Key Insights

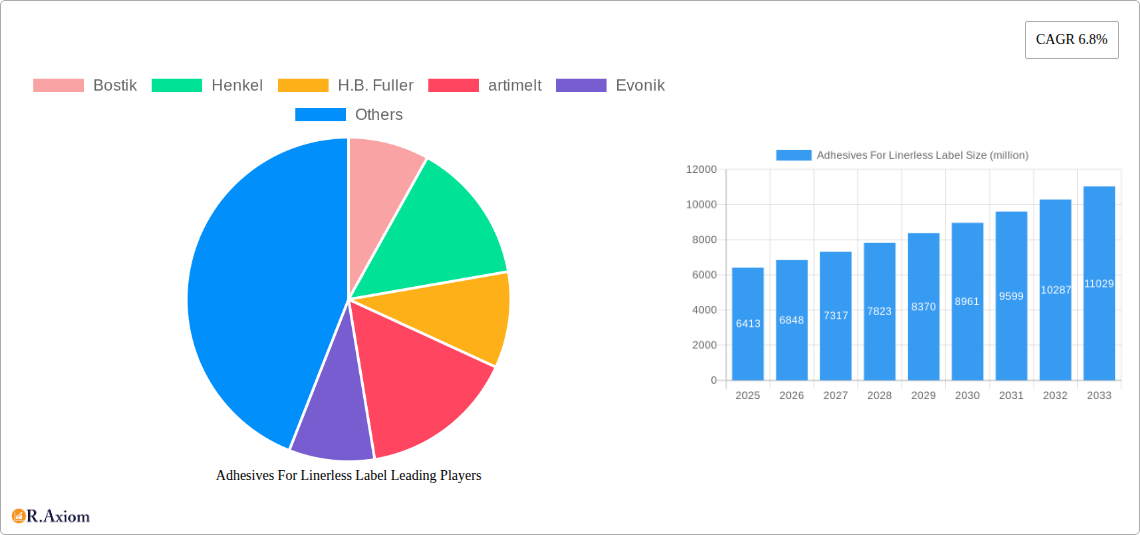

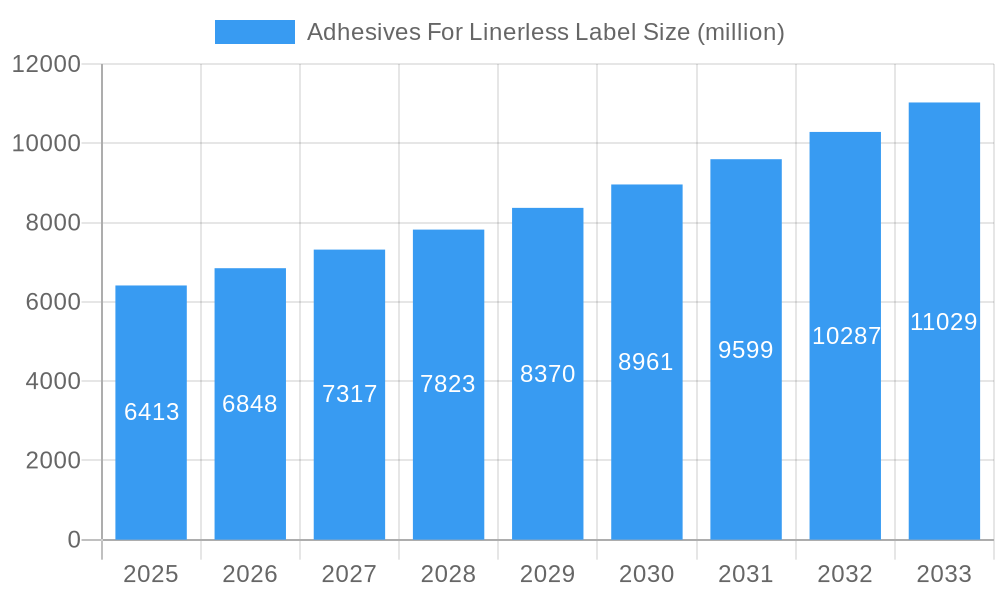

The global market for Adhesives for Linerless Labels is projected to experience robust growth, reaching an estimated market size of approximately USD 6,413 million by 2025. This expansion is driven by the increasing adoption of linerless labels across various industries, including transportation, e-commerce, retail, and food and beverage. Linerless labels offer significant environmental advantages by eliminating the silicone-coated backing liner, thereby reducing waste and material consumption. Furthermore, they provide operational efficiencies through higher label counts per roll, reduced downtime for roll changes, and lower shipping costs due to their lighter weight. The market's Compound Annual Growth Rate (CAGR) of 6.8% signifies a sustained upward trajectory fueled by these compelling benefits and a growing consumer and regulatory push towards sustainable packaging solutions.

Adhesives For Linerless Label Market Size (In Billion)

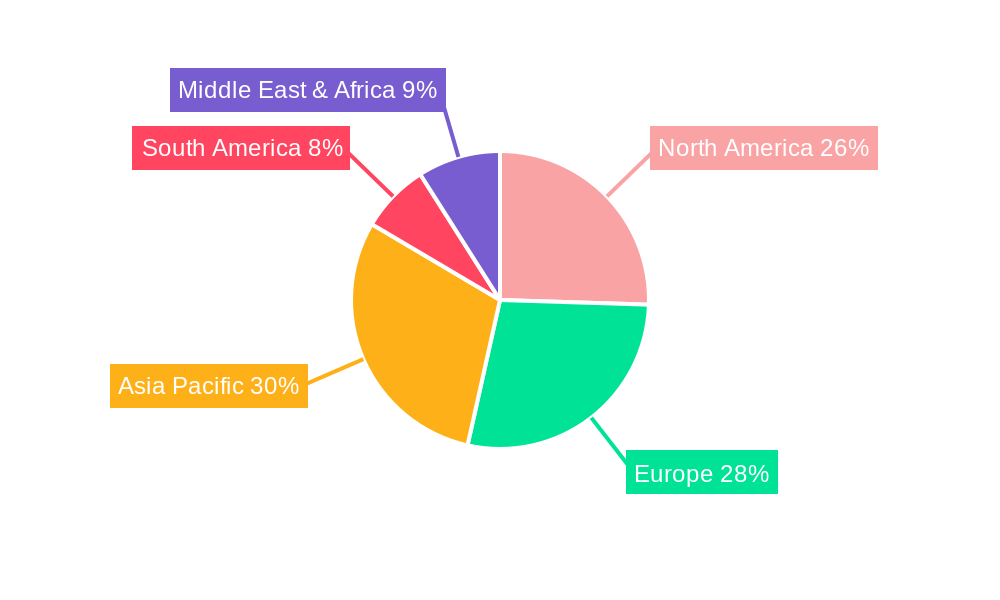

The market is segmented by adhesive type, with Acrylic Adhesives, Rubber-based Adhesives, Silicone Adhesives, and Water-based Adhesives all playing crucial roles. Acrylic and rubber-based adhesives are expected to dominate due to their versatility and cost-effectiveness in a wide range of applications. However, advancements in silicone and water-based adhesive technologies are enabling enhanced performance characteristics like higher temperature resistance and improved environmental profiles, positioning them for future growth. Key industry players such as Bostik, Henkel, and H.B. Fuller are actively investing in research and development to innovate and expand their product portfolios, catering to the evolving demands for specialized linerless label adhesives. Regional analysis indicates strong market penetration in North America and Europe, with the Asia Pacific region expected to witness the fastest growth due to rapid industrialization and expanding e-commerce sectors.

Adhesives For Linerless Label Company Market Share

Sure, here is the SEO-optimized, detailed report description for Adhesives for Linerless Labels:

Adhesives For Linerless Label Market Concentration & Innovation

The adhesives for linerless labels market is characterized by a moderate to high concentration, with key players like Bostik, Henkel, and H.B. Fuller holding significant market shares, estimated to be over 70% combined. Innovation is a crucial differentiator, driven by the demand for sustainable, high-performance adhesive solutions. Key innovation drivers include the development of environmentally friendly formulations, such as water-based and silicone adhesives with reduced VOC content, and the creation of high-tack adhesives capable of adhering to a wider range of substrates, including challenging surfaces found in transportation and e-commerce packaging. Regulatory frameworks, particularly those focused on environmental impact and food contact safety, are increasingly shaping product development. The threat of product substitutes, though present in traditional label formats, is diminishing as linerless technology offers superior efficiency and waste reduction. End-user trends strongly favor sustainability and cost-effectiveness, pushing manufacturers to innovate in adhesive chemistry and application processes. Mergers and acquisitions (M&A) activity, while not exceptionally high, has seen strategic consolidations to gain market access and technological expertise. For instance, artimelt's acquisition of innovative hot-melt adhesive technologies has bolstered its portfolio. The M&A deal value in this niche sector is estimated to be in the tens of millions of dollars, reflecting the specialized nature of the market.

Adhesives For Linerless Label Industry Trends & Insights

The adhesives for linerless labels industry is experiencing robust growth, driven by a confluence of evolving market dynamics and technological advancements. The estimated Compound Annual Growth Rate (CAGR) for this sector is projected to be around 6.5% over the forecast period of 2025–2033. This upward trajectory is underpinned by increasing environmental consciousness and stringent regulations globally, which favor sustainable packaging solutions. Linerless labels inherently reduce waste by eliminating the silicone-coated liner, directly contributing to a circular economy model and making them highly attractive to brands and consumers alike.

Technological disruptions are playing a pivotal role. Innovations in adhesive formulations, particularly in acrylic adhesives and water-based adhesives, are enhancing performance characteristics such as superior adhesion to diverse surfaces, including challenging low-surface-energy plastics used in the food and beverage sector, and improved resistance to moisture and temperature fluctuations. The development of specialized hot-melt adhesives by companies like artimelt has also opened new avenues for high-speed application and enhanced durability. Furthermore, advancements in printing technologies are enabling seamless integration with linerless labeling systems, improving overall operational efficiency for label converters and end-users.

Consumer preferences are increasingly shifting towards brands that demonstrate a commitment to sustainability. This trend is a significant market penetration driver, as companies strive to align their packaging with eco-friendly mandates. The demand for convenience and improved product presentation also fuels the adoption of linerless labels, which offer a premium aesthetic and enhanced brand messaging capabilities.

Competitive dynamics are intense, with established chemical giants like Henkel, Bostik, and H.B. Fuller vying for market dominance. These players are investing heavily in research and development to create next-generation adhesives that offer improved sustainability profiles, enhanced functionality, and cost-competitiveness. The entry of specialized adhesive manufacturers and the strategic partnerships formed between adhesive suppliers and label printing equipment manufacturers are further intensifying the competitive landscape. The global market penetration of linerless labels, though still in its growth phase, is projected to reach approximately 30% by 2033.

Dominant Markets & Segments in Adhesives For Linerless Label

The adhesives for linerless label market exhibits distinct regional dominance and segment preferences, driven by economic factors, regulatory environments, and industry-specific demands.

Dominant Application Segments

The Transportation and E-commerce segment is emerging as a significant growth driver, fueled by the explosive expansion of online retail. This sector demands robust, durable adhesives that can withstand the rigors of shipping and handling. Linerless labels offer advantages such as reduced void fill requirements and enhanced product protection during transit. The Retail sector, encompassing grocery stores and general merchandise, also represents a substantial market. Here, linerless labels are favored for their aesthetic appeal, ability to showcase product information effectively, and their contribution to in-store sustainability initiatives. The Food and Beverage industry is a cornerstone market, where the emphasis on food safety, shelf-life extension, and compliance with stringent packaging regulations makes specialized adhesives crucial. Linerless labels with food-grade compliant adhesives provide a secure and hygienic labeling solution, preventing contamination and ensuring product integrity.

Dominant Adhesive Types

Among the various adhesive types, Acrylic Adhesives hold a dominant position due to their versatility, excellent adhesion to a wide range of substrates, and good resistance to environmental factors like UV light and moisture. They are widely used across most application segments. Water-based Adhesives are gaining significant traction, driven by their low VOC emissions and eco-friendly profile, aligning perfectly with sustainability mandates. These are particularly prevalent in the food and beverage and retail sectors where environmental considerations are paramount. Rubber-based Adhesives offer a good balance of tack and adhesion, making them suitable for general-purpose labeling in the retail and transportation and e-commerce segments, especially where cost-effectiveness is a primary concern. Silicone Adhesives are increasingly important for specialized applications, particularly in the food and beverage and industrial sectors, due to their high temperature resistance and excellent release properties when applied to reusable containers.

The dominance of these segments is further influenced by regional economic policies that encourage sustainable manufacturing, infrastructure development that supports efficient logistics for e-commerce, and consumer preferences for eco-conscious products. For instance, in regions with strong environmental regulations and a mature e-commerce landscape, the adoption rate of linerless labels, particularly those utilizing water-based and acrylic adhesives, is significantly higher.

Adhesives For Linerless Label Product Developments

Product innovations in adhesives for linerless labels are focused on enhancing sustainability, performance, and application efficiency. Key developments include the creation of high-performance water-based adhesives with improved tack and water resistance, catering to the growing demand for eco-friendly solutions in the food and beverage sector. Advancements in acrylic adhesive formulations are yielding improved adhesion to challenging substrates like recycled plastics, critical for the e-commerce segment. artimelt is at the forefront of developing specialized hot-melt adhesives that offer faster curing times and enhanced bond strength for high-speed packaging lines. These innovations provide competitive advantages by reducing material waste, improving operational efficiency, and meeting stricter environmental regulations.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the Adhesives for Linerless Label market, segmented by Application and Type.

Application Segments:

- Transportation and E-commerce: This segment is expected to witness robust growth driven by the expanding online retail sector and the need for durable, space-saving labeling solutions. Market size is estimated to be over $500 million by 2033.

- Retail: A mature market characterized by demand for aesthetic appeal, efficient inventory management, and sustainability. Expected to reach over $700 million by 2033.

- Food and Beverage: A critical segment demanding high safety standards, moisture resistance, and compliance. Projections indicate a market size exceeding $900 million by 2033.

Type Segments:

- Acrylic Adhesives: Dominant type with broad applications, known for versatility and durability. Market size is projected to exceed $1.2 billion by 2033.

- Rubber-based Adhesives: Offers a cost-effective solution for general labeling needs. Expected to reach over $500 million by 2033.

- Silicone Adhesives: Utilized for specialized high-performance applications. Market size is estimated to be over $300 million by 2033.

- Water-based Adhesives: Experiencing significant growth due to their eco-friendly nature. Projected to reach over $800 million by 2033.

Key Drivers of Adhesives For Linerless Label Growth

The adhesives for linerless label market is propelled by several key drivers. The paramount driver is the escalating global demand for sustainable packaging solutions, directly addressed by the waste reduction inherent in linerless labels. Stricter environmental regulations worldwide are compelling manufacturers to adopt eco-friendlier alternatives. Technological advancements in adhesive formulations, particularly in water-based and acrylic chemistries, are enhancing performance and broadening application scope. The rapid growth of the e-commerce sector necessitates efficient, robust, and space-saving packaging, a niche linerless labels effectively fill. Furthermore, the pursuit of operational efficiency and cost reduction in labeling processes by businesses across various sectors, including food and beverage and retail, significantly boosts the adoption of linerless technology.

Challenges in the Adhesives For Linerless Label Sector

Despite the promising growth, the adhesives for linerless label sector faces several challenges. The initial investment cost for specialized linerless printing equipment can be a barrier for some smaller enterprises. While innovative, the development and commercialization of new adhesive formulations, especially those meeting stringent food contact regulations, require significant R&D expenditure. The supply chain for raw materials can be volatile, impacting production costs and availability. Furthermore, educating end-users about the benefits and proper application of linerless labels is an ongoing challenge. Competition from established traditional labeling methods, though diminishing, still exerts pressure, requiring continuous differentiation through performance and sustainability.

Emerging Opportunities in Adhesives For Linerless Label

Emerging opportunities in the adhesives for linerless label market are abundant and multifaceted. The growing consumer demand for traceable and tamper-evident packaging presents opportunities for advanced adhesive solutions with integrated security features. The expansion of the circular economy initiatives globally is creating a strong push for recyclable and biodegradable labeling materials, where linerless options can play a significant role. Innovations in smart packaging technologies, such as embedded sensors, can be integrated with linerless labels, opening new avenues for data collection and supply chain visibility. The increasing adoption of linerless labeling in niche industrial applications, beyond traditional consumer goods, also presents untapped potential. The development of specialized adhesives for extremely demanding environments, such as high-temperature industrial settings or extreme cold storage, offers a promising growth frontier.

Leading Players in the Adhesives For Linerless Label Market

- Bostik

- Henkel

- H.B. Fuller

- artimelt

- Evonik

- HERMA

Key Developments in Adhesives For Linerless Label Industry

- 2023 September: Bostik launched a new range of high-performance, eco-friendly water-based adhesives for linerless labels, enhancing sustainability in the food packaging sector.

- 2024 January: Henkel introduced a novel acrylic adhesive formulation for linerless labels, offering superior adhesion to difficult-to-stick substrates, benefiting the e-commerce industry.

- 2024 March: H.B. Fuller showcased its latest hot-melt adhesive solutions for linerless labels, emphasizing faster curing times and improved application efficiency for label converters.

- 2024 June: artimelt expanded its production capacity for specialized hot-melt adhesives, anticipating increased demand for linerless label applications in the European market.

- 2024 August: Evonik presented its advancements in silicone adhesive technologies for linerless labels, focusing on enhanced durability and temperature resistance for industrial uses.

- 2025 February: HERMA announced a strategic partnership with a leading label printing equipment manufacturer to optimize the integration of their adhesives with cutting-edge linerless printing systems.

Strategic Outlook for Adhesives For Linerless Label Market

The strategic outlook for the adhesives for linerless label market remains highly positive, driven by an unwavering global shift towards sustainable packaging practices and the continuous evolution of adhesive technologies. The increasing adoption of linerless solutions in the booming e-commerce and stringent food and beverage sectors, coupled with ongoing innovation in materials science, particularly in eco-friendly acrylic, water-based, and silicone adhesives, will continue to fuel market expansion. Investments in research and development focused on enhancing adhesive performance, reducing environmental impact, and optimizing application processes will be critical for market leaders. Strategic collaborations between adhesive manufacturers, label converters, and equipment providers will further accelerate market penetration and product development, solidifying linerless labels as a mainstream and indispensable labeling solution.

Adhesives For Linerless Label Segmentation

-

1. Application

- 1.1. Transportation and E-commerce

- 1.2. Retail

- 1.3. Food and Beverage

-

2. Type

- 2.1. Acrylic Adhesives

- 2.2. Rubber-based Adhesives

- 2.3. Silicone Adhesives

- 2.4. Water-based Adhesives

Adhesives For Linerless Label Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Adhesives For Linerless Label Regional Market Share

Geographic Coverage of Adhesives For Linerless Label

Adhesives For Linerless Label REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Transportation and E-commerce

- 5.1.2. Retail

- 5.1.3. Food and Beverage

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Acrylic Adhesives

- 5.2.2. Rubber-based Adhesives

- 5.2.3. Silicone Adhesives

- 5.2.4. Water-based Adhesives

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Adhesives For Linerless Label Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Transportation and E-commerce

- 6.1.2. Retail

- 6.1.3. Food and Beverage

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Acrylic Adhesives

- 6.2.2. Rubber-based Adhesives

- 6.2.3. Silicone Adhesives

- 6.2.4. Water-based Adhesives

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Adhesives For Linerless Label Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Transportation and E-commerce

- 7.1.2. Retail

- 7.1.3. Food and Beverage

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Acrylic Adhesives

- 7.2.2. Rubber-based Adhesives

- 7.2.3. Silicone Adhesives

- 7.2.4. Water-based Adhesives

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Adhesives For Linerless Label Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Transportation and E-commerce

- 8.1.2. Retail

- 8.1.3. Food and Beverage

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Acrylic Adhesives

- 8.2.2. Rubber-based Adhesives

- 8.2.3. Silicone Adhesives

- 8.2.4. Water-based Adhesives

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Adhesives For Linerless Label Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Transportation and E-commerce

- 9.1.2. Retail

- 9.1.3. Food and Beverage

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Acrylic Adhesives

- 9.2.2. Rubber-based Adhesives

- 9.2.3. Silicone Adhesives

- 9.2.4. Water-based Adhesives

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Adhesives For Linerless Label Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Transportation and E-commerce

- 10.1.2. Retail

- 10.1.3. Food and Beverage

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Acrylic Adhesives

- 10.2.2. Rubber-based Adhesives

- 10.2.3. Silicone Adhesives

- 10.2.4. Water-based Adhesives

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Adhesives For Linerless Label Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Transportation and E-commerce

- 11.1.2. Retail

- 11.1.3. Food and Beverage

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Acrylic Adhesives

- 11.2.2. Rubber-based Adhesives

- 11.2.3. Silicone Adhesives

- 11.2.4. Water-based Adhesives

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Bostik

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Henkel

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 H.B. Fuller

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 artimelt

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Evonik

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 HERMA

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.1 Bostik

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Adhesives For Linerless Label Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Adhesives For Linerless Label Revenue (million), by Application 2025 & 2033

- Figure 3: North America Adhesives For Linerless Label Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Adhesives For Linerless Label Revenue (million), by Type 2025 & 2033

- Figure 5: North America Adhesives For Linerless Label Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Adhesives For Linerless Label Revenue (million), by Country 2025 & 2033

- Figure 7: North America Adhesives For Linerless Label Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Adhesives For Linerless Label Revenue (million), by Application 2025 & 2033

- Figure 9: South America Adhesives For Linerless Label Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Adhesives For Linerless Label Revenue (million), by Type 2025 & 2033

- Figure 11: South America Adhesives For Linerless Label Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Adhesives For Linerless Label Revenue (million), by Country 2025 & 2033

- Figure 13: South America Adhesives For Linerless Label Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Adhesives For Linerless Label Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Adhesives For Linerless Label Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Adhesives For Linerless Label Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Adhesives For Linerless Label Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Adhesives For Linerless Label Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Adhesives For Linerless Label Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Adhesives For Linerless Label Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Adhesives For Linerless Label Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Adhesives For Linerless Label Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Adhesives For Linerless Label Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Adhesives For Linerless Label Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Adhesives For Linerless Label Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Adhesives For Linerless Label Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Adhesives For Linerless Label Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Adhesives For Linerless Label Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Adhesives For Linerless Label Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Adhesives For Linerless Label Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Adhesives For Linerless Label Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Adhesives For Linerless Label Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Adhesives For Linerless Label Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Adhesives For Linerless Label Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Adhesives For Linerless Label Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Adhesives For Linerless Label Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Adhesives For Linerless Label Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Adhesives For Linerless Label Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Adhesives For Linerless Label Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Adhesives For Linerless Label Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Adhesives For Linerless Label Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Adhesives For Linerless Label Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Adhesives For Linerless Label Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Adhesives For Linerless Label Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Adhesives For Linerless Label Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Adhesives For Linerless Label Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Adhesives For Linerless Label Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Adhesives For Linerless Label Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Adhesives For Linerless Label Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Adhesives For Linerless Label Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Adhesives For Linerless Label?

The projected CAGR is approximately 6.8%.

2. Which companies are prominent players in the Adhesives For Linerless Label?

Key companies in the market include Bostik, Henkel, H.B. Fuller, artimelt, Evonik, HERMA.

3. What are the main segments of the Adhesives For Linerless Label?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 6413 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Adhesives For Linerless Label," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Adhesives For Linerless Label report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Adhesives For Linerless Label?

To stay informed about further developments, trends, and reports in the Adhesives For Linerless Label, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence