Key Insights

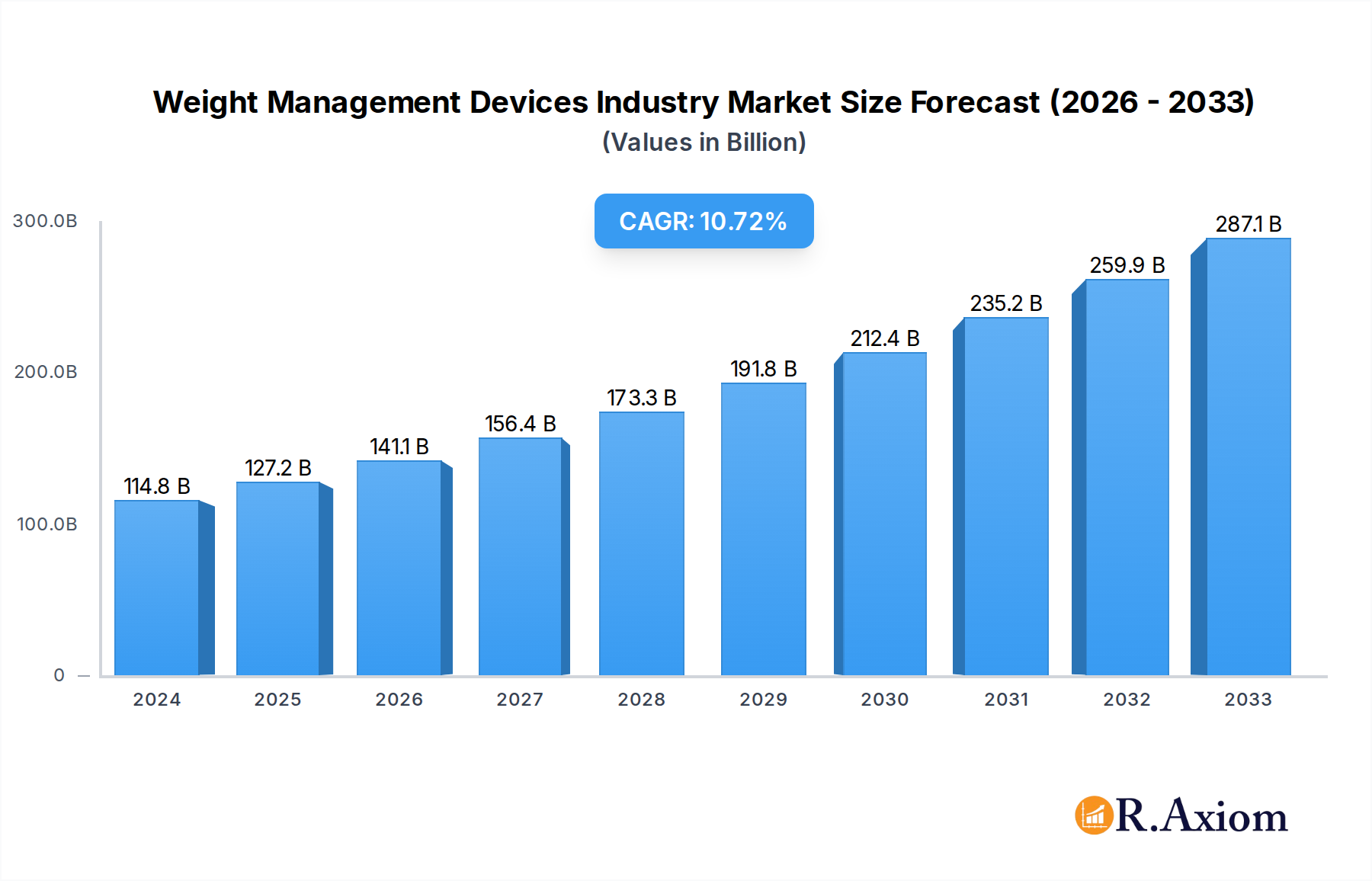

The global Weight Management Devices market is poised for substantial growth, with an estimated market size of USD 114.79 billion in 2024. This robust expansion is driven by a confluence of factors, including the rising global prevalence of obesity and related chronic diseases, increasing consumer awareness regarding health and fitness, and significant advancements in medical and fitness technology. The market's projected CAGR of 10.9% from 2019-2033 underscores its dynamic nature and strong future potential. Key growth drivers include technological innovations leading to more effective and user-friendly devices, a growing demand for non-invasive weight management solutions, and supportive government initiatives promoting public health. The increasing integration of smart technology, such as wearable fitness trackers and AI-powered weight management platforms, is further accelerating market penetration. The surgical equipment segment, though smaller, is also experiencing growth due to increasing acceptance of bariatric surgeries and advancements in minimally invasive techniques.

Weight Management Devices Industry Market Size (In Billion)

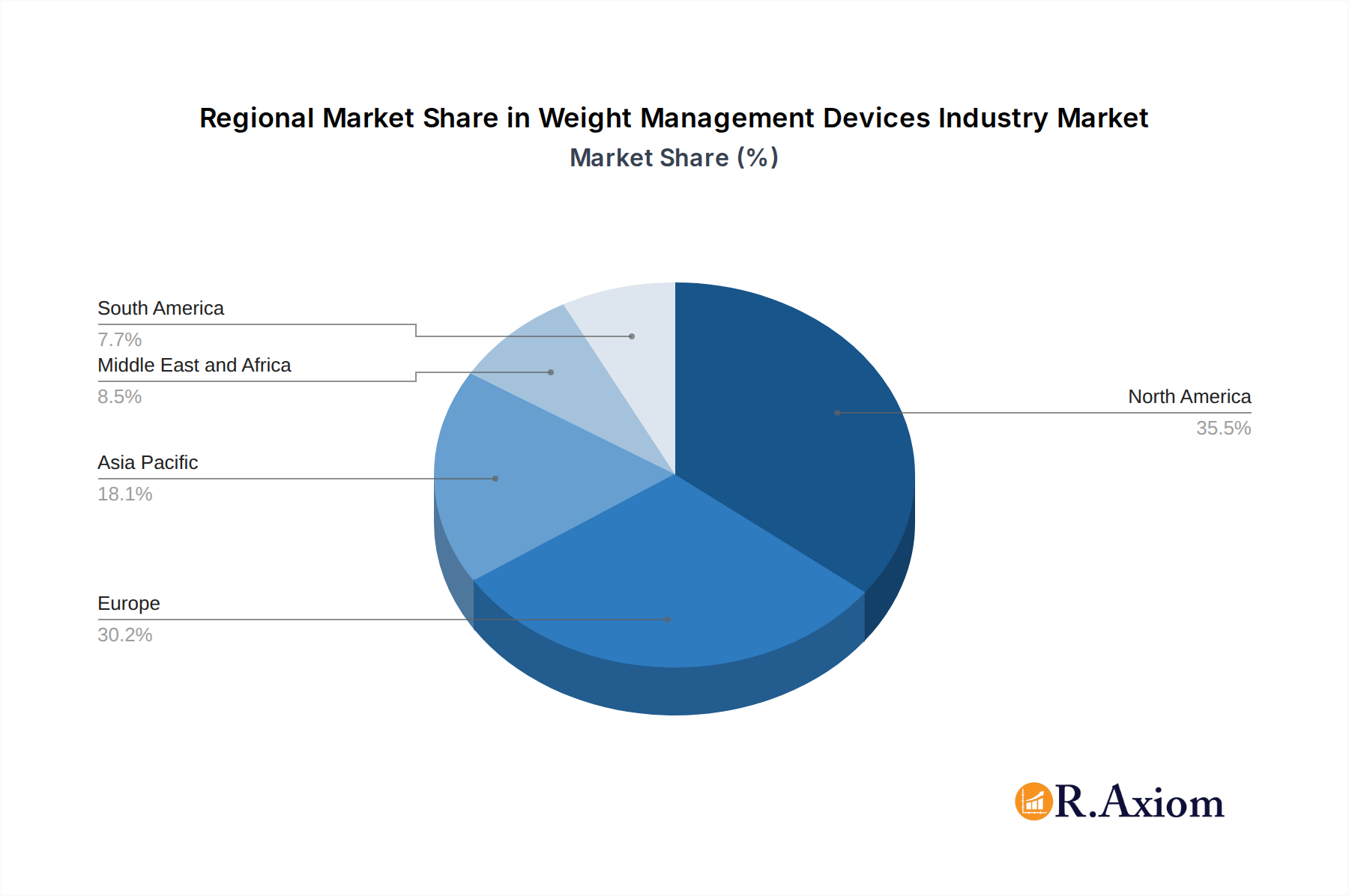

The market's segmentation reflects a diverse range of offerings catering to both the fitness and medical sectors. In the fitness segment, cardiovascular training equipment, strength training equipment, and fitness monitoring devices are leading the charge, benefiting from a heightened focus on preventive healthcare and wellness. Companies like Johnson Health Technology Co. Ltd, Life Fitness, and Technogym SpA are at the forefront of innovation in this space. Concurrently, the surgical equipment segment, with key players such as Medtronic PLC and Olympus Corporation, is driven by the need for effective solutions for severe obesity. Geographically, North America and Europe currently hold significant market shares, driven by high disposable incomes and established healthcare infrastructures. However, the Asia Pacific region is anticipated to exhibit the fastest growth, fueled by a burgeoning middle class, increasing health consciousness, and expanding healthcare access. The market, while promising, faces challenges such as high device costs and the need for greater consumer education on the proper and effective use of these devices to achieve sustained results.

Weight Management Devices Industry Company Market Share

This comprehensive report provides an in-depth analysis of the global Weight Management Devices Industry, offering critical insights for stakeholders navigating this dynamic market. Spanning from 2019 to 2033, with a base year of 2025, the report details historical trends and forecasts future market trajectories. The forecast period of 2025–2033 promises substantial growth driven by increasing health consciousness and technological advancements. The historical period of 2019–2024 sets the stage for understanding the foundational shifts and market evolution. The estimated year of 2025 highlights current market conditions and the immediate future. This report leverages high-traffic keywords such as "weight loss devices," "obesity management solutions," "fitness equipment market," "surgical weight loss," and "health monitoring technology" to ensure maximum search visibility.

Weight Management Devices Industry Market Concentration & Innovation

The Weight Management Devices Industry exhibits a moderate level of market concentration, with a blend of established conglomerates and specialized innovators. Key players like Johnson Health Technology Co Ltd, Life Fitness, and Technogym SpA dominate the fitness equipment segment, while companies such as Medtronic PLC and Apollo Endosurgery hold significant sway in the surgical devices arena. Innovation serves as a primary driver, with continuous advancements in smart fitness devices, non-invasive weight loss technologies, and AI-powered personalized health platforms. Regulatory frameworks, particularly those governing medical devices and health claims, play a crucial role in shaping market entry and product development. Product substitutes, ranging from dietary supplements to behavioral therapy, present a competitive challenge. End-user trends are increasingly leaning towards preventative healthcare, at-home fitness solutions, and data-driven wellness programs. Mergers and acquisitions (M&A) activities are strategically employed to gain market share and acquire innovative technologies. Notable M&A deal values are estimated to be in the billions, reflecting the industry's robust financial landscape.

- Market Share Drivers: Technological innovation, brand reputation, distribution networks, and strategic partnerships.

- Regulatory Impact: Stringent approvals for surgical devices versus more lenient oversight for fitness equipment.

- M&A Focus: Acquisition of early-stage tech startups and companies with unique therapeutic approaches.

Weight Management Devices Industry Industry Trends & Insights

The global Weight Management Devices Industry is experiencing robust growth, projected to expand at a significant Compound Annual Growth Rate (CAGR) of approximately 8.5% between 2025 and 2033. This upward trajectory is fueled by a confluence of factors, most notably the escalating global prevalence of obesity and associated comorbidities, which are driving increased demand for effective weight management solutions. Consumer awareness regarding the health risks linked to excess weight, such as cardiovascular diseases, diabetes, and certain cancers, is at an all-time high, prompting individuals to actively seek devices and technologies that aid in weight reduction and maintenance. Technological disruptions are rapidly reshaping the market landscape. The integration of artificial intelligence (AI) and machine learning (ML) into fitness trackers, smart scales, and even surgical navigation systems is enabling more personalized and effective interventions. Wearable technology, in particular, has witnessed exponential growth in market penetration, offering consumers continuous health monitoring, activity tracking, and personalized feedback.

Consumer preferences are evolving towards holistic wellness approaches. Beyond simple weight loss, individuals are increasingly prioritizing overall health improvement, encompassing nutrition, physical activity, and mental well-being. This shift is driving demand for integrated solutions that offer comprehensive health management rather than single-purpose devices. The competitive dynamics within the industry are intense. Established players are investing heavily in research and development to stay ahead of the curve, while emerging startups are disrupting the market with novel technologies and business models. The rise of telemedicine and remote patient monitoring is also creating new avenues for weight management, allowing for virtual consultations and personalized guidance from healthcare professionals. The market penetration of connected fitness devices is rapidly increasing, with consumers embracing interactive workouts and digital coaching. This trend is further amplified by the growing acceptance of subscription-based models, offering continuous engagement and value. The increasing disposable income in developing economies is also a significant growth driver, as more individuals can afford advanced weight management solutions. Furthermore, government initiatives promoting public health and combating obesity are indirectly boosting the market by raising awareness and encouraging healthier lifestyles, thereby increasing the demand for devices that support these efforts.

Dominant Markets & Segments in Weight Management Devices Industry

The Weight Management Devices Industry is characterized by significant regional and segmental dominance. North America, particularly the United States, stands as the leading market, driven by high disposable incomes, a strong emphasis on health and wellness, and a high prevalence of obesity. Government initiatives and robust healthcare infrastructure further bolster its leading position. Within North America, the Fitness Equipment segment, specifically Cardiovascular Training Equipment, commands the largest market share. This dominance is attributed to the widespread adoption of treadmills, elliptical trainers, stationary bikes, and rowing machines by both commercial gyms and individual households. Economic policies in developed nations favor increased consumer spending on health and fitness, supporting this segment's growth.

Leading Region: North America.

- Key Drivers: High disposable income, strong health consciousness, prevalence of obesity, advanced healthcare infrastructure, supportive government initiatives.

- Market Penetration: High penetration of fitness devices and surgical weight loss procedures.

Dominant Segment: Fitness Equipment.

- Sub-Segment Dominance: Cardiovascular Training Equipment.

- Key Drivers: Growing trend of home fitness, increasing popularity of gyms and fitness centers, technological advancements in cardio machines (e.g., interactive displays, pre-programmed workouts).

- Market Size: Significant portion of the overall weight management devices market.

- Sub-Segment Dominance: Cardiovascular Training Equipment.

Emerging Segment Growth: Surgical Equipment is also a significant segment, driven by advancements in bariatric surgery techniques and devices. Countries with well-developed surgical specialties and insurance coverage for obesity procedures exhibit strong demand. Economic development and healthcare spending in Asia-Pacific are contributing to a rapidly growing market for both fitness and surgical weight management solutions. The increasing disposable income and rising health awareness in countries like China and India are significant growth catalysts.

Weight Management Devices Industry Product Developments

Product development in the Weight Management Devices Industry is intensely focused on innovation and user-centric design. Companies are continuously launching advanced Fitness Equipment, incorporating smart technology for enhanced user experience and data tracking. Innovations include AI-powered personalized workout plans, virtual reality (VR) integrated exercise experiences, and highly compact, multi-functional home gym systems. In the Surgical Equipment domain, advancements are centered on minimally invasive techniques, robotic-assisted surgery, and improved implantable devices that offer greater efficacy and reduced recovery times. The competitive advantage lies in devices that demonstrate superior clinical outcomes, enhanced patient safety, and seamless integration with digital health platforms. Technological trends are pushing towards connectivity, personalized feedback, and non-invasive or less invasive solutions.

Report Scope & Segmentation Analysis

This report meticulously analyzes the Weight Management Devices Industry across key segments. The Fitness Equipment segment is further divided into Cardiovascular Training Equipment, Strength Training Equipment, Fitness Monitoring Equipment, and Other Fitness Equipment. Each sub-segment is analyzed for its market size, growth projections, and competitive dynamics. Cardiovascular training equipment is expected to maintain its leading position due to widespread adoption. Fitness monitoring equipment, including wearable devices and smart scales, is projected for substantial growth driven by increased health awareness. The Surgical Equipment segment focuses on bariatric and other weight-loss-related surgical devices, with strong growth anticipated due to technological advancements and increasing acceptance of surgical interventions for severe obesity.

- Fitness Equipment: Expected to dominate the market, with significant growth in connected and smart devices.

- Cardiovascular Training Equipment: High market share and steady growth due to home fitness trends.

- Fitness Monitoring Equipment: High CAGR driven by wearable technology and preventative health focus.

- Surgical Equipment: Robust growth driven by innovative minimally invasive procedures and improved patient outcomes.

Key Drivers of Weight Management Devices Industry Growth

The Weight Management Devices Industry is propelled by several key drivers. The escalating global obesity rates and the associated health risks create a persistent demand for effective solutions. Technological advancements, particularly in AI, IoT, and wearable technology, are enabling the development of more sophisticated and personalized weight management devices. Increasing consumer health consciousness and a proactive approach to wellness are driving individuals to invest in fitness equipment and health monitoring tools. Government initiatives and public health campaigns aimed at combating obesity further stimulate market growth. The growing acceptance and innovation in bariatric surgery and related medical devices also contribute significantly.

- Rising Obesity Epidemic: Direct demand for weight loss and management solutions.

- Technological Innovation: Smart wearables, AI-driven apps, and advanced medical devices.

- Health & Wellness Trends: Proactive consumer approach to fitness and preventative care.

- Government Support: Public health initiatives and healthcare policy changes.

Challenges in the Weight Management Devices Industry Sector

Despite its growth, the Weight Management Devices Industry faces several challenges. High product costs can be a barrier for widespread adoption, especially in developing economies. Stringent regulatory approvals, particularly for surgical devices, can lead to extended development timelines and increased expenses. The rapidly evolving technological landscape necessitates continuous investment in R&D, posing a challenge for smaller players. Intense competition from both established brands and emerging startups can lead to price wars and reduced profit margins. Furthermore, issues related to data privacy and security for connected devices need to be addressed to build consumer trust.

- High Product Costs: Limiting affordability for a significant portion of the population.

- Stringent Regulatory Hurdles: Lengthy approval processes for medical devices.

- Rapid Technological Obsolescence: Need for continuous innovation and investment.

- Data Security Concerns: Building trust in connected health platforms.

Emerging Opportunities in Weight Management Devices Industry

Emerging opportunities within the Weight Management Devices Industry are vast and varied. The expanding markets in Asia-Pacific and Latin America present significant untapped potential due to rising disposable incomes and growing health awareness. The integration of telehealth and remote patient monitoring offers a scalable model for delivering weight management services. Innovations in non-invasive and minimally invasive technologies are creating new treatment avenues. The increasing focus on personalized medicine and data analytics presents opportunities for developing tailored weight management programs and devices. Furthermore, collaborations between healthcare providers, technology companies, and fitness brands can unlock synergistic growth.

- Developing Markets: Untapped potential in Asia-Pacific and Latin America.

- Telehealth Integration: Scalable delivery of remote weight management solutions.

- Non-Invasive Technologies: New treatment paradigms and broader patient appeal.

- Personalized Medicine: Data-driven, customized weight management strategies.

Leading Players in the Weight Management Devices Industry Market

- Fitness World

- Johnson Health Technology Co Ltd

- Life Fitness

- Technogym SpA

- Medtronic PLC

- Cybex International Inc

- Atkins Nutritionals

- Olympus Corporation

- Life Time Inc

- Apollo Endosurgery

Key Developments in Weight Management Devices Industry Industry

- November 2022: Powermax Fitness launched cutting-edge fitness equipment with advanced technology in India. The new launch includes the quality elliptical cross trainer, Powermax EH 760, and commercial and semi-commercial motorized treadmills like Powermax TAC-3000, TAC-3500, TAC-550, and TAC-585.

- March 2021: Matrix launched a three-tiered cardio series - the performance series, the endurance series, and the lifestyle series - for cardiovascular training and weight monitoring purposes.

Strategic Outlook for Weight Management Devices Industry Market

The strategic outlook for the Weight Management Devices Industry is exceptionally positive, characterized by sustained growth driven by evolving consumer needs and continuous technological innovation. The increasing global focus on preventative healthcare and the management of chronic diseases like obesity will ensure a robust demand for both fitness and medical weight management solutions. Companies that can successfully integrate smart technologies, offer personalized experiences, and navigate the regulatory landscape will be well-positioned for success. Strategic partnerships and acquisitions will continue to play a vital role in consolidating market share and acquiring advanced capabilities. The industry's capacity to adapt to emerging trends, such as the growing demand for at-home fitness and the integration of digital health platforms, will be crucial for long-term prosperity and market leadership.

Weight Management Devices Industry Segmentation

-

1. Equipment

-

1.1. Fitness Equipment

- 1.1.1. Cardiovascular Training Equipment

- 1.1.2. Strength Training Equipment

- 1.1.3. Fitness Monitoring Equipment

- 1.1.4. Other Fitness Equipment

- 1.2. Surgical Equipment

-

1.1. Fitness Equipment

Weight Management Devices Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Weight Management Devices Industry Regional Market Share

Geographic Coverage of Weight Management Devices Industry

Weight Management Devices Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Equipment

- 5.1.1. Fitness Equipment

- 5.1.1.1. Cardiovascular Training Equipment

- 5.1.1.2. Strength Training Equipment

- 5.1.1.3. Fitness Monitoring Equipment

- 5.1.1.4. Other Fitness Equipment

- 5.1.2. Surgical Equipment

- 5.1.1. Fitness Equipment

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Middle East and Africa

- 5.2.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Equipment

- 6. Global Weight Management Devices Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Equipment

- 6.1.1. Fitness Equipment

- 6.1.1.1. Cardiovascular Training Equipment

- 6.1.1.2. Strength Training Equipment

- 6.1.1.3. Fitness Monitoring Equipment

- 6.1.1.4. Other Fitness Equipment

- 6.1.2. Surgical Equipment

- 6.1.1. Fitness Equipment

- 6.1. Market Analysis, Insights and Forecast - by Equipment

- 7. North America Weight Management Devices Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Equipment

- 7.1.1. Fitness Equipment

- 7.1.1.1. Cardiovascular Training Equipment

- 7.1.1.2. Strength Training Equipment

- 7.1.1.3. Fitness Monitoring Equipment

- 7.1.1.4. Other Fitness Equipment

- 7.1.2. Surgical Equipment

- 7.1.1. Fitness Equipment

- 7.1. Market Analysis, Insights and Forecast - by Equipment

- 8. Europe Weight Management Devices Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Equipment

- 8.1.1. Fitness Equipment

- 8.1.1.1. Cardiovascular Training Equipment

- 8.1.1.2. Strength Training Equipment

- 8.1.1.3. Fitness Monitoring Equipment

- 8.1.1.4. Other Fitness Equipment

- 8.1.2. Surgical Equipment

- 8.1.1. Fitness Equipment

- 8.1. Market Analysis, Insights and Forecast - by Equipment

- 9. Asia Pacific Weight Management Devices Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Equipment

- 9.1.1. Fitness Equipment

- 9.1.1.1. Cardiovascular Training Equipment

- 9.1.1.2. Strength Training Equipment

- 9.1.1.3. Fitness Monitoring Equipment

- 9.1.1.4. Other Fitness Equipment

- 9.1.2. Surgical Equipment

- 9.1.1. Fitness Equipment

- 9.1. Market Analysis, Insights and Forecast - by Equipment

- 10. Middle East and Africa Weight Management Devices Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Equipment

- 10.1.1. Fitness Equipment

- 10.1.1.1. Cardiovascular Training Equipment

- 10.1.1.2. Strength Training Equipment

- 10.1.1.3. Fitness Monitoring Equipment

- 10.1.1.4. Other Fitness Equipment

- 10.1.2. Surgical Equipment

- 10.1.1. Fitness Equipment

- 10.1. Market Analysis, Insights and Forecast - by Equipment

- 11. South America Weight Management Devices Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Equipment

- 11.1.1. Fitness Equipment

- 11.1.1.1. Cardiovascular Training Equipment

- 11.1.1.2. Strength Training Equipment

- 11.1.1.3. Fitness Monitoring Equipment

- 11.1.1.4. Other Fitness Equipment

- 11.1.2. Surgical Equipment

- 11.1.1. Fitness Equipment

- 11.1. Market Analysis, Insights and Forecast - by Equipment

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Fitness World

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Johnson Health Technology Co Ltd

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Life Fitness

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Technogym SpA

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Medtronic PLC

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Cybex International Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Atkins Nutritionals

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Olympus Corporation

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Life Time Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Apollo Endosurgery

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Fitness World

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Weight Management Devices Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Weight Management Devices Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Weight Management Devices Industry Revenue (billion), by Equipment 2025 & 2033

- Figure 4: North America Weight Management Devices Industry Volume (K Unit), by Equipment 2025 & 2033

- Figure 5: North America Weight Management Devices Industry Revenue Share (%), by Equipment 2025 & 2033

- Figure 6: North America Weight Management Devices Industry Volume Share (%), by Equipment 2025 & 2033

- Figure 7: North America Weight Management Devices Industry Revenue (billion), by Country 2025 & 2033

- Figure 8: North America Weight Management Devices Industry Volume (K Unit), by Country 2025 & 2033

- Figure 9: North America Weight Management Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: North America Weight Management Devices Industry Volume Share (%), by Country 2025 & 2033

- Figure 11: Europe Weight Management Devices Industry Revenue (billion), by Equipment 2025 & 2033

- Figure 12: Europe Weight Management Devices Industry Volume (K Unit), by Equipment 2025 & 2033

- Figure 13: Europe Weight Management Devices Industry Revenue Share (%), by Equipment 2025 & 2033

- Figure 14: Europe Weight Management Devices Industry Volume Share (%), by Equipment 2025 & 2033

- Figure 15: Europe Weight Management Devices Industry Revenue (billion), by Country 2025 & 2033

- Figure 16: Europe Weight Management Devices Industry Volume (K Unit), by Country 2025 & 2033

- Figure 17: Europe Weight Management Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Europe Weight Management Devices Industry Volume Share (%), by Country 2025 & 2033

- Figure 19: Asia Pacific Weight Management Devices Industry Revenue (billion), by Equipment 2025 & 2033

- Figure 20: Asia Pacific Weight Management Devices Industry Volume (K Unit), by Equipment 2025 & 2033

- Figure 21: Asia Pacific Weight Management Devices Industry Revenue Share (%), by Equipment 2025 & 2033

- Figure 22: Asia Pacific Weight Management Devices Industry Volume Share (%), by Equipment 2025 & 2033

- Figure 23: Asia Pacific Weight Management Devices Industry Revenue (billion), by Country 2025 & 2033

- Figure 24: Asia Pacific Weight Management Devices Industry Volume (K Unit), by Country 2025 & 2033

- Figure 25: Asia Pacific Weight Management Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Weight Management Devices Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Middle East and Africa Weight Management Devices Industry Revenue (billion), by Equipment 2025 & 2033

- Figure 28: Middle East and Africa Weight Management Devices Industry Volume (K Unit), by Equipment 2025 & 2033

- Figure 29: Middle East and Africa Weight Management Devices Industry Revenue Share (%), by Equipment 2025 & 2033

- Figure 30: Middle East and Africa Weight Management Devices Industry Volume Share (%), by Equipment 2025 & 2033

- Figure 31: Middle East and Africa Weight Management Devices Industry Revenue (billion), by Country 2025 & 2033

- Figure 32: Middle East and Africa Weight Management Devices Industry Volume (K Unit), by Country 2025 & 2033

- Figure 33: Middle East and Africa Weight Management Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East and Africa Weight Management Devices Industry Volume Share (%), by Country 2025 & 2033

- Figure 35: South America Weight Management Devices Industry Revenue (billion), by Equipment 2025 & 2033

- Figure 36: South America Weight Management Devices Industry Volume (K Unit), by Equipment 2025 & 2033

- Figure 37: South America Weight Management Devices Industry Revenue Share (%), by Equipment 2025 & 2033

- Figure 38: South America Weight Management Devices Industry Volume Share (%), by Equipment 2025 & 2033

- Figure 39: South America Weight Management Devices Industry Revenue (billion), by Country 2025 & 2033

- Figure 40: South America Weight Management Devices Industry Volume (K Unit), by Country 2025 & 2033

- Figure 41: South America Weight Management Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: South America Weight Management Devices Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Weight Management Devices Industry Revenue billion Forecast, by Equipment 2020 & 2033

- Table 2: Global Weight Management Devices Industry Volume K Unit Forecast, by Equipment 2020 & 2033

- Table 3: Global Weight Management Devices Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Weight Management Devices Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 5: Global Weight Management Devices Industry Revenue billion Forecast, by Equipment 2020 & 2033

- Table 6: Global Weight Management Devices Industry Volume K Unit Forecast, by Equipment 2020 & 2033

- Table 7: Global Weight Management Devices Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 8: Global Weight Management Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 9: United States Weight Management Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: United States Weight Management Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 11: Canada Weight Management Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Canada Weight Management Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 13: Mexico Weight Management Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Mexico Weight Management Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 15: Global Weight Management Devices Industry Revenue billion Forecast, by Equipment 2020 & 2033

- Table 16: Global Weight Management Devices Industry Volume K Unit Forecast, by Equipment 2020 & 2033

- Table 17: Global Weight Management Devices Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 18: Global Weight Management Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 19: Germany Weight Management Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Weight Management Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: United Kingdom Weight Management Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: United Kingdom Weight Management Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: France Weight Management Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: France Weight Management Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 25: Italy Weight Management Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Italy Weight Management Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 27: Spain Weight Management Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Spain Weight Management Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 29: Rest of Europe Weight Management Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of Europe Weight Management Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 31: Global Weight Management Devices Industry Revenue billion Forecast, by Equipment 2020 & 2033

- Table 32: Global Weight Management Devices Industry Volume K Unit Forecast, by Equipment 2020 & 2033

- Table 33: Global Weight Management Devices Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 34: Global Weight Management Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 35: China Weight Management Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: China Weight Management Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Japan Weight Management Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Japan Weight Management Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 39: India Weight Management Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: India Weight Management Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 41: Australia Weight Management Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Australia Weight Management Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 43: South Korea Weight Management Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: South Korea Weight Management Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 45: Rest of Asia Pacific Weight Management Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Weight Management Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 47: Global Weight Management Devices Industry Revenue billion Forecast, by Equipment 2020 & 2033

- Table 48: Global Weight Management Devices Industry Volume K Unit Forecast, by Equipment 2020 & 2033

- Table 49: Global Weight Management Devices Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 50: Global Weight Management Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 51: GCC Weight Management Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: GCC Weight Management Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 53: South Africa Weight Management Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: South Africa Weight Management Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 55: Rest of Middle East and Africa Weight Management Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 56: Rest of Middle East and Africa Weight Management Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 57: Global Weight Management Devices Industry Revenue billion Forecast, by Equipment 2020 & 2033

- Table 58: Global Weight Management Devices Industry Volume K Unit Forecast, by Equipment 2020 & 2033

- Table 59: Global Weight Management Devices Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global Weight Management Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 61: Brazil Weight Management Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Brazil Weight Management Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: Argentina Weight Management Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Argentina Weight Management Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 65: Rest of South America Weight Management Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: Rest of South America Weight Management Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Weight Management Devices Industry?

The projected CAGR is approximately 10.9%.

2. Which companies are prominent players in the Weight Management Devices Industry?

Key companies in the market include Fitness World, Johnson Health Technology Co Ltd, Life Fitness, Technogym SpA, Medtronic PLC, Cybex International Inc, Atkins Nutritionals, Olympus Corporation, Life Time Inc, Apollo Endosurgery.

3. What are the main segments of the Weight Management Devices Industry?

The market segments include Equipment.

4. Can you provide details about the market size?

The market size is estimated to be USD 114.79 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Prevalence of Obesity Cases; Increasing Number of Bariatric Surgeries; Launch of New and Advanced Products.

6. What are the notable trends driving market growth?

Cardiovascular Training Equipment is Expected to Witness a Healthy Growth Over the Forecast Period.

7. Are there any restraints impacting market growth?

Deceptive Marketing Practices; High Cost of Equipment.

8. Can you provide examples of recent developments in the market?

In November 2022, Powermax Fitness launched cutting-edge fitness equipment with advanced technology in India. The new launch includes the quality elliptical cross trainer, Powermax EH 760, and commercial and semi-commercial motorized treadmills like Powermax TAC-3000, TAC-3500, TAC-550, and TAC-585.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Weight Management Devices Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Weight Management Devices Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Weight Management Devices Industry?

To stay informed about further developments, trends, and reports in the Weight Management Devices Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence