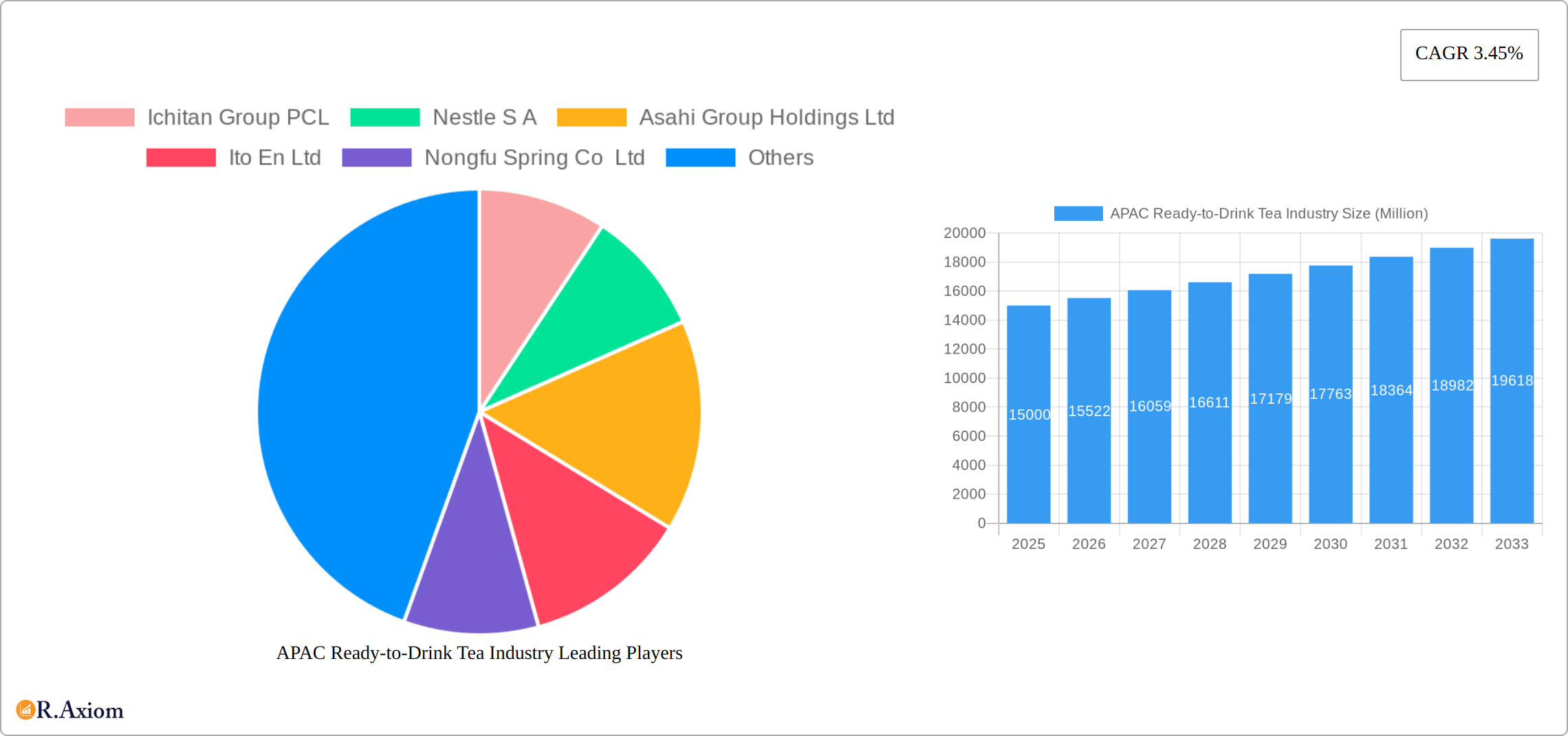

Key Insights

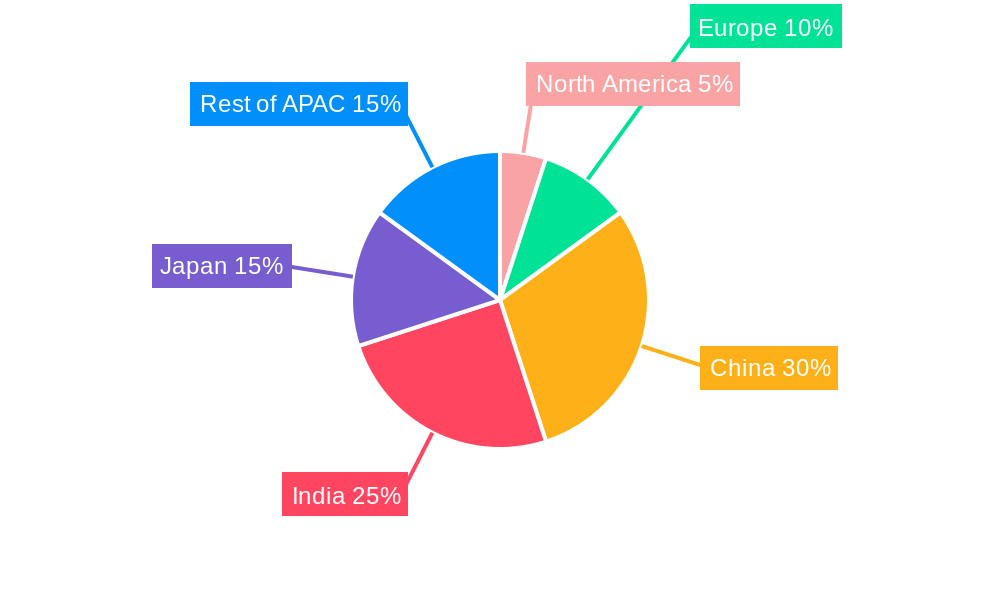

The Asia-Pacific Ready-to-Drink (RTD) tea market is experiencing robust growth, driven by increasing health consciousness, rising disposable incomes, and a preference for convenient beverages. The market, valued at approximately $XX million in 2025 (assuming a logical estimation based on the provided CAGR and market size), is projected to expand at a Compound Annual Growth Rate (CAGR) of 3.45% from 2025 to 2033. This growth is fueled by several key trends, including the increasing popularity of green and herbal teas, the expansion of distribution channels beyond traditional off-trade outlets (like supermarkets and convenience stores) into e-commerce and on-trade establishments (restaurants, cafes), and the introduction of innovative product formats like aseptic packaging that extends shelf life. However, the market faces some restraints including fluctuating raw material prices and intense competition among established players and emerging brands. Within the APAC region, countries like China, India, and Japan are major contributors, due to their large populations and established tea-drinking cultures. The market is segmented by packaging type (aseptic, glass bottles, metal cans, PET bottles), tea type (green tea, herbal tea, iced tea, other RTD teas), and distribution channel (off-trade, on-trade). Key players in this dynamic market include Ichitan Group PCL, Nestle S.A., Asahi Group Holdings Ltd., and others, continually innovating to cater to evolving consumer preferences and expand their market share.

The projected growth signifies significant opportunities for companies focusing on premiumization, sustainable packaging, and product diversification. The increasing demand for functional beverages infused with health benefits, like added vitamins or antioxidants, presents another key avenue for expansion. Furthermore, strategic partnerships and collaborations within the supply chain, including tea sourcing and distribution networks, are expected to shape the industry landscape. The ongoing economic development across several APAC nations, combined with the growing middle class, will continue to bolster the demand for convenient and readily available RTD tea options, further driving market expansion in the forecast period (2025-2033). Understanding regional nuances and consumer preferences across diverse markets within APAC will be vital for companies seeking to capitalize on this growth potential.

This comprehensive report provides an in-depth analysis of the Asia-Pacific (APAC) ready-to-drink (RTD) tea industry, covering the period 2019-2033. It offers actionable insights for industry stakeholders, including manufacturers, distributors, investors, and market entrants. The report leverages extensive market research and data analysis to provide a detailed understanding of market trends, competitive dynamics, and future growth opportunities. With a focus on key players like Ichitan Group PCL, Nestle S.A., Asahi Group Holdings Ltd, and Coca-Cola, the report provides a granular view of the market's evolution and future prospects. The total market size is predicted to reach xx Million by 2033.

APAC Ready-to-Drink Tea Industry Market Concentration & Innovation

This section analyzes the market concentration, examining the market share of key players such as Nestle S.A., Coca-Cola, and Uni-President Enterprises Corp. We assess the innovative drivers shaping the industry, including the rising demand for functional and premium teas, along with evolving consumer preferences. Regulatory frameworks impacting the RTD tea market across various APAC countries are also explored. The report includes an analysis of product substitutes, such as fruit juices and other beverages, and evaluates their impact on market share. Finally, the report details end-user trends, highlighting the growing preference for convenient and on-the-go beverages, and provides a comprehensive overview of recent mergers and acquisitions (M&A) activities within the industry, including deal values (where available). Examples of M&A activity could include (but are not limited to) smaller acquisitions of niche tea brands by larger corporations, consolidating market share.

- Market Concentration: The APAC RTD tea market exhibits a moderately concentrated structure, with a few major players holding significant market share. The exact figures are subject to detailed analysis within the full report.

- Innovation Drivers: Health and wellness trends, increasing disposable incomes, and the demand for premiumization are major drivers of innovation.

- Regulatory Landscape: Varying regulations across different APAC countries influence product formulations and labeling requirements.

- Product Substitutes: Fruit juices, carbonated soft drinks, and other functional beverages compete with RTD tea.

- M&A Activity: The report includes a detailed analysis of significant M&A deals within the APAC RTD tea industry, including deal values and their impact on market dynamics (xx Million in total deal value predicted for the period).

APAC Ready-to-Drink Tea Industry Industry Trends & Insights

This section delves into the key trends and insights shaping the APAC RTD tea market. The report examines market growth drivers, including rising consumer demand, increasing urbanization, and changing lifestyles. We analyze technological disruptions, such as advancements in packaging and distribution, and their impact on market dynamics. Consumer preferences for specific tea types (e.g., green tea, herbal tea, iced tea) and flavors are detailed, alongside an evaluation of emerging consumer trends like demand for organic and sustainably sourced teas. The competitive landscape is thoroughly analyzed, examining the strategies employed by leading players. The report will include a detailed analysis projecting the Compound Annual Growth Rate (CAGR) and market penetration rates for various segments.

Dominant Markets & Segments in APAC Ready-to-Drink Tea Industry

This section identifies the leading regions, countries, and segments within the APAC RTD tea market. Dominant segments are analyzed across packaging types (aseptic packages, glass bottles, metal cans, PET bottles), soft drink types (green tea, herbal tea, iced tea, other RTD tea), and distribution channels (off-trade, on-trade). Key drivers for dominance in each segment are outlined. For example, the high population density and rising disposable incomes in China contribute significantly to its dominance in the overall market. The report offers detailed insights into the market dynamics of each region and segment, exploring aspects like consumer preferences, distribution networks, and regulatory influences.

- China: High population, rising disposable incomes, and established distribution networks contribute to China's dominance.

- India: Large population, growing middle class, and increasing health consciousness drive market growth.

- Japan: Mature market with high per capita consumption and a preference for specific tea types (e.g., green tea).

- PET Bottles: Dominant packaging due to convenience and cost-effectiveness.

- Green Tea: Highest demand due to health benefits and established consumer preference.

- Off-Trade: The dominant distribution channel due to widespread retail availability.

APAC Ready-to-Drink Tea Industry Product Developments

This section details recent innovations in the APAC ready-to-drink (RTD) tea market, focusing on new product launches, exciting flavor profiles, and functional enhancements such as added vitamins, antioxidants, and adaptogens. We analyze the competitive advantages these innovations offer, including superior taste, unmatched convenience, and compelling health benefits. The analysis emphasizes technological advancements driving product development, such as sustainable packaging materials (e.g., plant-based plastics, recycled content) and innovative manufacturing processes designed for efficiency and reduced environmental impact. A crucial element of this section is assessing the market fit of new products, carefully considering evolving consumer preferences, emerging health trends, and the overall competitive landscape.

Report Scope & Segmentation Analysis

This report provides a granular segmentation of the APAC RTD tea market across several key dimensions: packaging type (aseptic packages, glass bottles, metal cans, PET bottles, and emerging sustainable options), beverage type (green tea, black tea, herbal tea, iced tea, fruit-infused teas, functional teas, and other RTD tea variations), distribution channel (off-trade encompassing supermarkets, convenience stores, and online retailers; and on-trade including restaurants, cafes, and foodservice establishments), and country (Australia, China, India, Indonesia, Japan, Malaysia, South Korea, Thailand, Vietnam, and the Rest of Asia-Pacific). For each segment, we offer detailed growth projections, precise market sizing, and a thorough analysis of competitive dynamics, providing a comprehensive understanding of the market structure and its future growth trajectory. This segmentation allows for a deep dive into specific market niches and opportunities.

Key Drivers of APAC Ready-to-Drink Tea Industry Growth

The robust growth of the APAC RTD tea market is fueled by a confluence of factors. These include the rise in disposable incomes across many APAC countries, leading to increased spending on premium and convenient beverages; the burgeoning popularity of health-conscious beverages, with consumers actively seeking functional drinks that offer both taste and health benefits; the expansion of retail infrastructure, providing wider access to RTD tea products; and significant advancements in packaging technology, resulting in more convenient, sustainable, and appealing packaging solutions. Furthermore, government initiatives promoting healthy lifestyles and reducing sugar consumption are creating a favorable regulatory environment for the growth of RTD tea.

Challenges in the APAP Ready-to-Drink Tea Industry Sector

Challenges include fluctuating raw material prices, intense competition from other beverage categories, stringent regulatory compliance requirements, and supply chain disruptions. These factors can impact profitability and market share. Competition from established players and the entry of new entrants also pose significant challenges.

Emerging Opportunities in APAC Ready-to-Drink Tea Industry

The market offers promising opportunities for companies focusing on premiumization, functional teas (e.g., with added vitamins or antioxidants), organic and sustainably sourced tea, and innovative packaging solutions. Expanding into untapped markets within the APAC region also presents significant opportunities for growth.

Leading Players in the APAC Ready-to-Drink Tea Industry Market

- Ichitan Group PCL

- Nestle S.A.

- Asahi Group Holdings Ltd

- Ito En Ltd

- Nongfu Spring Co Ltd

- Tata Consumer Products Ltd

- PT Anggada Putra Rekso Mulia

- Suntory Holdings Limited

- JDB Group

- Tingyi (Cayman Islands) Holding Corporation

- The Coca-Cola Company

- Uni-President Enterprises Corp

- Kirin Holdings Company Limited

- Thai Beverages PCL

- Sapporo Holdings Limited

Key Developments in APAC Ready-to-Drink Tea Industry Industry

- November 2023: The Coca-Cola Company's ChaiChun brand expands its footprint with a new flagship store in Delhi, India, signifying a commitment to the growing Indian market.

- September 2022: Coca-Cola successfully launches Ayataka Cafe Matcha Latte in Japan, capitalizing on the growing popularity of matcha and café-style beverages.

- June 2021: Sermsuk's launch of a vitamin-infused carbonated soft drink in Thailand demonstrates the trend towards functional beverages with added health benefits.

- [Add more recent developments here with dates and brief descriptions]

Strategic Outlook for APAC Ready-to-Drink Tea Industry Market

The APAC RTD tea market presents significant growth opportunities driven by evolving consumer preferences towards healthier, more convenient, and premium beverages; continuous technological advancements in packaging and production; and rising disposable incomes across the region. To succeed in this dynamic market, strategic investments in research and development (focusing on innovative flavors, functional benefits, and sustainable packaging), robust distribution networks, and effective marketing campaigns targeting specific consumer segments are crucial. A strong emphasis on functional and premium teas, coupled with strategic expansion into new and underserved markets, will be key differentiators in determining future market leadership.

APAC Ready-to-Drink Tea Industry Segmentation

-

1. Soft Drink Type

- 1.1. Green Tea

- 1.2. Herbal Tea

- 1.3. Iced Tea

- 1.4. Other RTD Tea

-

2. Packaging Type

- 2.1. Aseptic packages

- 2.2. Glass Bottles

- 2.3. Metal Can

- 2.4. PET Bottles

-

3. Distribution Channel

-

3.1. Off-trade

- 3.1.1. Convenience Stores

- 3.1.2. Online Retail

- 3.1.3. Supermarket/Hypermarket

- 3.1.4. Others

- 3.2. On-trade

-

3.1. Off-trade

APAC Ready-to-Drink Tea Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

APAC Ready-to-Drink Tea Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 3.45% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rising Trend of Ingestible Beauty Products; Growing demand for Nutrient-Enriched Cosmetic Products

- 3.3. Market Restrains

- 3.3.1. Availability of Counterfeit Beauty Supplements Products

- 3.4. Market Trends

- 3.4.1. OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global APAC Ready-to-Drink Tea Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Soft Drink Type

- 5.1.1. Green Tea

- 5.1.2. Herbal Tea

- 5.1.3. Iced Tea

- 5.1.4. Other RTD Tea

- 5.2. Market Analysis, Insights and Forecast - by Packaging Type

- 5.2.1. Aseptic packages

- 5.2.2. Glass Bottles

- 5.2.3. Metal Can

- 5.2.4. PET Bottles

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Off-trade

- 5.3.1.1. Convenience Stores

- 5.3.1.2. Online Retail

- 5.3.1.3. Supermarket/Hypermarket

- 5.3.1.4. Others

- 5.3.2. On-trade

- 5.3.1. Off-trade

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. South America

- 5.4.3. Europe

- 5.4.4. Middle East & Africa

- 5.4.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Soft Drink Type

- 6. North America APAC Ready-to-Drink Tea Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Soft Drink Type

- 6.1.1. Green Tea

- 6.1.2. Herbal Tea

- 6.1.3. Iced Tea

- 6.1.4. Other RTD Tea

- 6.2. Market Analysis, Insights and Forecast - by Packaging Type

- 6.2.1. Aseptic packages

- 6.2.2. Glass Bottles

- 6.2.3. Metal Can

- 6.2.4. PET Bottles

- 6.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.3.1. Off-trade

- 6.3.1.1. Convenience Stores

- 6.3.1.2. Online Retail

- 6.3.1.3. Supermarket/Hypermarket

- 6.3.1.4. Others

- 6.3.2. On-trade

- 6.3.1. Off-trade

- 6.1. Market Analysis, Insights and Forecast - by Soft Drink Type

- 7. South America APAC Ready-to-Drink Tea Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Soft Drink Type

- 7.1.1. Green Tea

- 7.1.2. Herbal Tea

- 7.1.3. Iced Tea

- 7.1.4. Other RTD Tea

- 7.2. Market Analysis, Insights and Forecast - by Packaging Type

- 7.2.1. Aseptic packages

- 7.2.2. Glass Bottles

- 7.2.3. Metal Can

- 7.2.4. PET Bottles

- 7.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.3.1. Off-trade

- 7.3.1.1. Convenience Stores

- 7.3.1.2. Online Retail

- 7.3.1.3. Supermarket/Hypermarket

- 7.3.1.4. Others

- 7.3.2. On-trade

- 7.3.1. Off-trade

- 7.1. Market Analysis, Insights and Forecast - by Soft Drink Type

- 8. Europe APAC Ready-to-Drink Tea Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Soft Drink Type

- 8.1.1. Green Tea

- 8.1.2. Herbal Tea

- 8.1.3. Iced Tea

- 8.1.4. Other RTD Tea

- 8.2. Market Analysis, Insights and Forecast - by Packaging Type

- 8.2.1. Aseptic packages

- 8.2.2. Glass Bottles

- 8.2.3. Metal Can

- 8.2.4. PET Bottles

- 8.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.3.1. Off-trade

- 8.3.1.1. Convenience Stores

- 8.3.1.2. Online Retail

- 8.3.1.3. Supermarket/Hypermarket

- 8.3.1.4. Others

- 8.3.2. On-trade

- 8.3.1. Off-trade

- 8.1. Market Analysis, Insights and Forecast - by Soft Drink Type

- 9. Middle East & Africa APAC Ready-to-Drink Tea Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Soft Drink Type

- 9.1.1. Green Tea

- 9.1.2. Herbal Tea

- 9.1.3. Iced Tea

- 9.1.4. Other RTD Tea

- 9.2. Market Analysis, Insights and Forecast - by Packaging Type

- 9.2.1. Aseptic packages

- 9.2.2. Glass Bottles

- 9.2.3. Metal Can

- 9.2.4. PET Bottles

- 9.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.3.1. Off-trade

- 9.3.1.1. Convenience Stores

- 9.3.1.2. Online Retail

- 9.3.1.3. Supermarket/Hypermarket

- 9.3.1.4. Others

- 9.3.2. On-trade

- 9.3.1. Off-trade

- 9.1. Market Analysis, Insights and Forecast - by Soft Drink Type

- 10. Asia Pacific APAC Ready-to-Drink Tea Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Soft Drink Type

- 10.1.1. Green Tea

- 10.1.2. Herbal Tea

- 10.1.3. Iced Tea

- 10.1.4. Other RTD Tea

- 10.2. Market Analysis, Insights and Forecast - by Packaging Type

- 10.2.1. Aseptic packages

- 10.2.2. Glass Bottles

- 10.2.3. Metal Can

- 10.2.4. PET Bottles

- 10.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.3.1. Off-trade

- 10.3.1.1. Convenience Stores

- 10.3.1.2. Online Retail

- 10.3.1.3. Supermarket/Hypermarket

- 10.3.1.4. Others

- 10.3.2. On-trade

- 10.3.1. Off-trade

- 10.1. Market Analysis, Insights and Forecast - by Soft Drink Type

- 11. United States APAC Ready-to-Drink Tea Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1.

- 12. Canada APAC Ready-to-Drink Tea Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1.

- 13. Mexico APAC Ready-to-Drink Tea Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1.

- 14. Rest of North America APAC Ready-to-Drink Tea Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1.

- 15. Competitive Analysis

- 15.1. Global Market Share Analysis 2024

- 15.2. Company Profiles

- 15.2.1 Ichitan Group PCL

- 15.2.1.1. Overview

- 15.2.1.2. Products

- 15.2.1.3. SWOT Analysis

- 15.2.1.4. Recent Developments

- 15.2.1.5. Financials (Based on Availability)

- 15.2.2 Nestle S A

- 15.2.2.1. Overview

- 15.2.2.2. Products

- 15.2.2.3. SWOT Analysis

- 15.2.2.4. Recent Developments

- 15.2.2.5. Financials (Based on Availability)

- 15.2.3 Asahi Group Holdings Ltd

- 15.2.3.1. Overview

- 15.2.3.2. Products

- 15.2.3.3. SWOT Analysis

- 15.2.3.4. Recent Developments

- 15.2.3.5. Financials (Based on Availability)

- 15.2.4 Ito En Ltd

- 15.2.4.1. Overview

- 15.2.4.2. Products

- 15.2.4.3. SWOT Analysis

- 15.2.4.4. Recent Developments

- 15.2.4.5. Financials (Based on Availability)

- 15.2.5 Nongfu Spring Co Ltd

- 15.2.5.1. Overview

- 15.2.5.2. Products

- 15.2.5.3. SWOT Analysis

- 15.2.5.4. Recent Developments

- 15.2.5.5. Financials (Based on Availability)

- 15.2.6 Tata Consumer Products Ltd

- 15.2.6.1. Overview

- 15.2.6.2. Products

- 15.2.6.3. SWOT Analysis

- 15.2.6.4. Recent Developments

- 15.2.6.5. Financials (Based on Availability)

- 15.2.7 PT Anggada Putra Rekso Mulia

- 15.2.7.1. Overview

- 15.2.7.2. Products

- 15.2.7.3. SWOT Analysis

- 15.2.7.4. Recent Developments

- 15.2.7.5. Financials (Based on Availability)

- 15.2.8 Suntory Holdings Limited

- 15.2.8.1. Overview

- 15.2.8.2. Products

- 15.2.8.3. SWOT Analysis

- 15.2.8.4. Recent Developments

- 15.2.8.5. Financials (Based on Availability)

- 15.2.9 JDB Group

- 15.2.9.1. Overview

- 15.2.9.2. Products

- 15.2.9.3. SWOT Analysis

- 15.2.9.4. Recent Developments

- 15.2.9.5. Financials (Based on Availability)

- 15.2.10 Tingyi (Cayman Islands) Holding Corporation

- 15.2.10.1. Overview

- 15.2.10.2. Products

- 15.2.10.3. SWOT Analysis

- 15.2.10.4. Recent Developments

- 15.2.10.5. Financials (Based on Availability)

- 15.2.11 The Coca-Cola Company

- 15.2.11.1. Overview

- 15.2.11.2. Products

- 15.2.11.3. SWOT Analysis

- 15.2.11.4. Recent Developments

- 15.2.11.5. Financials (Based on Availability)

- 15.2.12 Uni-President Enterprises Corp

- 15.2.12.1. Overview

- 15.2.12.2. Products

- 15.2.12.3. SWOT Analysis

- 15.2.12.4. Recent Developments

- 15.2.12.5. Financials (Based on Availability)

- 15.2.13 Kirin Holdings Company Limited

- 15.2.13.1. Overview

- 15.2.13.2. Products

- 15.2.13.3. SWOT Analysis

- 15.2.13.4. Recent Developments

- 15.2.13.5. Financials (Based on Availability)

- 15.2.14 Thai Beverages PCL

- 15.2.14.1. Overview

- 15.2.14.2. Products

- 15.2.14.3. SWOT Analysis

- 15.2.14.4. Recent Developments

- 15.2.14.5. Financials (Based on Availability)

- 15.2.15 Sapporo Holdings Limited

- 15.2.15.1. Overview

- 15.2.15.2. Products

- 15.2.15.3. SWOT Analysis

- 15.2.15.4. Recent Developments

- 15.2.15.5. Financials (Based on Availability)

- 15.2.1 Ichitan Group PCL

List of Figures

- Figure 1: Global APAC Ready-to-Drink Tea Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: United States APAC Ready-to-Drink Tea Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: United States APAC Ready-to-Drink Tea Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: Canada APAC Ready-to-Drink Tea Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Canada APAC Ready-to-Drink Tea Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: Mexico APAC Ready-to-Drink Tea Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: Mexico APAC Ready-to-Drink Tea Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: Rest of North America APAC Ready-to-Drink Tea Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: Rest of North America APAC Ready-to-Drink Tea Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: North America APAC Ready-to-Drink Tea Industry Revenue (Million), by Soft Drink Type 2024 & 2032

- Figure 11: North America APAC Ready-to-Drink Tea Industry Revenue Share (%), by Soft Drink Type 2024 & 2032

- Figure 12: North America APAC Ready-to-Drink Tea Industry Revenue (Million), by Packaging Type 2024 & 2032

- Figure 13: North America APAC Ready-to-Drink Tea Industry Revenue Share (%), by Packaging Type 2024 & 2032

- Figure 14: North America APAC Ready-to-Drink Tea Industry Revenue (Million), by Distribution Channel 2024 & 2032

- Figure 15: North America APAC Ready-to-Drink Tea Industry Revenue Share (%), by Distribution Channel 2024 & 2032

- Figure 16: North America APAC Ready-to-Drink Tea Industry Revenue (Million), by Country 2024 & 2032

- Figure 17: North America APAC Ready-to-Drink Tea Industry Revenue Share (%), by Country 2024 & 2032

- Figure 18: South America APAC Ready-to-Drink Tea Industry Revenue (Million), by Soft Drink Type 2024 & 2032

- Figure 19: South America APAC Ready-to-Drink Tea Industry Revenue Share (%), by Soft Drink Type 2024 & 2032

- Figure 20: South America APAC Ready-to-Drink Tea Industry Revenue (Million), by Packaging Type 2024 & 2032

- Figure 21: South America APAC Ready-to-Drink Tea Industry Revenue Share (%), by Packaging Type 2024 & 2032

- Figure 22: South America APAC Ready-to-Drink Tea Industry Revenue (Million), by Distribution Channel 2024 & 2032

- Figure 23: South America APAC Ready-to-Drink Tea Industry Revenue Share (%), by Distribution Channel 2024 & 2032

- Figure 24: South America APAC Ready-to-Drink Tea Industry Revenue (Million), by Country 2024 & 2032

- Figure 25: South America APAC Ready-to-Drink Tea Industry Revenue Share (%), by Country 2024 & 2032

- Figure 26: Europe APAC Ready-to-Drink Tea Industry Revenue (Million), by Soft Drink Type 2024 & 2032

- Figure 27: Europe APAC Ready-to-Drink Tea Industry Revenue Share (%), by Soft Drink Type 2024 & 2032

- Figure 28: Europe APAC Ready-to-Drink Tea Industry Revenue (Million), by Packaging Type 2024 & 2032

- Figure 29: Europe APAC Ready-to-Drink Tea Industry Revenue Share (%), by Packaging Type 2024 & 2032

- Figure 30: Europe APAC Ready-to-Drink Tea Industry Revenue (Million), by Distribution Channel 2024 & 2032

- Figure 31: Europe APAC Ready-to-Drink Tea Industry Revenue Share (%), by Distribution Channel 2024 & 2032

- Figure 32: Europe APAC Ready-to-Drink Tea Industry Revenue (Million), by Country 2024 & 2032

- Figure 33: Europe APAC Ready-to-Drink Tea Industry Revenue Share (%), by Country 2024 & 2032

- Figure 34: Middle East & Africa APAC Ready-to-Drink Tea Industry Revenue (Million), by Soft Drink Type 2024 & 2032

- Figure 35: Middle East & Africa APAC Ready-to-Drink Tea Industry Revenue Share (%), by Soft Drink Type 2024 & 2032

- Figure 36: Middle East & Africa APAC Ready-to-Drink Tea Industry Revenue (Million), by Packaging Type 2024 & 2032

- Figure 37: Middle East & Africa APAC Ready-to-Drink Tea Industry Revenue Share (%), by Packaging Type 2024 & 2032

- Figure 38: Middle East & Africa APAC Ready-to-Drink Tea Industry Revenue (Million), by Distribution Channel 2024 & 2032

- Figure 39: Middle East & Africa APAC Ready-to-Drink Tea Industry Revenue Share (%), by Distribution Channel 2024 & 2032

- Figure 40: Middle East & Africa APAC Ready-to-Drink Tea Industry Revenue (Million), by Country 2024 & 2032

- Figure 41: Middle East & Africa APAC Ready-to-Drink Tea Industry Revenue Share (%), by Country 2024 & 2032

- Figure 42: Asia Pacific APAC Ready-to-Drink Tea Industry Revenue (Million), by Soft Drink Type 2024 & 2032

- Figure 43: Asia Pacific APAC Ready-to-Drink Tea Industry Revenue Share (%), by Soft Drink Type 2024 & 2032

- Figure 44: Asia Pacific APAC Ready-to-Drink Tea Industry Revenue (Million), by Packaging Type 2024 & 2032

- Figure 45: Asia Pacific APAC Ready-to-Drink Tea Industry Revenue Share (%), by Packaging Type 2024 & 2032

- Figure 46: Asia Pacific APAC Ready-to-Drink Tea Industry Revenue (Million), by Distribution Channel 2024 & 2032

- Figure 47: Asia Pacific APAC Ready-to-Drink Tea Industry Revenue Share (%), by Distribution Channel 2024 & 2032

- Figure 48: Asia Pacific APAC Ready-to-Drink Tea Industry Revenue (Million), by Country 2024 & 2032

- Figure 49: Asia Pacific APAC Ready-to-Drink Tea Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Soft Drink Type 2019 & 2032

- Table 3: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Packaging Type 2019 & 2032

- Table 4: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 5: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 9: APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 11: APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 13: APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Soft Drink Type 2019 & 2032

- Table 15: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Packaging Type 2019 & 2032

- Table 16: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 17: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: United States APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Canada APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Mexico APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Soft Drink Type 2019 & 2032

- Table 22: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Packaging Type 2019 & 2032

- Table 23: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 24: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 25: Brazil APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Argentina APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Rest of South America APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Soft Drink Type 2019 & 2032

- Table 29: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Packaging Type 2019 & 2032

- Table 30: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 31: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 32: United Kingdom APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 33: Germany APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 34: France APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 35: Italy APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: Spain APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 37: Russia APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 38: Benelux APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 39: Nordics APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 40: Rest of Europe APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 41: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Soft Drink Type 2019 & 2032

- Table 42: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Packaging Type 2019 & 2032

- Table 43: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 44: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 45: Turkey APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: Israel APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 47: GCC APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 48: North Africa APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 49: South Africa APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 50: Rest of Middle East & Africa APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 51: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Soft Drink Type 2019 & 2032

- Table 52: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Packaging Type 2019 & 2032

- Table 53: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 54: Global APAC Ready-to-Drink Tea Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 55: China APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 56: India APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 57: Japan APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 58: South Korea APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 59: ASEAN APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 60: Oceania APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 61: Rest of Asia Pacific APAC Ready-to-Drink Tea Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the APAC Ready-to-Drink Tea Industry?

The projected CAGR is approximately 3.45%.

2. Which companies are prominent players in the APAC Ready-to-Drink Tea Industry?

Key companies in the market include Ichitan Group PCL, Nestle S A, Asahi Group Holdings Ltd, Ito En Ltd, Nongfu Spring Co Ltd, Tata Consumer Products Ltd, PT Anggada Putra Rekso Mulia, Suntory Holdings Limited, JDB Group, Tingyi (Cayman Islands) Holding Corporation, The Coca-Cola Company, Uni-President Enterprises Corp, Kirin Holdings Company Limited, Thai Beverages PCL, Sapporo Holdings Limited.

3. What are the main segments of the APAC Ready-to-Drink Tea Industry?

The market segments include Soft Drink Type, Packaging Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Trend of Ingestible Beauty Products; Growing demand for Nutrient-Enriched Cosmetic Products.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Availability of Counterfeit Beauty Supplements Products.

8. Can you provide examples of recent developments in the market?

November 2023: The Coca-Cola Company's brand ChaiChun brought exquisite teas to Delhi with its new store, The ChaiChun Store, expanding its business.September 2022: Ayataka, a brand of iced green tea produced by Coca-Cola, has announced the release of its new Ayataka Cafe Matcha Latte which will hit stores across JapanJune 2021: Sermsuk launched “est Play plus vitamins B6 and B12”, a vitamin-infused carbonated soft drink (CSD) certified by “Healthier Choice” nutritional logo.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "APAC Ready-to-Drink Tea Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the APAC Ready-to-Drink Tea Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the APAC Ready-to-Drink Tea Industry?

To stay informed about further developments, trends, and reports in the APAC Ready-to-Drink Tea Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence