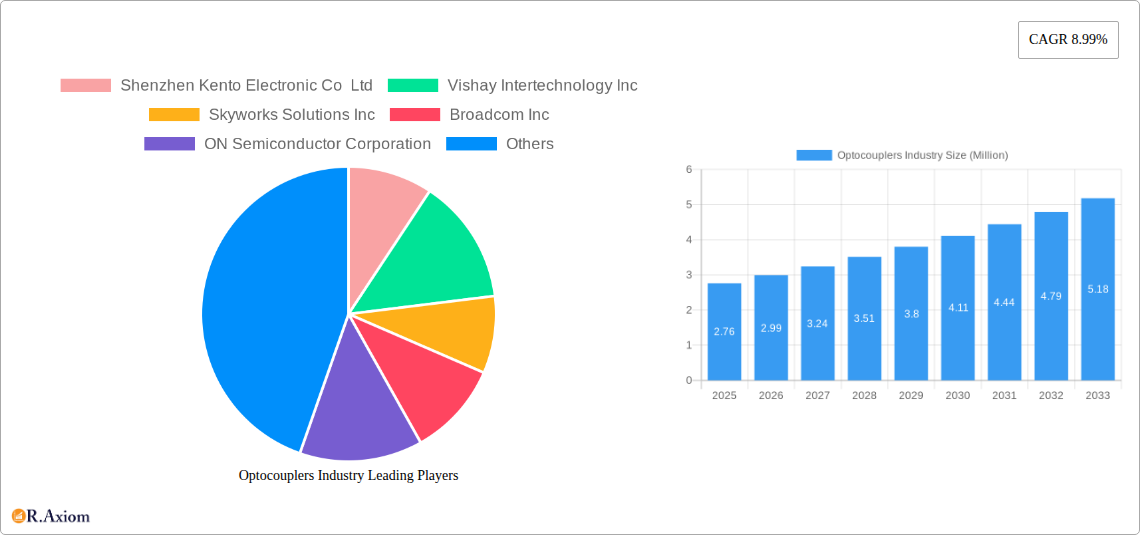

Key Insights

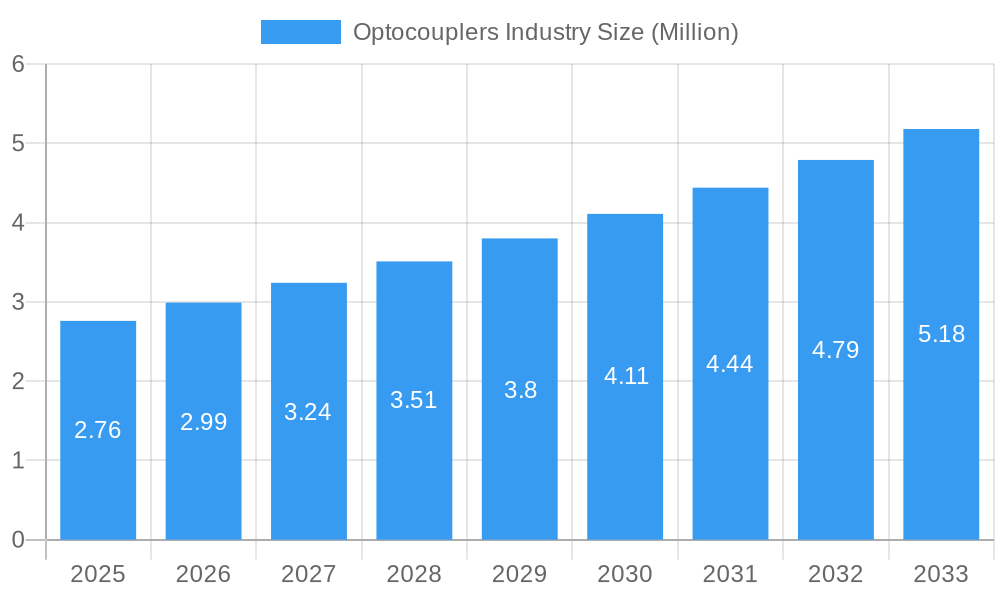

The global optocoupler market is poised for substantial growth, projected to reach $2.76 billion by 2025, with a robust Compound Annual Growth Rate (CAGR) of 8.99% during the forecast period of 2025-2033. This expansion is driven by the increasing demand for advanced isolation and signal transmission solutions across a multitude of industries. Key growth enablers include the burgeoning automotive sector, with its growing adoption of electric vehicles (EVs) and advanced driver-assistance systems (ADAS) that rely heavily on optocouplers for critical power management and control functions. The consumer electronics industry also presents a significant opportunity, fueled by the proliferation of smart home devices, wearables, and high-definition entertainment systems, all requiring reliable electrical isolation. Furthermore, the expansion of communication infrastructure, including 5G deployment and data centers, necessitates robust optocoupler solutions for signal integrity and protection.

Optocouplers Industry Market Size (In Million)

Despite the strong growth trajectory, the market faces certain restraints. The increasing integration of microcontrollers and advanced semiconductor technologies that offer on-chip isolation capabilities could potentially dampen demand for discrete optocoupler components in specific applications. However, the inherent reliability, cost-effectiveness, and established performance of optocouplers in demanding industrial environments, coupled with ongoing innovation in product development like higher voltage ratings, faster switching speeds, and improved thermal management, are expected to mitigate these challenges. The market is segmented by product type, with phototransistor-based optocouplers likely dominating due to their versatility, alongside growing demand for optocouplers based on Photo TRIAC and Photo SCR for power control applications. Geographically, Asia Pacific is anticipated to lead the market, driven by its strong manufacturing base in electronics and increasing investments in industrial automation and smart infrastructure.

Optocouplers Industry Company Market Share

Optocouplers Industry Market Analysis: Growth, Trends, and Future Outlook (2019-2033)

This comprehensive report delves into the global Optocouplers market, providing an in-depth analysis of its current landscape, historical performance, and future trajectory. Spanning the study period from 2019 to 2033, with a base and estimated year of 2025, this report offers critical insights for stakeholders seeking to understand market concentration, innovation drivers, key trends, dominant segments, and emerging opportunities within the optocoupler ecosystem. Leveraging high-traffic keywords such as "optocoupler market," "phototransistor optocoupler," "automotive optocoupler," "industrial optocoupler," and "high-speed optocoupler," this analysis aims to maximize search visibility and engagement within the industry. The report covers major players including Shenzhen Kento Electronic Co Ltd, Vishay Intertechnology Inc, Skyworks Solutions Inc, Broadcom Inc, ON Semiconductor Corporation, Senba Sensing Technology Co Ltd, Renesas Electronics Corporation, Standex Electronics Inc, Sharp Devices Europe, LITE-ON Technology Inc, Isocom Components Ltd, Everlight Electronics Co Ltd, Panasonic Corporation, and Toshiba Electronic Devices & Storage Corporation.

Optocouplers Industry Market Concentration & Innovation

The global optocouplers market exhibits a moderate to high level of concentration, with a few key players dominating market share. In the base year of 2025, the market is estimated to be valued at over 2,500 Million. Innovation remains a critical driver, fueled by the increasing demand for enhanced electrical isolation, signal integrity, and power efficiency across diverse end-user industries. The development of high-speed optocouplers, such as Vishay's VOIH72A capable of 25 MBd data transmission, exemplifies this trend. Regulatory frameworks, while not overly restrictive, emphasize safety and reliability standards, particularly in automotive and industrial applications. Product substitutes, though present in the form of digital isolators, are gradually being surpassed by the performance and cost-effectiveness of advanced optocouplers, especially those incorporating novel isolation technologies like Texas Instruments' silicon dioxide (SiO2)-based isolation in their new opto-emulators. Mergers and acquisitions (M&A) activities, with an estimated total deal value of approximately 800 Million over the historical period (2019-2024), have played a role in consolidating market share and expanding technological capabilities.

Optocouplers Industry Industry Trends & Insights

The optocouplers industry is experiencing robust growth, projected to achieve a Compound Annual Growth Rate (CAGR) of approximately 6.5% during the forecast period of 2025-2033. This expansion is primarily driven by the relentless proliferation of electronic devices across sectors like consumer electronics, communication infrastructure, and the automotive industry, all of which necessitate reliable electrical isolation. The escalating adoption of advanced driver-assistance systems (ADAS) and electric vehicles (EVs) within the automotive sector is a significant catalyst, demanding higher performance and reliability from optocoupler components. In the industrial segment, the trend towards automation, smart factories, and the Industrial Internet of Things (IIoT) further amplifies the need for robust signal isolation to protect sensitive control systems and ensure operational continuity. Consumer electronics, from smart home devices to wearable technology, are also contributing to market penetration, albeit with a focus on miniaturization and lower power consumption. The competitive landscape is characterized by continuous innovation in product design, aiming for higher data rates, lower power consumption, improved temperature resistance, and enhanced immunity to electromagnetic interference (EMI). Technological disruptions, such as the aforementioned development of opto-emulators by Texas Instruments, are poised to reshape the market by offering alternatives to traditional LED-based optocouplers, addressing concerns related to LED aging. Consumer preferences are increasingly tilting towards integrated solutions and components that simplify design and reduce system complexity.

Dominant Markets & Segments in Optocouplers Industry

The Industrial end-user industry stands as the most dominant segment within the global optocouplers market, accounting for an estimated 35% of the market share in 2025. This dominance is underpinned by several key drivers:

- Automation and IIoT Expansion: The widespread implementation of automation technologies, smart manufacturing processes, and the Industrial Internet of Things (IIoT) in factories and industrial facilities necessitates robust electrical isolation for control systems, power supplies, and communication interfaces. This creates a constant demand for high-reliability optocouplers.

- Power Grid Modernization: Investments in upgrading and modernizing power grids, including renewable energy integration, require sophisticated isolation components for grid monitoring, protection, and control systems.

- Heavy Machinery and Equipment: The continuous operation and demanding environments of heavy machinery, construction equipment, and agricultural machinery necessitate durable and reliable optocouplers to ensure safe and efficient operation.

- Harsh Environment Applications: Industrial settings often involve extreme temperatures, vibration, and electromagnetic interference, environments where the inherent robustness of optocouplers is a significant advantage.

Within product types, Phototransistor-based Optocouplers are expected to maintain their leading position, representing an estimated 45% of the market share in 2025. Their widespread availability, cost-effectiveness, and suitability for a broad range of applications contribute to their sustained dominance.

- Versatile Applications: Phototransistor-based optocouplers are employed in numerous applications, including power supply control, motor drives, AC line monitoring, and general signal isolation.

- Established Technology: This technology is mature and well-understood, making it a reliable choice for designers across various industries.

- Cost-Effectiveness: Their relatively lower cost compared to some other optocoupler types makes them a preferred choice for high-volume applications.

The Automotive end-user industry is another significant and rapidly growing segment, projected to capture a substantial market share of around 20% in 2025. The increasing sophistication of vehicle electronics, driven by the transition to electric vehicles (EVs) and the proliferation of advanced driver-assistance systems (ADAS), is fueling this demand.

- EV Powertrain Control: The electrification of vehicles requires robust isolation in battery management systems, onboard chargers, and motor control units to ensure safety and efficiency.

- ADAS and Infotainment: The integration of advanced safety features and complex infotainment systems necessitates reliable signal isolation for communication between various ECUs (Electronic Control Units).

- High-Voltage Applications: The growing prevalence of high-voltage systems in EVs demands optocouplers capable of withstanding higher voltages and providing superior isolation.

Optocouplers Industry Product Developments

The optocouplers industry is characterized by continuous product innovation focused on enhancing performance and expanding application possibilities. Recent developments highlight a trend towards higher speed and greater integration. Vishay Intertechnology's VOIH72A, a new high-speed optocoupler, exemplifies this with its 25 MBd data transmission capability and CMOS logic interface, simplifying integration into digital systems for industrial use. Furthermore, Texas Instruments' introduction of opto-emulators like the ISOM8710 and ISOM8110 addresses long-standing concerns about LED aging in traditional optocouplers, offering improved signal integrity, lower power consumption, and extended lifespan for high-voltage applications in industrial and automotive sectors. These advancements underscore the industry's commitment to providing more efficient, reliable, and integrated isolation solutions.

Report Scope & Segmentation Analysis

This report meticulously segments the optocouplers market across key product types and end-user industries. The Product Type segmentation includes Phototransistor-based Optocoupler, Optocoup, Optocoupler based on Photo TRIAC, Optocoupler with Photo SCR, and Other Types. The End-user Industry segmentation encompasses Automotive, Consumer Electronics, Communication, Industrial, and Other End-user Industries.

- Phototransistor-based Optocoupler: Projected to hold a significant market share, driven by its versatility and cost-effectiveness in a wide array of applications.

- Optocoupler based on Photo TRIAC & Photo SCR: These segments are expected to witness steady growth, primarily in power control and switching applications within industrial and consumer electronics.

- Automotive: Anticipated to be a high-growth segment, fueled by the EV revolution and the increasing adoption of ADAS.

- Industrial: Expected to remain the largest segment, driven by automation, IIoT, and the need for robust electrical isolation in demanding environments.

- Communication & Consumer Electronics: These segments will exhibit consistent growth, driven by the expansion of 5G networks, smart home devices, and connected technologies.

Key Drivers of Optocouplers Industry Growth

The optocouplers industry's growth is propelled by several interconnected factors. Technologically, the relentless pursuit of higher data transfer rates, enhanced isolation voltages, and lower power consumption in electronic devices is a primary driver. The burgeoning adoption of electric vehicles (EVs) and advanced driver-assistance systems (ADAS) in the automotive sector is creating substantial demand for optocouplers capable of handling higher voltages and offering superior safety features. The widespread implementation of industrial automation, smart factories, and the Industrial Internet of Things (IIoT) necessitates robust electrical isolation solutions to protect critical infrastructure and ensure operational efficiency. Furthermore, regulatory mandates and industry standards emphasizing electrical safety and reliability in critical applications, such as medical devices and power grids, contribute significantly to the sustained demand for optocouplers.

Challenges in the Optocouplers Industry Sector

Despite its growth trajectory, the optocouplers industry faces several challenges. The increasing competition from digital isolators, which offer advantages in terms of speed and integration in certain applications, poses a competitive threat. Supply chain disruptions, as witnessed in recent years, can impact the availability of raw materials and increase manufacturing costs. The rapid pace of technological advancement necessitates continuous investment in research and development to stay competitive, which can be a significant financial burden for smaller players. Furthermore, the commoditization of certain standard optocoupler types can lead to price pressures and reduced profit margins. Fluctuations in the cost of key components, such as LEDs and photodiodes, can also affect the overall profitability of optocoupler manufacturers.

Emerging Opportunities in Optocouplers Industry

The optocouplers industry is ripe with emerging opportunities. The continued expansion of 5G infrastructure globally will drive demand for high-speed and reliable optocouplers in communication equipment. The renewable energy sector, particularly solar and wind power, presents a significant growth avenue, requiring robust isolation solutions for inverters, grid-tie systems, and energy storage solutions. The burgeoning market for medical devices, from diagnostic equipment to wearable health monitors, demands highly reliable and safe isolation components. Furthermore, the increasing integration of artificial intelligence (AI) and machine learning (ML) in various industries will create new applications for optocouplers in edge computing devices and sensor networks requiring precise signal conditioning and isolation. The development of novel materials and manufacturing processes also presents opportunities for creating more compact, efficient, and cost-effective optocoupler solutions.

Leading Players in the Optocouplers Industry Market

- Shenzhen Kento Electronic Co Ltd

- Vishay Intertechnology Inc

- Skyworks Solutions Inc

- Broadcom Inc

- ON Semiconductor Corporation

- Senba Sensing Technology Co Ltd

- Renesas Electronics Corporation

- Standex Electronics Inc

- Sharp Devices Europe

- LITE-ON Technology Inc

- Isocom Components Ltd

- Everlight Electronics Co Ltd

- Panasonic Corporation

- Toshiba Electronic Devices & Storage Corporation

Key Developments in Optocouplers Industry Industry

- May 2024: Vishay Intertechnology, Inc. introduced the VOIH72A, a high-speed optocoupler capable of transmitting data at 25 MBd, featuring a CMOS logic interface for easier integration into digital systems. Designed for industrial applications, it offers minimal pulse width distortion and low supply current, operating efficiently across a wide voltage and temperature range.

- September 2024: Texas Instruments (TI) launched a new series of signal isolation semiconductors, opto-emulators (ISOM8710 and ISOM8110). These devices are engineered to enhance signal integrity, reduce power consumption, and extend the lifespan of high-voltage industrial and automotive applications, leveraging TI's unique silicon dioxide (SiO2)-based isolation technology to overcome LED aging issues common in traditional optocouplers.

Strategic Outlook for Optocouplers Industry Market

The strategic outlook for the optocouplers industry remains highly positive, driven by the pervasive digitalization across all sectors. The ongoing transition towards electrification in the automotive industry, coupled with the rapid expansion of renewable energy sources, will continue to be significant growth catalysts. The increasing complexity of industrial automation and the proliferation of IIoT devices will further solidify the demand for reliable isolation solutions. Emerging markets in Asia-Pacific, driven by robust manufacturing capabilities and increasing technological adoption, are expected to offer substantial growth opportunities. Companies focusing on high-performance, low-power consumption, and miniaturized optocoupler solutions will be well-positioned to capitalize on future market potential and technological advancements, ensuring sustained relevance in an evolving electronics landscape.

Optocouplers Industry Segmentation

-

1. Product Type

- 1.1. Phototransistor-based Optocoupler

- 1.2. Optocoup

- 1.3. Optocoupler based on Photo TRIAC

- 1.4. Optocoupler with Photo SCR

- 1.5. Other Types

-

2. End-user Industry

- 2.1. Automotive

- 2.2. Consumer Electronics

- 2.3. Communication

- 2.4. Industrial

- 2.5. Other End-user Industries

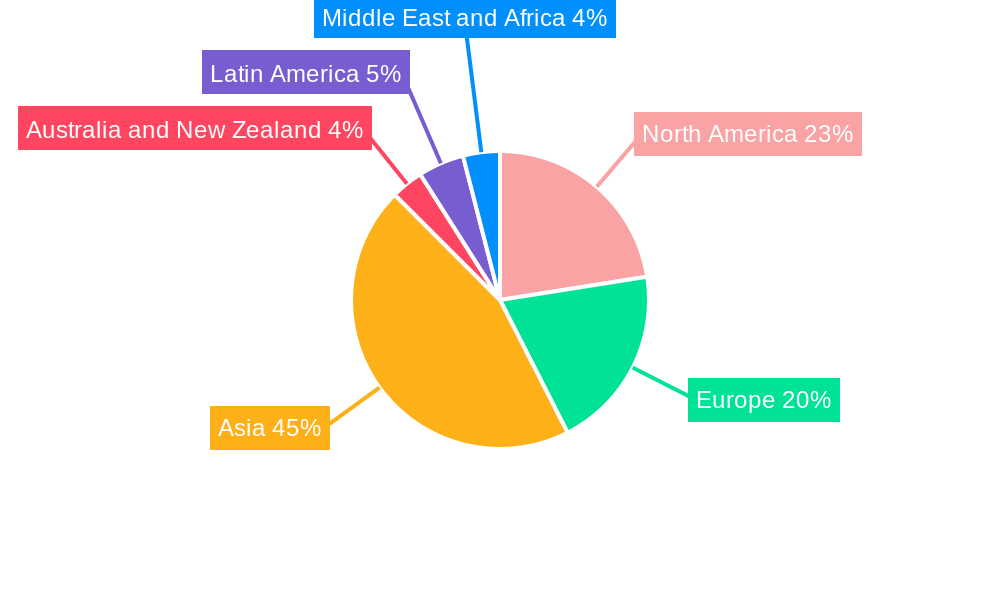

Optocouplers Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Australia and New Zealand

- 5. Latin America

- 6. Middle East and Africa

Optocouplers Industry Regional Market Share

Geographic Coverage of Optocouplers Industry

Optocouplers Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.99% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Phototransistor-based Optocoupler

- 5.1.2. Optocoup

- 5.1.3. Optocoupler based on Photo TRIAC

- 5.1.4. Optocoupler with Photo SCR

- 5.1.5. Other Types

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Automotive

- 5.2.2. Consumer Electronics

- 5.2.3. Communication

- 5.2.4. Industrial

- 5.2.5. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia

- 5.3.4. Australia and New Zealand

- 5.3.5. Latin America

- 5.3.6. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global Optocouplers Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Phototransistor-based Optocoupler

- 6.1.2. Optocoup

- 6.1.3. Optocoupler based on Photo TRIAC

- 6.1.4. Optocoupler with Photo SCR

- 6.1.5. Other Types

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Automotive

- 6.2.2. Consumer Electronics

- 6.2.3. Communication

- 6.2.4. Industrial

- 6.2.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. North America Optocouplers Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Phototransistor-based Optocoupler

- 7.1.2. Optocoup

- 7.1.3. Optocoupler based on Photo TRIAC

- 7.1.4. Optocoupler with Photo SCR

- 7.1.5. Other Types

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Automotive

- 7.2.2. Consumer Electronics

- 7.2.3. Communication

- 7.2.4. Industrial

- 7.2.5. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Europe Optocouplers Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Phototransistor-based Optocoupler

- 8.1.2. Optocoup

- 8.1.3. Optocoupler based on Photo TRIAC

- 8.1.4. Optocoupler with Photo SCR

- 8.1.5. Other Types

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Automotive

- 8.2.2. Consumer Electronics

- 8.2.3. Communication

- 8.2.4. Industrial

- 8.2.5. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Asia Optocouplers Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Phototransistor-based Optocoupler

- 9.1.2. Optocoup

- 9.1.3. Optocoupler based on Photo TRIAC

- 9.1.4. Optocoupler with Photo SCR

- 9.1.5. Other Types

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Automotive

- 9.2.2. Consumer Electronics

- 9.2.3. Communication

- 9.2.4. Industrial

- 9.2.5. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. Australia and New Zealand Optocouplers Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Phototransistor-based Optocoupler

- 10.1.2. Optocoup

- 10.1.3. Optocoupler based on Photo TRIAC

- 10.1.4. Optocoupler with Photo SCR

- 10.1.5. Other Types

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. Automotive

- 10.2.2. Consumer Electronics

- 10.2.3. Communication

- 10.2.4. Industrial

- 10.2.5. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Latin America Optocouplers Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Phototransistor-based Optocoupler

- 11.1.2. Optocoup

- 11.1.3. Optocoupler based on Photo TRIAC

- 11.1.4. Optocoupler with Photo SCR

- 11.1.5. Other Types

- 11.2. Market Analysis, Insights and Forecast - by End-user Industry

- 11.2.1. Automotive

- 11.2.2. Consumer Electronics

- 11.2.3. Communication

- 11.2.4. Industrial

- 11.2.5. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Middle East and Africa Optocouplers Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Product Type

- 12.1.1. Phototransistor-based Optocoupler

- 12.1.2. Optocoup

- 12.1.3. Optocoupler based on Photo TRIAC

- 12.1.4. Optocoupler with Photo SCR

- 12.1.5. Other Types

- 12.2. Market Analysis, Insights and Forecast - by End-user Industry

- 12.2.1. Automotive

- 12.2.2. Consumer Electronics

- 12.2.3. Communication

- 12.2.4. Industrial

- 12.2.5. Other End-user Industries

- 12.1. Market Analysis, Insights and Forecast - by Product Type

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Shenzhen Kento Electronic Co Ltd

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Vishay Intertechnology Inc

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Skyworks Solutions Inc

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Broadcom Inc

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 ON Semiconductor Corporation

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Senba Sensing Technology Co Ltd

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Renesas Electronics Corporation

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Standex Electronics Inc

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Sharp Devices Europe

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 LITE-ON Technology Inc (Lite-On Technology Corporation

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 Isocom Components Ltd

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.12 Everlight Electronics Co Ltd

- 13.1.12.1. Company Overview

- 13.1.12.2. Products

- 13.1.12.3. Company Financials

- 13.1.12.4. SWOT Analysis

- 13.1.13 Panasonic Corporation

- 13.1.13.1. Company Overview

- 13.1.13.2. Products

- 13.1.13.3. Company Financials

- 13.1.13.4. SWOT Analysis

- 13.1.14 Toshiba Electronic Devices & Storage Corporation (Toshiba Corp )

- 13.1.14.1. Company Overview

- 13.1.14.2. Products

- 13.1.14.3. Company Financials

- 13.1.14.4. SWOT Analysis

- 13.1.1 Shenzhen Kento Electronic Co Ltd

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Optocouplers Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Optocouplers Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 3: North America Optocouplers Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 4: North America Optocouplers Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 5: North America Optocouplers Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 6: North America Optocouplers Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Optocouplers Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Optocouplers Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 9: Europe Optocouplers Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 10: Europe Optocouplers Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 11: Europe Optocouplers Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 12: Europe Optocouplers Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Optocouplers Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Optocouplers Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 15: Asia Optocouplers Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 16: Asia Optocouplers Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 17: Asia Optocouplers Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 18: Asia Optocouplers Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Optocouplers Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Australia and New Zealand Optocouplers Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 21: Australia and New Zealand Optocouplers Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 22: Australia and New Zealand Optocouplers Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 23: Australia and New Zealand Optocouplers Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: Australia and New Zealand Optocouplers Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Australia and New Zealand Optocouplers Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Latin America Optocouplers Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 27: Latin America Optocouplers Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 28: Latin America Optocouplers Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 29: Latin America Optocouplers Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 30: Latin America Optocouplers Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Latin America Optocouplers Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: Middle East and Africa Optocouplers Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 33: Middle East and Africa Optocouplers Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 34: Middle East and Africa Optocouplers Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 35: Middle East and Africa Optocouplers Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 36: Middle East and Africa Optocouplers Industry Revenue (Million), by Country 2025 & 2033

- Figure 37: Middle East and Africa Optocouplers Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Optocouplers Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 2: Global Optocouplers Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 3: Global Optocouplers Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Optocouplers Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 5: Global Optocouplers Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 6: Global Optocouplers Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Global Optocouplers Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 8: Global Optocouplers Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 9: Global Optocouplers Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 10: Global Optocouplers Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 11: Global Optocouplers Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 12: Global Optocouplers Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global Optocouplers Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 14: Global Optocouplers Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 15: Global Optocouplers Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Optocouplers Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 17: Global Optocouplers Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 18: Global Optocouplers Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 19: Global Optocouplers Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 20: Global Optocouplers Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 21: Global Optocouplers Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Optocouplers Industry?

The projected CAGR is approximately 8.99%.

2. Which companies are prominent players in the Optocouplers Industry?

Key companies in the market include Shenzhen Kento Electronic Co Ltd, Vishay Intertechnology Inc, Skyworks Solutions Inc, Broadcom Inc, ON Semiconductor Corporation, Senba Sensing Technology Co Ltd, Renesas Electronics Corporation, Standex Electronics Inc, Sharp Devices Europe, LITE-ON Technology Inc (Lite-On Technology Corporation, Isocom Components Ltd, Everlight Electronics Co Ltd, Panasonic Corporation, Toshiba Electronic Devices & Storage Corporation (Toshiba Corp ).

3. What are the main segments of the Optocouplers Industry?

The market segments include Product Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.76 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Hybrid Electric Vehicles; Increasing Industrial Automation.

6. What are the notable trends driving market growth?

Increasing Industrial Automation to Drive the Market.

7. Are there any restraints impacting market growth?

Intrinsic Wear-out.

8. Can you provide examples of recent developments in the market?

May 2024 - Vishay Intertechnology, Inc. has introduced a new high-speed optocoupler, the VOIH72A, capable of transmitting data at 25 MBd. It includes a CMOS logic interface for digital input and output to make integration into digital systems easier. Created for use in industrial settings, this product provides a minimal 6 ns maximum pulse width distortion and requires only 2 mA of supply current. It can operate at voltages ranging from 2.7V to 5.5V and temperatures up to +110°C. The optocoupler includes CMOS logic for its digital input and output, allowing for a high-speed data rate of 25 MBd.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Optocouplers Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Optocouplers Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Optocouplers Industry?

To stay informed about further developments, trends, and reports in the Optocouplers Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence