Key Insights

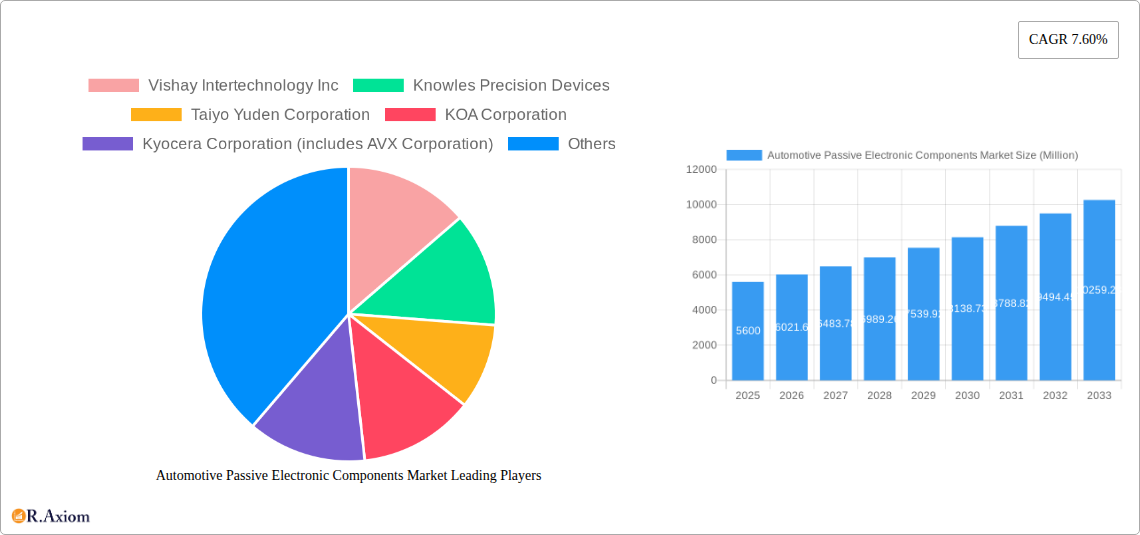

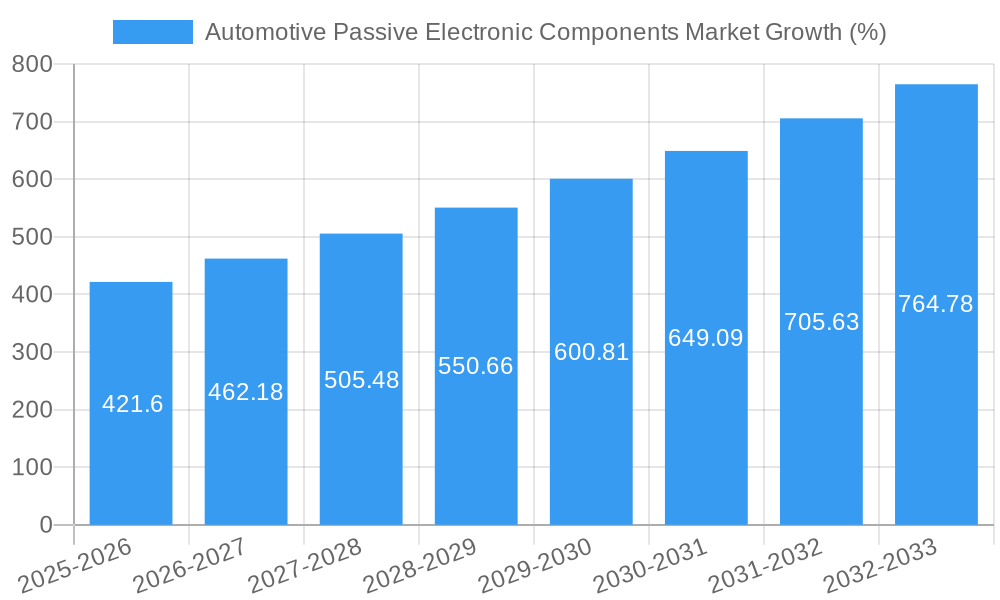

The Automotive Passive Electronic Components market is experiencing robust growth, projected to reach $5.60 billion in 2025 and maintain a Compound Annual Growth Rate (CAGR) of 7.60% from 2025 to 2033. This expansion is driven primarily by the increasing electrification of vehicles, the rising adoption of advanced driver-assistance systems (ADAS), and the growing demand for improved fuel efficiency and safety features. The integration of sophisticated electronics, including sensors, actuators, and control units, necessitates a higher volume and diversity of passive components such as capacitors, inductors, resistors, and EMC filters. Market trends indicate a shift towards miniaturization, higher power density, and improved performance characteristics in these components. Technological advancements like the development of high-performance film capacitors and advanced ceramic components are further fueling market growth. While supply chain disruptions and potential material cost fluctuations present some restraints, the overall long-term outlook for the Automotive Passive Electronic Components market remains exceptionally positive.

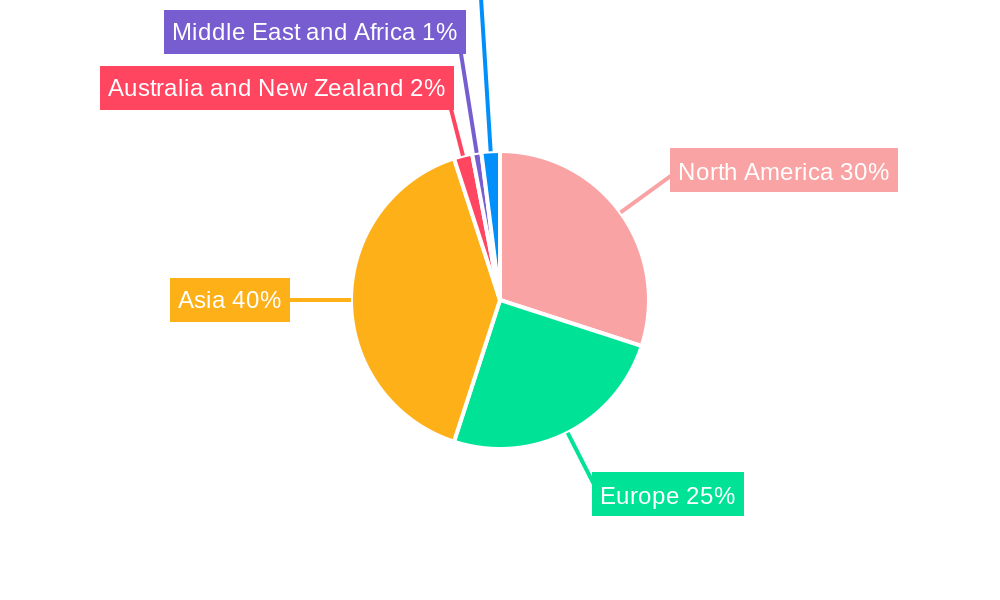

The market segmentation reveals capacitors and supercapacitors as dominant components, reflecting their critical roles in energy storage and power management within automotive electronics. Leading players like Vishay Intertechnology, Knowles Precision Devices, TDK Corporation, and Murata Manufacturing are actively investing in research and development to enhance component performance and meet the evolving demands of the automotive industry. Regional analysis suggests that Asia, driven by significant automotive manufacturing hubs in China, Japan, and South Korea, will likely hold the largest market share. However, North America and Europe will also contribute substantially, propelled by strong demand for advanced vehicle technologies in these regions. The forecast period (2025-2033) promises continued expansion, with the market likely surpassing $10 billion by the end of the forecast period, driven by factors such as the burgeoning electric vehicle (EV) market and the increasing complexity of automotive electronics.

Automotive Passive Electronic Components Market: A Comprehensive Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Automotive Passive Electronic Components Market, offering invaluable insights for industry stakeholders, investors, and strategic decision-makers. The study covers the period from 2019 to 2033, with a base year of 2025 and a forecast period spanning 2025-2033. The report utilizes detailed market segmentation, including by type (Capacitors, Supercapacitors, Inductors, Resistors, Other Specialty: EMC Filters) to provide a granular understanding of market dynamics and future trends. Key players like Vishay Intertechnology Inc, Knowles Precision Devices, Taiyo Yuden Corporation, and others are profiled, offering a competitive landscape analysis. The report's findings are supported by extensive data analysis and incorporate recent industry developments. The total market size in 2025 is estimated at xx Million, with a projected CAGR of xx% during the forecast period.

Automotive Passive Electronic Components Market Concentration & Innovation

The automotive passive electronic components market exhibits a moderately concentrated landscape, with several major players holding significant market share. Companies like TDK Corporation, Murata Manufacturing Co Ltd, and Vishay Intertechnology Inc. dominate the market, leveraging their extensive product portfolios and established distribution networks. However, the market also features a number of smaller, specialized players focusing on niche segments. Market share analysis reveals that the top five players collectively account for approximately xx% of the global market in 2025.

Innovation is a key driver in this market, spurred by the increasing demand for advanced vehicle functionalities and stricter regulatory standards. Significant investments in R&D are leading to the development of smaller, more efficient, and higher-performing components. Key innovations include the development of miniaturized components, improved energy storage solutions (e.g., advanced supercapacitors), and the integration of passive components with active functionalities.

Regulatory frameworks, such as those related to emissions and safety, significantly impact market dynamics. Stringent regulations promote the adoption of more energy-efficient and reliable components. Product substitution is another factor; for example, the rising adoption of supercapacitors as alternatives to batteries in certain applications is reshaping the market. End-user trends, including the growing preference for electric and hybrid vehicles, are fueling demand for higher-capacity and more robust passive components. Finally, M&A activity is shaping the competitive landscape, with deals focused on expanding product portfolios, geographic reach, and technological capabilities. Recent M&A deal values have averaged xx Million, though significant variations exist depending on deal size and participants.

Automotive Passive Electronic Components Market Industry Trends & Insights

The automotive passive electronic components market is experiencing robust growth driven by several key factors. The proliferation of advanced driver-assistance systems (ADAS), electric vehicles (EVs), and connected car technologies significantly increases the demand for passive components. The rising demand for miniaturization and higher performance is pushing technological innovation, with a particular focus on smaller, more energy-efficient, and reliable components. Consumers increasingly prioritize safety and advanced features in their vehicles, driving demand for sophisticated electronic systems. This trend is particularly evident in the rising adoption of EVs and the subsequent demand for high-performance energy storage solutions.

Technological disruptions, including the development of advanced materials and manufacturing processes, are shaping market dynamics. The transition towards electric and hybrid vehicles is creating a substantial demand for high-capacity supercapacitors and other energy storage solutions. The market is also witnessing a trend towards the integration of passive components within larger electronic modules, simplifying design and reducing assembly costs. Competitive dynamics are intense, with established players facing pressure from emerging competitors offering innovative products and technologies. The market's CAGR is expected to be xx% during the forecast period, with capacitors expected to maintain the largest market share due to their widespread use in various automotive applications. Market penetration of advanced technologies, such as miniaturized components and supercapacitors, is steadily increasing.

Dominant Markets & Segments in Automotive Passive Electronic Components Market

The automotive passive electronic components market demonstrates regional variations in growth and dominance. Asia Pacific is currently the leading region, driven by the rapid growth of the automotive industry and increasing vehicle production in countries like China, Japan, and South Korea. This dominance is further reinforced by the presence of several major component manufacturers in the region.

- Key Drivers for Asia Pacific dominance:

- Strong automotive manufacturing base.

- High vehicle production volume.

- Growing adoption of advanced automotive technologies.

- Favorable government policies promoting automotive industry growth.

- Availability of skilled labor and lower manufacturing costs.

North America and Europe also hold significant market shares, but their growth rates are anticipated to be more moderate compared to Asia Pacific. The growth trajectory will be influenced by factors such as the pace of EV adoption, the development of autonomous vehicle technology, and government regulations promoting energy efficiency.

In terms of segments, capacitors constitute the largest market segment owing to their extensive use in diverse automotive applications. The increasing complexity of automotive electronics, including advanced driver-assistance systems (ADAS) and infotainment systems, boosts capacitor demand. The supercapacitor segment is expected to witness significant growth due to its increasing adoption in hybrid and electric vehicles, alongside its potential in energy recovery systems. The inductor, resistor, and other specialty component segments are also experiencing growth, driven by the ongoing increase in vehicle electronic content.

Automotive Passive Electronic Components Market Product Developments

Recent product innovations highlight a focus on miniaturization, improved performance, and enhanced reliability. New materials and manufacturing processes are enabling the creation of smaller, lighter, and more efficient passive components. The integration of passive components into larger modules simplifies design and reduces assembly costs. Supercapacitors are experiencing rapid advancements, offering increased energy density and longer lifespans, thereby becoming a compelling alternative to batteries in some applications. These advancements enhance the performance and efficiency of automotive electronic systems, contributing to improved vehicle safety, fuel economy, and overall performance. The market is witnessing the integration of sensors and other functionalities into passive components, creating smart, integrated solutions.

Report Scope & Segmentation Analysis

This report comprehensively analyzes the automotive passive electronic components market, segmenting it by type:

Capacitors: This segment is further divided into various capacitor types based on their dielectric material, application, and other relevant parameters. The market is witnessing growth driven by the increasing demand for improved energy efficiency and performance in automotive applications.

Supercapacitors: This segment is experiencing rapid growth due to its increasing adoption in hybrid and electric vehicles, as well as in energy recovery systems. Growth projections for this segment are exceptionally positive.

Inductors: This segment is driven by the increasing complexity of automotive electronics and the need for effective power management.

Resistors: This is a large and established segment, expected to maintain steady growth in line with overall market trends.

Other Specialty Components (EMC Filters): This category comprises specialized components designed for electromagnetic compatibility (EMC) and interference suppression, critical for meeting increasingly stringent regulatory standards.

Each segment's analysis includes market size, growth projections, and competitive dynamics. Competitive intensity varies depending on the specific segment, with some experiencing more intense competition than others.

Key Drivers of Automotive Passive Electronic Components Market Growth

Several key factors drive the growth of the automotive passive electronic components market. Technological advancements, particularly in miniaturization and energy efficiency, are paramount. The rising adoption of electric and hybrid vehicles creates substantial demand for high-capacity energy storage solutions such as supercapacitors. Stringent government regulations regarding fuel efficiency and emissions push the adoption of energy-efficient electronic components. The increasing integration of advanced driver-assistance systems (ADAS) and connected car technologies significantly increases the demand for passive components. For instance, the rising popularity of features like adaptive cruise control and lane-keeping assist necessitates more sophisticated and reliable electronic systems.

Challenges in the Automotive Passive Electronic Components Market Sector

The automotive passive electronic components market faces several challenges. The increasing complexity of automotive electronic systems can lead to supply chain bottlenecks and potential component shortages, potentially impacting production timelines and costs. Fluctuations in raw material prices and geopolitical uncertainties contribute to cost volatility and margin pressures. Intense competition among manufacturers can lead to price erosion and pressure on profitability. Stricter regulatory requirements related to vehicle safety and emissions necessitate continuous innovation and adaptation, representing an ongoing cost for manufacturers.

Emerging Opportunities in Automotive Passive Electronic Components Market

Several emerging opportunities are shaping the automotive passive electronic components market. The increasing demand for electric and autonomous vehicles presents significant growth potential for high-performance energy storage solutions, such as supercapacitors. The development of advanced materials and manufacturing processes offers the potential for creating smaller, lighter, and more efficient components. The integration of sensors and other functionalities into passive components is creating new opportunities for smart, integrated solutions. The growing focus on vehicle electrification and the increasing adoption of advanced driver-assistance systems (ADAS) offer significant growth prospects for companies that can provide innovative and high-performance passive electronic components.

Leading Players in the Automotive Passive Electronic Components Market Market

- Vishay Intertechnology Inc

- Knowles Precision Devices

- Taiyo Yuden Corporation

- KOA Corporation

- Kyocera Corporation (includes AVX Corporation)

- Rubycon Corporation

- Yageo Corporation

- TDK Corporation

- Nippon Chemi-Con Corporation

- Murata Manufacturing Co Ltd

- Panasonic Corporation

- Samsung Electro-Mechanical

Key Developments in Automotive Passive Electronic Components Market Industry

March 2024: Knowles Precision Devices launched new Electric Double-Layer Capacitor (EDLC) modules (supercapacitor modules), offering increased operating voltages and space savings for applications like electric vehicles and battery/capacitor hybrids.

February 2024: Taiyo Yuden Co. Ltd completed construction of a new building to manufacture barium titanate, a key raw material for multilayer ceramic capacitors, ensuring a consistent supply to meet growing demand.

Strategic Outlook for Automotive Passive Electronic Components Market Market

The automotive passive electronic components market presents substantial growth potential driven by the ongoing expansion of the automotive industry, particularly the rapid growth of the electric vehicle market and the increasing demand for sophisticated electronic systems. Strategic investments in research and development, coupled with a focus on innovation and product differentiation, will be crucial for success in this dynamic and competitive market. Companies that can effectively leverage advanced materials, manufacturing processes, and strategic partnerships will be well-positioned to capitalize on emerging opportunities and drive sustained growth. The continuous evolution of automotive technology, regulatory changes, and consumer preferences necessitates a proactive and adaptable approach to remain competitive.

Automotive Passive Electronic Components Market Segmentation

-

1. Type

-

1.1. Capacitors

- 1.1.1. Ceramic Capacitors

- 1.1.2. Tantalum Capacitors

- 1.1.3. Aluminum Electrolytic Capacitors

- 1.1.4. Paper and Plastic Film Capacitors

- 1.1.5. Supercapacitors

- 1.2. Inductors

-

1.3. Resistors

- 1.3.1. Surface-mounted Chips

- 1.3.2. Network and Array

- 1.3.3. Other Specialty

- 1.4. EMC Filters

-

1.1. Capacitors

Automotive Passive Electronic Components Market Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Australia and New Zealand

- 5. Middle East and Africa

- 6. Latin America

Automotive Passive Electronic Components Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 7.60% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Usage of Advanced Electronic Devices in the Industry; Increasing Preference for Miniaturized Designs

- 3.3. Market Restrains

- 3.3.1. Fluctuating Prices of Critical Metals Used in Manufacturing of Passive Electronic Components/ Challenges in the manufacturing of various Passive Components

- 3.4. Market Trends

- 3.4.1. Capacitors to Witness Significant Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Automotive Passive Electronic Components Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Capacitors

- 5.1.1.1. Ceramic Capacitors

- 5.1.1.2. Tantalum Capacitors

- 5.1.1.3. Aluminum Electrolytic Capacitors

- 5.1.1.4. Paper and Plastic Film Capacitors

- 5.1.1.5. Supercapacitors

- 5.1.2. Inductors

- 5.1.3. Resistors

- 5.1.3.1. Surface-mounted Chips

- 5.1.3.2. Network and Array

- 5.1.3.3. Other Specialty

- 5.1.4. EMC Filters

- 5.1.1. Capacitors

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia

- 5.2.4. Australia and New Zealand

- 5.2.5. Middle East and Africa

- 5.2.6. Latin America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Automotive Passive Electronic Components Market Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Capacitors

- 6.1.1.1. Ceramic Capacitors

- 6.1.1.2. Tantalum Capacitors

- 6.1.1.3. Aluminum Electrolytic Capacitors

- 6.1.1.4. Paper and Plastic Film Capacitors

- 6.1.1.5. Supercapacitors

- 6.1.2. Inductors

- 6.1.3. Resistors

- 6.1.3.1. Surface-mounted Chips

- 6.1.3.2. Network and Array

- 6.1.3.3. Other Specialty

- 6.1.4. EMC Filters

- 6.1.1. Capacitors

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Europe Automotive Passive Electronic Components Market Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Capacitors

- 7.1.1.1. Ceramic Capacitors

- 7.1.1.2. Tantalum Capacitors

- 7.1.1.3. Aluminum Electrolytic Capacitors

- 7.1.1.4. Paper and Plastic Film Capacitors

- 7.1.1.5. Supercapacitors

- 7.1.2. Inductors

- 7.1.3. Resistors

- 7.1.3.1. Surface-mounted Chips

- 7.1.3.2. Network and Array

- 7.1.3.3. Other Specialty

- 7.1.4. EMC Filters

- 7.1.1. Capacitors

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Asia Automotive Passive Electronic Components Market Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Capacitors

- 8.1.1.1. Ceramic Capacitors

- 8.1.1.2. Tantalum Capacitors

- 8.1.1.3. Aluminum Electrolytic Capacitors

- 8.1.1.4. Paper and Plastic Film Capacitors

- 8.1.1.5. Supercapacitors

- 8.1.2. Inductors

- 8.1.3. Resistors

- 8.1.3.1. Surface-mounted Chips

- 8.1.3.2. Network and Array

- 8.1.3.3. Other Specialty

- 8.1.4. EMC Filters

- 8.1.1. Capacitors

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Australia and New Zealand Automotive Passive Electronic Components Market Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Capacitors

- 9.1.1.1. Ceramic Capacitors

- 9.1.1.2. Tantalum Capacitors

- 9.1.1.3. Aluminum Electrolytic Capacitors

- 9.1.1.4. Paper and Plastic Film Capacitors

- 9.1.1.5. Supercapacitors

- 9.1.2. Inductors

- 9.1.3. Resistors

- 9.1.3.1. Surface-mounted Chips

- 9.1.3.2. Network and Array

- 9.1.3.3. Other Specialty

- 9.1.4. EMC Filters

- 9.1.1. Capacitors

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Middle East and Africa Automotive Passive Electronic Components Market Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Capacitors

- 10.1.1.1. Ceramic Capacitors

- 10.1.1.2. Tantalum Capacitors

- 10.1.1.3. Aluminum Electrolytic Capacitors

- 10.1.1.4. Paper and Plastic Film Capacitors

- 10.1.1.5. Supercapacitors

- 10.1.2. Inductors

- 10.1.3. Resistors

- 10.1.3.1. Surface-mounted Chips

- 10.1.3.2. Network and Array

- 10.1.3.3. Other Specialty

- 10.1.4. EMC Filters

- 10.1.1. Capacitors

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Latin America Automotive Passive Electronic Components Market Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Capacitors

- 11.1.1.1. Ceramic Capacitors

- 11.1.1.2. Tantalum Capacitors

- 11.1.1.3. Aluminum Electrolytic Capacitors

- 11.1.1.4. Paper and Plastic Film Capacitors

- 11.1.1.5. Supercapacitors

- 11.1.2. Inductors

- 11.1.3. Resistors

- 11.1.3.1. Surface-mounted Chips

- 11.1.3.2. Network and Array

- 11.1.3.3. Other Specialty

- 11.1.4. EMC Filters

- 11.1.1. Capacitors

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. North America Automotive Passive Electronic Components Market Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1.

- 13. Europe Automotive Passive Electronic Components Market Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1.

- 14. Asia Automotive Passive Electronic Components Market Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1.

- 15. Australia and New Zealand Automotive Passive Electronic Components Market Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1.

- 16. Middle East and Africa Automotive Passive Electronic Components Market Analysis, Insights and Forecast, 2019-2031

- 16.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 16.1.1.

- 17. Latin America Automotive Passive Electronic Components Market Analysis, Insights and Forecast, 2019-2031

- 17.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 17.1.1.

- 18. Competitive Analysis

- 18.1. Global Market Share Analysis 2024

- 18.2. Company Profiles

- 18.2.1 Vishay Intertechnology Inc

- 18.2.1.1. Overview

- 18.2.1.2. Products

- 18.2.1.3. SWOT Analysis

- 18.2.1.4. Recent Developments

- 18.2.1.5. Financials (Based on Availability)

- 18.2.2 Knowles Precision Devices

- 18.2.2.1. Overview

- 18.2.2.2. Products

- 18.2.2.3. SWOT Analysis

- 18.2.2.4. Recent Developments

- 18.2.2.5. Financials (Based on Availability)

- 18.2.3 Taiyo Yuden Corporation

- 18.2.3.1. Overview

- 18.2.3.2. Products

- 18.2.3.3. SWOT Analysis

- 18.2.3.4. Recent Developments

- 18.2.3.5. Financials (Based on Availability)

- 18.2.4 KOA Corporation

- 18.2.4.1. Overview

- 18.2.4.2. Products

- 18.2.4.3. SWOT Analysis

- 18.2.4.4. Recent Developments

- 18.2.4.5. Financials (Based on Availability)

- 18.2.5 Kyocera Corporation (includes AVX Corporation)

- 18.2.5.1. Overview

- 18.2.5.2. Products

- 18.2.5.3. SWOT Analysis

- 18.2.5.4. Recent Developments

- 18.2.5.5. Financials (Based on Availability)

- 18.2.6 Rubycon Corporation

- 18.2.6.1. Overview

- 18.2.6.2. Products

- 18.2.6.3. SWOT Analysis

- 18.2.6.4. Recent Developments

- 18.2.6.5. Financials (Based on Availability)

- 18.2.7 Yageo Corporation

- 18.2.7.1. Overview

- 18.2.7.2. Products

- 18.2.7.3. SWOT Analysis

- 18.2.7.4. Recent Developments

- 18.2.7.5. Financials (Based on Availability)

- 18.2.8 TDK Corporation

- 18.2.8.1. Overview

- 18.2.8.2. Products

- 18.2.8.3. SWOT Analysis

- 18.2.8.4. Recent Developments

- 18.2.8.5. Financials (Based on Availability)

- 18.2.9 Nippon Chemi-Con Corporatio

- 18.2.9.1. Overview

- 18.2.9.2. Products

- 18.2.9.3. SWOT Analysis

- 18.2.9.4. Recent Developments

- 18.2.9.5. Financials (Based on Availability)

- 18.2.10 Murata Manufacturing Co Ltd

- 18.2.10.1. Overview

- 18.2.10.2. Products

- 18.2.10.3. SWOT Analysis

- 18.2.10.4. Recent Developments

- 18.2.10.5. Financials (Based on Availability)

- 18.2.11 Panasonic Corporation

- 18.2.11.1. Overview

- 18.2.11.2. Products

- 18.2.11.3. SWOT Analysis

- 18.2.11.4. Recent Developments

- 18.2.11.5. Financials (Based on Availability)

- 18.2.12 Samsung Electro-Mechanical

- 18.2.12.1. Overview

- 18.2.12.2. Products

- 18.2.12.3. SWOT Analysis

- 18.2.12.4. Recent Developments

- 18.2.12.5. Financials (Based on Availability)

- 18.2.1 Vishay Intertechnology Inc

List of Figures

- Figure 1: Global Automotive Passive Electronic Components Market Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America Automotive Passive Electronic Components Market Revenue (Million), by Country 2024 & 2032

- Figure 3: North America Automotive Passive Electronic Components Market Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe Automotive Passive Electronic Components Market Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe Automotive Passive Electronic Components Market Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Automotive Passive Electronic Components Market Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Automotive Passive Electronic Components Market Revenue Share (%), by Country 2024 & 2032

- Figure 8: Australia and New Zealand Automotive Passive Electronic Components Market Revenue (Million), by Country 2024 & 2032

- Figure 9: Australia and New Zealand Automotive Passive Electronic Components Market Revenue Share (%), by Country 2024 & 2032

- Figure 10: Middle East and Africa Automotive Passive Electronic Components Market Revenue (Million), by Country 2024 & 2032

- Figure 11: Middle East and Africa Automotive Passive Electronic Components Market Revenue Share (%), by Country 2024 & 2032

- Figure 12: Latin America Automotive Passive Electronic Components Market Revenue (Million), by Country 2024 & 2032

- Figure 13: Latin America Automotive Passive Electronic Components Market Revenue Share (%), by Country 2024 & 2032

- Figure 14: North America Automotive Passive Electronic Components Market Revenue (Million), by Type 2024 & 2032

- Figure 15: North America Automotive Passive Electronic Components Market Revenue Share (%), by Type 2024 & 2032

- Figure 16: North America Automotive Passive Electronic Components Market Revenue (Million), by Country 2024 & 2032

- Figure 17: North America Automotive Passive Electronic Components Market Revenue Share (%), by Country 2024 & 2032

- Figure 18: Europe Automotive Passive Electronic Components Market Revenue (Million), by Type 2024 & 2032

- Figure 19: Europe Automotive Passive Electronic Components Market Revenue Share (%), by Type 2024 & 2032

- Figure 20: Europe Automotive Passive Electronic Components Market Revenue (Million), by Country 2024 & 2032

- Figure 21: Europe Automotive Passive Electronic Components Market Revenue Share (%), by Country 2024 & 2032

- Figure 22: Asia Automotive Passive Electronic Components Market Revenue (Million), by Type 2024 & 2032

- Figure 23: Asia Automotive Passive Electronic Components Market Revenue Share (%), by Type 2024 & 2032

- Figure 24: Asia Automotive Passive Electronic Components Market Revenue (Million), by Country 2024 & 2032

- Figure 25: Asia Automotive Passive Electronic Components Market Revenue Share (%), by Country 2024 & 2032

- Figure 26: Australia and New Zealand Automotive Passive Electronic Components Market Revenue (Million), by Type 2024 & 2032

- Figure 27: Australia and New Zealand Automotive Passive Electronic Components Market Revenue Share (%), by Type 2024 & 2032

- Figure 28: Australia and New Zealand Automotive Passive Electronic Components Market Revenue (Million), by Country 2024 & 2032

- Figure 29: Australia and New Zealand Automotive Passive Electronic Components Market Revenue Share (%), by Country 2024 & 2032

- Figure 30: Middle East and Africa Automotive Passive Electronic Components Market Revenue (Million), by Type 2024 & 2032

- Figure 31: Middle East and Africa Automotive Passive Electronic Components Market Revenue Share (%), by Type 2024 & 2032

- Figure 32: Middle East and Africa Automotive Passive Electronic Components Market Revenue (Million), by Country 2024 & 2032

- Figure 33: Middle East and Africa Automotive Passive Electronic Components Market Revenue Share (%), by Country 2024 & 2032

- Figure 34: Latin America Automotive Passive Electronic Components Market Revenue (Million), by Type 2024 & 2032

- Figure 35: Latin America Automotive Passive Electronic Components Market Revenue Share (%), by Type 2024 & 2032

- Figure 36: Latin America Automotive Passive Electronic Components Market Revenue (Million), by Country 2024 & 2032

- Figure 37: Latin America Automotive Passive Electronic Components Market Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Automotive Passive Electronic Components Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Automotive Passive Electronic Components Market Revenue Million Forecast, by Type 2019 & 2032

- Table 3: Global Automotive Passive Electronic Components Market Revenue Million Forecast, by Region 2019 & 2032

- Table 4: Global Automotive Passive Electronic Components Market Revenue Million Forecast, by Country 2019 & 2032

- Table 5: Automotive Passive Electronic Components Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 6: Global Automotive Passive Electronic Components Market Revenue Million Forecast, by Country 2019 & 2032

- Table 7: Automotive Passive Electronic Components Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Global Automotive Passive Electronic Components Market Revenue Million Forecast, by Country 2019 & 2032

- Table 9: Automotive Passive Electronic Components Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Global Automotive Passive Electronic Components Market Revenue Million Forecast, by Country 2019 & 2032

- Table 11: Automotive Passive Electronic Components Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Global Automotive Passive Electronic Components Market Revenue Million Forecast, by Country 2019 & 2032

- Table 13: Automotive Passive Electronic Components Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Global Automotive Passive Electronic Components Market Revenue Million Forecast, by Country 2019 & 2032

- Table 15: Automotive Passive Electronic Components Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Global Automotive Passive Electronic Components Market Revenue Million Forecast, by Type 2019 & 2032

- Table 17: Global Automotive Passive Electronic Components Market Revenue Million Forecast, by Country 2019 & 2032

- Table 18: Global Automotive Passive Electronic Components Market Revenue Million Forecast, by Type 2019 & 2032

- Table 19: Global Automotive Passive Electronic Components Market Revenue Million Forecast, by Country 2019 & 2032

- Table 20: Global Automotive Passive Electronic Components Market Revenue Million Forecast, by Type 2019 & 2032

- Table 21: Global Automotive Passive Electronic Components Market Revenue Million Forecast, by Country 2019 & 2032

- Table 22: Global Automotive Passive Electronic Components Market Revenue Million Forecast, by Type 2019 & 2032

- Table 23: Global Automotive Passive Electronic Components Market Revenue Million Forecast, by Country 2019 & 2032

- Table 24: Global Automotive Passive Electronic Components Market Revenue Million Forecast, by Type 2019 & 2032

- Table 25: Global Automotive Passive Electronic Components Market Revenue Million Forecast, by Country 2019 & 2032

- Table 26: Global Automotive Passive Electronic Components Market Revenue Million Forecast, by Type 2019 & 2032

- Table 27: Global Automotive Passive Electronic Components Market Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Passive Electronic Components Market?

The projected CAGR is approximately 7.60%.

2. Which companies are prominent players in the Automotive Passive Electronic Components Market?

Key companies in the market include Vishay Intertechnology Inc, Knowles Precision Devices, Taiyo Yuden Corporation, KOA Corporation, Kyocera Corporation (includes AVX Corporation), Rubycon Corporation, Yageo Corporation, TDK Corporation, Nippon Chemi-Con Corporatio, Murata Manufacturing Co Ltd, Panasonic Corporation, Samsung Electro-Mechanical.

3. What are the main segments of the Automotive Passive Electronic Components Market?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.60 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Usage of Advanced Electronic Devices in the Industry; Increasing Preference for Miniaturized Designs.

6. What are the notable trends driving market growth?

Capacitors to Witness Significant Growth.

7. Are there any restraints impacting market growth?

Fluctuating Prices of Critical Metals Used in Manufacturing of Passive Electronic Components/ Challenges in the manufacturing of various Passive Components.

8. Can you provide examples of recent developments in the market?

March 2024: Knowles Precision Devices, a provider of top-quality components and solutions, released its newest Electric double-layer capacitor (EDLC) modules, also known as supercapacitor modules. These advanced capacitors, constructed using Knowles' Cornell Dubilier brand DGH and DSF Series supercapacitors, come in a three-cell package for increased operating voltages and save space on printed circuit boards. The high capacity of these supercapacitors enables them to support additional batteries or even replace batteries in various applications. These supercapacitors are well-suited for providing power for electric vehicle transportation, powering pulse battery packs, creating battery/capacitor hybrids, or any situation requiring substantial energy storage.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Passive Electronic Components Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Passive Electronic Components Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Passive Electronic Components Market?

To stay informed about further developments, trends, and reports in the Automotive Passive Electronic Components Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence