Key Insights

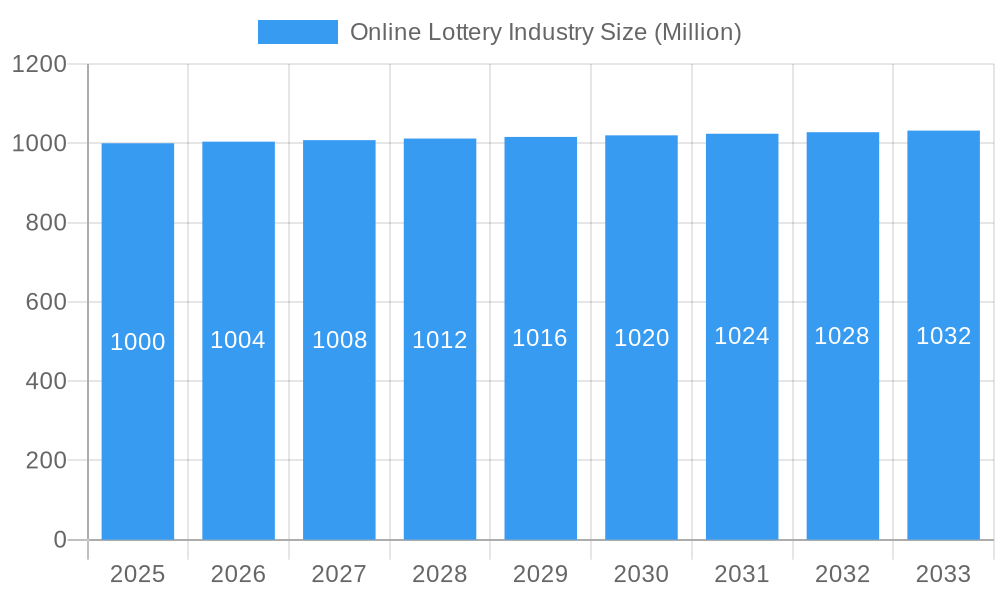

The global online lottery industry is experiencing robust expansion, driven by accelerating digital transformation, increasing internet penetration, and the pervasive adoption of mobile devices. Valued at a significant $19.43 billion in 2025, the market is projected to grow at a compelling 9.5% CAGR through the forecast period of 2025-2033. This growth is substantially fueled by the inherent convenience and accessibility that online platforms offer, allowing players to participate in diverse lottery games from anywhere at any time. The market benefits from continuous innovation in game types, including the growing popularity of instant win games and sports-themed lotteries, alongside traditional draw-based games. Furthermore, the expansion of regulated online gambling markets in various regions and the integration of secure digital payment methods like e-wallets and cryptocurrency are pivotal in enhancing player trust and expanding the user base, appealing to both individual players and lottery syndicates.

Online Lottery Industry Market Size (In Billion)

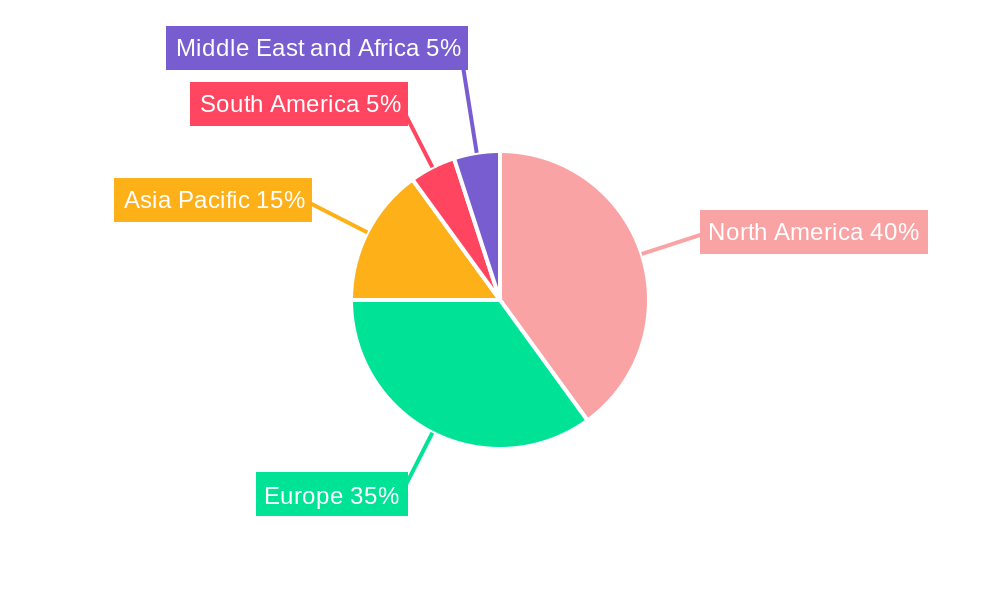

Key trends shaping the future of this dynamic market include the gamification of lottery experiences, AI-driven personalization to offer tailored game suggestions, and the increasing sophistication of mobile-first strategies. Technological advancements, such as blockchain for enhanced transparency and virtual reality (VR) for immersive gaming, are poised to redefine player engagement. However, the industry navigates a complex landscape of varying regulatory frameworks and potential concerns around responsible gaming and cybersecurity. Companies like Lotto Direct Limited, Camelot Group, and ZEAL Network SE are at the forefront, continually evolving their offerings. Geographically, North America and Europe remain dominant markets due to established regulatory environments and high disposable incomes, while the Asia Pacific region is rapidly emerging as a high-growth market, propelled by its massive digital consumer base and increasing digitalization initiatives.

Online Lottery Industry Company Market Share

This comprehensive SEO-optimized report description unveils the dynamic Global Online Lottery Industry, a rapidly expanding sector driven by digital transformation and evolving player preferences. Delving into the intricate landscape of online lottery platforms, digital lotteries, and iLottery innovations, this study provides unparalleled insights for investors, operators, technology providers, and regulators. Explore the future of online gambling technology, responsible gaming initiatives, and the strategic moves shaping this multi-billion dollar market.

Leveraging a robust market forecast from 2025 to 2033, with historical analysis spanning 2019-2024, and a base year of 2025, this report offers a meticulous examination of online lottery market trends, CAGR projections, and market share dynamics. Understand the critical factors influencing player engagement, mobile lottery adoption, and the competitive strategies of leading online lottery companies like Lotto Direct Limited, Camelot Group, Lottoland, Lotto Agent, LottoKings, WinTrillions, Lotto, ZEAL Network SE, Française des Jeux, and Annexio Limited. This essential guide is your gateway to understanding the vast global online lottery market opportunity.

Online Lottery Industry Market Concentration & Innovation

The online lottery industry, a burgeoning facet of the global gambling market, exhibits a fascinating blend of concentrated power among established entities and vibrant innovation from agile disruptors. Market concentration reveals that a few major players, including Lotto Direct Limited, Camelot Group, Lottoland, and ZEAL Network SE, command significant portions of the digital lottery landscape, with their combined revenues estimated to exceed xx billion annually. This dominance is often a result of strong brand recognition, extensive operational networks, and substantial marketing budgets. Innovation drivers are primarily centered around enhancing player experience, leveraging mobile lottery applications, and integrating advanced analytics. Companies are constantly developing new instant win games and refining existing draw-based games to capture broader demographics.

Regulatory frameworks play a pivotal role, with varying degrees of stringency and openness impacting market entry and operational scope, making compliance a key competitive advantage. Product substitutes, such as traditional brick-and-mortar lotteries and other forms of online gambling like sports betting or online casinos, consistently exert pressure, necessitating continuous innovation in offerings and engagement models. End-user trends show a clear shift towards convenience and accessibility, with a growing demand for cryptocurrency payment options and seamless mobile experiences. Merger and acquisition activities are frequent, driving market consolidation and strategic expansion. For instance, smaller innovative platforms are often acquired by larger players to expand their technological capabilities or geographical footprint, with M&A deal values frequently soaring into hundreds of millions or even billions, significantly reshaping the competitive structure and market share distribution within the online lottery market. The strategic integration of acquired technologies and customer bases allows companies to achieve greater economies of scale and reinforce their market positions, driving forward the overall iLottery market expansion.

Online Lottery Industry Industry Trends & Insights

The online lottery industry is experiencing unprecedented growth, propelled by a confluence of technological advancements, shifting consumer preferences, and evolving regulatory landscapes, positioning it as a significant component of the global digital gaming sector. A key market growth driver is the ubiquitous penetration of smartphones and internet connectivity, which has democratized access to online lottery platforms worldwide. This has led to a surge in participation, particularly in emerging economies where traditional lottery infrastructure might be limited but mobile penetration is high. The convenience of purchasing tickets, checking results, and claiming winnings through intuitive mobile lottery applications and responsive desktop platforms has fundamentally transformed consumer behavior, moving players from physical retail outlets to digital channels.

Technological disruptions, such as the integration of Artificial Intelligence for personalized gaming experiences, blockchain for enhanced transparency and security, and advanced data analytics for fraud detection and responsible gaming measures, are continuously reshaping the industry. These innovations not only improve operational efficiency but also foster greater trust and engagement among individual players and lottery syndicates. Consumer preferences are increasingly gravitating towards a diverse portfolio of gaming options beyond traditional draw-based games, with a rising demand for engaging instant win games, sports lotteries, and even quizzes games that offer immediate gratification and interactive experiences. The ability of platforms like Lottoland and ZEAL Network SE to offer a wide array of international lottery games through a single digital interface has significantly boosted player engagement and expanded the market's reach.

Competitive dynamics are intense, characterized by continuous product innovation, aggressive marketing strategies, and strategic partnerships. Companies vie for market share by offering attractive jackpots, loyalty programs, and localized content. The market is projected to grow at a robust CAGR of xx% over the forecast period (2025-2033), driven by sustained investment in technology and user acquisition. Regional variations in regulations, cultural attitudes towards gambling, and economic development further influence competitive strategies, with companies adapting their offerings to specific market nuances. This rapid expansion is also reflected in the increasing market penetration, achieving xx billion in digital sales by the base year 2025, underscoring the shift towards digital channels as the preferred mode of participation for millions of global consumers in the ever-evolving online lottery market.

Dominant Markets & Segments in Online Lottery Industry

The online lottery industry showcases distinct patterns of dominance across various geographical regions and segmentation categories, reflecting diverse regulatory environments, technological adoption rates, and player preferences. Among the various game types, Draw-Based Games continue to hold a significant market share, driven by the allure of massive jackpots from international giants like Powerball+ and Mega Millions+. However, Instant Win Games are rapidly gaining traction, particularly due to their immediate gratification and mobile-friendly design, catering to a younger demographic. Platforms like ZEAL Network SE's collaboration with Lotto Hessian for online instant games exemplifies this shift, providing a diverse portfolio that ranges from crosswords to bingo, appealing to a broader user base.

Regionally, Europe has historically been a dominant market, characterized by mature regulatory frameworks and a high degree of internet penetration. Countries like the UK, France, and Germany, home to companies such as Camelot Group, Française des Jeux, and ZEAL Network SE, lead in terms of revenue generated and player base. North America is also witnessing robust growth, propelled by increasing state-by-state legalization of online lottery and the immense popularity of national lotteries. Asia-Pacific, particularly countries like India, presents a massive untapped potential, with companies like Crypto Millions Lotto introducing India-specific games like India Fantasy 5 and India Million Lotto, indicating a strategic focus on this high-growth region.

- Key Drivers for Dominance:

- Economic Policies: Favorable taxation and licensing policies encourage investment and innovation.

- Technological Infrastructure: High internet and mobile penetration are crucial for digital platform accessibility.

- Regulatory Frameworks: Clear and stable regulations foster trust and attract both operators and players.

- Consumer Adoption: Cultural acceptance of online gambling and readiness to embrace digital payment methods.

- Marketing & Brand Building: Effective promotion and established trust for brands like Lotto Direct Limited and Lottoland.

- Product Diversification: Offering a wide range of game types (draw-based, instant win, sports lotteries, quizzes) to cater to varied preferences.

Regarding platforms, Mobile is undeniably the dominant mode of access, capturing the lion's share of player interactions. The convenience of playing on-the-go via dedicated apps or mobile-responsive websites has overshadowed desktop usage, especially among younger demographics. Payment modes are also seeing shifts, with Credit/Debit Cards remaining primary, but E-Wallets gaining substantial ground due to their speed and security. The emergence of Cryptocurrency as a payment option, as seen with Crypto Millions Lotto, represents an innovative, albeit nascent, segment with significant future potential, particularly appealing to tech-savvy users. Finally, Individual Players constitute the vast majority of the market, though Lottery Syndicates represent a significant niche, allowing groups to pool resources for higher chances of winning, appealing to collective engagement strategies within the online lottery market. The synergy of these dominant segments and drivers defines the competitive landscape and future trajectory of the global iLottery market.

Online Lottery Industry Product Developments

The online lottery industry is continually pushing boundaries with innovative product developments, enhancing player engagement and broadening market appeal. A significant trend is the expansion beyond traditional draw-based games to include dynamic instant win games and interactive quizzes games, catering to the demand for immediate gratification. Technological advancements in graphic design and user interface create immersive experiences, while the integration of AI personalizes game recommendations and promotions. For instance, the expansion of ZEAL Network SE's instant games business internationally and its partnership with Lotto Hessian to provide a diverse portfolio of online games exemplifies this push. Furthermore, the launch of new regional-specific games like India Fantasy 5 and India Million Lotto by Crypto Millions Lotto showcases a strategic focus on localized content, providing competitive advantages by tapping into specific market preferences. These developments, largely driven by mobile lottery and digital lottery platforms, ensure market fit by offering diverse, accessible, and technologically advanced gaming options.

Report Scope & Segmentation Analysis

This report meticulously segments the Online Lottery Industry to provide granular insights into its multifaceted structure. The Game Type segment comprises Draw-Based Games, estimated at over xx billion by 2033, driven by large jackpots; Instant Win Games, projected to reach xx billion by 2033, benefiting from immediate results; Sports Games, a niche but growing segment at xx billion; Quizzes Games, an emerging interactive category at xx billion; and Others, encompassing unique offerings. The competitive dynamics within these vary, with established players dominating draw-based, and new entrants innovating in instant win and quizzes.

The Platform segment differentiates between Desktop, with a market size of xx billion in 2025, offering robust gaming experiences; and Mobile, the dominant segment, projected to exceed xx billion by 2033, due to unparalleled convenience and widespread smartphone adoption. Competition on mobile is fierce, focusing on app performance and user experience. Payment Mode includes traditional Credit/Debit Cards (xx billion in 2025), widely accepted; E-Wallets (xx billion by 2033), growing rapidly for their security and speed; Bank Transfers (xx billion); and Cryptocurrency (xx billion), an emerging mode offering anonymity and lower transaction costs, influencing competitive strategies focused on secure and diverse payment gateways. Finally, the End User segment divides into Individual Players (xx billion by 2033), the largest consumer base; and Lottery Syndicates (xx billion), a smaller but significant segment focused on pooled play for higher chances. Each segment's growth projections and competitive landscapes are critically analyzed to understand market opportunities.

Key Drivers of Online Lottery Industry Growth

The Online Lottery Industry is experiencing robust growth fueled by several pivotal factors. Technologically, the ubiquitous penetration of high-speed internet and the widespread adoption of smartphones have made digital lottery platforms incredibly accessible, driving up participation. Innovations in mobile lottery applications offer seamless user experiences, personalized alerts, and secure transactions, attracting a broader demographic. Economically, increasing disposable incomes in emerging markets and the convenience of online play contribute significantly to market expansion. The allure of life-changing jackpots, often pooled across international lotteries by platforms like Lottoland and LottoKings, also acts as a potent magnet for players globally.

From a regulatory standpoint, the gradual legalization and regulated expansion of online gambling in various regions provide a stable environment for operators to thrive. Governments recognize the potential for tax revenue from iLottery operations, leading to more favorable legislative frameworks. For instance, the collaboration between ZEAL Network SE and state lotteries like Lotto Hessian exemplifies how regulated partnerships are driving growth. These factors combined create a powerful ecosystem that propels the global online lottery market forward, fostering increased player engagement and sustained revenue growth across draw-based games and instant win games.

Challenges in the Online Lottery Industry Sector

Despite its rapid growth, the Online Lottery Industry faces significant challenges that could impede its trajectory. Regulatory hurdles remain paramount, with fragmented and inconsistent legal frameworks across different jurisdictions creating operational complexities and limiting market access. The stringent licensing requirements and varying tax structures can impose substantial financial burdens on operators like Lotto Direct Limited and Annexio Limited, impacting profitability and growth strategies. Supply chain issues, particularly concerning secure digital payment processing and data management, pose risks to operational efficiency and player trust. Ensuring seamless integration of diverse payment modes, from Credit/Debit Cards to Cryptocurrency, while adhering to anti-money laundering regulations, is a constant struggle.

Competitive pressures are intense, not only from other online lottery platforms but also from other forms of online gambling such as sports betting and online casinos, vying for the same consumer spend. This necessitates continuous innovation and substantial marketing investments to maintain player engagement. Furthermore, concerns regarding responsible gaming and the potential for problem gambling present a reputational risk, requiring significant investment in player protection tools and robust compliance measures. These factors, alongside the persistent threat of cyber-attacks and data breaches, can significantly impact market confidence and growth potential within the online lottery market, potentially costing the industry billions in lost revenue or compliance penalties.

Emerging Opportunities in Online Lottery Industry

The Online Lottery Industry is ripe with emerging opportunities that promise to redefine its landscape. A key trend is the expansion into new geographical markets, particularly in underserved regions of Asia-Pacific and Latin America, where internet and mobile penetration are soaring but regulated online lottery options are scarce. This presents a billion-dollar opportunity for companies to establish early mover advantages. Technological advancements like integrating Virtual Reality (VR) and Augmented Reality (AR) into instant win games or quizzes games can create highly immersive player experiences, setting new standards for digital lottery engagement.

Furthermore, the growing acceptance and integration of Cryptocurrency as a payment mode, exemplified by Crypto Millions Lotto, opens doors to a global, tech-savvy demographic, potentially lowering transaction costs and enhancing security. The rising popularity of lottery syndicates and social gaming features offers avenues for increased community engagement and viral growth. Lastly, strategic partnerships between online lottery platforms and media companies or sports leagues can unlock new advertising channels and co-branded offerings, tapping into vast existing fan bases. These opportunities for technological innovation and market expansion are poised to drive the online lottery market to unprecedented heights, generating billions in new revenue streams.

Leading Players in the Online Lottery Industry Market

- Lotto Direct Limited

- Camelot Group

- Lottoland

- Lotto Agent

- LottoKings

- WinTrillions

- Lotto

- ZEAL Network SE

- Française des Jeux

- Annexio Limited

- Others

Key Developments in Online Lottery Industry Industry

- October 2022: ZEAL Network SE expanded its games business internationally. The German market leader for online lotteries collaborated with American online lottery provider Park Avenue Gaming to integrate the online instant games of Zeal into its video lottery terminal business in Argentina and its online platforms in Peru. This strategic move significantly broadened Zeal's global footprint, impacting regional market competition and expanding access to its innovative instant win games.

- February 2022: ZEAL Network SE launched a partnership with Lotto Hessian for instant win games. In this collaboration, Zeal provided Hessian with 15 online games of the state lottery, such as crosswords, bingo, or the world cup. This partnership bolstered the presence of digital lottery options within the German market, enhancing player choice and reinforcing Zeal's position as a key technology provider in the iLottery space.

- December 2021: Crypto Millions Lotto announced the launch of four new lottery games on its official website. Two of the above four games are India-based, namely, India Fantasy 5 and India Million Lotto, while the others are US-based, viz, Powerball+ and Mega Millions+. This development showcased a strategic focus on localized content and global market expansion, particularly capitalizing on the emerging markets of India and the established demand in the US for massive jackpots, impacting player acquisition and revenue diversification for online lottery platforms.

Strategic Outlook for Online Lottery Industry Market

The strategic outlook for the Online Lottery Industry is exceptionally positive, driven by persistent digital transformation and expanding regulatory acceptance. Future market potential is underscored by a projected CAGR of xx% through 2033, indicating a robust growth trajectory that will see the global online lottery market exceed hundreds of billions in value. Growth catalysts include continued innovation in mobile lottery applications and the diversification of game types, from immersive instant win games to interactive quizzes games, enhancing player engagement. The rising adoption of cryptocurrency as a payment option and the exploration of new technologies like blockchain for transparency will further fortify market trust and expand the player base.

Geographical expansion into emerging markets, particularly in Asia and Latin America, represents significant opportunities for revenue growth, as seen with localized product launches. Strategic partnerships between technology providers and traditional lottery operators will continue to drive market consolidation and operational efficiency. Furthermore, an increasing focus on responsible gaming initiatives will not only meet regulatory requirements but also build greater consumer confidence, attracting a wider audience to digital lottery platforms. The industry's capacity to adapt to evolving consumer preferences and technological shifts positions it for sustained exponential growth, cementing its role as a key player in the global online gambling ecosystem.

Online Lottery Industry Segmentation

-

1. Game Type

- 1.1. Draw-Based Games

- 1.2. Instant Win Games

- 1.3. Sports Games

- 1.4. Quizzes Games

- 1.5. Others

-

2. Platform

- 2.1. Desktop

- 2.2. Mobile

-

3. Payment Mode

- 3.1. Credit/Debit Cards

- 3.2. E-Wallets

- 3.3. Bank Transfers

- 3.4. Cryptocurrency

- 3.5. Others

-

4. End User

- 4.1. Individual Players

- 4.2. Lottery Syndicates

Online Lottery Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

- 1.4. Rest of North America

-

2. Europe

- 2.1. Spain

- 2.2. United Kingdom

- 2.3. Germany

- 2.4. France

- 2.5. Italy

- 2.6. Sweden

- 2.7. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. Australia

- 3.5. Rest of Asia Pacific

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. South Africa

- 5.2. United Arab Emirates

- 5.3. Rest of Middle East and Africa

Online Lottery Industry Regional Market Share

Geographic Coverage of Online Lottery Industry

Online Lottery Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Game Type

- 5.1.1. Draw-Based Games

- 5.1.2. Instant Win Games

- 5.1.3. Sports Games

- 5.1.4. Quizzes Games

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Platform

- 5.2.1. Desktop

- 5.2.2. Mobile

- 5.3. Market Analysis, Insights and Forecast - by Payment Mode

- 5.3.1. Credit/Debit Cards

- 5.3.2. E-Wallets

- 5.3.3. Bank Transfers

- 5.3.4. Cryptocurrency

- 5.3.5. Others

- 5.4. Market Analysis, Insights and Forecast - by End User

- 5.4.1. Individual Players

- 5.4.2. Lottery Syndicates

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. Europe

- 5.5.3. Asia Pacific

- 5.5.4. South America

- 5.5.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Game Type

- 6. Global Online Lottery Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Game Type

- 6.1.1. Draw-Based Games

- 6.1.2. Instant Win Games

- 6.1.3. Sports Games

- 6.1.4. Quizzes Games

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Platform

- 6.2.1. Desktop

- 6.2.2. Mobile

- 6.3. Market Analysis, Insights and Forecast - by Payment Mode

- 6.3.1. Credit/Debit Cards

- 6.3.2. E-Wallets

- 6.3.3. Bank Transfers

- 6.3.4. Cryptocurrency

- 6.3.5. Others

- 6.4. Market Analysis, Insights and Forecast - by End User

- 6.4.1. Individual Players

- 6.4.2. Lottery Syndicates

- 6.1. Market Analysis, Insights and Forecast - by Game Type

- 7. North America Online Lottery Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Game Type

- 7.1.1. Draw-Based Games

- 7.1.2. Instant Win Games

- 7.1.3. Sports Games

- 7.1.4. Quizzes Games

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Platform

- 7.2.1. Desktop

- 7.2.2. Mobile

- 7.3. Market Analysis, Insights and Forecast - by Payment Mode

- 7.3.1. Credit/Debit Cards

- 7.3.2. E-Wallets

- 7.3.3. Bank Transfers

- 7.3.4. Cryptocurrency

- 7.3.5. Others

- 7.4. Market Analysis, Insights and Forecast - by End User

- 7.4.1. Individual Players

- 7.4.2. Lottery Syndicates

- 7.1. Market Analysis, Insights and Forecast - by Game Type

- 8. Europe Online Lottery Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Game Type

- 8.1.1. Draw-Based Games

- 8.1.2. Instant Win Games

- 8.1.3. Sports Games

- 8.1.4. Quizzes Games

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Platform

- 8.2.1. Desktop

- 8.2.2. Mobile

- 8.3. Market Analysis, Insights and Forecast - by Payment Mode

- 8.3.1. Credit/Debit Cards

- 8.3.2. E-Wallets

- 8.3.3. Bank Transfers

- 8.3.4. Cryptocurrency

- 8.3.5. Others

- 8.4. Market Analysis, Insights and Forecast - by End User

- 8.4.1. Individual Players

- 8.4.2. Lottery Syndicates

- 8.1. Market Analysis, Insights and Forecast - by Game Type

- 9. Asia Pacific Online Lottery Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Game Type

- 9.1.1. Draw-Based Games

- 9.1.2. Instant Win Games

- 9.1.3. Sports Games

- 9.1.4. Quizzes Games

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Platform

- 9.2.1. Desktop

- 9.2.2. Mobile

- 9.3. Market Analysis, Insights and Forecast - by Payment Mode

- 9.3.1. Credit/Debit Cards

- 9.3.2. E-Wallets

- 9.3.3. Bank Transfers

- 9.3.4. Cryptocurrency

- 9.3.5. Others

- 9.4. Market Analysis, Insights and Forecast - by End User

- 9.4.1. Individual Players

- 9.4.2. Lottery Syndicates

- 9.1. Market Analysis, Insights and Forecast - by Game Type

- 10. South America Online Lottery Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Game Type

- 10.1.1. Draw-Based Games

- 10.1.2. Instant Win Games

- 10.1.3. Sports Games

- 10.1.4. Quizzes Games

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Platform

- 10.2.1. Desktop

- 10.2.2. Mobile

- 10.3. Market Analysis, Insights and Forecast - by Payment Mode

- 10.3.1. Credit/Debit Cards

- 10.3.2. E-Wallets

- 10.3.3. Bank Transfers

- 10.3.4. Cryptocurrency

- 10.3.5. Others

- 10.4. Market Analysis, Insights and Forecast - by End User

- 10.4.1. Individual Players

- 10.4.2. Lottery Syndicates

- 10.1. Market Analysis, Insights and Forecast - by Game Type

- 11. Middle East and Africa Online Lottery Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Game Type

- 11.1.1. Draw-Based Games

- 11.1.2. Instant Win Games

- 11.1.3. Sports Games

- 11.1.4. Quizzes Games

- 11.1.5. Others

- 11.2. Market Analysis, Insights and Forecast - by Platform

- 11.2.1. Desktop

- 11.2.2. Mobile

- 11.3. Market Analysis, Insights and Forecast - by Payment Mode

- 11.3.1. Credit/Debit Cards

- 11.3.2. E-Wallets

- 11.3.3. Bank Transfers

- 11.3.4. Cryptocurrency

- 11.3.5. Others

- 11.4. Market Analysis, Insights and Forecast - by End User

- 11.4.1. Individual Players

- 11.4.2. Lottery Syndicates

- 11.1. Market Analysis, Insights and Forecast - by Game Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Lotto Direct Limited

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Camelot Group

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Lottoland

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Lotto Agent

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 LottoKings

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 WinTrillions

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Lotto

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 ZEAL Network SE

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Française des Jeux

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Annexio Limited

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Others

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Lotto Direct Limited

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Online Lottery Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Online Lottery Industry Revenue (billion), by Game Type 2025 & 2033

- Figure 3: North America Online Lottery Industry Revenue Share (%), by Game Type 2025 & 2033

- Figure 4: North America Online Lottery Industry Revenue (billion), by Platform 2025 & 2033

- Figure 5: North America Online Lottery Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 6: North America Online Lottery Industry Revenue (billion), by Payment Mode 2025 & 2033

- Figure 7: North America Online Lottery Industry Revenue Share (%), by Payment Mode 2025 & 2033

- Figure 8: North America Online Lottery Industry Revenue (billion), by End User 2025 & 2033

- Figure 9: North America Online Lottery Industry Revenue Share (%), by End User 2025 & 2033

- Figure 10: North America Online Lottery Industry Revenue (billion), by Country 2025 & 2033

- Figure 11: North America Online Lottery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 12: Europe Online Lottery Industry Revenue (billion), by Game Type 2025 & 2033

- Figure 13: Europe Online Lottery Industry Revenue Share (%), by Game Type 2025 & 2033

- Figure 14: Europe Online Lottery Industry Revenue (billion), by Platform 2025 & 2033

- Figure 15: Europe Online Lottery Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 16: Europe Online Lottery Industry Revenue (billion), by Payment Mode 2025 & 2033

- Figure 17: Europe Online Lottery Industry Revenue Share (%), by Payment Mode 2025 & 2033

- Figure 18: Europe Online Lottery Industry Revenue (billion), by End User 2025 & 2033

- Figure 19: Europe Online Lottery Industry Revenue Share (%), by End User 2025 & 2033

- Figure 20: Europe Online Lottery Industry Revenue (billion), by Country 2025 & 2033

- Figure 21: Europe Online Lottery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Asia Pacific Online Lottery Industry Revenue (billion), by Game Type 2025 & 2033

- Figure 23: Asia Pacific Online Lottery Industry Revenue Share (%), by Game Type 2025 & 2033

- Figure 24: Asia Pacific Online Lottery Industry Revenue (billion), by Platform 2025 & 2033

- Figure 25: Asia Pacific Online Lottery Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 26: Asia Pacific Online Lottery Industry Revenue (billion), by Payment Mode 2025 & 2033

- Figure 27: Asia Pacific Online Lottery Industry Revenue Share (%), by Payment Mode 2025 & 2033

- Figure 28: Asia Pacific Online Lottery Industry Revenue (billion), by End User 2025 & 2033

- Figure 29: Asia Pacific Online Lottery Industry Revenue Share (%), by End User 2025 & 2033

- Figure 30: Asia Pacific Online Lottery Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Online Lottery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: South America Online Lottery Industry Revenue (billion), by Game Type 2025 & 2033

- Figure 33: South America Online Lottery Industry Revenue Share (%), by Game Type 2025 & 2033

- Figure 34: South America Online Lottery Industry Revenue (billion), by Platform 2025 & 2033

- Figure 35: South America Online Lottery Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 36: South America Online Lottery Industry Revenue (billion), by Payment Mode 2025 & 2033

- Figure 37: South America Online Lottery Industry Revenue Share (%), by Payment Mode 2025 & 2033

- Figure 38: South America Online Lottery Industry Revenue (billion), by End User 2025 & 2033

- Figure 39: South America Online Lottery Industry Revenue Share (%), by End User 2025 & 2033

- Figure 40: South America Online Lottery Industry Revenue (billion), by Country 2025 & 2033

- Figure 41: South America Online Lottery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Middle East and Africa Online Lottery Industry Revenue (billion), by Game Type 2025 & 2033

- Figure 43: Middle East and Africa Online Lottery Industry Revenue Share (%), by Game Type 2025 & 2033

- Figure 44: Middle East and Africa Online Lottery Industry Revenue (billion), by Platform 2025 & 2033

- Figure 45: Middle East and Africa Online Lottery Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 46: Middle East and Africa Online Lottery Industry Revenue (billion), by Payment Mode 2025 & 2033

- Figure 47: Middle East and Africa Online Lottery Industry Revenue Share (%), by Payment Mode 2025 & 2033

- Figure 48: Middle East and Africa Online Lottery Industry Revenue (billion), by End User 2025 & 2033

- Figure 49: Middle East and Africa Online Lottery Industry Revenue Share (%), by End User 2025 & 2033

- Figure 50: Middle East and Africa Online Lottery Industry Revenue (billion), by Country 2025 & 2033

- Figure 51: Middle East and Africa Online Lottery Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Online Lottery Industry Revenue billion Forecast, by Game Type 2020 & 2033

- Table 2: Global Online Lottery Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 3: Global Online Lottery Industry Revenue billion Forecast, by Payment Mode 2020 & 2033

- Table 4: Global Online Lottery Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 5: Global Online Lottery Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Online Lottery Industry Revenue billion Forecast, by Game Type 2020 & 2033

- Table 7: Global Online Lottery Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 8: Global Online Lottery Industry Revenue billion Forecast, by Payment Mode 2020 & 2033

- Table 9: Global Online Lottery Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 10: Global Online Lottery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 11: United States Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Canada Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Mexico Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Rest of North America Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Global Online Lottery Industry Revenue billion Forecast, by Game Type 2020 & 2033

- Table 16: Global Online Lottery Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 17: Global Online Lottery Industry Revenue billion Forecast, by Payment Mode 2020 & 2033

- Table 18: Global Online Lottery Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 19: Global Online Lottery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 20: Spain Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: United Kingdom Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Germany Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: France Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Italy Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Sweden Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Rest of Europe Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Global Online Lottery Industry Revenue billion Forecast, by Game Type 2020 & 2033

- Table 28: Global Online Lottery Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 29: Global Online Lottery Industry Revenue billion Forecast, by Payment Mode 2020 & 2033

- Table 30: Global Online Lottery Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 31: Global Online Lottery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 32: China Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: India Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Japan Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: Australia Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Asia Pacific Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Online Lottery Industry Revenue billion Forecast, by Game Type 2020 & 2033

- Table 38: Global Online Lottery Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 39: Global Online Lottery Industry Revenue billion Forecast, by Payment Mode 2020 & 2033

- Table 40: Global Online Lottery Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 41: Global Online Lottery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 42: Brazil Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: Argentina Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Rest of South America Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Global Online Lottery Industry Revenue billion Forecast, by Game Type 2020 & 2033

- Table 46: Global Online Lottery Industry Revenue billion Forecast, by Platform 2020 & 2033

- Table 47: Global Online Lottery Industry Revenue billion Forecast, by Payment Mode 2020 & 2033

- Table 48: Global Online Lottery Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 49: Global Online Lottery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 50: South Africa Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 51: United Arab Emirates Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Rest of Middle East and Africa Online Lottery Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Online Lottery Industry?

The projected CAGR is approximately 9.5%.

2. Which companies are prominent players in the Online Lottery Industry?

Key companies in the market include Lotto Direct Limited, Camelot Group, Lottoland, Lotto Agent, LottoKings, WinTrillions, Lotto, ZEAL Network SE, Française des Jeux, Annexio Limited, Others.

3. What are the main segments of the Online Lottery Industry?

The market segments include Game Type, Platform, Payment Mode, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 19.43 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Appeal for Multi-functional and Damage Control Hair Care Products; Prevalence of Different Hair Concerns Remains the Major Driving Force.

6. What are the notable trends driving market growth?

Improved Internet Connections. Advances in Security. and Increased Number of Internet Users.

7. Are there any restraints impacting market growth?

Growing Availability of Counterfeit Products.

8. Can you provide examples of recent developments in the market?

October 2022: Zeal Network SE expanded its games business internationally. The German market leader for online lotteries collaborated with American online lottery provider Park Avenue Gaming to integrate the online instant games of Zeal into its video lottery terminal business in Argentina and its online platforms in Peru.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Online Lottery Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Online Lottery Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Online Lottery Industry?

To stay informed about further developments, trends, and reports in the Online Lottery Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence