Key Insights

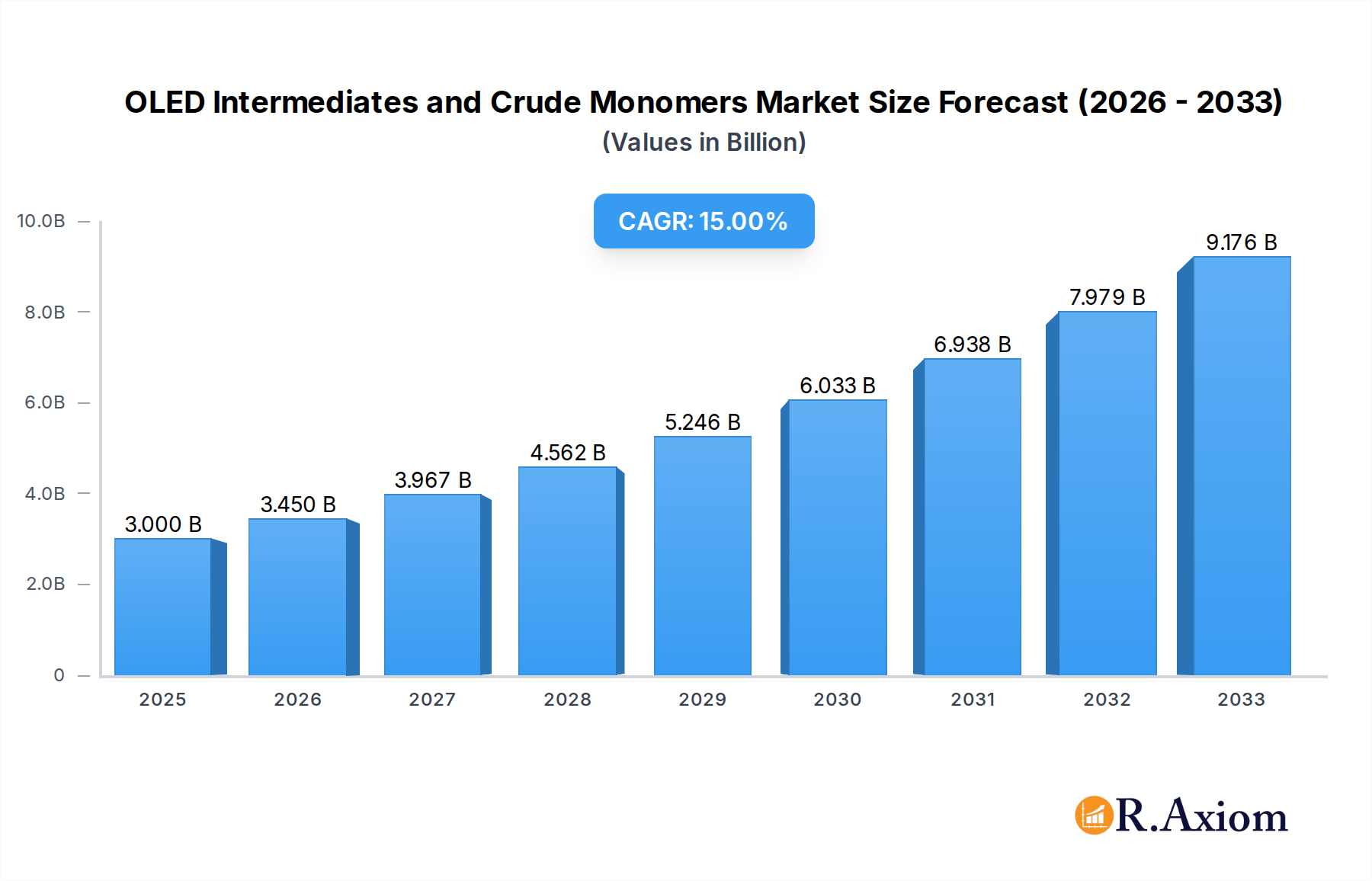

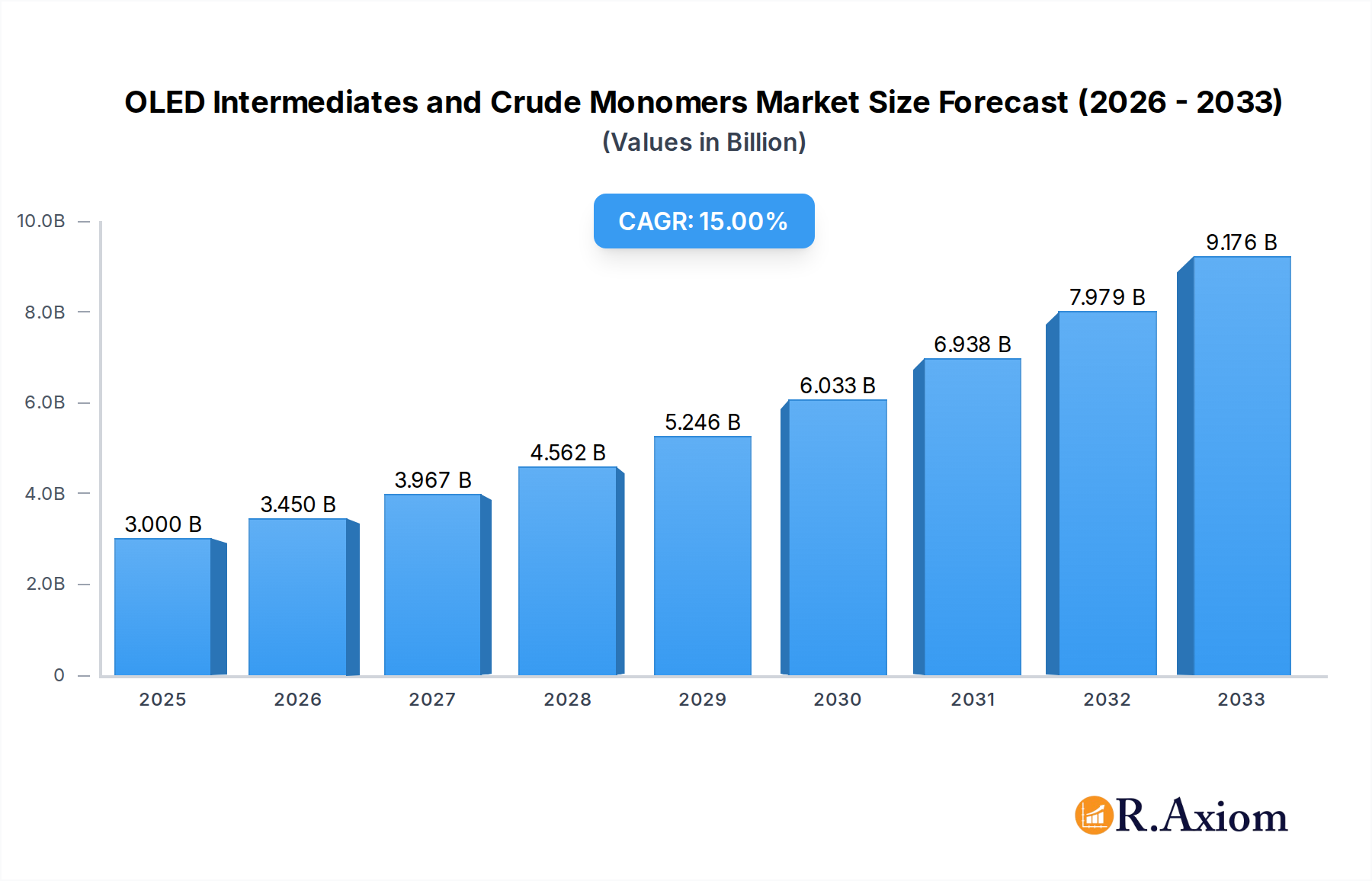

The global market for OLED Intermediates and Crude Monomers is poised for substantial growth, driven by the escalating demand for advanced display technologies across various consumer electronics and emerging applications. With an estimated market size of USD 3 billion in 2025, the sector is projected to expand at a robust Compound Annual Growth Rate (CAGR) of 15% through 2033. This remarkable growth is primarily fueled by the widespread adoption of OLED technology in smartphones, televisions, wearables, and automotive displays, which offer superior visual quality, energy efficiency, and design flexibility compared to traditional LCD panels. Furthermore, the increasing investment in research and development for next-generation OLED applications, such as flexible and transparent displays, is expected to create new avenues for market expansion. Key industry players are actively investing in capacity expansion and technological innovation to meet this surging demand and maintain a competitive edge.

OLED Intermediates and Crude Monomers Market Size (In Billion)

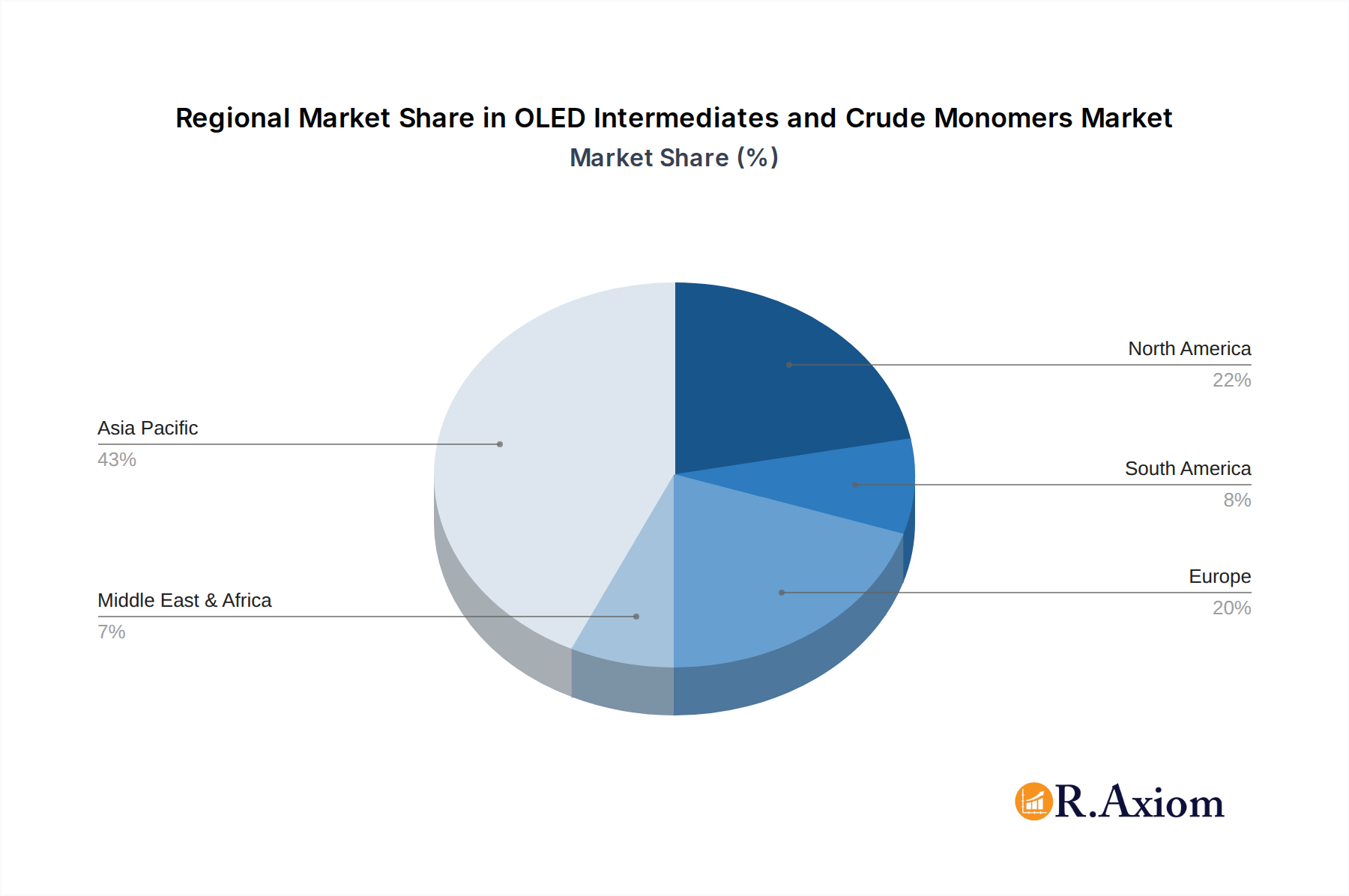

Despite the promising outlook, certain factors could pose challenges to market expansion. Supply chain complexities and fluctuations in raw material costs for OLED intermediates and crude monomers can impact profitability and production efficiency. Additionally, the high cost of OLED manufacturing equipment and the need for specialized expertise present barriers to entry for new players, potentially consolidating the market among established companies. Nevertheless, the fundamental drivers of OLED adoption, including its superior performance characteristics and growing integration into diverse product categories, are expected to outweigh these restraints. The market is segmented into OLED Panel applications, encompassing a broad range of display products, and other applications that leverage OLED technology. Within the product types, OLED Intermediates and OLED Coarse Monomers form the foundational building blocks for these advanced displays. The dominant regions for market growth are anticipated to be Asia Pacific, owing to the concentration of electronics manufacturing and a burgeoning consumer base, followed by North America and Europe, driven by premium product adoption and technological advancements.

OLED Intermediates and Crude Monomers Company Market Share

This in-depth report provides an exhaustive analysis of the global OLED Intermediates and Crude Monomers market, covering historical trends, current dynamics, and future projections. Spanning the Study Period of 2019–2033, with a Base Year of 2025 and an Estimated Year also of 2025, the report offers critical insights for stakeholders involved in the high-growth OLED technology ecosystem. The Forecast Period extends from 2025–2033, capturing the crucial expansion phase of this vital industry. Focusing on OLED Intermediate and OLED Coarse Monomer types, and examining applications in OLED Panel and Others, this report is an indispensable resource for understanding market concentration, innovation, dominant segments, product developments, key drivers, challenges, and emerging opportunities. With a projected market value reaching billions, this report details the strategic landscape shaped by key players like B&S Group, Henan Daken Chemical Co.,ltd, Guangdong Aglaia, Valiant Co.,Ltd, Shaanxi Lighte Optoelectronics, Puyang Huicheng, Beijing Greenguardee, Henan Sunfine Material, Jiangxi Guanmat Optoelectronic, Jilin Oled Material, and Yantai Jiumu Chemical Co.,Ltd.

OLED Intermediates and Crude Monomers Market Concentration & Innovation

The global OLED Intermediates and Crude Monomers market exhibits a moderate concentration, characterized by the presence of both established chemical giants and specialized niche players. Innovation is a paramount driver, with significant R&D investments directed towards developing novel, high-purity materials that enhance OLED device performance, longevity, and energy efficiency. The market's trajectory is influenced by evolving regulatory frameworks, particularly concerning environmental sustainability and chemical safety, which necessitate continuous process optimization and compliance. While direct product substitutes for OLED intermediates and monomers are limited in their ability to replicate OLED performance, advancements in alternative display technologies can indirectly impact demand. End-user trends, heavily driven by consumer electronics manufacturers' pursuit of thinner, brighter, and more flexible displays, are shaping the demand for specific material properties. Mergers and acquisitions (M&A) activities, valued in the billions, are anticipated to continue as companies seek to consolidate market share, acquire critical intellectual property, and expand their product portfolios. For instance, strategic acquisitions in the historical period have bolstered the capabilities of key entities, with M&A deal values in the billions demonstrating a strong consolidation trend.

OLED Intermediates and Crude Monomers Industry Trends & Insights

The OLED Intermediates and Crude Monomers industry is poised for remarkable growth, propelled by a confluence of technological advancements and burgeoning market demand. A significant market penetration rate is already evident, and the Compound Annual Growth Rate (CAGR) is projected to be exceptionally high throughout the forecast period. Key growth drivers include the escalating adoption of OLED technology in smartphones, televisions, wearables, and automotive displays, where superior contrast ratios, vibrant colors, and power efficiency are highly valued. Technological disruptions are constant, with ongoing research into new molecular structures for emissive layers, charge transport layers, and host materials, aiming to achieve higher quantum efficiencies and longer operational lifetimes, thereby reducing the overall cost of OLED panel production. Consumer preferences are increasingly leaning towards premium display experiences, fueling the demand for advanced OLED features. Competitive dynamics are intense, with companies investing heavily in proprietary synthesis routes and purification techniques to gain a competitive edge. The market is experiencing a continuous influx of new entrants and a strengthening of existing players' positions, all contributing to a dynamic and evolving landscape. The estimated market size in the base year is projected to reach billions, underscoring the economic significance of this sector. Continuous innovation in material science is crucial for maintaining market leadership and unlocking new application potentials.

Dominant Markets & Segments in OLED Intermediates and Crude Monomers

The OLED Panel application segment is unequivocally dominant within the OLED Intermediates and Crude Monomers market, accounting for the lion's share of demand. This dominance is primarily driven by the widespread integration of OLED technology in consumer electronics, with smartphones being the largest sub-segment. The increasing demand for high-resolution, energy-efficient displays in televisions and the growing adoption in smartwatches and other wearables further solidify this segment's leading position.

- Key Drivers for OLED Panel Dominance:

- Technological Superiority: OLED technology offers unparalleled contrast ratios, true blacks, wider color gamuts, and faster response times compared to traditional LCD technologies.

- Consumer Preference for Premium Displays: Consumers increasingly associate OLED with a superior viewing experience, driving demand for OLED-equipped devices.

- Advancements in Manufacturing Efficiency: Continuous improvements in OLED manufacturing processes, including material synthesis and panel fabrication, are making OLED displays more cost-competitive.

- Flexible and Foldable Display Innovation: The ability of OLED to be flexible and foldable opens up new form factors for electronic devices, further boosting demand for the underlying materials.

The OLED Intermediate type segment also commands a significant market share, as these precursor materials are essential building blocks for the synthesis of more complex OLED monomers. The production of high-purity OLED intermediates is critical for ensuring the performance and longevity of the final OLED device.

- Key Drivers for OLED Intermediate Dominance:

- Foundation for Monomer Synthesis: OLED intermediates are the foundational chemicals from which advanced OLED monomers are synthesized.

- Scalability of Production: Established chemical manufacturing processes allow for the large-scale production of intermediates, catering to the high volume demand from monomer manufacturers.

- Purity Requirements: The stringent purity demands of OLED applications necessitate sophisticated synthesis and purification techniques for intermediates.

Geographically, Asia Pacific is the leading region in the OLED Intermediates and Crude Monomers market. This dominance is attributed to the concentration of major OLED panel manufacturers, including South Korea, China, and Taiwan, which are the primary consumers of these chemical precursors. Government initiatives supporting the display industry, substantial R&D investments, and a robust manufacturing ecosystem further bolster the region's leading position.

- Key Drivers for Asia Pacific Dominance:

- Manufacturing Hub for Electronics: The region is the global epicenter for electronics manufacturing, including smartphones and televisions.

- Government Support for High-Tech Industries: Favorable policies and incentives for the display and semiconductor industries.

- Presence of Key OLED Panel Producers: Home to leading global OLED panel manufacturers.

- Integrated Supply Chain: A well-developed and integrated supply chain for display materials.

OLED Intermediates and Crude Monomers Product Developments

Product development in the OLED Intermediates and Crude Monomers sector is characterized by a relentless pursuit of enhanced performance and cost-effectiveness. Innovations focus on synthesizing novel molecular structures that improve charge transport efficiency, reduce voltage requirements, and extend the operational lifespan of OLED devices. Key advancements include the development of more stable and efficient emitter materials, phosphorescent dopants, and host materials tailored for specific color emissions and device architectures. These developments aim to achieve deeper blacks, more vibrant colors, and reduced power consumption, directly translating to superior display quality and user experience. The competitive advantage lies in achieving higher purity levels, lower synthesis costs, and proprietary intellectual property around unique molecular designs that offer distinct performance benefits.

Report Scope & Segmentation Analysis

This report segments the OLED Intermediates and Crude Monomers market based on Application into OLED Panel and Others. The OLED Panel segment is expected to witness substantial growth, driven by the ubiquitous demand for advanced displays in consumer electronics and automotive sectors, with a projected market size reaching billions by 2033. The Others segment, encompassing niche applications like specialized lighting and signage, is also projected for steady expansion.

The market is further segmented by Types into OLED Intermediate and OLED Coarse Monomer. The OLED Intermediate segment is foundational, providing the building blocks for advanced materials, and is anticipated to maintain a robust market share, driven by the sheer volume required for OLED panel production. The OLED Coarse Monomer segment, representing more refined precursors, is expected to experience higher growth rates as manufacturers push for greater material sophistication to achieve enhanced device performance, with its market size projected in the billions.

Key Drivers of OLED Intermediates and Crude Monomers Growth

The growth of the OLED Intermediates and Crude Monomers market is underpinned by several critical factors. Technologically, the insatiable demand for superior display performance—higher brightness, better color accuracy, faster refresh rates, and improved energy efficiency—is a primary catalyst. This is directly fueling the need for advanced chemical materials that enable these enhancements. Economically, the increasing disposable income globally and the growing consumer appetite for premium electronics, particularly smartphones and large-screen televisions, translate into increased demand for OLED panels and, consequently, their constituent chemical components. Regulatory factors, while sometimes posing challenges, can also drive growth through mandates for energy efficiency and environmental compliance, encouraging the development of more sustainable and efficient material production processes. The estimated market growth is projected to be in the billions, reflecting these strong underlying economic and technological forces.

Challenges in the OLED Intermediates and Crude Monomers Sector

Despite robust growth, the OLED Intermediates and Crude Monomers sector faces several challenges. Regulatory hurdles, particularly stringent environmental regulations regarding chemical synthesis and waste disposal, can increase operational costs and necessitate significant investment in compliance technologies. Supply chain complexities and the reliance on specialized raw materials can lead to price volatility and potential disruptions, impacting production schedules and profitability. Furthermore, intense competitive pressures from both established chemical giants and agile new entrants drive down profit margins and demand continuous innovation to maintain market share. The cost of production for high-purity OLED materials remains a significant factor, and any disruptions in the supply of critical precursors can lead to substantial financial impacts, estimated in the billions of dollars in potential lost revenue.

Emerging Opportunities in OLED Intermediates and Crude Monomers

Emerging opportunities within the OLED Intermediates and Crude Monomers market are abundant, driven by technological innovation and expanding application frontiers. The development of next-generation OLED materials, such as those for foldable, rollable, and transparent displays, presents a significant growth avenue. Advancements in blue emitter technology, a historically challenging area, offer substantial potential for improving overall OLED efficiency and lifespan. Furthermore, the expansion of OLED applications beyond consumer electronics into automotive displays, medical devices, and smart textiles opens up new, high-value markets. The increasing focus on sustainable manufacturing practices also creates opportunities for companies developing eco-friendly synthesis routes and materials. The projected market expansion is expected to reach billions, fueled by these emerging trends and new market penetrations.

Leading Players in the OLED Intermediates and Crude Monomers Market

- B&S Group

- Henan Daken Chemical Co.,ltd

- Guangdong Aglaia

- Valiant Co.,Ltd

- Shaanxi Lighte Optoelectronics

- Puyang Huicheng

- Beijing Greenguardee

- Henan Sunfine Material

- Jiangxi Guanmat Optoelectronic

- Jilin Oled Material

- Yantai Jiumu Chemical Co.,Ltd.

Key Developments in OLED Intermediates and Crude Monomers Industry

- 2023: Introduction of novel blue emissive materials with enhanced stability and efficiency, significantly improving OLED lifespan and reducing power consumption.

- 2022: Strategic collaborations between chemical manufacturers and OLED panel producers to co-develop customized intermediates for next-generation display technologies, leading to multi-billion dollar partnerships.

- 2021: Significant advancements in purification technologies, achieving ultra-high purity levels for OLED monomers, crucial for meeting the stringent demands of advanced display manufacturing.

- 2020: Increased investment in sustainable synthesis processes and the development of bio-based precursors for OLED materials, aligning with global environmental initiatives.

- 2019: Emergence of specialized companies focusing on the research and development of OLED materials for flexible and transparent display applications, signaling a shift towards innovative form factors.

Strategic Outlook for OLED Intermediates and Crude Monomers Market

The strategic outlook for the OLED Intermediates and Crude Monomers market is exceptionally bright, characterized by sustained high growth and continuous innovation. The increasing demand for premium display experiences across a widening array of electronic devices, coupled with technological breakthroughs in material science, will serve as primary growth catalysts. Companies that can effectively navigate the complexities of high-purity material synthesis, secure robust supply chains, and invest in next-generation material development will be best positioned for success. Strategic partnerships, mergers, and acquisitions will likely continue as firms seek to expand their technological capabilities and market reach. The projected market expansion, expected to reach billions, underscores the immense future potential and opportunities within this dynamic industry.

OLED Intermediates and Crude Monomers Segmentation

-

1. Application

- 1.1. OLED Panel

- 1.2. Others

-

2. Types

- 2.1. OLED Intermediate

- 2.2. OLED Coarse Monomer

OLED Intermediates and Crude Monomers Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

OLED Intermediates and Crude Monomers Regional Market Share

Geographic Coverage of OLED Intermediates and Crude Monomers

OLED Intermediates and Crude Monomers REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global OLED Intermediates and Crude Monomers Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. OLED Panel

- 5.1.2. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. OLED Intermediate

- 5.2.2. OLED Coarse Monomer

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America OLED Intermediates and Crude Monomers Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. OLED Panel

- 6.1.2. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. OLED Intermediate

- 6.2.2. OLED Coarse Monomer

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America OLED Intermediates and Crude Monomers Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. OLED Panel

- 7.1.2. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. OLED Intermediate

- 7.2.2. OLED Coarse Monomer

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe OLED Intermediates and Crude Monomers Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. OLED Panel

- 8.1.2. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. OLED Intermediate

- 8.2.2. OLED Coarse Monomer

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa OLED Intermediates and Crude Monomers Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. OLED Panel

- 9.1.2. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. OLED Intermediate

- 9.2.2. OLED Coarse Monomer

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific OLED Intermediates and Crude Monomers Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. OLED Panel

- 10.1.2. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. OLED Intermediate

- 10.2.2. OLED Coarse Monomer

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 B&S Group

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Henan Daken Chemical Co.

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 ltd

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Guangdong Aglaia

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Valiant Co.

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Ltd

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Shaanxi Lighte Optoelectronics

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Puyang Huicheng

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Beijing Greenguardee

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Henan Sunfine Material

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Jiangxi Guanmat Optoelectronic

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Jilin Oled Material

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Yantai Jiumu Chemical Co.

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Ltd.

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.1 B&S Group

List of Figures

- Figure 1: Global OLED Intermediates and Crude Monomers Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America OLED Intermediates and Crude Monomers Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America OLED Intermediates and Crude Monomers Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America OLED Intermediates and Crude Monomers Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America OLED Intermediates and Crude Monomers Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America OLED Intermediates and Crude Monomers Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America OLED Intermediates and Crude Monomers Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America OLED Intermediates and Crude Monomers Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America OLED Intermediates and Crude Monomers Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America OLED Intermediates and Crude Monomers Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America OLED Intermediates and Crude Monomers Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America OLED Intermediates and Crude Monomers Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America OLED Intermediates and Crude Monomers Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe OLED Intermediates and Crude Monomers Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe OLED Intermediates and Crude Monomers Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe OLED Intermediates and Crude Monomers Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe OLED Intermediates and Crude Monomers Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe OLED Intermediates and Crude Monomers Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe OLED Intermediates and Crude Monomers Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa OLED Intermediates and Crude Monomers Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa OLED Intermediates and Crude Monomers Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa OLED Intermediates and Crude Monomers Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa OLED Intermediates and Crude Monomers Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa OLED Intermediates and Crude Monomers Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa OLED Intermediates and Crude Monomers Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific OLED Intermediates and Crude Monomers Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific OLED Intermediates and Crude Monomers Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific OLED Intermediates and Crude Monomers Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific OLED Intermediates and Crude Monomers Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific OLED Intermediates and Crude Monomers Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific OLED Intermediates and Crude Monomers Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global OLED Intermediates and Crude Monomers Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global OLED Intermediates and Crude Monomers Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global OLED Intermediates and Crude Monomers Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global OLED Intermediates and Crude Monomers Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global OLED Intermediates and Crude Monomers Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global OLED Intermediates and Crude Monomers Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global OLED Intermediates and Crude Monomers Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global OLED Intermediates and Crude Monomers Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global OLED Intermediates and Crude Monomers Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global OLED Intermediates and Crude Monomers Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global OLED Intermediates and Crude Monomers Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global OLED Intermediates and Crude Monomers Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global OLED Intermediates and Crude Monomers Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global OLED Intermediates and Crude Monomers Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global OLED Intermediates and Crude Monomers Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global OLED Intermediates and Crude Monomers Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global OLED Intermediates and Crude Monomers Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global OLED Intermediates and Crude Monomers Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific OLED Intermediates and Crude Monomers Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the OLED Intermediates and Crude Monomers?

The projected CAGR is approximately 15%.

2. Which companies are prominent players in the OLED Intermediates and Crude Monomers?

Key companies in the market include B&S Group, Henan Daken Chemical Co., ltd, Guangdong Aglaia, Valiant Co., Ltd, Shaanxi Lighte Optoelectronics, Puyang Huicheng, Beijing Greenguardee, Henan Sunfine Material, Jiangxi Guanmat Optoelectronic, Jilin Oled Material, Yantai Jiumu Chemical Co., Ltd..

3. What are the main segments of the OLED Intermediates and Crude Monomers?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "OLED Intermediates and Crude Monomers," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the OLED Intermediates and Crude Monomers report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the OLED Intermediates and Crude Monomers?

To stay informed about further developments, trends, and reports in the OLED Intermediates and Crude Monomers, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence