Key Insights

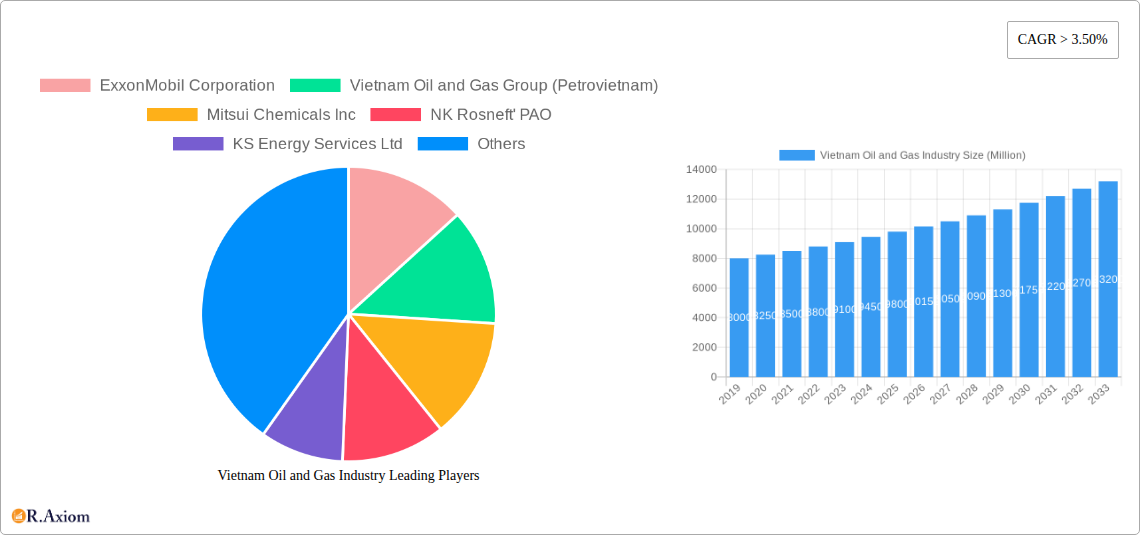

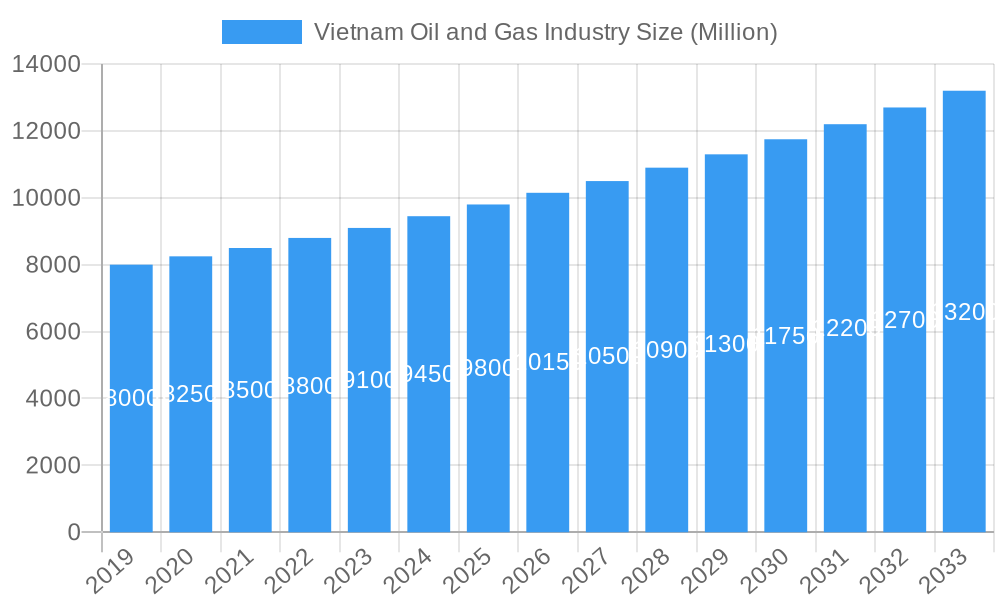

Vietnam's oil and gas sector is projected for significant expansion, forecasting a market size of $2.82 billion by 2025, with a projected Compound Annual Growth Rate (CAGR) of 5.64% through 2033. This growth is propelled by escalating energy demand from Vietnam's rapidly industrializing economy and a growing population. Government support for the oil and gas industry as a strategic resource further underpins this expansion. Continuous exploration and production activities, especially in offshore regions, are expected to boost domestic supply. Concurrently, substantial investments in the downstream refining and petrochemical segments aim to diversify product offerings and meet evolving consumer needs for refined fuels and petrochemical derivatives.

Vietnam Oil and Gas Industry Market Size (In Billion)

Despite a positive trajectory, the industry encounters challenges. Diminishing productivity in mature oil fields requires strategic investment in Enhanced Oil Recovery (EOR) techniques and exploration in new territories. Stringent environmental regulations, while vital for sustainability, can increase operational costs and compliance requirements. Geopolitical dynamics and global oil price fluctuations introduce investment uncertainties. The industry is responding by embracing technological advancements like digitalization and automation in upstream operations, alongside a focus on developing efficient and eco-friendly refining processes. Leading companies such as Petrovietnam, ExxonMobil Corporation, and Idemitsu Kosan Co Ltd are actively influencing the market through strategic collaborations and innovation. The market is segmented into upstream, midstream, and downstream sectors, with an emphasis on value chain optimization.

Vietnam Oil and Gas Industry Company Market Share

Vietnam Oil and Gas Industry: Comprehensive Market Analysis and Future Outlook (2019-2033)

This in-depth report provides a granular analysis of the Vietnam Oil and Gas Industry, covering the historical period (2019-2024), base year (2025), and forecast period (2025-2033). The study delves into market dynamics, segmentation, key players, and emerging trends, offering actionable insights for stakeholders seeking to capitalize on the nation's evolving energy landscape. We examine market concentration, innovation drivers, regulatory frameworks, product substitutes, end-user trends, and M&A activities, alongside dominant markets and segments within the Upstream, Downstream, and Midstream sectors. Discover key drivers of growth, prevailing challenges, and promising emerging opportunities, all while dissecting product developments and providing a strategic outlook for the industry's future.

Vietnam Oil and Gas Industry Market Concentration & Innovation

The Vietnam Oil and Gas Industry, while exhibiting significant growth potential, currently presents a moderately concentrated market. The Vietnam Oil and Gas Group (Petrovietnam) remains a dominant force, holding substantial market share across various segments. However, increasing foreign direct investment and strategic partnerships are fostering greater competition and driving innovation. Key innovation drivers include the adoption of advanced exploration technologies, enhanced oil recovery (EOR) techniques, and the development of cleaner energy solutions in response to evolving environmental regulations and global sustainability trends. The regulatory framework, while supportive of investment, is continuously being refined to encourage sustainable practices and ensure national energy security. Product substitutes, primarily renewable energy sources, are beginning to gain traction, prompting the industry to focus on efficiency and cost-effectiveness for its core products. End-user trends are shifting towards greater demand for cleaner fuels and petrochemical derivatives. Merger and acquisition (M&A) activities are expected to increase as companies seek to consolidate market positions and acquire advanced technologies. While specific M&A deal values are still emerging, significant strategic investments are anticipated, particularly in large-scale projects like offshore gas production.

Vietnam Oil and Gas Industry Industry Trends & Insights

The Vietnam Oil and Gas Industry is poised for substantial growth, driven by robust economic expansion and an increasing demand for energy to fuel its burgeoning industrial and consumer sectors. The industry's compound annual growth rate (CAGR) is projected to be significant over the forecast period (2025-2033), reflecting strong underlying market fundamentals. Technological disruptions are playing a pivotal role, with companies investing heavily in cutting-edge exploration and production (E&P) technologies to optimize resource extraction from both conventional and unconventional reserves. This includes the deployment of advanced seismic imaging, horizontal drilling, and hydraulic fracturing techniques where applicable and permissible. Furthermore, the industry is witnessing a greater focus on digitalization and automation, leading to improved operational efficiency, enhanced safety standards, and reduced environmental impact.

Consumer preferences are evolving, with a growing awareness of environmental issues influencing the demand for cleaner fuels and energy-efficient products. This trend is spurring investment in downstream refining capabilities to produce higher-quality fuels and a diversification into petrochemicals for a wider range of industrial applications. The competitive dynamics within the Vietnamese oil and gas sector are intensifying, characterized by a mix of state-owned enterprises, international oil companies (IOCs), and emerging independent players. This competitive landscape encourages continuous innovation and strategic alliances to secure market share and access new opportunities. Market penetration for advanced technologies and sustainable practices is on an upward trajectory, signaling a mature yet dynamic industry adapting to global energy transitions. The discovery of new reserves and the efficient development of existing ones remain critical for sustaining this growth momentum.

Dominant Markets & Segments in Vietnam Oil and Gas Industry

The Upstream sector stands as the dominant market within Vietnam's oil and gas industry, driven by significant proven reserves and ongoing exploration efforts. The economic policies of the Vietnamese government, aimed at maximizing domestic energy production and attracting foreign investment, are key drivers for this segment's prominence. Furthermore, substantial investments in exploration and production infrastructure, including offshore platforms and drilling rigs, underscore its leading position.

- Upstream:

- Economic Policies: Government incentives and favorable fiscal terms for exploration and production activities are major catalysts.

- Infrastructure Development: Significant investments in offshore exploration technology and pipeline networks support upstream operations.

- Resource Potential: The discovery and development of new oil and gas fields, particularly in deep-water areas, continue to fuel growth.

- Market Share: Petrovietnam holds a commanding market share, but IOCs are increasingly active.

The Downstream sector, encompassing refining and petrochemicals, is experiencing robust growth, intrinsically linked to the expanding domestic demand for refined products and industrial chemicals. This growth is propelled by the country's industrialization and rising consumer spending power.

- Downstream:

- Industrialization: Rapid industrial growth necessitates a steady supply of petrochemical feedstocks and refined products.

- Consumer Demand: Increasing disposable incomes lead to higher demand for petroleum-based consumer goods and transportation fuels.

- Refinery Modernization: Investments in upgrading existing refineries and building new facilities to meet international quality standards are crucial.

The Midstream sector, responsible for the transportation, storage, and processing of oil and gas, is also a critical and growing segment. The expansion of the national pipeline network and the development of LNG import terminals are essential to connect upstream production sites with downstream consumption centers and to ensure energy security.

- Midstream:

- Logistics and Infrastructure: Expansion of pipelines, storage facilities, and liquefaction/regasification terminals is vital for efficient energy distribution.

- Energy Security: The midstream segment plays a crucial role in ensuring a reliable and stable supply of energy to the nation.

Vietnam Oil and Gas Industry Product Developments

Product developments in the Vietnam Oil and Gas Industry are increasingly focused on enhancing the efficiency and sustainability of existing offerings while exploring new applications for petrochemical derivatives. This includes the refinement of cleaner fuels with reduced sulfur content to meet stricter environmental standards and the development of advanced lubricants and specialty chemicals catering to diverse industrial needs. Petrochemical innovations are leading to the creation of new polymers and materials used in manufacturing, construction, and consumer goods, offering competitive advantages through improved performance and recyclability. The industry is also exploring opportunities in hydrogen production and carbon capture technologies, aligning with global decarbonization efforts and opening avenues for future growth.

Report Scope & Segmentation Analysis

This report segments the Vietnam Oil and Gas Industry across its core operational sectors: Upstream, Downstream, and Midstream.

- Upstream: This segment encompasses exploration, drilling, and production of crude oil and natural gas. The market is projected to witness significant growth due to ongoing exploration activities and the development of new reserves. Competitive dynamics are characterized by major international players and Petrovietnam.

- Downstream: This segment covers refining of crude oil into various petroleum products and the production of petrochemicals. Growth is anticipated to be strong, driven by increasing domestic demand for fuels and chemical intermediates. Technological advancements in refining processes and product diversification are key areas of focus.

- Midstream: This segment includes the transportation, storage, and distribution of oil and gas, as well as processing and liquefaction. Market growth will be supported by the expansion of pipeline networks and the development of LNG infrastructure to meet evolving energy demands.

Key Drivers of Vietnam Oil and Gas Industry Growth

The Vietnam Oil and Gas Industry's growth is propelled by a confluence of factors. A rapidly expanding economy and increasing energy consumption are fundamental demand drivers. Government support through favorable policies, fiscal incentives for exploration, and a commitment to energy security are critical enablers. Technological advancements in E&P are unlocking new reserves and enhancing recovery rates, boosting production volumes. Furthermore, the strategic location of Vietnam within the Southeast Asian region presents opportunities for regional energy trade and development. Investments in infrastructure, including pipelines and LNG terminals, are crucial for efficient resource utilization and distribution, underpinning sustained growth.

Challenges in the Vietnam Oil and Gas Industry Sector

Despite its growth potential, the Vietnam Oil and Gas Industry faces several challenges. Fluctuations in global oil prices can impact investment decisions and profitability. Regulatory hurdles and evolving environmental standards require continuous adaptation and investment in cleaner technologies. The mature nature of some existing fields necessitates increased focus on enhanced oil recovery (EOR) techniques, which can be costly and technologically demanding. Supply chain disruptions, both domestic and international, can affect project timelines and operational efficiency. Intense competition from both domestic and international players can put pressure on margins. Furthermore, the increasing global push towards renewable energy sources presents a long-term challenge to the sustained demand for fossil fuels.

Emerging Opportunities in Vietnam Oil and Gas Industry

Emerging opportunities in the Vietnam Oil and Gas Industry are centered around several key areas. The ongoing exploration of deep-water and frontier basins holds significant potential for new hydrocarbon discoveries. The increasing demand for natural gas as a cleaner transition fuel presents opportunities for LNG import and domestic distribution expansion. Petrochemical diversification, moving beyond basic fuels to high-value specialty chemicals, offers avenues for enhanced profitability. The development of offshore wind energy projects, often integrated with existing offshore oil and gas infrastructure, represents a significant opportunity in the renewable energy space. Furthermore, advancements in carbon capture, utilization, and storage (CCUS) technologies could unlock new business models and contribute to decarbonization efforts.

Leading Players in the Vietnam Oil and Gas Industry Market

- ExxonMobil Corporation

- Vietnam Oil and Gas Group (Petrovietnam)

- Mitsui Chemicals Inc

- NK Rosneft' PAO

- KS Energy Services Ltd

- Idemitsu Kosan Co Ltd

- Essar Oil and Gas Exploration and Production Ltd

- Eni SpA

- Jadestone Energy PLC

- Japan Drilling Co Ltd

Key Developments in Vietnam Oil and Gas Industry Industry

- November 2021: ExxonMobil committed to investing in the Ca Voi Xanh (Blue Whale) gas production project off Vietnam's central coast. The company has finalized its FEED document and is progressing with the project's development plan. The field is estimated to hold approximately 150 billion cubic meters of reserves, with construction anticipated to commence during the forecast period.

- April 2021: Pharos, a UK-based exploration and production company, announced its intention to initiate the exploration phase in Block-125 of Vietnam's Phu Khanh basin. The company plans to explore two distinct areas within the block: a deep-water zone estimated to contain 1 billion barrels (bbl) of crude oil, and a shallow-water zone with reserves ranging from 100 to 200 million bbls of oil.

Strategic Outlook for Vietnam Oil and Gas Industry Market

The strategic outlook for the Vietnam Oil and Gas Industry is one of sustained growth and transformation. The industry is expected to capitalize on its significant hydrocarbon reserves and the increasing domestic demand for energy, while also navigating the global energy transition. Investments in advanced exploration and production technologies will be crucial for maximizing resource recovery. Diversification into petrochemicals and the exploration of cleaner energy sources like hydrogen will be key to long-term sustainability and profitability. The government's continued commitment to attracting foreign investment and fostering a stable regulatory environment will be paramount. Strategic partnerships and M&A activities are likely to shape the competitive landscape, driving innovation and operational efficiency. The industry's ability to adapt to evolving environmental regulations and embrace sustainable practices will determine its resilience and long-term success.

Vietnam Oil and Gas Industry Segmentation

-

1. Sector

- 1.1. Upstream

- 1.2. Downstream

- 1.3. Midstream

Vietnam Oil and Gas Industry Segmentation By Geography

- 1. Vietnam

Vietnam Oil and Gas Industry Regional Market Share

Geographic Coverage of Vietnam Oil and Gas Industry

Vietnam Oil and Gas Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.64% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 5.1.1. Upstream

- 5.1.2. Downstream

- 5.1.3. Midstream

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Vietnam

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 6. Vietnam Oil and Gas Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Sector

- 6.1.1. Upstream

- 6.1.2. Downstream

- 6.1.3. Midstream

- 6.1. Market Analysis, Insights and Forecast - by Sector

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 ExxonMobil Corporation

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Vietnam Oil and Gas Group (Petrovietnam)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Mitsui Chemicals Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 NK Rosneft' PAO

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 KS Energy Services Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Idemitsu Kosan Co Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Essar Oil and Gas Exploration and Production Ltd*List Not Exhaustive

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Eni SpA

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Jadestone Energy PLC

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Japan Drilling Co Ltd

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 ExxonMobil Corporation

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Vietnam Oil and Gas Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Vietnam Oil and Gas Industry Share (%) by Company 2025

List of Tables

- Table 1: Vietnam Oil and Gas Industry Revenue billion Forecast, by Sector 2020 & 2033

- Table 2: Vietnam Oil and Gas Industry Volume Tonnes Forecast, by Sector 2020 & 2033

- Table 3: Vietnam Oil and Gas Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Vietnam Oil and Gas Industry Volume Tonnes Forecast, by Region 2020 & 2033

- Table 5: Vietnam Oil and Gas Industry Revenue billion Forecast, by Sector 2020 & 2033

- Table 6: Vietnam Oil and Gas Industry Volume Tonnes Forecast, by Sector 2020 & 2033

- Table 7: Vietnam Oil and Gas Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 8: Vietnam Oil and Gas Industry Volume Tonnes Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Vietnam Oil and Gas Industry?

The projected CAGR is approximately 5.64%.

2. Which companies are prominent players in the Vietnam Oil and Gas Industry?

Key companies in the market include ExxonMobil Corporation, Vietnam Oil and Gas Group (Petrovietnam), Mitsui Chemicals Inc, NK Rosneft' PAO, KS Energy Services Ltd, Idemitsu Kosan Co Ltd, Essar Oil and Gas Exploration and Production Ltd*List Not Exhaustive, Eni SpA, Jadestone Energy PLC, Japan Drilling Co Ltd.

3. What are the main segments of the Vietnam Oil and Gas Industry?

The market segments include Sector.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.82 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Global Demand for Refined Petroleum Products4.; Economic Growth and Industrialization.

6. What are the notable trends driving market growth?

Upstream Segment Expected to Witness Significant Growth.

7. Are there any restraints impacting market growth?

Environmental Concerns and Regulations.

8. Can you provide examples of recent developments in the market?

In November 2021, ExxonMobil decided to invest in the Ca Voi Xanh (Blue Whale) gas production project located off Vietnam's central coast. The company is ready with the FEED document and is currently working on the project's development plan. The field is estimated to have around 150 billion cubic meters in reserves. The construction is expected to start during the forecast period.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in Tonnes.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Vietnam Oil and Gas Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Vietnam Oil and Gas Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Vietnam Oil and Gas Industry?

To stay informed about further developments, trends, and reports in the Vietnam Oil and Gas Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence