Key Insights

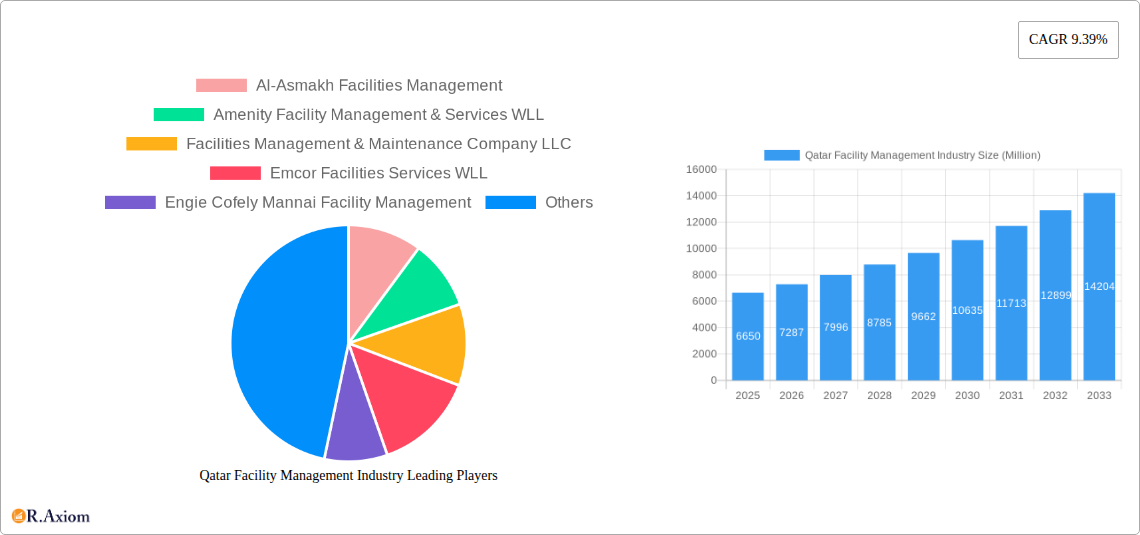

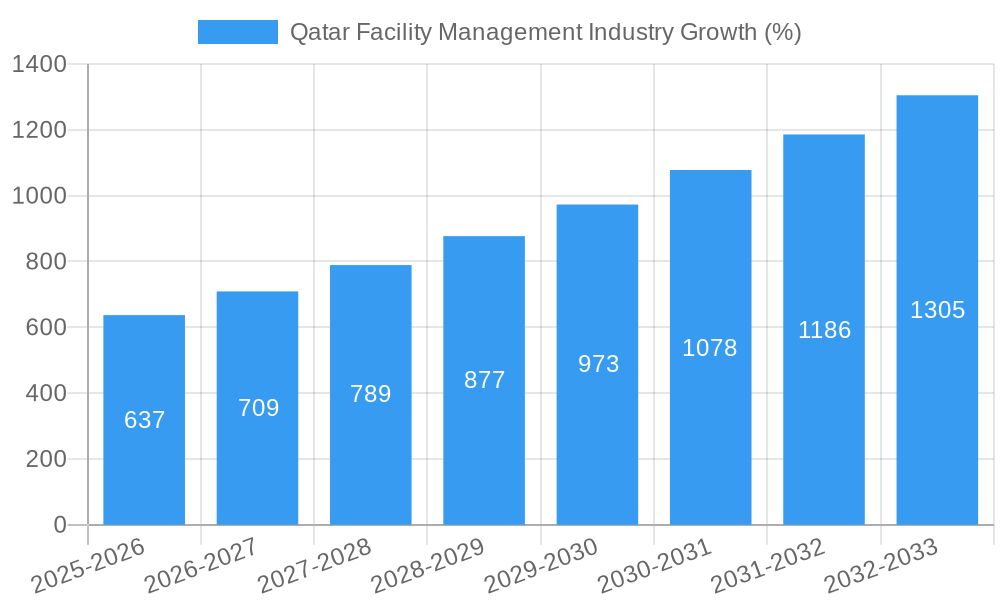

The Qatar facility management (FM) market, valued at $6.65 billion in 2025, is experiencing robust growth, projected to expand at a compound annual growth rate (CAGR) of 9.39% from 2025 to 2033. This significant expansion is fueled by several key factors. The country's ongoing infrastructure development, particularly in preparation for major events and diversification of its economy beyond hydrocarbons, is creating a substantial demand for comprehensive FM services. The increasing adoption of smart building technologies and a rising focus on sustainability within the built environment are further driving market growth. Furthermore, a growing awareness of the importance of efficient operational management and cost optimization within both public and private sectors is contributing to the outsourcing of FM services, thereby boosting market expansion. The market is segmented by type (in-house versus outsourced), offering (hard FM encompassing infrastructure and soft FM including cleaning services), and end-user (commercial, institutional, public/infrastructure, industrial). The significant investments in infrastructure projects, coupled with the nation’s commitment to creating world-class facilities, indicate that the demand for high-quality facility management services will continue to grow steadily over the forecast period.

The competitive landscape includes both international and local players, each vying for market share. Key players are likely to focus on strengthening their service portfolios to cater to the growing demand for specialized services, such as smart building management and sustainability solutions. Potential challenges include competition, the availability of skilled labor, and maintaining operational efficiency in light of potentially fluctuating economic conditions. However, with Qatar's consistent commitment to infrastructure development and its focus on improving the overall quality of life, the FM market is poised for continuous expansion and presents substantial opportunities for established and emerging companies alike. The forecast demonstrates a strong upward trajectory for the market throughout the projected period, indicating a positive outlook for investors and service providers alike.

Qatar Facility Management Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Qatar facility management industry, covering market size, segmentation, key players, growth drivers, challenges, and future outlook. The report utilizes data from the historical period (2019-2024), base year (2025), and forecast period (2025-2033), offering valuable insights for industry stakeholders, investors, and businesses operating within or looking to enter this dynamic market. The total market value in 2025 is estimated at xx Million.

Qatar Facility Management Industry Market Concentration & Innovation

The Qatar facility management market exhibits a moderately concentrated structure, with several large players holding significant market share. Al-Asmakh Facilities Management, Amenity Facility Management & Services WLL, and Emcor Facilities Services WLL are among the prominent players, although precise market share figures remain unavailable (xx%). Innovation is driven by increasing adoption of smart technologies, demand for sustainable practices, and government initiatives promoting efficiency in building operations. Regulatory frameworks, including building codes and safety standards, significantly influence market practices. While substitute services exist (e.g., individual contractors for specific tasks), integrated facility management solutions remain the dominant offering. End-user trends toward outsourcing and a preference for comprehensive service packages are shaping market demand. M&A activity has been moderate in recent years, with deal values averaging around xx Million per transaction. Key acquisitions have involved smaller firms being acquired by larger players to expand their service offerings and geographic reach.

Qatar Facility Management Industry Industry Trends & Insights

The Qatar facility management market is experiencing robust growth, driven by substantial investments in infrastructure development, a booming real estate sector, and the government's focus on creating smart cities. The Compound Annual Growth Rate (CAGR) during the forecast period (2025-2033) is projected to be xx%, fueled by increasing demand for efficient and sustainable building operations. Technological disruptions, such as the adoption of Building Information Modeling (BIM) and Internet of Things (IoT) solutions, are transforming industry operations. Consumer preference is shifting towards integrated, technology-driven facility management services that offer enhanced efficiency, cost optimization, and data-driven insights. Intense competition among established and emerging players is driving innovation and service differentiation. Market penetration of outsourced facility management services is increasing, exceeding xx% in 2025.

Dominant Markets & Segments in Qatar Facility Management Industry

- By Type: Outsourced facility management dominates the market, driven by the cost-effectiveness and expertise offered by specialized providers. Inhouse facility management remains prevalent for larger organizations with internal expertise.

- By Offering: Hard FM (technical services) and Soft FM (support services) are both significant segments. Hard FM enjoys slightly larger market share due to the extensive infrastructure needs of Qatar.

- By End-User: The commercial sector is the leading end-user, driven by the growth of the real estate and hospitality industries. The public/infrastructure sector is a significant contributor due to large-scale government projects. Institutional and industrial segments also contribute substantially, while other end-users represent a smaller but growing portion of the market. Key drivers include Qatar's substantial infrastructural investments, particularly in the lead-up to and following the FIFA World Cup 2022, and the rapid urbanization and economic diversification initiatives.

The dominance of Outsourced Facility Management and the Commercial sector is primarily due to the increasing focus on efficiency and specialized expertise required in managing large-scale commercial properties and infrastructure projects in Qatar. The high construction activity and focus on maintaining high-quality infrastructure further fuel this dominance.

Qatar Facility Management Industry Product Developments

Recent product innovations in Qatar's facility management sector involve integrated software platforms for managing maintenance, energy consumption, and security systems. The emphasis is on leveraging technologies such as IoT and AI for predictive maintenance, enhancing operational efficiency, and optimizing resource allocation. These solutions offer competitive advantages by delivering cost savings, improved operational visibility, and enhanced sustainability outcomes, aligning with the growing focus on smart buildings and sustainable practices in Qatar.

Report Scope & Segmentation Analysis

This report comprehensively analyzes the Qatar facility management industry across various segments:

- By Type: Inhouse and Outsourced Facility Management. Outsourced facility management is projected to show faster growth (xx% CAGR) than inhouse management (xx% CAGR) over the forecast period due to cost-effectiveness and expertise.

- By Offering: Hard FM (including HVAC, electrical, plumbing) and Soft FM (including cleaning, security, catering). Both segments are expected to experience similar growth rates, reflecting the integrated nature of modern facility management services.

- By End-User: Commercial, Institutional, Public/Infrastructure, Industrial, and Other End-Users. The commercial sector is expected to maintain its dominance, while the Public/Infrastructure sector will experience significant growth due to ongoing government initiatives. Competitive dynamics within each segment are influenced by the scale of operations and specific client needs.

Key Drivers of Qatar Facility Management Industry Growth

Several factors drive the growth of Qatar's facility management industry: Firstly, significant investments in infrastructure projects and real estate development fuel demand for efficient facility management services. Secondly, the government's focus on smart city initiatives and sustainable development promotes the adoption of technologically advanced solutions. Thirdly, the increasing awareness of the importance of efficient building operations and cost optimization drives outsourcing of facility management services. These combined factors have resulted in robust market growth and will continue to shape the industry's trajectory.

Challenges in the Qatar Facility Management Industry Sector

Challenges include the intense competition among providers, potentially leading to price pressures and reduced profit margins. Furthermore, attracting and retaining skilled personnel poses an ongoing challenge. Regulatory compliance and obtaining necessary permits can also create operational hurdles. These challenges impact the market's overall growth and operational efficiency, leading to a higher-than-average cost of service provision in certain areas. Supply chain disruptions, particularly during periods of global uncertainty, can also affect the timely delivery of services and materials.

Emerging Opportunities in Qatar Facility Management Industry

Emerging opportunities include the increasing adoption of smart building technologies, which will propel further growth. The growing demand for sustainable and green building practices presents new avenues for specialized providers. Expansion into underserved segments, such as healthcare facilities and specialized industrial operations, also offers significant potential. The government’s continued investments in mega-projects will create opportunities for large-scale facility management contracts.

Leading Players in the Qatar Facility Management Industry Market

- Al-Asmakh Facilities Management

- Amenity Facility Management & Services WLL

- Facilities Management & Maintenance Company LLC

- Emcor Facilities Services WLL

- Engie Cofely Mannai Facility Management

- G4S QATAR SPC

- Al Faisal Holdings (MMG Qatar)

- Sodexo Qatar Services

- Como Facility Management Services

- EFS Facilities Services

Key Developments in Qatar Facility Management Industry Industry

- March 2022: EDGNEX, a subsidiary of Damac Group, partnered with JLL for its facility management needs, signaling increased demand for professional services in the data center sector. This highlights the growing importance of specialized facility management solutions for technologically advanced industries.

Strategic Outlook for Qatar Facility Management Industry Market

The Qatar facility management market is poised for continued growth, driven by sustained investment in infrastructure and a focus on sustainable development. The adoption of innovative technologies and the increasing demand for integrated facility management solutions will shape the industry's future. Companies that can adapt to these trends, invest in technology, and deliver value-added services are expected to thrive in this dynamic market. The long-term growth potential is substantial, reflecting Qatar's ambitious development plans and the country's focus on creating a world-class infrastructure.

Qatar Facility Management Industry Segmentation

-

1. Offering Type

- 1.1. Hard FM

- 1.2. Soft FM

-

2. Type

- 2.1. In-house Facility Management

-

2.2. Outsourced Facility Management

- 2.2.1. Single FM

- 2.2.2. Bundled FM

- 2.2.3. Integrated FM

-

3. End User

- 3.1. Commercial

- 3.2. Institutional

- 3.3. Public/Infrastructure

- 3.4. Industrial

- 3.5. Other End Users

Qatar Facility Management Industry Segmentation By Geography

- 1. Qatar

Qatar Facility Management Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 9.39% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Emergence of Qatar as One of the Key Investment Destinations in the GCC; Growing Emphasis on the Outsourcing of Non-core Operations; Increase in Market Concentration Due to the Entry of Global Firms with Diversified Service Portfolios

- 3.3. Market Restrains

- 3.3.1. Regulatory & Legal Changes; Growing Presence of Global Firms Collaborating with Regional Entities Pose a Challenge for Local Firms

- 3.4. Market Trends

- 3.4.1. Public/ Infrastructure Sector Accounts for Significant Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Qatar Facility Management Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Offering Type

- 5.1.1. Hard FM

- 5.1.2. Soft FM

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. In-house Facility Management

- 5.2.2. Outsourced Facility Management

- 5.2.2.1. Single FM

- 5.2.2.2. Bundled FM

- 5.2.2.3. Integrated FM

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Commercial

- 5.3.2. Institutional

- 5.3.3. Public/Infrastructure

- 5.3.4. Industrial

- 5.3.5. Other End Users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Qatar

- 5.1. Market Analysis, Insights and Forecast - by Offering Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Al-Asmakh Facilities Management

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Amenity Facility Management & Services WLL

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Facilities Management & Maintenance Company LLC

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Emcor Facilities Services WLL

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Engie Cofely Mannai Facility Management

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 G4S QATAR SPC

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Al Faisal Holdings (MMG Qatar)

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Sodexo Qatar Services

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Como Facility Management Services

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 EFS Facilities Services

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Al-Asmakh Facilities Management

List of Figures

- Figure 1: Qatar Facility Management Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Qatar Facility Management Industry Share (%) by Company 2024

List of Tables

- Table 1: Qatar Facility Management Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Qatar Facility Management Industry Revenue Million Forecast, by Offering Type 2019 & 2032

- Table 3: Qatar Facility Management Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 4: Qatar Facility Management Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 5: Qatar Facility Management Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Qatar Facility Management Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: Qatar Facility Management Industry Revenue Million Forecast, by Offering Type 2019 & 2032

- Table 8: Qatar Facility Management Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 9: Qatar Facility Management Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 10: Qatar Facility Management Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Qatar Facility Management Industry?

The projected CAGR is approximately 9.39%.

2. Which companies are prominent players in the Qatar Facility Management Industry?

Key companies in the market include Al-Asmakh Facilities Management, Amenity Facility Management & Services WLL, Facilities Management & Maintenance Company LLC, Emcor Facilities Services WLL, Engie Cofely Mannai Facility Management, G4S QATAR SPC, Al Faisal Holdings (MMG Qatar), Sodexo Qatar Services, Como Facility Management Services, EFS Facilities Services.

3. What are the main segments of the Qatar Facility Management Industry?

The market segments include Offering Type, Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.65 Million as of 2022.

5. What are some drivers contributing to market growth?

Emergence of Qatar as One of the Key Investment Destinations in the GCC; Growing Emphasis on the Outsourcing of Non-core Operations; Increase in Market Concentration Due to the Entry of Global Firms with Diversified Service Portfolios.

6. What are the notable trends driving market growth?

Public/ Infrastructure Sector Accounts for Significant Growth.

7. Are there any restraints impacting market growth?

Regulatory & Legal Changes; Growing Presence of Global Firms Collaborating with Regional Entities Pose a Challenge for Local Firms.

8. Can you provide examples of recent developments in the market?

March 2022: EDGNEX, a subsidiary of Damac Group, operating in Qatar has partnered with JLL for its facility management needs as it pursues the first phase of its strategy to deliver data center facilities.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Qatar Facility Management Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Qatar Facility Management Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Qatar Facility Management Industry?

To stay informed about further developments, trends, and reports in the Qatar Facility Management Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence