Key Insights

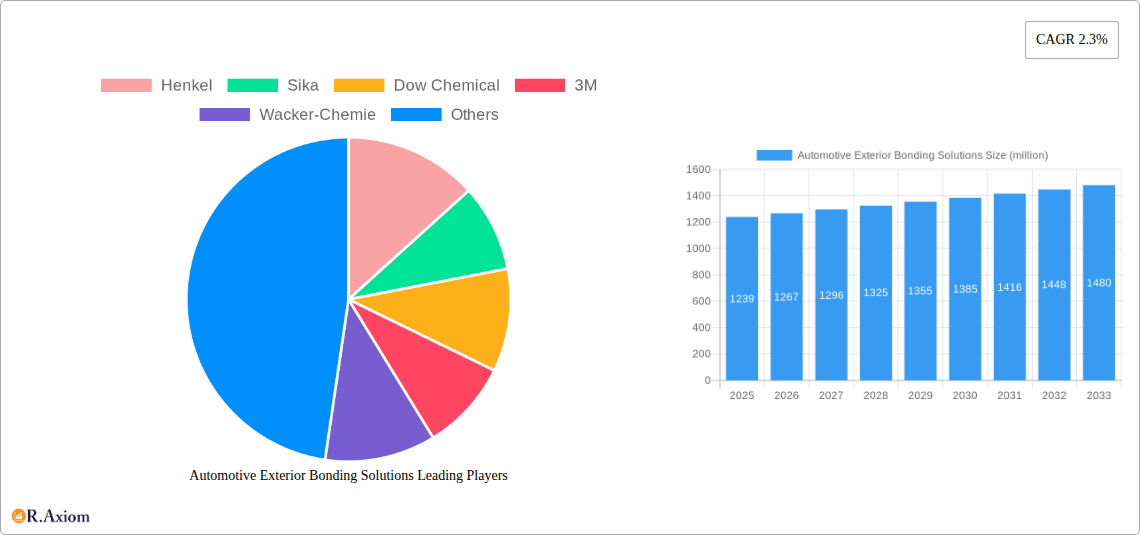

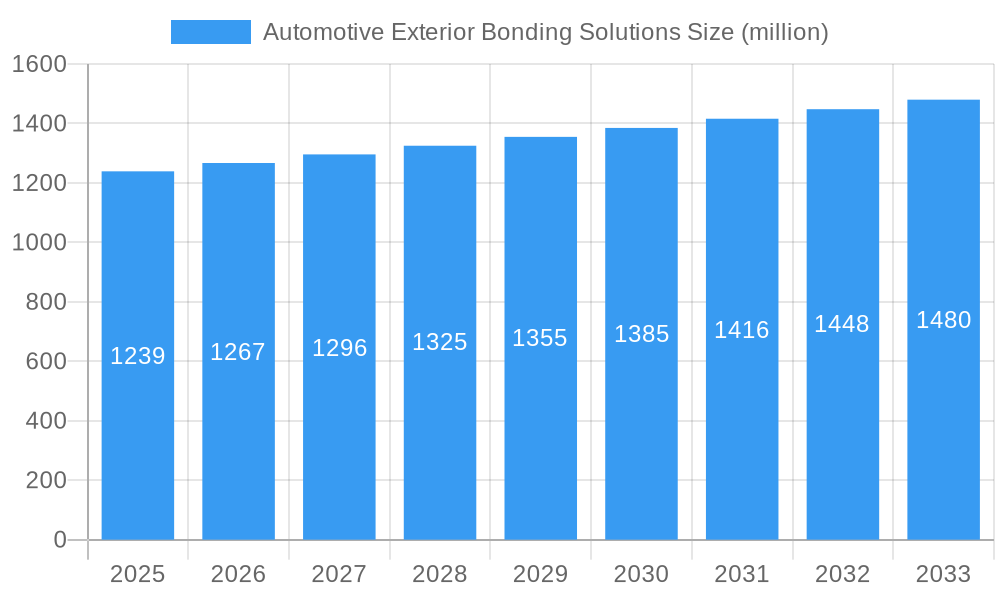

The global Automotive Exterior Bonding Solutions market is projected to reach a substantial valuation of $1,239 million by 2025, demonstrating a steady Compound Annual Growth Rate (CAGR) of 2.3% through 2033. This robust growth is primarily propelled by the increasing adoption of lightweight materials in vehicle construction, a critical trend aimed at enhancing fuel efficiency and reducing emissions. The shift towards advanced materials like composites and aluminum necessitates specialized bonding solutions that can effectively join dissimilar substrates, ensuring structural integrity and durability under demanding exterior conditions. Furthermore, the evolving design aesthetics in the automotive industry, with a greater emphasis on sleeker lines and integrated components, are driving demand for bonding agents that facilitate seamless integration and eliminate visible fasteners. The market is witnessing a significant push towards innovative adhesive technologies that offer superior performance characteristics, including high tensile strength, excellent weather resistance, and adaptability to diverse application environments. Key applications such as headlamp bonding and roof module bonding are expected to remain dominant, benefiting from the continuous innovation in automotive lighting and the growing popularity of panoramic sunroofs and integrated roof systems. The "Others" segment, encompassing a range of exterior components, is also anticipated to expand as manufacturers explore new bonding applications to improve overall vehicle performance and aesthetics.

Automotive Exterior Bonding Solutions Market Size (In Billion)

The market's trajectory is further influenced by evolving manufacturing processes and an increasing focus on sustainability. Manufacturers are actively seeking bonding solutions that contribute to a greener automotive footprint, either through solvent-free formulations or by enabling the use of recycled or bio-based materials. While the market exhibits a positive outlook, certain restraints such as the fluctuating raw material costs and the need for specialized application equipment could pose challenges. However, the strategic investments in research and development by leading players like Henkel, Sika, Dow Chemical, and 3M, among others, are continuously addressing these limitations by introducing cost-effective and user-friendly solutions. The competitive landscape is characterized by a mix of global giants and regional specialists, all vying to capture market share through product innovation, strategic partnerships, and geographical expansion. The Asia Pacific region, particularly China and India, is expected to be a significant growth engine due to the burgeoning automotive production and the increasing demand for advanced vehicle features. North America and Europe will continue to be mature yet vital markets, driven by stringent regulatory standards and a strong consumer preference for high-quality, durable vehicles.

Automotive Exterior Bonding Solutions Company Market Share

Automotive Exterior Bonding Solutions Market Concentration & Innovation

The automotive exterior bonding solutions market exhibits a moderate to high concentration, with a few global leaders like Henkel, Sika, Dow Chemical, and 3M holding significant market shares. These key players dominate through extensive R&D investments, robust distribution networks, and strategic acquisitions. Innovation is a critical driver, fueled by the automotive industry's demand for lightweighting, improved aesthetics, and enhanced vehicle performance. Advancements in urethane and epoxy adhesives, offering superior strength, flexibility, and durability, are transforming traditional fastening methods. Regulatory frameworks, particularly those focusing on emissions reduction and safety standards, indirectly influence the adoption of advanced bonding solutions that enable lighter vehicle construction. Product substitutes, such as traditional mechanical fasteners, are gradually being displaced by the superior performance characteristics of modern adhesives. End-user trends are leaning towards sophisticated assembly processes that reduce manufacturing time and cost, further propelling the demand for innovative bonding solutions. Mergers and acquisitions play a vital role in consolidating the market and expanding technological capabilities. For instance, recent M&A activities have seen deal values in the hundreds of millions, as major companies aim to acquire specialized technologies and market access.

- Market Share Dynamics: Top players like Henkel and Sika collectively hold an estimated 40% of the global market.

- M&A Deal Values: Recent strategic acquisitions in the adhesives sector for automotive applications have ranged from $100 million to $500 million.

- Innovation Focus: Key areas of R&D include high-strength structural adhesives, temperature-resistant formulations, and sustainable bonding materials.

- Regulatory Impact: Stringent automotive safety regulations are driving the demand for adhesives capable of withstanding extreme conditions and enhancing structural integrity.

Automotive Exterior Bonding Solutions Industry Trends & Insights

The global automotive exterior bonding solutions market is poised for substantial growth, driven by a confluence of escalating automotive production, the relentless pursuit of vehicle lightweighting, and evolving consumer preferences for aesthetically pleasing and durable exteriors. The market is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 6.5% over the forecast period of 2025–2033, reaching an estimated market size of over $15,000 million by 2033. This expansion is underpinned by several key growth drivers, including the increasing adoption of advanced manufacturing techniques in the automotive sector, the continuous development of new adhesive chemistries, and the growing demand for electric and autonomous vehicles, which often incorporate novel material combinations requiring specialized bonding. Technological disruptions are at the forefront of this evolution, with the advent of high-performance urethane, epoxy, and acrylic adhesives that offer superior adhesion to a wider range of substrates, including composite materials and advanced high-strength steels. These advancements are critical for meeting the automotive industry's dual objectives of enhancing structural integrity and reducing overall vehicle weight, thereby improving fuel efficiency and range in the case of EVs. Consumer preferences are increasingly aligning with manufacturers' efforts to create sleeker, more aerodynamic vehicle designs, which are often achieved through the seamless integration of exterior components facilitated by advanced bonding. The competitive dynamics within the market are characterized by intense innovation and strategic collaborations between adhesive manufacturers and automotive OEMs. Companies are investing heavily in research and development to create next-generation bonding solutions that offer faster curing times, improved environmental resistance, and enhanced recyclability. Market penetration of advanced adhesives is steadily increasing across various automotive applications, from headlamp assemblies and roof modules to body panels and spoilers. The historical period from 2019 to 2024 saw a steady rise in adoption, with the base year of 2025 expected to set a robust foundation for accelerated growth. The estimated market size for 2025 is projected to be around $9,500 million, with continued upward trajectory anticipated. The industry is also witnessing a shift towards more sustainable and environmentally friendly bonding solutions, driven by global sustainability initiatives and evolving consumer awareness.

- Market Growth Drivers: Increasing vehicle production, lightweighting initiatives, and the rise of EVs are primary catalysts.

- Technological Disruptions: Advancements in urethane, epoxy, and acrylic adhesives are enabling new design possibilities and manufacturing efficiencies.

- Consumer Preferences: Demand for sleek, integrated exterior designs and durable finishes is influencing adhesive selection.

- Competitive Dynamics: Innovation, strategic partnerships, and R&D investments define the competitive landscape.

- CAGR Projection: An estimated CAGR of 6.5% for the forecast period 2025–2033.

- Market Penetration: Growing adoption of advanced adhesives in various automotive exterior applications.

- Market Size (Base Year 2025): Approximately $9,500 million.

- Market Size (Estimated Year 2033): Over $15,000 million.

Dominant Markets & Segments in Automotive Exterior Bonding Solutions

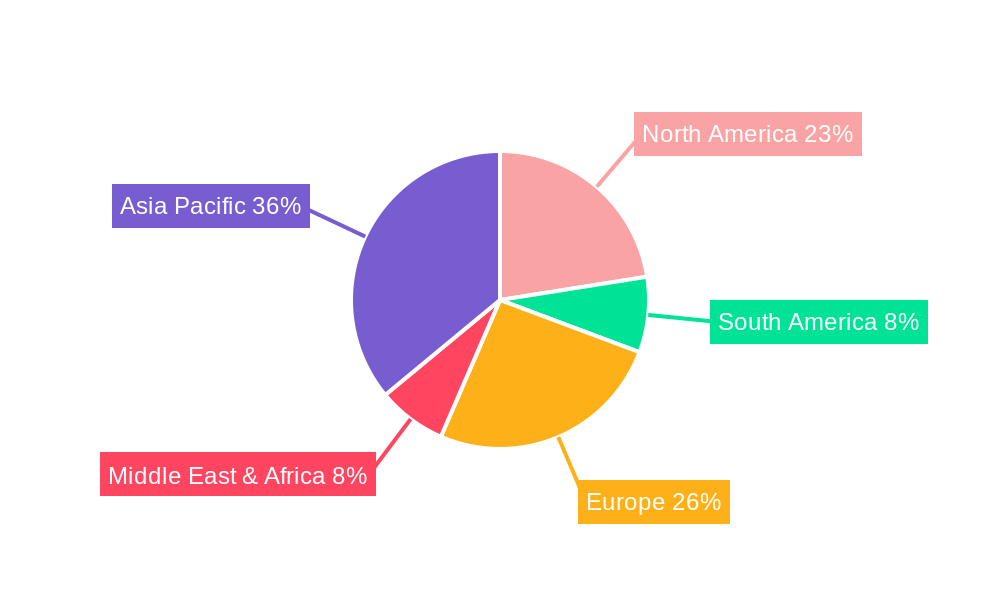

The automotive exterior bonding solutions market's dominance is sculpted by geographical strengths and specialized segment penetration. North America and Europe currently lead the charge, driven by the presence of major automotive manufacturers, stringent quality standards, and a high adoption rate of advanced automotive technologies. Within these regions, Germany stands out as a pivotal country, owing to its strong automotive engineering heritage and its leading role in premium vehicle manufacturing. The United States also represents a significant market, fueled by its substantial vehicle production volumes and a burgeoning demand for innovative automotive components.

In terms of applications, Headlamp Bonding represents a crucial and high-volume segment. The increasing complexity of headlamp designs, incorporating LED and adaptive lighting technologies, necessitates sophisticated bonding solutions that ensure optical clarity, resistance to extreme temperatures, and durability against road debris and environmental factors. Manufacturers like Henkel and Sika have developed specialized epoxy and urethane adhesives that meet these stringent requirements, offering excellent adhesion to polycarbonate and glass substrates. The market for headlamp bonding is projected to grow at a CAGR of approximately 6.8% from 2025 to 2033, reaching an estimated market size of over $3,500 million.

Roof Module Bonding, encompassing panoramic sunroofs, roof racks, and antenna integrations, is another dominant application. This segment is characterized by the need for structural integrity, weatherproofing, and aesthetic appeal. The growing popularity of panoramic glass roofs, particularly in SUVs and premium vehicles, is a significant growth driver. Urethane adhesives are widely favored for their flexibility, impact resistance, and ability to bond dissimilar materials like glass, metal, and composites. The roof module bonding segment is expected to witness a CAGR of around 6.2% during the forecast period, with an estimated market value exceeding $3,000 million by 2033.

The Others segment, encompassing a wide array of applications such as bonding of spoilers, body panels, side moldings, and trim components, also holds substantial market share. This diverse category benefits from the overall growth in vehicle production and the trend towards more intricate exterior designs. The development of advanced acrylic and hybrid adhesives, offering rapid curing times and excellent adhesion to painted surfaces and plastics, is driving innovation in this segment. The "Others" segment is anticipated to grow at a CAGR of approximately 6.0%, contributing significantly to the overall market expansion, with an estimated market size of over $8,500 million by 2033.

By type of adhesive, Urethane Adhesives currently hold the largest market share due to their versatility, excellent mechanical properties, and adaptability to various bonding challenges in automotive exteriors. They offer a good balance of strength, flexibility, and UV resistance. The urethane adhesives segment is projected to grow at a CAGR of 7.0%, with an estimated market size exceeding $6,000 million by 2033.

Epoxy Adhesives are also critical, particularly for structural bonding applications where high strength and stiffness are paramount. They are favored for their exceptional resistance to chemicals and high temperatures, making them ideal for demanding exterior applications. The epoxy adhesives segment is expected to grow at a CAGR of 6.3%, reaching an estimated market size of over $5,000 million by 2033.

Acrylic Adhesives, known for their fast curing times and good adhesion to a wide range of substrates, including plastics and painted surfaces, are gaining traction, especially in applications requiring quick assembly processes. The acrylic adhesives segment is projected to experience a CAGR of 5.9%, with an estimated market size surpassing $3,000 million by 2033.

- Leading Regions: North America and Europe.

- Dominant Country: Germany.

- Key Application Segments:

- Headlamp Bonding: Expected market size over $3,500 million by 2033; CAGR ~6.8%.

- Roof Module Bonding: Expected market size over $3,000 million by 2033; CAGR ~6.2%.

- Others: Expected market size over $8,500 million by 2033; CAGR ~6.0%.

- Dominant Adhesive Types:

- Urethane Adhesives: Expected market size over $6,000 million by 2033; CAGR ~7.0%.

- Epoxy Adhesives: Expected market size over $5,000 million by 2033; CAGR ~6.3%.

- Acrylic Adhesives: Expected market size over $3,000 million by 2033; CAGR ~5.9%.

- Growth Drivers for Segments: Increasing complexity of automotive designs, demand for improved aesthetics and performance, and advancements in adhesive technology.

Automotive Exterior Bonding Solutions Product Developments

Recent product developments in automotive exterior bonding solutions are focused on enhancing performance, sustainability, and manufacturing efficiency. Innovations include the introduction of new urethane adhesives with improved UV resistance and faster curing times, ideal for exterior trim and panel bonding. Advanced epoxy formulations are emerging with higher shear strength and thermal stability, crucial for structural applications in electric vehicles. Acrylic-based adhesives are being optimized for greater flexibility and adhesion to challenging substrates like advanced composites and coated metals. These developments aim to reduce vehicle weight, improve aerodynamic profiles, and meet evolving aesthetic demands, while also addressing environmental concerns through the development of solvent-free and low-VOC (Volatile Organic Compound) options. Companies like 3M and Wacker-Chemie are at the forefront, offering solutions that enhance durability and simplify assembly processes for OEMs.

Report Scope & Segmentation Analysis

This comprehensive report analyzes the global automotive exterior bonding solutions market, providing in-depth insights into market dynamics, trends, and future projections. The segmentation covers key aspects to offer a holistic view of the market landscape.

Application Segmentation: The market is segmented based on the primary applications of exterior bonding solutions. This includes Headlamp Bonding, crucial for integrating lighting systems with the vehicle’s exterior, ensuring both aesthetic appeal and functional integrity. Roof Module Bonding, encompassing elements like panoramic sunroofs and antennas, is another significant application requiring robust and weather-resistant adhesives. The Others category encompasses a broad spectrum of exterior bonding needs, such as body panels, spoilers, side moldings, and trim, reflecting the diverse and evolving design requirements of modern vehicles.

Type Segmentation: The report further categorizes the market by the type of adhesive technology employed. Urethane Adhesives are a dominant category, offering a strong combination of flexibility, durability, and adhesion properties. Epoxy Adhesives are vital for structural applications demanding high strength and resistance to harsh environmental conditions. Acrylic Adhesives are recognized for their fast curing capabilities and versatility across various substrates. The Others segment includes emerging adhesive technologies and specialized formulations catering to niche requirements within the automotive exterior sector.

Key Drivers of Automotive Exterior Bonding Solutions Growth

The growth of the automotive exterior bonding solutions market is propelled by several interconnected factors. The automotive industry's unwavering commitment to lightweighting vehicles to improve fuel efficiency and reduce emissions is a primary driver. Advanced adhesives enable the use of lighter materials like composites and high-strength aluminum, replacing heavier traditional materials. The increasing complexity of automotive designs, with a focus on seamless integration of components and aerodynamic profiles, necessitates the use of bonding solutions over mechanical fasteners for aesthetic and performance benefits. Furthermore, the burgeoning demand for electric vehicles (EVs), which often utilize novel material combinations and require specialized thermal management solutions, further stimulates the need for innovative bonding technologies. Supportive regulatory frameworks promoting sustainability and safety standards also indirectly encourage the adoption of advanced, lighter, and more efficient automotive assembly methods facilitated by adhesives.

- Lightweighting Initiatives: Crucial for fuel efficiency and emissions reduction.

- Complex Automotive Designs: Driving demand for seamless integration and aesthetic appeal.

- Electric Vehicle (EV) Growth: Requiring specialized bonding for new materials and thermal management.

- Regulatory Support: Pushing for sustainable and safer automotive manufacturing practices.

Challenges in the Automotive Exterior Bonding Solutions Sector

Despite robust growth prospects, the automotive exterior bonding solutions sector faces several challenges. Regulatory hurdles related to environmental compliance and evolving safety standards for adhesives can create adoption barriers and necessitate continuous product reformulation. The volatility of raw material prices, particularly for petrochemical-based components, can impact profit margins and pricing strategies for adhesive manufacturers. Supply chain disruptions, as evidenced by recent global events, can affect the availability and lead times of critical raw materials and finished products, posing challenges for just-in-time manufacturing in the automotive industry. Furthermore, the competitive pressure from established players and emerging technologies necessitates continuous innovation and cost optimization to maintain market share.

- Regulatory Compliance: Navigating evolving environmental and safety standards.

- Raw Material Price Volatility: Impacting cost structures and pricing.

- Supply Chain Vulnerabilities: Potential for disruptions in material availability.

- Intense Competition: Requiring ongoing innovation and cost-efficiency.

Emerging Opportunities in Automotive Exterior Bonding Solutions

The automotive exterior bonding solutions market is ripe with emerging opportunities driven by technological advancements and evolving consumer demands. The rapid expansion of the electric vehicle (EV) market presents significant opportunities for specialized bonding solutions that can handle battery pack integration, thermal management, and the use of lightweight composite materials. The growing trend towards autonomous vehicles will also necessitate advanced bonding for the integration of sophisticated sensor arrays and enhanced structural integrity. Furthermore, the increasing consumer preference for customization and personalization in vehicle exteriors opens avenues for flexible bonding solutions that can accommodate diverse design elements. The drive towards sustainability is also creating demand for eco-friendly, recyclable, and bio-based adhesive formulations.

- Electric Vehicle (EV) Integration: Bonding for battery packs, thermal management, and lightweight materials.

- Autonomous Vehicle Technology: Adhesives for sensors and enhanced structural integrity.

- Vehicle Customization: Demand for flexible solutions for personalized exterior designs.

- Sustainable Adhesives: Growth in eco-friendly, recyclable, and bio-based formulations.

Leading Players in the Automotive Exterior Bonding Solutions Market

- Henkel

- Sika

- Dow Chemical

- 3M

- Wacker-Chemie

- PPG Industries

- Arkema Group

- BASF

- Lord

- H.B. Fuller

- ITW

- Hubei Huitian

- Ashland

- ThreeBond

- Huntsman

Key Developments in Automotive Exterior Bonding Solutions Industry

- 2023: Henkel launches a new line of high-performance urethane adhesives for electric vehicle body structures, offering enhanced thermal conductivity and impact resistance.

- 2023: Sika introduces a novel structural adhesive for lightweight automotive body assembly, enabling greater design freedom and reduced assembly time.

- 2024: 3M unveils an advanced acrylic adhesive designed for bonding dissimilar materials in automotive exteriors, with improved weatherability and UV resistance.

- 2024: Dow Chemical announces significant R&D investment in sustainable adhesive technologies, focusing on bio-based and recyclable formulations for automotive applications.

- 2024: Wacker-Chemie expands its portfolio of silicone adhesives for automotive exterior sealing and bonding, offering enhanced performance in extreme temperature conditions.

Strategic Outlook for Automotive Exterior Bonding Solutions Market

The strategic outlook for the automotive exterior bonding solutions market is exceptionally bright, characterized by continuous innovation and expanding applications. The persistent drive for vehicle lightweighting and the accelerating adoption of electric vehicles will serve as significant growth catalysts. Strategic partnerships between adhesive manufacturers and automotive OEMs will be crucial for co-developing tailored solutions that meet the evolving demands of vehicle design and performance. Investment in research and development focused on sustainable and advanced adhesive technologies will remain paramount for competitive advantage. The market is poised for sustained growth, with opportunities arising from emerging trends such as autonomous driving and increasing demand for personalized vehicle aesthetics, ensuring a dynamic and prosperous future for this vital sector of the automotive supply chain.

Automotive Exterior Bonding Solutions Segmentation

-

1. Application

- 1.1. Headlamp Bonding

- 1.2. Roof Module Bonding

- 1.3. Others

-

2. Type

- 2.1. Urethane Adhesives

- 2.2. Epoxy Adhesives

- 2.3. Acrylic Adhesives

- 2.4. Others

Automotive Exterior Bonding Solutions Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Exterior Bonding Solutions Regional Market Share

Geographic Coverage of Automotive Exterior Bonding Solutions

Automotive Exterior Bonding Solutions REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Headlamp Bonding

- 5.1.2. Roof Module Bonding

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Urethane Adhesives

- 5.2.2. Epoxy Adhesives

- 5.2.3. Acrylic Adhesives

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Automotive Exterior Bonding Solutions Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Headlamp Bonding

- 6.1.2. Roof Module Bonding

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Urethane Adhesives

- 6.2.2. Epoxy Adhesives

- 6.2.3. Acrylic Adhesives

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Automotive Exterior Bonding Solutions Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Headlamp Bonding

- 7.1.2. Roof Module Bonding

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Urethane Adhesives

- 7.2.2. Epoxy Adhesives

- 7.2.3. Acrylic Adhesives

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Automotive Exterior Bonding Solutions Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Headlamp Bonding

- 8.1.2. Roof Module Bonding

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Urethane Adhesives

- 8.2.2. Epoxy Adhesives

- 8.2.3. Acrylic Adhesives

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Automotive Exterior Bonding Solutions Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Headlamp Bonding

- 9.1.2. Roof Module Bonding

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Urethane Adhesives

- 9.2.2. Epoxy Adhesives

- 9.2.3. Acrylic Adhesives

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Automotive Exterior Bonding Solutions Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Headlamp Bonding

- 10.1.2. Roof Module Bonding

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Urethane Adhesives

- 10.2.2. Epoxy Adhesives

- 10.2.3. Acrylic Adhesives

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Automotive Exterior Bonding Solutions Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Headlamp Bonding

- 11.1.2. Roof Module Bonding

- 11.1.3. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Urethane Adhesives

- 11.2.2. Epoxy Adhesives

- 11.2.3. Acrylic Adhesives

- 11.2.4. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Henkel

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Sika

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Dow Chemical

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 3M

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Wacker-Chemie

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 PPG Industries

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Arkema Group

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 BASF

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Lord

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 H.B. Fuller

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 ITW

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Hubei Huitian

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Ashland

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 ThreeBond

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Huntsman

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 Henkel

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Automotive Exterior Bonding Solutions Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Automotive Exterior Bonding Solutions Revenue (million), by Application 2025 & 2033

- Figure 3: North America Automotive Exterior Bonding Solutions Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive Exterior Bonding Solutions Revenue (million), by Type 2025 & 2033

- Figure 5: North America Automotive Exterior Bonding Solutions Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Automotive Exterior Bonding Solutions Revenue (million), by Country 2025 & 2033

- Figure 7: North America Automotive Exterior Bonding Solutions Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automotive Exterior Bonding Solutions Revenue (million), by Application 2025 & 2033

- Figure 9: South America Automotive Exterior Bonding Solutions Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automotive Exterior Bonding Solutions Revenue (million), by Type 2025 & 2033

- Figure 11: South America Automotive Exterior Bonding Solutions Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Automotive Exterior Bonding Solutions Revenue (million), by Country 2025 & 2033

- Figure 13: South America Automotive Exterior Bonding Solutions Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive Exterior Bonding Solutions Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Automotive Exterior Bonding Solutions Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive Exterior Bonding Solutions Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Automotive Exterior Bonding Solutions Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Automotive Exterior Bonding Solutions Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Automotive Exterior Bonding Solutions Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automotive Exterior Bonding Solutions Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automotive Exterior Bonding Solutions Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automotive Exterior Bonding Solutions Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Automotive Exterior Bonding Solutions Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Automotive Exterior Bonding Solutions Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automotive Exterior Bonding Solutions Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive Exterior Bonding Solutions Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Automotive Exterior Bonding Solutions Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automotive Exterior Bonding Solutions Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Automotive Exterior Bonding Solutions Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Automotive Exterior Bonding Solutions Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Automotive Exterior Bonding Solutions Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Exterior Bonding Solutions Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Automotive Exterior Bonding Solutions Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Automotive Exterior Bonding Solutions Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Automotive Exterior Bonding Solutions Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Automotive Exterior Bonding Solutions Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Automotive Exterior Bonding Solutions Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive Exterior Bonding Solutions Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Automotive Exterior Bonding Solutions Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Automotive Exterior Bonding Solutions Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive Exterior Bonding Solutions Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Automotive Exterior Bonding Solutions Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Automotive Exterior Bonding Solutions Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Automotive Exterior Bonding Solutions Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Automotive Exterior Bonding Solutions Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Automotive Exterior Bonding Solutions Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Automotive Exterior Bonding Solutions Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Automotive Exterior Bonding Solutions Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Automotive Exterior Bonding Solutions Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automotive Exterior Bonding Solutions Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Exterior Bonding Solutions?

The projected CAGR is approximately 2.3%.

2. Which companies are prominent players in the Automotive Exterior Bonding Solutions?

Key companies in the market include Henkel, Sika, Dow Chemical, 3M, Wacker-Chemie, PPG Industries, Arkema Group, BASF, Lord, H.B. Fuller, ITW, Hubei Huitian, Ashland, ThreeBond, Huntsman.

3. What are the main segments of the Automotive Exterior Bonding Solutions?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 1239 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Exterior Bonding Solutions," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Exterior Bonding Solutions report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Exterior Bonding Solutions?

To stay informed about further developments, trends, and reports in the Automotive Exterior Bonding Solutions, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence