Key Insights

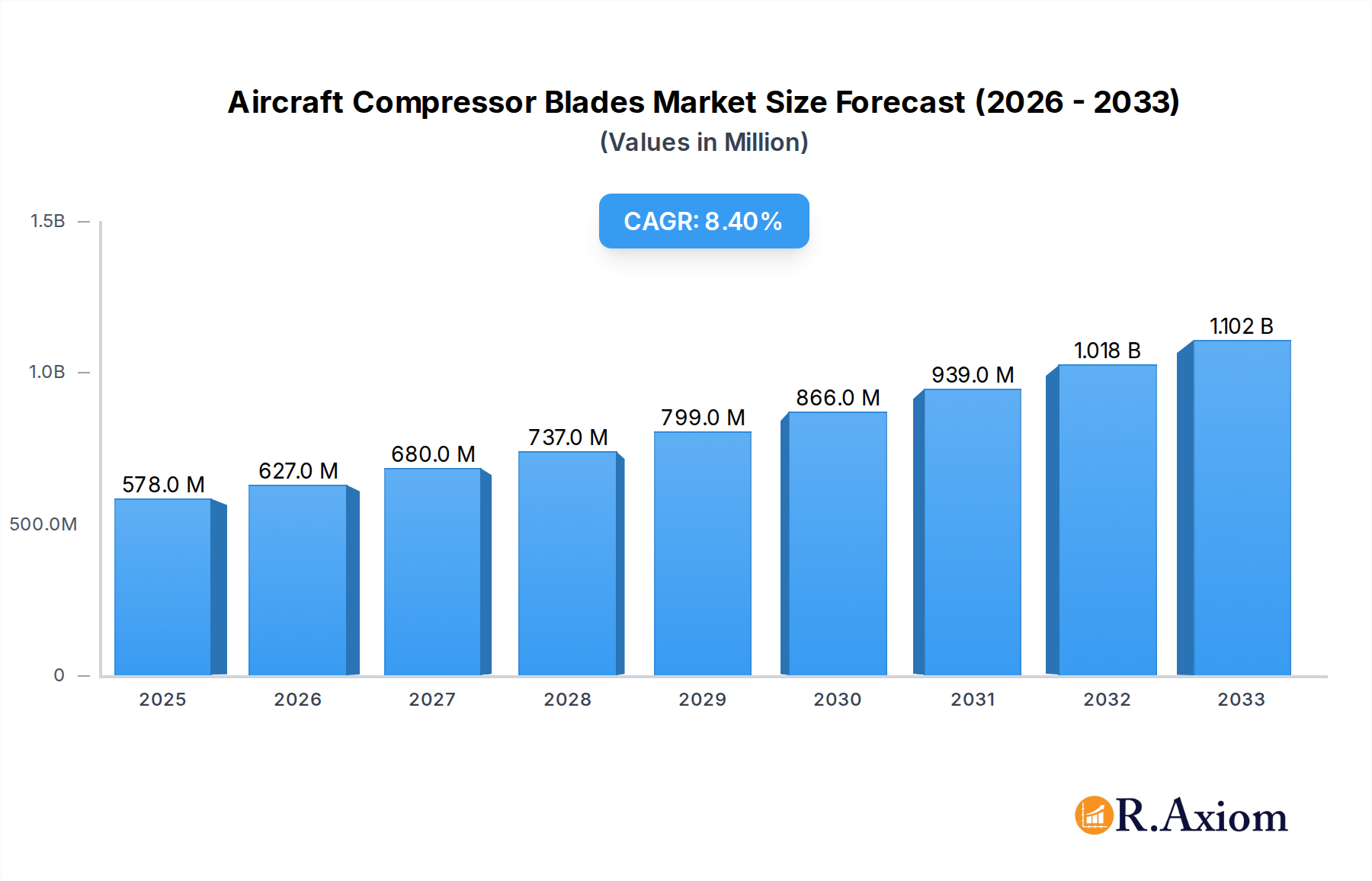

The global aircraft compressor blades market is poised for significant expansion, projected to reach an estimated $578 million in 2025, driven by a robust CAGR of 8.6% through 2033. This substantial growth is underpinned by the increasing demand for air travel, necessitating the production and maintenance of a larger commercial aircraft fleet. Furthermore, ongoing advancements in aerospace technology, including the development of more fuel-efficient engines that rely on sophisticated compressor blade designs, are fueling market momentum. The military aviation sector also contributes significantly, with continuous upgrades and the introduction of new platforms requiring high-performance compressor blades. The market is segmented into high-pressure and low-pressure blades, catering to diverse engine requirements across civil and military applications. Key players like GE Aviation, Rolls Royce, and UTC Aerospace are at the forefront, investing in research and development to create lighter, more durable, and performance-optimized blades.

Aircraft Compressor Blades Market Size (In Million)

The market's trajectory is further shaped by emerging trends such as the integration of advanced materials like titanium alloys and ceramic matrix composites, enhancing blade efficiency and longevity. Innovations in manufacturing processes, including additive manufacturing (3D printing), are also gaining traction, promising reduced lead times and cost efficiencies. While the market enjoys strong growth drivers, certain restraints, such as stringent regulatory approvals and the high cost of raw materials and advanced manufacturing, need to be navigated. Geographically, North America and Europe currently dominate the market due to the presence of major aerospace manufacturers and extensive MRO (Maintenance, Repair, and Overhaul) infrastructure. However, the Asia Pacific region is expected to witness the fastest growth, driven by its expanding aviation sector and increasing investments in domestic aircraft manufacturing capabilities. The study period from 2019 to 2033, with a base year of 2025, provides a comprehensive outlook on this dynamic market.

Aircraft Compressor Blades Company Market Share

This in-depth report provides a detailed analysis of the global Aircraft Compressor Blades market, offering insights into market dynamics, trends, competitive landscape, and future projections. Spanning a study period from 2019 to 2033, with a base year of 2025, this report is an indispensable resource for industry stakeholders seeking to understand the current state and future trajectory of this critical aerospace component sector. The report examines market segmentation, growth drivers, challenges, and emerging opportunities, providing actionable intelligence for strategic decision-making.

Aircraft Compressor Blades Market Concentration & Innovation

The Aircraft Compressor Blades market exhibits a moderate level of concentration, with several key players dominating a significant portion of the global market share. Major industry participants like GE Aviation, Rolls Royce, and UTC Aerospace Systems are continuously investing in research and development, driving innovation in material science, aerodynamic design, and manufacturing processes. Regulatory frameworks, primarily overseen by aviation authorities such as the FAA and EASA, play a crucial role in dictating safety standards and operational requirements, influencing product development and market entry.

- Market Share: Leading companies hold substantial market share, with GE Aviation and Rolls Royce collectively estimated to account for over 40% of the global market.

- Innovation Drivers:

- Demand for enhanced fuel efficiency and reduced emissions.

- Development of advanced composite materials and additive manufacturing techniques.

- Need for increased engine performance and durability.

- Stringent safety and performance certifications.

- Product Substitutes: While direct substitutes are limited due to the specialized nature of compressor blades, advancements in engine architecture and alternative propulsion systems could indirectly impact demand over the long term.

- End-User Trends: A growing emphasis on lighter, stronger, and more resilient compressor blades to meet the evolving demands of both civil and military aircraft.

- M&A Activities: Mergers and acquisitions, with recent deals valued in the range of tens to hundreds of millions, are shaping the competitive landscape, allowing companies to expand their product portfolios and market reach. Notable M&A activities include the acquisition of smaller specialized manufacturers by larger aerospace conglomerates to enhance their integrated engine component offerings.

Aircraft Compressor Blades Industry Trends & Insights

The Aircraft Compressor Blades industry is experiencing robust growth, driven by several interconnected factors. The escalating demand for air travel, particularly in emerging economies, is fueling the expansion of commercial aviation fleets, directly translating into increased demand for new aircraft and, consequently, compressor blades. Furthermore, ongoing advancements in engine technology, aimed at improving fuel efficiency, reducing emissions, and enhancing performance, necessitate the development and adoption of next-generation compressor blade designs and materials. This includes the exploration and integration of advanced composites, ceramic matrix composites (CMCs), and additive manufacturing (3D printing) techniques to produce lighter, stronger, and more heat-resistant blades.

Technological disruptions are playing a pivotal role. The increasing adoption of sophisticated design software and simulation tools allows for the rapid prototyping and optimization of blade aerodynamics, leading to improved performance and reduced development cycles. Additive manufacturing, in particular, is revolutionizing production by enabling the creation of complex geometries that were previously impossible to achieve with traditional methods, offering significant weight savings and design flexibility.

Consumer preferences, in this context, are indirectly driven by the airline industry's focus on operational costs and passenger experience. Airlines are keen on fuel-efficient aircraft, which translates into a demand for engines equipped with the latest compressor blade technology that contributes to significant fuel savings. Moreover, the drive towards quieter and more environmentally friendly aircraft engines is also influencing the design and material choices for compressor blades.

The competitive dynamics within the market are characterized by intense innovation and strategic collaborations. Established aerospace giants are investing heavily in R&D and often acquire smaller, specialized companies to gain access to new technologies or expand their production capabilities. The market penetration of advanced materials and manufacturing processes is steadily increasing, although traditional nickel-based superalloys remain prevalent for many applications. The compound annual growth rate (CAGR) of the Aircraft Compressor Blades market is projected to be in the range of 5% to 7% over the forecast period. This growth is underpinned by the continuous replacement cycles of existing aircraft and the sustained demand for new builds. The market penetration of advanced materials like CMCs is expected to rise significantly as their cost-effectiveness and performance benefits become more widely recognized and adopted.

Dominant Markets & Segments in Aircraft Compressor Blades

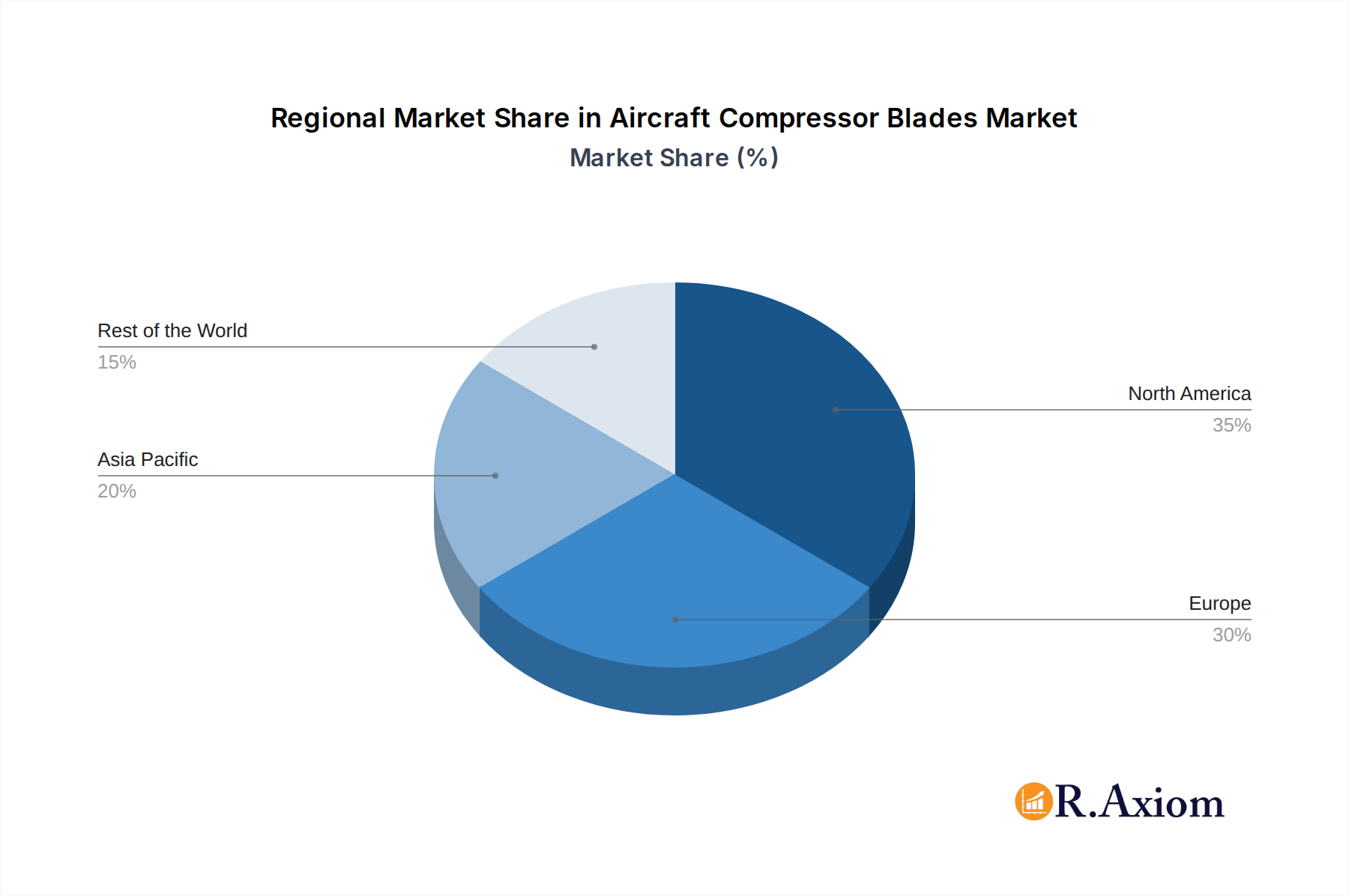

The global Aircraft Compressor Blades market is characterized by strong regional dominance and significant segmentation across different aircraft applications and blade types. The Civil Aircraft segment consistently leads the market, propelled by the ever-increasing global demand for air travel. Factors such as economic growth, rising disposable incomes in developing nations, and expanding tourism industries are key drivers for the expansion of commercial aviation fleets. Major economic policies promoting trade and connectivity, alongside significant investments in airport infrastructure and air traffic control systems, further bolster the growth of the civil aviation sector. The sheer volume of commercial aircraft manufactured and operated worldwide creates a substantial and sustained demand for compressor blades.

- Leading Region: North America currently holds a dominant position in the Aircraft Compressor Blades market, owing to the presence of major aerospace manufacturers, a robust MRO (Maintenance, Repair, and Overhaul) infrastructure, and a high concentration of air traffic. The United States, in particular, is a powerhouse in both aircraft manufacturing and military aviation, contributing significantly to market demand.

- Key Drivers for Civil Aircraft Dominance:

- Economic Growth & Disposable Income: Global economic expansion and rising middle-class populations in emerging economies are fueling air travel demand.

- Fleet Expansion & Replacement: Airlines are continuously expanding their fleets to meet passenger demand and replacing older, less fuel-efficient aircraft.

- Tourism & Globalization: Increased international tourism and global business travel necessitate a larger and more efficient air transport network.

- Low-Cost Carriers: The proliferation of low-cost airlines has made air travel accessible to a wider demographic, driving passenger volumes.

- High-Pressure Compressor Blades: This segment is critical and commands a significant market share due to its integral role in achieving high engine thrust and efficiency. The development of advanced materials and sophisticated designs for high-pressure blades is a constant area of innovation, driven by the need for improved performance under extreme temperatures and pressures. The manufacturing of these blades often involves complex processes and high-value materials, contributing to their market importance.

- Dominance Factors for High-Pressure Blades:

- Engine Performance Requirements: Essential for achieving optimal combustion and maximum thrust in jet engines.

- Extreme Operating Conditions: Require advanced materials and manufacturing techniques to withstand high temperatures and pressures.

- Technological Advancement: Continuous innovation in materials science and aerodynamic design to enhance efficiency and durability.

While the Civil Aircraft segment is the largest, the Military Aircraft segment represents a substantial and strategically important market. Government defense budgets, geopolitical tensions, and the modernization of air forces worldwide drive the demand for advanced military aircraft, which in turn require high-performance compressor blades. The development of specialized blades for fighter jets, bombers, and transport aircraft, often designed for extreme durability and performance in demanding combat environments, contributes to this segment's value.

Aircraft Compressor Blades Product Developments

The Aircraft Compressor Blades market is witnessing continuous product innovation focused on enhancing performance, durability, and efficiency. Companies are actively developing lighter and stronger blades using advanced materials such as nickel-based superalloys, titanium alloys, and emerging ceramic matrix composites (CMCs). Additive manufacturing (3D printing) is also gaining traction, enabling the production of complex geometries with improved aerodynamic profiles and reduced part counts. These innovations lead to significant fuel savings, extended engine life, and reduced maintenance requirements, providing a competitive advantage to manufacturers and airlines alike.

Report Scope & Segmentation Analysis

This report comprehensively analyzes the Aircraft Compressor Blades market, segmenting it by Application and Type. The Application segment includes Civil Aircraft and Military Aircraft, while the Type segment categorizes blades into High-pressure and Low-pressure.

- Civil Aircraft: This segment is projected to maintain its dominance, driven by sustained growth in global air travel demand. Market size is expected to reach over $10,000 million by 2033, with a CAGR of approximately 6.5%. Competitive dynamics are characterized by strong brand loyalty to established engine manufacturers and a focus on lifecycle cost for airlines.

- Military Aircraft: This segment, while smaller, is crucial due to the high-value components and advanced technology involved. Growth is driven by defense spending and modernization programs. Market size is projected to exceed $3,000 million by 2033, with a CAGR of around 5.8%. Competitive dynamics involve long-term government contracts and stringent performance requirements.

- High-pressure: This segment is vital for engine performance and efficiency. It is expected to exhibit strong growth, with market size projected to reach over $8,000 million by 2033, at a CAGR of approximately 7.0%. Key competitive factors include material innovation and advanced manufacturing capabilities.

- Low-pressure: This segment is essential for initial airflow stages and contributes to overall engine efficiency. Market size is anticipated to grow to over $5,000 million by 2033, with a CAGR of around 5.5%. Competition revolves around cost-effectiveness and reliable performance.

Key Drivers of Aircraft Compressor Blades Growth

The growth of the Aircraft Compressor Blades market is propelled by a confluence of technological, economic, and regulatory factors. The relentless pursuit of enhanced fuel efficiency by airlines, driven by rising fuel costs and environmental regulations, is a primary catalyst. This necessitates the development and adoption of advanced compressor blade designs and materials that optimize engine performance and reduce fuel consumption.

- Technological Advancements: Innovations in materials science, including the development of lightweight and high-temperature resistant composites, coupled with advancements in additive manufacturing (3D printing), are enabling the creation of more efficient and durable compressor blades.

- Economic Growth & Air Travel Demand: The steady increase in global air passenger traffic, fueled by economic growth and rising disposable incomes, directly translates into increased demand for new aircraft and subsequent compressor blade requirements.

- Regulatory Mandates: Stringent environmental regulations regarding emissions and noise pollution are pushing engine manufacturers to innovate, leading to a demand for compressor blades that contribute to cleaner and quieter operations.

- Engine Modernization Programs: Ongoing efforts to upgrade existing aircraft engines with more fuel-efficient and performance-enhanced components create a significant aftermarket demand for compressor blades.

Challenges in the Aircraft Compressor Blades Sector

Despite the robust growth prospects, the Aircraft Compressor Blades sector faces several significant challenges. The extremely rigorous certification processes mandated by aviation authorities can be time-consuming and costly, potentially slowing down the adoption of new technologies and materials. Supply chain disruptions, exacerbated by global geopolitical events and the specialized nature of raw materials, can lead to production delays and increased costs.

- Stringent Regulatory Hurdles: Obtaining certifications for new blade designs and materials from aviation authorities like the FAA and EASA requires extensive testing and documentation, adding significant time and cost.

- Supply Chain Volatility: The reliance on specialized raw materials and complex manufacturing processes makes the supply chain vulnerable to disruptions, impacting production schedules and costs.

- High Research & Development Costs: Developing next-generation compressor blades requires substantial investment in R&D, including advanced simulation tools, material testing, and prototype manufacturing.

- Intense Competition & Pricing Pressures: The market is highly competitive, with established players and emerging manufacturers vying for market share, leading to significant pricing pressures.

Emerging Opportunities in Aircraft Compressor Blades

The Aircraft Compressor Blades market is rife with emerging opportunities for innovation and growth. The increasing adoption of additive manufacturing (3D printing) presents a significant opportunity for producing complex blade geometries more efficiently and cost-effectively, leading to lighter components and reduced assembly. The development and integration of advanced materials like Ceramic Matrix Composites (CMCs) offer the potential for higher operating temperatures, leading to improved engine performance and fuel efficiency.

- Additive Manufacturing (3D Printing): Enables the creation of complex, optimized designs, reducing weight and part count.

- Advanced Materials (e.g., CMCs): Offer superior heat resistance and durability, leading to higher engine efficiency.

- Sustainable Aviation Fuel (SAF) Compatibility: Development of blades optimized for engines running on SAF, supporting the industry's decarbonization efforts.

- Digitalization & AI in Design & Manufacturing: Leveraging AI and advanced simulation for faster design cycles, predictive maintenance, and optimized manufacturing processes.

Leading Players in the Aircraft Compressor Blades Market

- BTL

- GE Aviation

- GKN Aerospace

- Rolls Royce

- Turbocam International

- UTC Aerospace

- Chromalloy

- Hi-Tek Manufacturing

- Moeller Aerospace

- Snecma

- C*Blade S.p.a. Forging & Manufacturing

- Stork

- Pacific Sky Supply, Inc.

Key Developments in Aircraft Compressor Blades Industry

- 2023: GE Aviation announces significant advancements in CMC blade technology for its LEAP engines, promising enhanced fuel efficiency and durability.

- 2022: Rolls Royce unveils its latest generation of compressor blades for its UltraFan engine demonstrator, incorporating novel aerodynamic designs and advanced materials.

- 2021: GKN Aerospace invests heavily in expanding its additive manufacturing capabilities for aerospace components, including compressor blades.

- 2020: UTC Aerospace Systems (now part of Collins Aerospace) showcases breakthroughs in blade cooling technologies, extending operational life under extreme conditions.

- 2019: Snecma (Safran Aircraft Engines) highlights the successful implementation of AI-driven design optimization for its next-generation compressor blades.

Strategic Outlook for Aircraft Compressor Blades Market

The strategic outlook for the Aircraft Compressor Blades market remains highly positive, driven by the sustained growth in global air travel and the imperative for more fuel-efficient and environmentally friendly aircraft engines. Key growth catalysts include the continuous demand for new aircraft, the ongoing modernization of existing fleets, and the relentless pursuit of technological innovation. Companies that can effectively leverage advancements in materials science, additive manufacturing, and digital technologies will be well-positioned to capture market share. Strategic partnerships, focused R&D investments, and a keen understanding of evolving regulatory landscapes will be crucial for navigating the competitive environment and capitalizing on emerging opportunities within this dynamic sector of the aerospace industry.

Aircraft Compressor Blades Segmentation

-

1. Application

- 1.1. Civil Aircraft

- 1.2. Military Aircraft

-

2. Types

- 2.1. High-pressure

- 2.2. Low-pressure

Aircraft Compressor Blades Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Aircraft Compressor Blades Regional Market Share

Geographic Coverage of Aircraft Compressor Blades

Aircraft Compressor Blades REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Civil Aircraft

- 5.1.2. Military Aircraft

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. High-pressure

- 5.2.2. Low-pressure

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Aircraft Compressor Blades Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Civil Aircraft

- 6.1.2. Military Aircraft

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. High-pressure

- 6.2.2. Low-pressure

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Aircraft Compressor Blades Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Civil Aircraft

- 7.1.2. Military Aircraft

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. High-pressure

- 7.2.2. Low-pressure

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Aircraft Compressor Blades Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Civil Aircraft

- 8.1.2. Military Aircraft

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. High-pressure

- 8.2.2. Low-pressure

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Aircraft Compressor Blades Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Civil Aircraft

- 9.1.2. Military Aircraft

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. High-pressure

- 9.2.2. Low-pressure

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Aircraft Compressor Blades Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Civil Aircraft

- 10.1.2. Military Aircraft

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. High-pressure

- 10.2.2. Low-pressure

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Aircraft Compressor Blades Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Civil Aircraft

- 11.1.2. Military Aircraft

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. High-pressure

- 11.2.2. Low-pressure

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 BTL

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 GE Aviation

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 GKN Aerospace

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Rolls Royce

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Turbocam International

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 UTC Aerospace

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Chromalloy

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Hi-Tek Manufacturing

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Moeller Aerospace

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Snecma

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 C*Blade S.p.a. Forging & Manufacturing

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Stork

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Pacific Sky Supply

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Inc.

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 BTL

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Aircraft Compressor Blades Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Aircraft Compressor Blades Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Aircraft Compressor Blades Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Aircraft Compressor Blades Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Aircraft Compressor Blades Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Aircraft Compressor Blades Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Aircraft Compressor Blades Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Aircraft Compressor Blades Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Aircraft Compressor Blades Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Aircraft Compressor Blades Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Aircraft Compressor Blades Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Aircraft Compressor Blades Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Aircraft Compressor Blades Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Aircraft Compressor Blades Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Aircraft Compressor Blades Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Aircraft Compressor Blades Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Aircraft Compressor Blades Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Aircraft Compressor Blades Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Aircraft Compressor Blades Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Aircraft Compressor Blades Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Aircraft Compressor Blades Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Aircraft Compressor Blades Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Aircraft Compressor Blades Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Aircraft Compressor Blades Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Aircraft Compressor Blades Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Aircraft Compressor Blades Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Aircraft Compressor Blades Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Aircraft Compressor Blades Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Aircraft Compressor Blades Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Aircraft Compressor Blades Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Aircraft Compressor Blades Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Aircraft Compressor Blades Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Aircraft Compressor Blades Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Aircraft Compressor Blades Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Aircraft Compressor Blades Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Aircraft Compressor Blades Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Aircraft Compressor Blades Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Aircraft Compressor Blades Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Aircraft Compressor Blades Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Aircraft Compressor Blades Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Aircraft Compressor Blades Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Aircraft Compressor Blades Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Aircraft Compressor Blades Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Aircraft Compressor Blades Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Aircraft Compressor Blades Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Aircraft Compressor Blades Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Aircraft Compressor Blades Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Aircraft Compressor Blades Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Aircraft Compressor Blades Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Aircraft Compressor Blades Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Aircraft Compressor Blades?

The projected CAGR is approximately 8.6%.

2. Which companies are prominent players in the Aircraft Compressor Blades?

Key companies in the market include BTL, GE Aviation, GKN Aerospace, Rolls Royce, Turbocam International, UTC Aerospace, Chromalloy, Hi-Tek Manufacturing, Moeller Aerospace, Snecma, C*Blade S.p.a. Forging & Manufacturing, Stork, Pacific Sky Supply, Inc..

3. What are the main segments of the Aircraft Compressor Blades?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Aircraft Compressor Blades," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Aircraft Compressor Blades report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Aircraft Compressor Blades?

To stay informed about further developments, trends, and reports in the Aircraft Compressor Blades, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence