Key Insights

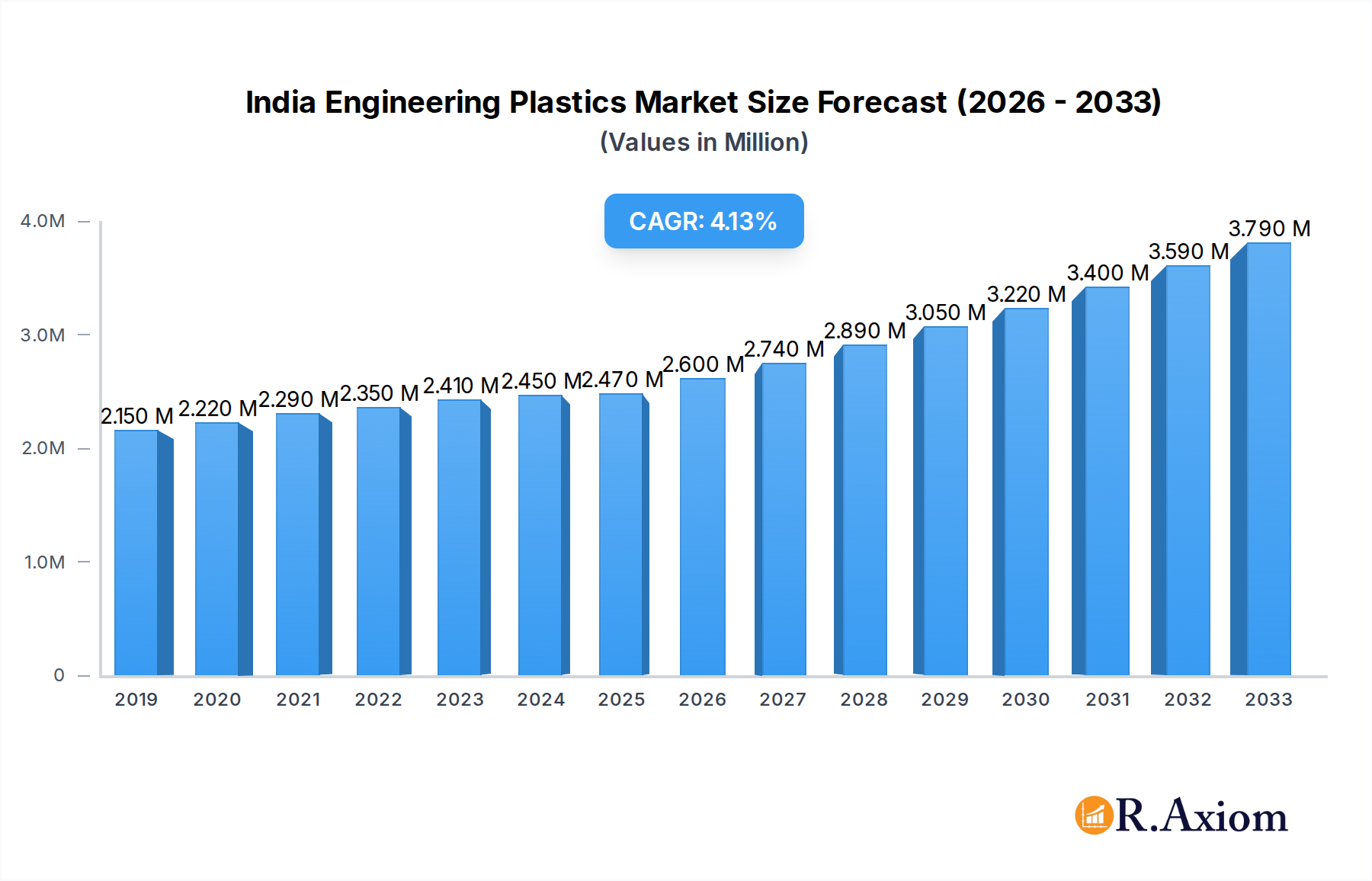

The Indian engineering plastics market is poised for significant expansion, projected to reach an estimated USD 2.47 million by 2025. This growth is underpinned by a robust Compound Annual Growth Rate (CAGR) of 5.31% from 2019 to 2033. Key drivers fueling this upward trajectory include the burgeoning demand from end-user industries such as automotive, electrical and electronics, and building and construction. The automotive sector, in particular, is increasingly adopting engineering plastics for lightweighting initiatives and enhanced fuel efficiency, while the electrical and electronics segment benefits from the material's excellent insulation properties and durability. Furthermore, the 'Make in India' initiative and government support for domestic manufacturing are creating a conducive environment for increased production and consumption of these high-performance materials. The evolving consumer preferences towards durable, aesthetically pleasing, and sustainable products also contribute to the market's buoyancy.

India Engineering Plastics Market Market Size (In Million)

The market's dynamism is further shaped by several prominent trends, including the growing preference for high-performance polymers like Polyether Ether Ketone (PEEK) and Polyvinylidene Fluoride (PVDF) due to their superior thermal and chemical resistance. The increasing focus on sustainability is also driving the adoption of recyclable and bio-based engineering plastics, albeit at an nascent stage. However, certain restraints, such as the volatility in raw material prices and the high initial investment cost for advanced manufacturing facilities, could temper the market's pace. Despite these challenges, the extensive product portfolio, encompassing a wide range of resin types from Fluoropolymers to Polycarbonates and Styrene Copolymers, coupled with the presence of major global and domestic players like Reliance Industries Limited, DuPont, and Mitsubishi Chemical Corporation, indicates a competitive and innovative landscape. The strategic focus on expanding production capacities and developing novel applications will be crucial for capitalizing on the immense growth potential within the Indian engineering plastics market.

India Engineering Plastics Market Company Market Share

India Engineering Plastics Market: Comprehensive Analysis and Future Outlook (2019-2033)

This in-depth report provides a granular analysis of the India Engineering Plastics Market, a dynamic sector poised for significant growth. We explore market trends, key drivers, competitive landscape, and future opportunities from 2019 to 2033, with a base year of 2025. The study encompasses a comprehensive segmentation of end-user industries and resin types, offering actionable insights for stakeholders seeking to capitalize on the expanding Indian market. This report is designed for immediate use without requiring further modification.

India Engineering Plastics Market Market Concentration & Innovation

The India Engineering Plastics Market exhibits a moderately concentrated landscape, with a few dominant players holding substantial market share, alongside a growing number of specialized manufacturers. Innovation is a key driver, fueled by the demand for advanced materials with enhanced properties like high thermal resistance, chemical inertness, and superior mechanical strength. These advancements are critical for applications in the automotive, electrical and electronics, and aerospace sectors. Regulatory frameworks, particularly those promoting sustainable manufacturing and waste management, are increasingly influencing product development and market entry strategies. The threat of product substitutes, while present from commodity plastics in some less demanding applications, is mitigated by the unique performance advantages of engineering plastics. End-user trends, such as lightweighting in automotive and miniaturization in electronics, are consistently pushing the boundaries of material science. Merger and acquisition (M&A) activities, though not extensively detailed here due to placeholder constraints, are expected to play a role in market consolidation and technology acquisition, with potential deal values in the tens to hundreds of millions of dollars.

- Market Concentration: Dominated by a few large players with significant production capacities.

- Innovation Drivers: Demand for high-performance materials, sustainability initiatives, and technological advancements in end-user industries.

- Regulatory Frameworks: Emphasis on environmental compliance, recycling, and safety standards.

- Product Substitutes: Limited in high-performance applications, but a consideration in cost-sensitive segments.

- End-User Trends: Lightweighting, miniaturization, electrification, and enhanced durability.

- M&A Activities: Potential for consolidation and technology integration, with estimated deal values in the range of xx million to xx million.

India Engineering Plastics Market Industry Trends & Insights

The India Engineering Plastics Market is experiencing robust growth, projected to expand at a compound annual growth rate (CAGR) of approximately 7.8% during the forecast period (2025–2033). This upward trajectory is propelled by a confluence of factors including India's burgeoning manufacturing sector, increasing disposable incomes, and a strong push towards self-reliance (Atmanirbhar Bharat) in critical industries. Technological disruptions, such as advancements in polymer synthesis and compounding, are leading to the development of novel engineering plastics with superior performance characteristics. Consumer preferences are shifting towards durable, lightweight, and aesthetically pleasing products, directly impacting the demand for engineering plastics in sectors like consumer durables and packaging. Competitive dynamics are intensifying, with both domestic and international players vying for market share. Manufacturers are investing heavily in research and development to cater to evolving application requirements and to offer sustainable alternatives. The increasing adoption of electric vehicles (EVs), for instance, is creating new avenues for engineering plastics in battery components, charging infrastructure, and lightweight structural elements, replacing traditional metal parts. Furthermore, the "Make in India" initiative and Production Linked Incentive (PLI) schemes are providing a significant impetus for domestic manufacturing and innovation within the engineering plastics domain, fostering higher market penetration across various industrial verticals. The overall market penetration is estimated to reach approximately 65% by 2033.

Dominant Markets & Segments in India Engineering Plastics Market

The Automotive sector is a dominant end-user industry for engineering plastics in India, driven by the constant need for lightweighting to improve fuel efficiency and reduce emissions. The increasing production of passenger cars and commercial vehicles, coupled with the rapid growth of the electric vehicle segment, fuels substantial demand.

- Key Drivers in Automotive:

- Government mandates for fuel efficiency and emission reduction.

- Growing adoption of electric vehicles (EVs).

- Demand for enhanced safety features and aesthetic appeal.

- Cost-effectiveness and design flexibility offered by engineering plastics.

The Electrical and Electronics sector is another significant market, where engineering plastics are indispensable for their insulating properties, flame retardancy, and dimensional stability. The proliferation of consumer electronics, telecommunications infrastructure, and smart grid development are major contributors.

- Key Drivers in Electrical and Electronics:

- Rapid digitalization and expansion of the telecommunications network.

- Growth in the consumer electronics market (smartphones, appliances, TVs).

- Demand for energy-efficient and miniaturized electronic components.

- Stringent safety regulations requiring flame-retardant materials.

Among resin types, Polyamide (PA), particularly PA 6 and PA 66, commands a substantial market share due to its excellent balance of mechanical properties, thermal resistance, and chemical resistance, making it ideal for automotive under-the-hood applications, electrical connectors, and industrial components.

- Dominance of Polyamide (PA):

- PA 6 and PA 66: Widely used in automotive parts like engine covers, intake manifolds, and gears.

- Applications: Electrical casings, power tool housings, and industrial machinery components.

- Growth Factors: Replacement of metal parts, demand for higher performance.

Polycarbonate (PC) is also a leading resin type, valued for its exceptional impact strength, optical clarity, and heat resistance. Its applications span across automotive glazing, electrical enclosures, and medical devices. The increasing use of PC in sustainable packaging solutions is further bolstering its market presence.

- Dominance of Polycarbonate (PC):

- Applications: Automotive headlamp lenses, safety glasses, medical device components.

- Growth Factors: High impact resistance, transparency, and UV stability.

- Emerging Trends: Use in durable consumer goods and renewable energy applications.

The Packaging segment, especially for industrial and specialized food packaging, represents a growing market for engineering plastics, offering superior barrier properties, durability, and shelf-life extension.

- Dominance in Packaging:

- Applications: High-performance films, rigid containers for sensitive goods.

- Growth Factors: Demand for extended shelf life, protection against environmental factors.

India Engineering Plastics Market Product Developments

Product development in the India Engineering Plastics Market is characterized by a strong focus on enhancing performance and sustainability. Manufacturers are introducing advanced grades of existing polymers and exploring novel materials to meet the evolving demands of industries like automotive and electronics. Innovations include the development of higher heat-resistant polyamides, impact-modified polycarbonates, and chemically resistant fluoropolymers. A significant trend is the integration of recycled content and the development of bio-based alternatives to reduce the environmental footprint of engineering plastics. These developments aim to offer improved mechanical strength, chemical resistance, and processing efficiency, providing a competitive edge to end-users by enabling lighter, more durable, and more sustainable products. The market is witnessing a surge in specialized compounds tailored for specific high-growth applications, such as e-mobility and advanced electronics, demonstrating a clear alignment with industry needs.

Report Scope & Segmentation Analysis

This report meticulously analyzes the India Engineering Plastics Market segmented by End User Industry and Resin Type.

End User Industry Segmentation: This includes a detailed examination of Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging, and Other End-user Industries. The automotive sector is projected to lead, driven by vehicle production and electrification. The electrical and electronics segment follows closely, supported by digitalization and consumer demand. Growth projections for these segments are expected to be robust, with the automotive segment estimated to reach approximately INR 15,000 million by 2025 and the electrical and electronics segment around INR 12,000 million.

Resin Type Segmentation: The market is analyzed across Fluoropolymer (further by ETFE, FEP, PTFE, PVF, PVDF, Other Sub Resin Types), Liquid Crystal Polymer (LCP), Polyamide (PA) (Aramid, PA 6, PA 66, Polyphthalamide), Polybutylene Terephthalate (PBT), Polycarbonate (PC), Polyether Ether Ketone (PEEK), Polyethylene Terephthalate (PET), Polyimide (PI), Polymethyl Methacrylate (PMMA), Polyoxymethylene (POM), and Styrene Copolymers (ABS and SAN). Polyamide and Polycarbonate are anticipated to hold significant market shares, driven by their widespread applications. Fluoropolymers will exhibit strong growth due to their niche high-performance applications in demanding environments.

Key Drivers of India Engineering Plastics Market Growth

The growth of the India Engineering Plastics Market is propelled by several key factors. India's rapidly expanding manufacturing base, particularly in the automotive, electrical & electronics, and consumer goods sectors, creates sustained demand for high-performance materials. Government initiatives like "Make in India" and Production Linked Incentive (PLI) schemes are encouraging domestic production and innovation, fostering a conducive environment for market expansion. The increasing disposable income and urbanization are driving consumer demand for durable, aesthetically pleasing, and technologically advanced products, which in turn boosts the consumption of engineering plastics. Furthermore, a global push towards lightweighting and electrification, especially in the automotive industry, is a significant catalyst, as engineering plastics offer superior strength-to-weight ratios compared to traditional materials.

- Manufacturing Sector Growth: Expansion of key industries like automotive and electronics.

- Government Support: Initiatives promoting domestic production and innovation.

- Rising Disposable Income: Increased consumer spending on durable goods.

- Lightweighting and Electrification: Demand for advanced materials in transportation.

- Technological Advancements: Development of higher-performing and sustainable polymer solutions.

Challenges in the India Engineering Plastics Market Sector

Despite the robust growth prospects, the India Engineering Plastics Market faces certain challenges. Fluctuations in raw material prices, particularly crude oil derivatives, can impact manufacturing costs and profit margins. The availability of skilled labor for specialized manufacturing processes and handling advanced materials is another concern. Stringent environmental regulations and the growing emphasis on recyclability and waste management require significant investment in sustainable production practices and infrastructure. Furthermore, competition from lower-cost commodity plastics in less demanding applications and the threat of imports from countries with lower production costs can pose market entry barriers for new players. Supply chain disruptions, as witnessed in recent global events, can also impact the availability and timely delivery of raw materials and finished products.

- Raw Material Price Volatility: Impact on manufacturing costs and profitability.

- Skilled Labor Shortage: Need for specialized expertise in polymer processing.

- Environmental Regulations: Compliance costs and the need for sustainable solutions.

- Competition: Pressure from commodity plastics and imports.

- Supply Chain Vulnerabilities: Potential disruptions affecting availability and delivery.

Emerging Opportunities in India Engineering Plastics Market

The India Engineering Plastics Market is ripe with emerging opportunities. The burgeoning electric vehicle (EV) market presents a significant growth avenue, with demand for lightweight components, battery casings, and high-voltage insulation. The expansion of renewable energy infrastructure, particularly solar power, creates opportunities for engineering plastics in panel frames, connectors, and mounting systems. The growth of the medical devices sector, driven by an aging population and increasing healthcare awareness, offers a strong market for biocompatible and sterilizable engineering plastics. Furthermore, the increasing focus on sustainable packaging solutions, including biodegradable and recyclable engineering plastics, presents a considerable opportunity for market expansion and product innovation. The development of advanced composites and smart polymers with enhanced functionalities will also pave the way for new applications and market penetration.

- Electric Vehicle (EV) Sector: Lightweighting and battery component demand.

- Renewable Energy Infrastructure: Solar panel components and electrical insulation.

- Medical Devices: Biocompatible and sterilizable materials.

- Sustainable Packaging: Biodegradable and recyclable solutions.

- Advanced Composites & Smart Polymers: Novel applications and functionalities.

Leading Players in the India Engineering Plastics Market Market

- JBF Industries Ltd

- INEOS

- Mitsubishi Chemical Corporation

- Gujarat Fluorochemicals Limited (GFL)

- Reliance Industries Limited

- Gujarat State Fertilizers & Chemicals Limited (GSFC)

- LANXESS

- DuPont

- Ester Industries Limited

- IVL Dhunseri Petrochem Industries Private Limited (IDPIPL)

- Polyplex

- Chiripal Poly Film

- Bhansali Engineering Polymers Limited

- Solva

- Hindustan Fluorocarbons Limited

Key Developments in India Engineering Plastics Market Industry

- September 2022: LANXESS introduced Durethan ECO, a sustainable polyamide resin incorporating recycled fibers from waste glass, aiming to reduce its carbon footprint and cater to eco-conscious markets.

- September 2022: LANXESS launched Pocan E, a new polybutylene terephthalate (PBT) compound featuring excellent tracking resistance, specifically designed for demanding applications in e-mobility and the electrical and electronics industry.

- August 2022: INEOS announced the expansion of its high-performance Novodur line with Novodur E3TZ, an extrusion-grade specialty ABS product suitable for diverse applications including food trays, sanitary ware, and luggage.

Strategic Outlook for India Engineering Plastics Market Market

The strategic outlook for the India Engineering Plastics Market is highly promising, driven by strong domestic demand and supportive government policies. The market is expected to witness continued growth fueled by innovation in material science, particularly in areas of sustainability, high-performance applications, and custom compounding. Companies that focus on developing eco-friendly alternatives, investing in R&D for niche applications like electric mobility and advanced electronics, and strengthening their supply chain resilience will be well-positioned for success. Strategic partnerships and collaborations will be crucial for technology adoption and market penetration. The increasing emphasis on localization and the "Make in India" initiative will likely foster greater domestic production capabilities, reducing import reliance and creating export opportunities. The market's future hinges on its ability to adapt to evolving technological landscapes and stringent environmental standards, ensuring long-term sustainable growth.

India Engineering Plastics Market Segmentation

-

1. End User Industry

- 1.1. Aerospace

- 1.2. Automotive

- 1.3. Building and Construction

- 1.4. Electrical and Electronics

- 1.5. Industrial and Machinery

- 1.6. Packaging

- 1.7. Other End-user Industries

-

2. Resin Type

-

2.1. Fluoropolymer

-

2.1.1. By Sub Resin Type

- 2.1.1.1. Ethylenetetrafluoroethylene (ETFE)

- 2.1.1.2. Fluorinated Ethylene-propylene (FEP)

- 2.1.1.3. Polytetrafluoroethylene (PTFE)

- 2.1.1.4. Polyvinylfluoride (PVF)

- 2.1.1.5. Polyvinylidene Fluoride (PVDF)

- 2.1.1.6. Other Sub Resin Types

-

2.1.1. By Sub Resin Type

- 2.2. Liquid Crystal Polymer (LCP)

-

2.3. Polyamide (PA)

- 2.3.1. Aramid

- 2.3.2. Polyamide (PA) 6

- 2.3.3. Polyamide (PA) 66

- 2.3.4. Polyphthalamide

- 2.4. Polybutylene Terephthalate (PBT)

- 2.5. Polycarbonate (PC)

- 2.6. Polyether Ether Ketone (PEEK)

- 2.7. Polyethylene Terephthalate (PET)

- 2.8. Polyimide (PI)

- 2.9. Polymethyl Methacrylate (PMMA)

- 2.10. Polyoxymethylene (POM)

- 2.11. Styrene Copolymers (ABS and SAN)

-

2.1. Fluoropolymer

India Engineering Plastics Market Segmentation By Geography

- 1. India

India Engineering Plastics Market Regional Market Share

Geographic Coverage of India Engineering Plastics Market

India Engineering Plastics Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.31% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 5.1.1. Aerospace

- 5.1.2. Automotive

- 5.1.3. Building and Construction

- 5.1.4. Electrical and Electronics

- 5.1.5. Industrial and Machinery

- 5.1.6. Packaging

- 5.1.7. Other End-user Industries

- 5.2. Market Analysis, Insights and Forecast - by Resin Type

- 5.2.1. Fluoropolymer

- 5.2.1.1. By Sub Resin Type

- 5.2.1.1.1. Ethylenetetrafluoroethylene (ETFE)

- 5.2.1.1.2. Fluorinated Ethylene-propylene (FEP)

- 5.2.1.1.3. Polytetrafluoroethylene (PTFE)

- 5.2.1.1.4. Polyvinylfluoride (PVF)

- 5.2.1.1.5. Polyvinylidene Fluoride (PVDF)

- 5.2.1.1.6. Other Sub Resin Types

- 5.2.1.1. By Sub Resin Type

- 5.2.2. Liquid Crystal Polymer (LCP)

- 5.2.3. Polyamide (PA)

- 5.2.3.1. Aramid

- 5.2.3.2. Polyamide (PA) 6

- 5.2.3.3. Polyamide (PA) 66

- 5.2.3.4. Polyphthalamide

- 5.2.4. Polybutylene Terephthalate (PBT)

- 5.2.5. Polycarbonate (PC)

- 5.2.6. Polyether Ether Ketone (PEEK)

- 5.2.7. Polyethylene Terephthalate (PET)

- 5.2.8. Polyimide (PI)

- 5.2.9. Polymethyl Methacrylate (PMMA)

- 5.2.10. Polyoxymethylene (POM)

- 5.2.11. Styrene Copolymers (ABS and SAN)

- 5.2.1. Fluoropolymer

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. India

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 6. India Engineering Plastics Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End User Industry

- 6.1.1. Aerospace

- 6.1.2. Automotive

- 6.1.3. Building and Construction

- 6.1.4. Electrical and Electronics

- 6.1.5. Industrial and Machinery

- 6.1.6. Packaging

- 6.1.7. Other End-user Industries

- 6.2. Market Analysis, Insights and Forecast - by Resin Type

- 6.2.1. Fluoropolymer

- 6.2.1.1. By Sub Resin Type

- 6.2.1.1.1. Ethylenetetrafluoroethylene (ETFE)

- 6.2.1.1.2. Fluorinated Ethylene-propylene (FEP)

- 6.2.1.1.3. Polytetrafluoroethylene (PTFE)

- 6.2.1.1.4. Polyvinylfluoride (PVF)

- 6.2.1.1.5. Polyvinylidene Fluoride (PVDF)

- 6.2.1.1.6. Other Sub Resin Types

- 6.2.1.1. By Sub Resin Type

- 6.2.2. Liquid Crystal Polymer (LCP)

- 6.2.3. Polyamide (PA)

- 6.2.3.1. Aramid

- 6.2.3.2. Polyamide (PA) 6

- 6.2.3.3. Polyamide (PA) 66

- 6.2.3.4. Polyphthalamide

- 6.2.4. Polybutylene Terephthalate (PBT)

- 6.2.5. Polycarbonate (PC)

- 6.2.6. Polyether Ether Ketone (PEEK)

- 6.2.7. Polyethylene Terephthalate (PET)

- 6.2.8. Polyimide (PI)

- 6.2.9. Polymethyl Methacrylate (PMMA)

- 6.2.10. Polyoxymethylene (POM)

- 6.2.11. Styrene Copolymers (ABS and SAN)

- 6.2.1. Fluoropolymer

- 6.1. Market Analysis, Insights and Forecast - by End User Industry

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 JBF Industries Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 INEOS

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Mitsubishi Chemical Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Gujarat Fluorochemicals Limited (GFL)

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Reliance Industries Limited

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Gujarat State Fertilizers & Chemicals Limited (GSFC)

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 LANXESS

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 DuPont

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Ester Industries Limited

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 IVL Dhunseri Petrochem Industries Private Limited (IDPIPL)

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Polyplex

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Chiripal Poly Film

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Bhansali Engineering Polymers Limited

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Solva

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 Hindustan Fluorocarbons Limited

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.1 JBF Industries Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: India Engineering Plastics Market Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: India Engineering Plastics Market Share (%) by Company 2025

List of Tables

- Table 1: India Engineering Plastics Market Revenue million Forecast, by End User Industry 2020 & 2033

- Table 2: India Engineering Plastics Market Volume K Tons Forecast, by End User Industry 2020 & 2033

- Table 3: India Engineering Plastics Market Revenue million Forecast, by Resin Type 2020 & 2033

- Table 4: India Engineering Plastics Market Volume K Tons Forecast, by Resin Type 2020 & 2033

- Table 5: India Engineering Plastics Market Revenue million Forecast, by Region 2020 & 2033

- Table 6: India Engineering Plastics Market Volume K Tons Forecast, by Region 2020 & 2033

- Table 7: India Engineering Plastics Market Revenue million Forecast, by End User Industry 2020 & 2033

- Table 8: India Engineering Plastics Market Volume K Tons Forecast, by End User Industry 2020 & 2033

- Table 9: India Engineering Plastics Market Revenue million Forecast, by Resin Type 2020 & 2033

- Table 10: India Engineering Plastics Market Volume K Tons Forecast, by Resin Type 2020 & 2033

- Table 11: India Engineering Plastics Market Revenue million Forecast, by Country 2020 & 2033

- Table 12: India Engineering Plastics Market Volume K Tons Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Engineering Plastics Market?

The projected CAGR is approximately 5.31%.

2. Which companies are prominent players in the India Engineering Plastics Market?

Key companies in the market include JBF Industries Ltd, INEOS, Mitsubishi Chemical Corporation, Gujarat Fluorochemicals Limited (GFL), Reliance Industries Limited, Gujarat State Fertilizers & Chemicals Limited (GSFC), LANXESS, DuPont, Ester Industries Limited, IVL Dhunseri Petrochem Industries Private Limited (IDPIPL), Polyplex, Chiripal Poly Film, Bhansali Engineering Polymers Limited, Solva, Hindustan Fluorocarbons Limited.

3. What are the main segments of the India Engineering Plastics Market?

The market segments include End User Industry, Resin Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.47 million as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand in Automotive Industry; Rising Use in Electronics and Electrical Applications.

6. What are the notable trends driving market growth?

Increased Focus on High-Performance Materials.

7. Are there any restraints impacting market growth?

Fluctuating Raw Material Prices.

8. Can you provide examples of recent developments in the market?

September 2022: LANXESS introduced a sustainable polyamide resin, Durethan ECO, which consists of recycled fibers made from waste glass to reduce its carbon footprint.September 2022: LANXESS introduced Pocan E, a new polybutylene terephthalate (PBT) compound with excellent tracking resistance that is particularly suited to applications in e-mobility and the electrical and electronics industry.August 2022: INEOS announced the introduction of an extension to its high-performance Novodur line of specialty ABS products. The new Novodur E3TZ is an extrusion grade that is suitable for a variety of applications, including food trays, sanitary applications, and suitcases.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Engineering Plastics Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Engineering Plastics Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Engineering Plastics Market?

To stay informed about further developments, trends, and reports in the India Engineering Plastics Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence