Key Insights

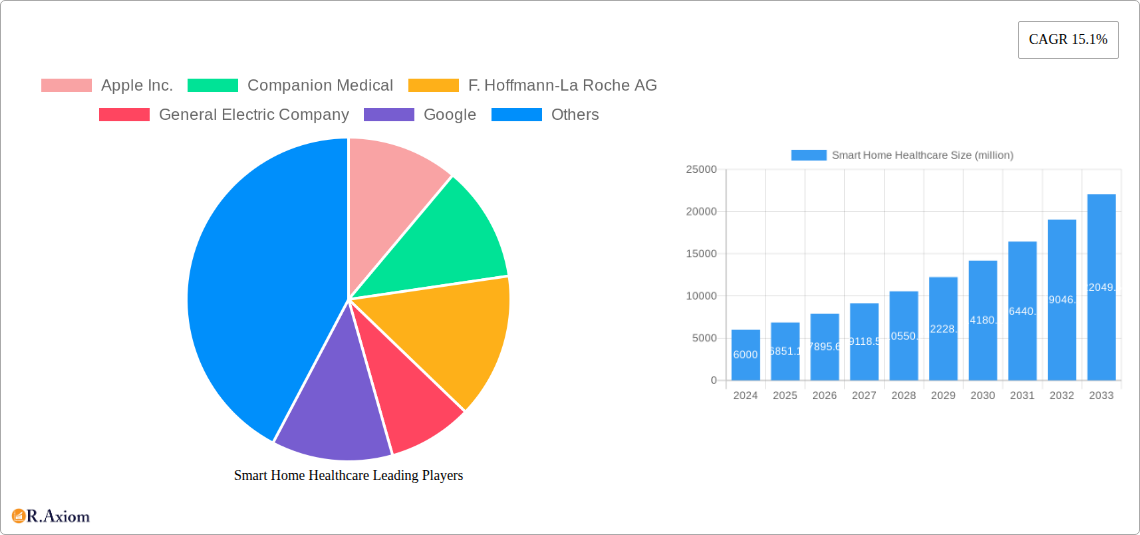

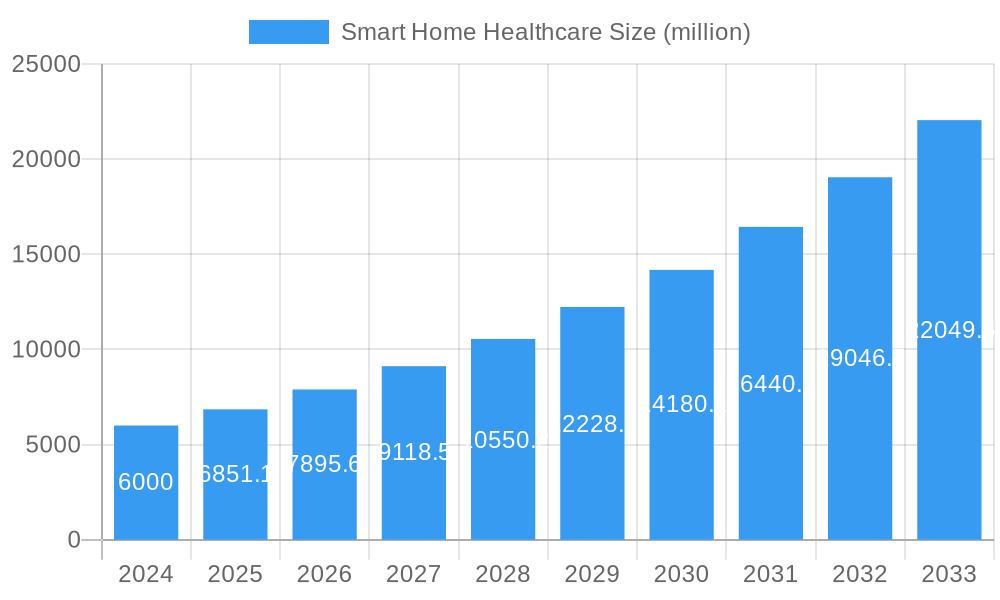

The global Smart Home Healthcare market is poised for remarkable expansion, projected to reach a substantial market size of $6,851.1 million by 2025, and expected to surge at a compelling Compound Annual Growth Rate (CAGR) of 15.1% through 2033. This robust growth is propelled by a confluence of critical factors, primarily the escalating need for continuous health monitoring among aging populations, a growing desire for independent living facilitated by remote care solutions, and the increasing adoption of advanced IoT devices within domestic environments. The market's dynamism is further fueled by significant investments in research and development by leading technology and healthcare companies, leading to innovative solutions that enhance patient outcomes and streamline healthcare delivery. Key applications like Fall Prevention and Detection, Health Status Monitoring, and Nutrition and Diet Monitoring are at the forefront of this transformation, addressing prevalent health concerns and providing proactive care.

Smart Home Healthcare Market Size (In Billion)

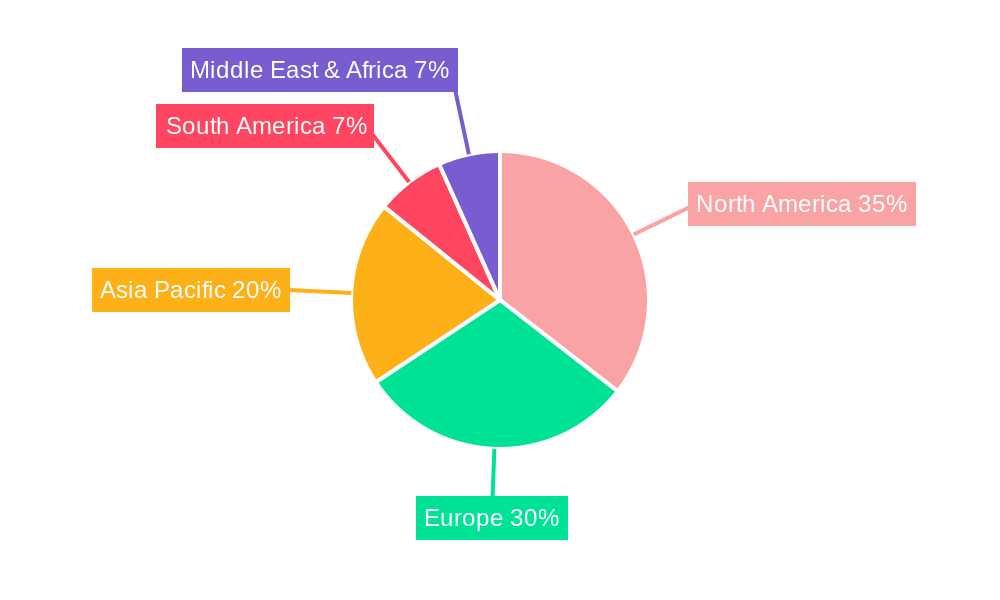

The competitive landscape is characterized by the presence of major technology giants like Apple Inc., Google, and Samsung Electronics, alongside established healthcare players such as Medtronic and F. Hoffmann-La Roche AG, all vying to capture market share. This intense competition is driving rapid technological advancements and fostering a market rich with diverse product offerings, from wired to wireless solutions. The "Others" segment, encompassing a range of emerging smart home healthcare applications, is also expected to witness significant growth as new use cases are identified and developed. Geographically, North America and Europe are anticipated to lead the market due to early adoption of technology, supportive government initiatives, and high healthcare expenditure. However, the Asia Pacific region, driven by a large and aging population, burgeoning healthcare infrastructure, and increasing disposable incomes, presents the most significant growth potential in the coming years, indicating a substantial shift in global market dynamics.

Smart Home Healthcare Company Market Share

The smart home healthcare market exhibits a moderate to high concentration, driven by significant investment and rapid technological advancement. Key players like Apple Inc., Google, Samsung Electronics Co. Ltd, and Medtronic are heavily investing in research and development, contributing to innovation in areas such as remote patient monitoring and telehealth solutions. Innovation drivers include the increasing prevalence of chronic diseases, the growing elderly population, and the demand for convenient, personalized healthcare services. Regulatory frameworks, while evolving, are increasingly supportive of digital health solutions, particularly those that improve patient outcomes and reduce healthcare costs. Product substitutes, such as traditional in-home care services, are facing competition from more scalable and cost-effective smart home healthcare solutions. End-user trends show a strong preference for user-friendly interfaces, data security, and seamless integration with existing smart home ecosystems. Merger and acquisition (M&A) activities are prevalent, with significant deal values observed as larger tech companies and established healthcare providers acquire innovative startups. For instance, M&A deal values in the last three years have reached approximately $500 million to $1 billion annually. This consolidation aims to broaden product portfolios, expand market reach, and leverage synergistic technologies. The market share of leading players is estimated to range from 10% to 25% for the top five companies.

Smart Home Healthcare Industry Trends & Insights

The smart home healthcare industry is experiencing robust growth, fueled by a confluence of technological advancements, shifting consumer demographics, and evolving healthcare paradigms. The market is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 15-20% over the forecast period of 2025-2033. This impressive growth is underpinned by a significant increase in market penetration, which is expected to rise from 20% in the base year of 2025 to over 45% by 2033. Technological disruptions are at the forefront of this expansion, with the integration of Artificial Intelligence (AI) and Machine Learning (ML) enabling more sophisticated health status monitoring and predictive analytics. Wearable devices, smart sensors, and connected medical devices are becoming indispensable tools for continuous data collection, providing real-time insights into patient well-being. Consumer preferences are increasingly leaning towards proactive and preventative healthcare, driving demand for solutions that empower individuals to manage their health from the comfort of their homes. The aging global population, coupled with a desire for independent living, further accentuates the need for smart home healthcare technologies that can provide safety, support, and remote assistance. Competitive dynamics are intense, with established technology giants like Apple Inc., Google, and Samsung Electronics Co. Ltd vying for market dominance alongside specialized healthcare technology companies such as Medtronic, Companion Medical, and Medical Guardian, LLC. The industry is also seeing strategic collaborations and partnerships aimed at developing integrated ecosystems that offer a comprehensive suite of smart home healthcare services. The increasing adoption of telehealth services, accelerated by recent global events, has further normalized remote healthcare delivery, paving the way for wider acceptance and implementation of smart home healthcare solutions. Furthermore, the growing awareness of the cost-effectiveness of home-based care compared to traditional hospital settings is a significant catalyst for market expansion. The ability of these technologies to reduce hospital readmissions and manage chronic conditions more effectively at home is a key selling point for both healthcare providers and consumers.

Dominant Markets & Segments in Smart Home Healthcare

The smart home healthcare market is dominated by the Health Status Monitoring application segment, driven by its broad utility across various patient demographics and its ability to provide continuous, actionable health insights. Within this segment, the increasing prevalence of chronic conditions such as cardiovascular diseases, diabetes, and respiratory illnesses necessitates constant monitoring, making it a high-demand area. The Fall Prevention and Detection segment also holds significant market share, particularly due to the aging global population and the inherent risks associated with falls among the elderly. Wireless type devices are overwhelmingly dominant across all segments, offering greater flexibility, ease of installation, and user convenience compared to their wired counterparts. The leading geographical market is North America, primarily driven by the United States, due to its advanced healthcare infrastructure, high disposable income, strong government support for digital health initiatives, and a mature market for smart home technologies.

Health Status Monitoring Dominance:

- Key Drivers: Rising incidence of chronic diseases, increasing adoption of wearable health trackers, demand for remote patient management, and the growing elderly population seeking to maintain independence.

- Detailed Analysis: This segment benefits from continuous innovation in biosensors and AI-powered analytics, enabling the detection of subtle physiological changes that could indicate an impending health issue. The integration of smart devices like blood pressure monitors, glucose meters, and ECG sensors directly into the home environment provides healthcare providers with a comprehensive, real-time view of a patient's health, leading to more timely interventions and improved treatment outcomes. The market size for this segment alone is projected to exceed $50 million by 2028.

Fall Prevention and Detection Dominance:

- Key Drivers: Aging population, rising healthcare costs associated with fall-related injuries, advancements in sensor technology for motion detection and gait analysis, and the desire for independent living.

- Detailed Analysis: This segment leverages technologies ranging from passive infrared sensors and accelerometers in wearable devices to sophisticated AI-powered video analysis. The ability to quickly detect a fall and automatically alert caregivers or emergency services is a critical factor driving adoption. The development of unobtrusive and aesthetically pleasing devices that blend into the home environment further enhances user acceptance.

Wireless Type Dominance:

- Key Drivers: Ease of installation and use, mobility and flexibility for users, integration with existing smart home ecosystems, and reduced infrastructure costs.

- Detailed Analysis: The ubiquity of Wi-Fi and Bluetooth technologies has made wireless connectivity the standard for smart home healthcare devices. This allows for seamless data transmission between devices and central hubs or cloud platforms without the need for complex wiring, making it ideal for both new installations and retrofitting existing homes.

Smart Home Healthcare Product Developments

Product innovation in smart home healthcare is characterized by the convergence of advanced sensor technology, AI-driven analytics, and user-centric design. Companies are focusing on developing integrated solutions that offer proactive health management, early disease detection, and personalized care plans. Key trends include the miniaturization of wearable sensors for continuous physiological monitoring, the development of non-invasive diagnostic tools, and smart home devices capable of environmental monitoring for health-related factors. Competitive advantages are being built on data accuracy, ease of integration with existing platforms like Google Home and Apple Health, and enhanced data security features.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the global smart home healthcare market, segmented by Application and Type. The Application segments include Fall Prevention and Detection, Health Status Monitoring, Nutrition and Diet Monitoring, Memory Aids, and Others. The Type segments comprise Wired and Wireless devices.

- Fall Prevention and Detection: This segment is expected to grow at a CAGR of 18% from 2025-2033, with a projected market size of $40 million by 2028. It focuses on technologies that identify and alert for falls, crucial for the elderly and those with mobility issues.

- Health Status Monitoring: Anticipated to be the largest segment, with a CAGR of 20% and a market size of $60 million by 2028. It encompasses continuous tracking of vital signs and health metrics, supporting chronic disease management and remote patient care.

- Nutrition and Diet Monitoring: This segment, projected to grow at 16% CAGR, will focus on smart devices that assist in tracking food intake, caloric consumption, and dietary adherence, with a market size expected around $25 million by 2028.

- Memory Aids: This niche segment, with an 11% CAGR, will include smart devices designed to assist individuals with cognitive impairments, such as medication reminders and appointment alerts, estimated at $15 million by 2028.

- Others: This category will capture emerging applications and innovative solutions not fitting into the above, with an estimated market size of $10 million by 2028.

- Wired: While declining in market share due to convenience, wired systems will still hold relevance in specialized medical facilities and applications requiring high reliability, with a projected market size of $20 million by 2028.

- Wireless: This segment is expected to dominate the market, with a CAGR of 22% and a market size of $150 million by 2028, driven by its flexibility and widespread adoption in residential settings.

Key Drivers of Smart Home Healthcare Growth

The smart home healthcare market is propelled by several potent growth drivers. Technologically, advancements in AI, IoT, and wearable sensors enable more sophisticated remote monitoring and personalized interventions. Economically, the rising healthcare expenditures and the demand for cost-effective solutions are pushing towards home-based care. Regulatory bodies are increasingly fostering an environment conducive to digital health innovation, with supportive policies for telehealth and data privacy. The growing elderly population and the increasing prevalence of chronic diseases globally create a substantial and expanding user base. Furthermore, the consumer shift towards proactive health management and the desire for independent living are significant behavioral drivers fueling market expansion. The convergence of these factors creates a fertile ground for the growth of smart home healthcare solutions.

Challenges in the Smart Home Healthcare Sector

Despite its promising growth, the smart home healthcare sector faces several challenges. Regulatory hurdles, particularly concerning data privacy (e.g., HIPAA compliance) and device certification, can slow down market entry and product development. Interoperability issues between different devices and platforms remain a significant concern, hindering the creation of seamless integrated systems. Cybersecurity threats to sensitive health data are a constant apprehension for both providers and consumers. The high initial cost of some advanced smart home healthcare systems can be a barrier to adoption for a segment of the population. Supply chain disruptions, as seen in recent global events, can impact the availability and pricing of essential components. Finally, the need for extensive consumer education and trust-building is crucial to overcome initial resistance to adopting new healthcare technologies in the home.

Emerging Opportunities in Smart Home Healthcare

Emerging opportunities in smart home healthcare are vast and diverse. The integration of AI and ML for predictive health analytics offers a significant avenue for early disease detection and personalized treatment plans. The expansion of telehealth services and remote patient monitoring creates a continuous demand for connected devices and platforms. The burgeoning market for elder care solutions, driven by an aging global population, presents substantial growth potential. Furthermore, opportunities exist in developing smart home solutions tailored for specific chronic conditions, such as diabetes management or respiratory care. The increasing focus on preventative healthcare and wellness also opens doors for devices that promote healthy lifestyles. The development of more affordable and accessible smart home healthcare solutions can unlock new market segments and drive wider adoption.

Leading Players in the Smart Home Healthcare Market

- Apple Inc.

- Companion Medical

- F. Hoffmann-La Roche AG

- General Electric Company

- Health Care Originals

- Hocoma

- Medical Guardian, LLC

- Medtronic

- Proteus Digital Health

- Samsung Electronics Co. Ltd

- VitalConnect

- Zanthion

Key Developments in Smart Home Healthcare Industry

- 2023/08: Apple releases watchOS 10 with enhanced mental health and vision features, further integrating health monitoring into its ecosystem.

- 2023/07: Google expands its AI capabilities in healthcare with new diagnostic tools, potentially impacting remote health analysis.

- 2023/06: Medtronic announces advancements in its remote patient monitoring solutions, focusing on cardiovascular disease management.

- 2022/11: Samsung Electronics launches new smart home appliances with integrated health monitoring features.

- 2022/09: Companion Medical receives FDA clearance for an improved insulin pen system, enhancing diabetes management at home.

- 2022/04: Medical Guardian, LLC introduces new fall detection technologies with enhanced GPS accuracy and longer battery life.

- 2021/10: VitalConnect showcases its latest innovations in wearable biosensors for continuous patient monitoring in home settings.

- 2021/05: F. Hoffmann-La Roche AG partners with a smart home technology provider to develop integrated health monitoring solutions.

- 2020/09: Health Care Originals receives significant funding to scale its remote patient monitoring platform.

Strategic Outlook for Smart Home Healthcare Market

The strategic outlook for the smart home healthcare market is overwhelmingly positive, driven by sustained technological innovation and increasing market acceptance. Key growth catalysts include the continuous evolution of AI and IoT, the growing demand for telehealth and remote care, and the expanding needs of an aging global population. Strategic investments in research and development, coupled with potential mergers and acquisitions, will continue to shape the competitive landscape. Companies that focus on developing user-friendly, secure, and interoperable solutions that address specific health needs are poised for significant success. The market is expected to witness a deeper integration of smart home healthcare into mainstream living, transforming how individuals manage their health and well-being from the comfort of their homes.

Smart Home Healthcare Segmentation

-

1. Application

- 1.1. Fall Prevention and Detection

- 1.2. Health Status Monitoring

- 1.3. Nutrition and Diet Monitoring

- 1.4. Memory Aids

- 1.5. Others

-

2. Types

- 2.1. Wired

- 2.2. Wireless

Smart Home Healthcare Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Smart Home Healthcare Regional Market Share

Geographic Coverage of Smart Home Healthcare

Smart Home Healthcare REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 29.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Fall Prevention and Detection

- 5.1.2. Health Status Monitoring

- 5.1.3. Nutrition and Diet Monitoring

- 5.1.4. Memory Aids

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Wired

- 5.2.2. Wireless

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Smart Home Healthcare Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Fall Prevention and Detection

- 6.1.2. Health Status Monitoring

- 6.1.3. Nutrition and Diet Monitoring

- 6.1.4. Memory Aids

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Wired

- 6.2.2. Wireless

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Smart Home Healthcare Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Fall Prevention and Detection

- 7.1.2. Health Status Monitoring

- 7.1.3. Nutrition and Diet Monitoring

- 7.1.4. Memory Aids

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Wired

- 7.2.2. Wireless

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Smart Home Healthcare Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Fall Prevention and Detection

- 8.1.2. Health Status Monitoring

- 8.1.3. Nutrition and Diet Monitoring

- 8.1.4. Memory Aids

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Wired

- 8.2.2. Wireless

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Smart Home Healthcare Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Fall Prevention and Detection

- 9.1.2. Health Status Monitoring

- 9.1.3. Nutrition and Diet Monitoring

- 9.1.4. Memory Aids

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Wired

- 9.2.2. Wireless

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Smart Home Healthcare Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Fall Prevention and Detection

- 10.1.2. Health Status Monitoring

- 10.1.3. Nutrition and Diet Monitoring

- 10.1.4. Memory Aids

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Wired

- 10.2.2. Wireless

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Smart Home Healthcare Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Fall Prevention and Detection

- 11.1.2. Health Status Monitoring

- 11.1.3. Nutrition and Diet Monitoring

- 11.1.4. Memory Aids

- 11.1.5. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Wired

- 11.2.2. Wireless

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Apple Inc.

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Companion Medical

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 F. Hoffmann-La Roche AG

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 General Electric Company

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Google

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Health Care Originals

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Hocoma

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Medical Guardian

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 LLC

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Medtronic

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Proteus Digital Health

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Samsung Electronics Co. Ltd

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 VitalConnect

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Zanthion

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 Apple Inc.

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Smart Home Healthcare Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Smart Home Healthcare Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Smart Home Healthcare Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Smart Home Healthcare Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Smart Home Healthcare Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Smart Home Healthcare Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Smart Home Healthcare Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Smart Home Healthcare Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Smart Home Healthcare Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Smart Home Healthcare Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Smart Home Healthcare Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Smart Home Healthcare Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Smart Home Healthcare Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Smart Home Healthcare Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Smart Home Healthcare Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Smart Home Healthcare Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Smart Home Healthcare Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Smart Home Healthcare Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Smart Home Healthcare Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Smart Home Healthcare Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Smart Home Healthcare Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Smart Home Healthcare Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Smart Home Healthcare Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Smart Home Healthcare Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Smart Home Healthcare Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Smart Home Healthcare Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Smart Home Healthcare Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Smart Home Healthcare Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Smart Home Healthcare Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Smart Home Healthcare Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Smart Home Healthcare Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Smart Home Healthcare Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Smart Home Healthcare Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Smart Home Healthcare Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Smart Home Healthcare Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Smart Home Healthcare Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Smart Home Healthcare Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Smart Home Healthcare Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Smart Home Healthcare Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Smart Home Healthcare Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Smart Home Healthcare Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Smart Home Healthcare Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Smart Home Healthcare Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Smart Home Healthcare Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Smart Home Healthcare Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Smart Home Healthcare Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Smart Home Healthcare Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Smart Home Healthcare Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Smart Home Healthcare Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Smart Home Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Smart Home Healthcare?

The projected CAGR is approximately 29.3%.

2. Which companies are prominent players in the Smart Home Healthcare?

Key companies in the market include Apple Inc., Companion Medical, F. Hoffmann-La Roche AG, General Electric Company, Google, Health Care Originals, Hocoma, Medical Guardian, LLC, Medtronic, Proteus Digital Health, Samsung Electronics Co. Ltd, VitalConnect, Zanthion.

3. What are the main segments of the Smart Home Healthcare?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Smart Home Healthcare," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Smart Home Healthcare report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Smart Home Healthcare?

To stay informed about further developments, trends, and reports in the Smart Home Healthcare, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence