Key Insights

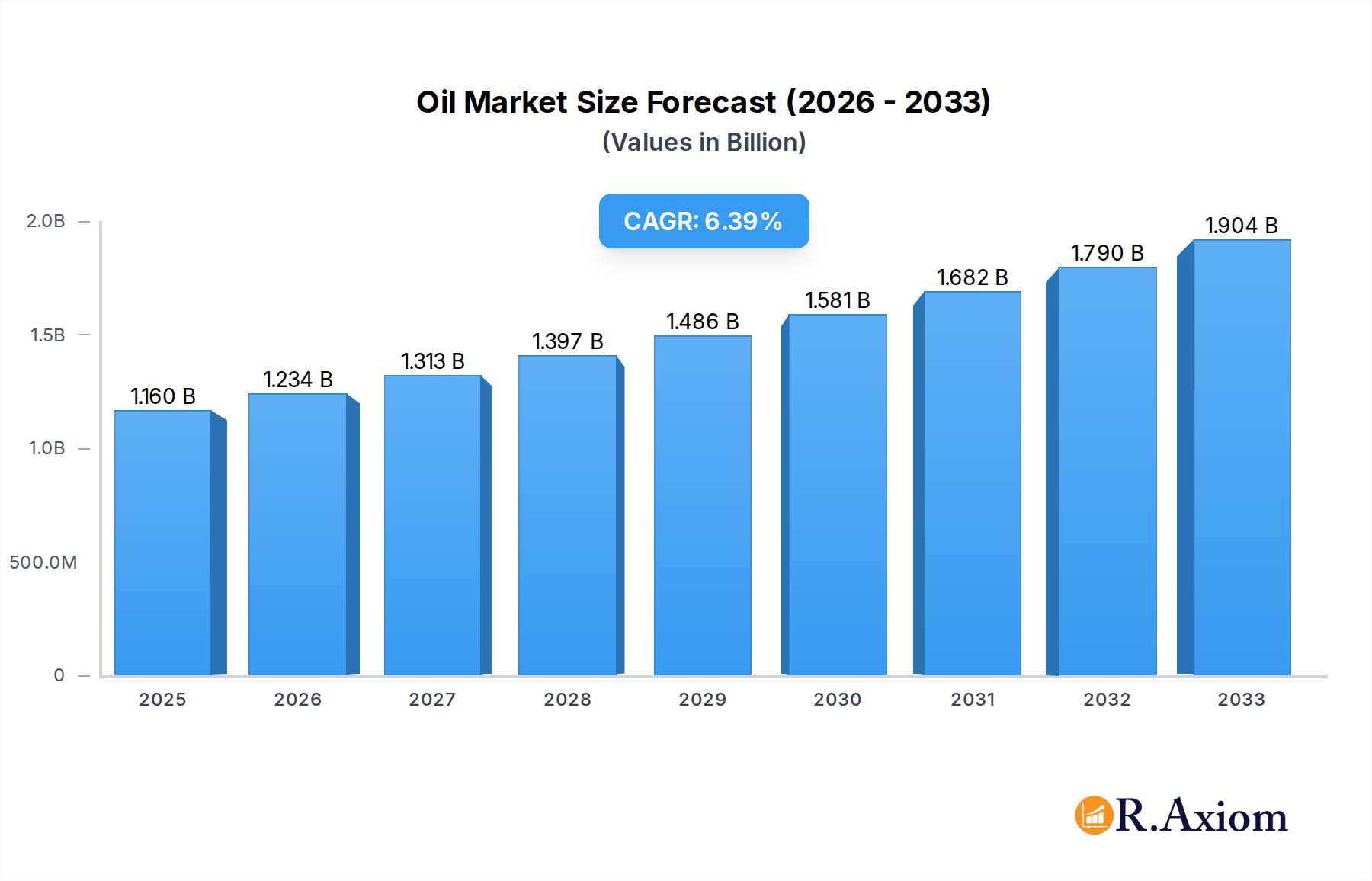

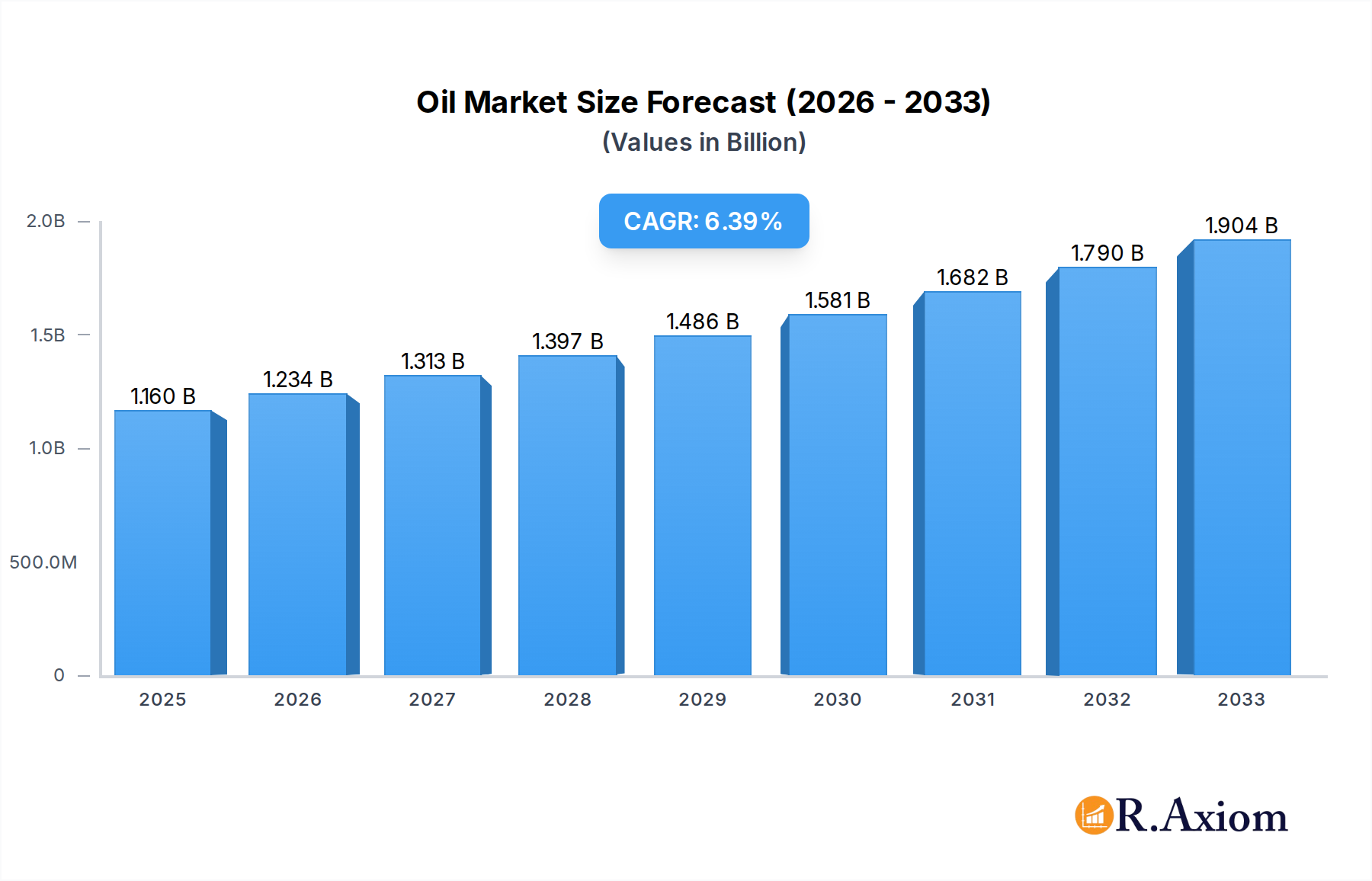

The Oil & Gas Main Automation Contractor (MAC) industry is poised for significant growth, with a market size of USD 1.16 billion and a projected Compound Annual Growth Rate (CAGR) of 6.28% from 2025 to 2033. This expansion is fueled by several critical drivers, including the increasing complexity of offshore and onshore exploration and production, necessitating advanced automation solutions for enhanced efficiency and safety. The midstream sector's demand for sophisticated pipeline monitoring and control systems, coupled with the downstream segment's focus on optimizing refinery operations and minimizing environmental impact, further bolsters market expansion. Furthermore, the continuous evolution of digital technologies, such as the Industrial Internet of Things (IIoT), artificial intelligence (AI), and predictive analytics, is transforming the landscape, enabling predictive maintenance, real-time data analysis, and remote operational management. This technological advancement is a key trend driving the adoption of integrated automation solutions, enhancing operational resilience and profitability across the entire oil and gas value chain.

Oil & Gas Main Automation Contractor Industry Market Size (In Billion)

Despite the robust growth trajectory, the industry faces certain restraints, primarily revolving around the high initial investment costs associated with implementing comprehensive automation systems, particularly for small and medium-sized projects ranging from USD 5 million to USD 30 million. Cybersecurity concerns also present a significant challenge, as increased connectivity in automated systems creates vulnerabilities that require robust protective measures. However, the overarching trend of digitalization and the imperative for operational excellence continue to drive innovation and investment. The market is segmented across upstream (offshore and onshore), midstream, and downstream sectors, with significant opportunities also arising from large-scale projects exceeding USD 31 million. Leading companies such as ABB Ltd., Honeywell International Inc., Emerson Electric Co., Siemens AG, Schneider Electric SE, Rockwell Automation Inc., and Yokogawa Electric Corporation are at the forefront, offering cutting-edge solutions and contributing to the industry's dynamic evolution.

Oil & Gas Main Automation Contractor Industry Company Market Share

Oil & Gas Main Automation Contractor Industry: Comprehensive Market Analysis and Strategic Outlook 2025-2033

This in-depth report provides a definitive analysis of the global Oil & Gas Main Automation Contractor industry, offering critical insights for stakeholders seeking to navigate this dynamic sector. Spanning the historical period of 2019–2024 and projecting to 2033, with a base and estimated year of 2025, this study delves into market concentration, growth drivers, segmentation, competitive landscape, and future opportunities. We examine the crucial role of Main Automation Contractors (MACs) in enabling efficient, safe, and sustainable operations across Upstream, Midstream, and Downstream oil and gas sectors. The report leverages extensive data and expert analysis to forecast market trajectories and identify key strategic imperatives for continued success in this multi-billion dollar market.

Oil & Gas Main Automation Contractor Industry Market Concentration & Innovation

The Oil & Gas Main Automation Contractor industry is characterized by a moderate to high level of market concentration, with a select group of major global players dominating the landscape. These companies, including ABB Ltd, Honeywell International Inc., Emerson Electric Co., Siemens AG, Schneider Electric SE, Rockwell Automation Inc., and Yokogawa Electric Corporation, command significant market share due to their extensive technological capabilities, established global presence, and strong client relationships. Innovation serves as a primary driver, with continuous advancements in Industrial Internet of Things (IIoT), artificial intelligence (AI), machine learning (ML), digital twins, and cybersecurity solutions reshaping the offerings of MACs. These technologies are crucial for optimizing production, enhancing safety protocols, and reducing operational costs for oil and gas companies. Regulatory frameworks, particularly concerning environmental protection, safety standards, and data privacy, also play a pivotal role in shaping industry practices and mandating the adoption of advanced automation solutions. The threat of product substitutes is relatively low for comprehensive main automation contracting services, as specialized expertise and integrated solutions are paramount. End-user trends are heavily influenced by the industry's pursuit of operational efficiency, cost reduction, and decarbonization goals. Mergers and acquisitions (M&A) activities are sporadic but impactful, often driven by strategic consolidation to expand service portfolios, geographical reach, or technological prowess. Recent M&A deals in the broader industrial automation space have seen valuations in the hundreds of millions of dollars. The market size for oil and gas automation is projected to reach over $50 billion by 2028.

Oil & Gas Main Automation Contractor Industry Industry Trends & Insights

The Oil & Gas Main Automation Contractor industry is witnessing robust growth, propelled by several interconnected trends and critical insights. The global market for oil and gas automation is anticipated to expand at a Compound Annual Growth Rate (CAGR) of approximately 7.5% over the forecast period (2025-2033). This growth is primarily fueled by the increasing demand for enhanced operational efficiency and productivity across the entire oil and gas value chain. Companies are investing heavily in automation to streamline complex processes, minimize human intervention in hazardous environments, and optimize resource utilization. The digital transformation wave is a dominant force, with the integration of IIoT devices, cloud computing, and advanced analytics enabling real-time data monitoring, predictive maintenance, and remote asset management. This shift towards data-driven decision-making is enhancing reliability and reducing downtime, thereby improving overall profitability. Technological disruptions, such as the development of AI-powered control systems and autonomous operations, are further revolutionizing how oil and gas facilities are managed. These innovations allow for more intelligent process control, anomaly detection, and optimized performance, contributing to significant cost savings and improved safety records. Consumer preferences are evolving towards solutions that offer greater sustainability and reduced environmental impact. MACs are increasingly expected to provide automation solutions that support emissions monitoring, carbon capture technologies, and energy-efficient operations. The competitive dynamics are intensifying, with established players leveraging their expertise and smaller, specialized firms focusing on niche solutions. The market penetration of advanced automation technologies is steadily increasing, driven by both the economic benefits and the imperative for compliance with stringent environmental and safety regulations. The drive for digital transformation and the pursuit of operational excellence are the bedrock of growth, compelling oil and gas operators to invest in sophisticated automation and control systems provided by specialized MACs. The market is projected to exceed $60 billion by 2030, with significant contributions from both new project installations and upgrade/modernization initiatives in existing facilities.

Dominant Markets & Segments in Oil & Gas Main Automation Contractor Industry

The Oil & Gas Main Automation Contractor industry is segmented across various sectors and project sizes, with distinct dominance patterns observed.

Dominant Sector: Upstream (Offshore and Onshore)

- The Upstream sector, encompassing both offshore and onshore exploration and production, represents the largest and most dynamic segment for Main Automation Contractors. This dominance is driven by the inherent complexity and high-risk nature of upstream operations, necessitating advanced automation for safety, efficiency, and remote management.

- Offshore: The development of deep-sea and harsh-environment offshore fields requires highly sophisticated automation systems for well control, subsea operations, and topside processing. The substantial investment in offshore mega-projects, often valued in the billions of dollars, makes them prime opportunities for large-scale MAC contracts. Economic policies supporting energy security and exploration, coupled with technological advancements in subsea robotics and floating production systems, further bolster this segment.

- Onshore: While perhaps less capital-intensive per project than offshore, the sheer volume of onshore exploration and production activities, particularly in regions with vast reserves, makes it a significant contributor. Automation is crucial for optimizing well performance, managing mid-to-large-scale processing facilities, and enhancing safety in remote or challenging terrains. Infrastructure development and governmental support for domestic energy production are key drivers.

Dominant Project Size: Large (USD 31 million and Above)

- Large-scale projects, typically exceeding USD 31 million, are the primary focus for major Main Automation Contractors. These projects, often involving the construction of new refineries, petrochemical plants, offshore platforms, or the substantial upgrade of existing facilities, demand comprehensive automation solutions that integrate multiple systems.

- The economic policies supporting the development of new energy infrastructure, coupled with the need for cutting-edge technology to ensure operational efficiency and compliance, drive investment in large projects. For example, the construction of a new petrochemical complex or a large offshore production facility can involve MAC contracts worth hundreds of millions of dollars, making them highly lucrative for leading contractors. The long lifecycle of these projects also provides sustained revenue streams for ongoing support and modernization.

Midstream and Downstream Sectors:

- The Midstream sector, encompassing transportation and storage of oil and gas, is also a significant area for automation, particularly for pipeline monitoring, leak detection, and terminal management. While project sizes might vary, the increasing focus on pipeline integrity and safety drives demand for advanced control systems.

- The Downstream sector, including refining and petrochemicals, presents substantial opportunities, especially in the construction of new mega-refineries and specialty chemical plants. The demand for precision control in complex chemical processes, product quality consistency, and stringent environmental regulations are key drivers for automation in this segment. The integration of advanced process control (APC) and optimization software is paramount.

The dominance in these segments is underpinned by the substantial capital investments characteristic of the oil and gas industry, the critical need for safety and reliability, and the ongoing drive to improve operational efficiency and reduce costs through technological advancements.

Oil & Gas Main Automation Contractor Industry Product Developments

Product developments in the Oil & Gas Main Automation Contractor industry are centered on enhancing intelligent automation and digital solutions. Key innovations include the integration of AI and ML for predictive analytics, enabling proactive maintenance and optimizing production parameters. Advanced cybersecurity features are being embedded to protect critical infrastructure from evolving threats. Furthermore, the development of modular and scalable automation platforms allows for flexible deployment and easier upgrades across Upstream, Midstream, and Downstream operations. The focus remains on providing integrated solutions that offer seamless connectivity, real-time data visualization, and remote management capabilities, thereby improving operational efficiency, safety, and environmental compliance for oil and gas enterprises.

Report Scope & Segmentation Analysis

This report meticulously segments the Oil & Gas Main Automation Contractor industry to provide granular insights into specific market dynamics. The segmentation encompasses:

Sector:

- Upstream (Offshore and Onshore): This segment focuses on automation solutions for exploration, drilling, and production activities. Growth projections are robust due to ongoing E&P investments, with market sizes influenced by the number and scale of new field developments. Competitive dynamics are shaped by specialized technological requirements for offshore versus onshore.

- Midstream: This segment covers automation for pipelines, storage terminals, and transportation logistics. Market sizes are driven by infrastructure expansion and maintenance needs, with growth projections indicating steady demand for pipeline integrity management and control systems.

- Downstream: This segment addresses automation for refining, petrochemicals, and chemical processing. Market sizes are substantial, tied to new plant constructions and upgrades. Growth projections are strong, fueled by the demand for precision control, product quality, and environmental compliance.

Project Size:

- Small and Medium (USD 5 million to USD 30 million): This segment involves automation for smaller-scale projects, facility upgrades, or expansions. Growth projections are stable, catering to the ongoing modernization needs of the industry. Competitive dynamics are influenced by agility and cost-effectiveness.

- Large (USD 31 million and Above): This segment covers mega-projects like new refineries, petrochemical complexes, and offshore platforms. Growth projections are significant, driven by major capital investments. Market sizes are substantial, and competitive dynamics are dominated by large, integrated solution providers with extensive project execution capabilities.

Key Drivers of Oil & Gas Main Automation Contractor Industry Growth

The growth of the Oil & Gas Main Automation Contractor industry is propelled by a confluence of powerful factors.

- Technological Advancements: The relentless evolution of technologies such as IIoT, AI, ML, and cloud computing is enabling more sophisticated, efficient, and safer automation solutions. These advancements are critical for optimizing production, predictive maintenance, and real-time operational insights.

- Increasing Demand for Operational Efficiency and Cost Reduction: In an era of volatile commodity prices, oil and gas companies are under immense pressure to enhance productivity, minimize downtime, and reduce operating expenses. Advanced automation directly addresses these needs by streamlining processes and improving resource utilization.

- Stringent Safety and Environmental Regulations: Growing global emphasis on worker safety and environmental protection mandates the adoption of automated systems that reduce human exposure to hazardous conditions and enable better emissions monitoring and control.

- Digital Transformation Initiatives: The broader industry-wide push for digital transformation is accelerating the adoption of integrated automation platforms, data analytics, and smart technologies across the value chain.

Challenges in the Oil & Gas Main Automation Contractor Industry Sector

Despite its growth trajectory, the Oil & Gas Main Automation Contractor industry faces several significant challenges.

- High Initial Investment Costs: The implementation of comprehensive automation systems often requires substantial upfront capital expenditure, which can be a barrier for some companies, particularly in smaller projects or during periods of economic uncertainty.

- Cybersecurity Risks: As operations become more interconnected and digitized, the threat of cyberattacks on critical infrastructure increases. Ensuring robust cybersecurity measures for all automated systems is a continuous and significant challenge.

- Skilled Workforce Shortage: The industry faces a persistent shortage of skilled personnel capable of designing, implementing, operating, and maintaining advanced automation systems, leading to potential project delays and increased operational complexities.

- Regulatory Compliance Complexity: Navigating the diverse and evolving regulatory landscapes across different regions for safety, environmental impact, and data management adds complexity and cost to automation projects.

Emerging Opportunities in Oil & Gas Main Automation Contractor Industry

The Oil & Gas Main Automation Contractor industry is ripe with emerging opportunities driven by new technological paradigms and shifting industry priorities.

- Decarbonization and Energy Transition: The growing focus on sustainability presents significant opportunities for automation solutions that support carbon capture, utilization, and storage (CCUS) technologies, emissions monitoring, and the integration of renewable energy sources into oil and gas operations.

- Digitalization of Brownfield Assets: Modernizing and retrofitting existing (brownfield) oil and gas facilities with advanced automation and IIoT solutions offers a substantial market for MACs seeking to enhance efficiency and safety in established operations.

- Growth in Emerging Markets: Rapid industrialization and increasing energy demands in developing economies are creating new markets for automation projects, particularly in regions with significant untapped hydrocarbon reserves.

- AI and Machine Learning Integration: The continued advancement and adoption of AI and ML for predictive analytics, autonomous operations, and real-time optimization present ongoing opportunities for contractors to offer cutting-edge, value-added solutions.

Leading Players in the Oil & Gas Main Automation Contractor Industry Market

The Oil & Gas Main Automation Contractor industry is characterized by the presence of several global leaders:

- ABB Ltd

- Honeywell International Inc.

- Emerson Electric Co.

- Siemens AG

- Schneider Electric SE

- Rockwell Automation Inc.

- Yokogawa Electric Corporation

Key Developments in Oil & Gas Main Automation Contractor Industry Industry

- June 2022: Honeywell and Anchorage Investments Ltd inked a memorandum of understanding (MoU), opening the door for Honeywell's cutting-edge industrial autonomous technologies to be incorporated into the advanced Anchor Benitoite Petrochemicals Complex, located within Egypt's Suez Canal Economic Zone. As per the terms of the MoU, both companies will commence initial deliberations to appoint Honeywell Process Solutions (HPS) as the integrated main automation contractor (IMAC) for the facility. This development highlights the growing trend of integrating autonomous technologies and strategic partnerships for large-scale petrochemical projects.

- January 2022: Honeywell, a renowned leader in Main Automation Contracts (MAC), inaugurated a state-of-the-art production facility dedicated to oil and gas projects in the Kingdom of Saudi Arabia (KSA). This facility is the result of a joint venture partnership known as Elster Instromet Saudi Arabia, established in collaboration with Gas Arabian Services. It has been designed to provide advanced infrastructure for the manufacturing and assembly of liquid fuel and natural gas solutions, marking a significant milestone in the industry by enhancing local manufacturing capabilities and supply chain resilience for crucial automation components.

Strategic Outlook for Oil & Gas Main Automation Contractor Industry Market

The strategic outlook for the Oil & Gas Main Automation Contractor industry is exceptionally positive, driven by an imperative for greater efficiency, enhanced safety, and environmental stewardship. The ongoing digital transformation, coupled with the global push towards a more sustainable energy future, positions automation as a cornerstone of future oil and gas operations. MACs that can offer integrated, intelligent, and secure solutions, particularly those supporting decarbonization efforts and the modernization of existing assets, will be best positioned for sustained growth. Strategic partnerships, a focus on cybersecurity, and the development of skilled workforces will be critical for navigating the evolving landscape and capitalizing on the immense potential within this multi-billion dollar market. The demand for advanced automation will continue to be a key enabler of operational excellence and profitability in the oil and gas sector for the foreseeable future.

Oil & Gas Main Automation Contractor Industry Segmentation

-

1. Sector

- 1.1. Upstream (Offshore and Onshore)

- 1.2. Midstream

- 1.3. Downstream

-

2. Project Size

- 2.1. Small and Medium (USD 5 million to USD 30 million)

- 2.2. Large (USD 31 million and Above)

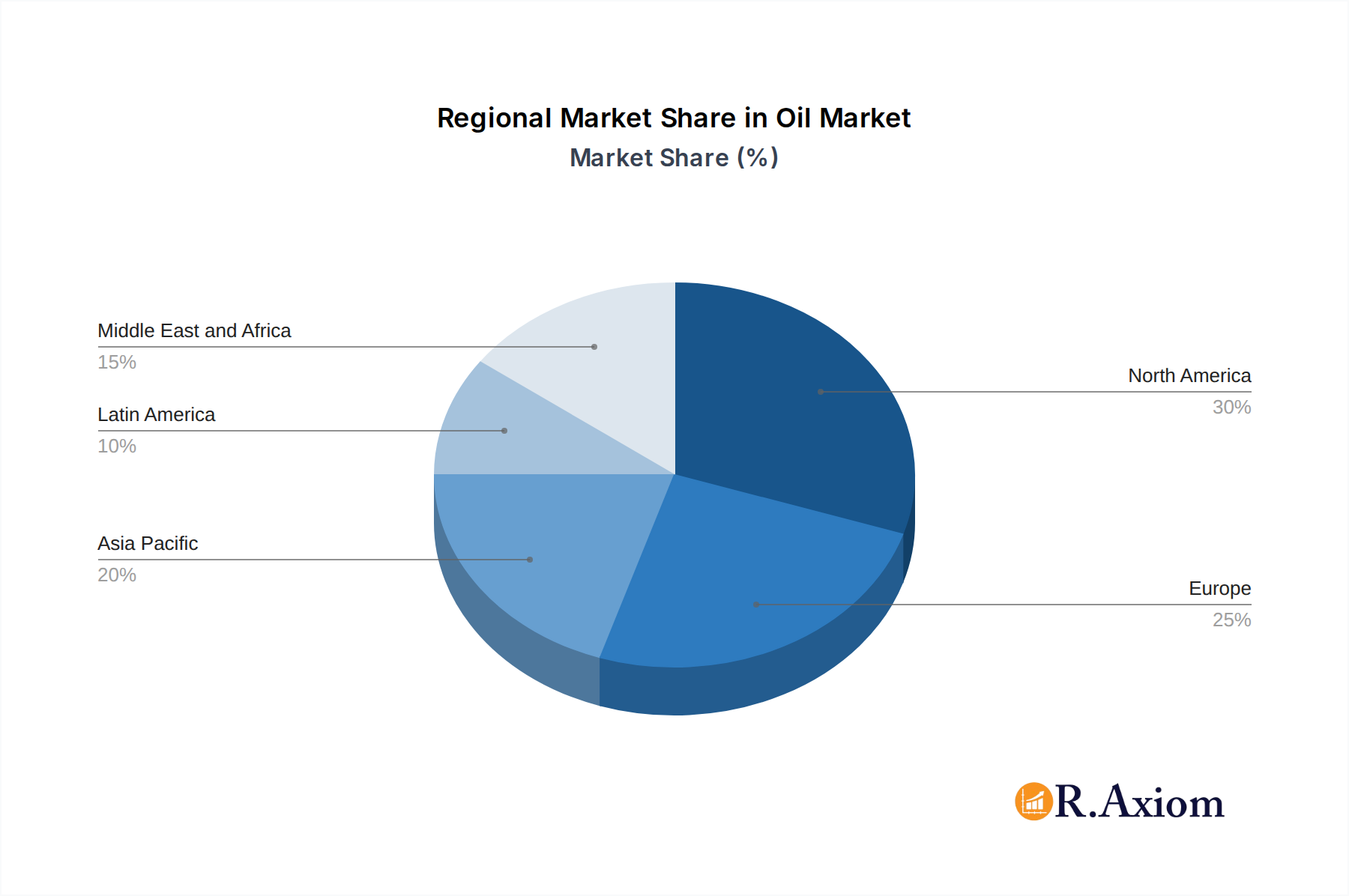

Oil & Gas Main Automation Contractor Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Oil & Gas Main Automation Contractor Industry Regional Market Share

Geographic Coverage of Oil & Gas Main Automation Contractor Industry

Oil & Gas Main Automation Contractor Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.28% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 5.1.1. Upstream (Offshore and Onshore)

- 5.1.2. Midstream

- 5.1.3. Downstream

- 5.2. Market Analysis, Insights and Forecast - by Project Size

- 5.2.1. Small and Medium (USD 5 million to USD 30 million)

- 5.2.2. Large (USD 31 million and Above)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 6. Global Oil & Gas Main Automation Contractor Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Sector

- 6.1.1. Upstream (Offshore and Onshore)

- 6.1.2. Midstream

- 6.1.3. Downstream

- 6.2. Market Analysis, Insights and Forecast - by Project Size

- 6.2.1. Small and Medium (USD 5 million to USD 30 million)

- 6.2.2. Large (USD 31 million and Above)

- 6.1. Market Analysis, Insights and Forecast - by Sector

- 7. North America Oil & Gas Main Automation Contractor Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Sector

- 7.1.1. Upstream (Offshore and Onshore)

- 7.1.2. Midstream

- 7.1.3. Downstream

- 7.2. Market Analysis, Insights and Forecast - by Project Size

- 7.2.1. Small and Medium (USD 5 million to USD 30 million)

- 7.2.2. Large (USD 31 million and Above)

- 7.1. Market Analysis, Insights and Forecast - by Sector

- 8. Europe Oil & Gas Main Automation Contractor Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Sector

- 8.1.1. Upstream (Offshore and Onshore)

- 8.1.2. Midstream

- 8.1.3. Downstream

- 8.2. Market Analysis, Insights and Forecast - by Project Size

- 8.2.1. Small and Medium (USD 5 million to USD 30 million)

- 8.2.2. Large (USD 31 million and Above)

- 8.1. Market Analysis, Insights and Forecast - by Sector

- 9. Asia Pacific Oil & Gas Main Automation Contractor Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Sector

- 9.1.1. Upstream (Offshore and Onshore)

- 9.1.2. Midstream

- 9.1.3. Downstream

- 9.2. Market Analysis, Insights and Forecast - by Project Size

- 9.2.1. Small and Medium (USD 5 million to USD 30 million)

- 9.2.2. Large (USD 31 million and Above)

- 9.1. Market Analysis, Insights and Forecast - by Sector

- 10. Latin America Oil & Gas Main Automation Contractor Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Sector

- 10.1.1. Upstream (Offshore and Onshore)

- 10.1.2. Midstream

- 10.1.3. Downstream

- 10.2. Market Analysis, Insights and Forecast - by Project Size

- 10.2.1. Small and Medium (USD 5 million to USD 30 million)

- 10.2.2. Large (USD 31 million and Above)

- 10.1. Market Analysis, Insights and Forecast - by Sector

- 11. Middle East and Africa Oil & Gas Main Automation Contractor Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Sector

- 11.1.1. Upstream (Offshore and Onshore)

- 11.1.2. Midstream

- 11.1.3. Downstream

- 11.2. Market Analysis, Insights and Forecast - by Project Size

- 11.2.1. Small and Medium (USD 5 million to USD 30 million)

- 11.2.2. Large (USD 31 million and Above)

- 11.1. Market Analysis, Insights and Forecast - by Sector

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 ABB Lt

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Honeywell International Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Emerson Electric Co

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Siemens AG

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Schneider Electric SE

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Rockwell Automation Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Yokogawa Electric Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.1 ABB Lt

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Oil & Gas Main Automation Contractor Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Oil & Gas Main Automation Contractor Industry Revenue (Million), by Sector 2025 & 2033

- Figure 3: North America Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Sector 2025 & 2033

- Figure 4: North America Oil & Gas Main Automation Contractor Industry Revenue (Million), by Project Size 2025 & 2033

- Figure 5: North America Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Project Size 2025 & 2033

- Figure 6: North America Oil & Gas Main Automation Contractor Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Oil & Gas Main Automation Contractor Industry Revenue (Million), by Sector 2025 & 2033

- Figure 9: Europe Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Sector 2025 & 2033

- Figure 10: Europe Oil & Gas Main Automation Contractor Industry Revenue (Million), by Project Size 2025 & 2033

- Figure 11: Europe Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Project Size 2025 & 2033

- Figure 12: Europe Oil & Gas Main Automation Contractor Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Oil & Gas Main Automation Contractor Industry Revenue (Million), by Sector 2025 & 2033

- Figure 15: Asia Pacific Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Sector 2025 & 2033

- Figure 16: Asia Pacific Oil & Gas Main Automation Contractor Industry Revenue (Million), by Project Size 2025 & 2033

- Figure 17: Asia Pacific Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Project Size 2025 & 2033

- Figure 18: Asia Pacific Oil & Gas Main Automation Contractor Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Pacific Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America Oil & Gas Main Automation Contractor Industry Revenue (Million), by Sector 2025 & 2033

- Figure 21: Latin America Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Sector 2025 & 2033

- Figure 22: Latin America Oil & Gas Main Automation Contractor Industry Revenue (Million), by Project Size 2025 & 2033

- Figure 23: Latin America Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Project Size 2025 & 2033

- Figure 24: Latin America Oil & Gas Main Automation Contractor Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Latin America Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Oil & Gas Main Automation Contractor Industry Revenue (Million), by Sector 2025 & 2033

- Figure 27: Middle East and Africa Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Sector 2025 & 2033

- Figure 28: Middle East and Africa Oil & Gas Main Automation Contractor Industry Revenue (Million), by Project Size 2025 & 2033

- Figure 29: Middle East and Africa Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Project Size 2025 & 2033

- Figure 30: Middle East and Africa Oil & Gas Main Automation Contractor Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Middle East and Africa Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Sector 2020 & 2033

- Table 2: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Project Size 2020 & 2033

- Table 3: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Sector 2020 & 2033

- Table 5: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Project Size 2020 & 2033

- Table 6: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Sector 2020 & 2033

- Table 8: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Project Size 2020 & 2033

- Table 9: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 10: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Sector 2020 & 2033

- Table 11: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Project Size 2020 & 2033

- Table 12: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Sector 2020 & 2033

- Table 14: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Project Size 2020 & 2033

- Table 15: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Sector 2020 & 2033

- Table 17: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Project Size 2020 & 2033

- Table 18: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Oil & Gas Main Automation Contractor Industry?

The projected CAGR is approximately 6.28%.

2. Which companies are prominent players in the Oil & Gas Main Automation Contractor Industry?

Key companies in the market include ABB Lt, Honeywell International Inc, Emerson Electric Co, Siemens AG, Schneider Electric SE, Rockwell Automation Inc, Yokogawa Electric Corporation.

3. What are the main segments of the Oil & Gas Main Automation Contractor Industry?

The market segments include Sector, Project Size.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.16 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Preference of Oil and Gas Companies for a MAC Approach to Avoid Project Management and Integration Complexities.

6. What are the notable trends driving market growth?

Upstream Segment to Witness Significant Growth.

7. Are there any restraints impacting market growth?

Additional Costs Associated with Machine Safety Systems.

8. Can you provide examples of recent developments in the market?

June 2022: In a significant development, Honeywell and Anchorage Investments Ltd inked a memorandum of understanding (MoU), opening the door for Honeywell's cutting-edge industrial autonomous technologies to be incorporated into the advanced Anchor Benitoite Petrochemicals Complex, located within Egypt's Suez Canal Economic Zone. As per the terms of the MoU, both companies will commence initial deliberations to appoint Honeywell Process Solutions (HPS) as the integrated main automation contractor (IMAC) for the facility.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Oil & Gas Main Automation Contractor Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Oil & Gas Main Automation Contractor Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Oil & Gas Main Automation Contractor Industry?

To stay informed about further developments, trends, and reports in the Oil & Gas Main Automation Contractor Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence