Key Insights

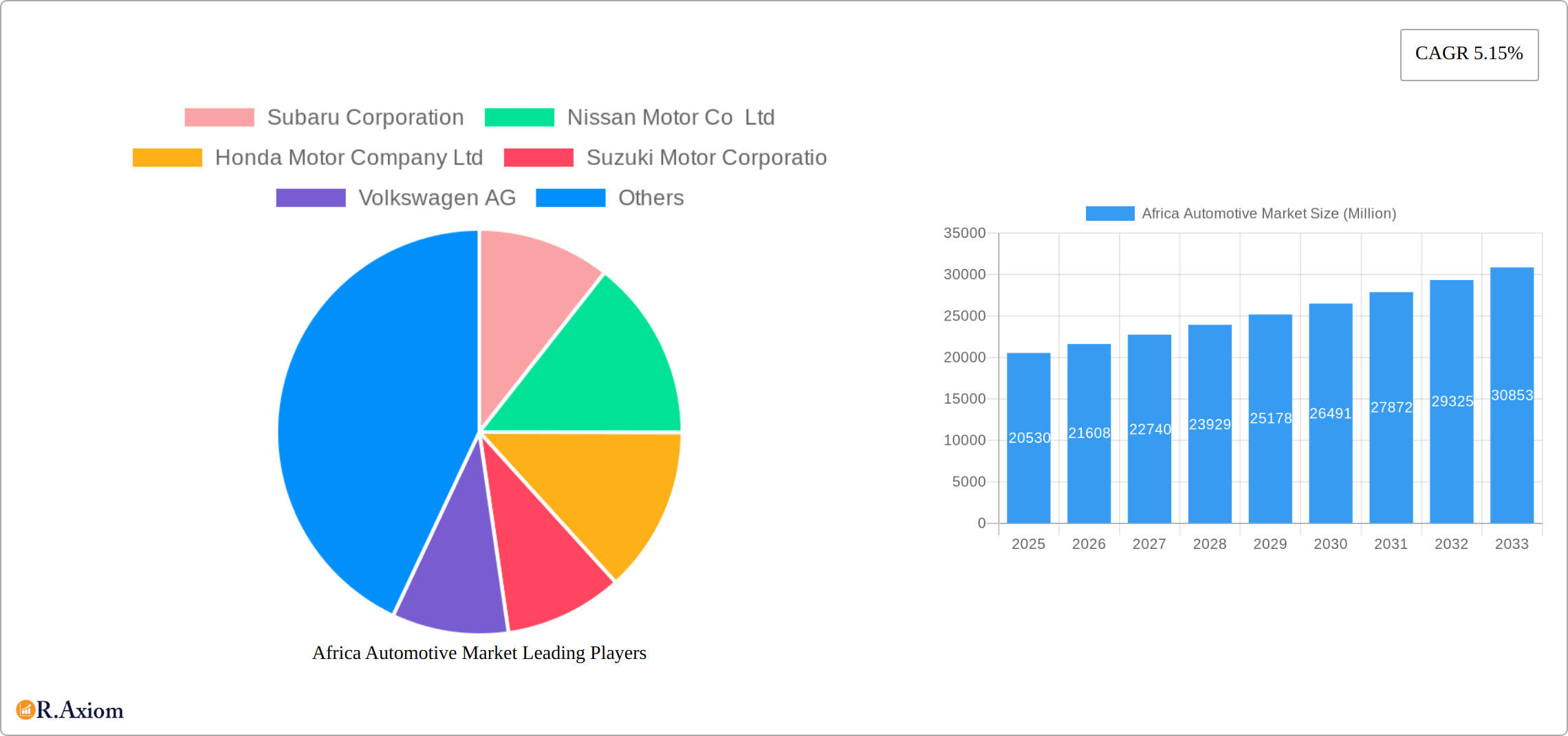

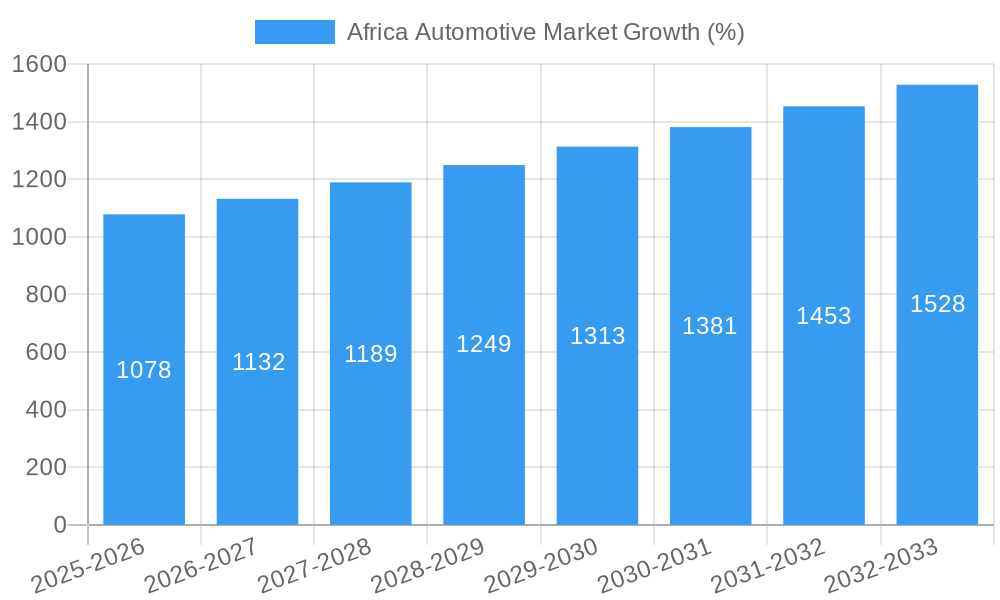

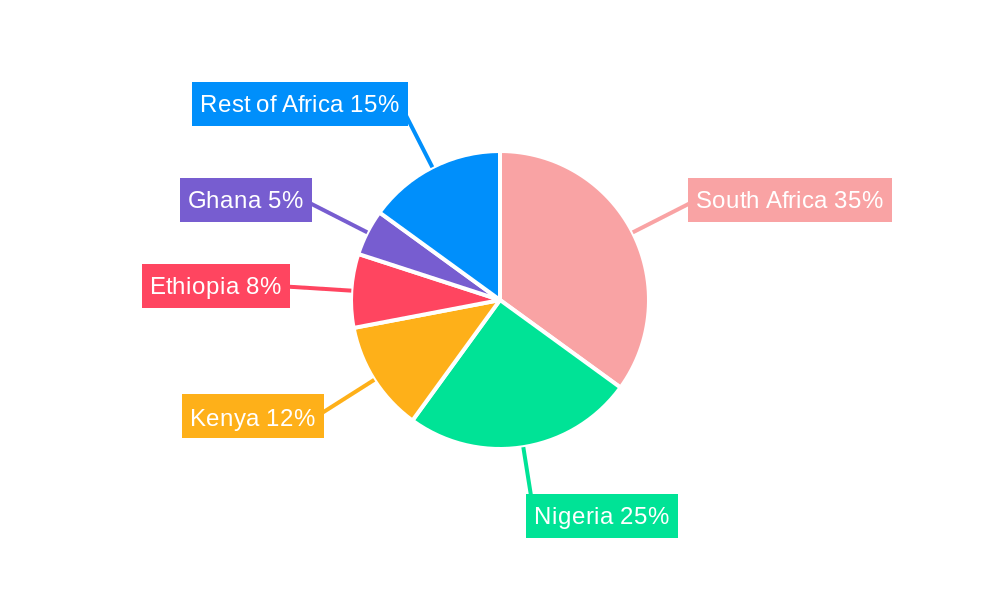

The African automotive market, valued at $20.53 billion in 2025, is projected to experience robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 5.15% from 2025 to 2033. This expansion is driven by several key factors. Rising disposable incomes across several key African nations, coupled with increasing urbanization and infrastructure development, are fueling demand for personal vehicles. Government initiatives aimed at improving road networks and promoting vehicle manufacturing within the continent also contribute significantly. Furthermore, a burgeoning middle class in countries like South Africa, Nigeria, and Kenya is seeking greater mobility and convenience, leading to higher vehicle purchases. The market is segmented by body style (hatchbacks, sedans, SUVs dominating), vehicle type (passenger and commercial), and fuel type (gasoline and diesel remaining prevalent, with gradual uptake of alternative fuels). South Africa, Nigeria, and Kenya represent the largest national markets, reflecting their relatively higher levels of economic development and infrastructure. Leading automotive manufacturers like Toyota, Volkswagen, and Nissan are actively investing in the region, further consolidating market growth.

However, challenges remain. High import duties and taxes in some countries can inflate vehicle prices, limiting accessibility for a large segment of the population. Furthermore, inconsistent regulatory frameworks across different African nations present hurdles for manufacturers and distributors. Fluctuations in currency exchange rates and economic instability also pose risks to market predictability. Despite these obstacles, the long-term outlook for the African automotive market remains positive, driven by sustained economic growth, population expansion, and ongoing infrastructural improvements. The increasing availability of financing options and the introduction of more affordable vehicle models are also anticipated to significantly boost market penetration in the coming years.

Africa Automotive Market: A Comprehensive Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Africa automotive market, offering invaluable insights for stakeholders across the industry. Covering the period 2019-2033, with a focus on 2025, this report meticulously examines market dynamics, segment performance, key players, and future growth potential. The study incorporates detailed segmentation by body style, vehicle type, fuel type, and country, providing a granular understanding of this rapidly evolving market.

Africa Automotive Market Market Concentration & Innovation

This section analyzes the competitive landscape of the African automotive market, assessing market concentration, innovation drivers, and regulatory influences. We examine the impact of mergers and acquisitions (M&A) activities, product substitution trends, and evolving end-user preferences. Key metrics like market share and M&A deal values are included.

Market Concentration: The market exhibits a moderate level of concentration, with a few major players holding significant market share, while numerous smaller players compete for niche segments. Toyota, Nissan, and Volkswagen are amongst the leading players, with estimated combined market share of xx%. However, increased competition from local assemblers and importers of used vehicles presents a dynamic environment.

Innovation Drivers: Rising demand for fuel-efficient vehicles, increasing urbanization, and the growing adoption of connected car technologies are driving innovation within the industry. Investment in electric vehicle (EV) technology is expected to significantly increase in the coming years, influencing future market dynamics.

Regulatory Frameworks: Government regulations regarding vehicle emissions, safety standards, and import tariffs have a significant impact on market access and product development. Variations in regulations across different African nations add to the complexity of the market landscape.

Product Substitutes: The increasing availability of public transport and ride-hailing services presents a growing challenge to private car ownership, especially in urban areas. Additionally, the second-hand vehicle market offers an affordable alternative for many consumers.

End-User Trends: Growing disposable incomes and a preference for SUVs among middle-class consumers are significant market drivers. However, infrastructural constraints and affordability continue to limit overall vehicle penetration.

M&A Activities: While the number of reported M&A activities in the African automotive sector is relatively low compared to other regions, strategic partnerships and joint ventures are gaining momentum. xx Million is the estimated total value of M&A deals in the sector over the past five years.

Africa Automotive Market Industry Trends & Insights

This section delves into the key trends shaping the African automotive market, including market growth drivers, technological disruptions, and shifts in consumer behavior. We examine competitive dynamics and quantify market growth with precise metrics.

The African automotive market experienced a CAGR of xx% during 2019-2024, driven by factors such as increasing urbanization, improving infrastructure in certain regions, and the rising purchasing power of the middle class. Technological advancements, particularly in safety and connectivity features, are enhancing consumer preferences. However, economic instability in some countries and a lack of adequate infrastructure in others pose challenges to market growth. The penetration rate of passenger cars is still relatively low compared to other regions globally, indicating significant untapped market potential. The market is witnessing a gradual shift towards gasoline and diesel vehicles, although alternative fuels are slowly gaining traction. The competitive landscape is characterized by the presence of both established multinational automakers and a growing number of local assemblers. The market is also witnessing an influx of pre-owned vehicle imports which often compete strongly on price with new vehicles. The average transaction value of vehicles is estimated at xx Million.

Dominant Markets & Segments in Africa Automotive Market

This section identifies the dominant regions, countries, and market segments within the African automotive market.

Leading Country: South Africa, owing to its established automotive industry and relatively developed infrastructure, maintains its position as the largest automotive market in Africa. Nigeria is also a significant market, driven by its large population and economic growth.

Leading Body Style: Sports Utility Vehicles (SUVs) are the most dominant body style, appealing to consumer preferences for spaciousness and perceived higher status. The popularity of hatchbacks is also notable in several countries.

Leading Vehicle Type: Passenger cars dominate the market, although the commercial vehicle segment is expected to grow significantly over the forecast period, influenced by the rise in e-commerce and logistics activities.

Leading Fuel Type: Gasoline and diesel fuels remain the dominant fuel types, though the uptake of alternative fuels is slowly growing. Government incentives and investments in charging infrastructure are expected to drive higher adoption of EVs in the longer term.

Key Drivers:

- South Africa: Strong automotive manufacturing base, relatively developed infrastructure, government support for the industry.

- Nigeria: Large population, growing economy, increased urbanisation.

- Kenya: Expanding middle class, increasing infrastructure development, supportive government policies.

- Ethiopia: Growing economy, government focus on infrastructure development, potential for future growth.

- Ghana: Improving infrastructure, increasing urbanization, growing middle class.

Africa Automotive Market Product Developments

The African automotive market witnesses ongoing product innovation, primarily focusing on enhancing fuel efficiency, incorporating advanced safety features, and improving connectivity. Manufacturers are increasingly adapting their vehicle designs and specifications to meet local needs and preferences. The introduction of new models with enhanced features caters to the rising consumer demand for more technologically advanced and comfortable vehicles. The focus on affordability and durability remains paramount, given the specific market conditions in Africa.

Report Scope & Segmentation Analysis

This report provides a comprehensive market segmentation, covering various aspects to give a detailed understanding of the African automotive industry.

By Body Style Type: Hatchbacks, Sedans, SUVs, and Others (Mini-vans, MPVs) are analyzed separately. SUVs are projected to maintain strong growth, while hatchbacks will hold a steady market share. Sedans are expected to see slightly less growth due to increasing demand for SUVs.

By Vehicle Type: Passenger cars and commercial vehicles are explored, assessing their respective market sizes, growth rates, and competitive dynamics. The commercial vehicle segment is expected to show robust growth, owing to expanding logistics and transportation needs.

By Fuel Type: Gasoline, diesel, and other alternative fuels (including electric and hybrid) are analyzed. While gasoline and diesel fuel continue to dominate, alternative fuels will gain traction.

By Country: South Africa, Nigeria, Kenya, Ethiopia, Ghana, and other countries (Tanzania, Angola, Zambia, etc.) are analyzed individually, providing a country-specific overview of market size, growth, and competitive landscape.

Key Drivers of Africa Automotive Market Growth

The growth of the African automotive market is propelled by several key factors. The rising middle class is a primary driver, leading to increased disposable incomes and demand for vehicles. Government initiatives focused on infrastructure development and economic diversification are also creating a favorable environment for market expansion. Technological advancements in vehicle safety and connectivity features are also attracting consumers to purchase newer vehicles.

Challenges in the Africa Automotive Market Sector

Several challenges hinder the growth of the African automotive market. High import duties and tariffs impose significant costs, impacting vehicle affordability. Inadequate infrastructure in certain regions hampers market penetration. Fluctuating exchange rates and economic instability pose significant risks. The presence of large numbers of pre-owned imports present substantial competitive challenges to new vehicles.

Emerging Opportunities in Africa Automotive Market

Despite challenges, significant opportunities exist. The growing demand for commercial vehicles within the logistics and transportation sectors presents a major growth area. Government initiatives to develop infrastructure create a supportive environment for market expansion. The increasing adoption of technology and the rise of the sharing economy present significant opportunities for innovation.

Leading Players in the Africa Automotive Market Market

- Subaru Corporation

- Nissan Motor Co Ltd

- Honda Motor Company Ltd

- Suzuki Motor Corporation

- Volkswagen AG

- Hyundai Motor Company

- Groupe Renault

- Isuzu Motors Ltd

- Toyota Motor Corporation

- Ford Motor Company

Key Developments in Africa Automotive Market Industry

- May 2022: The 2022 Toyota Starlet launched in South Africa at a starting price of SAR 226,200.

Strategic Outlook for Africa Automotive Market Market

The African automotive market holds significant long-term potential. Continued economic growth, infrastructure development, and technological advancements will drive market expansion. The increasing adoption of electric vehicles and the growth of the commercial vehicle segment present compelling opportunities. Adapting to local market conditions and addressing infrastructural challenges will be crucial for sustained success.

Africa Automotive Market Segmentation

-

1. Body Style Type

- 1.1. Hatchback

- 1.2. Sedan

- 1.3. Sports Utility Vehicles

- 1.4. Others (Mini-vans, MPV, etc.)

-

2. Vehicle Type

- 2.1. Passenger Cars

- 2.2. Commercial Vehicles

-

3. Fuel Type

- 3.1. Gasoline

- 3.2. Diesel

- 3.3. Other Alternative Fuels

Africa Automotive Market Segmentation By Geography

-

1. Africa

- 1.1. Nigeria

- 1.2. South Africa

- 1.3. Egypt

- 1.4. Kenya

- 1.5. Ethiopia

- 1.6. Morocco

- 1.7. Ghana

- 1.8. Algeria

- 1.9. Tanzania

- 1.10. Ivory Coast

Africa Automotive Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 5.15% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increased Focus On Safety

- 3.3. Market Restrains

- 3.3.1. High Initial Investment

- 3.4. Market Trends

- 3.4.1. Rising Other Alternative Fuel to Drive Demand in the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Africa Automotive Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Body Style Type

- 5.1.1. Hatchback

- 5.1.2. Sedan

- 5.1.3. Sports Utility Vehicles

- 5.1.4. Others (Mini-vans, MPV, etc.)

- 5.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.2.1. Passenger Cars

- 5.2.2. Commercial Vehicles

- 5.3. Market Analysis, Insights and Forecast - by Fuel Type

- 5.3.1. Gasoline

- 5.3.2. Diesel

- 5.3.3. Other Alternative Fuels

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Africa

- 5.1. Market Analysis, Insights and Forecast - by Body Style Type

- 6. South Africa Africa Automotive Market Analysis, Insights and Forecast, 2019-2031

- 7. Sudan Africa Automotive Market Analysis, Insights and Forecast, 2019-2031

- 8. Uganda Africa Automotive Market Analysis, Insights and Forecast, 2019-2031

- 9. Tanzania Africa Automotive Market Analysis, Insights and Forecast, 2019-2031

- 10. Kenya Africa Automotive Market Analysis, Insights and Forecast, 2019-2031

- 11. Rest of Africa Africa Automotive Market Analysis, Insights and Forecast, 2019-2031

- 12. Competitive Analysis

- 12.1. Market Share Analysis 2024

- 12.2. Company Profiles

- 12.2.1 Subaru Corporation

- 12.2.1.1. Overview

- 12.2.1.2. Products

- 12.2.1.3. SWOT Analysis

- 12.2.1.4. Recent Developments

- 12.2.1.5. Financials (Based on Availability)

- 12.2.2 Nissan Motor Co Ltd

- 12.2.2.1. Overview

- 12.2.2.2. Products

- 12.2.2.3. SWOT Analysis

- 12.2.2.4. Recent Developments

- 12.2.2.5. Financials (Based on Availability)

- 12.2.3 Honda Motor Company Ltd

- 12.2.3.1. Overview

- 12.2.3.2. Products

- 12.2.3.3. SWOT Analysis

- 12.2.3.4. Recent Developments

- 12.2.3.5. Financials (Based on Availability)

- 12.2.4 Suzuki Motor Corporatio

- 12.2.4.1. Overview

- 12.2.4.2. Products

- 12.2.4.3. SWOT Analysis

- 12.2.4.4. Recent Developments

- 12.2.4.5. Financials (Based on Availability)

- 12.2.5 Volkswagen AG

- 12.2.5.1. Overview

- 12.2.5.2. Products

- 12.2.5.3. SWOT Analysis

- 12.2.5.4. Recent Developments

- 12.2.5.5. Financials (Based on Availability)

- 12.2.6 Hyundai Motor Company

- 12.2.6.1. Overview

- 12.2.6.2. Products

- 12.2.6.3. SWOT Analysis

- 12.2.6.4. Recent Developments

- 12.2.6.5. Financials (Based on Availability)

- 12.2.7 Groupe Renault

- 12.2.7.1. Overview

- 12.2.7.2. Products

- 12.2.7.3. SWOT Analysis

- 12.2.7.4. Recent Developments

- 12.2.7.5. Financials (Based on Availability)

- 12.2.8 Isuzu Motors Ltd

- 12.2.8.1. Overview

- 12.2.8.2. Products

- 12.2.8.3. SWOT Analysis

- 12.2.8.4. Recent Developments

- 12.2.8.5. Financials (Based on Availability)

- 12.2.9 Toyota Motor Corporation

- 12.2.9.1. Overview

- 12.2.9.2. Products

- 12.2.9.3. SWOT Analysis

- 12.2.9.4. Recent Developments

- 12.2.9.5. Financials (Based on Availability)

- 12.2.10 Ford Motor Company

- 12.2.10.1. Overview

- 12.2.10.2. Products

- 12.2.10.3. SWOT Analysis

- 12.2.10.4. Recent Developments

- 12.2.10.5. Financials (Based on Availability)

- 12.2.1 Subaru Corporation

List of Figures

- Figure 1: Africa Automotive Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Africa Automotive Market Share (%) by Company 2024

List of Tables

- Table 1: Africa Automotive Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Africa Automotive Market Revenue Million Forecast, by Body Style Type 2019 & 2032

- Table 3: Africa Automotive Market Revenue Million Forecast, by Vehicle Type 2019 & 2032

- Table 4: Africa Automotive Market Revenue Million Forecast, by Fuel Type 2019 & 2032

- Table 5: Africa Automotive Market Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Africa Automotive Market Revenue Million Forecast, by Country 2019 & 2032

- Table 7: South Africa Africa Automotive Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Sudan Africa Automotive Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Uganda Africa Automotive Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Tanzania Africa Automotive Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Kenya Africa Automotive Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Rest of Africa Africa Automotive Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Africa Automotive Market Revenue Million Forecast, by Body Style Type 2019 & 2032

- Table 14: Africa Automotive Market Revenue Million Forecast, by Vehicle Type 2019 & 2032

- Table 15: Africa Automotive Market Revenue Million Forecast, by Fuel Type 2019 & 2032

- Table 16: Africa Automotive Market Revenue Million Forecast, by Country 2019 & 2032

- Table 17: Nigeria Africa Automotive Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: South Africa Africa Automotive Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Egypt Africa Automotive Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Kenya Africa Automotive Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Ethiopia Africa Automotive Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Morocco Africa Automotive Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Ghana Africa Automotive Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Algeria Africa Automotive Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Tanzania Africa Automotive Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Ivory Coast Africa Automotive Market Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Africa Automotive Market?

The projected CAGR is approximately 5.15%.

2. Which companies are prominent players in the Africa Automotive Market?

Key companies in the market include Subaru Corporation, Nissan Motor Co Ltd, Honda Motor Company Ltd, Suzuki Motor Corporatio, Volkswagen AG, Hyundai Motor Company, Groupe Renault, Isuzu Motors Ltd, Toyota Motor Corporation, Ford Motor Company.

3. What are the main segments of the Africa Automotive Market?

The market segments include Body Style Type, Vehicle Type, Fuel Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 20.53 Million as of 2022.

5. What are some drivers contributing to market growth?

Increased Focus On Safety.

6. What are the notable trends driving market growth?

Rising Other Alternative Fuel to Drive Demand in the Market.

7. Are there any restraints impacting market growth?

High Initial Investment.

8. Can you provide examples of recent developments in the market?

In May 2022, The 2022 Toyota Starlet arrived in South Africa, with a starting price of SAR 226,200. The premium hatchback, known as the Toyota Glanza in the U.S., is manufactured in India and exported under the Starlet brand. It was recently relaunched in India with significant changes.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Africa Automotive Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Africa Automotive Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Africa Automotive Market?

To stay informed about further developments, trends, and reports in the Africa Automotive Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence