Key Insights

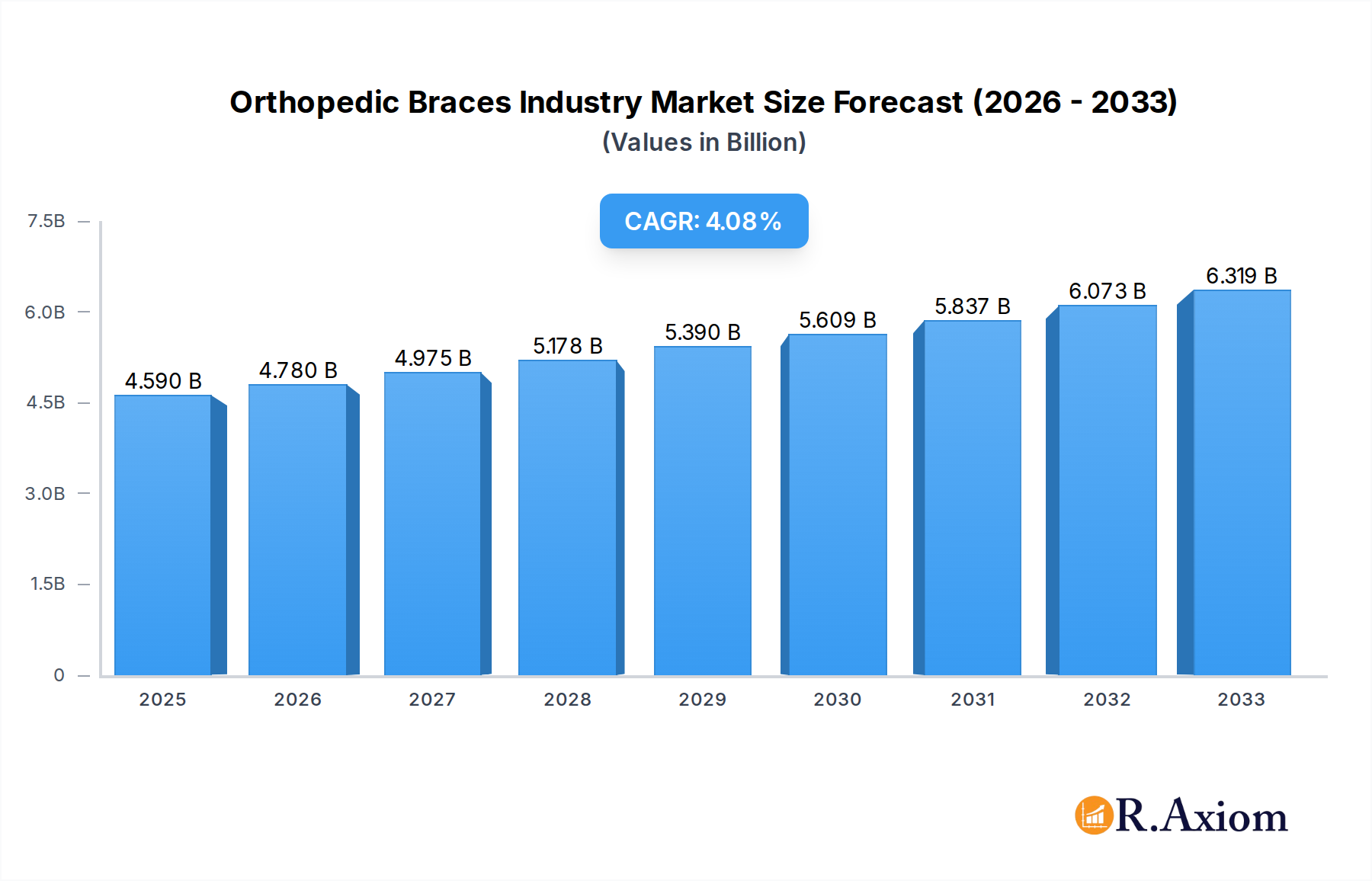

The global Orthopedic Braces and Supports market is poised for substantial growth, projected to reach approximately $4.59 billion by 2025. This expansion is driven by a confluence of factors, including the increasing prevalence of orthopedic conditions such as osteoarthritis and sports-related injuries, an aging global population leading to a higher incidence of musculoskeletal disorders, and growing awareness and adoption of non-invasive treatment options. Technological advancements in materials science and design have led to the development of more comfortable, effective, and personalized bracing solutions, further fueling market demand. The rising participation in sports and athletic activities, both professional and recreational, also contributes significantly to the need for specialized orthopedic supports for injury prevention and rehabilitation. Furthermore, the increasing disposable income in emerging economies is enabling greater access to advanced medical devices like orthopedic braces, expanding the market's reach and potential.

Orthopedic Braces Industry Market Size (In Billion)

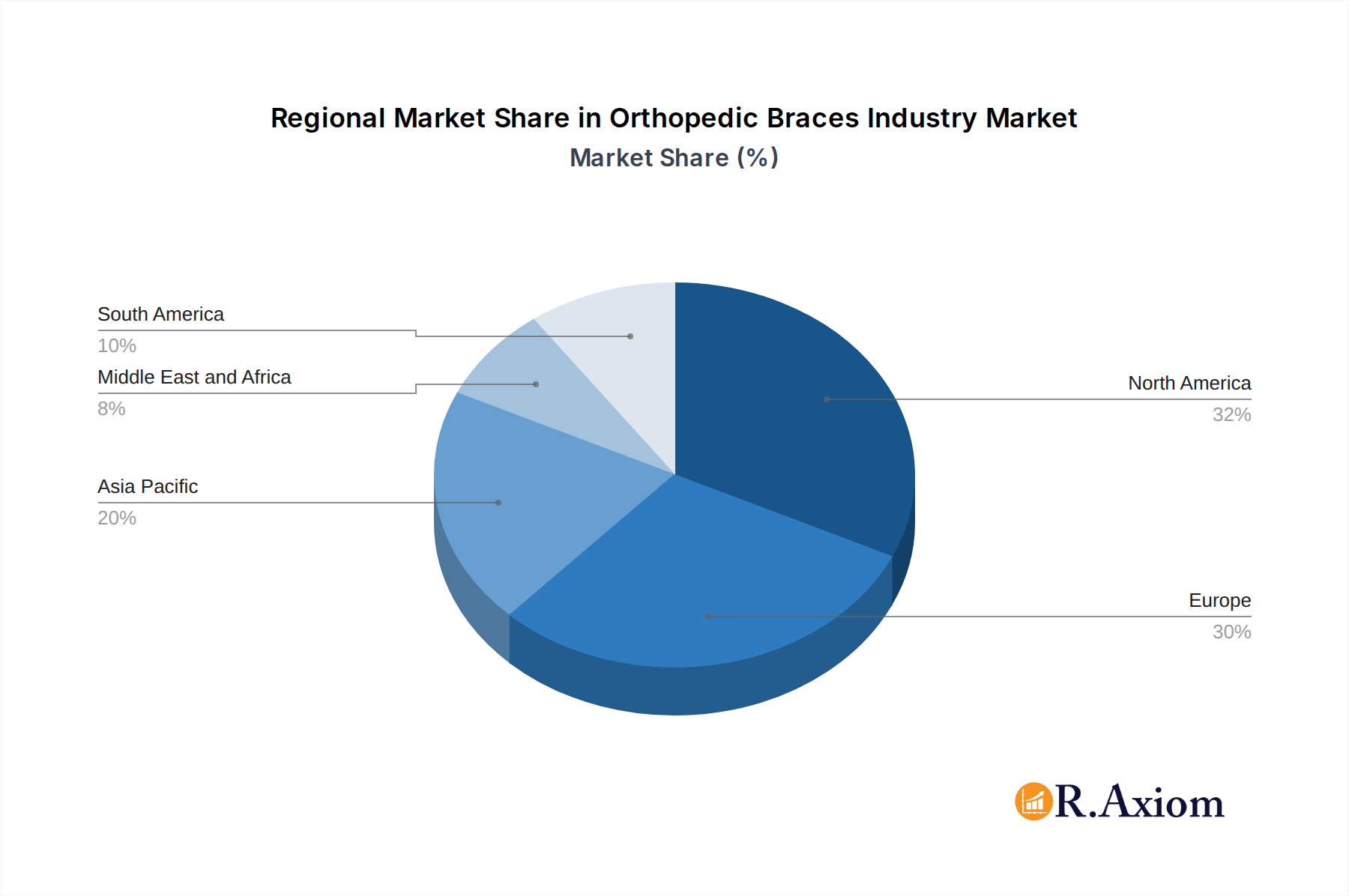

The market is anticipated to expand at a Compound Annual Growth Rate (CAGR) of 4.40% from 2025 through 2033, indicating a steady and robust upward trajectory. Key segments within this market include lower extremity braces (ankle and foot, hip, knee), spinal braces, and upper extremity braces (elbow, hand, and wrist). The end-user landscape is dominated by hospitals and orthopedic centers, with a growing contribution from other end-user segments as home healthcare and personalized rehabilitation solutions gain traction. Geographically, North America and Europe currently represent the largest markets due to advanced healthcare infrastructure and high patient awareness. However, the Asia Pacific region is expected to witness the fastest growth, driven by increasing healthcare investments, a growing middle class, and a rising incidence of lifestyle-related orthopedic issues. Major players like Ossur, Medi GmbH & Co KG, and DJO LLC (Enovis) are actively engaged in research and development, strategic partnerships, and product innovation to capture market share in this dynamic sector.

Orthopedic Braces Industry Company Market Share

This in-depth report provides a strategic analysis of the global Orthopedic Braces Industry, offering critical insights for stakeholders. Spanning a study period from 2019 to 2033, with a base year of 2025 and a forecast period of 2025–2033, this report leverages historical data from 2019–2024 to present a robust market outlook. The Orthopedic Braces market is projected to reach XX Billion by 2025, with a Compound Annual Growth Rate (CAGR) of XX% during the forecast period. This report delves into market concentration, innovation, trends, dominant segments, product developments, key drivers, challenges, emerging opportunities, leading players, and crucial industry developments, providing a definitive guide for navigating this dynamic sector.

Orthopedic Braces Industry Market Concentration & Innovation

The Orthopedic Braces Industry is characterized by a moderate market concentration, with several key players dominating market share. However, the landscape is continuously evolving due to technological advancements and strategic acquisitions. Innovation is a primary driver, focusing on lightweight materials, improved biomechanics, and smart functionalities for enhanced patient outcomes and user comfort. Regulatory frameworks, including FDA approvals and CE marking, play a crucial role in product validation and market access, influencing the pace of new product introductions. The presence of product substitutes, such as therapeutic exercises and surgical interventions, necessitates continuous product differentiation and value proposition enhancement. End-user preferences are shifting towards personalized solutions and post-operative rehabilitation support, driving demand for customized braces. Mergers and acquisitions (M&A) are significant strategic maneuvers, with recent deal values reaching hundreds of millions, consolidating market share and expanding product portfolios. For instance, Enovis Corporation's acquisition of LimaCorporate S.p.A. in September 2023, a move valued at approximately XX Million, underscores the industry's consolidation trend. This activity aims to leverage synergistic benefits, expand geographical reach, and capitalize on evolving market needs.

Orthopedic Braces Industry Industry Trends & Insights

The Orthopedic Braces Industry is experiencing robust growth driven by an aging global population, increasing incidence of sports-related injuries, and a rising awareness of non-surgical treatment options. Technological disruptions are transforming the market, with advancements in 3D printing enabling custom-fit braces and the integration of sensors for real-time monitoring of patient recovery. The adoption of wearable technology and data analytics is further enhancing the efficacy and personalized nature of orthopedic support. Consumer preferences are leaning towards minimally invasive treatments and faster recovery times, directly boosting the demand for advanced orthopedic braces. The competitive dynamics are intense, with companies investing heavily in research and development to gain a competitive edge. Market penetration is expected to surge as healthcare systems increasingly recognize the cost-effectiveness and efficacy of orthopedic bracing in managing a wide spectrum of musculoskeletal conditions. The market penetration for orthopedic braces is estimated to reach XX% by 2025, indicating substantial growth potential. The industry's CAGR is projected to be XX% between 2025 and 2033, reflecting sustained expansion.

Dominant Markets & Segments in Orthopedic Braces Industry

The Lower Extremity Braces and Supports segment, encompassing Ankle and Foot, Hip, and Knee braces, currently dominates the global Orthopedic Braces market, contributing an estimated XX% to the overall market value in 2025. This dominance is primarily attributed to the high prevalence of conditions such as osteoarthritis, sports injuries, and fractures affecting these extremities. The Knee Braces sub-segment, in particular, is a significant revenue generator, driven by the increasing incidence of sports-related ligament injuries and degenerative joint diseases among aging populations.

Geographically, North America stands out as the leading market for orthopedic braces, accounting for approximately XX% of the global market share. This leadership is underpinned by a well-established healthcare infrastructure, high disposable incomes, extensive insurance coverage for medical devices, and a strong culture of sports participation leading to a higher incidence of sports injuries. Within North America, the United States is the largest national market, propelled by advanced healthcare facilities, significant R&D investments, and a strong demand for advanced orthopedic solutions. Economic policies supporting healthcare innovation and infrastructure development further bolster this position.

The Hospitals segment represents the largest end-user category, accounting for XX% of the market in 2025. Hospitals are primary centers for diagnosis, treatment, and post-operative care, where orthopedic braces are frequently prescribed for a wide range of acute and chronic conditions. The increasing number of orthopedic surgeries performed globally also contributes to the demand from this segment. Orthopedic Centers follow closely, offering specialized care and rehabilitation services, and are key drivers for specialized and custom bracing solutions. The growth in specialized orthopedic clinics and rehabilitation facilities is a significant trend.

Key drivers for the dominance of these segments include:

- High Prevalence of Musculoskeletal Disorders: The increasing burden of conditions like arthritis, osteoporosis, and sports injuries directly fuels demand for orthopedic braces.

- Technological Advancements: Innovations in materials science and design lead to more effective and comfortable braces, enhancing patient compliance and outcomes.

- Aging Global Population: As life expectancy increases, so does the incidence of age-related orthopedic issues, driving the demand for supportive devices.

- Growing Sports Participation: The rise in recreational and professional sports globally contributes to a higher number of sports-related injuries requiring bracing.

- Increased Awareness and Diagnosis: Greater patient and physician awareness of non-surgical treatment options and early diagnosis leads to earlier intervention with braces.

- Reimbursement Policies: Favorable reimbursement policies in developed nations for orthopedic devices facilitate access and adoption.

Orthopedic Braces Industry Product Developments

Product innovation in the Orthopedic Braces Industry is centered on enhancing patient comfort, improving functional recovery, and integrating smart technologies. Advancements include the development of lightweight, breathable materials that improve compliance, alongside sophisticated biomechanical designs that offer targeted support and controlled motion. 3D printing technology is revolutionizing the production of highly customized braces, providing an optimal fit and addressing unique anatomical needs. Smart braces equipped with sensors are emerging, enabling remote patient monitoring, data collection on adherence and progress, and personalized rehabilitation guidance, offering significant competitive advantages.

Report Scope & Segmentation Analysis

This comprehensive report segments the Orthopedic Braces Industry by Product and End User. The Product segmentation includes Lower Extremity Braces and Supports (Ankle and Foot, Hip, Knee), Spinal Braces and Supports, and Upper Extremity Braces and Supports (Elbow, Hand and Wrist, Others). The End User segmentation comprises Hospitals, Orthopedic Centers, and Other End Users. The Lower Extremity Braces and Supports segment, projected to reach a market size of approximately XX Billion by 2025, is expected to witness a CAGR of XX% during the forecast period, driven by the high incidence of associated conditions. Spinal Braces and Supports, estimated at XX Billion in 2025, are expected to grow at a CAGR of XX%. Upper Extremity Braces and Supports are anticipated to reach XX Billion by 2025, with a CAGR of XX%. Hospitals are expected to maintain their dominance as the primary end-user segment, projected at XX% market share in 2025, while Orthopedic Centers and Other End Users will also exhibit steady growth.

Key Drivers of Orthopedic Braces Industry Growth

The Orthopedic Braces Industry's growth is propelled by several key factors. The escalating prevalence of chronic orthopedic conditions such as osteoarthritis and osteoporosis, exacerbated by an aging global population, is a primary driver. Furthermore, the increasing incidence of sports-related injuries among both professional athletes and the general populace fuels demand for effective support and rehabilitation solutions. Technological innovations, including the development of lightweight materials, advanced designs for enhanced mobility, and the integration of smart sensors for patient monitoring, are also significant growth catalysts. Regulatory support for non-surgical treatment options and favorable reimbursement policies in various regions further contribute to market expansion.

Challenges in the Orthopedic Braces Industry Sector

Despite robust growth, the Orthopedic Braces Industry faces several challenges. Stringent regulatory approval processes in different countries can delay market entry for new products, increasing R&D costs and time-to-market. Supply chain disruptions, particularly in raw material sourcing and manufacturing, can impact production volumes and delivery timelines. The high cost of some advanced orthopedic braces can be a barrier to access for certain patient populations and healthcare systems. Moreover, the competitive landscape is intense, with a constant pressure to innovate and offer cost-effective solutions, while the availability of alternative treatments like physical therapy and minimally invasive surgical procedures poses a competitive threat.

Emerging Opportunities in Orthopedic Braces Industry

Emerging opportunities within the Orthopedic Braces Industry are multifaceted. The growing demand for personalized and custom-fit braces, facilitated by advancements in 3D printing and digital scanning technologies, presents a significant market. The development and adoption of smart braces with integrated sensors for remote patient monitoring and rehabilitation tracking offer substantial potential for improved patient outcomes and new revenue streams. The expanding geriatric population globally, coupled with a rising awareness of proactive joint health management, creates a sustained demand for orthopedic support. Furthermore, the increasing focus on preventive care and sports injury management in emerging economies represents untapped market potential for both established and new players.

Leading Players in the Orthopedic Braces Industry Market

- Frank Stubbs Company Inc

- Bauerfeind

- Ossur

- Medi GmbH & Co KG

- Essity Medical Solutions (BSN Medical)

- DeRoyal Industries Inc

- 3M

- DJO LLC (Enovis)

- Bird & Cronin LLC

- Becker Orthopedic

- ALCARE Co Ltd

- Ottobock SE & Co KGaA

- Zimmer Biomet

Key Developments in Orthopedic Braces Industry Industry

- October 2023: OrthoPediatrics Corp. announced the limited release of the DF2 Brace as part of its expansion in the non-surgical business for treating kids with musculoskeletal injuries.

- September 2023: Enovis Corporation has agreed to acquire LimaCorporate S.p.A. It offers a wide variety of orthopedic medical devices, including braces and other support apparatus.

Strategic Outlook for Orthopedic Braces Industry Market

The strategic outlook for the Orthopedic Braces Industry remains highly positive, driven by ongoing innovation and expanding market needs. The increasing adoption of digital health technologies, including wearable sensors and AI-powered analytics for personalized rehabilitation, will be a key growth catalyst. Strategic partnerships between brace manufacturers and healthcare providers will be crucial for enhancing patient care pathways and expanding market reach. Furthermore, the growing emphasis on sports medicine and preventive healthcare will continue to fuel demand for advanced orthopedic solutions. Companies focusing on product differentiation through superior design, material innovation, and a strong emphasis on clinical outcomes are well-positioned for sustained success in this dynamic and evolving market.

Orthopedic Braces Industry Segmentation

-

1. Product

-

1.1. Lower Extremity Braces and Supports

- 1.1.1. Ankle and Foot

- 1.1.2. Hip

- 1.1.3. Knee

- 1.2. Spinal Braces and Supports

-

1.3. Upper Extremity Braces and Supports

- 1.3.1. Elbow

- 1.3.2. Hand and Wrist

- 1.3.3. Others

-

1.1. Lower Extremity Braces and Supports

-

2. End User

- 2.1. Hospitals

- 2.2. Orthopedic Centers

- 2.3. Other End Users

Orthopedic Braces Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Orthopedic Braces Industry Regional Market Share

Geographic Coverage of Orthopedic Braces Industry

Orthopedic Braces Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.40% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Lower Extremity Braces and Supports

- 5.1.1.1. Ankle and Foot

- 5.1.1.2. Hip

- 5.1.1.3. Knee

- 5.1.2. Spinal Braces and Supports

- 5.1.3. Upper Extremity Braces and Supports

- 5.1.3.1. Elbow

- 5.1.3.2. Hand and Wrist

- 5.1.3.3. Others

- 5.1.1. Lower Extremity Braces and Supports

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Hospitals

- 5.2.2. Orthopedic Centers

- 5.2.3. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. Global Orthopedic Braces Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Lower Extremity Braces and Supports

- 6.1.1.1. Ankle and Foot

- 6.1.1.2. Hip

- 6.1.1.3. Knee

- 6.1.2. Spinal Braces and Supports

- 6.1.3. Upper Extremity Braces and Supports

- 6.1.3.1. Elbow

- 6.1.3.2. Hand and Wrist

- 6.1.3.3. Others

- 6.1.1. Lower Extremity Braces and Supports

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Hospitals

- 6.2.2. Orthopedic Centers

- 6.2.3. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. North America Orthopedic Braces Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product

- 7.1.1. Lower Extremity Braces and Supports

- 7.1.1.1. Ankle and Foot

- 7.1.1.2. Hip

- 7.1.1.3. Knee

- 7.1.2. Spinal Braces and Supports

- 7.1.3. Upper Extremity Braces and Supports

- 7.1.3.1. Elbow

- 7.1.3.2. Hand and Wrist

- 7.1.3.3. Others

- 7.1.1. Lower Extremity Braces and Supports

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. Hospitals

- 7.2.2. Orthopedic Centers

- 7.2.3. Other End Users

- 7.1. Market Analysis, Insights and Forecast - by Product

- 8. Europe Orthopedic Braces Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product

- 8.1.1. Lower Extremity Braces and Supports

- 8.1.1.1. Ankle and Foot

- 8.1.1.2. Hip

- 8.1.1.3. Knee

- 8.1.2. Spinal Braces and Supports

- 8.1.3. Upper Extremity Braces and Supports

- 8.1.3.1. Elbow

- 8.1.3.2. Hand and Wrist

- 8.1.3.3. Others

- 8.1.1. Lower Extremity Braces and Supports

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. Hospitals

- 8.2.2. Orthopedic Centers

- 8.2.3. Other End Users

- 8.1. Market Analysis, Insights and Forecast - by Product

- 9. Asia Pacific Orthopedic Braces Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product

- 9.1.1. Lower Extremity Braces and Supports

- 9.1.1.1. Ankle and Foot

- 9.1.1.2. Hip

- 9.1.1.3. Knee

- 9.1.2. Spinal Braces and Supports

- 9.1.3. Upper Extremity Braces and Supports

- 9.1.3.1. Elbow

- 9.1.3.2. Hand and Wrist

- 9.1.3.3. Others

- 9.1.1. Lower Extremity Braces and Supports

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. Hospitals

- 9.2.2. Orthopedic Centers

- 9.2.3. Other End Users

- 9.1. Market Analysis, Insights and Forecast - by Product

- 10. Middle East and Africa Orthopedic Braces Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product

- 10.1.1. Lower Extremity Braces and Supports

- 10.1.1.1. Ankle and Foot

- 10.1.1.2. Hip

- 10.1.1.3. Knee

- 10.1.2. Spinal Braces and Supports

- 10.1.3. Upper Extremity Braces and Supports

- 10.1.3.1. Elbow

- 10.1.3.2. Hand and Wrist

- 10.1.3.3. Others

- 10.1.1. Lower Extremity Braces and Supports

- 10.2. Market Analysis, Insights and Forecast - by End User

- 10.2.1. Hospitals

- 10.2.2. Orthopedic Centers

- 10.2.3. Other End Users

- 10.1. Market Analysis, Insights and Forecast - by Product

- 11. South America Orthopedic Braces Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product

- 11.1.1. Lower Extremity Braces and Supports

- 11.1.1.1. Ankle and Foot

- 11.1.1.2. Hip

- 11.1.1.3. Knee

- 11.1.2. Spinal Braces and Supports

- 11.1.3. Upper Extremity Braces and Supports

- 11.1.3.1. Elbow

- 11.1.3.2. Hand and Wrist

- 11.1.3.3. Others

- 11.1.1. Lower Extremity Braces and Supports

- 11.2. Market Analysis, Insights and Forecast - by End User

- 11.2.1. Hospitals

- 11.2.2. Orthopedic Centers

- 11.2.3. Other End Users

- 11.1. Market Analysis, Insights and Forecast - by Product

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Frank Stubbs Company Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Bauerfeind

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Ossur

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Medi GmbH & Co KG

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Essity Medical Solutions (BSN Medical)

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 DeRoyal Industries Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 3M

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 DJO LLC (Enovis)

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Bird & Cronin LLC

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Becker Orthopedic

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 ALCARE Co Ltd

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Ottobock SE & Co KGaA

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Zimmer Biomet

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.1 Frank Stubbs Company Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Orthopedic Braces Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Orthopedic Braces Industry Revenue (Million), by Product 2025 & 2033

- Figure 3: North America Orthopedic Braces Industry Revenue Share (%), by Product 2025 & 2033

- Figure 4: North America Orthopedic Braces Industry Revenue (Million), by End User 2025 & 2033

- Figure 5: North America Orthopedic Braces Industry Revenue Share (%), by End User 2025 & 2033

- Figure 6: North America Orthopedic Braces Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Orthopedic Braces Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Orthopedic Braces Industry Revenue (Million), by Product 2025 & 2033

- Figure 9: Europe Orthopedic Braces Industry Revenue Share (%), by Product 2025 & 2033

- Figure 10: Europe Orthopedic Braces Industry Revenue (Million), by End User 2025 & 2033

- Figure 11: Europe Orthopedic Braces Industry Revenue Share (%), by End User 2025 & 2033

- Figure 12: Europe Orthopedic Braces Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Orthopedic Braces Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Orthopedic Braces Industry Revenue (Million), by Product 2025 & 2033

- Figure 15: Asia Pacific Orthopedic Braces Industry Revenue Share (%), by Product 2025 & 2033

- Figure 16: Asia Pacific Orthopedic Braces Industry Revenue (Million), by End User 2025 & 2033

- Figure 17: Asia Pacific Orthopedic Braces Industry Revenue Share (%), by End User 2025 & 2033

- Figure 18: Asia Pacific Orthopedic Braces Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Pacific Orthopedic Braces Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East and Africa Orthopedic Braces Industry Revenue (Million), by Product 2025 & 2033

- Figure 21: Middle East and Africa Orthopedic Braces Industry Revenue Share (%), by Product 2025 & 2033

- Figure 22: Middle East and Africa Orthopedic Braces Industry Revenue (Million), by End User 2025 & 2033

- Figure 23: Middle East and Africa Orthopedic Braces Industry Revenue Share (%), by End User 2025 & 2033

- Figure 24: Middle East and Africa Orthopedic Braces Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Middle East and Africa Orthopedic Braces Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Orthopedic Braces Industry Revenue (Million), by Product 2025 & 2033

- Figure 27: South America Orthopedic Braces Industry Revenue Share (%), by Product 2025 & 2033

- Figure 28: South America Orthopedic Braces Industry Revenue (Million), by End User 2025 & 2033

- Figure 29: South America Orthopedic Braces Industry Revenue Share (%), by End User 2025 & 2033

- Figure 30: South America Orthopedic Braces Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: South America Orthopedic Braces Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Orthopedic Braces Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 2: Global Orthopedic Braces Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 3: Global Orthopedic Braces Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Orthopedic Braces Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 5: Global Orthopedic Braces Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 6: Global Orthopedic Braces Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States Orthopedic Braces Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada Orthopedic Braces Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Orthopedic Braces Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Global Orthopedic Braces Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 11: Global Orthopedic Braces Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 12: Global Orthopedic Braces Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Germany Orthopedic Braces Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom Orthopedic Braces Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: France Orthopedic Braces Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Italy Orthopedic Braces Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Spain Orthopedic Braces Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Rest of Europe Orthopedic Braces Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Global Orthopedic Braces Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 20: Global Orthopedic Braces Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 21: Global Orthopedic Braces Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 22: China Orthopedic Braces Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Japan Orthopedic Braces Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: India Orthopedic Braces Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Australia Orthopedic Braces Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: South Korea Orthopedic Braces Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Asia Pacific Orthopedic Braces Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Global Orthopedic Braces Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 29: Global Orthopedic Braces Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 30: Global Orthopedic Braces Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 31: GCC Orthopedic Braces Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: South Africa Orthopedic Braces Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: Rest of Middle East and Africa Orthopedic Braces Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Global Orthopedic Braces Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 35: Global Orthopedic Braces Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 36: Global Orthopedic Braces Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 37: Brazil Orthopedic Braces Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Argentina Orthopedic Braces Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 39: Rest of South America Orthopedic Braces Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Orthopedic Braces Industry?

The projected CAGR is approximately 4.40%.

2. Which companies are prominent players in the Orthopedic Braces Industry?

Key companies in the market include Frank Stubbs Company Inc, Bauerfeind, Ossur, Medi GmbH & Co KG, Essity Medical Solutions (BSN Medical), DeRoyal Industries Inc, 3M, DJO LLC (Enovis), Bird & Cronin LLC, Becker Orthopedic, ALCARE Co Ltd, Ottobock SE & Co KGaA, Zimmer Biomet.

3. What are the main segments of the Orthopedic Braces Industry?

The market segments include Product, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 4.59 Million as of 2022.

5. What are some drivers contributing to market growth?

Rise in Bone Fracture Cases; Rise in Musculoskeletal Disorders; Growing Number of Road Accidents and Sport-related Injuries.

6. What are the notable trends driving market growth?

Spinal Braces and Supports Segment is Expected to Witness Significant Growth Over the Forecast Period.

7. Are there any restraints impacting market growth?

Negligence Toward Minor Injuries; Lack of Awareness Regarding the New Orthopedic Braces and Supports.

8. Can you provide examples of recent developments in the market?

October 2023: OrthoPediatrics Corp. announced the limited release of the DF2 Brace as part of its expansion in the non-surgical business for treating kids with musculoskeletal injuries.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Orthopedic Braces Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Orthopedic Braces Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Orthopedic Braces Industry?

To stay informed about further developments, trends, and reports in the Orthopedic Braces Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence