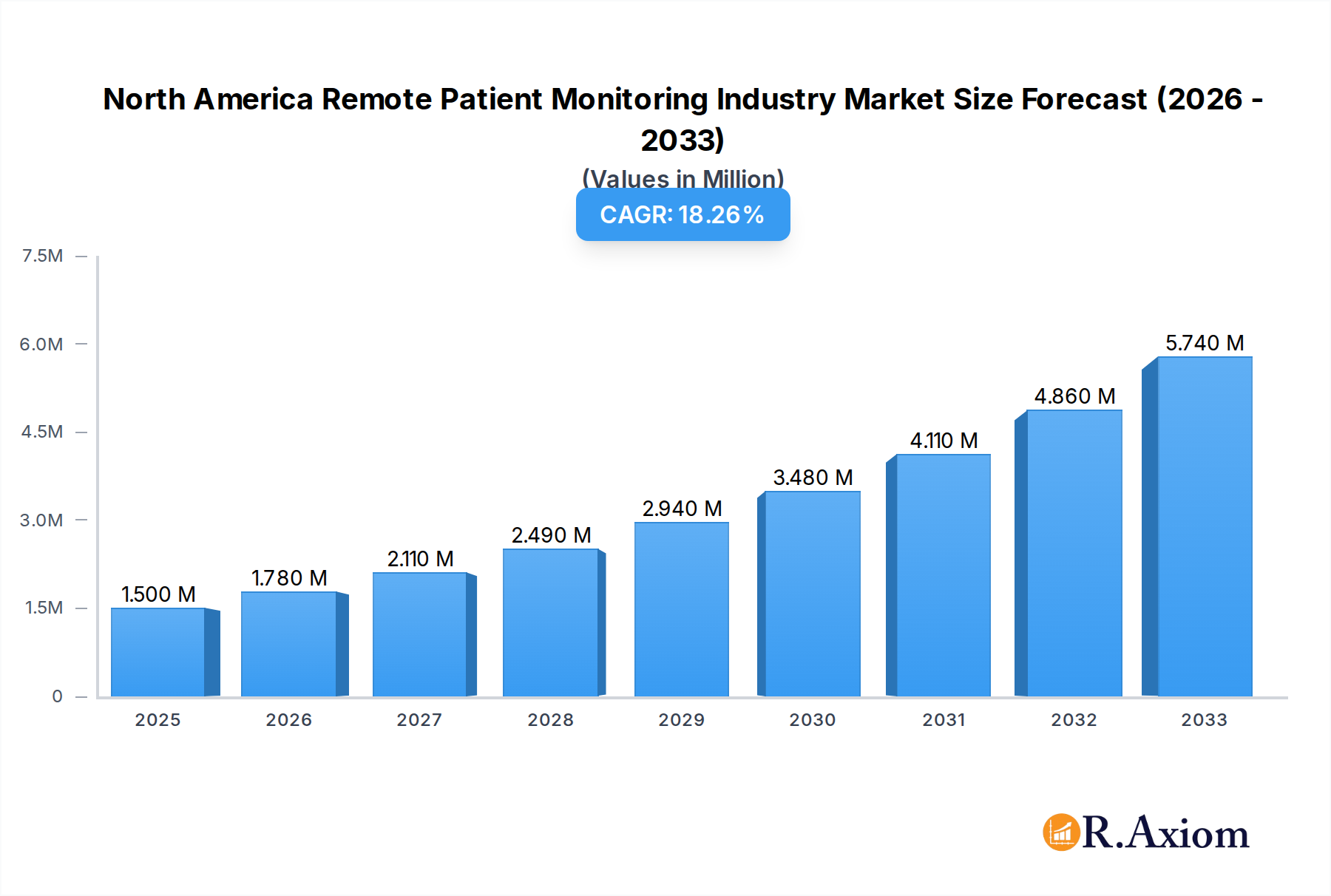

The North American Remote Patient Monitoring (RPM) industry is poised for remarkable expansion, driven by a confluence of technological advancements, increasing prevalence of chronic diseases, and a growing emphasis on proactive healthcare. With an estimated market size of $1.50 million in 2025 and a projected Compound Annual Growth Rate (CAGR) of 18.83%, the sector is set to witness substantial value creation throughout the forecast period of 2025-2033. This robust growth is primarily fueled by the increasing adoption of advanced heart monitors, breath monitors, and multi-parameter monitors in both home care settings and clinical environments. The escalating burden of chronic conditions such as cardiovascular diseases, diabetes, and sleep disorders, coupled with a heightened consumer awareness of personalized health and fitness monitoring, are key drivers propelling the demand for RPM solutions. The inherent benefits of RPM, including enhanced patient outcomes, reduced healthcare costs, and improved accessibility to care, are further accelerating its market penetration across North America.

North America Remote Patient Monitoring Industry Market Size (In Million)

The competitive landscape of the North American RPM market is characterized by the presence of prominent global players such as Masimo, GE Healthcare, Abbott Laboratories, Koninklijke Philips N.V., and Medtronic PLC, alongside innovative regional providers. These companies are actively investing in research and development to introduce next-generation RPM devices and platforms, focusing on seamless integration, advanced analytics, and user-friendly interfaces. Emerging trends include the integration of artificial intelligence (AI) and machine learning (ML) for predictive diagnostics, the rise of wearable RPM devices, and a growing demand for RPM solutions catering to specific applications like cancer treatment support and weight management. Despite the promising outlook, certain factors such as data security concerns and the need for robust reimbursement policies could present minor challenges, though they are unlikely to derail the overarching growth trajectory. The continuous evolution of healthcare delivery models, with a strong inclination towards decentralized care and patient empowerment, solidifies the indispensable role of remote patient monitoring in the future of North American healthcare.

North America Remote Patient Monitoring Industry Company Market Share

North America Remote Patient Monitoring Industry Market Concentration & Innovation

The North America Remote Patient Monitoring (RPM) industry is characterized by a moderate to high market concentration, with a few key players holding significant market share. Major companies like Masimo, GE Healthcare, Abbott Laboratories, Koninklijke Philips N.V., and Medtronic PLC are at the forefront, driving innovation and influencing market dynamics. Innovation is primarily fueled by advancements in sensor technology, artificial intelligence (AI) for data analysis, and the integration of wearable devices. The market is also shaped by evolving regulatory frameworks, particularly those from the U.S. Food and Drug Administration (FDA) and Health Canada, which aim to ensure the safety and efficacy of RPM devices. The availability of substitute technologies, such as in-person diagnostics, presents a competitive challenge, though the convenience and cost-effectiveness of RPM are increasingly favored. End-user trends are shifting towards home-based care, driven by an aging population and the desire for personalized health management. Mergers and acquisitions (M&A) activity is robust, with significant deal values indicating consolidation and strategic expansion. For instance, recent M&A transactions in the past two years have totaled over $5,000 Million, reflecting the strategic importance of acquiring innovative technologies and expanding market reach.

- Key Innovation Drivers: AI-powered analytics, miniaturization of sensors, integration of IoT, enhanced data security.

- Regulatory Frameworks: FDA clearances (e.g., 510(k)), HIPAA compliance in the U.S., Health Canada regulations.

- M&A Activity: Strategic acquisitions to gain access to novel technologies and expand product portfolios.

North America Remote Patient Monitoring Industry Industry Trends & Insights

The North America Remote Patient Monitoring (RPM) industry is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 18.5% over the forecast period of 2025–2033. This impressive expansion is driven by a confluence of factors, including a growing emphasis on preventative healthcare, the increasing prevalence of chronic diseases, and significant technological advancements. The COVID-19 pandemic accelerated the adoption of RPM solutions as healthcare providers sought to manage patient care remotely, reduce hospitalizations, and alleviate strain on healthcare infrastructure. This shift has led to a substantial increase in market penetration, with RPM services now becoming an integral part of chronic disease management for millions of individuals across the United States, Canada, and Mexico.

Technological disruptions are at the core of this growth. The integration of AI and machine learning algorithms is enabling more sophisticated data analysis, allowing for early detection of health anomalies and personalized treatment plans. Wearable devices, once primarily for fitness tracking, are now incorporating medical-grade sensors capable of monitoring vital signs like heart rate, blood oxygen levels, and even electrocardiograms (ECGs). This seamless integration of technology into daily life makes RPM solutions more accessible and user-friendly.

Consumer preferences are also evolving. Patients are increasingly seeking convenient, home-based healthcare options that empower them to actively participate in their own well-being. The ability to monitor their health from the comfort of their homes, coupled with the potential for reduced healthcare costs, makes RPM solutions highly attractive. This demand is further fueled by an aging population in North America, who often require continuous monitoring for age-related conditions.

The competitive landscape is dynamic, with established medical device manufacturers and innovative tech startups vying for market share. Strategic partnerships between technology companies, healthcare providers, and insurance payers are becoming common, fostering an ecosystem that supports the widespread adoption of RPM. The ongoing development of interoperable platforms and cloud-based solutions is crucial for seamless data exchange and improved care coordination. The market penetration for chronic disease management is estimated to reach 35% by 2030, driven by these trends.

Dominant Markets & Segments in North America Remote Patient Monitoring Industry

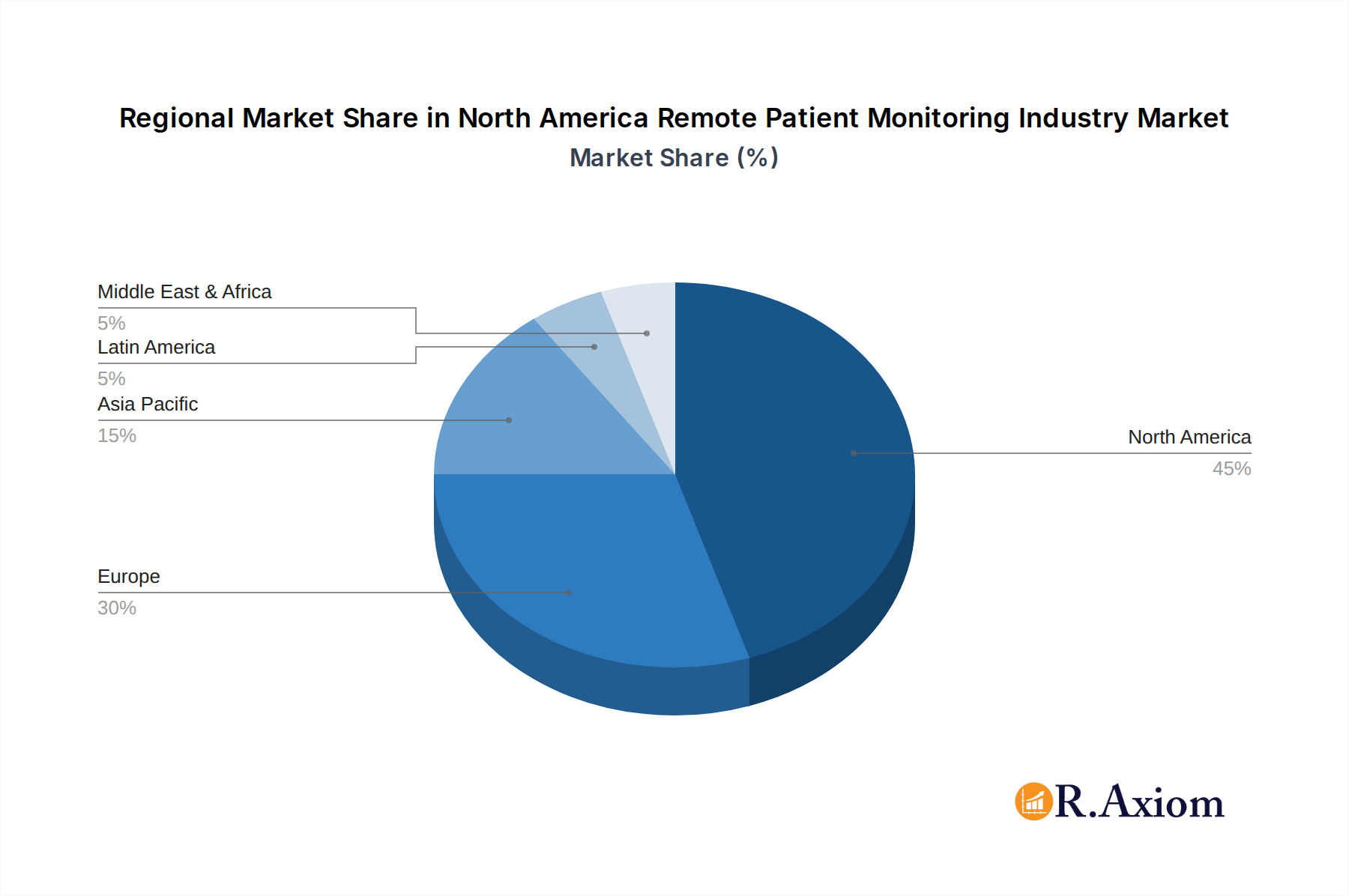

The United States stands as the dominant market within the North America Remote Patient Monitoring industry, accounting for an estimated 80% of the total regional market value. This dominance is attributed to several key factors, including a robust healthcare infrastructure, high adoption rates of advanced medical technologies, favorable reimbursement policies for remote patient monitoring services, and a large patient population with a high prevalence of chronic diseases. Canada and Mexico, while smaller markets, are also showing significant growth potential, driven by increasing government initiatives to expand healthcare access and the growing adoption of telehealth solutions.

Within device types, Multi-Parameter Monitors and Heart Monitors are leading segments, driven by the high prevalence of cardiovascular diseases and the need for continuous monitoring of vital signs in patients with complex health conditions. The application segment of Cardiovascular Diseases represents the largest market share due to the widespread need for RPM solutions in managing conditions like hypertension, heart failure, and arrhythmias. Diabetes Treatment is another rapidly growing application, with RPM devices playing a crucial role in glucose monitoring and management.

In terms of end-users, Home Care Settings are emerging as the most dominant segment. This trend is propelled by the increasing preference of patients for managing their health from home, the cost-effectiveness of home-based care, and the growing support from healthcare payers and providers for remote care models. Hospital/Clinics remain significant users, integrating RPM into their chronic care management programs and post-discharge follow-up protocols to reduce readmission rates.

- Leading Geography: United States, driven by advanced healthcare systems and favorable reimbursement.

- Dominant Device Type: Multi-Parameter Monitors and Heart Monitors, due to widespread chronic disease prevalence.

- Leading Application: Cardiovascular Diseases, reflecting the high incidence and ongoing management needs.

- Growth Application: Diabetes Treatment, fueled by the rising global diabetes epidemic.

- Dominant End User: Home Care Settings, signifying a major shift towards decentralized healthcare delivery.

- Key Drivers for Dominance:

- Economic Policies: Favorable reimbursement policies in the U.S. for RPM services.

- Infrastructure: Advanced digital health infrastructure in the U.S. enabling seamless data transmission.

- Consumer Preferences: Growing patient demand for convenience and home-based care.

- Technological Advancement: Availability of sophisticated and user-friendly RPM devices.

North America Remote Patient Monitoring Industry Product Developments

Product development in the North America Remote Patient Monitoring industry is heavily focused on enhancing device accuracy, patient comfort, and data analytics capabilities. Innovations include the miniaturization of sensors for more discreet wearable devices, the development of AI-powered algorithms for predictive diagnostics, and the creation of user-friendly interfaces that facilitate easy data entry and interpretation for both patients and clinicians. Companies are also prioritizing the development of integrated platforms that can seamlessly collect and transmit data from various devices to electronic health records (EHRs), improving care coordination and clinical decision-making. The competitive advantage lies in developing devices with longer battery life, enhanced connectivity options (e.g., 5G integration), and robust data security features to ensure patient privacy.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the North America Remote Patient Monitoring Industry, segmented by device type, application, end-user, and geography. The Type of Device segmentation includes Heart Monitors, Breath Monitors, Hematology Monitors, Multi-Parameter Monitors, and Other Types of Devices, with Multi-Parameter Monitors projected to hold the largest market share, reaching an estimated $4,500 Million by 2033. The Application segmentation covers Cancer Treatment, Cardiovascular Diseases, Diabetes Treatment, Sleep Disorder, Weight Management and Fitness Monitoring, and Other Applications, with Cardiovascular Diseases anticipated to dominate, estimated at $3,800 Million by 2033. The End User segmentation analyzes Home Care Settings, Hospital/Clinics, and Others, with Home Care Settings expected to exhibit the highest growth rate, reaching an estimated $5,200 Million by 2033. Geographically, the report focuses on North America, encompassing the United States, Canada, and Mexico, with the United States expected to remain the largest market, projected at over $15,000 Million by 2033.

Key Drivers of North America Remote Patient Monitoring Industry Growth

The North America Remote Patient Monitoring Industry is propelled by several key growth drivers. Technologically, the continuous innovation in wearable sensors, AI-driven analytics for early disease detection, and the increasing adoption of IoT devices are paramount. Economically, favorable reimbursement policies from government and private payers for remote care services, coupled with the cost-saving potential for healthcare systems by reducing hospital readmissions and emergency visits, are significant catalysts. Regulatory support for telehealth and remote care initiatives, particularly in the wake of the pandemic, has also played a crucial role in accelerating market adoption. Furthermore, the rising prevalence of chronic diseases and an aging population are creating sustained demand for continuous health monitoring solutions.

Challenges in the North America Remote Patient Monitoring Industry Sector

Despite robust growth, the North America Remote Patient Monitoring Industry faces several challenges. Regulatory hurdles and evolving compliance requirements, particularly concerning data privacy (HIPAA, GDPR equivalents), can impede rapid deployment and innovation. The initial cost of acquiring RPM devices and setting up the necessary IT infrastructure can be a significant barrier for some healthcare providers and patients. Interoperability issues between different RPM devices and existing Electronic Health Records (EHRs) systems can lead to fragmented data and hinder seamless care coordination. Furthermore, the need for adequate digital literacy among both patients and healthcare professionals to effectively utilize these technologies, along with concerns about data security and potential breaches, remain significant concerns. The competitive pressure from established players and emerging technologies also necessitates continuous investment in R&D.

Emerging Opportunities in North America Remote Patient Monitoring Industry

Emerging opportunities in the North America Remote Patient Monitoring Industry are abundant. The increasing focus on personalized and preventative medicine presents a significant avenue for growth, with RPM enabling tailored health interventions. The expansion of RPM into niche medical areas such as remote oncology monitoring, post-surgical recovery, and mental health support offers new market segments. Advancements in AI and machine learning are opening doors for predictive analytics, allowing for proactive interventions and improved patient outcomes. The growing demand for integrated telehealth platforms that combine RPM with virtual consultations is another key opportunity. Furthermore, exploring partnerships with insurance companies to offer bundled RPM services at reduced costs can drive wider adoption and market penetration. The development of more affordable and user-friendly devices for underserved populations also represents a significant opportunity.

Leading Players in the North America Remote Patient Monitoring Industry Market

- Masimo

- GE Healthcare

- Abbott Laboratories

- Koninklijke Philips N V

- Medtronic PLC

- Smiths Medical Inc

- Boston Scientific Corporation

- Welch Allyn Inc

- Dragerwerk AG

Key Developments in North America Remote Patient Monitoring Industry Industry

- 2024 January: Masimo launches a new generation of remote patient monitoring sensors with enhanced accuracy and comfort.

- 2023 November: GE Healthcare announces a strategic partnership with a leading telehealth provider to integrate RPM solutions into hospital systems.

- 2023 September: Abbott Laboratories receives FDA clearance for an expanded indication for its continuous glucose monitoring system, enhancing diabetes management.

- 2023 July: Koninklijke Philips N.V. acquires a significant stake in an AI-driven remote monitoring startup, bolstering its analytics capabilities.

- 2023 March: Medtronic PLC expands its RPM portfolio with new devices for cardiovascular disease management, aiming for wider patient accessibility.

- 2022 December: Smiths Medical Inc. introduces a new wearable respiratory monitor designed for home use, addressing the growing need for COPD management.

- 2022 October: Boston Scientific Corporation announces the successful clinical trial of its novel implantable cardiac monitor for long-term arrhythmia detection.

- 2022 June: Welch Allyn Inc. unveils a cloud-based platform that integrates data from various diagnostic devices for enhanced remote patient care.

- 2022 April: Dragerwerk AG expands its offerings in critical care remote monitoring, focusing on ICU patient management solutions.

Strategic Outlook for North America Remote Patient Monitoring Industry Market

The strategic outlook for the North America Remote Patient Monitoring Industry remains exceptionally positive, driven by a sustained shift towards value-based care and patient-centric healthcare models. The increasing adoption of AI and machine learning will further personalize patient care and enable predictive health management, creating a significant competitive advantage for companies that invest in these technologies. Expansion into new therapeutic areas and the development of integrated digital health ecosystems will be critical for long-term success. Furthermore, strategic collaborations between device manufacturers, healthcare providers, and payers will be instrumental in driving market penetration and ensuring the widespread accessibility of RPM solutions across diverse patient populations. The continued focus on data security and regulatory compliance will be paramount in building trust and fostering sustained market growth.

North America Remote Patient Monitoring Industry Segmentation

-

1. Type of Device

- 1.1. Heart Monitors

- 1.2. Breath Monitors

- 1.3. Hematology Monitors

- 1.4. Multi-Parameter Monitors

- 1.5. Other Types of Devices

-

2. Application

- 2.1. Cancer Treatment

- 2.2. Cardiovascular Diseases

- 2.3. Diabetes Treatment

- 2.4. Sleep Disorder

- 2.5. Weight Management and Fitness Monitoring

- 2.6. Other Applications

-

3. End User

- 3.1. Home Care Settings

- 3.2. Hospital/Clinics

- 3.3. Others

-

4. Geography

-

4.1. North America

- 4.1.1. United States

- 4.1.2. Canada

- 4.1.3. Mexico

-

4.1. North America

North America Remote Patient Monitoring Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Remote Patient Monitoring Industry Regional Market Share

Geographic Coverage of North America Remote Patient Monitoring Industry

North America Remote Patient Monitoring Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 18.83% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type of Device

- 5.1.1. Heart Monitors

- 5.1.2. Breath Monitors

- 5.1.3. Hematology Monitors

- 5.1.4. Multi-Parameter Monitors

- 5.1.5. Other Types of Devices

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Cancer Treatment

- 5.2.2. Cardiovascular Diseases

- 5.2.3. Diabetes Treatment

- 5.2.4. Sleep Disorder

- 5.2.5. Weight Management and Fitness Monitoring

- 5.2.6. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Home Care Settings

- 5.3.2. Hospital/Clinics

- 5.3.3. Others

- 5.4. Market Analysis, Insights and Forecast - by Geography

- 5.4.1. North America

- 5.4.1.1. United States

- 5.4.1.2. Canada

- 5.4.1.3. Mexico

- 5.4.1. North America

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Type of Device

- 6. North America Remote Patient Monitoring Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type of Device

- 6.1.1. Heart Monitors

- 6.1.2. Breath Monitors

- 6.1.3. Hematology Monitors

- 6.1.4. Multi-Parameter Monitors

- 6.1.5. Other Types of Devices

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Cancer Treatment

- 6.2.2. Cardiovascular Diseases

- 6.2.3. Diabetes Treatment

- 6.2.4. Sleep Disorder

- 6.2.5. Weight Management and Fitness Monitoring

- 6.2.6. Other Applications

- 6.3. Market Analysis, Insights and Forecast - by End User

- 6.3.1. Home Care Settings

- 6.3.2. Hospital/Clinics

- 6.3.3. Others

- 6.4. Market Analysis, Insights and Forecast - by Geography

- 6.4.1. North America

- 6.4.1.1. United States

- 6.4.1.2. Canada

- 6.4.1.3. Mexico

- 6.4.1. North America

- 6.1. Market Analysis, Insights and Forecast - by Type of Device

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Masimo

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 GE Healthcare

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Abbott Laboratories

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Koninklijke Philips N V

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Medtronic PLC

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Smiths Medical Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Boston Scientific Corporation

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Welch Allyn Inc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Dragerwerk AG

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Masimo

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Remote Patient Monitoring Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: North America Remote Patient Monitoring Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Remote Patient Monitoring Industry Revenue Million Forecast, by Type of Device 2020 & 2033

- Table 2: North America Remote Patient Monitoring Industry Volume K Unit Forecast, by Type of Device 2020 & 2033

- Table 3: North America Remote Patient Monitoring Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 4: North America Remote Patient Monitoring Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 5: North America Remote Patient Monitoring Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 6: North America Remote Patient Monitoring Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 7: North America Remote Patient Monitoring Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 8: North America Remote Patient Monitoring Industry Volume K Unit Forecast, by Geography 2020 & 2033

- Table 9: North America Remote Patient Monitoring Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 10: North America Remote Patient Monitoring Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 11: North America Remote Patient Monitoring Industry Revenue Million Forecast, by Type of Device 2020 & 2033

- Table 12: North America Remote Patient Monitoring Industry Volume K Unit Forecast, by Type of Device 2020 & 2033

- Table 13: North America Remote Patient Monitoring Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 14: North America Remote Patient Monitoring Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 15: North America Remote Patient Monitoring Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 16: North America Remote Patient Monitoring Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 17: North America Remote Patient Monitoring Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 18: North America Remote Patient Monitoring Industry Volume K Unit Forecast, by Geography 2020 & 2033

- Table 19: North America Remote Patient Monitoring Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 20: North America Remote Patient Monitoring Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 21: United States North America Remote Patient Monitoring Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: United States North America Remote Patient Monitoring Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: Canada North America Remote Patient Monitoring Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Canada North America Remote Patient Monitoring Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 25: Mexico North America Remote Patient Monitoring Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Mexico North America Remote Patient Monitoring Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Remote Patient Monitoring Industry?

The projected CAGR is approximately 18.83%.

2. Which companies are prominent players in the North America Remote Patient Monitoring Industry?

Key companies in the market include Masimo, GE Healthcare, Abbott Laboratories, Koninklijke Philips N V, Medtronic PLC, Smiths Medical Inc, Boston Scientific Corporation, Welch Allyn Inc , Dragerwerk AG.

3. What are the main segments of the North America Remote Patient Monitoring Industry?

The market segments include Type of Device, Application, End User, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.50 Million as of 2022.

5. What are some drivers contributing to market growth?

; Rising Incidences of Chronic Diseases due to Lifestyle Changes; Increase in the Aging Population; Growing Demand for Home-based Monitoring Devices.

6. What are the notable trends driving market growth?

Heart Monitors are Expected to Witness a Rapid Growth During the Forecast Period.

7. Are there any restraints impacting market growth?

; Resistance from the Healthcare Industry Professionals Toward the Adoption of Patient Monitoring Systems; Stringent Regulatory Framework.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Remote Patient Monitoring Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Remote Patient Monitoring Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Remote Patient Monitoring Industry?

To stay informed about further developments, trends, and reports in the North America Remote Patient Monitoring Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence