Key Insights

The space lander and rover industry is experiencing robust growth, driven by increasing government and private investments in space exploration. A Compound Annual Growth Rate (CAGR) exceeding 9% from 2019 to 2033 indicates a significant expansion of this market. This surge is fueled by ambitious lunar missions, the pursuit of Martian colonization, and the burgeoning interest in asteroid mining. Key market drivers include the technological advancements in robotics, autonomous navigation, and power systems that enable more sophisticated and durable landers and rovers. Furthermore, the growing need for in-situ resource utilization (ISRU) and scientific research on celestial bodies is significantly boosting market demand. While regulatory hurdles and the high cost of space missions pose certain challenges, the long-term potential for scientific discovery, resource extraction, and human expansion beyond Earth is propelling significant investment. The market is segmented by target celestial body – lunar, Martian, and asteroid exploration – reflecting the diverse applications of these technologies. Major players like SpaceX, Blue Origin, Lockheed Martin, and various national space agencies are leading the charge in technological innovation and mission development, driving further market expansion.

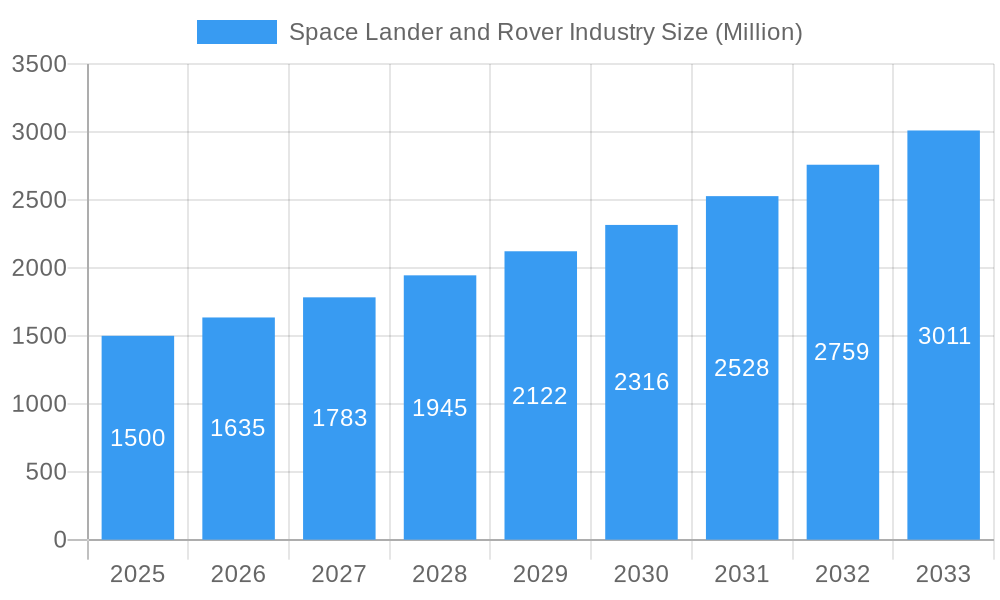

Space Lander and Rover Industry Market Size (In Billion)

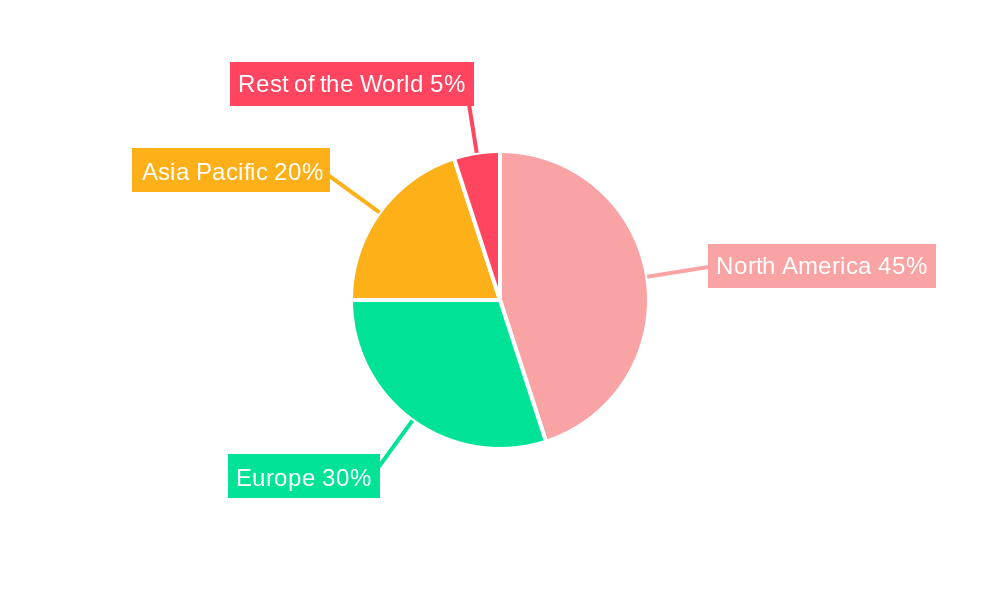

The segmentation by target celestial body reveals interesting dynamics. Lunar surface exploration currently dominates the market due to increased accessibility and the focus on establishing a lunar base. However, Mars surface exploration is projected to experience the fastest growth rate due to long-term ambitions for human settlement and scientific research on the planet. Asteroid surface exploration remains a niche segment but holds enormous future potential, driven by the possibilities of resource extraction and space-based manufacturing. North America and Europe currently hold the largest market shares, driven by strong government funding and private sector participation. However, the Asia-Pacific region is emerging as a significant player with growing investment from countries like India, Japan, and China. This competitive landscape and geographically diverse investment underscore the industry's rapid evolution and its potential for continued expansion throughout the forecast period (2025-2033).

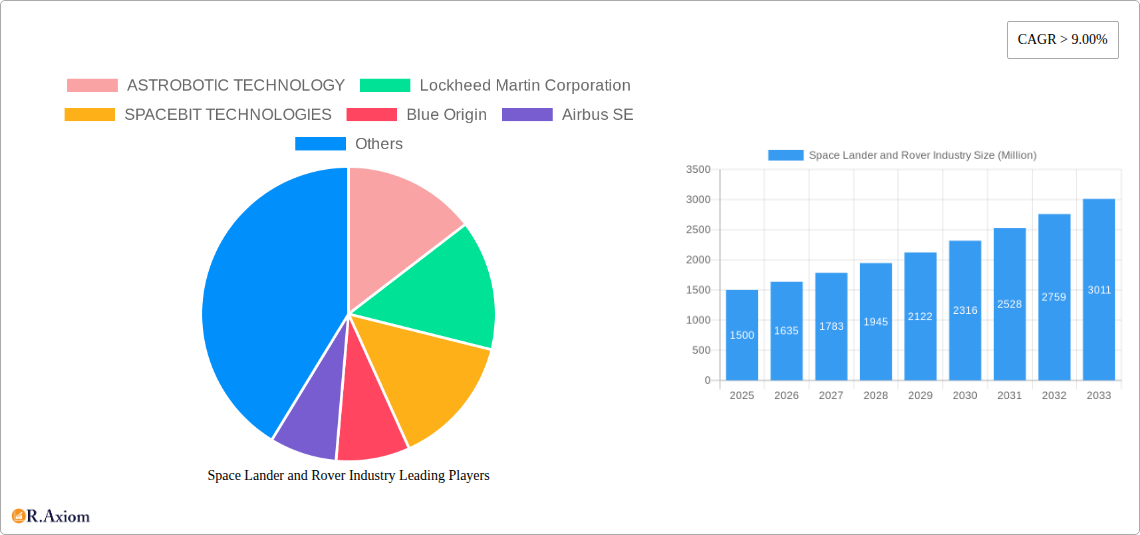

Space Lander and Rover Industry Company Market Share

Space Lander and Rover Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Space Lander and Rover industry, encompassing market size, growth projections, competitive landscape, technological advancements, and key industry trends from 2019 to 2033. The report utilizes data from the historical period (2019-2024), base year (2025), and estimated year (2025) to forecast market dynamics from 2025 to 2033. The analysis covers key segments like Lunar Surface Exploration, Mars Surface Exploration, and Asteroids Surface Exploration, identifying dominant players and emerging opportunities within each. This report is invaluable for industry stakeholders, investors, and researchers seeking a comprehensive understanding of this rapidly evolving sector.

Space Lander and Rover Industry Market Concentration & Innovation

The Space Lander and Rover industry exhibits a notable level of market concentration, featuring a handful of major aerospace corporations alongside a growing number of agile, specialized firms. As of 2025, key industry leaders such as Lockheed Martin Corporation and Northrop Grumman Corporation command substantial market shares, estimated at approximately xx% and xx% respectively. Their dominance is largely attributed to a long-standing history of successful government contracts and substantial investments in research and development. However, the landscape is rapidly evolving with the emergence of pioneering space technology companies, including ASTROBOTIC TECHNOLOGY and SPACEBIT TECHNOLOGIES, which are actively challenging the established players through novel approaches and disruptive technologies.

Innovation within the industry is a multifaceted endeavor, propelled by significant breakthroughs in fields such as advanced robotics, artificial intelligence, next-generation propulsion systems, and cutting-edge materials science. The trajectory of industry development is also profoundly shaped by evolving regulatory environments, particularly concerning space debris mitigation protocols and international space law. While direct product substitutes are scarce due to the highly specialized nature of space landers and rovers, the increasing affordability and accessibility of launch services are paving the way for new market participants and intensifying competitive pressures. The trend of mergers and acquisitions (M&A) is also on an upward trajectory, with recent deal values frequently reaching hundreds of millions of US dollars. A prime example of this collaborative spirit is the 2021 partnership between Lockheed Martin and General Motors, focused on developing advanced lunar rovers. Further analysis of M&A activities over the past five years indicates an average deal valuation of roughly USD xx Million, signaling a sustained period of industry consolidation that is expected to further refine the competitive dynamics.

- Key Performance Indicators:

- Combined Market Share of Lockheed Martin & Northrop Grumman: xx% (2025 Estimate)

- Average M&A Deal Value (2020-2024): USD xx Million

- Total Number of M&A Deals (2020-2024): xx

Space Lander and Rover Industry Industry Trends & Insights

The Space Lander and Rover industry is currently experiencing a period of dynamic and robust expansion, largely fueled by escalating governmental and private sector investments directed towards space exploration initiatives. Projections indicate a compound annual growth rate (CAGR) of xx% for the period spanning 2025 to 2033, with the market anticipated to reach a valuation of USD xx Million by 2033. This impressive growth trajectory is primarily underpinned by several critical factors: the resurgent global emphasis on lunar exploration, exemplified by programs like Artemis; sustained interest in Mars exploration missions; and the burgeoning presence of commercial space ventures. Technological advancements are acting as significant catalysts, with innovations in autonomous navigation, efficient power systems, and in-situ resource utilization (ISRU) capabilities dramatically enhancing the performance and cost-effectiveness of space landers and rovers.

In this sector, "consumer preferences" are largely dictated by the stringent requirements of governmental space agencies and forward-thinking private companies. There is a discernible and growing demand for more resilient, versatile, and economically viable systems capable of withstanding the extreme conditions of extraterrestrial environments. The competitive landscape is characterized by a dual nature of both strategic collaboration and intense competition. Leading organizations are increasingly forming partnerships to share the inherent risks and leverage complementary resources, while simultaneously competing vigorously for lucrative government contracts and significant private sector funding. The market penetration of commercially developed space landers and rovers is steadily increasing, with projections suggesting a penetration rate of xx% by 2033. The amplified involvement of private enterprises is a key driver of innovation and cost reduction, thereby accelerating overall market growth.

Dominant Markets & Segments in Space Lander and Rover Industry

The prevailing market segment within the space lander and rover industry is presently centered on Lunar Surface Exploration. This dominance is predominantly a consequence of the renewed global interest in lunar endeavors, significantly bolstered by initiatives such as NASA's Artemis program and the increasing participation of private sector entities. Currently, the United States holds a substantial market share in this segment, a position reinforced by its formidable space program and extensive operational experience.

- Principal Catalysts for Lunar Surface Exploration Leadership:

- Substantial government funding and supportive policy frameworks (e.g., the Artemis program).

- Significant advancements in lunar lander and rover technologies.

- Reliable and accessible launch capabilities.

- Growing commercial interest in lunar resource extraction.

While the Mars Surface Exploration and Asteroids Surface Exploration segments currently represent smaller portions of the market, they are strongly positioned for substantial expansion in the coming decade. Mars exploration is primarily driven by the compelling scientific objective of searching for evidence of past or present life, alongside the long-term vision of enabling future human habitation. Asteroid mining, though still in its nascent developmental stages, holds immense promise for the extraction of valuable resources, thereby providing a potent impetus for future growth. Ongoing investments from both governmental bodies and private enterprises in the development of requisite technologies are actively fostering growth across these emerging segments.

Space Lander and Rover Industry Product Developments

Recent years have witnessed significant advancements in space lander and rover technology, including the development of more autonomous systems, improved power sources, advanced sensing capabilities, and enhanced mobility. These innovations aim to increase the operational efficiency and scientific return of space exploration missions. The increased focus on ISRU (in-situ resource utilization) technology is expected to play a crucial role in reducing reliance on Earth-based resources and enabling longer, more sustainable missions. The market fit of these innovations is directly related to the increasing demand for cost-effective and reliable solutions for space exploration.

Report Scope & Segmentation Analysis

This report segments the Space Lander and Rover market based on exploration type:

Lunar Surface Exploration: This segment projects significant growth, driven by increased governmental and commercial activity, with a projected market size of USD xx Million by 2033. The market is highly competitive, with numerous players vying for contracts and partnerships.

Mars Surface Exploration: This segment shows moderate growth potential, primarily driven by scientific exploration and the possibility of future human missions. The market size is projected to reach USD xx Million by 2033.

Asteroids Surface Exploration: Currently the smallest segment, it holds the greatest potential for future growth due to the prospect of resource extraction. Market size predictions are uncertain at this stage, estimated at USD xx Million by 2033. The competitive landscape remains relatively nascent with significant opportunities for new entrants.

Key Drivers of Space Lander and Rover Industry Growth

The expansion of the Space Lander and Rover industry is being propelled by a confluence of significant factors. Foremost among these is the substantial increase in government funding allocated to space exploration programs across the globe. Initiatives like NASA's Artemis program and similar endeavors by other international space agencies are directly translating into heightened demand for sophisticated landers and rovers. Secondly, rapid technological advancements, encompassing enhanced robotics, sophisticated autonomous navigation systems, and more efficient power sources, are playing a crucial role in elevating mission capabilities while simultaneously reducing operational costs. Lastly, the burgeoning presence of commercial space companies is acting as a powerful engine for innovation and a catalyst for increased competition, further contributing to the overall market expansion.

Challenges in the Space Lander and Rover Industry Sector

The Space Lander and Rover industry faces challenges such as high development costs and the complexity of operating in extreme environments. Regulatory hurdles in securing launch permits and complying with international space laws can add to project delays and cost overruns. Supply chain disruptions, particularly for specialized components, can impact project timelines and budgets. Finally, intense competition from established players and new entrants requires continuous innovation and adaptation to maintain market share.

Emerging Opportunities in Space Lander and Rover Industry

Emerging opportunities exist in the development of more autonomous and intelligent systems, the exploration of new celestial bodies (e.g., asteroids, moons of other planets), and the commercialization of space resources. Advancements in ISRU technology and increased private sector investment hold the potential to significantly reduce mission costs and enable longer-duration missions. New markets are opening up as space tourism and the mining of extraterrestrial resources gain traction, generating substantial opportunities for innovative companies.

Leading Players in the Space Lander and Rover Industry Market

- ASTROBOTIC TECHNOLOGY

- Lockheed Martin Corporation

- SPACEBIT TECHNOLOGIES

- Blue Origin

- Airbus SE

- Canadian Space Agency

- ISRO

- National Aeronautics and Space Administration

- Roscosmos

- ispace inc

- Japanese Aerospace Exploration Agency (JAXA)

- Northrop Grumman Corporation

- China Academy of Space Technology

Key Developments in Space Lander and Rover Industry Industry

- May 2021: Lockheed Martin partnered with General Motors to design next-generation lunar rovers. This collaboration significantly impacted the market by leveraging automotive expertise in rover design and enhancing capabilities.

- March 2021: NASA awarded Northrop Grumman a contract (USD 60.2 - 84.5 Million potential value) for Mars Ascent Vehicle (MAV) propulsion systems, demonstrating continued investment in Mars exploration and boosting Northrop Grumman's market position.

Strategic Outlook for Space Lander and Rover Industry Market

The Space Lander and Rover industry is strategically positioned for continued and sustained growth, a trajectory fueled by escalating investments from both governmental entities and the private sector in the realm of space exploration. The intensified focus on lunar exploration missions, ambitious Mars expeditions, and the prospective opportunities in asteroid mining are collectively expected to sustain and amplify the demand for innovative lander and rover solutions. The future prosperity of this industry will be intrinsically linked to the relentless pursuit of technological advancements, effective cost reduction strategies, and the establishment of sustainable exploration frameworks. The ongoing influx of new market entrants and the accelerating commercialization of space activities will undoubtedly continue to shape and redefine this dynamic sector.

Space Lander and Rover Industry Segmentation

-

1. Type

- 1.1. Lunar Surface Exploration

- 1.2. Mars Surface Exploration

- 1.3. Asteroids Surface Exploration

Space Lander and Rover Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Rest of the World

Space Lander and Rover Industry Regional Market Share

Geographic Coverage of Space Lander and Rover Industry

Space Lander and Rover Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of > 9.00% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Lunar Surface Exploration

- 5.1.2. Mars Surface Exploration

- 5.1.3. Asteroids Surface Exploration

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Space Lander and Rover Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Lunar Surface Exploration

- 6.1.2. Mars Surface Exploration

- 6.1.3. Asteroids Surface Exploration

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Space Lander and Rover Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Lunar Surface Exploration

- 7.1.2. Mars Surface Exploration

- 7.1.3. Asteroids Surface Exploration

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Space Lander and Rover Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Lunar Surface Exploration

- 8.1.2. Mars Surface Exploration

- 8.1.3. Asteroids Surface Exploration

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific Space Lander and Rover Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Lunar Surface Exploration

- 9.1.2. Mars Surface Exploration

- 9.1.3. Asteroids Surface Exploration

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Rest of the World Space Lander and Rover Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Lunar Surface Exploration

- 10.1.2. Mars Surface Exploration

- 10.1.3. Asteroids Surface Exploration

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 ASTROBOTIC TECHNOLOGY

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Lockheed Martin Corporation

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 SPACEBIT TECHNOLOGIES

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Blue Origin

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Airbus SE

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Canadian Space Agency

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 ISRO

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 National Aeronautics and Space Administration

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Roscosmos

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 ispace inc

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 Japanese Aerospace Exploration Agency (JAXA)

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 Northrop Grumman Corporation

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.13 China Academy of Space Technology

- 11.1.13.1. Company Overview

- 11.1.13.2. Products

- 11.1.13.3. Company Financials

- 11.1.13.4. SWOT Analysis

- 11.1.1 ASTROBOTIC TECHNOLOGY

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Space Lander and Rover Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Space Lander and Rover Industry Revenue (Million), by Type 2025 & 2033

- Figure 3: North America Space Lander and Rover Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Space Lander and Rover Industry Revenue (Million), by Country 2025 & 2033

- Figure 5: North America Space Lander and Rover Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe Space Lander and Rover Industry Revenue (Million), by Type 2025 & 2033

- Figure 7: Europe Space Lander and Rover Industry Revenue Share (%), by Type 2025 & 2033

- Figure 8: Europe Space Lander and Rover Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: Europe Space Lander and Rover Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific Space Lander and Rover Industry Revenue (Million), by Type 2025 & 2033

- Figure 11: Asia Pacific Space Lander and Rover Industry Revenue Share (%), by Type 2025 & 2033

- Figure 12: Asia Pacific Space Lander and Rover Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Asia Pacific Space Lander and Rover Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Rest of the World Space Lander and Rover Industry Revenue (Million), by Type 2025 & 2033

- Figure 15: Rest of the World Space Lander and Rover Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Rest of the World Space Lander and Rover Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Rest of the World Space Lander and Rover Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Space Lander and Rover Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Global Space Lander and Rover Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Global Space Lander and Rover Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 4: Global Space Lander and Rover Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 5: Global Space Lander and Rover Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 6: Global Space Lander and Rover Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Global Space Lander and Rover Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 8: Global Space Lander and Rover Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: Global Space Lander and Rover Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 10: Global Space Lander and Rover Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Space Lander and Rover Industry?

The projected CAGR is approximately > 9.00%.

2. Which companies are prominent players in the Space Lander and Rover Industry?

Key companies in the market include ASTROBOTIC TECHNOLOGY, Lockheed Martin Corporation, SPACEBIT TECHNOLOGIES, Blue Origin, Airbus SE, Canadian Space Agency, ISRO, National Aeronautics and Space Administration, Roscosmos, ispace inc, Japanese Aerospace Exploration Agency (JAXA), Northrop Grumman Corporation, China Academy of Space Technology.

3. What are the main segments of the Space Lander and Rover Industry?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Growing Focus On Space Exploration Driving the Demand for Landers and Rovers.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

In May 2021, Lockheed Martin announced that it has teamed up with General Motors to design the next generation of lunar rovers, capable of transporting astronauts across farther distances on the lunar surface.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Space Lander and Rover Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Space Lander and Rover Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Space Lander and Rover Industry?

To stay informed about further developments, trends, and reports in the Space Lander and Rover Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence