Key Insights

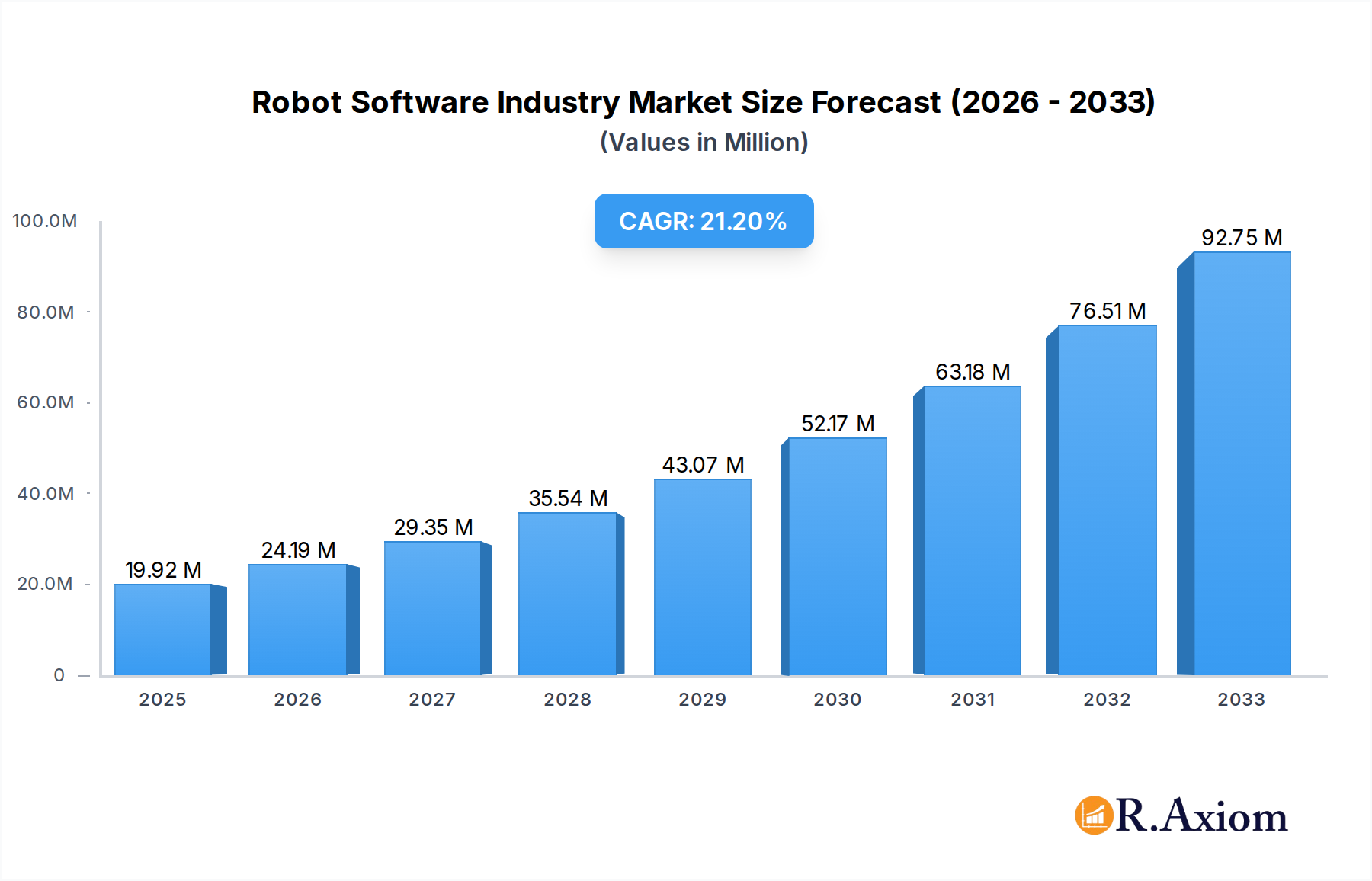

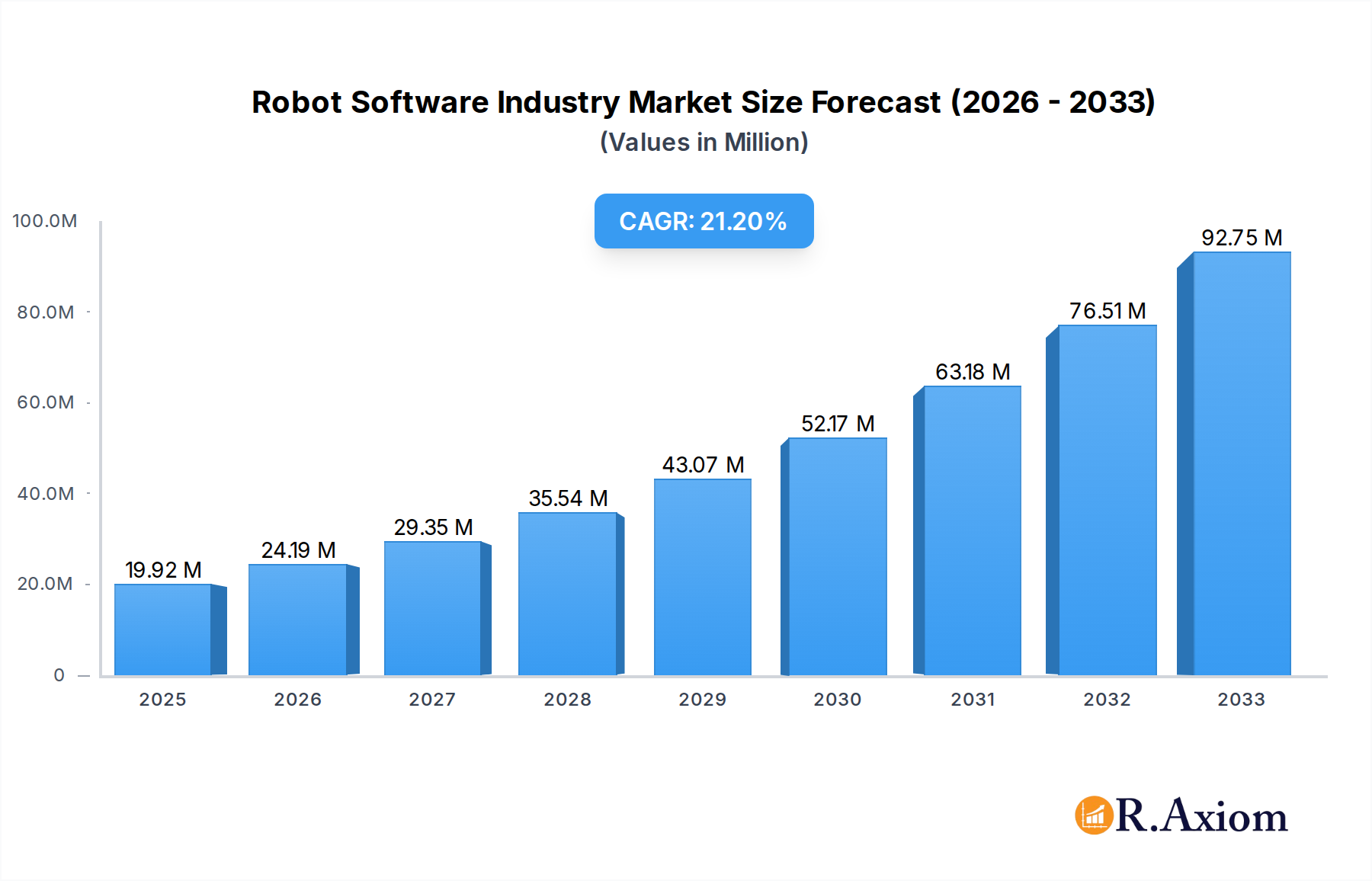

The global Robot Software market is experiencing robust expansion, projected to reach an estimated $19.92 million in 2025, fueled by an impressive compound annual growth rate (CAGR) of 21.62% through 2033. This significant growth is underpinned by several key drivers, including the increasing adoption of automation across various industries to enhance efficiency and productivity, the continuous advancements in Artificial Intelligence (AI) and machine learning that are making robots more intelligent and capable, and the burgeoning demand for sophisticated robotic solutions in sectors like healthcare, logistics, and manufacturing. The market is characterized by a dynamic landscape of software types, with Recognition Software, Simulation Software, and Predictive Maintenance Software emerging as critical components for advanced robotic operations. Furthermore, the integration of robots into both industrial and service applications, alongside flexible deployment models like on-premise and on-demand solutions, highlights the evolving nature of the robot software ecosystem. The expanding enterprise adoption, from small and medium-sized businesses to large corporations, signifies a broad market appeal and significant growth potential.

Robot Software Industry Market Size (In Million)

Key trends shaping the Robot Software market include the rise of collaborative robots (cobots) that work alongside humans, necessitating more intuitive and adaptable software. The increasing sophistication of AI algorithms is enabling robots to perform more complex tasks, driving demand for advanced data management and analysis software. Predictive maintenance software is gaining traction as businesses seek to minimize downtime and optimize robot performance. While the market is poised for substantial growth, potential restraints such as the high initial investment costs for advanced robotic systems and the need for skilled personnel to develop, implement, and maintain these software solutions could pose challenges. However, the overwhelming benefits of robotic automation, including improved safety, reduced operational costs, and enhanced precision, are expected to outweigh these limitations, propelling the market forward. The market is also seeing significant investment and innovation across diverse end-user verticals, from automotive manufacturing to cutting-edge healthcare applications, underscoring its widespread impact and transformative potential.

Robot Software Industry Company Market Share

Robot Software Industry Market Concentration & Innovation

The Robot Software Industry is characterized by a dynamic market concentration driven by significant innovation. Key players like NVIDIA Corporation, ABB Ltd, and CloudMinds Technology Inc are investing heavily in research and development, fueling advancements in areas such as AI-powered robotics, machine learning, and enhanced human-robot interaction. The market is witnessing robust M&A activity, with recent acquisitions like Rockwell's move for Clearpath Robotics (deal value estimated at over a billion dollars) signaling a consolidation trend and a focus on expanding automation capabilities in manufacturing. Regulatory frameworks are evolving to address safety, ethics, and data privacy in robotic deployments, impacting the pace of innovation and market entry. Product substitutes, while nascent, are emerging in the form of advanced automation tools and software-as-a-service (SaaS) solutions that can augment or replace certain robotic functions. End-user trends, including the increasing demand for automation in logistics and healthcare, are directly influencing the direction of software development, prioritizing efficiency, precision, and adaptability.

- Innovation Drivers: Artificial Intelligence (AI), Machine Learning (ML), Computer Vision, Edge Computing, 5G Connectivity.

- M&A Activities: Increased consolidation, strategic partnerships aimed at expanding product portfolios and market reach.

- Market Share Landscape: Dominated by a few large corporations with significant R&D budgets, but with growing niches for specialized software providers.

- Regulatory Impact: Focus on ethical AI, data security, and interoperability standards.

Robot Software Industry Industry Trends & Insights

The Robot Software Industry is poised for substantial growth, driven by a confluence of technological advancements and increasing adoption across diverse sectors. The projected Compound Annual Growth Rate (CAGR) for the forecast period of 2025–2033 is estimated to be a robust XX%, indicating a significant expansion of the market. Market penetration is accelerating as businesses recognize the tangible benefits of robotic automation, including enhanced productivity, reduced operational costs, and improved safety. Key growth drivers include the escalating demand for automation in manufacturing and logistics to address labor shortages and optimize supply chains. Furthermore, the continuous evolution of AI and ML algorithms is enabling robots to perform more complex tasks with greater autonomy and intelligence, thereby expanding their application scope.

Technological disruptions are a constant feature, with advancements in areas like natural language processing (NLP) enabling more intuitive human-robot communication and computer vision systems improving object recognition and navigation capabilities. Consumer preferences are shifting towards more personalized and efficient services, which robots can facilitate through automated order fulfillment, delivery, and customer support. The competitive dynamics within the industry are intensifying, with both established technology giants and agile startups vying for market share. This competition fosters rapid innovation and leads to the development of specialized software solutions catering to niche market needs. The integration of robots with the Internet of Things (IoT) is creating smarter, more interconnected ecosystems, unlocking new possibilities for data analysis and predictive maintenance.

The increasing adoption of cloud-based robotics platforms is also a significant trend, offering scalability, flexibility, and cost-effectiveness for businesses of all sizes. This shift towards on-demand deployment models democratizes access to advanced robotic capabilities, enabling small and medium enterprises (SMEs) to compete more effectively. The ongoing investment in robotics research and development, particularly in areas like soft robotics and human-robot collaboration, promises to further broaden the application landscape and drive market growth. The healthcare sector, for instance, is increasingly leveraging robotic software for surgical assistance, patient care, and diagnostics. Similarly, the retail and e-commerce sector is utilizing robots for inventory management, warehousing, and last-mile delivery. The government and defense sectors are exploring robotic solutions for surveillance, reconnaissance, and hazardous environment operations. This widespread applicability underscores the pervasive impact of robot software across the global economy.

Dominant Markets & Segments in Robot Software Industry

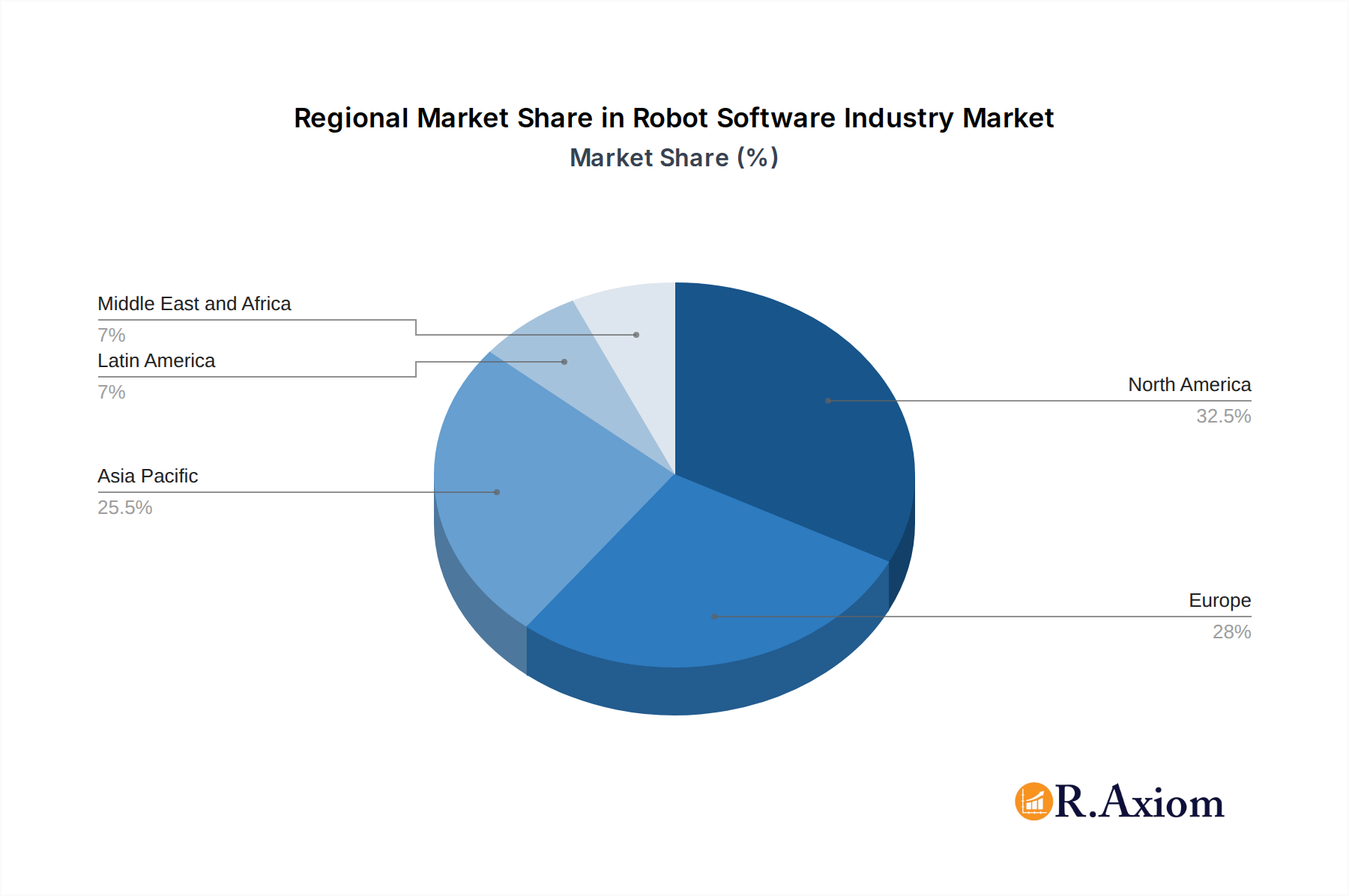

The Robot Software Industry exhibits a pronounced dominance in specific regions and segments, driven by a combination of economic policies, robust infrastructure, and a high degree of technological adoption.

Leading Regions:

- North America: This region is a major contributor due to significant R&D investments from leading technology companies, strong government support for automation initiatives, and a large presence of end-user industries like automotive, manufacturing, and healthcare. The presence of key players like NVIDIA Corporation and Brain Corporation further bolsters its dominance.

- Europe: Driven by a strong industrial base, particularly in Germany, and government initiatives promoting Industry 4.0, Europe is a significant market. Stringent quality and safety standards also drive demand for sophisticated robot software.

- Asia Pacific: This region is experiencing rapid growth fueled by its burgeoning manufacturing sector, increasing adoption of automation in countries like China and Japan, and a growing demand for service robots in emerging economies.

Dominant Software Types:

- Recognition Software: This segment is crucial for enabling robots to perceive and interpret their environment, driving applications in autonomous navigation, object manipulation, and human-robot interaction.

- Data Management and Analysis Software: As robots generate vast amounts of data, the software for collecting, organizing, and analyzing this information for insights into performance optimization and predictive maintenance is paramount.

- Simulation Software: Essential for designing, testing, and validating robot behaviors and environments in a virtual setting, reducing development costs and risks.

Dominant Robot Types:

- Industrial Robots: While a mature market, the software controlling these robots continues to evolve for greater flexibility, precision, and collaboration with human workers in manufacturing settings.

- Service Robots: This segment is experiencing exponential growth, particularly in areas like logistics, healthcare, and hospitality, driven by increasing demand for automation in non-industrial environments.

Dominant Deployment Models:

- On-Premise: Traditional deployment for organizations with stringent data security requirements or existing IT infrastructure.

- On-Demand: Increasingly popular due to its scalability, flexibility, and cost-effectiveness, particularly for SMEs and cloud-intensive applications.

Dominant Enterprise Sizes:

- Large Enterprises: These organizations are early adopters, investing heavily in comprehensive robotic solutions to achieve significant operational efficiencies and competitive advantages.

- Small and Medium Enterprises (SMEs): With the advent of more accessible and affordable robot software solutions, SMEs are increasingly integrating automation into their operations.

Dominant End-user Verticals:

- Manufacturing: This sector remains the largest consumer of industrial robot software, driven by the need for increased production efficiency, quality control, and customization.

- Transportation and Logistics: The demand for automated warehousing, inventory management, and last-mile delivery is propelling the growth of robotic solutions in this vertical.

- Automotive: A pioneer in industrial robotics, the automotive sector continues to drive innovation in robot software for assembly, welding, and painting applications.

Robot Software Industry Product Developments

Recent product developments highlight a strong emphasis on enhancing robot autonomy, intelligence, and ease of integration. Innovations are focused on AI-driven perception, sophisticated navigation algorithms, and seamless communication protocols. Companies are developing specialized software modules for tasks like complex manipulation, predictive maintenance, and human-robot collaboration. These advancements are creating robots that are more adaptable to dynamic environments and capable of performing a wider range of tasks with greater precision and efficiency, thereby expanding their market applicability and providing a significant competitive advantage to early adopters.

Report Scope & Segmentation Analysis

This report offers a comprehensive analysis of the Robot Software Industry, segmented across key areas to provide granular insights into market dynamics. The Software Type segmentation includes Recognition Software, Simulation Software, Predictive Maintenance Software, Data Management and Analysis Software, and Communication Management Software, each with projected market sizes and growth rates. The Robot Type segmentation covers Industrial Robots and Service Robots, detailing their respective market shares and adoption trends. Furthermore, the Deployment segmentation analyzes On-Premise and On-Demand models, assessing their market penetration and future potential. The Enterprise Size segmentation focuses on Small and Medium Enterprises and Large Enterprises, examining their unique adoption patterns and investment strategies. Finally, the End-user Vertical segmentation provides in-depth analysis of Automotive, Retail and E-commerce, Government and Defense, Healthcare, Transportation and Logistics, Manufacturing, IT and Telecommunications, and Other End-user Verticals, highlighting the specific software needs and growth projections within each.

Key Drivers of Robot Software Industry Growth

The Robot Software Industry's growth is propelled by several key factors. Technologically, advancements in Artificial Intelligence, machine learning, and computer vision are enabling more sophisticated and autonomous robotic capabilities. Economically, the drive for increased productivity, reduced operational costs, and a response to labor shortages across various sectors are significant catalysts. Regulatory factors, such as government initiatives promoting automation and Industry 4.0, also play a crucial role in fostering market expansion. The increasing demand for optimized supply chains and the burgeoning e-commerce sector further fuel the need for advanced robotic solutions.

Challenges in the Robot Software Industry Sector

Despite its strong growth trajectory, the Robot Software Industry faces several challenges. Regulatory hurdles related to safety standards, data privacy, and ethical considerations can slow down adoption. Supply chain issues, particularly for specialized components, can impact production timelines and costs. High initial investment costs for complex robotic systems can be a barrier for smaller enterprises. Furthermore, the need for skilled personnel to operate, maintain, and program robots presents a talent gap that requires ongoing attention. Competitive pressures from both established players and new entrants necessitate continuous innovation and cost optimization.

Emerging Opportunities in Robot Software Industry

Emerging opportunities in the Robot Software Industry are abundant, driven by new technological frontiers and evolving market demands. The integration of robots with 5G technology promises enhanced real-time communication and remote operation capabilities. The expansion of collaborative robots (cobots) designed for safe human-robot interaction opens up new applications in diverse environments. The growing demand for robots in healthcare, particularly for surgical assistance and elder care, presents a significant growth avenue. Furthermore, the development of more intuitive, low-code/no-code robot programming platforms is democratizing automation, enabling wider adoption by businesses of all sizes.

Leading Players in the Robot Software Industry Market

- CloudMinds Technology Inc

- ABB Ltd

- Brain Corporation

- Furhat Corporation

- NVIDIA Corporation

- AIBrain Inc

- Liquid Robotics Inc

- Neurala Inc

- Clearpath Robotics

Key Developments in Robot Software Industry Industry

- September 2023: Rockwell announced Acquisition of Clearpath Robotics Demonstrates Growth of Mobile Robots, While Rockwell's acquisition of Clearpath Robotics, including its OTTO Motors Division which develops AMRs as well as fleet management and navigation software, is expected to help expand Rockwell's range of automation solutions aimed at creating more connected and thus productive manufacturing operations.

- May 2023: Clearpath Robotics announced Husky observer an all-terrain, rugged robot with an integrated payload for inspection, Where the new robotic system combines Husky, a popular and versatile robot from Clearpath Robotics with OutdoorNav Autonomy Software; a software platform that enables autonomous navigation for unmanned ground vehicles.

Strategic Outlook for Robot Software Industry Market

The strategic outlook for the Robot Software Industry remains exceptionally positive, driven by persistent innovation and widespread market demand. Future growth catalysts include the continued advancement of AI and machine learning, enabling more sophisticated robot autonomy and intelligence. The increasing adoption of robots in emerging sectors like healthcare and agriculture, alongside their established presence in manufacturing and logistics, will fuel market expansion. The trend towards more collaborative and human-centric robotic systems will unlock new application possibilities. Furthermore, the development of more accessible and scalable cloud-based robotics solutions will democratize access to automation, empowering a broader range of businesses to leverage robotic capabilities and drive significant future market potential.

Robot Software Industry Segmentation

-

1. Software Type

- 1.1. Recognition Software

- 1.2. Simulation Software

- 1.3. Predictive Maintenance Software

- 1.4. Data Management and Analysis Software

- 1.5. Communication Management Software

-

2. Robot Type

- 2.1. Industrial Robots

- 2.2. Service Robots

-

3. Deployment

- 3.1. On-Premise

- 3.2. On-Demand

-

4. Enterprise Size

- 4.1. Small and Medium Enterprises

- 4.2. Large Enterprises

-

5. End-user Vertical

- 5.1. Automotive

- 5.2. Retail and E-commerce

- 5.3. Government and Defense

- 5.4. Healthcare

- 5.5. Transportation and Logistics

- 5.6. Manufacturing

- 5.7. IT and Telecommunications

- 5.8. Other End-user Verticals

Robot Software Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Robot Software Industry Regional Market Share

Geographic Coverage of Robot Software Industry

Robot Software Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 21.62% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Software Type

- 5.1.1. Recognition Software

- 5.1.2. Simulation Software

- 5.1.3. Predictive Maintenance Software

- 5.1.4. Data Management and Analysis Software

- 5.1.5. Communication Management Software

- 5.2. Market Analysis, Insights and Forecast - by Robot Type

- 5.2.1. Industrial Robots

- 5.2.2. Service Robots

- 5.3. Market Analysis, Insights and Forecast - by Deployment

- 5.3.1. On-Premise

- 5.3.2. On-Demand

- 5.4. Market Analysis, Insights and Forecast - by Enterprise Size

- 5.4.1. Small and Medium Enterprises

- 5.4.2. Large Enterprises

- 5.5. Market Analysis, Insights and Forecast - by End-user Vertical

- 5.5.1. Automotive

- 5.5.2. Retail and E-commerce

- 5.5.3. Government and Defense

- 5.5.4. Healthcare

- 5.5.5. Transportation and Logistics

- 5.5.6. Manufacturing

- 5.5.7. IT and Telecommunications

- 5.5.8. Other End-user Verticals

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. North America

- 5.6.2. Europe

- 5.6.3. Asia Pacific

- 5.6.4. Latin America

- 5.6.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Software Type

- 6. Global Robot Software Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Software Type

- 6.1.1. Recognition Software

- 6.1.2. Simulation Software

- 6.1.3. Predictive Maintenance Software

- 6.1.4. Data Management and Analysis Software

- 6.1.5. Communication Management Software

- 6.2. Market Analysis, Insights and Forecast - by Robot Type

- 6.2.1. Industrial Robots

- 6.2.2. Service Robots

- 6.3. Market Analysis, Insights and Forecast - by Deployment

- 6.3.1. On-Premise

- 6.3.2. On-Demand

- 6.4. Market Analysis, Insights and Forecast - by Enterprise Size

- 6.4.1. Small and Medium Enterprises

- 6.4.2. Large Enterprises

- 6.5. Market Analysis, Insights and Forecast - by End-user Vertical

- 6.5.1. Automotive

- 6.5.2. Retail and E-commerce

- 6.5.3. Government and Defense

- 6.5.4. Healthcare

- 6.5.5. Transportation and Logistics

- 6.5.6. Manufacturing

- 6.5.7. IT and Telecommunications

- 6.5.8. Other End-user Verticals

- 6.1. Market Analysis, Insights and Forecast - by Software Type

- 7. North America Robot Software Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Software Type

- 7.1.1. Recognition Software

- 7.1.2. Simulation Software

- 7.1.3. Predictive Maintenance Software

- 7.1.4. Data Management and Analysis Software

- 7.1.5. Communication Management Software

- 7.2. Market Analysis, Insights and Forecast - by Robot Type

- 7.2.1. Industrial Robots

- 7.2.2. Service Robots

- 7.3. Market Analysis, Insights and Forecast - by Deployment

- 7.3.1. On-Premise

- 7.3.2. On-Demand

- 7.4. Market Analysis, Insights and Forecast - by Enterprise Size

- 7.4.1. Small and Medium Enterprises

- 7.4.2. Large Enterprises

- 7.5. Market Analysis, Insights and Forecast - by End-user Vertical

- 7.5.1. Automotive

- 7.5.2. Retail and E-commerce

- 7.5.3. Government and Defense

- 7.5.4. Healthcare

- 7.5.5. Transportation and Logistics

- 7.5.6. Manufacturing

- 7.5.7. IT and Telecommunications

- 7.5.8. Other End-user Verticals

- 7.1. Market Analysis, Insights and Forecast - by Software Type

- 8. Europe Robot Software Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Software Type

- 8.1.1. Recognition Software

- 8.1.2. Simulation Software

- 8.1.3. Predictive Maintenance Software

- 8.1.4. Data Management and Analysis Software

- 8.1.5. Communication Management Software

- 8.2. Market Analysis, Insights and Forecast - by Robot Type

- 8.2.1. Industrial Robots

- 8.2.2. Service Robots

- 8.3. Market Analysis, Insights and Forecast - by Deployment

- 8.3.1. On-Premise

- 8.3.2. On-Demand

- 8.4. Market Analysis, Insights and Forecast - by Enterprise Size

- 8.4.1. Small and Medium Enterprises

- 8.4.2. Large Enterprises

- 8.5. Market Analysis, Insights and Forecast - by End-user Vertical

- 8.5.1. Automotive

- 8.5.2. Retail and E-commerce

- 8.5.3. Government and Defense

- 8.5.4. Healthcare

- 8.5.5. Transportation and Logistics

- 8.5.6. Manufacturing

- 8.5.7. IT and Telecommunications

- 8.5.8. Other End-user Verticals

- 8.1. Market Analysis, Insights and Forecast - by Software Type

- 9. Asia Pacific Robot Software Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Software Type

- 9.1.1. Recognition Software

- 9.1.2. Simulation Software

- 9.1.3. Predictive Maintenance Software

- 9.1.4. Data Management and Analysis Software

- 9.1.5. Communication Management Software

- 9.2. Market Analysis, Insights and Forecast - by Robot Type

- 9.2.1. Industrial Robots

- 9.2.2. Service Robots

- 9.3. Market Analysis, Insights and Forecast - by Deployment

- 9.3.1. On-Premise

- 9.3.2. On-Demand

- 9.4. Market Analysis, Insights and Forecast - by Enterprise Size

- 9.4.1. Small and Medium Enterprises

- 9.4.2. Large Enterprises

- 9.5. Market Analysis, Insights and Forecast - by End-user Vertical

- 9.5.1. Automotive

- 9.5.2. Retail and E-commerce

- 9.5.3. Government and Defense

- 9.5.4. Healthcare

- 9.5.5. Transportation and Logistics

- 9.5.6. Manufacturing

- 9.5.7. IT and Telecommunications

- 9.5.8. Other End-user Verticals

- 9.1. Market Analysis, Insights and Forecast - by Software Type

- 10. Latin America Robot Software Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Software Type

- 10.1.1. Recognition Software

- 10.1.2. Simulation Software

- 10.1.3. Predictive Maintenance Software

- 10.1.4. Data Management and Analysis Software

- 10.1.5. Communication Management Software

- 10.2. Market Analysis, Insights and Forecast - by Robot Type

- 10.2.1. Industrial Robots

- 10.2.2. Service Robots

- 10.3. Market Analysis, Insights and Forecast - by Deployment

- 10.3.1. On-Premise

- 10.3.2. On-Demand

- 10.4. Market Analysis, Insights and Forecast - by Enterprise Size

- 10.4.1. Small and Medium Enterprises

- 10.4.2. Large Enterprises

- 10.5. Market Analysis, Insights and Forecast - by End-user Vertical

- 10.5.1. Automotive

- 10.5.2. Retail and E-commerce

- 10.5.3. Government and Defense

- 10.5.4. Healthcare

- 10.5.5. Transportation and Logistics

- 10.5.6. Manufacturing

- 10.5.7. IT and Telecommunications

- 10.5.8. Other End-user Verticals

- 10.1. Market Analysis, Insights and Forecast - by Software Type

- 11. Middle East and Africa Robot Software Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Software Type

- 11.1.1. Recognition Software

- 11.1.2. Simulation Software

- 11.1.3. Predictive Maintenance Software

- 11.1.4. Data Management and Analysis Software

- 11.1.5. Communication Management Software

- 11.2. Market Analysis, Insights and Forecast - by Robot Type

- 11.2.1. Industrial Robots

- 11.2.2. Service Robots

- 11.3. Market Analysis, Insights and Forecast - by Deployment

- 11.3.1. On-Premise

- 11.3.2. On-Demand

- 11.4. Market Analysis, Insights and Forecast - by Enterprise Size

- 11.4.1. Small and Medium Enterprises

- 11.4.2. Large Enterprises

- 11.5. Market Analysis, Insights and Forecast - by End-user Vertical

- 11.5.1. Automotive

- 11.5.2. Retail and E-commerce

- 11.5.3. Government and Defense

- 11.5.4. Healthcare

- 11.5.5. Transportation and Logistics

- 11.5.6. Manufacturing

- 11.5.7. IT and Telecommunications

- 11.5.8. Other End-user Verticals

- 11.1. Market Analysis, Insights and Forecast - by Software Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 CloudMinds Technology Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 ABB Ltd

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Brain Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Furhat Corporation

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 NVIDIA Corporation

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 AIBrain Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Liquid Robotics Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Neurala Inc *List Not Exhaustive

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Clearpath Robotics

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.1 CloudMinds Technology Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Robot Software Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Robot Software Industry Revenue (Million), by Software Type 2025 & 2033

- Figure 3: North America Robot Software Industry Revenue Share (%), by Software Type 2025 & 2033

- Figure 4: North America Robot Software Industry Revenue (Million), by Robot Type 2025 & 2033

- Figure 5: North America Robot Software Industry Revenue Share (%), by Robot Type 2025 & 2033

- Figure 6: North America Robot Software Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 7: North America Robot Software Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 8: North America Robot Software Industry Revenue (Million), by Enterprise Size 2025 & 2033

- Figure 9: North America Robot Software Industry Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 10: North America Robot Software Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 11: North America Robot Software Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 12: North America Robot Software Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: North America Robot Software Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Robot Software Industry Revenue (Million), by Software Type 2025 & 2033

- Figure 15: Europe Robot Software Industry Revenue Share (%), by Software Type 2025 & 2033

- Figure 16: Europe Robot Software Industry Revenue (Million), by Robot Type 2025 & 2033

- Figure 17: Europe Robot Software Industry Revenue Share (%), by Robot Type 2025 & 2033

- Figure 18: Europe Robot Software Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 19: Europe Robot Software Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 20: Europe Robot Software Industry Revenue (Million), by Enterprise Size 2025 & 2033

- Figure 21: Europe Robot Software Industry Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 22: Europe Robot Software Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 23: Europe Robot Software Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 24: Europe Robot Software Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Europe Robot Software Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Robot Software Industry Revenue (Million), by Software Type 2025 & 2033

- Figure 27: Asia Pacific Robot Software Industry Revenue Share (%), by Software Type 2025 & 2033

- Figure 28: Asia Pacific Robot Software Industry Revenue (Million), by Robot Type 2025 & 2033

- Figure 29: Asia Pacific Robot Software Industry Revenue Share (%), by Robot Type 2025 & 2033

- Figure 30: Asia Pacific Robot Software Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 31: Asia Pacific Robot Software Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 32: Asia Pacific Robot Software Industry Revenue (Million), by Enterprise Size 2025 & 2033

- Figure 33: Asia Pacific Robot Software Industry Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 34: Asia Pacific Robot Software Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 35: Asia Pacific Robot Software Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 36: Asia Pacific Robot Software Industry Revenue (Million), by Country 2025 & 2033

- Figure 37: Asia Pacific Robot Software Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Latin America Robot Software Industry Revenue (Million), by Software Type 2025 & 2033

- Figure 39: Latin America Robot Software Industry Revenue Share (%), by Software Type 2025 & 2033

- Figure 40: Latin America Robot Software Industry Revenue (Million), by Robot Type 2025 & 2033

- Figure 41: Latin America Robot Software Industry Revenue Share (%), by Robot Type 2025 & 2033

- Figure 42: Latin America Robot Software Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 43: Latin America Robot Software Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 44: Latin America Robot Software Industry Revenue (Million), by Enterprise Size 2025 & 2033

- Figure 45: Latin America Robot Software Industry Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 46: Latin America Robot Software Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 47: Latin America Robot Software Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 48: Latin America Robot Software Industry Revenue (Million), by Country 2025 & 2033

- Figure 49: Latin America Robot Software Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East and Africa Robot Software Industry Revenue (Million), by Software Type 2025 & 2033

- Figure 51: Middle East and Africa Robot Software Industry Revenue Share (%), by Software Type 2025 & 2033

- Figure 52: Middle East and Africa Robot Software Industry Revenue (Million), by Robot Type 2025 & 2033

- Figure 53: Middle East and Africa Robot Software Industry Revenue Share (%), by Robot Type 2025 & 2033

- Figure 54: Middle East and Africa Robot Software Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 55: Middle East and Africa Robot Software Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 56: Middle East and Africa Robot Software Industry Revenue (Million), by Enterprise Size 2025 & 2033

- Figure 57: Middle East and Africa Robot Software Industry Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 58: Middle East and Africa Robot Software Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 59: Middle East and Africa Robot Software Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 60: Middle East and Africa Robot Software Industry Revenue (Million), by Country 2025 & 2033

- Figure 61: Middle East and Africa Robot Software Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Robot Software Industry Revenue Million Forecast, by Software Type 2020 & 2033

- Table 2: Global Robot Software Industry Revenue Million Forecast, by Robot Type 2020 & 2033

- Table 3: Global Robot Software Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 4: Global Robot Software Industry Revenue Million Forecast, by Enterprise Size 2020 & 2033

- Table 5: Global Robot Software Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 6: Global Robot Software Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 7: Global Robot Software Industry Revenue Million Forecast, by Software Type 2020 & 2033

- Table 8: Global Robot Software Industry Revenue Million Forecast, by Robot Type 2020 & 2033

- Table 9: Global Robot Software Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 10: Global Robot Software Industry Revenue Million Forecast, by Enterprise Size 2020 & 2033

- Table 11: Global Robot Software Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 12: Global Robot Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global Robot Software Industry Revenue Million Forecast, by Software Type 2020 & 2033

- Table 14: Global Robot Software Industry Revenue Million Forecast, by Robot Type 2020 & 2033

- Table 15: Global Robot Software Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 16: Global Robot Software Industry Revenue Million Forecast, by Enterprise Size 2020 & 2033

- Table 17: Global Robot Software Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 18: Global Robot Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 19: Global Robot Software Industry Revenue Million Forecast, by Software Type 2020 & 2033

- Table 20: Global Robot Software Industry Revenue Million Forecast, by Robot Type 2020 & 2033

- Table 21: Global Robot Software Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 22: Global Robot Software Industry Revenue Million Forecast, by Enterprise Size 2020 & 2033

- Table 23: Global Robot Software Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 24: Global Robot Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 25: Global Robot Software Industry Revenue Million Forecast, by Software Type 2020 & 2033

- Table 26: Global Robot Software Industry Revenue Million Forecast, by Robot Type 2020 & 2033

- Table 27: Global Robot Software Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 28: Global Robot Software Industry Revenue Million Forecast, by Enterprise Size 2020 & 2033

- Table 29: Global Robot Software Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 30: Global Robot Software Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 31: Global Robot Software Industry Revenue Million Forecast, by Software Type 2020 & 2033

- Table 32: Global Robot Software Industry Revenue Million Forecast, by Robot Type 2020 & 2033

- Table 33: Global Robot Software Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 34: Global Robot Software Industry Revenue Million Forecast, by Enterprise Size 2020 & 2033

- Table 35: Global Robot Software Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 36: Global Robot Software Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Robot Software Industry?

The projected CAGR is approximately 21.62%.

2. Which companies are prominent players in the Robot Software Industry?

Key companies in the market include CloudMinds Technology Inc, ABB Ltd, Brain Corporation, Furhat Corporation, NVIDIA Corporation, AIBrain Inc, Liquid Robotics Inc, Neurala Inc *List Not Exhaustive, Clearpath Robotics.

3. What are the main segments of the Robot Software Industry?

The market segments include Software Type, Robot Type, Deployment, Enterprise Size, End-user Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 19.92 Million as of 2022.

5. What are some drivers contributing to market growth?

Rise in need for automation and safety in organizations; Rapid adoption of robot software by SMEs to reduce labor and energy costs.

6. What are the notable trends driving market growth?

Industrial Robots to Have the Majority Application.

7. Are there any restraints impacting market growth?

Vulnerabilities Associated with Cloud Technologies.

8. Can you provide examples of recent developments in the market?

September 2023 - Rockwell has announced Acquisition of Clearpath Robotics Demonstrates Growth of Mobile Robots, While Rockwell's acquisition of Clearpath Robotics, including its OTTO Motors Division which develops AMRs as well as fleet management and navigation software, is expected to help expand Rockwell's range of automation solutions aimed at creating more connected and thus productive manufacturing operations.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Robot Software Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Robot Software Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Robot Software Industry?

To stay informed about further developments, trends, and reports in the Robot Software Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence