Key Insights

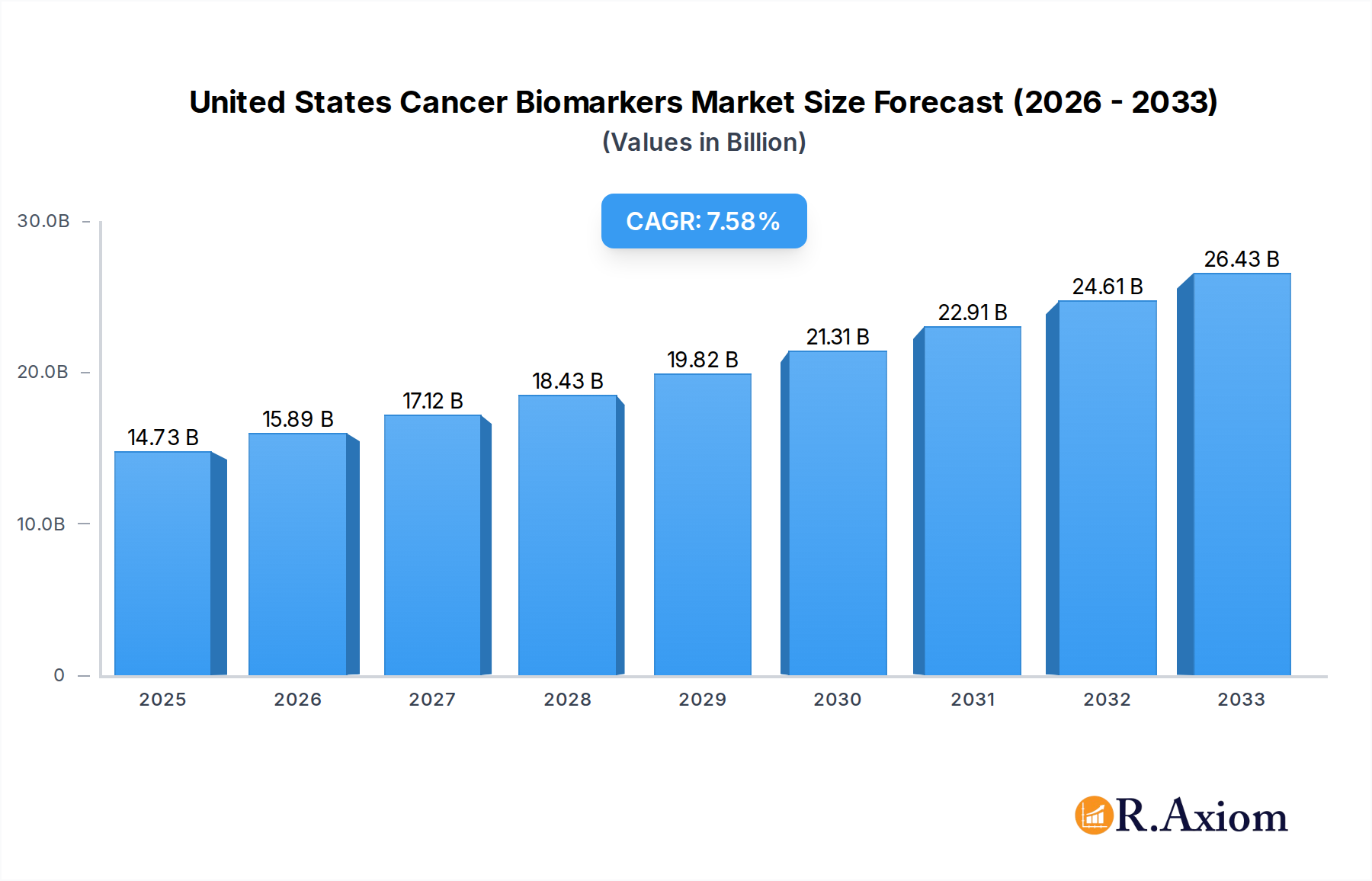

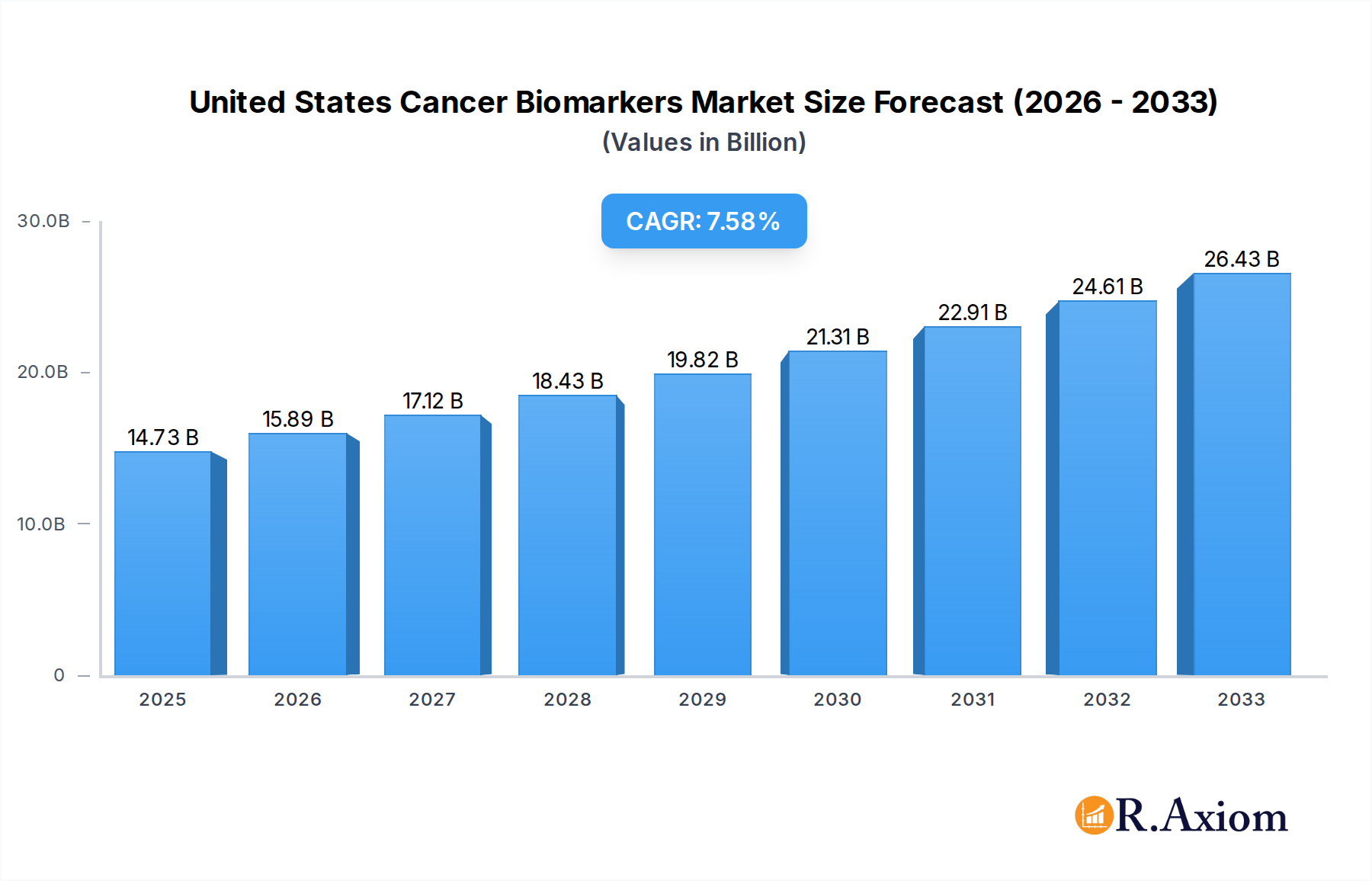

The United States cancer biomarkers market is projected to reach a substantial $14.73 billion in 2025, demonstrating robust growth driven by increasing cancer prevalence and advancements in diagnostic technologies. The market is expected to witness a Compound Annual Growth Rate (CAGR) of 7.88% during the forecast period of 2025-2033. Key drivers propelling this expansion include the rising incidence of prevalent cancers such as prostate, breast, lung, and colorectal cancers, necessitating early detection and personalized treatment strategies. Furthermore, significant investments in research and development by leading companies, coupled with the expanding application of OMICS technologies, imaging technologies, and immunoassays, are fueling market innovation. The growing emphasis on precision medicine and the increasing adoption of companion diagnostics are also pivotal factors contributing to this upward trajectory.

United States Cancer Biomarkers Market Market Size (In Billion)

The market is segmented by disease, with prostate, breast, lung, and colorectal cancers representing the most significant segments due to their high incidence rates. In terms of type, protein and genetic biomarkers are dominating the market, reflecting the advancements in molecular diagnostics. Profiling technologies, particularly OMICS technologies and immunoassays, are crucial in enabling the identification and validation of these biomarkers. The United States is the leading region, driven by its advanced healthcare infrastructure, high healthcare expenditure, and proactive approach to adopting cutting-edge diagnostic solutions. While the market presents immense opportunities, potential restraints such as high regulatory hurdles and the cost of advanced diagnostic tests could influence the pace of growth in certain areas. Companies like F. Hoffmann-La Roche Ltd, Thermo Fisher Scientific, and Abbott Laboratories are actively shaping this dynamic market through product innovation and strategic collaborations.

United States Cancer Biomarkers Market Company Market Share

Here is the SEO-optimized, detailed report description for the United States Cancer Biomarkers Market:

The United States cancer biomarkers market is characterized by a moderate to high level of concentration, with a few key players holding significant market share. Innovation is a primary driver, fueled by continuous advancements in diagnostic technologies and a growing understanding of cancer biology. Regulatory frameworks, particularly those set by the FDA, play a crucial role in approving novel biomarkers and diagnostic assays, impacting market entry and product lifecycles. The presence of readily available substitutes, such as traditional diagnostic methods, necessitates constant innovation and demonstration of superior performance for cancer biomarker solutions. End-user trends show a strong preference for minimally invasive diagnostic techniques and personalized medicine approaches, driving demand for targeted therapies and companion diagnostics. Mergers and acquisition (M&A) activities are prevalent as larger companies seek to expand their portfolios, acquire innovative technologies, and gain a competitive edge. M&A deal values in this sector can range from tens of millions to billions of dollars, reflecting the strategic importance of acquiring specialized expertise and proprietary technologies. For instance, key companies like Thermo Fisher Scientific and F Hoffmann-La Roche Ltd are actively involved in strategic acquisitions to bolster their offerings in oncology diagnostics.

United States Cancer Biomarkers Market Industry Trends & Insights

The United States cancer biomarkers market is poised for substantial growth, projected to reach an estimated value of over $25 billion by 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) of approximately 11.5% during the forecast period of 2025–2033. This expansion is propelled by a confluence of factors, including the escalating incidence of cancer nationwide, a growing emphasis on early detection and prevention, and significant advancements in molecular diagnostics and genomics. The increasing adoption of personalized medicine, where treatment strategies are tailored to the individual genetic makeup of a patient's tumor, is a major catalyst for the biomarker market. This trend is further supported by the development of sophisticated profiling technologies such as OMICS (genomics, proteomics, metabolomics) and advanced Immunoassays, which enable the identification of subtle molecular signatures indicative of disease presence, progression, or response to therapy.

Technological disruptions are continually reshaping the competitive landscape. The integration of artificial intelligence (AI) and machine learning in biomarker discovery and interpretation is revolutionizing the field, allowing for faster and more accurate analysis of complex datasets. This includes AI-driven image analysis for imaging biomarkers and predictive modeling for treatment outcomes. Consumer preferences are increasingly shifting towards proactive health management and non-invasive diagnostic methods. This is driving the demand for liquid biopsy technologies, which analyze biomarkers in bodily fluids like blood or urine, offering a less invasive alternative to traditional tissue biopsies. Market penetration of advanced cancer biomarker tests is growing, especially for prevalent cancers like breast, lung, and prostate cancer, where early detection significantly improves patient survival rates.

The competitive dynamics are intense, with established diagnostic giants and innovative biotech startups vying for market share. Companies are investing heavily in research and development to discover novel biomarkers, develop validated assays, and secure regulatory approvals. Strategic partnerships and collaborations between academic institutions, pharmaceutical companies, and diagnostic providers are crucial for accelerating the translation of research into clinical practice. The growing awareness of the economic benefits of early cancer detection, including reduced treatment costs and improved patient outcomes, is also a significant growth driver. The increasing availability of comprehensive genomic profiling panels and the subsequent use of these insights in clinical decision-making are solidifying the role of biomarkers in routine cancer care within the United States.

Dominant Markets & Segments in United States Cancer Biomarkers Market

The dominance within the United States Cancer Biomarkers Market is multi-faceted, driven by specific disease prevalence, technological superiority, and segment growth.

Disease Segmentation Dominance:

- Prostate Cancer: This segment consistently holds a significant market share due to its high prevalence among the aging male population and the availability of well-established biomarkers like Prostate-Specific Antigen (PSA). Economic factors, such as the widespread availability of PSA screening programs and the associated lower cost compared to some other cancer diagnostics, contribute to its market penetration.

- Breast Cancer: Another dominant segment, driven by advanced screening technologies (mammography, MRI) that often necessitate biomarker analysis for further characterization and personalized treatment. Factors like increased awareness campaigns, growing patient advocacy, and substantial investment in breast cancer research contribute to its leading position.

- Lung Cancer: This segment is experiencing rapid growth, particularly with the advent of targeted therapies and companion diagnostics for non-small cell lung cancer (NSCLC). Advances in liquid biopsy technologies are also significantly impacting this segment by enabling non-invasive detection and monitoring.

- Colorectal Cancer: While established, this segment continues to grow with the adoption of advanced screening methods and the development of molecular markers for risk stratification and treatment selection.

Type Segmentation Dominance:

- Protein Biomarkers: This category remains a cornerstone of the market, encompassing widely used biomarkers like PSA, CA-125, and CEA. Their widespread clinical validation and established assay platforms contribute to their sustained dominance.

- Genetic Biomarkers: This segment is experiencing the most rapid growth due to the rise of precision medicine. The ability to identify specific gene mutations (e.g., EGFR, BRAF) that predict drug response is a key driver. The decreasing cost of genomic sequencing and the increasing availability of multi-gene panels are further fueling this dominance.

Profiling Technology Dominance:

- OMICS Technology: Particularly genomics and proteomics, are emerging as dominant profiling technologies. These advanced techniques allow for comprehensive molecular profiling of tumors, uncovering a vast array of potential biomarkers for diagnosis, prognosis, and therapeutic guidance. The ability to identify novel targets and understand complex biological pathways is paramount.

- Immunoassays: Continue to be a dominant technology due to their established efficacy, cost-effectiveness for many routine tests, and wide range of applications in detecting various cancer-related proteins. Enzyme-linked immunosorbent assays (ELISA) and immunohistochemistry (IHC) remain prevalent.

- Imaging Technology: While not solely a biomarker technology, advanced imaging techniques are increasingly being integrated with biomarker analysis, particularly in areas like assessing tumor response to therapy. The synergistic use of imaging and molecular data is enhancing diagnostic accuracy and treatment planning.

United States Cancer Biomarkers Market Product Developments

Product development in the United States cancer biomarkers market is characterized by a focus on enhanced sensitivity, specificity, and multiplexing capabilities. Innovations are centered around the discovery of novel protein and genetic biomarkers for early detection, prognosis, and treatment selection across various cancer types. Companies are leveraging advanced OMICS technologies and AI-driven analytics to identify more precise molecular signatures. Competitive advantages are being built through the development of liquid biopsy assays, which offer less invasive alternatives to traditional methods, and companion diagnostics that enable personalized treatment strategies, directly impacting patient outcomes and therapeutic efficacy.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the United States Cancer Biomarkers Market, segmented by Disease, Type, and Profiling Technology.

Disease Segmentation: This section delves into the market dynamics for Prostate Cancer, Breast Cancer, Lung Cancer, Colorectal Cancer, and Other Cancers. Each disease segment is analyzed for its growth projections, estimated market sizes, and the competitive landscape specific to biomarker applications in its diagnosis and management.

Type Segmentation: The report examines the market for Protein Biomarkers, Genetic Biomarkers, and Other Types of biomarkers. Growth trajectories, current market valuations, and the competitive environment for each biomarker type are detailed.

Profiling Technology Segmentation: This analysis focuses on the market share and growth prospects of OMICS Technology, Imaging Technology, Immunoassays, and Cytogenetics in cancer biomarker detection and profiling. The competitive strategies and technological advancements within each profiling technology are explored.

Key Drivers of United States Cancer Biomarkers Market Growth

The United States cancer biomarkers market is propelled by several key drivers. The rising global cancer incidence and mortality rates are creating an ever-increasing demand for advanced diagnostic tools. Significant investments in cancer research and development by both public and private entities are leading to the discovery of new biomarkers and the refinement of existing ones. The accelerating adoption of personalized medicine, driven by a deeper understanding of cancer's molecular heterogeneity, is a crucial growth factor, necessitating the use of biomarkers for patient stratification and targeted therapy selection. Furthermore, favorable regulatory landscapes, coupled with increasing healthcare expenditure and government initiatives aimed at early cancer detection, are creating a supportive environment for market expansion.

Challenges in the United States Cancer Biomarkers Market Sector

Despite its robust growth, the United States cancer biomarkers market faces several challenges. The stringent and lengthy regulatory approval processes for new diagnostic tests can impede market entry and delay the commercialization of innovative biomarkers. High development costs associated with biomarker discovery, validation, and assay development represent a significant financial barrier for smaller companies. The lack of standardization in biomarker testing and reporting across different laboratories can lead to variations in results and impact clinical decision-making. Furthermore, issues related to reimbursement policies for novel biomarker tests by insurance providers can limit their widespread adoption. Intense competition and the threat of market saturation for well-established biomarkers also pose challenges.

Emerging Opportunities in United States Cancer Biomarkers Market

Emerging opportunities in the United States cancer biomarkers market are abundant. The rapid advancements in liquid biopsy technologies present a significant opportunity for non-invasive cancer detection, monitoring, and recurrence surveillance. The growing focus on rare and pediatric cancers, which have historically been underserved, offers new avenues for biomarker discovery and development. The integration of artificial intelligence and machine learning in biomarker analysis and interpretation is creating opportunities for more accurate and efficient diagnostics. Furthermore, the increasing demand for companion diagnostics to guide the use of novel targeted therapies and immunotherapies presents a substantial market for biomarker companies. Expansion into emerging markets and the development of cost-effective biomarker solutions will also drive future growth.

Leading Players in the United States Cancer Biomarkers Market Market

- Biomerieux

- F Hoffmann-La Roche Ltd

- Hologic Inc

- Quest Diagnostics

- Thermo Fisher Scientific

- 23andMe

- Illumina Inc

- Abbott Laboratories Inc

- Agilent Technologies

Key Developments in United States Cancer Biomarkers Market Industry

- 2023/2024: Increased focus on the development and validation of liquid biopsy panels for early cancer detection across multiple tumor types.

- 2023: Several collaborations were announced between diagnostic companies and pharmaceutical firms to develop companion diagnostics for new targeted therapies.

- 2022: Regulatory approvals for novel genetic biomarker assays for hereditary cancer predisposition.

- 2021: Significant investment in AI-driven platforms for accelerating biomarker discovery and data analysis.

- 2020: Launch of new protein biomarker assays with enhanced sensitivity for detecting minimal residual disease.

Strategic Outlook for United States Cancer Biomarkers Market Market

The strategic outlook for the United States cancer biomarkers market remains exceptionally strong, driven by the unrelenting pursuit of precision oncology and early disease intervention. Future growth catalysts include the continued evolution of multi-omics platforms, enabling a more holistic understanding of tumor biology and the identification of novel therapeutic targets. The increasing integration of artificial intelligence and big data analytics will further refine biomarker discovery and clinical utility. Strategic partnerships will be crucial for navigating complex regulatory pathways and for translating laboratory discoveries into accessible clinical tools. The market will witness further consolidation as companies seek to achieve economies of scale and expand their comprehensive diagnostic offerings, ultimately benefiting patients with more accurate and personalized cancer care.

United States Cancer Biomarkers Market Segmentation

-

1. Disease

- 1.1. Prostate Cancer

- 1.2. Breast Cancer

- 1.3. Lung Cancer

- 1.4. Colorectal Cancer

- 1.5. Others

-

2. Type

- 2.1. Protein Biomarkers

- 2.2. Genetic Biomarkers

- 2.3. Other Types

-

3. Profiling Technology

- 3.1. OMICS Technology

- 3.2. Imaging Technology

- 3.3. Immunoassays

- 3.4. Cytogenetics

United States Cancer Biomarkers Market Segmentation By Geography

- 1. United States

United States Cancer Biomarkers Market Regional Market Share

Geographic Coverage of United States Cancer Biomarkers Market

United States Cancer Biomarkers Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.88% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Disease

- 5.1.1. Prostate Cancer

- 5.1.2. Breast Cancer

- 5.1.3. Lung Cancer

- 5.1.4. Colorectal Cancer

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Protein Biomarkers

- 5.2.2. Genetic Biomarkers

- 5.2.3. Other Types

- 5.3. Market Analysis, Insights and Forecast - by Profiling Technology

- 5.3.1. OMICS Technology

- 5.3.2. Imaging Technology

- 5.3.3. Immunoassays

- 5.3.4. Cytogenetics

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.1. Market Analysis, Insights and Forecast - by Disease

- 6. United States Cancer Biomarkers Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Disease

- 6.1.1. Prostate Cancer

- 6.1.2. Breast Cancer

- 6.1.3. Lung Cancer

- 6.1.4. Colorectal Cancer

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Protein Biomarkers

- 6.2.2. Genetic Biomarkers

- 6.2.3. Other Types

- 6.3. Market Analysis, Insights and Forecast - by Profiling Technology

- 6.3.1. OMICS Technology

- 6.3.2. Imaging Technology

- 6.3.3. Immunoassays

- 6.3.4. Cytogenetics

- 6.1. Market Analysis, Insights and Forecast - by Disease

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Biomerieux

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 F Hoffmann-La Roche Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Hologic Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Quest Diagnostics

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Thermo Fisher Scientific*List Not Exhaustive

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 23andMe

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Illumina Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Abbott Laboratories Inc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Agilent Technologies

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Biomerieux

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: United States Cancer Biomarkers Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: United States Cancer Biomarkers Market Share (%) by Company 2025

List of Tables

- Table 1: United States Cancer Biomarkers Market Revenue billion Forecast, by Disease 2020 & 2033

- Table 2: United States Cancer Biomarkers Market Revenue billion Forecast, by Type 2020 & 2033

- Table 3: United States Cancer Biomarkers Market Revenue billion Forecast, by Profiling Technology 2020 & 2033

- Table 4: United States Cancer Biomarkers Market Revenue billion Forecast, by Region 2020 & 2033

- Table 5: United States Cancer Biomarkers Market Revenue billion Forecast, by Disease 2020 & 2033

- Table 6: United States Cancer Biomarkers Market Revenue billion Forecast, by Type 2020 & 2033

- Table 7: United States Cancer Biomarkers Market Revenue billion Forecast, by Profiling Technology 2020 & 2033

- Table 8: United States Cancer Biomarkers Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United States Cancer Biomarkers Market?

The projected CAGR is approximately 7.88%.

2. Which companies are prominent players in the United States Cancer Biomarkers Market?

Key companies in the market include Biomerieux, F Hoffmann-La Roche Ltd, Hologic Inc, Quest Diagnostics, Thermo Fisher Scientific*List Not Exhaustive, 23andMe, Illumina Inc, Abbott Laboratories Inc, Agilent Technologies.

3. What are the main segments of the United States Cancer Biomarkers Market?

The market segments include Disease, Type, Profiling Technology.

4. Can you provide details about the market size?

The market size is estimated to be USD 14.73 billion as of 2022.

5. What are some drivers contributing to market growth?

; Increased Burden of Cancer in the US; Increasing Focus on Innovative Drug Development.

6. What are the notable trends driving market growth?

Lung Cancer Segment is Expected to Hold a Major Market Share During the Forecast Period.

7. Are there any restraints impacting market growth?

; High Cost of Diagnosis and Reimbursement Issues.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United States Cancer Biomarkers Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United States Cancer Biomarkers Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United States Cancer Biomarkers Market?

To stay informed about further developments, trends, and reports in the United States Cancer Biomarkers Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence